Degenerative Disc Disease Market

Degenerative Disc Disease (DDD) Insights and Trends

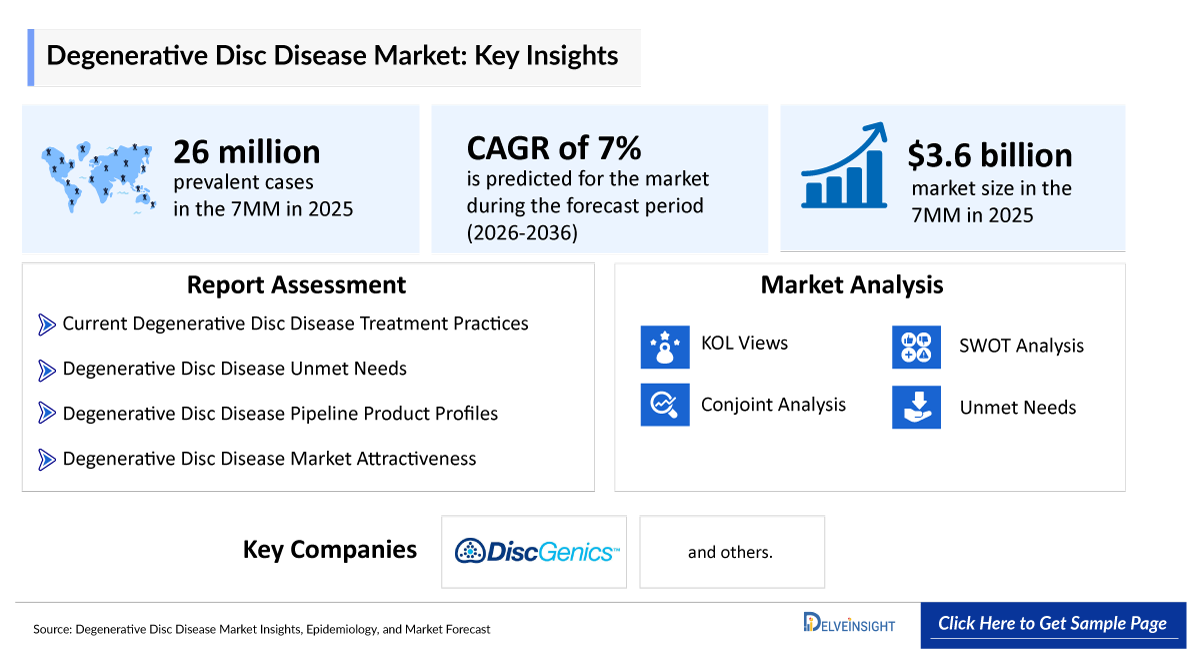

- According to DelveInsight’s analysis, the DDD market size was found to be ~USD 1,200 million in the leading markets (the United States, the EU4 (Germany, France, Italy, and Spain), the United Kingdom, and Japan) in 2025.

- DDD remains a major contributor to chronic low back pain (CLBP), highlighting a significant unmet need for minimally invasive, safe, and durable treatment options. Among all DDD types, lumbar DDD accounts for the largest disease burden, with increasing focus on the development of therapies targeting chronic lumbar discogenic back pain. Rising disease prevalence, aging populations, and limitations of current therapies continue to drive demand for innovative regenerative and targeted treatment approaches.

- Women experience accelerated post-menopausal disc degeneration linked to estrogen-dependent proteoglycan decline; however, sex-specific disease progression remains significantly underrepresented in current treatment guidelines and clinical trial stratification.

- DDD lacks a universally accepted, validated classification system that integrates imaging grade, clinical phenotype, biomechanical subtype, and psychosocial risk. This nosological ambiguity is a root cause of heterogeneous trial outcomes and inconsistent treatment algorithms.

- Conservative management (physiotherapy, NSAIDs, activity modification) remains first-line, yet adherence rates are <40% at 12 months, exposing a critical implementation gap that drives premature escalation to invasive interventions.

- Oral pharmacotherapy (NSAIDs, muscle relaxants, short-course opioids) provides symptom palliation without disease modification; long-term opioid use in DDD carries addiction risk and evidence of opioid-induced hyperalgesia, counterproductively worsening pain chronicity.

