Diabetes Care Devices Market Summary

- The global diabetes care devices market size is expected to increase from USD 40,781.76 million in 2025 to USD 76,404.07 million by 2034, reflecting strong and sustained growth.

- The global diabetes care devices market is growing at a CAGR of 7.26% during the forecast period from 2026 to 2034.

- The diabetes care devices market is primarily driven by the rising global prevalence of diabetes, fueled by increasing obesity rates, sedentary lifestyles, and aging populations. Growing awareness about early diagnosis and the importance of continuous glucose monitoring is boosting the adoption of advanced devices such as CGMs, insulin pumps, and smart insulin pens. Technological advancements, including digital connectivity, AI integration, and wearable solutions, are further enhancing patient convenience and treatment accuracy. Additionally, supportive reimbursement policies, expanding healthcare infrastructure, and increasing emphasis on self-management and home-based care are contributing to sustained market growth.

- The leading companies operating in the diabetes care devices market include Becton, Dickinson and Company, Novo Nordisk A/S, Ypsomed Holding AG, Tandem Diabetes Care, Inc., Biocon Ltd., Eli Lilly and Company, Insulet Corporation, Abbott, Terumo Corporation, CeQur, EOFLOW CO., LTD, Sanofi, Medtronic, F. Hoffmann-La Roche Ltd., Johnson & Johnson Services, Inc., Dexcom Inc., ARKRAY, Inc., Senseonics, WaveForm Technologies, Inc., B. Braun Melsungen AG, and others.

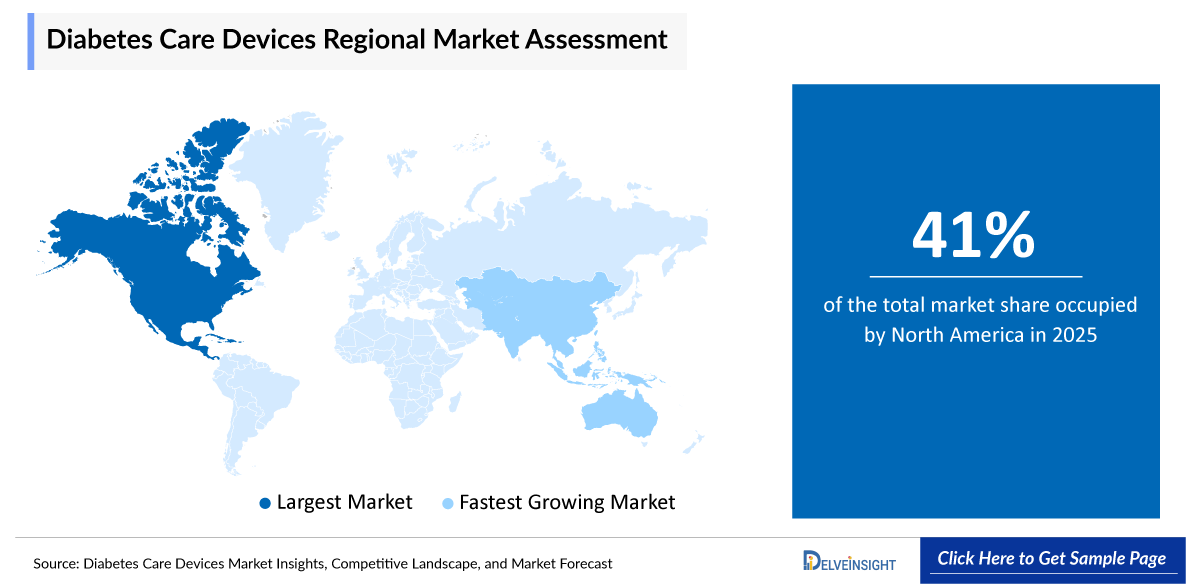

- North America is expected to dominate the diabetes care devices market due to the high prevalence of diabetes, strong healthcare infrastructure, and widespread adoption of advanced technologies such as continuous glucose monitoring (CGM) systems and insulin pumps. The region also benefits from favorable reimbursement policies, high healthcare expenditure, and strong presence of leading market players, which further support innovation and rapid product adoption. Additionally, increasing awareness about early diagnosis and effective disease management continues to drive demand for diabetes care devices in the region.

