Glioma Market Summary

Glioma Market Insights and Trends

- According to DelveInsight estimates, in 2025, the United States accounted for the highest glioma market size, i.e. over USD 600 million, with recent analyses suggest potential upside driven by increasing adoption of novel and targeted therapies.

- The current standard of care for glioma management, surgical resection, radiation therapy, and TEMODAR (including maintenance therapy), remains largely non-curative, with recurrence rates approaching ~90–95% in high-grade gliomas such as glioblastoma.

- FDA-approved therapies for treating glioma include OPTUNE (novocure), AVASTIN (Genentech), TEMODAR (Merck), and TAFINLAR + MEKINIST (Novartis), the latter approved for BRAF V600E-mutant low-grade glioma, particularly in pediatric patients.

- Biosimilars of bevacizumab, including ZIRABEV (Pfizer), approved in June 2019, and MVASI (Amgen), approved in 2017, have expanded access across all eligible indications of the reference product. The introduction of these biosimilars has led to pricing pressure and is expected to reduce the market share of Avastin in the United States.

- In August 2025, Jazz Pharmaceuticals Announced US FDA Approval of dordaviprone (MODEYSO) as the first and only treatment for recurrent H3 K27M-mutant diffuse midline glioma.

- Our estimates indicate that the Glioma Market is anticipated to witness a significant positive shift owing to encouraging outcomes from several pipeline products, including AV-GBM-1, ITI-1000, LAM561, DCVax-L, INO-5401 + INO-9012 in combination with LIBTAYO, SurVaxM, enzastaurin, VAL-083, temferon, DAY101 (tovorafenib).

- While the expansion of Novartis’ TAFINLAR + MEKINIST to include pediatric patients aged ≥1 year with BRAF V600E–mutant low-grade glioma broadens its commercial potential, the scarcity of approved therapies in this segment underscores a substantial unmet clinical need, thereby signaling a compelling opportunity for the development of novel targeted treatments.

Request for Unlocking the Sample Page of the "Glioma Treatment Market"

Factors Contributing to the Growth of the Glioma Market by DelveInsight

-

Rising Glioma Prevalence

The increasing incidence and prevalence of glioma, particularly aggressive forms such as glioblastoma, remain a key driver of market growth. Although glioma is a relatively rare cancer, its high mortality and recurrence rates contribute to a sustained patient pool requiring continuous treatment. In major markets such as the US, thousands of new glioma cases are diagnosed annually, and the burden is expected to rise further due to improved diagnostic capabilities and aging populations.

-

Advancements in Treatment Approaches

The evolution of glioma treatment beyond conventional surgery, radiation, and chemotherapy has significantly contributed to market expansion. The introduction of novel modalities such as tumor treating fields (OPTUNE), targeted therapies for specific mutations (e.g., BRAF inhibitors), immunotherapies, and oncolytic virus therapies has improved clinical outcomes and broadened treatment options, thereby driving therapeutic adoption.

-

Rising Opportunities in Glioma

Recent progress in immunotherapy, vaccine-based approaches, and precision medicine has created substantial opportunities for emerging players in the glioma market. Innovative therapies such as dendritic cell vaccines including DCVax-L and AV-GBM-1, along with peptide vaccines like SurVaxM, are gaining traction due to their potential to induce durable anti-tumor immune responses. Targeted therapies addressing specific genetic alterations are also expanding the treatment landscape. Agents such as dordaviprone (MODEYSO) for H3K27M-mutant glioma, dabrafenib (TAFINLAR) + trametinib (MEKINIST) for BRAF V600E-mutant tumors, and vorasidenib (VORANIGO) for IDH-mutant glioma highlight the growing importance of biomarker-driven treatment approaches.

In parallel, novel platforms such as oncolytic viruses including DNX-2401 and teserpaturev and targeted agents like regorafenib and AV-GBM-1 are being actively investigated, further strengthening the pipeline.