- Lumbar fusion (anterior [ALIF], lateral or extreme lateral interbody fusion [LLIF or XLIF], transforaminal [TLIF], and posterior [PLIF]) is the most widely performed surgical intervention, yet data demonstrate only modest superiority over intensive conservative care at 4-year follow-up, raising significant cost-effectiveness concerns at ~USD 60,000–100,000 per procedure.

- Reoperation rates for lumbar spine surgery reach 15–20% within 5 years; "failed back surgery syndrome" affects an estimated 10–40% of patients, a significant outcome burden rarely foregrounded in patient consent discussions.

- Although Rebonuputemcel is considered the most promising emerging therapy in the 7MM DDD landscape, closely following candidates such as Rexlemestrocel-L and BRTX-100 based regenerative approaches also demonstrate strong potential, while earlier-stage assets, including CELZ-201-DDT, AMG0103, and SB-01, remain in relatively nascent development stages with more limited clinical validation at present.

- For most people, DDD can be successfully treated with conservative (meaning non-surgical) care consisting of medication to control inflammation and pain (steroid medications delivered either orally or through an epidural injection) and physical therapy and exercise. Surgery is only considered when patients have not achieved relief over 6 months of non-surgical care and/or are significantly constrained in performing everyday activities.

- The emerging DDD pipeline comprises several notable companies, including DiscGenics, Mesoblast, BioRestorative Therapies, Creative Medical Technology, AnGes, VIVEX Biologics, and others, which are advancing regenerative, cell-based, tissue-engineered, and nucleic acid-based investigational therapies across multiple stages of clinical development.

Degenerative Disc Disease (DDD) Market Size and Forecast in the 7MM

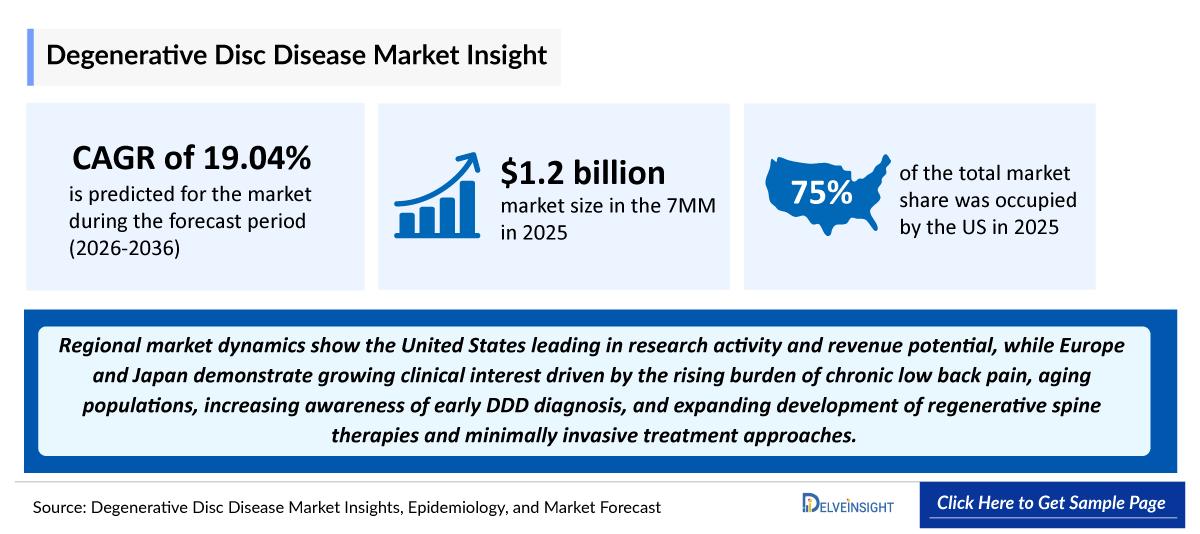

- 2025 DDD Market Size: ~USD 1,200 million

- Projected 2036 DDD Market Size: ~USD 7,200 million

- DDD Growth Rate (2026–2036): ~19.04% CAGR

DelveInsight's ‘Degenerative Disc Disease (DDD) – Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of the DDD, historical and forecasted epidemiology, as well as the DDD market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The DDD market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates DDD patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment, and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in DDD and maps the competitive and clinical landscape to uncover high-value opportunities, providing a clear outlook on future market growth potential.

