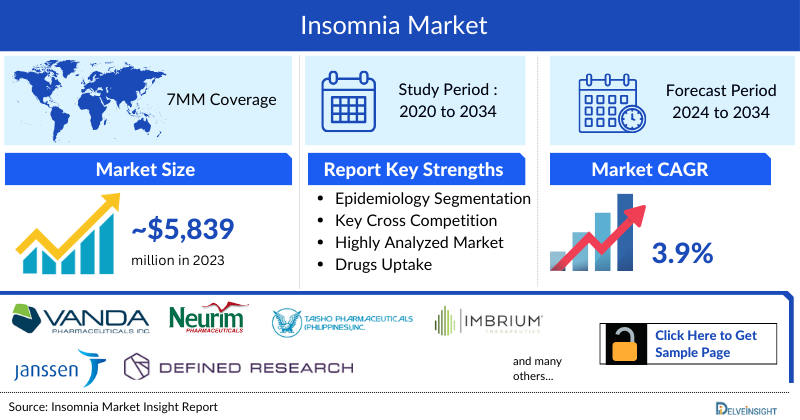

Insomnia Market

- In 2023, the market size of Insomnia in the 7MM, accounted for approximately USD 5,839 million which is further expected to increase at a significant compound annual growth rate (CAGR) by 2036.

- The Insomnia Market companies developing therapies include - Merck & Co., Eisai Co. Ltd., Idorsia Ltd., Takeda Pharmaceutical, Pfizer Inc., Sanofi S.A., Viatris Inc., Teva Pharmaceutical, Dr. Reddy's Laboratories, Big Health, Pear Therapeutics, and others.

Insomnia Market and Epidemiology Analysis

- In 2025, diagnosed prevalent cases of insomnia across the 7MM were estimated at approximately 90 million.

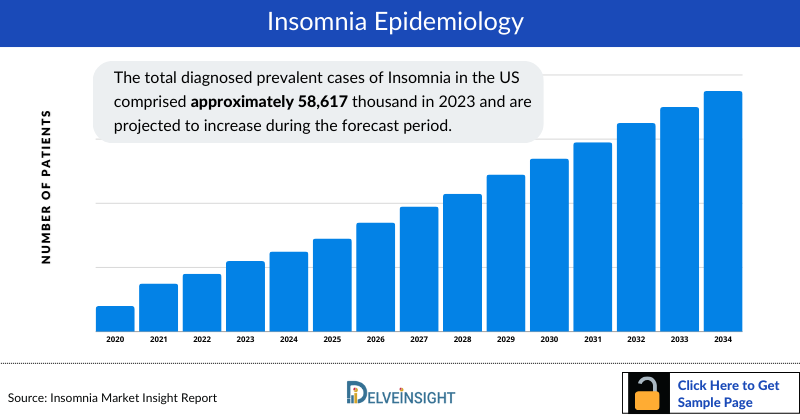

- According to DelveInsight, the total diagnosed prevalent cases of insomnia in the US comprised approximately 60 million in 2025 and are projected to increase during the forecast period.

- The insomnia market faces challenges such as high costs and market saturation. Complex drug development and patient non-compliance further complicate outcomes. Key unmet needs in the Insomnia management include long-term, low-side-effect solutions, therapies targeting root causes, and personalized treatments.

- The total market size of Insomnia is anticipated to upsurge during the forecast period due to the expected entry of emerging therapies.

Factors Affecting the Insomnia Market Growth

-

Rising Prevalence of Sleep Disorders

Chronic insomnia cases are increasing worldwide due to anxiety, depression, work-related stress, and irregular sleeping patterns. The growing patient pool directly contributes to the rising demand for insomnia treatments and sleep aids.

-

Increasing Mental Health Concerns

Stress, anxiety, and depression are major contributors to insomnia. Growing mental health disorders among adults and adolescents have accelerated the adoption of sleep medications, behavioral therapies, and digital sleep solutions.

