Acromegaly Market Summary

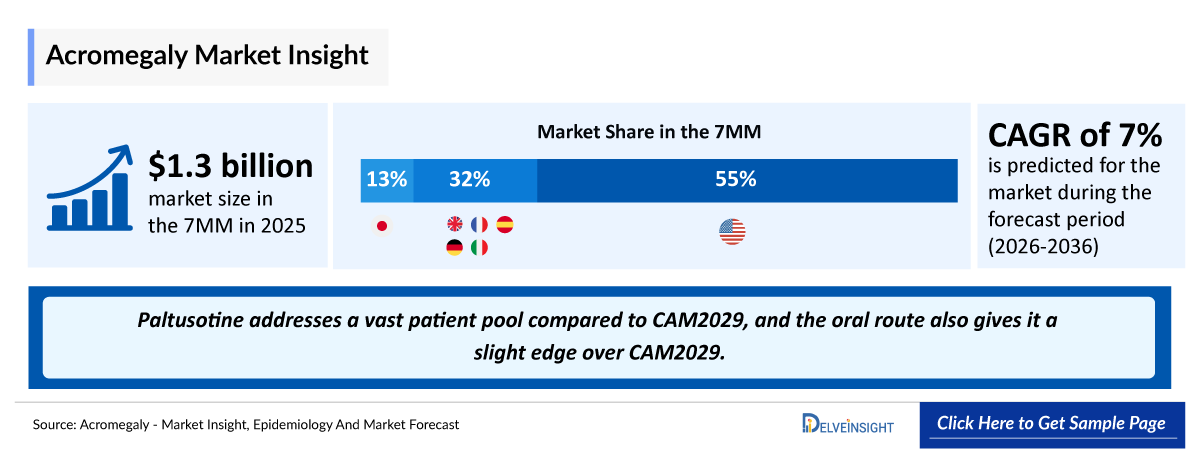

- The Acromegaly Market Size is valued at approximately USD 1,300 million in 2025, is projected to grow significantly at a CAGR of 1.5% during 2026–2036.