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

DDD Market CAGR (Forecast period) |

~19.04% (2026–2036) |

|

DDD Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

DDD Companies |

|

|

DDD Therapies |

|

|

DDD Market |

Segmented by

|

|

Analysis |

|

Key Factors Driving the Degenerative Disc Disease (DDD) Market

Rising DDD Prevalence

The increasing prevalence of DDD, particularly among females, is a primary driver of DDD market expansion. In the US, in 2025, there were ~14 million diagnosed prevalent cases of DDD.

Rising Opportunities in Targeted Therapies for DDD

Advancing understanding of disc degeneration and inflammation is driving opportunities for targeted DDD therapies focused on pain reduction, tissue regeneration, and slowing disease progression through regenerative and cell-based approaches.

Emerging DDD Competitive Landscape

The therapeutic landscape for DDD is evolving, with several regenerative and disease-modifying candidates under clinical development. Some of the emerging DDD therapies include SB-01, IDCT (Rebonuputemcel), Rexlemestrocel-L (MPC-06-ID), AMG0103 (NF-?B decoy oligonucleotide), and BRTX-100, among others.

Degenerative Disc Disease (DDD) Understanding and Treatment Algorithm

Degenerative Disc Disease (DDD) Overview and Diagnosis

DDD is a progressive spinal condition characterized by the gradual breakdown of intervertebral discs, which act as cushions between the vertebrae. It commonly occurs due to age-related wear and tear, leading to loss of disc hydration, elasticity, and structural integrity. As the discs deteriorate, patients may experience chronic neck or lower back pain, stiffness, reduced flexibility, and pain radiating to the arms or legs due to nerve compression. In advanced stages, DDD can contribute to disc herniation, spinal instability, or osteoarthritis of the spine. The condition is primarily caused by aging, repetitive mechanical stress, obesity, spinal injuries, poor posture, and genetic predisposition.

DDD is diagnosed through clinical evaluation and imaging tests in patients with chronic back or neck pain. Physical examination assesses pain, mobility, and neurological function, while X-rays, MRI, or CT scans help identify disc degeneration, nerve compression, and spinal abnormalities. In some cases, nerve conduction studies or EMG may also be performed.

Note: Further details are provided in the report.

Degenerative Disc Disease (DDD) Treatment

The primary goals of DDD treatment are to relieve pain, improve mobility, reduce inflammation, and enhance quality of life. Current management includes physical therapy, lifestyle modification, NSAIDs, muscle relaxants, corticosteroid injections, and surgical procedures such as spinal fusion or artificial disc replacement in severe cases. Emerging regenerative therapies, including SB-01, IDCT (Rebonuputemcel), Rexlemestrocel-L (MPC-06-ID), AMG0103 (NF-?B decoy oligonucleotide), and BRTX-100, are being developed to restore disc function and target the underlying disease pathology.

Note: Further details related to country-based variations are provided in the report.

Degenerative Disc Disease (DDD) Unmet Needs

The section “unmet needs of DDD” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Delayed diagnosis and difficulty identifying the exact pain source

- Significant impact on quality of life (QoL) and daily functioning

- Chronic pain and mobility limitations in aging populations

- Limitations of existing pain management therapies, and others…..

Note: Comprehensive unmet needs insights in Degenerative Disc Disease (DDD) and their strategic implications are provided in the full report.

Degenerative Disc Disease (DDD) Epidemiology

Key Findings from Degenerative Disc Disease (DDD) Epidemiological Analysis and Forecast

