-market-Goutieres-Syndrome.png&w=256&q=75)

Hematopoietic Stem Cell Transplantation Market

Hematopoietic Stem cell transplantation (HSCT) Insights and Trends

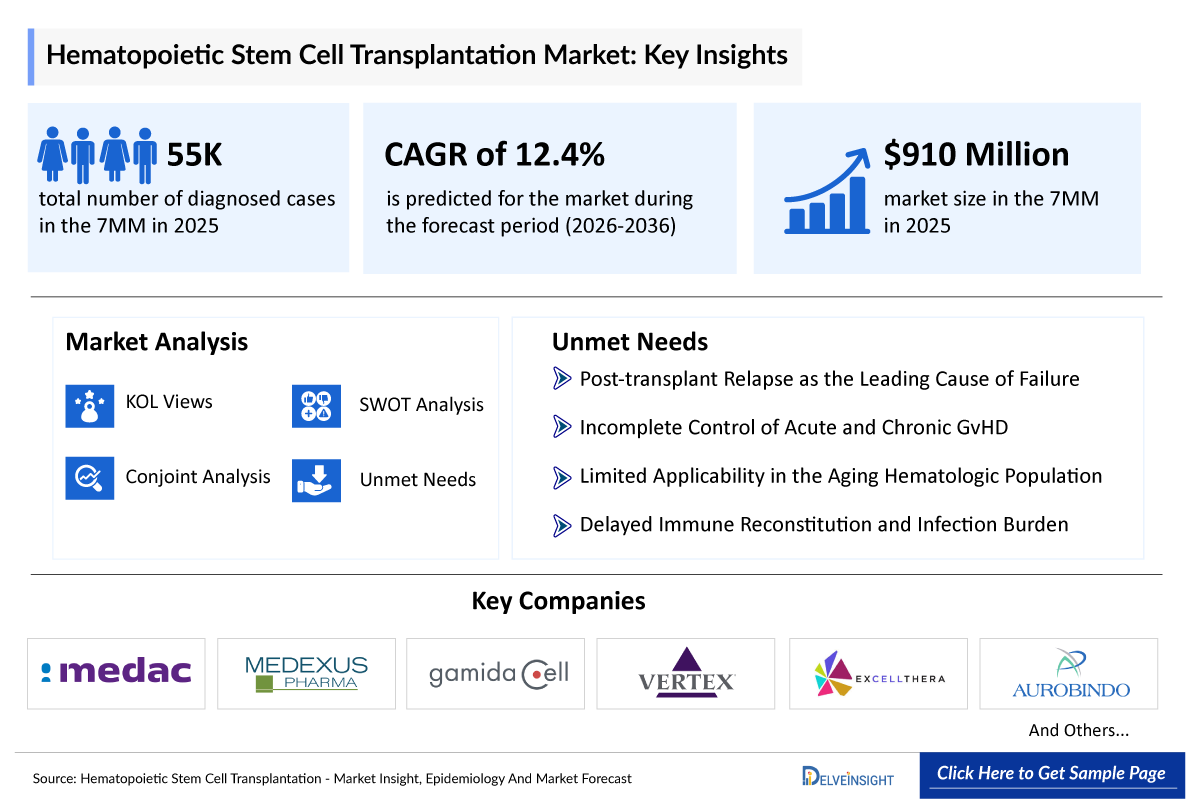

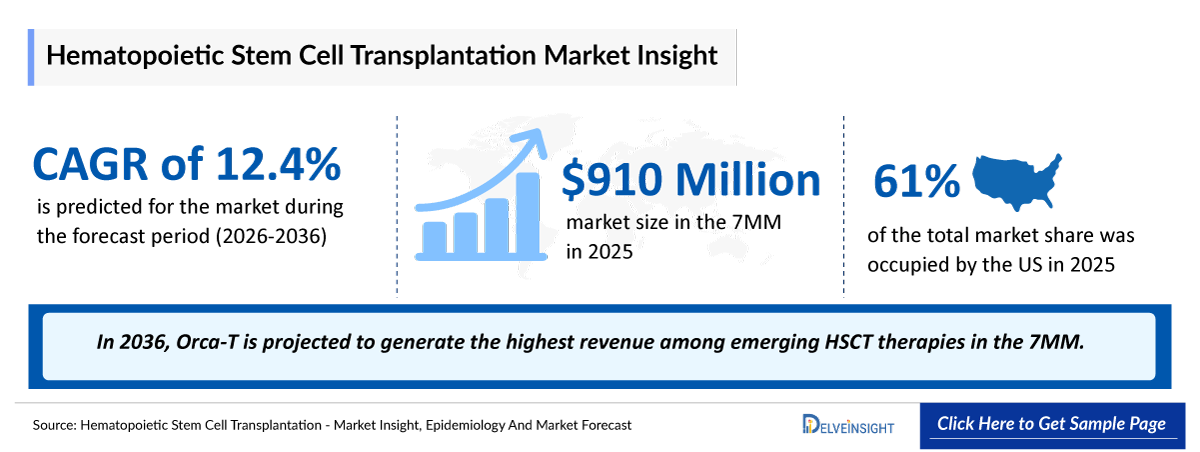

- According to DelveInsight’s analysis, the HSCT market across the 7MM was valued at USD 910 million in 2025, reflecting a growing clinical and commercial focus on advanced cellular therapies within the broader hematologic and oncologic landscape.

- According to DelveInsight’s analysis, the HSCT market in the US was valued at USD 555 million in 2025, reflecting a strong clinical and commercial focus on advanced cellular therapies within the country’s hematologic and oncologic landscape.

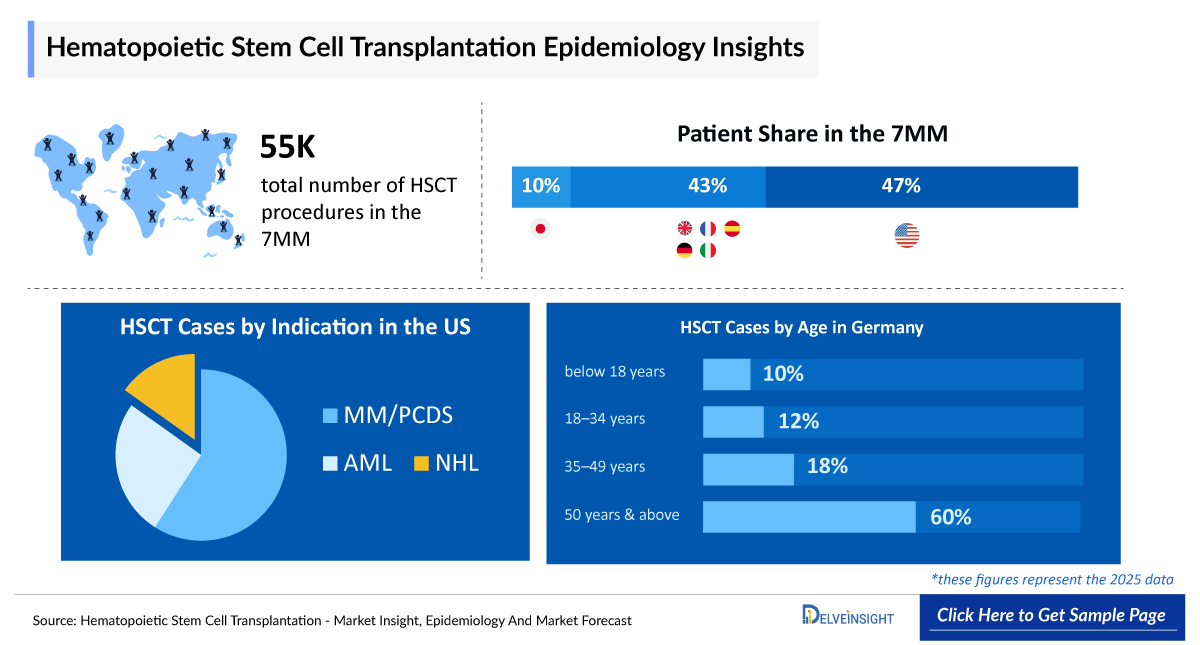

- In 2025, the total number of HSCT procedures across the 7MM was around 55,000 cases, distributed unevenly across regions. Among the 7MM countries, EU4 and the UK accounted for the highest share, contributing around 47%, followed by the US at approximately 43%, while Japan represented about 10% of the total in 2025.

- Current HSCT approaches rely on conditioning regimens and supportive pharmacologic interventions, with key products including Treosulfan (GRAFAPEX/TRECONDI), Omidubicel-onlv (OMISIRGE), Exagamglogene autotemcel (CASGEVY), UM171-expanded CD34+ dorocubicel (ZEMCELPRO), Motixafortide (APHEXDA), MABCAMPATH, and Anti-human thymocyte immunoglobulin (THYMOGLOBULIN). Despite these options, challenges such as graft failure and transplant-related complications persist, underscoring the need for more durable innovations in HSCT.

