Non-Small Cell Lung Cancer Market Summary

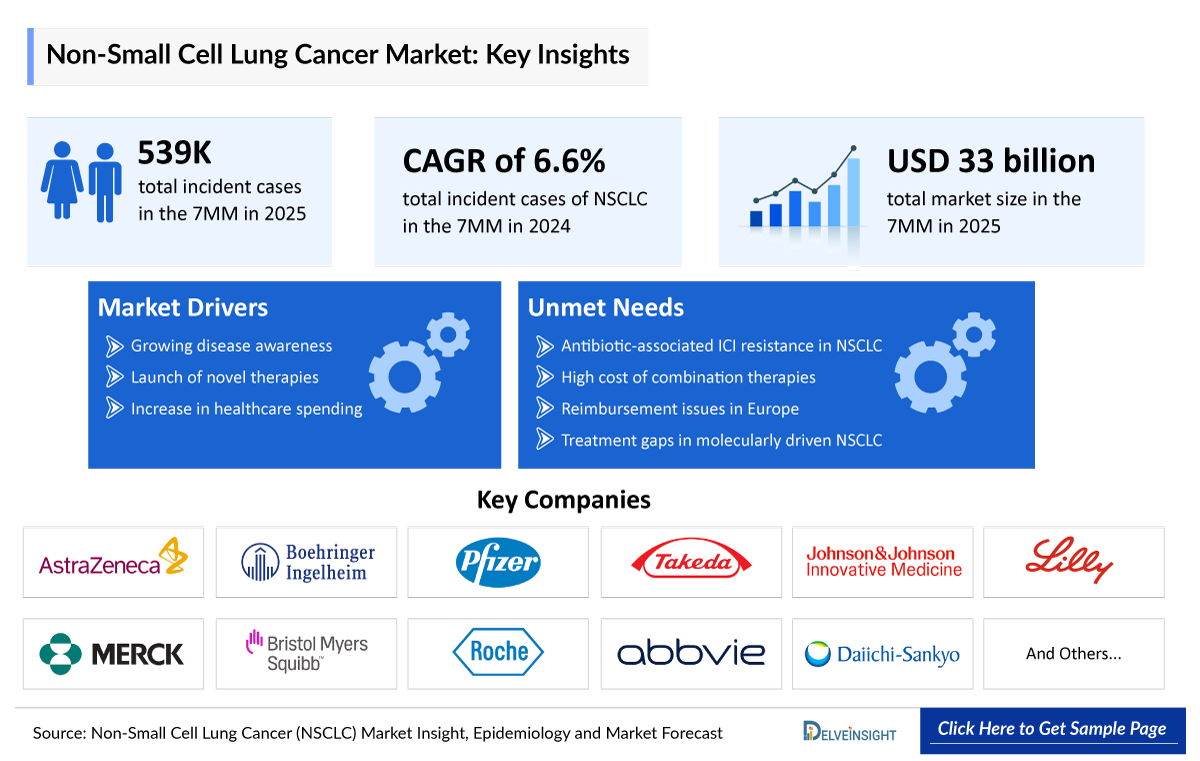

- According to DelveInsight’s analysis, NSCLC market size was found to be ~33 billion in the leading markets (the United States, the EU4 (Germany, France, Italy, and Spain), the United Kingdom, and Japan) in 2025.

Non-Small Cell Lung Cancer (NSCLC) Insights and Trends

- According to DelveInsight’s analysis, NSCLC market size was found to be ~33 billion in the leading markets (the United States, the EU4 (Germany, France, Italy, and Spain), the United Kingdom, and Japan) in 2025.

- NSCLC is the most common type of lung cancer accounted for approximately 85% of all lung cancers. However, NSCLC metastasizes to other organs slower in comparison to small cell lung cancer, and microscopically, SCLC is composed of much smaller cells. NSCLC is mainly subcategorized into adenocarcinomas, squamous cell carcinomas, large cell carcinomas and several other types that occur less frequently include adenosquamous carcinomas, and sarcomatoid carcinomas.

- The real-world treatment trend depicts a significant shift towards targeted and immunotherapies (from only systemic therapies in the past), which is expected to contribute the most now.

- A majority of the population of NSCLC patients are not candidates for targeted therapy. PD-L1 therapies are mainly utilized in patients without genetic drivers. Merck’s KEYTRUDA is generally considered the ‘gold standard’ of care in 1L NSCLC when combined with platinum chemotherapy, regardless of PD-1 status.

- Acquired resistance to anti-PD-1/L1 therapies is a key issue. Acquired resistance renders these therapies effectively useless in half of the patient population after this period where they fall back to chemotherapy approaches which are often ineffective and/or toxic. Given the high unmet need in this area, many companies are exploring novel molecules and combinations in second-line NSCLC post-IO.

- From last few years, exon 20 insertions EGFR mutations have received the most attention and this space has become competitive. In EGFR NSCLC, uncommon/atypical EGFR mutations (G719X, S768I, as well as PACC mutations), represent another frontier in this segment.

- At present, ALECENSA and ALUNBRIG are the preferred first-line ALK TKIs. ALECENSA is much more widely used compared to ALUNBRIG and dominate the ALK market. Prior to entry of ALECENSA and ALUNBRIG, XALKORI was the first-line treatment choice in ALK patients.

- The most frequent KRAS variants in NSCLC is G12C. Since the majority of treatments for NSCLC now target the G12C variant, this variant type is likely to become crowded and competitive. Future opportunities in G12C may be found in patient’s pool of approved KRAS drugs and in the first-line setting.