- In the product type segment of the diabetes care devices market, the blood glucose monitoring devices category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Diabetes Care Devices Market Trends

Diabetes Care Devices Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 40,781.76 million |

|

2034 Projected Market Size |

USD 76,404.07 million |

|

Growth Rate (2026-2034) |

7.26% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Diabetes Care Devices Market

- Increasing prevalence of diabetes and associated risk factors leading to a surge in diabetes care devices: The increasing prevalence of diabetes and its associated risk factors, such as obesity, sedentary lifestyles, unhealthy diets, and aging populations, is significantly driving the demand for diabetes care devices. As the number of individuals diagnosed with diabetes continues to rise globally, there is a growing need for effective glucose monitoring and insulin delivery solutions to manage the condition and prevent complications. This surge in patient population directly contributes to increased adoption of devices such as glucose monitors, continuous glucose monitoring systems, and insulin pumps.

- Rising patient awareness and self-management trends is escalating the market of diabetes care devices: Rising patient awareness about diabetes management and the importance of regular glucose monitoring is significantly accelerating the adoption of diabetes care devices. Increasing health education, digital health campaigns, and access to online information are encouraging patients to take a proactive approach toward self-management. As a result, there is growing demand for user-friendly devices such as blood glucose monitors, continuous glucose monitoring (CGM) systems, and smart insulin delivery solutions that enable better control, improved outcomes, and reduced complications.

- Increase in product development activites among the key market players: An increase in product development activities among key market players is driving the growth of the diabetes care devices market. Companies are continuously investing in research and development to introduce advanced technologies such as continuous glucose monitoring (CGM) systems, smart insulin pens, wearable insulin pumps, and integrated digital health platforms. These innovations enhance accuracy, convenience, and real-time data tracking, improving patient outcomes and user experience. Frequent product launches and technological advancements also strengthen competitive positioning and expand market adoption globally.

Diabetes Care Devices Market Report Segmentation

This diabetes care devices market report offers a comprehensive overview of the global diabetes care devices market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product Type (Blood Glucose Monitoring Devices {Wearable and Non Wearable}, Insulin Delivery Devices {Insulin Syringes, Insulin Pens, Insulin Pumps, and Others} and Integrated Systems), Monitoring (Self-Monitoring and Continous Monitoring), Patient Type (Type 1, Type 2, and Gestational Diabetes), End-Users (Hospitals & Clinics, Homecare Settings, and Others), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing Diabetes Care Devices market.

A diabetes care device is a medical device used to monitor and manage blood glucose levels in individuals with diabetes. These devices help patients and healthcare professionals track glucose levels, deliver insulin, and improve overall disease management. Common examples include blood glucose meters, continuous glucose monitoring (CGM) systems, insulin pens, insulin syringes, and insulin pumps, all designed to support effective diabetes control and reduce the risk of complications.

The diabetes care devices market is primarily driven by the rising global prevalence of diabetes, which is largely influenced by increasing obesity rates, sedentary lifestyles, unhealthy dietary habits, and the growing aging population worldwide. As the number of people diagnosed with diabetes continues to expand, there is a stronger need for effective tools to monitor and manage blood glucose levels, leading to higher adoption of advanced diabetes care solutions. Growing awareness about the importance of early diagnosis, regular monitoring, and maintaining optimal glycemic control is further encouraging patients and healthcare providers to use continuous glucose monitoring (CGM) systems, insulin pumps, and smart insulin pens. In addition, rapid technological advancements such as digital connectivity, mobile app integration, cloud-based data sharing, artificial intelligence (AI)-enabled analytics, and wearable devices are significantly improving accuracy, convenience, and real-time monitoring capabilities. These innovations enhance patient engagement and support personalized treatment approaches. Supportive reimbursement policies, expanding healthcare infrastructure, increasing healthcare expenditure, and the shift toward home-based care and self-management practices are also playing a crucial role in driving market growth. Together, these factors are creating a strong and sustained demand for modern diabetes care devices across global markets.

Get More Insights into the Report @ Diabetes Care Devices Market Insights

What are the latest diabetes care devices market dynamics and trends?

The global diabetes care devices market is growing significantly, driven by the increasing prevalence of diabetes andassociated risk factors such as obesity, sedentary lifestyles, unhealthy diets, and aging populations. Additionally, the market is further escalated by the increasing product development activites among the key market players.

