Automated Organoid Culturing Market Summary

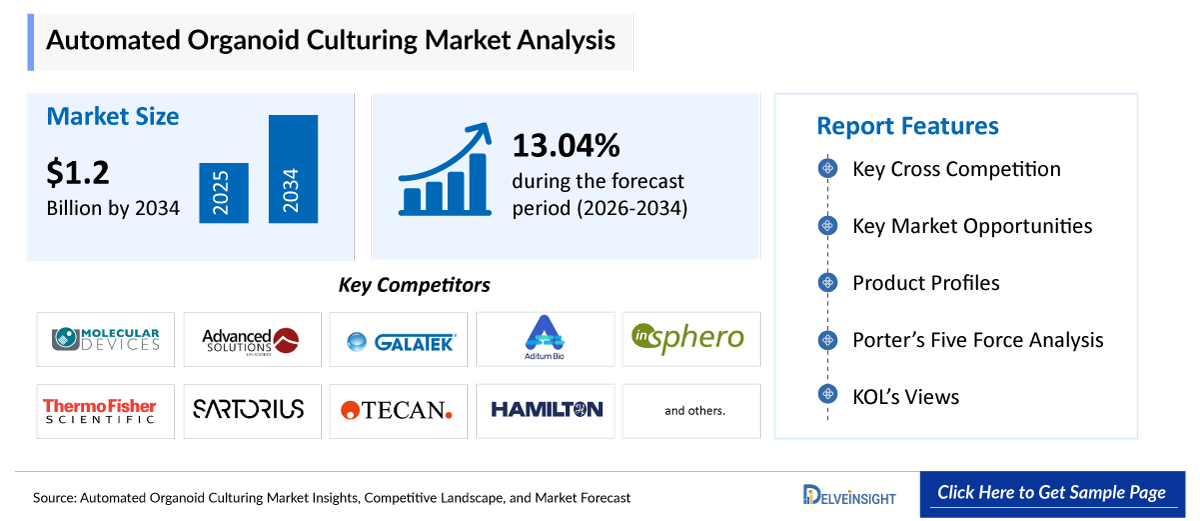

- The global automated organoid culturing market is expected to increase from USD 420.98 million in 2025 to USD 1,257.72 million by 2034, reflecting strong and sustained growth.

- The global automated organoid culturing market is growing at a CAGR of 13.04% during the forecast period from 2026 to 2034.

- The market for Automated Organoid Culturing is being strongly driven by the convergence of three key factors that are transforming biomedical research and drug development. First, the rising demand for advanced 3D cell culture models is pushing researchers away from conventional 2D systems, as organoids more accurately replicate human tissue architecture and physiological responses, making them highly valuable for predictive studies in drug discovery and disease modeling. Second, the increasing adoption of personalized medicine is accelerating demand for patient-derived organoids, which allow clinicians and researchers to test drug responses on individualized biological models, improving treatment precision, especially in oncology and rare diseases. Third, technological advancements in automation and artificial intelligence are enabling scalable, reproducible, and high-throughput organoid production by integrating robotics, AI-based imaging, and data analytics, significantly reducing manual variability and operational costs. Collectively, these factors are transforming organoid research from a manual, low-throughput laboratory process into a standardized, industrial-scale platform, thereby significantly boosting the growth of the automated organoid culturing market.

- The leading companies operating in the automated organoid culturing market include Molecular Devices LLC, Advanced Solutions Life Sciences LLC, Galatek, Addimus Bio, InSphero AG, Thermo Fisher Scientific Inc., Sartorius AG, Tecan Group Ltd., Hamilton Company, Revvity Inc., Danaher Corporation, Corning Incorporated, STEMCELL Technologies Inc., Greiner Bio-One International GmbH, Eppendorf SE, Beckman Coulter Life Sciences (Danaher Corporation), Yokogawa Electric Corporation, Curi Bio Inc., Emulate Inc., CN Bio Innovations Ltd., Mimetas B.V., TissUse GmbH, and others.

- North America is expected to dominate the automated organoid culturing market due to its strong biotechnology and pharmaceutical ecosystem, high adoption of advanced laboratory automation, and significant R&D investments in drug discovery and regenerative medicine. The region is home to leading research institutions, well-established biopharma companies, and a high concentration of technology providers developing automated cell culture and organoid platforms. Additionally, supportive government funding, early adoption of AI-driven lab workflows, and increasing demand for high-throughput, reproducible in-vitro models further strengthen market growth in the region.