- Due to rarity of some biomarkers in NSCLC and the lack of late-stage clinical studies, the treatment paradigm for rare NSCLC mutations is less clear. Rare biomarkers like ROS-1, HER2, RET fusion, and NTRK1/2/3 Gene fusion have seen a lot of progress in past few years.

- Despite advances in precision medicine and immunotherapy, early-stage NSCLC (Stages I–III) remains a major unmet need. Standard treatment, surgery with adjuvant platinum-based chemotherapy, offers limited survival benefit, significant toxicity, and inconsistent patient benefit. Although immunotherapies such as PD-1/PD-L1 inhibitors and neoadjuvant chemo-immunotherapy show promising improvements in event-free survival and pathological response, their routine use in early-stage care is still evolving, unevenly accessible, and not yet widely personalized.

Non-Small Cell Lung Cancer (NSCLC) Market size and forecast in the 7MM

- 2025 NSCLC Market Size: ~USD 33 billion

- 2036 Projected NSCLC Market Size: ~USD 67 billion

- NSCLC Growth Rate (2026–2036): 6.6% CAGR

DelveInsight's ‘Non-Small Cell Lung Cancer (NSCLC) Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of the NSCLC, historical and forecasted epidemiology, as well as the NSCLC market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan

The NSCLC market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates, NSCLC patient burden trends, revenue & market share dynamics, peak patient share and therapy uptake analysis, and provides an in-depth market size assessment, and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in NSCLC and maps the competitive and clinical landscape to uncover high-value opportunities, providing a clear outlook on future market growth potential.

Scope of the Non-Small Cell Lung Cancer Market Report | |

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

NSCLC Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

NSCLC Companies |

|

|

NSCLC Therapies |

|

|

NSCLC Market |

Segmented by

|

|

Analysis |

|

Key Factors Driving the Non-Small Cell Lung Cancer (NSCLC) Market

Rising NSCLC Incidence

NSCLC incident cases in the US form a substantial yet gradually stabilizing disease burden, characterized by declining overall incidence driven by long-term tobacco control measures alongside rising early-stage detections from expanded low-dose CT screening programs and incidental imaging findings in routine care. In the US, in 2025, there were ~203,000 incident cases of NSCLC, which will further reach ~205,000 by 2036.

Rising Opportunities in EGFR NSCLC Therapies

In EGFR-mutated NSCLC, where TAGRISSO is the industry leader, J&J's RYBREVANT is gradually gaining ground. RYBREVANT from J&J has joined the broad first-line EGFR-mutated NSCLC market (RYBREVANT in combination with the oral EGFR-TKI LAZCLUZE). The company also intends to launch the SC version of RYBREVANT.

Emerging NSCLC Competitive Landscape

The most frequent KRAS variants in NSCLC is G12C. Since the majority of treatments for NSCLC now target the G12C variant, this variant type is likely to become crowded and competitive. Future opportunities in G12C may be found in R/R patient’s pool of approved KRAS drugs and in the first-line setting. Emerging key players in the pipeline include Eli Lilly, Genfleet Therapeutics/Merck, Merck/Otsuka Pharmaceutical, BioAtla, Taiho Pharmaceutical, Astex Pharmaceuticals, Revolution Medicines, Roche, Verastem Oncology, and others.

Non-Small Cell Lung Cancer (NSCLC) Understanding and Treatment Algorithm

NSCLC Overview and Diagnosis

Lung cancer primarily originates in the lungs and may spread to lymph nodes or distant organs such as the brain; this process is called metastasis. It is mainly classified into two types: small cell lung cancer (SCLC) and NSCLC. NSCLC is the most common type, accounting for about 85% of all lung cancers. Compared with NSCLC, SCLC is more aggressive, composed of smaller cells, spreads rapidly, and can become fatal within weeks if untreated. NSCLC refers to all epithelial lung cancers other than SCLC and is mainly classified into adenocarcinoma, squamous cell carcinoma, and large cell carcinoma, with less common types including adenosquamous and sarcomatoid carcinomas. Although strongly associated with cigarette smoking, adenocarcinoma may also occur in never-smokers. NSCLC is generally less sensitive to chemotherapy and radiation therapy than SCLC.

NSCLC arises from epithelial cells along the respiratory tract, from central bronchi to terminal alveoli. Histological subtype often correlates with the site of origin: squamous cell carcinoma typically develops near central bronchi, whereas adenocarcinoma and bronchioloalveolar carcinoma usually arise in peripheral lung tissue. Common symptoms of both NSCLC and SCLC include persistent cough, chest pain, shortness of breath, wheezing, loss of appetite, weight loss, and fatigue.

Further details are provided in the report.