- The emergence of pipeline therapies such as OTL-203, Orca-T, Iomab-B (I-131-Apamistamab), and MaaT033 is reshaping the HSCT landscape by leveraging novel conditioning approaches, cell engineering, and microbiome-based strategies. These innovations are expected to expand therapeutic possibilities and drive continued evolution in HSCT.

- Significant gaps persist as relapse remains the primary cause of mortality in high-risk malignancies, often driven by pre-transplant MRD and immune escape mechanisms. Furthermore, acute and chronic GvHD continue to be dominant drivers of long-term morbidity, frequently requiring prolonged immunosuppression due to the lack of standardized maintenance protocols. There remains an urgent unmet need for therapies that improve durable remission while reliably preventing steroid-refractory complications.

Hematopoietic Stem cell transplantation (HSCT) Market size and forecast

- 2025 HSCT Market Size in the 7MM: USD 910 million

- 2036 Projected HSCT Market Size in the 7MM: USD 3 billion

- HSCT Growth Rate (2026–2036) in the 7MM: 12.4% CAGR

DelveInsight's ‘Hematopoietic Stem cell transplantation (HSCT)– Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of HSCT , historical and forecasted epidemiology, as well as the HSCT market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The HSCT market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates, HSCT patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment, and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in HSCT and maps the competitive and clinical landscape to uncover high-value opportunities, providing a clear outlook on future market growth potential.

Geography Covered

- North America: The United States

- Europe: Germany, France, Italy, and Spain and the UK

- Asia-Pacific: Japan

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

HSCT Market CAGR (Forecast period) |

12.4% (2022-2036) |

|

HSCT Epidemiology Segmentation Analysis |

Patient Burden Assesment

|

|

HSCT Companies |

|

|

HSCT Therapies |

and more. |

|

HSCT Market |

Segmented by

|

|

Analysis |

|

Hematopoietic Stem cell transplantation (HSCT) Understanding and Treatment Algorithm

HSCT Overview and Diagnosis

Hematopoietic stem cell transplantation (HSCT) is an advanced cellular therapy that restores hematopoiesis and immune function through stem cell infusion after conditioning therapy. It is used in hematologic malignancies and severe non-malignant disorders when conventional treatments fail to achieve durable disease control or cure. The HSCT approach is based on conditioning-driven disease eradication followed by stem cell engraftment, enabling regeneration of healthy blood and immune cells. Patient selection depends on disease risk, age, comorbidities, and transplant eligibility, as HSCT is an intensive procedure requiring specialized clinical management.

Autologous HSCT primarily supports dose-intensified chemotherapy using the patient’s own stem cells, offering lower immune complications and minimal graft-versus-host risk. In contrast, allogeneic HSCT uses donor stem cells and provides a graft-versus-disease effect, increasing curative potential but also introducing higher risks of immune toxicity, graft-versus-host disease, and long-term morbidity. Treatment pathways typically include stem cell mobilization and collection, conditioning regimens (myeloablative or reduced-intensity), stem cell infusion, and post-transplant immune management, with long-term monitoring focused on engraftment, relapse prevention, and immune recovery.

Further details are provided in the report.

Current HSCT Treatment Landscape

The overall HSCT landscape is evolving rapidly due to the advancement of next-generation conditioning platforms, engineered graft technologies, and gene-modified cellular therapies. Key innovations include reduced-toxicity conditioning agents such as treosulfan (GRAFAPEX/ TRECONDI), stem cell mobilization therapy motixafortide (APHEXDA), and immune-modulating agents like Alemtuzumab and Anti thymocyte globulin used to control transplant-related immune complications. In addition, engineered graft platforms such as Omidubicel-onlv (OMISIRGE), and UM171-expanded CD34 + dorocubicel (ZEMCELPRO) are improving engraftment and immune recovery. Collectively, these therapies- along with gene-edited approaches such as Exagamglogene autotemcel (CASGEVY) are expected to transform HSCT by improving safety, durability of response, and expanding transplant access for a broader patient population.

Further details related to country-based variations are provided in the report.

Hematopoietic Stem cell transplantation (HSCT) Unmet Needs

The section “unmet needs of HSCT” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Post-transplant Relapse as the Leading Cause of Failure

- Incomplete Control of Acute and Chronic GvHD

- Limited Applicability in the Aging Hematologic Population

- Delayed Immune Reconstitution and Infection Burden

- Long-term Toxicities and Secondary Malignancies

and others…..