- In the product and services segment of the automated organoid culturing market, the consumables category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Automated Organoid Culturing Market

Automated Organoid Culturing Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 420.98 million |

|

2034 Projected Market Size |

USD 1,257.72 million |

|

Growth Rate (2026-2034) |

13.04% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Automated Organoid Culturing Market

Rising demand for advanced 3D cell culture models is leading to a surge in automated organoid culturing:

Traditional 2D cell cultures fail to replicate real human physiology, which creates a strong need for more predictive models. Organoids, being 3D structures that closely mimic human organ architecture and function, are highly valuable in drug discovery and disease research. Automation further enhances their usability by enabling standardized and scalable production, which is critical for industrial applications.

Increasing adoption in personalized medicine:

Automated organoid culturing is playing a pivotal role in Personalized Medicine, particularly through patient-derived organoids. These models allow researchers to test multiple therapies on an individual patient’s cells before clinical treatment. Automation ensures rapid turnaround time, consistency, and the ability to handle multiple patient samples simultaneously, driving strong adoption in oncology and rare disease treatment.

Technological Advancements in Automation and AI:

Technological advancements in automation and AI are significantly boosting the automated organoid culturing market by improving efficiency, scalability, and reproducibility of complex biological experiments. Automated liquid handling systems, robotic culture platforms, and AI-driven imaging and data analytics enable precise control of organoid growth conditions while reducing manual errors and variability. AI algorithms further help in real-time monitoring, pattern recognition, and predictive modeling of organoid development, accelerating drug screening and disease modeling processes. Together, automation and AI are transforming organoid research into a high-throughput, standardized, and more cost-effective workflow, driving broader adoption across pharmaceutical and biotechnology companies.

Automated Organoid Culturing Market Report Segmentation

This automated organoid culturing market report offers a comprehensive overview of the global automated organoid culturing market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product and Services (Instruments, Consumables, and Services), Organoids (Pancreas, Intestine, Liver, Lung, Neural, and Others), Application (Disease Pathology, Regenerative Medicine, Drug Testing, Drug Discovery And Personalized Medicine, and Others), End-Users (Pharmaceutical & Biotechnology Companies, Contract Research Organizations (CROs), and Others), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing Automated Organoid Culturing market.

Automated organoid culturing refers to the use of advanced robotic systems, laboratory automation platforms, and digital technologies to grow, maintain, and analyze organoids, three-dimensional miniaturized tissue models derived from stem cells. In this process, steps such as cell seeding, media exchange, incubation control, monitoring, and imaging are performed with minimal human intervention, ensuring higher precision, reproducibility, and scalability compared to manual methods. By integrating automation with software-driven controls and sometimes AI-based analytics, automated organoid culturing enables consistent production of complex biological models used in drug discovery, disease modeling, and personalized medicine research.

The market for automated organoid culturing is being strongly driven by the convergence of three major factors that are reshaping modern biomedical research and drug development. Firstly, the growing demand for advanced 3D cell culture models is shifting research practices away from traditional 2D cell systems. Organoids are able to replicate key aspects of human tissue architecture, cellular diversity, and physiological function more accurately, making them far more predictive for preclinical drug testing, toxicity studies, and disease modeling. This improved biological relevance is increasing their adoption across pharmaceutical and academic research settings.

Secondly, the rise of personalized medicine is significantly accelerating the use of patient-derived organoids. These models are created from individual patients’ cells and allow researchers and clinicians to evaluate how specific drugs will respond in a patient-specific biological environment. This is particularly valuable in oncology, rare genetic disorders, and precision therapeutics, where treatment outcomes vary widely among individuals. As healthcare moves toward more targeted and personalized treatment strategies, demand for such individualized organoid models is expanding rapidly.