According to data provided by the International Diabetes Federation (2025), approximately, 590 million worldwide had diabetes that is around 11.1% or 1 in 9 of the adult population (20-79 years) was living with diabetes. The projections further estimated that by 2050, 1 in 8 adults, approximately 853 million, will be living with diabetes, an increase of 46%. The increasing number of diabetes cases worldwide is significantly boosting the overall diabetes care devices market, as more patients require continuous monitoring and effective disease management solutions. Rising prevalence of type 1 and type 2 diabetes, driven by factors such as obesity, sedentary lifestyles, unhealthy diets, and aging populations, is expanding the patient pool in need of glucose monitoring and insulin delivery devices. This growing demand is encouraging the adoption of blood glucose meters, continuous glucose monitoring (CGM) systems, insulin pens, and insulin pumps to help maintain optimal blood sugar levels and reduce the risk of complications.

Furthermore, the technological advancements have also reshaped the industry, as the industry is experiencing a notable shift towards wearable and automated insulin delivery (AID) devices. Insulin pumps and patch pumps offer continuous insulin infusion, providing greater convenience and discretion for users. A key development in this space is the push for regulatory approvals. For instance, in January 2024, PharmaSens, a Swiss medical device company, submitted an FDA application for its 'niia essential' insulin patch pump system. This application, following its ISO 13485 certification in November 2023, is a significant step toward making advanced, patient-centric insulin pump technology more widely available.

Thus, the factors mentioned above are expected to boost the overall market of diabetes care devices during the forecast period.

However, False readings or technical errors in diabetes care devices, such as glucose meters and continuous glucose monitoring systems, can lead to incorrect insulin dosing, increasing the risk of hypoglycemia or hyperglycemia and posing serious health concerns for patients. Such inaccuracies may reduce user confidence in the devices and negatively impact treatment outcomes. Additionally, increasing instances of product recalls due to safety or performance issues can further challenge market growth by affecting brand reputation, regulatory scrutiny, and overall consumer trust. These factors act as significant restraints in the diabetes care devices market.

Diabetes Care Devices Market Segment Analysis

Diabetes Care Devices Market Product Type (Blood Glucose Monitoring Devices {Wearable and Non Wearable}, Insulin Delivery Devices {Insulin Syringes, Insulin Pens, Insulin Pumps, and Others} and Integrated Systems), Monitoring (Self-Monitoring and Continous Monitoring), Patient Type (Type 1, Type 2, and Gestational Diabetes), End-Users (Hospitals & Clinics, Homecare Settings, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product Type: Under Blood Glucose Monitoring Devices Segment, Wearable Category Projected to Register Largest Revenue Share

In the product type segment of the diabetes care devices market, under under blood glucose monitoring devices segment, wearable category is estimated to account for the largest market share of 65% in 2025, due to the increasing adoption of advanced and convenient monitoring solutions such as continuous glucose monitoring (CGM) systems. Wearable devices provide real-time, continuous tracking of glucose levels, reducing the need for frequent finger-prick testing and improving patient comfort and compliance. These devices offer enhanced accuracy, instant alerts for high or low glucose levels, and seamless integration with smartphones and digital health platforms, enabling better data management and personalized diabetes care. The growing preference for minimally invasive and user-friendly technologies, along with rising awareness about tight glycemic control, is further driving demand for wearable glucose monitoring devices. Additionally, technological advancements, increasing prevalence of diabetes, supportive reimbursement policies in developed regions, and the shift toward home-based and remote patient monitoring are contributing to the dominance of the wearable category within the blood glucose monitoring segment.

Additioanlly, the increasing product development activities are further boosting the segment. For instance, in March 2024, the U.S. FDA cleared the first over-the-counter (OTC) continuous glucose monitor, Dexcom Stelo, making wearable CGM accessible without a prescription.

Thus, the factors mentioned above are expected to boost the market of segment and thereby escalating the overall market diabetes care devices.