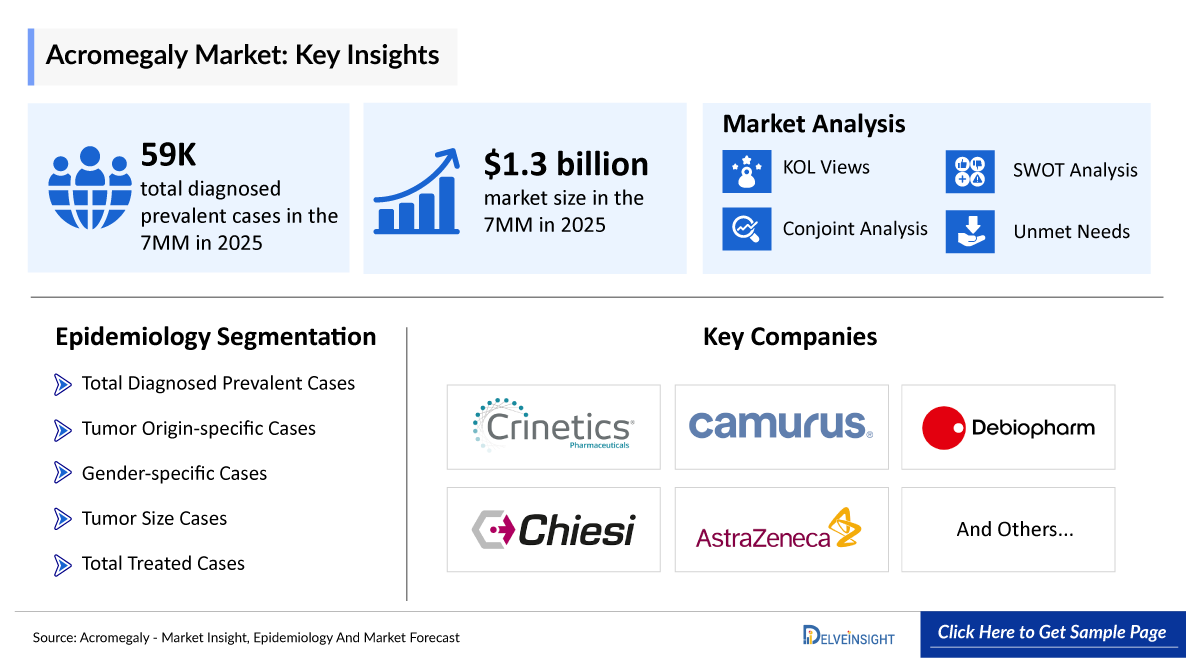

- The leading Acromegaly companies developing therapies in the treatment market include - Debiopharm International SA, AstraZeneca, Marea Therapeutics, Crinetics, Camurus, Chiesi, and others

Acromegaly Market & Epidemiology Insights

- The majority of acromegaly cases (~95%) are caused by benign pituitary adenomas, while a small proportion (~5%) arises from ectopic or non-pituitary sources. Despite being benign, these tumors can lead to significant morbidity and increased mortality if not adequately controlled.

- The burden of acromegaly is higher in middle-aged adults, typically diagnosed between 40 and 50 years, primarily due to the slow and insidious progression of symptoms, which often results in delayed diagnosis and advanced disease at presentation.

- While surgery remains the standard of care (SOC) and first-line treatment, a substantial proportion of patients require adjunctive medical therapy and/or radiotherapy due to incomplete tumor resection or persistent biochemical activity.

- The introduction of novel therapies, including oral and long-acting agents, represents a significant advancement in the treatment landscape by addressing limitations of traditional injectable therapies and improving patient convenience and adherence.

- Pharmaceutical companies actively developing therapies for acromegaly include Crinetics Pharmaceuticals (Paltusotine), Camurus (CAM2029), Debiopharm (Debio 4126), Alexion Pharmaceuticals (ALXN2420), and Marea Therapeutics (MAR002), reflecting a growing and competitive pipeline.

- Limitations in current management, including incomplete biochemical control, treatment burden, and lack of highly sensitive biomarkers, highlight the need for improved diagnostic tools and more effective, patient-friendly therapies to optimize long-term outcomes.

Acromegaly Market Size and Forecast in the 7MM

- 2025 Acromegaly Market Size: ~USD 1,300 million

- 2036 Projected Acromegaly Market Size: ~USD XXXX million

- Acromegaly Growth Rate (2026–2036): ~1.5% CAGR

DelveInsight's ‘Acromegaly Market Insights, Epidemiology and Market Forecast-2036’ report delivers an in-depth understanding of acromegaly, historical and forecasted epidemiology, as well as the acromegaly market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The Acromegaly market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates acromegaly patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment, and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in acromegaly and maps the competitive and clinical landscape to uncover high‑value opportunities, providing a clear outlook on future market growth potential.

Scope of the Acromegaly Market Report | |

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

Acromegaly Market CAGR (Forecast period) |

~1.5% (2026–2036) |

|

Acromegaly Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

Acromegaly Companies |

|

|

Acromegaly Therapies |

|

|

Acromegaly Market |

Segmented by

|

|

Analysis |

|

|

| |

Key Factors Driving the Acromegaly Market

- Rising Disease Recognition and Diagnosis: The increasing diagnosis of acromegaly is primarily driven by greater clinical awareness and improved imaging techniques, particularly widespread use of MRI for pituitary adenomas. Although acromegaly remains a rare disorder, studies suggest that prevalence has increased over time due to earlier detection of previously unrecognized cases, especially in patients presenting with subtle or slowly progressive symptoms.

- Advancements in Targeted Medical Therapies: The acromegaly treatment landscape has evolved with the availability of somatostatin receptor ligands (SRLs), growth hormone receptor antagonists, and dopamine agonists, enabling better biochemical control in patients who are not cured by surgery. Long-acting formulations and newer agents have improved treatment adherence and disease control, highlighting opportunities for continued innovation in targeted therapies.