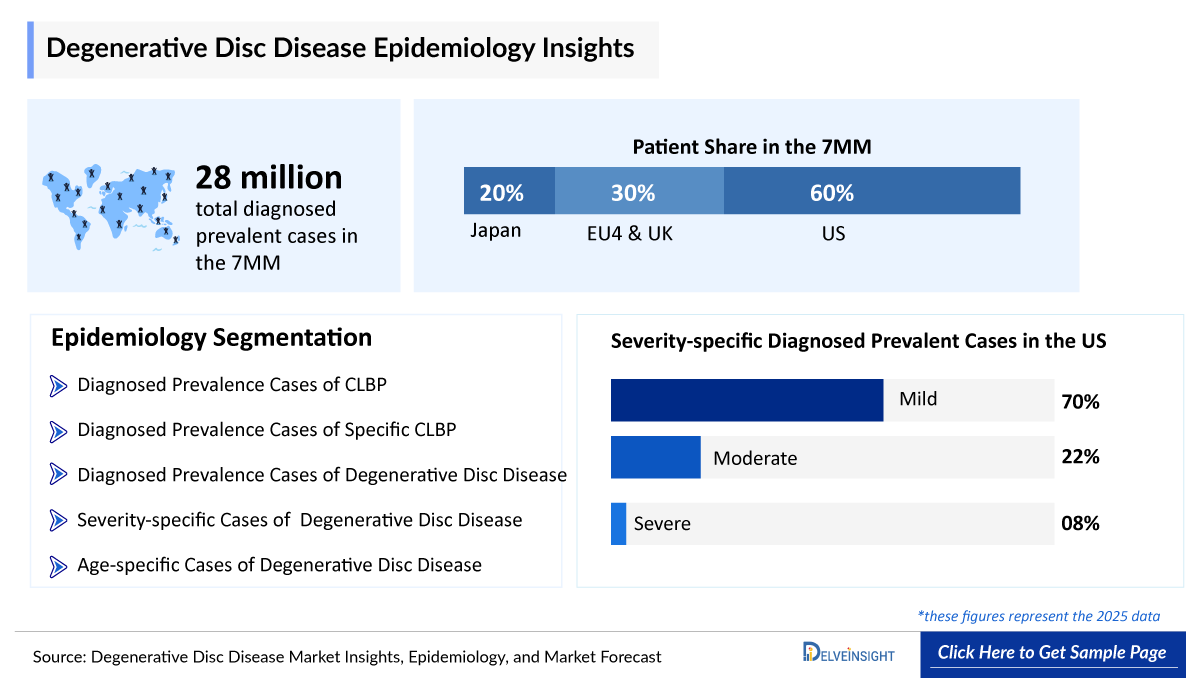

- According to DelveInsight’s estimates, the total number of diagnosed prevalent cases of DDD in the 7MM was nearly 28 million cases in 2025 and is projected to increase during the forecasted period.

- The total number of diagnosed prevalent cases of DDD in the United States was nearly 14 million in 2025.

- Among the EU4, France accounted for the highest number of diagnosed prevalent cases of DDD, followed by Germany, whereas Spain accounted for the lowest number of cases in 2025.

- In 2025, DDD predominantly affected females in the United States, with 7,951,082 cases, while the Males population accounted for 6,282,074 cases. By 2036, these numbers are expected to rise to 8,933,829 cases in females and 7,058,533 cases in males.

- In the US, approximately 30.8% of prevalent DDD cases in 2025 were observed in individuals aged below 60 years, while around 69.2% of cases were reported in the population aged 60 years and above.

Degenerative Disc Disease (DDD) Drug Chapters & Competitive Analysis

The DDD drug chapter provides a detailed, market-focused review of the emerging pipeline across Phase I–III clinical trials. It covers the mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, and strategic partnerships for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the DDD treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the DDD therapeutics market.

Degenerative Disc Disease (DDD) Pipeline Analysis

SB-01: Spine Biopharma

SB-01, developed by Spine BioPharma, is a first-in-class intradiscal injectable peptide therapy designed for the treatment of chronic low back pain associated with DDD. The therapy targets Transforming Growth Factor Beta 1 (TGF-ß1), which is linked to inflammation, disc degeneration, and discogenic pain. By modulating abnormal TGF-ß1 signaling, SB-01 aims to reduce pain, improve function, and potentially slow disease progression. Clinical studies have demonstrated encouraging safety and efficacy results, supporting its potential as a non-surgical and non-opioid treatment option for DDD patients with limited therapeutic alternatives.