Thirdly, rapid advancements in automation and artificial intelligence are transforming organoid culturing into a scalable and standardized process. Automated systems such as robotic liquid handlers, incubators, and microfluidic platforms reduce manual intervention, while AI-powered imaging and analytics enable real-time monitoring, quality control, and predictive assessment of organoid growth and behavior. These technologies not only enhance reproducibility and reduce human error but also significantly improve throughput and reduce operational costs. Collectively, these three drivers are converting organoid research from a labor-intensive, low-throughput laboratory technique into a highly efficient, industrial-scale platform, thereby strongly propelling the growth of the automated organoid culturing market.

Get More Insights into the Report @Automated Organoid Culturing Market

What are the latest automated organoid culturing market dynamics and trends?

The rising demand for advanced 3D cell culture models is significantly accelerating the growth of the automated organoid culturing market because researchers are increasingly replacing traditional 2D cell cultures with organoids that better mimic the structural, functional, and biological complexity of human tissues. These 3D systems provide more physiologically relevant results for disease modeling, toxicity testing, and drug screening, which have made them highly valuable in pharmaceutical and biomedical research. However, manual organoid cultivation is labor-intensive, time-consuming, and prone to variability, which limits scalability. This challenge is driving strong adoption of automated platforms that can standardize culture conditions, improve reproducibility, and enable high-throughput production of organoids.

Recent technological developments further reinforce this trend. For example, in December 2025, the CellXpress.ai automated cell culture system at Emory University’s Brain Organoid Hub was installed. The system was designed to automate complex and repetitive steps such as cell feeding, incubation, imaging, and data analysis, allowing organoids to be cultured continuously for weeks or even months with minimal human intervention. It was also highlighted that the platform could culture thousands of organoids simultaneously while using AI-based imaging to track cell growth and differentiation patterns, improving consistency and reproducibility in experiments.

Additionally, the increasing adoption of personalized medicine is significantly boosting the automated organoid culturing market because it shifts healthcare from a “one-size-fits-all” approach to highly individualized treatment strategies. In this approach, patient-derived organoids (PDOs) are grown from a specific patient’s cells to create miniature models of their organs or tumors, which closely replicate their unique genetic and biological characteristics. These organoids allow researchers to test multiple drugs directly on a patient-specific model, helping predict treatment response, identify the most effective therapy, and reduce trial-and-error in clinical decision-making. As a result, demand for scalable and reproducible organoid production is rising, driving adoption of automated culturing systems that can handle high-throughput generation, reduce variability, and integrate AI-based analysis for faster therapeutic insights. Recent developments further highlight this trend. For instance, in November 2025, clinical researchers reported expanding use of organoid-based platforms in oncology to guide chemotherapy and immunotherapy selection, improving personalized cancer treatment outcomes through patient-specific tumor modelling. Thus, the factors mentioned above are expected to boost the overall market of automated organoid culturing during the forecast period.

However, the high initial setup costs, data management, and AI dependency issues are acting as key limiting factors for the automated organoid culturing market. The requirement for advanced automation platforms, robotics, imaging systems, and AI-integrated software leads to substantial upfront investment, making it difficult for smaller research institutes and laboratories to adopt these technologies. Additionally, automated systems generate large volumes of complex biological and imaging data that require robust storage infrastructure, high computational power, and sophisticated AI models for analysis. Any limitations in data processing accuracy or AI interpretation can affect experimental outcomes and reproducibility. Together, these factors increase operational complexity and cost burdens, thereby restraining the broader adoption of automated organoid culturing systems.

Automated Organoid Culturing Market Segment Analysis

Automated Organoid Culturing Market by Product and Services (Instruments, Consumables, and Services), Organoids (Pancreas, Intestine, Liver, Lung, Neural, and Others), Application (Disease Pathology, Regenerative Medicine, Drug Testing, Drug Discovery And Personalized Medicine, and Others), End-Users (Pharmaceutical & Biotechnology Companies, Contract Research Organizations (CROs), and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product and Services: Consumables under the segment product and services are expected to dominate the market with the largest revenue share.

In the product and services segment of the automated organoid culturing market, the consumables category is contributing to 53% of total market revenue in 2025, because it represents the most recurring and essential component of the workflow. Consumables such as culture media, extracellular matrices (ECM), growth factors, reagents, hydrogels, and specialized plates are required at every stage of organoid development, maintenance, and experimental analysis. Since organoids need continuous replenishment of these materials for long-term 3D culture, consumables generate repeat demand, making them a major revenue driver compared to one-time instrument purchases. Additionally, increasing demand for standardized and chemically defined media and ECM systems is improving reproducibility in organoid experiments, further accelerating adoption across pharmaceutical and biotechnology companies.