Current NSCLC Treatment Landscape

Treatment options for NSCLC vary depending on disease stage and patient condition. Surgery is a primary treatment for early-stage NSCLC and includes procedures such as wedge or segmental resection (removal of the tumor with a small margin of healthy tissue), lobectomy (removal of a lung lobe), pneumonectomy (removal of an entire lung), and sleeve resection (removal of part of the bronchus while preserving lung tissue). After surgery, some patients may receive adjuvant chemotherapy or radiation therapy to eliminate residual microscopic disease and reduce recurrence risk

Radiation therapy uses high-energy radiation to destroy or inhibit cancer cell growth and can be delivered externally or internally. External radiation therapy directs radiation from outside the body, with advanced methods such as stereotactic body radiation therapy (SBRT) providing highly precise high-dose radiation to the tumor while minimizing damage to healthy tissue. Stereotactic radiosurgery is often used when lung cancer metastasizes to the brain. Internal radiation therapy involves placing radioactive materials directly into or near the tumor, sometimes through an endoscope for airway tumors. Chemotherapy involves drugs that kill cancer cells or prevent their division and is usually administered systemically through oral or intravenous routes. Common agents include carboplatin, cisplatin, docetaxel, doxorubicin, etoposide, gemcitabine, paclitaxel, pemetrexed, and vinorelbine. Chemotherapy may be used alone or in combination with other treatments such as radiation therapy or immunotherapy. Targeted therapy focuses on specific molecular abnormalities in cancer cells, and biomarker testing is often performed to identify suitable patients. Major targeted therapies include EGFR inhibitors (osimertinib, erlotinib, gefitinib), ALK inhibitors (alectinib, brigatinib, lorlatinib), KRAS inhibitors (sotorasib, adagrasib), and inhibitors targeting RET, MET, BRAF, and NTRK alterations (such as selpercatinib, capmatinib, dabrafenib, and larotrectinib). Angiogenesis inhibitors and monoclonal antibodies, including bevacizumab, ramucirumab, and cetuximab, are also used. Immunotherapy enhances the body’s immune response against cancer cells. Approved agents for NSCLC include atezolizumab, cemiplimab, durvalumab, ipilimumab, nivolumab, pembrolizumab, and tremelimumab, which may be used alone or combined with chemotherapy or other immunotherapies.

Additional local treatments are sometimes used for airway tumors or symptom relief. Laser therapy uses focused light energy to destroy cancer cells and relieve airway obstruction. Photodynamic therapy (PDT) combines a photosensitizing drug with laser light to selectively destroy cancer cells, typically administered through an endoscope. Cryosurgery (cryotherapy) destroys abnormal tissue by freezing it and is useful for carcinoma in situ or airway tumors. Electrocautery uses an electrically heated probe to destroy abnormal tissue and is commonly performed endoscopically..

Further details related to country-based variations are provided in the report.

Non-Small Cell Lung Cancer (NSCLC) Unmet Needs

The section “unmet needs of NSCLC” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Antibiotic-associated ICI resistance in NSCLC

- High cost of combination therapies

- Reimbursement issues in Europe

- Treatment gaps in molecularly driven NSCLC

and others…..

Note: Comprehensive unmet needs insights in NSCLC and their strategic implications are provided in the full report.

Non-Small Cell Lung Cancer (NSCLC) Epidemiology

Key Findings from NSCLC Epidemiological Analysis and Forecast

- Based on DelveInsight's assessment in 2025, the 7MM had approximately 539,000 incident cases of NSCLC. These are expected to rise due to the growing incident population and advancements in diagnostic capabilities during the forecast period (2026-2036).

- Among the 7MM, the US accounted for the highest incident cases of NSCLC in 2025. This was followed by Japan, whereas the least number of cases were accounted by Spain.

- In 2025, Germany had the highest number (~57,000) of NSCLC cases among the EU4 and the UK, while Spain had the lowest number (~27,00).

- NSCLC is slightly more common in men than in women. In addition, NSCLC has a substantially higher prevalence in individuals aged 65 years and older; alarmingly, however, the number of cases in persons younger than age 65 years has risen.

- Most cases of NSCLC are diagnosed at advanced Stage IV, primarily due to delayed detection, limited access to screening in underserved populations, nonspecific early symptoms, and socioeconomic barriers to timely healthcare. However, diagnoses at early stages (Stage I) have been increasing, largely driven by the wider use of low-dose CT screening in high-risk individuals and the growing number of incidental findings during imaging performed for other medical conditions. In contrast, the incidence of Stage II–III disease has remained relatively stable.

- The rising incidence of adenocarcinoma may partly reflect improved evaluation and reporting practices, along with underlying idiopathic trends. This increase is also likely influenced by a sustained rise in cigarette smoking, as adenocarcinoma shows a strong dose response relationship with tobacco exposure and a slower decline in risk after smoking cessation compared with squamous cell carcinoma. Consequently, increasing regional smoking prevalence has contributed to higher overall NSCLC incidence, including adenocarcinoma.

-Epidemiology-Insights1.png)

Recent Development

- In May 2026, China's NMPA has formally accepted for review a Supplemental New Drug Application (sNDA) for sacituzumab tirumotecan (Sac-TMT) in combination with pembrolizumab as a frontline treatment for advanced PD-L1 positive non-small cell lung cancer (NSCLC). Sac-TMT is an innovative antibody-drug conjugate (ADC), and its therapeutic combination with the established checkpoint inhibitor pembrolizumab represents a major clinical effort to improve progression-free survival in lung cancer patients. The regulatory acceptance initiates an official review process that could establish a highly potent, chemotherapy-free targeted regimen as a first-line standard of care.

- In May 2026, Nuvation Bio has entered into a strategic collaboration with Thermo Fisher Scientific for the U.S.-based manufacturing of ibtrozi, an investigational drug targeting ROS1-positive non-small cell lung cancer (NSCLC). This partnership secures high-quality, domestic commercial manufacturing capacity as Nuvation Bio prepares for the potential regulatory approval and commercial launch of ibtrozi. Thermo Fisher will leverage its extensive global pharma services network to manage the production scale-up, formulation, and supply chain logistics. By establishing a robust local manufacturing foundation, Nuvation Bio aims to ensure a stable, uninterrupted market supply of this critical oncology therapy for patients across the United States.