-

Emerging Glioma Competitive Landscape

The emerging glioma competitive landscape is highly dynamic and increasingly driven by innovation across immunotherapy, targeted therapy, and novel delivery platforms. A diverse pipeline of active investigational therapies is being developed to address the significant unmet need in both newly diagnosed and recurrent glioma, particularly glioblastoma, where current standards offer limited survival benefit. Among the most competitive segments, cancer vaccines and cell-based immunotherapies are gaining strong momentum, with candidates such as DCVax-L, SurVaxM, AV-GBM-1, and ITI-1000 showing encouraging clinical outcomes. These therapies aim to induce durable anti-tumor immune responses and are increasingly being evaluated in combination with standard-of-care regimens, positioning them as potential game changers in long-term disease control.

Another key competitive class includes oncolytic viruses, such as DNX-2401, teserpaturev, and Ofranergene Obadenovec. These agents offer a dual mechanism of direct tumor cell lysis and immune activation, making them particularly attractive for overcoming tumor resistance and immunosuppressive microenvironments. Their continued advancement in mid-to-late stage trials highlights their competitive potential. In the targeted therapy space, several late-stage and emerging agents are intensifying competition. These include enzastaurin, regorafenib, and paxalisib. These therapies are designed to target specific molecular pathways involved in glioma progression and are expected to play a critical role in biomarker-driven treatment approaches.

Additionally, novel metabolic and membrane-targeting therapies such as LAM561 and BBB-penetrating cytotoxic agents like berubicin are expanding the competitive landscape by addressing key challenges such as drug delivery across the blood–brain barrier and tumor resistance.

Overall, the emerging glioma pipeline reflects a shift toward multi-mechanistic and combination-based strategies, with increasing emphasis on immunotherapy, precision medicine, and improved CNS penetration. As clinical data matures and regulatory milestones are achieved, these active emerging therapies are expected to intensify competition, reshape treatment paradigms, and drive the future growth of the glioma marke

DelveInsight's ‘Glioma Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of the Glioma, historical and forecasted epidemiology, as well as the Glioma market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The Glioma Treatment Market Report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates glioma patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in glioma and maps the competitive and clinical landscape to uncover high‑value opportunities, providing a clear outlook on future market growth potential.