By Monitoring: Continous Monitoring Category Dominates the Market

In the monitoring segment of the diabetes care devices market, continuous monitoring category are projected to hold the largest market share of 66% in 2025. Continuous monitoring systems, particularly continuous glucose monitoring (CGM) devices, are significantly boosting the overall diabetes care devices market by transforming how diabetes is managed. Unlike traditional finger-prick methods, CGM systems provide real-time, continuous tracking of glucose levels, offering greater accuracy, convenience, and improved glycemic control. These devices generate instant alerts for high and low blood sugar levels, helping reduce the risk of severe complications such as hypoglycemia and hyperglycemia. The ability to share data with healthcare providers through digital platforms also supports remote monitoring and personalized treatment adjustments, which is especially valuable in home-based care settings. Increasing adoption of wearable and minimally invasive technologies, growing awareness about tight glucose control, and advancements in connectivity features such as smartphone integration and cloud-based analytics are further accelerating demand. Additionally, expanding reimbursement coverage and the rising preference for proactive disease management are driving widespread acceptance of continuous monitoring systems, thereby contributing strongly to market growth.

Additionally, the increase in approvals and launches in diabetes care devices is further boosting the overall market. For instance, in June 2024, Abbott announced that the US Food and Drug Administration (FDA) approved two new over-the-counter continuous glucose monitoring systems – Lingo™ and Libre Rio™. These systems were based on Abbott's world-leading FreeStyle Libre® continuous glucose monitoring technology.

Thus, the factors mentioned above are expected to boost the market of continous category therby escalating the overall market of diabetes care devices.

By Patient Type: Type 2 Category Dominates the Market

In the patient type segment of the diabetes care devices market, Type 2 category is projected to hold the largest market share of 70% in 2025, due to the high and continuously rising prevalence of the condition worldwide. According to the data provided by the International Diabetes Federation (2025), over 90% of people with diabetes have type 2 diabetes.

As type 2 diabetes accounts for the majority of total diabetes cases, the large patient population creates sustained demand for blood glucose monitoring devices, continuous glucose monitoring (CGM) systems, insulin delivery devices, and related accessories. Many type 2 patients require regular monitoring to manage blood sugar levels, prevent complications, and adjust treatment plans effectively. The increasing shift toward early diagnosis, preventive care, and home-based disease management is further encouraging the use of user-friendly and connected devices. Additionally, growing awareness about the importance of lifestyle management combined with technological advancements in wearable and digital monitoring solutions is expanding adoption among type 2 diabetes patients, thereby driving overall market growth.

Diabetes Care Devices Market Regional Analysis

North America Diabetes Care Devices Market Trends

North America is poised to secure the largest share of 41% in the global diabetes care devices market in 2025, due to the high prevalence of diabetes, strong healthcare infrastructure, and widespread adoption of advanced technologies such as continuous glucose monitoring (CGM) systems and insulin pumps. The region also benefits from favorable reimbursement policies, high healthcare expenditure, and strong presence of leading market players, which further support innovation and rapid product adoption. Additionally, increasing awareness about early diagnosis and effective disease management continues to drive demand for diabetes care devices in the region.

According to data provided by the Centre for Disease Control and Prevention (2026), around 40.1 million people were living with diagnosed or undiagnosed diabetes in the United States. In which 29.1 million people were living with diagnosed diabetes, including 28.8 million adults aged ≥18 years. Blood glucose monitoring systems and insulin delivery devices are essential tools for managing diabetes, helping individuals regularly check and maintain their blood sugar levels. These systems, including finger-stick glucometers and continuous glucose monitors, which enable users to track glucose fluctuations throughout the day. This information allows for timely adjustments in diet, physical activity, and medication to maintain optimal blood sugar levels, prevent complications, and manage diabetes effectively.

Additionally, the increasing number of product development activities in the region by the regulatory bodies is further going to accelerate the growth of the blood glucose monitoring systems market. For instance, in August 2024, Medtronic plc, a global leader in healthcare technology, announced the U.S. Food and Drug Administration (FDA) approved its Simplera™ continuous glucose monitor (CGM). This approval marked the launch of the company's first disposable, all-in-one CGM, which was half the size of previous Medtronic CGMs.

In addition to this in June 2024, Prevounce Health, a leading provider of remote care management software, devices, and services, announced the launch of its first remote blood glucose monitoring device, the Pylo GL1-LTE. The blood glucose meter was clinically validated and connected to multiple cellular networks to ensure reliable data transmission throughout the US.

Thus, the factors mentioned above are expected to boost the overall market of diabetes care devices across the region.