- In May 2026, Innovent Biologics announced that preliminary proof-of-concept data for IBI363—a first-in-class PD-1/IL-2α-bias bispecific fusion protein—will be highlighted at the 2026 ASCO Annual Meeting. Evaluated in combination with platinum-based doublet chemotherapy as a first-line treatment for advanced non-small cell lung cancer (NSCLC) with low or negative PD-L1 expression, IBI363 demonstrated remarkable efficacy signals. In the optimized step-down dosing cohort (3 mg/kg transitioning to 1.5 mg/kg), the treatment achieved an objective response rate of 86.4% and a 100% disease control rate, outperforming traditional checkpoint inhibitor therapies in this tough-to-treat population. Furthermore, the optimized regimen showed a favorable safety profile with lower rates of severe treatment-emergent adverse events compared to flat-dose groups. Backed by these successful results, Innovent has initiated a randomized Stage II trial comparing this IBI363 combo head-to-head against standard pembrolizumab plus chemotherapy.

- In May 2026, Nuvation Bio shared patient-reported outcome data from its pivotal TRUST-II study evaluating IBTROZI (taletrectinib) in patients with advanced ROS1-positive non-small cell lung cancer (NSCLC). To be presented at ASCO 2026, the data showed that 88% of patients reported improved or stable health-related quality of life at the very first post-baseline assessment. IBTROZI demonstrated rapid, clinically meaningful improvements in severe cancer symptoms, significantly easing persistent coughing, chest pain, and shortness of breath. Crucially, the treatment successfully preserved cognitive function and mental clarity over time, addressing a major concern for patients undergoing intensive tyrosine kinase inhibitor (TKI) therapies. Because ROS1-positive NSCLC frequently metastasizes to the brain, maintaining cognitive health while aggressively shrinking tumors is a vital therapeutic milestone. These outcomes position IBTROZI as a highly effective, well-tolerated next-generation treatment option that prioritizes long-term patient well-being alongside oncological efficacy.

- In May 2026, Dizal announced positive topline results from its global Phase 3 WU-KONG28 trial. The study demonstrated that Zegfrovy (sunvozertinib) significantly outperformed standard platinum-doublet chemotherapy when used as a first-line treatment for patients with advanced non-small cell lung cancer (NSCLC) harboring EGFR exon 20 insertion mutations. Zegfrovy showed superior progression-free survival (PFS)—the length of time a patient lives without the disease worsening—and a highly favorable objective response rate. Because EGFR exon 20 insertion mutations have historically responded poorly to standard targeted treatments, these trial results position Zegfrovy as a potential breakthrough frontline therapy, shifting the treatment paradigm away from traditional chemotherapy for this specific patient population.

Non-Small Cell Lung Cancer (NSCLC) Drug Analysis & Competitive Landscape

The NSCLC drug chapter provides a detailed, market-focused review of approved therapies and the emerging pipeline across Phase I–III clinical trials. It covers mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, strategic partnerships, upcoming key catalyst for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the NSCLC treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the NSCLC market.

Approved Therapies for NSCLC

AUMSEQA (Aumolertinib): Jiangsu Hansoh Pharmaceutical

Aumolertinib is a third-generation EGFR-TKI for the treatment of locally advanced or metastatic NSCLC with activating EGFR mutations, including EGFR T790M-positive disease. In June 2025, the UK MHRA granted marketing authorization to aumolertinib mesilate tablets as monotherapy for these indications.

TEVIMBRA (Tislelizumab): BeiGene

EVIMBRA is a humanized IgG4 anti-PD-1 monoclonal antibody with high affinity and specificity for PD-1, designed to minimize Fc? receptor binding and enhance immune-mediated tumor recognition. In August 2025, the European Commission approved it in combination with platinum-based chemotherapy as neoadjuvant therapy followed by TEVIMBRA monotherapy as adjuvant treatment for adults with resectable NSCLC at high risk of recurrence.

HERNEXEOS (Zongertinib): Boehringer Ingelheim

Zongertinib (BI 1810631) is an investigational oral HER2-specific tyrosine kinase inhibitor being developed for HER2 (ERBB2)-mutant NSCLC. In September 2025, Boehringer Ingelheim received approval in Japan for HERNEXEOS, the first oral targeted therapy for previously treated HER2-mutant advanced NSCLC, and in November 2025 the FDA granted zongertinib a Commissioner’s National Priority Voucher (CNPV) recognizing its potential to address this rare and aggressive cancer.