Scope of the Glioma Market Report | |

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

Glioma Market CAGR |

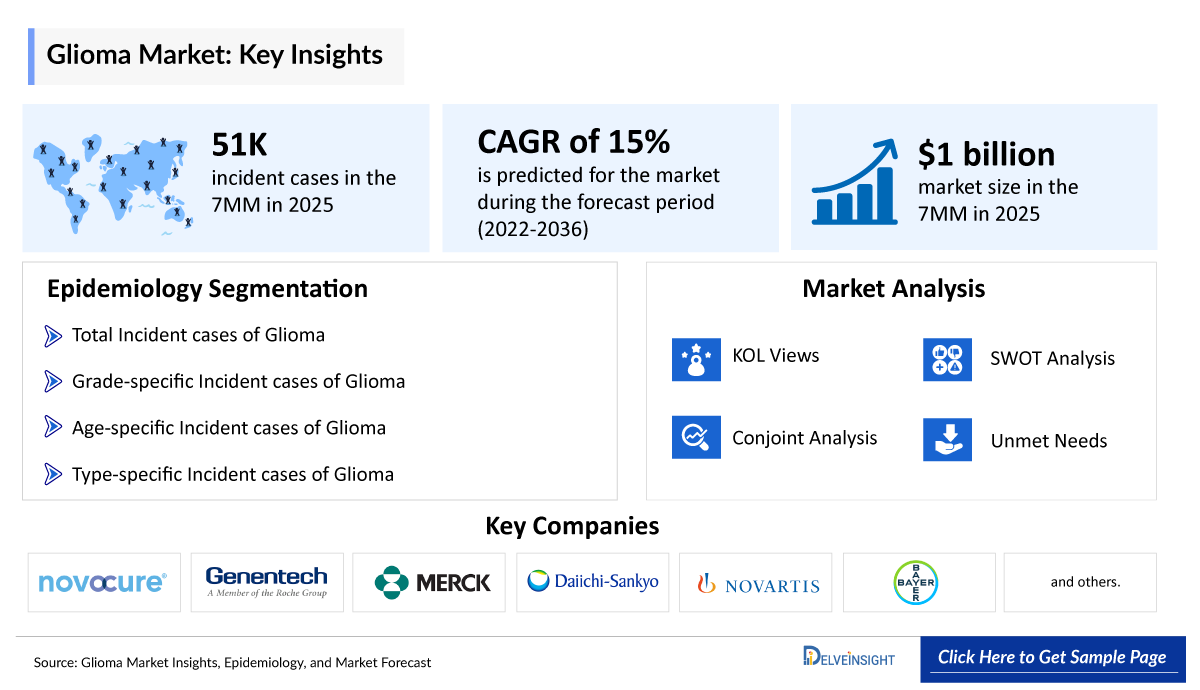

∼15% (2022 ̶ 2036) |

|

Glioma Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

Glioma Companies |

|

|

Glioma Therapies |

|

|

Glioma Market |

Segmented by

|

|

Analysis |

|

Glioma Understanding

Glioma Overview and Diagnosis

Glioma is the most common Central Nervous System (CNS) neoplasm originating from glial cells. They are very diffusely infiltrative tumors that affect the surrounding brain tissue. Three common types of gliomas are classified based on phenotypic cell characteristics: Astrocytomas, ependymomas, and oligodendrogliomas. Gliomas are caused by the accumulation of genetic mutations in glial stem or progenitor cells, leading to their uncontrolled growth. Gliomas are further classified into Grades I–IV. Glioblastoma (GBM Grade IV) is the most malignant type, while pilocytic astrocytomas (Grade I) are the least malignant brain tumors among these Grades I–IV. Mutated genes are typically involved in the etiology of glioma. Examples of mutated genes in certain types of glioma include TP53, PTEN (tumor suppressor genes), BRAF (involved in cell growth), and IDH1 (involved in cellular metabolism).

Glioma Diagnosis

The diagnosis of glioma includes neurological exams (this exam tests vision, hearing, speech, strength, sensation, balance, coordination, reflexes, and the ability to think and remember), angiograms, magnetic resonance imaging (MRI), computerized tomography (CT), surgical biopsy, and others. The patient’s journey typically starts with the onset of symptoms like seizures, unusual headaches, mood and sensory disturbances, and difficulties in walking. Following an initial visit with a general practitioner, during which the patient underwent a complete physical examination, and the results revealed a few alarming findings related to a brain tumor, the patient was referred to a neuro-oncologist. Further, a neuro-oncologist will immediately recommend an MRI, given that it is the most prominent imaging method, gives good brain images, and aids in the accurate differential diagnosis of brain cancers. A biopsy is carried out to determine the disease’s stage if the MRI scans reflect glioma. Moreover, molecular examination of biomarkers may be applied to evaluate the type and grade. Once the grade of the glioma is determined, the appropriate treatment is provided to the patient.

Further details are provided in the report.

Glioma Treatment

Therapeutic management depends on the type of glioma, its size and location, and the specific characteristics of the patient. Especially in patients where the tumor cannot be entirely removed because it invades the brain in crucial areas or is not accessible, chemotherapy and radiation therapy will follow surgery. The standard treatment regimen includes surgery, chemotherapy, and radiation. Chemotherapy includes carmustine (BCNU), lomustine (CCNU), or gleostine (generic), Gliadel wafer (biodegradable discs infused with BCNU), temozolomide (TEMODAR) cisplatin, carboplatin, etoposide, and irinotecan. They may be given as a single agent or combination, i.e., PCV (procarbazine, CCNU, and vincristine), carboplatin/ etoposide. Temozolomide and bevacizumab are the most commonly used drugs to treat brain tumors. However, the current treatment market lacks an effective strategy to cure glioma, so the survival rate of patients diagnosed with glioma remains low. Glioma is not curable, and approved treatment options are limited. Moreover, the tumor has a high recurrence rate and poor patient prognosis. Also, currently there is no approved therapy for unmethylated MGMT patient pool.

Further details related to country-based variations are provided in the report.

Glioma Unmet Needs

The section “unmet needs of Glioma” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Lack of effective treatment options

- Lack of diagnostic accuracy

- Lack of information and supportive care

- High clinical trial failure rate and lack of larger multicenter studies with a wide patient pool

- Need for successful target inhibition and drug delivery strategies and others…..

Comprehensive unmet needs insights in Glioma and their strategic implications are provided in the full report.