-

Lifestyle Changes and Digital Exposure

Excessive screen time, late-night work schedules, social media use, and irregular routines are disrupting natural sleep cycles. Shift work culture and increased caffeine and alcohol consumption are also contributing to insomnia prevalence.

-

Growing Aging Population

Older adults are more likely to experience sleep disturbances due to chronic illnesses, medication use, and physiological changes. The expanding geriatric population is therefore boosting the insomnia therapeutics market.

-

Advancements in Sleep Technologies

Wearable sleep trackers, AI-powered monitoring systems, digital therapeutics, and mobile sleep applications are improving diagnosis and treatment adherence. These innovations are expanding the market beyond traditional pharmaceuticals.

Request a sample to unlock the CAGR for "Insomnia Market Forecast"

DelveInsight’s “Insomnia Market Insights, Epidemiology, and Market Forecast 2036” report delivers an in-depth understanding of the Insomnia, historical and forecasted epidemiology as well as the Insomnia therapeutics market trends in the United States, EU4 and the UK (Germany, France, Italy, Spain) and the United Kingdom, and Japan.

The Insomnia market report provides current treatment practices, emerging drugs, and market share of the individual therapies, current and forecasted 7MM Insomnia market size from 2022 to 2036. The Report also covers current Insomnia treatment practice, market drivers, market barriers, SWOT analysis, reimbursement and market access, and unmet medical needs to curate the best of the opportunities and assess the underlying potential of the market.

Scope of the Insomnia Market | |

|

Study Period |

2022 to 2036 |

|

Forecast Period |

2026-2036 |

|

Geographies Covered |

|

|

Insomnia Market |

|

|

Insomnia Market Size | |

|

Insomnia Companies |

Merck & Co., Eisai Co. Ltd., Idorsia Ltd., Takeda Pharmaceutical, Pfizer Inc., Sanofi S.A., Viatris Inc., Teva Pharmaceutical, Dr. Reddy's Laboratories, Big Health, Pear Therapeutics, and others. |

|

Insomnia Epidemiology Segmentation |

|

Insomnia Disease Understanding

Insomnia Overview

Insomnia, a prevalent sleep–wake disorder, is marked by dissatisfaction with sleep quality or duration, manifesting as difficulties falling asleep, frequent awakenings, or early-morning wakefulness with inability to return to sleep. The American Academy of Sleep Medicine defines insomnia as trouble falling or staying asleep with resultant daytime impairments. The International Classification of Sleep Disorders (ICSD-3) characterizes it by issues initiating, maintaining sleep, or early awakenings, accompanied by daytime dysfunction. The DSM-V describes insomnia as dissatisfaction with sleep quantity or quality, often involving difficulty falling or staying asleep, present for at least three months or occurring three times per week, now termed Insomnia disorder.

Although no single cause is established, physiological arousal, including heightened heart rate and increased cortisol, often disrupts sleep. Insomnia is categorized into short-term and chronic types, with chronic insomnia marked by persistent symptoms over three months or longer. Age, gender, medical and psychiatric conditions, and shift work are significant risk factors.

Insomnia Diagnosis

Insomnia diagnosis relies on subjective reports of sleep initiation or maintenance difficulties and associated daytime impairments. Objective assessment uses actigraphy, which tracks limb movements with wearable devices, providing data on sleep patterns like latency and efficiency. For detailed sleep analysis, including Non-REM and REM cycles, polysomnography is employed but is not routinely used for insomnia unless another disorder is suspected, such as sleep apnea. Additionally, diagnostic tools include the Insomnia Severity Index (ISI), which scores up to 28 to gauge insomnia severity, and the Pittsburgh Sleep Quality Index (PSQI), a 19-question survey assessing various sleep aspects over a month.