Additionally, the consumables segment is witnessing strong innovation activity from leading life science companies, as they focus on improving reproducibility, scalability, and standardization of 3D organoid workflows. In February 2026, Bio-Techne launched the Cultrex™ Synthetic Hydrogel, a fully defined extracellular matrix (ECM) designed specifically for 3D stem cell and organoid cultures. This development aimed to reduce lot-to-lot variability and improve consistency in automated organoid production workflows, directly strengthening demand for high-quality consumables in research and translational applications. Similarly, in April 2026, TheWell Bioscience introduced a Universal Xeno-Free Organoid Medium, designed to standardize organoid culture conditions and reduce cost and variability in long-term 3D cell culture experiments.

Furthermore, the expansion of high-throughput organoid platforms integrating consumables with automated systems has strengthened demand for specialized reagents and microplates designed for automation compatibility, reinforcing the consumables segment as a key growth engine in the automated organoid culturing market.

By Organoids: Intestine category dominates the market

Within the organoids segment of the automated organoid culturing market, the intestine category is anticipated to dominate, accounting for around 33% of the market share in 2025, primarily due to its superior physiological relevance and broad translational utility. Intestinal organoids closely replicate the native architecture and functional complexity of the human gut, including epithelial diversity, stem cell regeneration, nutrient absorption, and host microbiome interactions. This makes them highly valuable for drug absorption studies, gastrointestinal disease modeling (such as Crohn’s disease, ulcerative colitis, and colorectal cancer), infectious disease research, and toxicology screening. Compared to other organoid types (such as liver, brain, pancreas, or lung), intestinal organoids are more widely adopted in high-throughput automated platforms, as they are relatively more stable in long-term culture and show strong reproducibility in standardized workflows. In automated systems, they also benefit significantly from advances in microfluidics, robotic liquid handling, and scalable 3D culture systems, which reduce manual variability and increase experimental throughput, further reinforcing their dominance in this segment. Industry analyses also indicate that intestinal organoids hold the largest share among organoid types (around one-fourth of total organoid revenues in 2024), driven by their extensive use in pharmaceutical R&D and precision medicine applications.

From a competitive and innovation standpoint, key players are actively advancing intestinal organoid technologies to strengthen their position in automated culture systems. For instance, in August 2025, for the first time in medical history, researchers from Sheba Medical Center and Tel Aviv University successfully grew a human kidney organoid, a synthetic 3D organ culture, from tissue-specific stem cells that mirror natural fetal kidney development. This breakthrough offers new hope for advances in regenerative medicine, birth defect research, and drug toxicity testing during pregnancy.

Overall, the dominance of intestinal organoids is being reinforced by a combination of biological relevance, automation readiness, strong pharmaceutical demand, and continuous commercial investments, positioning them as the most commercially scalable and widely adopted organoid type within the automated organoid culturing market.

By Application: Drug discovery and personalized medicine categories dominate the market.

Within the application segment of the automated organoid culturing market, the drug discovery and personalized medicine category is anticipated to dominate, accounting for around 49% of the market share in 2025, due to its strong integration into pharmaceutical pipelines and growing reliance on human-relevant 3D disease models. Automated organoid systems are increasingly being used across target identification, high-throughput drug screening, toxicity assessment, and efficacy validation, offering superior physiological relevance compared to conventional 2D cell cultures and animal models. This has significantly improved predictive accuracy in preclinical studies and reduced late-stage clinical failure rates, making organoid-based platforms a critical tool for pharmaceutical and biotech companies. In parallel, the rise of personalized medicine—especially in oncology—has accelerated adoption, as patient-derived organoids enable real-time testing of drug response tailored to individual genetic and tumor profiles, strengthening precision therapy selection and biomarker-driven treatment strategies. The segment’s dominance is further reinforced by regulatory and industry momentum supporting New Approach Methodologies (NAMs), including reduced reliance on animal testing and increased acceptance of advanced in vitro systems in drug development workflows.