Glioma Epidemiology Insights Report in the 7MM

Key Findings from Glioma Epidemiological Analysis and Forecast

- According to DelveInsight’s estimates, the Glioma Incident Cases in the 7MM were approximately 51, 000 in 2025.

- It has been observed that the incidence of high-grade glioma is higher (~16,700) as compared to low grade glioma (~4,170) in the United States in 2025.

- According to DelveInsight estimates, in the United States, among all the grades, Grade IV accounted for the highest number of incident cases (~70%), followed by Grade II glioma (~15%), while Grade I had the least number of cases (~7%).

- In 2025, among gliomas in other parts of central nervous system in the United States, glioblastoma was the most prevalent in adults than in pediatrics, followed by anaplastic astrocytoma which was also found to be more prevalent in adults than in pediatrics.

- In Japan among gliomas in other parts of the central nervous system, Glioblastoma was found to be more incident in Adults (~2,735) in 2025.

Glioma Drug Chapters & Competitive Analysis

The Glioma drug chapter provides a detailed, market-focused review of approved therapies and the emerging pipeline across Phase I–III clinical trials. It covers the mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, and strategic partnerships for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the glioma treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the glioma therapeutics market.

Glioma Approved Therapies

-

Vorasidenib (VORANIGO): Servier Pharmaceuticals

Vorasidenib (VORANIGO) is a first-in-class, brain-penetrant inhibitor targeting IDH1 and IDH2 enzymes. Vorasidenib acts by inhibiting mutant IDH1 and IDH2 enzymes, which reduces the production of the oncometabolite D-2-hydroxyglutarate (2-HG) that drives tumor growth. On August 6, 2024, the US FDA approved vorasidenib (VORANIGO), an isocitrate dehydrogenase-1 (IDH1) and isocitrate dehydrogenase-2 (IDH2) inhibitor, for adult and pediatric patients 12 years and older with Grade 2 astrocytoma or oligodendroglioma with a susceptible IDH1 or IDH2 mutation, following surgery including biopsy, sub-total resection, or gross total resection.

-

Dordaviprone (MODEYSO): Jazz Pharmaceuticals

MODEYSO is the first and only treatment option approved by the FDA for this ultra-rare and aggressive brain tumor that affects an estimated 2,000 people in the US each year, many of whom are children and young adults.

In August 2025, Jazz Pharmaceutical announced that the US FDA has granted accelerated approval for dordaviprone (MODEYSO) for the treatment of adult and pediatric patients 1 year of age and older with diffuse midline glioma harboring an H3 K27M mutation with progressive disease following prior therapy.1 Continued approval for this indication may be contingent upon verification and description of clinical benefit in the Phase 3 ACTION confirmatory trial.

Comparison of Marketed Drugs | ||||||

|

Drug/Therapy |

Company |

Indication |

Molecule Type |

RoA |

MoA |

Marketed Region |

|

Temozolomide (TEMODAR) |

Merck |

Glioblastoma |

Alkylating Agent |

Oral; Injection |

Alkylation (methylation) mainly at the O6 and N7 positions of guanine |

US: 2005 EU: 1999 JP: 2006 |

|

DELYTACT (teserpaturev) |

Daiichi Sankyo |

Malignant Glioma |

Genetically engineered oncolytic herpes simplex virus type 1 |

Intra-tumoral |

Selective replication in cancer cells and enhanced induction of antitumor immune response |

JP: 2021 |

|

TAFINLAR (dabrafenib) + MEKINIST (trametinib) |

Novartis |

Low-grade and high-grade glioma (BRAF mutation) |

Small Molecule |

Oral |

Inhibits MAPK pathway and inhibits cell growth of various BRAFV600E positive tumors |

US: 2022 |

Note: Detailed marketed therapies assessment will be provided in the final report.

Glioma Emerging Therapies

-

Regorafenib: Bayer

Regorafenib is an oral multi-kinase inhibitor that potently blocks multiple protein kinases involved in tumor angiogenesis (VEGFR1, -2, -3, TIE2), oncogenesis (KIT, RET, RAF-1, BRAF), metastasis (VEGFR3, PDGFR, FGFR) and tumor immunity (CSF1R). It is an inhibitor of multiple membrane-bound and intracellular kinases involved in normal cellular functions and pathologic processes such as oncogenesis, tumor angiogenesis, and maintenance of the tumor microenvironment.