IDCT (Rebonuputemcel): DiscGenics

Rebonuputemcel, being developed by DiscGenics, is an allogeneic injectable cell therapy for DDD. The therapy uses progenitor disc cells derived from adult human intervertebral disc tissue to promote disc regeneration, reduce chronic low back pain, and improve disc function. Unlike conventional symptomatic treatments, Rebonuputemcel is designed to target the underlying disc degeneration process. Clinical studies have shown promising improvements in pain and function, and the therapy has received RMAT designation from the US FDA for its potential to address significant unmet needs in DDD.

|

Comparison of Emerging Drugs Under Development | |||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Molecule Type |

Anticipated Launch in the US |

|

SB-01 |

Spine Biopharma |

III |

Moderate-to-severe lumbar DDD |

Intradiscal injection |

TGFβ1 antagonists |

Biologic (Peptide) |

Information is available in the full report |

|

IDCT (Rebonuputemcel) |

DiscGenics |

III |

Mild to moderate lumbar DDD |

Intradiscal injection |

Cell therapy that utilizes proprietary discogenic Cells |

Allogenic Stem Cell |

2028 |

|

Rexlemestrocel-L (MPC-06-ID) |

Mesoblast and Grünenthal |

III |

CLBP associated with DDD |

Intradiscal injection |

Regeneration on Mesenchymal precursor cells |

Allogenic Stem Cell |

Information is available in the full report |

|

AMG0103 (NF-κB decoy oligonucleotide) |

AnGes |

II |

Chronic discogenic lumber back pain |

Intradiscal injection |

NF-kappa B inhibitors |

Synthetic oligonucleotides |

Information is available in the full report |

|

BRTX-100 |

BioRestorative Therapies |

II |

Chronic Lumbar Disc Disease |

Intradiscal injection |

Cell replacements |

Autologous Stem Cell |

Information is available in the full report |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | |||||||

Degenerative Disc Disease (DDD) Key Players, Market Leaders, and Emerging Companies

- Spine Biopharma

- DiscGenics

- Mesoblast

- Grünenthal

- AnGes

- BioRestorative Therapies, and others

Degenerative Disc Disease (DDD) Drug Updates

- In April 2026, in the R&D presentation, Mesoblast announced that, following the topline Phase III results and a planned BLA submission, rexlemestrocel-L for CLBP associated with DDD may potentially receive FDA approval in Q2 CY2028 under a Priority Review pathway. The anticipated timeline reflects the company’s regulatory strategy to accelerate the development and commercialization of the program.

- In April 2026, BioRestorative Therapies announced a strategic partnership with global dermatology leader Dr. David J. Goldberg to lead clinical evaluation and Seek Multi-Channel Adoption of Its Regenerative BioCosmeceutical Platform.

- In April 2026, BioRestorative Therapies announced a strategic collaboration with 203 Creates to build and commercialize a Biocosmeceutical Platform.

- In March 2026, DiscGenics’s CEO highlighted the launch of the FDA-approved Phase III Program for IDCT (rebonuputemcel) at the CG 2026 Musculoskeletal Conference.

- In January 2026, DiscGenics announced that the first patient treated in their Phase III clinical trial evaluating IDCT (rebonuputemcel) in subjects with single-level, symptomatic mild-to-moderate lumbar DDD. Site activation is underway across the United States.

Degenerative Disc Disease (DDD) Market Outlook

The DDD market is undergoing a significant transformation, moving beyond conventional pain management and surgical interventions toward regenerative and disease-modifying therapeutic approaches. The growing development of cell-based therapies, biologics, and gene-based technologies reflects a shift toward addressing the underlying mechanisms of disc degeneration, inflammation, and tissue damage in DDD. These advancements validate innovative strategies focused on disc regeneration, restoration of spinal function, and long-term pain reduction, while strengthening clinical and commercial interest in next-generation DDD therapies and reshaping the competitive landscape.

With the continued advancement of pipeline candidates such as SB-01 (Spine Biopharma), IDCT (Rebonuputemcel) (DiscGenics), Rexlemestrocel-L (MPC-06-ID) (Mesoblast and Grünenthal), AMG0103 (NF-?B decoy oligonucleotide) (AnGes), and BRTX-100 (BioRestorative Therapies), the DDD treatment landscape is evolving similarly to other chronic musculoskeletal disorders, where regenerative medicine is driving broader therapeutic innovation. The United States is expected to remain a major DDD market due to the high prevalence of chronic low back pain, aging population, sedentary lifestyle patterns, increasing adoption of minimally invasive procedures, and improved access to advanced spine care and diagnostic technologies compared with several other global markets.

Overall, the introduction of differentiated regenerative therapies, increasing research into spine degeneration and chronic pain management, advancements in biologics and cell therapies, and rising awareness among high-risk populations such as older adults, obese individuals, and patients with physically demanding occupations are expected to drive growth in the DDD market during the forecast period, creating significant commercial opportunities for both currently available treatments and emerging pipeline therapies.