Recent developments also highlight this trend. In December 2024, Merck KGaA completed the acquisition of HUB Organoids Holding B.V., strengthening its capabilities in organoid-based drug discovery and early efficacy testing platforms. In November 2025, InSphero expanded its 3D organoid ecosystem by acquiring DOPPL SA and Sun Bioscience’s Gri3D® technology, enhancing scalable, automated organoid models for high-throughput screening and translational drug research. More recently, in April 2026, InSphero launched its 3D InSight™ DIGIT platform, integrating patient-derived intestinal organoids with automated imaging for early gastrointestinal toxicity assessment in drug discovery workflows. Collectively, these developments underscore how pharmaceutical investments, automation technologies, and precision medicine applications are converging to make drug discovery and personalized medicine the leading and most revenue-generating application area in the automated organoid culturing market.

By End-Users: Pharmaceutical & biotechnology companies dominate the market

In the end-user segment of the automated organoid culturing market, pharmaceutical and biotechnology companies dominate the market due to their extensive use of organoid platforms in drug discovery, preclinical screening, toxicity testing, and precision medicine development. These companies are the primary drivers of innovation and investment in automated organoid technologies, as organoids provide more physiologically relevant models that improve drug efficacy prediction and reduce late-stage clinical trial failures. The increasing focus on high-throughput screening, personalized medicine, and cost-efficient R&D pipelines has further accelerated adoption. Additionally, large-scale collaborations between pharma firms and biotech innovators, along with integration of automation and AI-driven analytics, are strengthening the reliance of this segment on organoid culturing systems, making it the leading end-user category in the market.

Automated Organoid Culturing Market Regional Analysis

North America Automated Organoid Culturing Market Trends

North America is expected to account for the highest proportion of 41% of the automated organoid culturing market in 2025, out of all regions. North America is expected to dominate the automated organoid culturing market due to its highly advanced biomedical research ecosystem, strong presence of leading life sciences companies, and rapid adoption of cutting-edge technologies such as robotics-enabled 3D cell culture systems, microfluidics, and AI-driven automated platforms. The region benefits from substantial R&D investments by pharmaceutical and biotechnology companies, extensive government and private funding for regenerative medicine and precision medicine research, and a dense network of academic–industry collaborations that accelerate translation of organoid-based models into drug discovery and toxicology testing workflows.

Additionally, North America leads in early adoption of high-throughput automated organoid production systems, integration of 3D imaging with organoid assays, and increasing use of patient-derived organoids for personalized medicine applications, which further strengthens its market dominance.

Recent developments by North America-based and globally active key players further reinforce this leadership position. In February 2024, Cell Microsystems (U.S.) partnered with OMNI Life Science to introduce advanced cellular analysis solutions such as CERO, CASY, and TIGR across the U.S. and Canada, strengthening automated organoid and cell culture analytics capabilities. In January 2025, Merck acquired HUB Organoids Holding B.V., expanding its organoid technology portfolio and enhancing automated organoid-based drug development workflows. Additionally, collaborations such as those involving distribution and automation partners in North America have expanded access to robotics-enabled 3D cell culture platforms, supporting broader adoption in pharmaceutical research.

Overall, the dominance of North America is driven by the convergence of strong R&D funding, high concentration of leading biotech and life science companies, rapid technological integration (automation, AI, microfluidics), and continuous innovation through mergers, acquisitions, and product launches that collectively accelerate the adoption of automated organoid culturing systems across drug discovery, disease modeling, and personalized medicine.

Europe Automated Organoid Culturing Market Trend

The automated organoid culturing market in Europe is witnessing strong and sustained growth, driven by rapid advancements in 3D cell culture technologies, increasing adoption of organoid-based models in drug discovery and toxicology testing, and rising demand for physiologically relevant human disease models in precision medicine and regenerative medicine research. Europe benefits from a highly collaborative research environment supported by leading academic institutions, biotech startups, and established life science companies, alongside strong government funding initiatives aimed at reducing animal testing and accelerating advanced therapy development. The region is also experiencing increasing integration of automation, AI-driven image analysis, and microfluidics-based organoid platforms, which are significantly improving reproducibility, scalability, and throughput in organoid production workflows. As a result, Europe remains one of the most important hubs for organoid innovation, accounting for a substantial share of the global market and expected to grow at a high double-digit CAGR over the forecast period.