Despite advances in insomnia diagnostics, several unmet needs persist. Current diagnostic tools, while useful, often lack sensitivity in distinguishing between primary insomnia and secondary sleep disorders, leading to potential misdiagnoses. Actigraphy and polysomnography, although valuable, can be costly and cumbersome, limiting their accessibility and routine use. There is also a need for more precise biomarkers or objective measures to complement subjective reports and improve diagnostic accuracy. Additionally, existing questionnaires like the ISI and PSQI may not fully capture the complexity of insomnia's impact on daily functioning. Enhanced diagnostic methods that integrate comprehensive sleep assessments with technological innovations and personalized approaches could address these gaps and lead to more effective management strategies.

Further details related to diagnosis are provided in the report…

Insomnia Treatment

The treatment goal for insomnia is improving the patient’s ability to fall, stay, wake, and function well. According to various guidelines, insomnia is primarily treated using behavioral and psychological therapies such as Cognitive Behavioral Therapy for insomnia (CBT-I).

CBT-I is a multi-component gold standard for treating chronic insomnia, including cognitive, behavioral, and psychoeducational interventions. The first line of treatment recommended for insomnia is delivered through 4–8 sessions, typically by a clinician with specialized training in this area. In 2020, the US FDA approved Pear Therapeutics, SOMRYST, the first digital therapeutic drug to chronic insomnia.

In most acute cases, to increase the effectiveness of non-pharmacological therapies, various pharmacological therapies are also recommended to ameliorate the condition.

Across decades, various classes have been approved by the US FDA for the treatment of insomnia, that include benzodiazepines (temazepam, triazolam, estazolam, flurazepam, and quazepam), non-benzodiazepines (also called “Z-drugs”) (zolpidem, eszopiclone, zaleplon, or zolpidem tartrate), both of which are used as first-line pharmacotherapy. The additional classes approved by the US FDA include selective histamines antagonists, melatonin receptor agonists, such as ramelteon, and orexin receptor antagonists, such as suvorexant, lemborexant, and daridorexant.

Dual orexin receptor antagonists (DORAs), the latest entrants in the treatment landscape, changed this treatment paradigm of Z-drug or a benzodiazepine associated with some significant side effects, including drowsiness the next morning, impacting the quality of life. The three approved products in this class include BELSOMRA, DAYVIGO, and QUVIVIQ.

Merck’s BELSOMRA (suvorexant) is the first entrant in the US (2014) market, followed by Eisai’s DAYVIGO (lemborexant). The recent product to be marketed in the US and Europe is Idorsia, Syneos Health, and Mochida Pharmaceutical’s QUVIVIQ (daridorexant), a dual orexin receptor antagonist. This product was approved by the US FDA in January 2014 for the treatment of adults with insomnia.

Further details related to treatment are provided in the report…

Insomnia Epidemiology

As the market is derived using the patient-based model, the Insomnia epidemiology chapter in the report provides historical as well as forecasted epidemiology segmented by Total Diagnosed Prevalent Cases of Insomnia, Type-Specific Cases of Insomnia, Gender-Specific Cases of Insomnia, and Age-Specific Cases of Insomnia in the 7MM covering the United States, EU4 countries (Germany, France, Italy, and Spain) and the United Kingdom, and Japan, from 2022 to 2036.

Key Findings from Insomnia Epidemiological Analyses and Forecast

- In 2025, diagnosed prevalent cases of insomnia across the 7MM were estimated at approximately 90 million.

- According to DelveInsight, among the 7MM, the US had the highest number of cases of insomnia, followed by France, Japan, and Germany in 2025.

- In 2025, age-specific diagnosed prevalent cases of insomnia showed the highest prevalence among individuals aged ≥65 with nearly 2 million cases and the lowest among those aged 18–24 with approximately 300,000 cases in Japan.

- According to DelveInsight estimates, acute insomnia had the highest number of cases in the US in 2025, totaling ~33 million, while chronic insomnia accounted for ~27 million cases.

- According to DelveInsight, the total diagnosed prevalent cases of insomnia in the US comprised approximately 60 million in 2025 and are projected to increase during the forecast period.