Europe Diabetes Care Devices Market Trends

Europe is increasingly poised to play a leading role in the overall diabetes care devices market due to the rising prevalence of diabetes, strong healthcare infrastructure, and supportive government initiatives focused on chronic disease management. The region benefits from favorable reimbursement policies, growing adoption of advanced technologies such as continuous glucose monitoring (CGM) systems and insulin pumps, and increasing awareness about early diagnosis and preventive care. Additionally, continuous investments in research and innovation by key market players further support market growth across European countries.

According to the International Diabetes Federation (2024), approximately 65.6 million people in Europe were living with diabetes in 2024, with that number projected to increase to 72.4 million by 2050. This demographic shift has created a pressing need for effective and accessible diabetes management tools. In response, European countries are actively promoting early diagnosis and proactive care through awareness campaigns and favorable reimbursement policies, which have encouraged the adoption of innovative solutions like reusable pens, insulin pumps, and smart devices.

The European market is also a hub for innovation, with leading manufacturers continually launching new products and expanding the indications for existing ones. A prime example is Medtronic plc, which in July 2025 received CE Mark approval to expand the use of its MiniMed™ 780G system. This pivotal approval allows the automated insulin delivery (AID) system to be used by a much broader patient population, thereby escalating the overall market of diabetes drug devices.

Thus, the factors mentioned are expected to boost the market of diabetes care devices market in Europe.

Asia-Pacific Diabetes Care Devices Market Trends

The Asia-Pacific region is rapidly emerging as one of the fastest-growing and most influential markets in the global diabetes care devices industry due to the increasing prevalence of diabetes, large population base, and rising urbanization. Growing awareness about early diagnosis and improved disease management, along with expanding healthcare infrastructure, is driving greater adoption of glucose monitoring and insulin delivery devices. Additionally, improving access to healthcare services, increasing healthcare expenditure, and the growing penetration of advanced technologies are further supporting market growth across key countries in the region.

According to the International Diabetes Federation (2024), approximately 106.9 million people in South-East Asia were living with diabetes in 2024, with that number projected to increase to 184.5 million by 2050. This significant patient pool makes advanced diabetes drug delivery devices essential for managing the disease and improving patient outcomes.

Thus, the factors mentioned above are expected to boost the overall market of diabetes care devcies across the Asia-Pacific region.

Who are the major players in the diabetes care devices market?

The following are the leading companies in the diabetes care devices market. These companies collectively hold the largest market share and dictate industry trends.

- Becton, Dickinson and Company

- Novo Nordisk A/S

- Ypsomed Holding AG

- Tandem Diabetes Care, Inc.

- Biocon Ltd.

- Eli Lilly and Company

- Insulet Corporation

- Abbott

- Terumo Corporation

- CeQur

- EOFLOW CO., LTD

- Sanofi

- Medtronic

- F. Hoffmann-La Roche Ltd.

- Johnson & Johnson Services, Inc.

- Dexcom Inc.

- ARKRAY, Inc.

- Senseonics

- WaveForm Technologies, Inc.

- B. Braun Melsungen AG, and others

How is the competitive landscape shaping the Diabetes Care Devices market?

The competitive landscape of the diabetes care devices market is characterized by the presence of well-established global players alongside emerging technology innovators, leading to a moderately concentrated but dynamic market environment. Major companies are increasingly focusing on product innovation, strategic partnerships, and geographic expansion to gain competitive advantage, resulting in the frequent launch of advanced continuous glucose monitoring (CGM) systems, smart insulin delivery devices, and connected digital solutions. Competitive strategies such as mergers and acquisitions, collaborations with technology firms, and investments in research and development are intensifying as players strive to differentiate their offerings and capture larger market share. While a few key players hold significant influence due to strong brand recognition, extensive distribution networks, and robust patent portfolios, smaller specialized firms are also shaping the market by introducing niche and next-generation wearable technologies. This combination of established dominance and emerging competition is driving technological advancements, improving product quality, and expanding access to diabetes care devices globally.

Recent Developmental Activities in the Diabetes Care Devices Market

- In August 2025, Signos launched the Signos Glucose Monitoring System, the first FDA-cleared, over-the-counter glucose monitoring system designed for weight management. The system integrates the Stelo by Dexcom glucose biosensor with an AI-powered platform, providing personalized, real-time insights into how food, activity, stress, and sleep impact metabolic health.