In November 2025, Regorafenib (STIVARGA) in combination with temozolomide (TEMODAR) and radiotherapy was tolerable for the treatment of patients with MGMT-methylated, IDH wild-type glioblastoma, according to data from the phase 1 REGOMA-2 study (NCT06095375) presented during the 2025 Society of Neuro-Oncology Annual Meeting.

-

AV-GBM-1: Aivita Biomedical

AV-GBM-1 is novel immunotherapy consisting of autologous dendritic cells loaded with autologous tumor antigens derived from self-renewing tumor-initiating cells derived from cultured autologous GBM tumor cells, with potential immunostimulatory and antineoplastic activities. The treatment is administered in a series of SC injections as adjunctive therapy. It is uniquely pan-antigenic, targeting multiple antigens on autologous tumor-initiating cells responsible for the rapid growth of the disease and resistance to standard therapy.

In January 2024, TAE Life Sciences and AIVITA Biomedical announced a partnership to address an unmet need in glioblastoma treatment. Acquiring significant amounts of quality glioblastoma tissue samples has long been a barrier in developing novel cancer therapeutics, with samples often plagued by misleading signals such as dead cells, normal cells and extracellular matrix.

Comparison of Emerging Drugs Under Development | |||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Molecule Type |

Anticipated Launch in the US |

|

DCVax-L |

Northwest Therapeutics |

III |

Glioblastoma |

Intradermal injection |

Incorporates the full set of tumor antigens, making it difficult for tumors to find ways around it |

Dendritic vaccine |

2027 |

|

Enzastaurin |

Denovo Pharma |

II |

Newly diagnosed GBM |

Oral |

Inhibits protein kinase C beta activity |

Small Molecule |

Information is available in the full report |

|

Paxalisib (GDC-0084) |

Kazia Therapeutics |

II/III |

newly-diagnosed glioblastoma multiforme, newly diagnosed diffuse intrinsic pontine glioma or diffuse midline gliomas and progressive or recurrent high-grade glioma |

oral |

pi3k pathway inhibitor |

small molecule |

information is available in the full report |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | |||||||

Note: A detailed emerging therapies assessment will be provided in the final report

Glioma Companies

- Novocure

- Genentech

- Merck

- Daiichi Sankyo

- Novartis

- Bayer

- Servier Pharmaceuticals

- Kazia Therapeutics

- Aivita Biomedical

- Northwest Therapeutics

- VBL Therapeutics

- Laminar Pharmaceuticals

- Immunomic Therapeutics, and others

Glioma Drug Updates

- In January 2026, Bayer reported ongoing evaluation of regorafenib in glioblastoma through platform trials such as GBM AGILE, highlighting its continued investigation in both newly diagnosed and recurrent settings.

- In November 2025, Northwest Biotherapeutics advanced regulatory engagement for DCVax-L following Phase III data demonstrating improved overall survival in glioblastoma patients, with efforts focused on potential approvals.

- In September 2025, Daiichi Sankyo continued post-marketing and clinical development activities for teserpaturev (DELYTACT), an oncolytic virus approved in Japan for malignant glioma, with additional studies exploring global expansion opportunities.

- In August 2025, the US FDA has granted accelerated approval for dordaviprone (MODEYSO) for the treatment of patients one year of age and older with diffuse midline glioma harboring an H3 K27M mutation with progressive disease following prior therapy. MODEYSO is the first treatment option approved by the FDA for this ultra-rare and aggressive brain tumor that affects an estimated 2,000 people in the US each year.

Glioma Drug Class Insights

Glioma Market Outlook

Gliomas are classified into four grades based on differentiation, with Grade I being least malignant and Grade IV (glioblastoma, GBM) being the most aggressive with poor prognosis. Management requires a multidisciplinary approach due to tumor heterogeneity and variable treatment response. The current standard of care includes maximum safe surgical resection followed by radiation and chemotherapy with temozolomide (TEMODAR), with the addition of OPTUNE (tumor treating fields) in eligible patients. In the recurrent setting, bevacizumab (AVASTIN) remains a key therapeutic option.