- According to DelveInsight, in 2025, the prevalence of insomnia was greater among females, making up 58%, while males accounted for 42% in the US.

Stay Informed on Insomnia Epidemiology! Access comprehensive data on demographics and disease burden for effective healthcare planning.

Insomnia Market Drug Analysis

The drug chapter segment of the Insomnia report encloses a detailed analysis of Insomnia off-label drugs and late-stage (Phase-III and Phase-II) pipeline drugs. It also helps to understand the Insomnia clinical trial details, expressive pharmacological action, agreements and collaborations, approval and patent details, advantages and disadvantages of each included drug, and the latest news and press releases.

Insomnia Marketed Drugs

QUVIVIQ (daridorexant): Idorsia Pharmaceutical/ Syneos Health/ Mochida Pharmaceutical

QUVIVIQ (daridorexant), developed by Idorsia Pharmaceuticals, is an orexin receptor antagonist designed to treat insomnia in adults by addressing difficulties with sleep onset and maintenance. By targeting orexin, a neuropeptide that promotes wakefulness, QUVIVIQ reduces nocturnal hyperarousal, enhancing sleep quality without causing next-morning residual effects. Initially developed by Actelion and later acquired by Johnson & Johnson, Idorsia now leads its development. The drug has completed Phase III trials in Japan, with an NDA submitted, as per the company’s latest July 2024 corporate presentation. In Japan, Idorsia has a license agreement with Mochida Pharmaceutical for the supply, co-development and comarketing of daridorexant. All potential milestones have been assigned to Nxera. The recommended dose is 25–50 mg taken orally before bed.

In January 2022, the US FDA approved QUVIVIQ (daridorexant) 25 mg and 50 mg for treating adults with insomnia characterized by difficulties with sleep onset and/or sleep maintenance. QUVIVIQ was launched in the US in May 2022. In November 2022, QUVIVIQ was launched in Italy and Germany, followed by Spain in September 2023, the UK in October 2023, and France in March 2024.

DAYVIGO: Eisai

DAYVIGO (lemborexant) is an orexin receptor antagonist indicated for treating adult patients with insomnia, characterized by difficulties with sleep onset and/or sleep maintenance. The recommended dosage of DAYVIGO is 5 mg, taken no more than once per night immediately before going to bed, with at least 7 h remaining before the planned time of awakening. In December 2019, the US FDA approved DAYVIGO (lemborexant) for treating insomnia characterized by difficulties with sleep onset and/or sleep maintenance in adults. In January 2020, Japan approved DAYVIGO (lemborexant) for the treatment of insomnia.

Insomnia Emerging Drugs

Seltorexant (JNJ-42847922): Janssen Pharmaceutical

Seltorexant, with the code name JNJ-42847922, is a selective orexin-2 receptor antagonist developed by Janssen Pharmaceutical as adjunctive therapy for major depressive disorder (MDD) and the treatment of insomnia disorder. In September 2025, Johnson & Johnson reported results from the Phase III MDD3005 26-week clinical trial evaluating Seltorexant as an adjunctive treatment in adults and elderly patients with MDD experiencing Insomnia symptoms. The study assessed the efficacy and safety of seltorexant compared with Quetiapine Extended‑Release in patients with MDD and comorbid sleep disturbances.

HETLIOZ (tasimelteon): Vanda Pharmaceuticals

HETLIOZ (tasimelteon), also known as VEC-162, developed by Vanda Pharmaceuticals, is a melatonin receptor agonist of the human MT1 and MT2 receptors, with greater specificity for MT2. The drug is a circadian regulator that can reset the master body clock in the suprachiasmatic nucleus (SCN) located in the hypothalamus. In September 2025, Vanda Pharmaceuticals reported the publication of a study evaluating tasimelteon (marketed as HETLIOZ) in PLOS One, assessing its efficacy in patients with Primary Insomnia. The multicenter, randomized, double-blind, placebo-controlled trial demonstrated that tasimelteon met its primary endpoint, showing a mean improvement in latency to persistent sleep (LPS) from baseline to the average of Nights 1 and 8. Vanda Pharmaceuticals continues to pursue development of tasimelteon for insomnia following the 2024 refusal decision by the US FDA.