NSCLC Marketed Therapies Key Competitors in 7MM | ||||||||

|

Drug |

Developer |

MoA |

RoA |

Molecule Type |

Patient segment |

US Approval |

EU Approval |

Japan Approval |

|

TAGRISSO (osimertinib) |

AstraZeneca |

EGFR TKI |

Oral |

Small molecule |

EGFR T790M mutation-positive mNSCLC |

Conditional approval: November 2015 Full approval: March 2017 |

Conditional approval: February 2016 Full approval: April 2017 |

March 2016 |

|

EGFR mutated mNSCLC |

April 2018 |

June 2018 |

August 2018 | |||||

|

EGFR mutation-positive LA or mNSCLC combination with chemotherapy |

February 2024 |

July 2024 |

June 2024 | |||||

|

Locally advanced, unresectable (Stage III) EGFR mutation-positive NSCLC |

September 2024 |

December 2024 |

- | |||||

|

EGFR mutation-positive NSCLC |

December 2020 |

May 2021 |

August 2022 | |||||

|

GILOTRIF/GIOTRIF (afatinib maleate) |

Boehringer Ingelheim |

EGFR TKI |

Oral |

Small molecule |

Metastatic NSCLC with EGFR mutations |

July 2013 |

September 2013 |

January 2014 |

|

Advanced squamous cell carcinoma of the lung |

April 2016 |

April 2016 |

- | |||||

|

Metastatic NSCLC with non-resistant EGFR mutations |

January 2018 |

- |

- | |||||

|

VIZIMPRO (dacomitinib) |

Pfizer |

EGFR TKI |

Oral |

Small molecule |

Metastatic NSCLC with EGFR mutations |

September 2018 |

April 2019 |

January 2019 |

|

EXKIVITY (mobocertinib) |

Takeda Pharmaceuticals |

EGFR TKI |

Oral |

Small molecule |

LA/mNSCLCwith EGFR Exon 20 insertion mutations |

September 2021; 2024 (withdrawn) |

March 2022 (UK); July 2022 (withdrawn) |

- |

|

AUMSEQA (aumolertinib mesylate) |

Hansoh Pharma |

EGFR TKI |

Oral |

Small molecule |

LA or mNSCLC with activating EGFR mutations, LA or metastatic EGFR T790M mutation-positive NSCLC |

- |

June 2025 (UK); December 2025 (EMA) |

- |

|

ZEGFROVY (sunvozertinib) |

Dizal (Jiangsu) Pharmaceutical |

EGFR TKI |

Oral |

Small molecule |

LA or mNSCLC with EGFR exon 20 insertion mutations |

July 2025 |

- |

- |

|

RYBREVANT (amivantamab) |

Johnson & Johnson Innovative Medicine (Janssen) |

EGFR and MET inhibitor |

IV infusion |

bsMb |

LA/mNSCLCwith EGFR Exon 20 insertion mutations |

May 2021 |

December 2021 |

September 2024 |

|

NSCLC with EGFR Exon 20 mutation in combination with carboplatin and pemetrexed |

March 2024 |

April 2024 | ||||||

|

LA/mNSCLCwith EGFR Exon 19 or Exon 21 L858R mutations in combination with carboplatin and pemetrexed | September 2024 |

August 2024 |

- | |||||

|

LA/mNSCLCwith EGFR Exon 19 or Exon 21 L858R mutations in combination with LAZCLUZE |

August 2024 |

November 2024 |

- | |||||

|

DATROWAY (datopotamab deruxtecan) |

Daiichi Sankyo/AstraZeneca |

TROP2-directed ADC |

IV infusion |

ADC |

Locally advanced or metastatic EGFR-mutated NSCLC |

June 2025 |

December 2024 Withdrawn |

- |

|

PORTRAZZA (necitumumab) |

Eli Lilly and Company |

EGFR inhibitor |

IV infusion |

mAb |

Metastatic squamous NSCLC |

November 2015 |

- |

June 2019 |

|

KEYTRUDA (pembrolizumab) |

Merck (MSD) |

PD-1 Inhibitor |

IV infusion |

mAb |

Metastatic nsq-NSCLC without EGFR or ALK alterations with ALIMTA + platinum chemotherapy |

August 2018 |

September 2018 |

- |

|

mNSCLC with carboplatin and either paclitaxel/nab-paclitaxel |

October 2018 |

March 2019 |

January 2019 | |||||

|

Stage III or IV NSCLC expressing PD-L1 ≥1% with no EGFR or ALK genomic tumor aberrations |

April 2019 |

- |

- | |||||

|

Metastatic NSCLC with high PDL1 expression with no EGFR or ALK genomic tumor aberrations |

October 2016 |

January 2017 |

- | |||||

|

Metastatic NSCLC expressing PD-L1 on or after platinum-containing chemotherapy |

October 2015 |

August 2016 |

December 2016 | |||||

|

Resectable Stage II, IIIA, or IIIB (N2) NSCLC |

October 2023 |

March 2024 |

September 2024 | |||||

|

Resected Stage IB (T2a ≥4 cm), II, or IIIA NSCLC |

January 2023 |

October 2023 |

- | |||||

|

Metastatic non-squamous NSCLC irrespective of PD-L1 expression combination with ALIMTA and carboplatin |

May 2017 | |||||||

|

OPDIVO (nivolumab) |

Bristol-Myers Squibb (BMS)/Ono Pharmaceutical |

PD-1 Inhibitor |

IV infusion |

mAb |

Resectable NSCLC |

March 2022 |

- |

- |

|

Resectable NSCLC and no known EGFR mutation or ALK rearrangement |

October 2024 |

June 2023 |

March, 2023 (supplemental approval) | |||||

|

Metastatic or recurrent NSCLC with no EGFR or ALK genomic tumor aberrations |

May 2020 |

November 2020 |

November 2020 | |||||

|

Metastatic squamous NSCLC |

March 2015 |

- |

- | |||||

|

Metastatic NSCLC with EGFR mutation or ALK translocation |

October 2015 |

- |

- | |||||

Non-Small Cell Lung Cancer (NSCLC) Pipeline Analysis

Iza-bren (izalontamab brengitecan): SystImmune and Bristol Myers Squibb

Izalontamab brengitecan is a first-in-class bispecific EGFR×HER3 antibody–drug conjugate (ADC) developed by SystImmune and Bristol Myers Squibb that simultaneously blocks EGFR/HER3 signaling and delivers a cytotoxic payload to induce cancer cell death, showing potential as a monotherapy or in combination with osimertinib for EGFR-mutant NSCLC. Phase II results in metastatic or unresectable NSCLC and other solid tumors were presented at ESMO 2025.