- Emerging Competitive Pipeline and Novel Mechanisms: The robust competitive pipeline featuring novel mechanisms such as Debio 4126 (Debiopharm), ALXN2420 (AstraZeneca), MAR002 (Marea Therapeutics), and others in clinical trials stands to propel acromegaly market expansion.

Acromegaly Disease Understanding

Acromegaly Overview and Diagnosis

Acromegaly is a rare endocrine disorder characterized by chronic overproduction of growth hormone (GH), most commonly caused by a benign pituitary adenoma arising from somatotroph cells. Excess GH leads to elevated insulin-like growth factor 1 (IGF-1) levels, resulting in progressive somatic overgrowth, metabolic dysfunction, and multisystem complications. The disease typically develops insidiously in adults, leading to delayed diagnosis due to gradual symptom progression.

Diagnosis of acromegaly primarily involves biochemical confirmation followed by imaging studies. The initial step includes measurement of serum IGF-1 levels, which serve as a sensitive screening marker. This is followed by a growth hormone suppression test (oral glucose tolerance test, OGTT), where failure of GH suppression confirms the diagnosis. Once biochemical evidence is established, pituitary MRI is performed to localize and characterize the adenoma. Additional evaluation may include assessment of pituitary function and screening for associated comorbidities. Genetic testing may be considered in selected cases, particularly in younger patients or those with a family history suggestive of hereditary syndromes.

Further details are provided in the report...

Current Acromegaly Treatment Landscape

The treatment of acromegaly is primarily centered on transsphenoidal surgical resection of the pituitary adenoma, which remains the first-line and potentially curative option for localized disease. In patients with persistent or inoperable disease, medical therapy is the mainstay, including somatostatin receptor ligands (SRLs), growth hormone receptor antagonists (e.g., pegvisomant), and dopamine agonists, aimed at normalizing GH and IGF-1 levels.

For patients who are refractory to surgery and medical therapy, radiotherapy (conventional or stereotactic radiosurgery) may be considered as an adjunctive treatment. Overall management is tailored based on tumor characteristics, biochemical control, and patient-specific factors, with a goal of reducing morbidity and long-term complications.

Further details related to country-based variations are provided in the report....

Acromegaly Unmet Needs

The section “unmet needs of Acromegaly” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Incomplete biochemical control with existing therapies

- Burden of long-term treatment and monitoring

- Delayed diagnosis and disease recognition

- Treatment-related limitations and tolerability issues, and others…..

Note: Comprehensive unmet needs insights in Acromegaly and their strategic implications are provided in the full report...

Acromegaly Epidemiology

The Acromegaly epidemiology section provides insights about the historical and current Acromegaly patient pool and forecasted trends for individual seven major countries. It helps to recognize the causes of current and forecasted trends by exploring numerous studies and views of key opinion leaders. This part of the Acromegaly market report also provides the diagnosed patient pool and their trends along with assumptions undertaken.