- According to the estimates, the largest market size of DDD was captured by the United States, i.e., ~USD 900 million in 2025.

- The DDD market is evolving as treatment focus shifts from conventional pain management and surgical interventions toward regenerative and disease-modifying therapies addressing disc degeneration, inflammation, and tissue repair, with emerging candidates such as rebonuputemcel (DiscGenics), VIA Disc NP, and other cell-based therapies driving interest due to their potential to restore disc function and provide long-term pain relief.

- Regional market dynamics show the United States leading in research activity and revenue potential, while Europe and Japan demonstrate growing clinical interest driven by the rising burden of chronic low back pain, aging populations, increasing awareness of early DDD diagnosis, and expanding development of regenerative spine therapies and minimally invasive treatment approaches.

Note: Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in Degenerative Disc Disease (DDD) (2022–2036 Forecast)

The DDD market comprises tansforming Growth Factor Beta 1 (TGFß1) antagonists and anabolic growth factor modulators, NF-kappa B (NF-?B) inhibitors and anti-inflammatory pathway modulators, Platelet-Rich Plasma (PRP) and cytokine-modulating biologics, Mesenchymal Stem Cell (MSC) therapies and regenerative cell-based therapies, and extracellular matrix regenerative therapies and nucleus pulposus restoration agents, with multiple drug classes targeting disc degeneration, chronic pain, inflammation, extracellular matrix breakdown, and functional impairment associated with DDD.

Transforming Growth Factor Beta 1 (TGFß1) antagonists and anabolic growth factor modulators: These therapies are being investigated to regulate fibrotic signaling, stimulate extracellular matrix repair, promote disc cell regeneration, and restore intervertebral disc integrity. Representative agents include SB-431542, LY2109761 (TGFß pathway inhibitors), rhBMP-7/OP-1, Growth Differentiation Factor-5 (GDF-5), and Link N peptide.

Mesenchymal stem cell (MSC) therapies and regenerative cell-based therapies: Stem cell-based approaches are designed to regenerate damaged disc tissue, restore disc hydration and structure, and potentially provide disease-modifying benefits by promoting cellular repair and matrix synthesis. Leading therapies include Rexlemestrocel-L (Mesoblast), IDCT/Rebonuputemcel (DiscGenics), AlloRx Stem Cell Therapy, BMAC (Bone Marrow Aspirate Concentrate) therapies, and Autologous Adipose-Derived MSC therapies.

Conservative therapies and surgical interventions currently dominate the DDD treatment landscape, while biologic, anti-inflammatory, and regenerative therapies are driving the next generation of innovation aimed at addressing the underlying causes of disc degeneration rather than providing symptomatic relief alone.

Note: Further details will be provided in the report….

Degenerative Disc Disease (DDD) Drug Uptake

This section focuses on the uptake rate of potential drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the DDD market's uptake by drugs, patient uptake by therapy, and sales of each drug.

The uptake of therapies in DDD is expected to vary across conventional pain management approaches and emerging regenerative treatments. Existing therapies such as NSAIDs and other conventional approaches currently account for the highest uptake, despite their limited disease-modifying benefits. Among emerging therapies, Rebonuputemcel and Rexlemestrocel-L are anticipated to witness relatively better future uptake owing to their regenerative and anti-inflammatory potential in DDD treatment, while therapies such as AMG0103 (NF-?B decoy oligonucleotide), BRTX-100, and CELZ-201-DDT are expected to gain gradual adoption as clinical evidence matures.

Note: Further detailed analysis of emerging therapies' drug uptake in the report…

Market Access and Reimbursement of DDD

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of approved therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

Reimbursement remains a key determinant in the adoption of emerging DDD therapies, with payers increasingly demanding strong clinical and economic evidence to support coverage of high-cost implants and biologics. Prior authorization requirements continue to create access barriers, as major insurers often mandate failure of conservative therapies before approving advanced procedures such as total disc arthroplasty and interbody fusion. Historically, certain technologies, including legacy annular closure devices, faced limited or no coverage; however, the reimbursement landscape is gradually improving with the introduction of new payment pathways and procedure codes. Recent developments, such as CMS granting New Technology Add-on Payment (NTAP) status for Carlsmed’s aprevo implants and the implementation of a new Category 1 CPT code for annular closure in 2026, are expected to support physician adoption and market uptake. In parallel, payers are encouraging a shift toward outpatient and ambulatory surgical settings, while products demonstrating reduced reoperation rates and long-term cost savings are gaining greater reimbursement support due to their potential to lower the overall healthcare burden.