|

Drug |

MoA |

RoA |

Company |

Logo |

Phase |

|

Seltorexant (JNJ-42847922) |

Orexin receptor antagonist |

Oral |

Janssen Pharmaceutical |

III | |

|

XXX |

Nociceptin receptor agonist |

XXX |

XXX |

II |

Explore the latest insights into the Insomnia pipeline, emerging therapies, and future treatment potential. Stay informed today!

Insomnia Market Outlook

Insomnia, the most prevalent sleep-wake disorder, often remains inadequately treated. It is marked by difficulties with falling or staying asleep, leading to daytime issues such as fatigue, concentration problems, and irritability. The disorder is linked to increased risks of comorbidities, accidents, and workplace impairment. Cognitive Behavioral Therapy for Insomnia (CBT-I) is recommended as a primary treatment by leading sleep organizations but faces challenges like limited access to trained therapists and high costs, leaving pharmacotherapy as a crucial management option.

Approved pharmacotherapies in the US for insomnia include benzodiazepines and non-benzodiazepines or Z-drugs. Additional options include selective histamine H1 antagonists, melatonin receptor agonists like ramelteon, and orexin receptor antagonists such as suvorexant and lemborexant. The latest addition is QUVIVIQ, by Idorsia, which is also being developed in Japan.

Benzodiazepines and Z-drugs are associated with significant side effects like next-day drowsiness, while melatonin receptor agonists are more effective for sleep onset but less so for maintaining sleep. Existing drugs are facing revenue declines due to generic competition. DORAs like BELSOMRA and DAYVIGO have struggled with market adoption, but QUVIVIQ’s recent approval in Europe positions Idorsia with a potential breakthrough advantage in the insomnia treatment landscape.

The current market has been segmented into different commonly used therapeutic classes based on the prevailing treatment pattern across the 7MM, which presents minor variations in the overall prescription pattern. Benzodiazepines, non-benzodiazepines, melatonin receptor agonists, other antidepressants, BELSOMRA, DAYVIGO, and QUVIVIQ are the major drugs covered in the forecast model.

Key Findings from Insomnia Market Forecast Report

The launch of emerging therapies, such as Seltorexant (JNJ-42847922), and others are expected to impact the market positively. The approval of these therapies could significantly impact market dynamics, although their success rates remain uncertain.

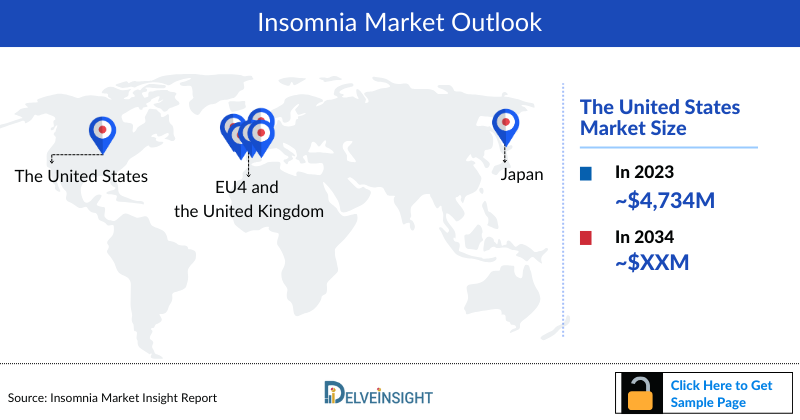

- The market size of Insomnia in the US was nearly USD 4,734 million in 2023, which is further anticipated to increase during the forecast period.

- The EU4 and the UK accounted for the approximately USD 774 million market size of Insomnia approximately in 2023.

- Among the EU countries, France had the highest market size with nearly ~USD 352 million in 2023, while Spain had the lowest market size for Insomnia with USD ~82 million in 2023.