Key Findings from Acromegaly Epidemiological Analysis and Forecast

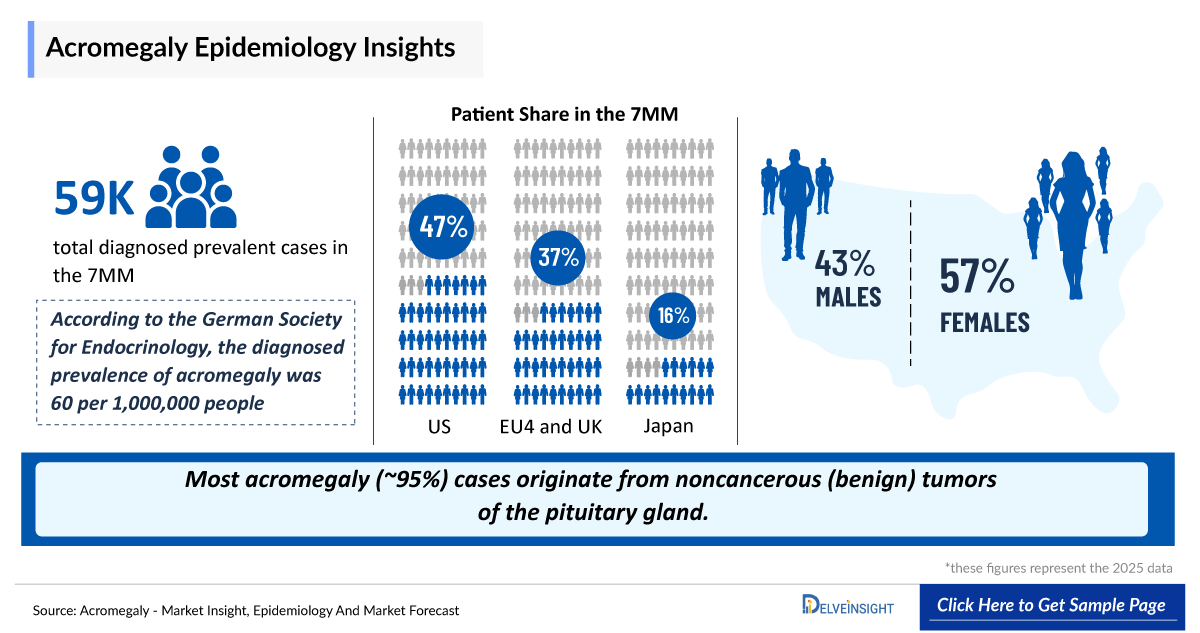

- According to DelveInsight’s estimates, in 2025, the total number of diagnosed prevalent cases of acromegaly in the 7MM was ~59,000.

- In the United States, acromegaly has an estimated incidence of ~2–11 new cases per million annually, with approximately 20,000–45,000 prevalent cases, though the true burden is likely underestimated due to underdiagnosis.

- The total diagnosed prevalent cases of acromegaly in the United States were estimated at ~27,500 in 2025, and are projected to increase by 2036, driven by improved detection and greater disease awareness.

- In the United States, ~95% of cases are attributed to pituitary adenomas, while only ~5% arise from non-pituitary sources, underscoring the dominant role of pituitary-origin disease.

- Acromegaly demonstrates a slight female predominance (~51% vs. ~49% in males), with most patients diagnosed in their 40s to 50s, reflecting the slow and progressive nature of the disease.

- In EU4 and the UK countries, Germany had the highest number of diagnosed prevalent cases, while Spain had the least.

- Based on tumor size, acromegaly is classified into microadenoma and macroadenoma, which are key determinants of disease severity and treatment strategy.

Acromegaly Epidemiology Segmentation

- Total Diagnosed Prevalent Cases of Acromegaly Occurrence

- Tumor Origin-specific Diagnosed Prevalent Cases of Acromegaly

- Gender-specific Diagnosed Prevalent Cases of Acromegaly

- Tumor Size-specific Diagnosed Prevalent Cases of Acromegaly

- Total Treated Cases of Acromegaly

Recent Developments in the Acromegaly Treatment Landscape

- In January 2026, Camurus announced that the US Food and Drug Administration (FDA) had accepted for review the resubmitted New Drug Application (NDA) for CAM2029 (Oclaiz), an octreotide extended-release injection, for the treatment of patients with acromegaly. The application has been assigned a Prescription Drug User Fee Act (PDUFA) target action date of June 10, 2026.

- In January 2026, Marea announced positive Phase I topline results for MAR002 in acromegaly, highlighting potential for best-in-class efficacy and a favorable dosing profile.

- In December 2025, Debiopharm announced that the first patient had been randomized in the Phase III (OXTEND-03) clinical trial for adults with acromegaly who are currently maintained on somatostatin analogs.