Recent development activities by key market players further highlight this growth trajectory. In March 2024, CHA Biotech entered into a collaboration with Cell in Cells to develop organoid-based regenerative therapies for cartilage diseases, reflecting Europe’s increasing focus on clinical translation of organoid research. In addition, expanded its organoid and 3D cell culture commercialization efforts through distribution partnerships aimed at improving access to automated spheroid and organoid platforms across research laboratories. These developments are complemented by continuous innovation from European-based companies, which are advancing organ-on-chip systems and standardized organoid culture media to support automation and high-throughput screening applications.

Collectively, these strategic expansions, acquisitions, and collaborations are accelerating the adoption of automated organoid culturing technologies across Europe, reinforcing its position as a high-growth regional market driven by innovation, translational research, and strong regulatory support for alternative testing models.

Asia-Pacific Automated Organoid Culturing Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the automated organoid culturing market due to increasing investments in biotechnology research, rapid expansion of pharmaceutical manufacturing capabilities, and growing adoption of advanced 3D cell culture technologies across countries such as China, Japan, South Korea, and India. The region is witnessing strong government support for regenerative medicine, precision medicine, and drug discovery innovation, along with rising collaborations between academic institutions and biotech companies that are accelerating organoid-based research. Additionally, the increasing prevalence of chronic diseases and cancer is driving demand for more predictive and human-relevant preclinical models, boosting the adoption of automated organoid systems. The presence of expanding contract research organizations (CROs), cost-effective R&D infrastructure, and growing focus on AI-integrated laboratory automation further strengthens APAC’s position as a high-growth region in this market.

Who are the major players in the automated organoid culturing market?

The following are the leading companies in the automated organoid culturing market. These companies collectively hold the largest market share and dictate industry trends.

- Molecular Devices LLC

- Advanced Solutions Life Sciences LLC

- Galatek

- Addimus Bio

- InSphero AG

- Thermo Fisher Scientific Inc.

- Sartorius AG

- Tecan Group Ltd.

- Hamilton Company

- Revvity Inc.

- Danaher Corporation

- Corning Incorporated

- STEMCELL Technologies Inc.

- Greiner Bio-One International GmbH

- Eppendorf SE

- Beckman Coulter Life Sciences (Danaher Corporation)

- Yokogawa Electric Corporation

- Curi Bio Inc.

- Emulate Inc.

- CN Bio Innovations Ltd.

- Mimetas B.V.

- TissUse GmbH

- Others

How is the competitive landscape shaping the automated organoid culturing market?

The competitive landscape of the automated organoid culturing market is moderately consolidated and increasingly innovation-driven, where a small group of global life science giants and specialized biotech firms collectively shape market direction. Large players such as Thermo Fisher Scientific, Corning Incorporated, Sartorius AG, and Merck KGaA dominate due to their strong portfolios in cell culture media, bioreactors, scaffolds, and laboratory automation systems that directly support scalable organoid production. These companies benefit from deep R&D capabilities, global distribution networks, and established relationships with pharmaceutical and biotech customers, allowing them to integrate organoid workflows into drug discovery and translational research pipelines at scale.

Alongside these incumbents, highly specialized organoid-focused firms such as InSphero AG, HUB Organoids, Emulate, and STEMCELL Technologies are strengthening their positions by offering disease-specific organoid models, patient-derived systems, and advanced 3D culture platforms tailored for precision medicine and toxicity testing. These niche players compete primarily through technological differentiation, such as organ-on-chip integration, automation compatibility, and improved biological fidelity rather than scale alone.

At the same time, startups and emerging biotech companies are intensifying competition by introducing cost-effective automated platforms, microfluidic systems, and AI-integrated culturing workflows, which are challenging traditional manual and semi-automated systems. The market is also seeing growing involvement from contract research organizations (CROs) and CDMOs, which are helping pharmaceutical companies scale organoid use in drug discovery, further expanding the ecosystem and increasing competitive density. Overall, the competitive landscape is being shaped by a clear shift toward automation, standardization, and scalability, with mergers, acquisitions, and strategic collaborations becoming key strategies for companies to expand technology portfolios and strengthen their positions in the rapidly evolving organoid cultivation ecosystem.