- In July 2025, Medtronic plc. announced that it had received CE Mark in Europe to expand indications of the MiniMed™ 780G system for individuals aged 2 years and older, during pregnancy, and for those with type 2 insulin-requiring diabetes.

- In May 2025, GO-Pen ApS received FDA 510(k) clearance for the GO-PEN®, a user-filled insulin pen compatible with standard insulin vials, providing an affordable alternative to traditional disposable pens.

- In April 2025, Dexcom received FDA clearance for the G7 15-Day sensor, which boasts extended wear time and enhanced accuracy for diabetes management.

- In September 2024, the Eversense 365 received FDA clearance as an integrated continuous glucose monitoring (iCGM) system for individuals with diabetes. Unlike short-term CGMs that typically last 10 to 14 days, the Eversense 365 features a single sensor that can be used for an entire year, offering minimal disruption to daily life.

- In August 2024, Medtronic plc., a global leader in healthcare technology, announced that the U.S. FDA had approved its Simplera™ continuous glucose monitor (CGM), the company’s first disposable, all-in-one CGM. The device was half the size of previous Medtronic CGMs, with a discreet design that simplified insertion and wear, eliminating the need for overtape.

- In May 2024, Smart Meter launched iGlucose Plus for diabetes management, a cellular-enabled glucose meter that eliminated the need for syncing, pairing, or relying on smartphones and Wi-Fi.

- In April 2024, Omnipod 5 by Insulet was approved by Health Canada. Omnipod 5 is an automated insulin delivery system.

- In February 2024, Dexcom launched its real-time continuous glucose monitoring solution, Dexcom ONE+, in Europe. Dexcom ONE+ was a customizable CGM solution designed to be worn at three different locations on the body.

- In February 2024, Insulet Corporation announced that it had received CE Mark approval under the European Medical Device Regulation for compatibility of the Abbott FreeStyle Libre 2 Plus sensor with its Omnipod 5 Automated Insulin Delivery System for individuals aged two years and older with type 1 diabetes.

- In February 2024, Tandem's Mobi pump, a tubeless insulin delivery device, was launched by Tandem Diabetes Care.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Diabetes Care Devices Market CAGR (2026-2034) |

7.26% |

|

Key Companies in the Diabetes Care Devices Market |

Becton, Dickinson and Company, Novo Nordisk A/S, Ypsomed Holding AG, Tandem Diabetes Care, Inc., Biocon Ltd., Eli Lilly and Company, Insulet Corporation, Abbott, Terumo Corporation, CeQur, EOFLOW CO., LTD, Sanofi, Medtronic, F. Hoffmann-La Roche Ltd., Johnson & Johnson Services, Inc., Dexcom Inc., ARKRAY, Inc., Senseonics, WaveForm Technologies, Inc., B. Braun Melsungen AG, and others. |

|

Diabetes Care Devices Market Segments |

by Product Type, by Monitoring, by Patient Type, by End-users, and by Geography |

|

Diabetes Care Devices Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Diabetes Care Devices Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Diabetes Care Devices Market Segmentation

- Diabetes Care Devices by Product Type Exposure

- Blood Glucose Monitoring Devices

- Wearable

- Non Wearable

- Insulin Delivery Devices

- Insulin Syringes

- Insulin Pens

- Insulin Pumps

- Others

- Integrated Systems

- Blood Glucose Monitoring Devices

- Diabetes Care Devices Monitoring Exposure

- Self-Monitoring

- Continous Monitoring

- Diabetes Care Devices Patient Type Exposure

- Type 1

- Type 2

- Gestational Diabetes

- Diabetes Care Devices End-Users Exposure

- Hospitals & Clinics

- Homecare Settings

- Others

Diabetes Care Devices Geography Exposure

- North America Diabetes Care Devices Market

- United States Diabetes Care Devices Market

- Canada Diabetes Care Devices Market

- Mexico Diabetes Care Devices Market

- Europe Diabetes Care Devices Market

- United Kingdom Diabetes Care Devices Market

- Germany Diabetes Care Devices Market

- France Diabetes Care Devices Market

- Italy Diabetes Care Devices Market

- Spain Diabetes Care Devices Market

- Rest of Europe Diabetes Care Devices Market

- Asia-Pacific Diabetes Care Devices Market

- China Diabetes Care Devices Market

- Japan Diabetes Care Devices Market

- India Diabetes Care Devices Market

- Australia Diabetes Care Devices Market

- South Korea Diabetes Care Devices Market

- Rest of Asia-Pacific Diabetes Care Devices Market

- Rest of the World Diabetes Care Devices Market

- South America Diabetes Care Devices Market

- Middle East Diabetes Care Devices Market

- Africa Diabetes Care Devices Market

Diabetes Care Devices Market Recent Industry Trends and Milestones (2022-2026):