- In February 2026, Crinetics Pharmaceuticals announced that the Committee for Medicinal Products for Human Use (CHMP) of the European Medicines Agency (EMA) had adopted a positive opinion recommending the marketing authorization of PALSONIFY (paltusotine) for the treatment of adult patients with acromegaly. The opinion has been forwarded to the European Commission (EC), which will make the final approval decision.

Acromegaly Drug Analysis & Competitive Landscape

The Acromegaly drug chapter provides a detailed, market-focused review of approved therapies and the emerging pipeline across Phase I–III Acromegaly clinical trials. It covers the mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, and strategic partnerships for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the Acromegaly treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the Acromegaly therapeutics market.

Approved Therapies for Acromegaly

Paltusotine (PALSONIFY): Crinetics

PALSONIFY, developed by Crinetics, is a somatostatin receptor agonist indicated for the treatment of adults with acromegaly who have had an inadequate response to surgery and/or for whom surgery is not an option. It offers a first-line, non-injectable alternative to traditional somatostatin analogs, with clinical data showing rapid normalization or lowering of IGF-1 levels and reduction in acromegaly-related symptoms in a substantial proportion of patients.

CAM2029 (OCZYESA): Camurus

OCZYESA, developed by Camurus, is a ready-to-use, long-acting subcutaneous injection depot based on the active substance octreotide formulated with Camurus' proprietary Fluid Crystal injection depot technology and is designed for self-administration via a pre-filled autoinjector pen, enabling convenient at-home dosing.

Note: Detailed marketed therapies assessment will be provided in the final report....

Acromegaly Marketed/Approved Therapies | ||||||

|

Drug/Therapy |

Company |

Indication |

Molecule Type |

MoA |

RoA |

Marketed Region |

|

Paltusotine (PALSONIFY) |

Crinetics |

Acromegaly |

Small molecule |

Somatostatin receptor agonist |

Oral |

US: 2025 |

|

CAM2029 (OCZYESA) |

Camurus |

Acromegaly |

Peptide |

Somatostatin receptor agonist |

Subcutaneous injection |

EU: 2025 |

|

Octreotide (MYCAPSSA) |

Chiesi |

Acromegaly |

Peptide |

Somatostatin analog |

Oral |

US: 2020 EU: 2022 |

Acromegaly Pipeline Analysis

Debio 4126: Debiopharm International SA

Debio 4126 is an innovative, long-acting octreotide designed for intramuscular administration every three months. Early clinical data and robust pharmacokinetic modeling have demonstrated sustained octreotide release, consistent inhibition of IGF-1, and a safety profile comparable to marketed Somatostatin Analogues (SSAs), providing strong support for the initiation of this Phase III trial.

ALXN2420: AstraZeneca

ALXN2420 is a novel small-peptide antagonist of the GHR being developed as an add-on therapy to SSAs to further suppress and normalize IGF-1 levels. ALXN2420 binds to human GHR and inhibits its activation by growth hormone in vitro. In vivo administration of ALXN2420 led to a robust reduction in IGF-1 levels, which was associated with decreased growth in juvenile rats. Importantly, when combined with an SSA, ALXN2420 demonstrated an additive effect on IGF-1 reduction.

|

Competitive Landscape of Acromegaly Pipeline Drugs | ||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Anticipated Launch in the US |

|

Debio 4126 |

Debiopharm International |

III |

Acromegaly |

Intramuscular |

Somatostatin receptor agonist |

Information is available in the full report |

|

ALXN2420 |

AstraZeneca |

II |

Acromegaly |

SC |

GHR antagonist |

Information is available in the full report |

|

MAR002 |

Marea Therapeutics |

I |

Acromegaly |

SC |

GHR antagonist |

Information is available in the full report |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | ||||||

Note: Detailed emerging therapies assessment will be provided in the final report...