From a market perspective, high-grade gliomas, particularly GBM, continue to dominate due to high unmet need and poor survival outcomes. While low-grade gliomas historically had limited options, recent approvals and advancements in targeted therapies such as dabrafenib (TAFINLAR) + trametinib (MEKINIST) are expanding treatment opportunities in molecularly defined populations.

The pipeline remains active but challenging, with moderate attrition rates in late-stage trials. Prominent emerging therapies include vaccines such as DCVax-L and SurVaxM, oncolytic viruses such as DNX-2401 and teserpaturev (DELYTACT). Additionally, regorafenib is being actively evaluated and is included in treatment guidelines for recurrent GBM in some settings.

Current treatment patterns across major markets remain consistent, centered on surgery followed by chemoradiation, with targeted and novel therapies gradually being incorporated. Future growth will be driven by precision medicine, biomarker-driven therapies (e.g., IDH, H3K27M), and combination strategies. However, challenges such as lack of robust biomarkers, high clinical trial failure rates, and the immunosuppressive tumor microenvironment continue to limit progress.

Overall, despite significant challenges, continued innovation across immunotherapy, targeted therapy, and novel platforms is expected to gradually reshape the glioma treatment landscape in the coming years.

- The Glioma Market Size in the 7MM is over USD 1 billion in 2025 and is projected to grow during the forecast period (2026–2036).

- According to the estimates, the United States recorded the highest Glioma market share, i.e., around 65% of the Glioma market size in 2025.

- Among the EU4 and the UK, Germany (~USD 95 million) has the maximum revenue share in 2025, while Spain has the lowest Glioma market share.

- In 2025, OPTUNE ± TMZ captured the highest Glioma market size in Japan. This combination is expected to generate maximum revenue during the forecast period (2026–2036).

- Conditional and time-limited approval of Daiichi’s DELYTACT, an intratumoral oncolytic virus therapy, has opened new doors for other players, such as DNAtrix and Istari Oncology, to develop oncolytic virus therapies, which can prove to be a potential mechanism of action in brain cancer treatment in future.

- Currently, Jazz Pharmaceuticals/Chimerix is the only company in the advanced stage of developing treatments for the H3K27M mutation. Other key players in the early stages of development include Rigel Pharmaceuticals, Aminex Therapeutics, Bexion Pharmaceuticals, OX2 Therapeutics, Neonc Technologies, and others

Glioma Drug Class/Insights into Leading Emerging and Marketed Therapies (2022–2036 Forecast)

The existing glioma treatment landscape is primarily dominated by therapeutic classes such as vascular endothelial growth factor (VEGF) inhibitors, alkylating agents, MAPK pathway inhibitors, IDH inhibitors, multikinase inhibitors, and emerging targeted and immunotherapy approaches. Among anti-angiogenic agents, bevacizumab (AVASTIN) remains a key therapy designed to inhibit VEGF, a signaling protein that promotes tumor angiogenesis. By blocking VEGF, bevacizumab prevents the formation of new blood vessels that supply nutrients and oxygen to tumors, thereby restricting tumor growth. Although widely used, its role is largely confined to recurrent settings due to modest survival benefits.

Moving to alkylating agents, temozolomide (TEMODAR/TEMODAL) continues to serve as the backbone of glioma therapy. It acts by methylating DNA, leading to DNA damage and inhibition of tumor cell replication. Its ability to cross the blood–brain barrier and its strong clinical evidence in combination with radiation therapy have driven its widespread adoption and sustained utilization in both newly diagnosed and recurrent glioma. Other agents such as carmustine and lomustine also contribute to this class, particularly in specific treatment settings.

Targeted therapies are increasingly shaping the glioma market, particularly with the emergence of biomarker-driven approaches. IDH inhibitors such as vorasidenib (VORANIGO) represent a significant advancement, targeting IDH-mutant gliomas and demonstrating the ability to delay disease progression and postpone the need for more aggressive treatments. Similarly, newer agents such as dordaviprone (MODEYSO) are gaining attention for their activity in specific molecular subtypes, further reinforcing the shift toward precision oncology.