- With the expected launch of upcoming therapies, such as Seltorexant (JNJ-42847922) among others, the total market size of Insomnia is expected to show change in the upcoming years.

Insomnia Market Competitive Landscape

The global insomnia market is highly competitive and moderately consolidated, with leading pharmaceutical companies, digital therapeutics providers, and generic drug manufacturers competing through innovation, strategic collaborations, geographic expansion, and product launches. The market is witnessing rapid advancements in orexin receptor antagonists, cognitive behavioral therapy for insomnia (CBT-I), and next-generation sleep therapeutics.

Key Insomnia Market Companies

The Insomnia Market companies developing therapies include -

- Merck & Co.,

- Eisai Co. Ltd.,

- Idorsia Ltd.,

- Takeda Pharmaceutical,

- Pfizer Inc.,

- Sanofi S.A.,

- Viatris Inc.,

- Teva Pharmaceutical,

- Dr. Reddy's Laboratories,

- Big Health, Pear Therapeutics, and others.

Insomnia Drugs Uptake

This section focuses on the uptake rate of potential drugs expected to launch in the market during 2020–2034. For example, Seltorexant in the US is expected to be launched by 2025 with a peak share of 6.6%. TS-142 is anticipated to take 9 years to peak with a slow uptake.

Further detailed analysis of emerging therapies drug uptake in the report…

Insomnia Clinical Trial Activities

The Insomnia Pipeline report provides insights into Insomnia clinical trials within Phase III, Phase II, and Phase I stage. It also analyzes key players involved in developing targeted therapeutics.

Insomnia Pipeline Development Activities

The Insomnia Clinical Trial analysis report covers information on collaborations, acquisitions and mergers, licensing, and patent details for Insomnia emerging therapies.

Latest KOL Views on Insomnia

To keep up with current market trends, we take KOLs and SMEs’ opinions working in the domain through primary research to fill the data gaps and validate the secondary research. Industry Experts were contacted for insights on Insomnia evolving treatment landscape, patient reliance on conventional therapies, patient therapy switching acceptability, and drug uptake along with challenges related to accessibility, including KOL from The University of Missouri, Columbia, Missouri, US; University of Iowa, Iowa City, Iowa, US; Keele University, Staffordshire, UK; Hospital Universitari de la Ribera, Alzira, Valencia, Spain; Université Montpellier, Montpellier, France; University of Pisa, Pisa, Italy; Robert Koch Institute, Berlin, Germany; Teikyo University School of Medicine, Tokyo, Japan; and others.

Delveinsight’s analysts connected with 50+ KOLs to gather insights; however, interviews were conducted with 15+ KOLs in the 7MM. Their opinion helps understand and validate current and emerging therapies, treatment patterns, or Insomnia market trends. This will support the clients in potential upcoming novel treatments by identifying the overall scenario of the market and the unmet needs.

Insomnia Market Access and Reimbursement

The high cost of therapies for the treatment is a major factor restraining the growth of the global drug market. Because of the high cost, the economic burden is increasing, leading the patient to escape from proper treatment.

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of approved therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

Scope of the Insomnia Market Report

- The Insomnia Market report covers a segment of key events, an executive summary, descriptive overview of Insomnia, explaining its causes, signs and symptoms, and currently available therapies.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of diagnosis rate, disease progression, and treatment guidelines.

- Additionally, an all-inclusive account of the current and emerging therapies and the elaborative profiles of late-stage and prominent therapies will impact the current treatment landscape.

- A detailed review of the Insomnia market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind the approach is included in the report covering the 7MM drug outreach.

- The Insomnia Market report provides an edge while developing business strategies, by understanding trends, through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help shape and drive the 7MM Insomnia market.