Acromegaly Key Players, Market Leaders, and Emerging Companies

- Debiopharm International SA

- AstraZeneca

- Marea Therapeutics

- Crinetics

- Camurus

- Chiesi, and others

Acromegaly Market Outlook

The acromegaly treatment landscape is well-established but continues to evolve, with management centered on a multimodal approach involving surgery, pharmacotherapy, and radiotherapy. Transsphenoidal surgery remains the gold standard and first-line treatment, particularly for microadenomas and symptomatic macroadenomas, offering the potential for rapid biochemical control. However, complete surgical cure is achieved in a limited proportion of patients, especially in cases with larger or invasive tumors, necessitating the use of adjunctive therapies.

Medical therapy plays a critical role in patients with persistent or inoperable disease. Somatostatin receptor ligands (SRLs) remain the cornerstone of pharmacologic management, effectively suppressing growth hormone secretion, while dopamine agonists and growth hormone receptor antagonists (e.g., pegvisomant) are used in selected patients or in combination regimens to achieve biochemical control. Despite these options, limitations such as incomplete response, injectable burden, and tolerability issues highlight the need for improved therapies. Radiotherapy, including conventional radiation and stereotactic radiosurgery, is typically reserved for refractory or recurrent disease but requires long-term monitoring due to the risk of hypopituitarism.

The pipeline is increasingly focused on next-generation somatostatin analogs, oral therapies, and novel receptor-targeting approaches, reflecting a shift toward improved convenience and efficacy. Emerging agents aim to address patients inadequately controlled on existing treatments and reduce treatment burden, supporting a gradual transition toward more patient-centric and mechanism-driven therapies.

Overall, advancements in diagnostic practices, therapeutic innovation, and disease awareness are expected to support steady growth in the acromegaly market over the forecast period, with increasing emphasis on achieving sustained biochemical control and improving long-term outcomes.

- According to estimates, the total acromegaly market size in 7MM was approximately USD 1,300 million in 2025, with the United States accounting for the largest share, and the market is projected to grow at a significant CAGR through 2036.

- In 2025, among the EU4 and the UK, the UK held the largest market share, followed by Germany, while Spain accounted for the smallest share.

Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in Acromegaly (2022–2036 Forecast)

The acromegaly market comprises a mix of peptide-based therapies, small molecules, and biologics, each targeting different aspects of disease pathophysiology, particularly growth hormone (GH) hypersecretion and IGF-1 signaling.

- Peptide-based therapies (somatostatin analogs): Agents such as octreotide and lanreotide, along with newer formulations, act as somatostatin receptor agonists (primarily SSTR2/5) to suppress GH secretion and reduce IGF-1 levels, forming the backbone of current pharmacologic management.

- Small molecules: Emerging oral therapies such as paltusotine represent nonpeptide somatostatin receptor agonists, offering improved convenience and the potential to reduce reliance on injectable treatments, thereby enhancing patient adherence.

- Biologics (GH receptor antagonists): Therapies such as pegvisomant act by blocking GH receptor signaling, effectively reducing IGF-1 levels in patients inadequately controlled with other treatments.

Small molecules define the core innovation landscape, with radioligand therapies currently commercially validated and small molecules driving pipeline growth. Peptide-based therapies remain commercially established and widely used, while small molecules and next-generation agents are defining the evolving innovation landscape, driving pipeline growth and shifting the market toward more patient-friendly and mechanism-driven treatment options.

Acromegaly Drug Uptake

This section focuses on the uptake rate of potential drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the acromegaly drug’s uptake, performance at peak, factors affecting performance during the prime years of growth, patient uptake by therapy, and anticipated sales generated by each drug.

The uptake of therapies in acromegaly is expected to vary based on clinical positioning, mechanism of action, and stage of development. Recently approved and emerging oral therapies such as PALSONIFY are projected to demonstrate relatively faster uptake, driven by their nonpeptide mechanism, oral administration, and potential to reduce the burden of chronic injectable treatments.

In contrast, investigational agents such as ALXN2420 and MAR002 are expected to follow a moderate uptake trajectory, reflecting their early-stage development and the need for robust clinical validation before broader adoption. Meanwhile, established therapies, including somatostatin analogs (e.g., octreotide, lanreotide), are anticipated to maintain steady but plateauing uptake, as their use is well established but limited by injectable administration, tolerability concerns, and incomplete biochemical control in a subset of patients.