In the MAPK pathway segment, dabrafenib (TAFINLAR) and trametinib (MEKINIST) target BRAF V600E-mutant gliomas by inhibiting key signaling proteins involved in tumor growth. These agents, used as monotherapy or in combination, have demonstrated improved outcomes in biomarker-selected populations. Competing agents within this class, such as tovorafenib (DAY101), are also emerging, highlighting growing competition within targeted therapy segments.

Furthermore, multikinase inhibitors such as regorafenib are being explored in recurrent glioma and offer an alternative mechanism by targeting multiple signaling pathways involved in tumor proliferation and angiogenesis. Moreover, the upcoming glioma treatment landscape is poised for significant expansion with the emergence of novel therapeutic classes. These include cancer vaccines (e.g., DCVax-L, SurVaxM), oncolytic viruses (e.g., DNX-2401), and protein kinase C beta inhibitors such as enzastaurin, and cell and gene therapies (e.g., ofranergene obadenovec/VB-111). These emerging approaches aim to overcome key limitations of current treatments, including resistance, tumor heterogeneity, and poor long-term outcomes. Over the forecast period (2022–2036), these innovations are expected to diversify the therapeutic landscape, enhance treatment efficacy, and gradually shift glioma management toward more personalized and mechanism-driven strategies.

Further details will be provided in the report….

Glioma Drug Uptake

This section focuses on the uptake rate of potential Glioma drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the glioma market's uptake by drugs, patient uptake by therapy, and sales of each drug.

The uptake of therapies in glioma is expected to evolve significantly across standard chemotherapies, targeted therapies, device-based treatments, and emerging immunotherapies. Established treatments such as temozolomide (TEMODAR) and bevacizumab (AVASTIN) are anticipated to maintain baseline utilization due to their long-standing inclusion in clinical guidelines; however, their growth is expected to stabilize given limited impact on long-term survival. Device-based therapy such as OPTUNE will continue to witness steady adoption, particularly in newly diagnosed glioblastoma, supported by survival benefits in combination with chemotherapy.

A major shift in uptake is being driven by newly approved targeted therapies. vorasidenib (VORANIGO), approved in 2024 for IDH-mutant low-grade glioma, is expected to see strong and sustained uptake in early-stage, biomarker-defined populations due to its ability to significantly delay disease progression and defer the need for more toxic therapies. Similarly, dordaviprone (MODEYSO), approved in 2025 for H3 K27M-mutant diffuse midline glioma, represents a breakthrough in a high unmet need segment and is expected to witness rapid uptake in eligible patients, particularly in recurrent settings where treatment options have historically been limited. These agents mark a transition toward precision medicine and are likely to capture increasing market share over the forecast period.

In contrast, other targeted therapies such as dabrafenib (TAFINLAR) + trametinib (MEKINIST) and multikinase inhibitors like regorafenib are expected to see moderate uptake in niche, biomarker-selected populations. Their adoption will be driven by molecular testing uptake and clinical positioning in later lines of therapy.

Emerging therapies including cancer vaccines such as DCVax-L and SurVaxM, oncolytic viruses such as DNX-2401 and teserpaturev, and investigational agents like ONC201 are expected to demonstrate gradual but progressive uptake over the forecast period. Their adoption will depend on clinical trial outcomes, regulatory approvals, and validation of predictive biomarkers. As combination strategies with existing standards of care (including OPTUNE) are optimized, these therapies are anticipated to gain traction, particularly in recurrent and treatment-resistant glioma populations.

Overall, the glioma drug uptake landscape is shifting from a historically chemotherapy-dominated paradigm toward a biomarker-driven, targeted, and immunotherapy-based approach. Newly approved agents such as vorasidenib and dordaviprone are expected to redefine treatment algorithms, while emerging therapies will further diversify the market and gradually improve patient outcomes over the 2022–2036 forecast period.

Further detailed analysis of emerging therapies' drug uptake in the report…

Glioma Market Access and Reimbursement

- The United States

The US Reimbursement for Glioma Therapies | |

|

Drug |

Access Program |

|

Vorasidenib (VORANIGO) |

|

|

Dordaviprone (Modeyso) |

|

Reimbursement is a crucial factor that affects the drug’s access to the market. Often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

Further details are provided in the final report….