Daraxonrasib (RMC-6236): Revolution Medicines

Daraxonrasib (RMC-6236) is an oral, multi-selective RAS(ON) inhibitor designed to block active RAS signaling and target multiple oncogenic RAS mutations (G12X, G13X, Q61X) across cancers such as NSCLC, PDAC, and CRC. In November 2025, Revolution Medicines announced plans to initiate a registrational trial in 2026 evaluating daraxonrasib with pembrolizumab and chemotherapy as first-line treatment for metastatic RAS-mutant NSCLC.

NSCLC Competitive Landscape of Pipeline Drugs | ||||||

|

Drug Name |

Company |

Indication |

Highest Phase |

RoA |

MoA |

Anticipated Launch in the US |

|

BMS-986504 + Pembrolizumab |

BMS |

mNSCLC with homozygous MTAP deletion |

III |

Oral + IV |

PRMT5 inhibitor + PD-1 inhibitor |

Information is available in the full report |

|

Iza-bren (izalontamab brengitecan) |

SystImmune and Bristol Myers Squibb |

EFDR-mutated LA/mNSCLC |

III |

IV + Oral |

EGFR × HER3 inhibitor + EGFR TKI |

2029 (2L) |

|

Neladalkib (NVL-655) |

Nuvalent |

Advanced ALK-positive NSCLC |

III |

Oral |

ALK inhibitor |

Information is available in the full report |

|

PF-08046054 (SGN-PDL1V) |

Pfizer |

PD-L1 positive NSCLC |

III |

IV infusion |

PD-L1 inhibitor |

Information is available in the full report |

|

FF-10832 |

FUJIFILM Corporation |

Advanced NSCLC |

II |

Oral |

DNA synthesis inhibitors |

Information is available in the full report |

|

BNT116 |

BioNTech SE/Regeneron Pharmaceuticals |

NSCLC |

II |

IV |

Immunostimulants |

Information is available in the full report |

|

CAN-2409 |

Candel Therapeutics |

Advance NSCLC |

II |

Intramural |

Gene transferase |

Information is available in the full report |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | ||||||

Non-Small Cell Lung Cancer (NSCLC) Key Players, Market Leaders and Emerging Companies

- AstraZeneca

- Boehringer Ingelheim

- Pfizer

- Takeda Pharmaceuticals

- Johnson & Johnson

- Eli Lilly

- Bristol-Myers Squibb

- Merck

- AbbVie, and others

Non-Small Cell Lung Cancer (NSCLC) Drug Updates

- Nuvalent anticipates the submission of NDA or neladalkib in TKI-pretreated ALK-positive NSCLC in 1H 2026.

- Revolution Medicines plans to start a registrational trial in 2026 of daraxonrasib in 1L metastatic RAS-mutant NSCLC, combined with pembrolizumab and chemotherapy.

- The IOV-LUN-202 trial is expected to complete enrollment in 2026, supporting a supplemental BLA for lifileucel in nonsquamous NSCLC, with a potential launch in H2 2027.

- MK-1084’s KANDLELIT-004 study anticipates the data readout in Q1 2029.

Non-Small Cell Lung Cancer (NSCLC) Market Outlook

With more than 500,000 cases in the 7MM region, lung cancer is one of the leading causes of death worldwide. This condition is often diagnosed when the patient reaches the advanced, inoperable, or metastatic stage, adversely affecting their quality of life.

-Market-Insight1.png)

In April 2024, TEVIMBRA (tislelizumab) received approval in Europe across three indications in the first and second line for select patients with NSCLC. Then in July 2024 in the first-line setting, CEJEMLY (sugemalimab) plus chemotherapy received approved in Europe. Sugemalimab has not only become CStone's first independently developed product to receive overseas marketing authorization but it is also the world's first anti–PD-L1 monoclonal antibody to receive regulatory approval in Europe in combination with chemotherapy as first-line treatment for both squamous and nonsquamous NSCLC.

TROP-2-directed ADCs such as Dato-DXd, Sacituzumab Tirumotecan, and TRODELVY are being tested across various lines of therapy. In November, AstraZeneca and Daiichi pulled the US marketing application for Dato-DXd in NSCLC and instead sought the FDA’s accelerated approval for the product in EGFR-mutated NSCLC. AstraZeneca and Daiichi Sankyo are evaluating datopotamab deruxtecan alone and in novel combinations as treatment for patients with NSCLC in seven Phase III trials.

TAGRISSO is the first and only targeted therapy to demonstrate survival benefits across all stages of EGFR-mutated NSCLC. It is approved in more than 100 countries for both early-stage (adjuvant) and late-stage (metastatic) disease. Multiple landmark clinical trials, including AURA trial, FLAURA trial, ADAURA trial, LAURA trial, and FLAURA2 trial, have consistently demonstrated significant improvements in progression-free survival (PFS) and overall survival.

EXKIVITY received conditional approvals but was later withdrawn in the US, UK, and EU due to insufficient confirmatory data, leaving amivantamab as the only FDA-approved therapy for EGFR exon 20 insertions until recently.