Recent Developmental Activities in the Automated Organoid Culturing Market

- In April 2026, TheWell Bioscience introduced a Universal Xeno-Free Organoid Medium, designed to standardize organoid culture conditions and reduce cost and variability in long-term 3D cell culture experiments.

- In February 2026, Bio-Techne launched the Cultrex™ Synthetic Hydrogel, a fully defined extracellular matrix (ECM) designed specifically for 3D stem cell and organoid cultures.

- In December 2025, the CellXpress.ai automated cell culture system at Emory University’s Brain Organoid Hub was installed. The system was designed to automate complex and repetitive steps such as cell feeding, incubation, imaging, and data analysis, allowing organoids to be cultured continuously for weeks or even months with minimal human intervention. It was also highlighted that the platform could culture thousands of organoids simultaneously while using AI-based imaging to track cell growth and differentiation patterns, improving consistency and reproducibility in experiments.

- In August 2025, for the first time in medical history, researchers from Sheba Medical Center and Tel Aviv University successfully grew a human kidney organoid, a synthetic 3D organ culture, from tissue-specific stem cells that mirrors natural fetal kidney development. This breakthrough offers new hope for advances in regenerative medicine, birth defect research, and drug toxicity testing during pregnancy.

- In December 2024, Merck completed the acquisition of HUB Organoids Holding B.V., a major organoid technology company, to expand its organoid-based drug discovery and disease modeling capabilities, including intestinal models used in translational research.

- In March 2024, CHA Biotech signed a CDMO agreement to develop organoid-based regenerative therapies, reinforcing the growing commercial pipeline for organoid systems, including intestinal models used in disease simulation and therapeutic research.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Automated Organoid Culturing Market CAGR |

13.04% |

|

Key Companies in the Automated Organoid Culturing Market |

Molecular Devices LLC, Advanced Solutions Life Sciences LLC, Galatek, Addimus Bio, InSphero AG, Thermo Fisher Scientific Inc., Sartorius AG, Tecan Group Ltd., Hamilton Company, Revvity Inc., Danaher Corporation, Corning Incorporated, STEMCELL Technologies Inc., Greiner Bio-One International GmbH, Eppendorf SE, Beckman Coulter Life Sciences (Danaher Corporation), Yokogawa Electric Corporation, Curi Bio Inc., Emulate Inc., CN Bio Innovations Ltd., Mimetas B.V., TissUse GmbH, and others. |

|

Automated Organoid Culturing Market Segments |

by Product and Services, by Organoid, by Application, by End-Users, and by Geography |

|

Automated Organoid Culturing Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Automated Organoid Culturing Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Automated Organoid Culturing Market Segmentation

-

Automated Organoid Culturing by Product and Services Exposure

-

Instruments

-

Consumables

-

Services

-

Automated Organoid Culturing Organoid Exposure

-

Pancreas

-

Intestine

-

Liver

-

Lung

-

Neural

-

Others

-

Automated Organoid Culturing Application Exposure

-

Disease Pathology

-

Regenerative Medicine

-

Drug Testing

-

Drug Discovery and Personalized Medicine

-

Others

-

Automated Organoid Culturing End-Users Exposure

-

Pharmaceutical & Biotechnology Companies

-

Contract Research Organizations (CROs)

-

Others

-

Automated Organoid Culturing Geography Exposure

-

North America Automated Organoid Culturing Market

-

United States Automated Organoid Culturing Market

-

Canada Automated Organoid Culturing Market

-

Mexico Automated Organoid Culturing Market

-

Europe Automated Organoid Culturing Market

-

United Kingdom Automated Organoid Culturing Market

-

Germany Automated Organoid Culturing Market

-

France Automated Organoid Culturing Market

-

Italy Automated Organoid Culturing Market

-

Spain Automated Organoid Culturing Market

-

Rest of Europe Automated Organoid Culturing Market

-

Asia-Pacific Automated Organoid Culturing Market

-

China Automated Organoid Culturing Market

-

Japan Automated Organoid Culturing Market

-

India Automated Organoid Culturing Market

-

Australia Automated Organoid Culturing Market

-

South Korea Automated Organoid Culturing Market

-

Rest of Asia-Pacific Automated Organoid Culturing Market

-

Rest of the World Automated Organoid Culturing Market

-

South America Automated Organoid Culturing Market

-

Middle East Automated Organoid Culturing Market

-

Africa Automated Organoid Culturing Market

Automated Organoid Culturing Market Recent Industry Trends and Milestones (2023-2026)