Insomnia Market Report Insights

- Insomnia Patient Population

- Insomnia Therapeutic Approaches

- Insomnia Pipeline Analysis

- Insomnia Market Size and Trends

- Existing and Future Insomnia Market Opportunity

Insomnia Market Report Key Strengths

- 11 years Forecast

- The 7MM Coverage

- Insomnia Epidemiology Segmentation

- Key Cross Competition

- Conjoint Analysis

- Insomnia Drugs Uptake

- Key Insomnia Market Forecast Assumptions

Insomnia Market Report Assessment

- Current Treatment Practices

- Insomnia Market Unmet Needs

- Insomnia Pipeline Product Profiles

- Insomnia Market Attractiveness

- Qualitative Analysis (SWOT and Conjoint Analysis)

- Insomnia Market Drivers

- Insomnia Market Barriers

Key Questions Answered In The Insomnia Market Report:

Insomnia Market Insights

- What was the Insomnia market share (%) distribution in 2022 and how it would look like in 2036?

- What would be the Insomnia total market size as well as market size by therapies across the 7MM during the forecast period (2026–2036)?

- What are the key findings pertaining to the market across the 7MM and which country will have the largest Insomnia market size during the forecast period (2026–2036)?

- At what CAGR, the Insomnia market is expected to grow at the 7MM level during the forecast period (2026–2036)?

- What would be the Insomnia market outlook across the 7MM during the forecast period (2026–2036)?

- What would be the Insomnia market growth till 2036 and what will be the resultant market size in the year 2036?

- How would the market drivers, barriers, and future opportunities affect the market dynamics and subsequent analysis of the associated trends?

Insomnia Epidemiology Insights

- What is the disease risk, burden, and unmet needs of Insomnia?

- What is the historical Insomnia patient population in the United States, EU5 (Germany, France, Italy, Spain, and the UK), and Japan?

- What would be the forecasted patient population of Insomnia at the 7MM level?

- What will be the growth opportunities across the 7MM with respect to the patient population pertaining to Insomnia?

- Out of the above-mentioned countries, which country would have the highest prevalent population of Insomnia during the forecast period (2026–2036)?

- At what CAGR the population is expected to grow across the 7MM during the forecast period (2026–2036)?

Current Insomnia Treatment Scenario, Marketed Drugs, and Emerging Therapies

- What are the current options for the treatment of Insomnia along with the approved therapy?

- What are the current treatment guidelines for the treatment of Insomnia in the US, Europe, And Japan?

- What are the Insomnia marketed drugs and their MOA, regulatory milestones, product development activities, advantages, disadvantages, safety, and efficacy, etc.?

- How many companies are developing therapies for the treatment of Insomnia?

- How many emerging therapies are in the mid-stage and late stages of development for the treatment of Insomnia?

- What are the key collaborations (Industry–Industry, Industry-Academia), Mergers and acquisitions, licensing activities related to the Insomnia therapies?

- What are the recent therapies, targets, mechanisms of action and technologies developed to overcome the limitation of existing therapies?

- What are the clinical studies going on for Insomnia and their status?

- What are the key designations that have been granted for the emerging therapies for Insomnia?

- What are the 7MM historical and forecasted market of Insomnia?

Reasons to Buy Insomnia Market Forecast Report

- The Insomnia Market report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the Insomnia Market.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- To understand the existing market opportunity in varying geographies and the growth potential over the coming years.

- Distribution of historical and current patient share based on real-world prescription data along with reported sales of approved products in the US, EU4 (Germany, France, Italy, and Spain), the United Kingdom, and Japan.

- Identification of strong upcoming players in the market will help in devising strategies that will help in getting ahead of competitors.

- Detailed analysis and potential of current and emerging therapies under the conjoint analysis section to provide visibility around leading emerging drugs.

- Highlights of Access and Reimbursement policies of approved therapies, barriers to accessibility of off-label expensive therapies, and patient assistance programs.

- To understand the perspective of Key Opinion Leaders around the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in future.

- Detailed insights on the Insomnia Market unmet need of the existing market so that the upcoming players can strengthen their development and launch strategy.