Beyond ADCs, innovation is extending into gene therapy approaches such as Reqorsa in combination with osimertinib, as well as a new wave of next-generation TKIs like sutetinib, silevertinib (BDTX-1535), and JIN-A02, all targeting resistance pathways. The bispecific antibody pamvatamig (MCLA-129) with chemotherapy adds further diversity to the evolving treatment mix.

LUMAKRAS sales is seeing a lots of pressure on the other hand, KRAZATI is gaining ground. While LUMAKRAS was the first KRAS inhibitor approved in 2021, sales have faced pressure. Sales began to face pressure in 2023. Q3 2025 sales dipped by 2%, and previous reports indicated declines for consecutive quarters, such as a 5% dip in Q4 2022.

For patients with c-Met overexpressed NSCLC, no particular cancer treatments are currently licensed in the 7MM. Companies like AbbVie, Mythic Therapeutics, Regeneron Pharmaceuticals, and others are targeting c-met overexpressed NSCLC patients.

Despite advances in NSCLC treatment with EGFR/ALK TKIs, platinum-based combinations, and immune checkpoint inhibitors, significant unmet needs remain. Primary and acquired resistance limit durable disease control, while treatment gaps persist in molecularly driven NSCLC, including limited post-TKI options, challenges with exon 20 mutations, and restricted immunotherapy data. Additionally, late diagnosis, emerging resistance, and treatment-related toxicities continue to impact long-term survival and quality of life.

Key findings from NSCLC Market Forecast and Analysis

- The total market size of EGFR-mutated NSCLC in the US was nearly USD 3.8 billion in 2025. EGFR is one of the profitable biomarker segments, with blockbuster therapies such as TAGRISSO. TAGRISSO is now the dominant EGFR inhibitor.

- Several anti-PD-1/L1 therapies are expected to enter the NSCLC market. In 2025, the highest revenue was captured by KEYTRUDA. Merck’s KEYTRUDA is generally considered the ‘gold standard’ of care in first-line NSCLC when combined with platinum chemotherapy, regardless of PD-L1 status.

- The total market size of ALK-mutated NSCLC in the US was nearly USD 1.28 billion in 2025. In the adjuvant setting, ALECENSA has become the first approved ALK inhibitor following surgical resection, expanding treatment duration and increasing the addressable early-stage population. In the 1L metastatic setting, next-generation ALK inhibitors including ALECENSA, LORBRENA/LORVIQUA, and ZYKADIA, ALUNBRIG dominate the standard of care due to superior progression-free survival and robust intracranial activity, which is critical given the high incidence of brain metastases in ALK-positive patients.

Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in NSCLC (2022–2036 Forecast)

The NSCLC market comprises monoclonal antibodies, small molecules, bispecific antibodies, and others, each targeting different aspects of tumor growth and progression.

Monoclonal antibody: Nivolumab (OPDIVO) is a human IgG4 monoclonal antibody that targets the PD-1 immune checkpoint receptor, enhancing T-cell–mediated antitumor activity. Pembrolizumab (KEYTRUDA) is a PD-1–blocking antibody used across multiple cancers, particularly advanced or PD-L1–positive tumors, and may also be used after surgery to reduce recurrence risk. Cemiplimab (LIBTAYO) is a fully human anti-PD-1 monoclonal antibody indicated for NSCLC, including use with platinum-based chemotherapy as first-line therapy in certain patients. Tislelizumab (TEVIMBRA) is a humanized IgG4 anti-PD-1 monoclonal antibody engineered to reduce Fc? receptor binding on macrophages, helping enhance immune recognition and destruction of tumors.

Small molecule: Dacomitinib is a small-molecule EGFR tyrosine kinase inhibitor used as first-line therapy for metastatic NSCLC with EGFR exon 19 deletion or exon 21 L858R mutations, blocking EGFR signaling to slow tumor growth. Afatinib maleate, developed by Boehringer Ingelheim, is an irreversible ErbB family TKI that inhibits EGFR, HER2, and HER4, suppressing downstream cancer signaling. Osimertinib is a third-generation, irreversible EGFR TKI used for EGFR-mutant NSCLC both as adjuvant therapy after tumor resection and as first-line treatment. Sunvozertinib is an oral irreversible kinase inhibitor indicated for locally advanced or metastatic NSCLC with EGFR exon 20 insertion mutations after progression on platinum-based chemotherapy.

Non-Small Cell Lung Cancer (NSCLC) Drug Uptake

This section focuses on the uptake rate of potential drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the NSCLC drug’s uptake, performance at peak, factors affecting performance during prime years of growth, patient uptake by therapy, and anticipated sales generated by each drug.

Among the emerging first-line therapies are Zipalertinib (TAS6417) + CTx; Furmonertinib/Firmonertinib; Pamvatamig (MCLA-129) ± Osimertinib; Aumolertinib (AUMSEQA); Sunvozertinib (ZEGFROVY); Datopotamab deruxtecan (DATROWAY) ± Osimertinib (TAGRISSO); Telisotuzumab adizutecan (Temab-A) + TAGRISSO; Sutetinib; JMT101 + Osimertinib; and other investigational approaches, Firmonertinib, sunvozertinib, and JMT101 in combination with osimertinib are anticipated to be among the first to enter the market by 2027 and are expected to compete closely with established therapies such as RYBREVANT and TAGRISSO.