|

Category |

Key Developments |

|

Automated Organoid Culturing Product Launch |

Bio-Techne launched the Cultrex™ Synthetic Hydrogel, a fully defined extracellular matrix (ECM) designed specifically for 3D stem cell and organoid cultures. The CellXpress.ai automated cell culture system at Emory University’s Brain Organoid Hub was installed. |

|

Automated Organoid Culturing Product Acquisition |

Merck KGaA completed the acquisition of HUB Organoids Holding B.V |

|

Company Strategy |

Corning Incorporated

Merck KGaA

|

|

Emerging Technology |

AI-Driven Organoid Monitoring and Analysis, Organoid-on-a-Chip (Microfluidic Platforms), 3D Bioprinting of Organoids, Robotics and Full Automation Platforms, Advanced Biomaterials and Synthetic Hydrogels, and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations in automated organoid culturing are transforming the field by enabling fully autonomous experimental workflows, predictive modeling, and high-resolution biological decision-making. Machine learning and deep learning systems are now being integrated into automated cell culture platforms to control processes such as organoid seeding, feeding, passaging, and maturation in real time, while continuously analyzing imaging data to adjust experimental conditions dynamically. These AI systems can perform automated image segmentation, morphological profiling, and viability assessment, allowing researchers to classify organoid growth patterns and drug responses with high accuracy and minimal human intervention. AI is also being used for predictive drug screening and toxicity evaluation, where trained models analyze large-scale organoid datasets to forecast how specific compounds will behave in human-like tissues, significantly improving the efficiency of drug discovery pipelines.

Additionally, emerging AI-driven “closed-loop” systems combine robotics, imaging, and feedback algorithms, where organoid growth outcomes directly influence the next experimental step, making cultures more standardized and reproducible. More advanced concepts, such as digital twin or “virtual organoids,” are also emerging, where computational models simulate organoid development and guide physical experiments, reducing cost and experimental time. Overall, AI is shifting automated organoid culturing from a manual laboratory technique into a self-optimizing, data-driven biological engineering platform that accelerates disease modeling, personalized medicine, and high-throughput drug development.

U.S. Tariff Impact Analysis on Automated Organoid Culturing Market:

The U.S. tariff impact on the automated organoid culturing market is primarily reflected through rising costs of imported laboratory instruments, consumables, bioreactors, microfluidic devices, and advanced cell culture materials that are heavily dependent on global supply chains, especially from Europe and Asia. Since many key components used in organoid automation, such as liquid handling systems, 3D scaffolds, microplates, imaging systems, and bioreactor parts, are manufactured outside the U.S., tariffs increase procurement and production costs for both domestic biotech companies and research institutions. This leads to higher end-user prices for organoid culture platforms and slower adoption in cost-sensitive academic and clinical research settings. At the same time, tariffs are encouraging companies to adopt supply chain diversification, nearshoring, and increased domestic manufacturing of lab automation tools, as seen broadly across the life sciences sector, where firms are shifting investments toward U.S.-based production to avoid import duties and reduce geopolitical risk.

In addition, tariff-driven cost inflation is indirectly affecting R&D timelines in drug discovery and personalized medicine, since automated organoid systems are critical for high-throughput screening and toxicity testing. Companies may respond by forming strategic partnerships, localizing manufacturing of organoid platforms, or redesigning products to rely more on domestically sourced consumables. Overall, the tariff environment is reshaping the market by accelerating regionalization of supply chains, increasing vertical integration among leading players, and pushing innovation in cost-efficient automation technologies, while also creating short-term pricing pressure across the automated organoid culturing ecosystem.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Key takeaways from the automated organoid culturing market report study

- Market size analysis for the current automated organoid culturing market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the automated organoid culturing market.

- Various opportunities available for the other competitors in the automated organoid culturing market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current automated organoid culturing market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the automated organoid culturing market growth in the future.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

MIMETAS |

$20.5 million |

Series B |

OrganoPlate platform |

The OrganoPlate platform uses microfluidic 3D tissue culture in a high-throughput plate format for drug discovery and toxicity testing. |