Glioma Therapies Price Scenario & Trends

Pricing and analogue assessment of glioma therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, closest and most appropriate analogue selection for emerging therapies, and understanding of how pricing influences market access, adherence, and long-term uptake.

- Pricing of Glioma Approved Drugs

The wholesale acquisition cost (WAC) of temozolomide (TEMODAR) oral capsules varies by strength; for example, a 100 mg capsule costs approximately USD 150–200 per unit, resulting in an estimated annual cost of USD 6,000–12,000 depending on dosing regimen and treatment duration.

The Cost of Therapy is INDICATIVE and will be provided in the updated report...

Industry Experts and Physician Views for Glioma

To keep up with glioma market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry experts were contacted for insights on the glioma emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in glioma, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 10+ KOLs to gather insights; however, interviews were conducted with 6+ KOLs in the 7MM. Centers such as the Michigan State University, University of California, and the Johns Hopkins University School of Medicine, etc. were contacted. Their opinion helps understand and validate current and emerging glioma therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in glioma.

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“The emerging picture from the Phase II and Phase III trials points to study regimen as a key factor for ofranergene obadenovec efficacy in rGBM, these results warrant further assessment of ofranergene obadenovec, which we intend to advance in a new randomized, controlled, clinical trial in patients with rGBM undergoing a second surgery.” |

|

France |

“To the best of my knowledge, we have bioprinted cancer-on-a-chip for the first time, furthermore, our study is the first attempt to actually reproduce the patient’s therapeutic responses with personalized cancer-on-a-chip. I believe the day when we test cancer cells derived from patients that are cultured with a platform that mimics real cancer biology will come soon.” |

Glioma Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of Glioma, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are majorly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Glioma Market Report

- The Glioma Market Report covers a segment of key events, an executive summary, a descriptive overview, explaining its causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along Glioma treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current Glioma Treatment landscape.

- A detailed review of the Glioma Therapeutics Market, historical and forecasted Glioma Treatment Market Size, Glioma Drugs Market Share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The Glioma Therapeutics Market Report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM Glioma Drugs Market.

Glioma Market Report Insights

- Glioma Patient Population Forecast

- Glioma Therapeutics Market Size

- Glioma Pipeline Analysis

- Glioma Market Size and Trends

- Glioma Market Opportunity (Current and Forecasted)

Glioma Market Report Key Strengths

- Epidemiology‑based (Epi‑based) Bottom‑up Forecasting

- Artificial Intelligence (AI)-enabled Market Research Report

- 11-Year Glioma Market Forecast

- Glioma Market Outlook (North America, Europe, Asia-Pacific)

- Patient Burden Trends (by geography)

- Glioma Treatment Addressable Market (TAM)

- Glioma Competitive Landscape

- Glioma Major Companies Insights

- Glioma Price Trends and Analogue Assessment

- Glioma Therapies Drug Adoption/Uptake

- Glioma Therapies Peak Patient Share analysis

Glioma Market Report Assessment

- Current Glioma Treatment Practices

- Glioma Unmet Needs

- Glioma Clinical Development Analysis

- Glioma Emerging Drugs Product Profiles

- Glioma Market Attractiveness

- Glioma Qualitative Analysis (SWOT and Conjoint Analysis)

Key Questions Answered in the Glioma Market Report

Glioma Market Insights

- What was the Glioma Market Size, the Glioma Market Size by therapies, Glioma Market Share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of glioma?

- What are the disease risks, burdens, and unmet needs of glioma? What will be the growth opportunities across the 7MM concerning the patient population with glioma?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of glioma? What are the current guidelines for treating glioma in the US, Europe, and Japan?

Reasons to Buy the Glioma Market Report

- The Glioma Market Report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the Glioma Drugs Market.

- Bottom-up forecasting builds from the affected population to product forecasts, delivering a robust, data-driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease Glioma Incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing Glioma Drugs Market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the Glioma Drugs Market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the unmet needs of the existing Glioma Drugs Market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI)-enabled report summarize and simplify complex datasets within the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data-driven decisions.

Stay updated with us for Recent Articles

.png&w=256&q=75)