Detailed insights into emerging therapies' drug uptake are included in the report...

Market Access and Reimbursement of Approved Therapies in Acromegaly

The United States

US Reimbursement of Therapies Approved for Acromegaly | |

|

Drug/Therapy |

Access Program |

|

Paltusotine (PALSONIFY) |

CrinetiCARE Program |

Reimbursement is a crucial factor that affects the drug’s access to the market. Often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

NOTE: Further Details are provided in the final report….

Acromegaly Therapies Price Scenario & Trends

Pricing and analogue assessment of Acromegaly therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, the closest and most appropriate analogue selection for emerging therapies, and the understanding of how pricing influences market access, adherence, and long-term uptake.

Industry Experts and Physician Views for Acromegaly

To keep up with Acromegaly market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry experts were contacted for insights on the acromegaly emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in acromegaly, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 10+ KOLs to gather insights at the country level. Centers such as NHS Foundation Trust London, Hospital Universitario de La Princesa, and Klinikum der Universität München, etc., were contacted. Their opinion helps understand and validate current and emerging acromegaly therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in acromegaly.

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United Kingdom |

If left untreated, acromegaly and gigantism increase morbidity and death due to the systemic consequences of chronic GH and IGF-1 excess. Recognizing the most significant disease behavior signs may aid the medical team in designing interventions for each instance of acromegaly and gigantism. |

|

Spain |

Despite the availability of multimodal therapy options for acromegaly, many individuals experience unsatisfactory long-term disease management. Furthermore, illness control as defined by biochemical normalization does not necessarily correspond to disease-related symptoms or the patient’s subjective quality of life. |

Acromegaly Report Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of acromegaly, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are mainly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Acromegaly Market Report

- The Scope of the Acromegaly Market report covers a segment of key events, an executive summary, a descriptive overview of acromegaly, explaining its causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the acromegaly market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The Acromegaly Market report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM acromegaly market.

Acromegaly Market Report Insights

- Acromegaly Patient Population Forecast

- Acromegaly Therapeutics Market Size

- Acromegaly Pipeline Analysis

- Acromegaly Market Size and Trends

- Acromegaly Market Opportunity (Current and forecasted)

Acromegaly Market Report Key Strengths

- Epidemiology‑based (Epi‑based) Bottom‑up Forecasting

- Artificial Intelligence (AI)-Enabled Market Research Report

- 11-Year Forecast

- Acromegaly Market Outlook (North America, Europe, Asia-Pacific)

- Patient Burden Trends (By Geography)

- Acromegaly Treatment Addressable Market (TAM)

- Acromegaly Competitive Landscape

- Acromegaly Major Companies Insights

- Acromegaly Price Trends and Analogue Assessment

- Acromegaly Therapies Drug Adoption/Uptake

- Acromegaly Therapies Peak Patient Share Analysis

Acromegaly Market Report Assessment

- Acromegaly Current Treatment Practices

- Acromegaly Unmet Needs

- Acromegaly Clinical Development Analysis

- Acromegaly Emerging Drugs Product Profiles

- Acromegaly Market Attractiveness

- Acromegaly Qualitative Analysis (SWOT and Conjoint Analysis)

- Acromegaly Market Drivers

- Acromegaly Market Barriers

FAQs Related to Acromegaly Market Report:

Acromegaly Market Insights

- What was the acromegaly market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of acromegaly?

- What are the disease risks, burdens, and unmet needs of acromegaly? What will be the growth opportunities across the 7MM concerning the acromegaly patient population?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of acromegaly? What are the current guidelines for treating acromegaly in the US, Europe, and Japan?

Reasons to Buy the Acromegaly Market Forecast Report

- The Acromegaly Marke report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the acromegaly market.

- Bottom-up forecasting builds from the affected population to product forecasts, delivering a robust, data-driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights into the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI)-enabled report summarize and simplify complex datasets with in the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data-driven decisions.