Detailed insights of emerging therapies' drug uptake is included in the report

Market Access and Reimbursement of Approved therapies in Non-Small Cell Lung Cancer (NSCLC)

The Non-Small Cell Lung Cancer market report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of approved therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

US Reimbursement of Therapies Approved for NSCLC | |

|

Drug/Therapy |

Access Program |

|

TAGRISSO |

|

|

RYBREVANT |

|

|

OPDIVO |

|

|

KEYTRUDA |

|

Reimbursement is a crucial factor that affects the drug’s access to the market. Often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

NSCLC therapies Price Scenario & Trends

Pricing and analogue assessment of NSCLC therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, closest and most appropriate analogue selection for emerging therapies, and understanding of how pricing influences market access, adherence, and long-term uptake.

Pricing of NSCLC Approved Drugs

EXKIVITY dosing is 160mg (four 40mg capsules) taken by mouth once daily until disease progression or unacceptable toxicity occur. Capsules should be swallowed whole. Based on this, the estimated annual treatment cost is approximately USD 182,500.

Industry Experts and Physician Views for Non-Small Cell Lung Cancer (NSCLC)

To keep up with NSCLC market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry Experts were contacted for insights on the NSCLC emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in NSCLC, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 10+ KOLs to gather insights at country level. Centers such as the University of Southern California, Ohio State University, Norris Comprehensive Cancer Center, Paris-Saclay University, and Germans Trias i Pujol Research Institute, etc. were contacted.Their opinion helps understand and validate current and emerging NSCLC therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in NSCLC.

What are the KOL Views on Non-Small Cell Lung Cancer Market? | |

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“In the ALK space, biomarker testing beyond identifying the ALK mutation currently does not influence drug indications. However, its clinical relevance is expected to grow, particularly as more patients receive multiple ALK inhibitors and develop compound resistance mutations. In the future, identifying resistance mutations in the second-line and later settings may help guide treatment selection.” |

|

Italy |

“The heterogeneity of uncommon mutations and their differential sensitivity to EGFR TKIs such as GIOTRIF underscores the need for precise detection and detailed reporting of these mutations in real-world practice, especially for complex alterations such as Exon 20 insertions.” |

Non-Small Cell Lung Cancer Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of NSCLC, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are majorly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Non-Small Cell Lung Cancer Market Report

- The Non-Small Cell Lung Cancer Market report covers a segment of key events, an executive summary, a descriptive overview of NSCLC, explaining their causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the NSCLC market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The Non-Small Cell Lung Cancer Market report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM NSCLC market.

Non-Small Cell Lung Cancer Market Report Insights

- Non-Small Cell Lung Cancer (NSCLC) Patient Population Forecast

- Non-Small Cell Lung Cancer (NSCLC) Therapeutics Market Size

- Non-Small Cell Lung Cancer (NSCLC) Pipeline Analysis

- Non-Small Cell Lung Cancer (NSCLC) Market Size and Trends

Non-Small Cell Lung Cancer Market Report Key Strengths

- Epidemiology-based (Epi-based) Bottom-up Forecasting

- Artificial Intelligence (AI)-enabled Market Research Report

- 11-year Forecast

- Non-Small Cell Lung Cancer (NSCLC) Market Outlook (North America, Europe, Asia-Pacific)

- Patient Burden Trends (by geography)

- Non-Small Cell Lung Cancer (NSCLC) Treatment Addressable Market (TAM)

- Non-Small Cell Lung Cancer (NSCLC) Competitve Landscape

- Non-Small Cell Lung Cancer (NSCLC) Major Companies Insights

- Non-Small Cell Lung Cancer (NSCLC) Price Trends and Analogue Assessment

- Non-Small Cell Lung Cancer (NSCLC) Therapies and Drug Adoption/Uptake

- Non-Small Cell Lung Cancer (NSCLC) therapies Peak Patient Share Analysis

Non-Small Cell Lung Cancer Market Report Assessment

- Non-Small Cell Lung Cancer (NSCLC) Current Treatment Practices

- Non-Small Cell Lung Cancer (NSCLC) Unmet Needs

- Non-Small Cell Lung Cancer (NSCLC) Clinical Development Analysis

- Non-Small Cell Lung Cancer (NSCLC) Emerging Drugs Product Profiles

- Non-Small Cell Lung Cancer (NSCLC) Market Attractiveness

- Non-Small Cell Lung Cancer (NSCLC) Qualitative Analysis (SWOT and Conjoint Analysis)

Frequently Asked Questions from Non-Small Cell Lung Cancer Market Report

Non-Small Cell Lung Cancer Market Insights

- What was the NSCLC market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of NSCLC?

- What are the disease risks, burdens, and unmet needs of NSCLC? What will be the growth opportunities across the 7MM concerning the patient population with NSCLC?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of NSCLC? What are the current guidelines for treating NSCLC in the US, Europe, and Japan?

Reasons to Buy the Non-Small Cell Lung Cancer Market Report

- The Non-Small Cell Lung Cancer Market report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the NSCLC market.

- Bottom up forecasting builds from the affected population to product forecasts, delivering a robust, data driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing Non-Small Cell Lung Cancer Market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming Non-Small Cell Lung Cancer companies in the Non-Small Cell Lung Cancer companies will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the unmet needs of the existing Non-Small Cell Lung Cancer Market so that the upcoming Non-Small Cell Lung Cancer companies can strengthen their development and launch strategy.

- This Artificial Intelligence (AI) enabled report summarize and simplify complex datasets withing the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data driven decisions.