Note: Further details are provided in the final report….

Degenerative Disc Disease (DDD) Therapies Price Scenario & Trends

Pricing and analogue assessment of DDD therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, the closest and most appropriate analogue selection for emerging therapies, and the understanding of how pricing influences market access, adherence, and long-term uptake.

NSAIDs like Ibuprofen are commonly used as first-line therapies. For cost estimation, ibuprofen was assumed at 1,600 mg/day, based on a pricing of approximately USD 4.87 for six tablets, translating to an estimated therapy cost of approximately USD 146.

Further details are provided in the final report….

Industry Experts and Physician Views for Degenerative Disc Disease (DDD)

To keep up with DDD market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry experts were contacted for insights on the DDD emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in DDD, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 10+ KOLs to gather insights; however, interviews were conducted with 6+ KOLs in the 7MM. Centers such as Stanford University, University College London, Joslin Diabetes Center, and Hospital Clínic de Barcelona, etc. were contacted. Their opinion helps understand and validate current and emerging DDD therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in DDD.

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“Degenerative Disc Disease is a major contributor to chronic back and neck pain, where progressive disc degeneration can significantly impair mobility, daily functioning, and overall quality of life, particularly in aging populations.” |

|

Japan |

“DDD management remains challenging due to the chronic and recurrent nature of the condition, highlighting the need for early diagnosis, minimally invasive interventions, and regenerative therapies that can restore disc function and reduce long-term disability.” |

Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of Degenerative Disc Disease (DDD), strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are mainly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Report

- The report covers a segment of key events, an executive summary, a descriptive overview of DDD, explaining its causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the DDD market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM DDD market.

Report Insights

- Degenerative Disc Disease (DDD) Patient Population Forecast

- Degenerative Disc Disease (DDD) Therapeutics Market Size

- Degenerative Disc Disease (DDD) Pipeline Analysis

- Degenerative Disc Disease (DDD) Market Size and Trends

- Degenerative Disc Disease (DDD) Market Opportunity (Current and forecasted)

Report Key Strengths

- Epidemiology-based (Epi-based) Bottom-up Forecasting

- Artificial Intelligence (AI)-enabled Market Research Report

- 11-year Forecast

- Degenerative Disc Disease (DDD) Market Outlook (North America, Europe, Asia-Pacific)

- Patient Burden Trends (by geography)

- Degenerative Disc Disease (DDD) Treatment Addressable Market (TAM)

- Degenerative Disc Disease (DDD) Competitive Landscape

- Degenerative Disc Disease (DDD) Major Companies Insights

- Degenerative Disc Disease (DDD) Price Trends and Analogue Assessment

- Degenerative Disc Disease (DDD) Therapies Drug Adoption/Uptake

- Degenerative Disc Disease (DDD) Therapies Peak Patient Share analysis

Report Assessment

- Degenerative Disc Disease (DDD) Current Treatment Practices

- Degenerative Disc Disease (DDD) Unmet Needs

- Degenerative Disc Disease (DDD) Clinical Development Analysis

- Degenerative Disc Disease (DDD) Emerging Drugs Product Profiles

- Degenerative Disc Disease (DDD) Market Attractiveness

- Degenerative Disc Disease (DDD) Qualitative Analysis (SWOT and Conjoint Analysis)

FAQs

Market Insights

- What was the Degenerative Disc Disease (DDD) market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of Degenerative Disc Disease (DDD)?

- What are the disease risks, burdens, and unmet needs of Degenerative Disc Disease (DDD)?

- What will be the growth opportunities across the 7MM concerning the patient population with Degenerative Disc Disease (DDD)?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of Degenerative Disc Disease (DDD)? What are the current guidelines for treating Degenerative Disc Disease (DDD) in the US, Europe, and Japan?

Reasons to Buy

- The report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the Degenerative Disc Disease (DDD) market.

- Bottom up forecasting builds from the affected population to product forecasts, delivering a robust, data driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights into the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI) enabled report summarize and simplify complex datasets within the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data driven decisions.