|

Category |

Key Developments |

|

Diabetes Care Devices Regulatory Approvals |

Medtronic plc. - MiniMed™ 780G system (CE), Insulet Corporation - FreeStyle Libre 2 Plus (CE), GO-Pen ApS - GO-Pen (FDA) |

|

Diabetes Care Devices Launches |

Insulet launched Omnipod 5, an AID System, launched Sequel Twiist, and Tandem Diabetes Care launched Tandem Mobi Insulin Pump. |

|

Partnerships in Diabetes Care Devices |

Abbott, the leader in CGM with its FreeStyle Libre platform, is collaborating with Medtronic, a key player in insulin pumps. Sequel Med Tech and Senseonics announced a collaboration to create the first automated insulin delivery (AID) system featuring a one-year continuous glucose monitoring (CGM) sensor. |

|

Acquisitions in Diabetes Care Devices |

Novo Nordisk, the world's largest insulin manufacturer, acquired BIOCORP to enhance its portfolio of connected insulin pens. Abbott Acquires Bigfoot Biomedical, a developer of smart insulin management systems. |

|

Company Strategy |

Medtronic: Announced plans to separate its Diabetes business into an independent entity, aiming to enhance focus and agility in the evolving diabetes care market. Insulet Corporation: The company is working on new automated insulin delivery systems, including a next-generation hybrid closed-loop system and a fully closed-loop system, to further enhance diabetes management. |

|

Emerging Technology |

Closed-Loop/Artificial Pancreas Systems, Non-Invasive Glucose Monitoring, Wearable Biosensors and Multi-Analyte Devices, Digital Health & Mobile Integration, and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations in drug delivery devices are transforming treatment by enabling smarter, more personalized, and automated therapy management. Artificial intelligence is being integrated into connected insulin pumps, smart inhalers, wearable injectors, and infusion systems to analyze real-time patient data and optimize dosage adjustments. These systems use predictive analytics to forecast patient needs, reduce dosing errors, and improve adherence through reminders and behavioral tracking. AI algorithms can also detect usage patterns, identify potential complications, and provide decision-support insights to both patients and healthcare providers. Additionally, integration with mobile apps and cloud platforms allows remote monitoring, data sharing, and personalized treatment recommendations, enhancing safety, efficiency, and overall therapeutic outcomes.

U.S. Tariff Impact Analysis on Diabetes Care Devices Market:

U.S. tariffs have increasingly become an important factor influencing the economics of drug delivery and related medical device markets. Tariffs on imported medical devices and components can raise manufacturing and acquisition costs since many devices or parts are sourced through complex global supply chains; these added costs may either erode manufacturer margins or be passed on as higher prices for healthcare providers and patients. Higher import duties can also disrupt supply chains by making certain overseas suppliers less competitive, prompting companies to reassess sourcing strategies, diversify suppliers, or consider reshoring production to avoid tariff impacts. Although some recent tariff adjustments such as the U.S. reduction of tariffs on Indian medical device exports from 50% to 18% have improved cost competitiveness for products from select countries, broader tariff policies still pose cost pressures and uncertainty across the sector. Such tariff dynamics affect pricing strategies, supply availability, and long-term planning for manufacturers of drug delivery devices and other medical technologies.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends:

|

Company Name |

Total Funding |

Main Products |

Stage of Development |

Core Technology |

|

Luna Health |

$23.6 million |

Luna insulin patch pump |

Series A |

Automated insulin delivery for insulin pen users. |

Key takeaways from the Diabetes Care devices market report study

- Market size analysis for the current diabetes care devices market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the diabetes care devices market.

- Various opportunities available for the other competitors in the diabetes care devices market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current diabetes care devices market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the diabetes care devices market growth in the future?