Note: Comprehensive unmet needs insights in HSCT and their strategic implications are provided in the full report.

Hematopoietic Stem cell transplantation (HSCT) Epidemiology

Key Findings from HSCT Epidemiological Analysis and Forecast

- The total number of HSCT procedures in the 7MM was around 55,000 cases in 2025, reflecting a substantial clinical burden and the growing reliance on advanced transplant approaches for managing complex hematologic conditions across major markets.

- According to DelveInsight’s estimates, in 2025, in the US, HSCT procedures were distributed across a range of indications, led by MM/PCDS (Multiple Myeloma/Plasma Cell Diseases) with ~9,200 cases, followed by AML (Acute Myeloid Leukemia) with ~4,000 cases, NHL (Non-Hodgkin Lymphoma) and MDS/MPN (Myelodysplastic Syndromes/Myeloproliferative Neoplasms) with ~2,500 cases each, ALL (Acute Lymphoblastic Leukemia) with ~1,525 cases, HL (Hodgkin Lymphoma) with ~1,100 cases, Other Malignant with ~2,000 cases, and Non Malignant with more than 1,000 cases, reflecting the broad clinical application of HSCT across both malignant and non-malignant diseases.

- According to DelveInsight’s estimates, in 2025, in EU4 and the UK, HSCT procedures were categorized by transplant type, with autologous HSCT accounting for 15,000 cases and allogeneic HSCT comprising 11,500 cases, highlighting the utilization of both transplant approaches across the region.

- According to DelveInsight’s estimates, in 2025, in Germany, HSCT procedures by age were predominantly concentrated in older populations, with approximately more than 700 cases in patients below 18 years, around 850 cases in the 18–34 years group, nearly 1,280 cases in the 35–49 years group, and about 4,250 cases in those aged 50 years and above, reflecting higher utilization among older patients.

Hematopoietic Stem cell transplantation (HSCT) Drug Analysis & Competitive Landscape

The HSCT drug chapter provides a detailed, market-focused review of approved therapies and the emerging pipeline across Phase II clinical trials. It covers mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, strategic partnerships upcoming Key catalyst for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the HSCT treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the HSCT therapeutics market.

Approved Therapies for HSCT

Treosulfan (GRAFAPEX/ TRECONDI): Medac GmbH/ Medexus Pharma

Treosulfan (GRAFAPEX) for injection is an alkylating agent indicated in combination with fludarabine as a conditioning regimen prior to alloHSCT in adult and pediatric patients aged one year and older with AML or MDS. The therapy has received Orphan Drug Designation (ODD) under the Orphan Drug Act, granting seven years of regulatory exclusivity for the FDA-approved indication.

- In January 2025, the FDA approved GRAFAPEX (treosulfan) for injection, an alkylating agent, in combination with fludarabine as a preparative regimen for alloHSCT in adult and pediatric patients aged one year and older with AML or MDS, as reported by Medexus Pharma. Commercial availability was confirmed in February 2025.

- In February 2021, Medexus Pharmaceuticals and its US subsidiary, Medexus Pharma, entered into a commercialisation and supply agreement with Medac GmbH, granting Medexus Pharma an exclusive license to commercialise treosulfan, a bifunctional alkylating agent, in the United States for use in conditioning treatment prior to alloHSCT.

- In June 2019, the European Commission granted marketing authorization to Trecondi (treosulfan), an alkylating agent, in combination with fludarabine as a preparative regimen for alloHSCT in adult patients with AML or MDS.

|

HSCT Marketed/Approved Therapies | ||||||

|

Drug/Therapy |

Company |

Indication |

Molecule Type |

MoA |

RoA |

Marketed Region |

|

Treosulfan (GRAFAPEX/ TRECONDI) |

Medac GmbH/ Medexus Pharma |

AML, MDS |

Small molecule |

Alkylating agent |

IV |

US: 2025; EU: 2019 |

|

Omidubicel-onlv (OMISIRGE) |

Gamida Cell |

Hematologic malignancies severe aplastic anemia (SAA) |

Cell therapy |

Nicotinamide (NAM) technology |

IV |

US: 2023, 2025 |

|

Exagamglogene autotemcel (CASGEVY) |

Vertex Pharmaceuticals |

Sickle cell disease (SCD) in patients with recurrent vaso-occlusive crisis (VOCs) |

Stem cell therapy |

CRISPR/Cas9 gene editing |

IV |

US: 2023, 2024 ; UK: 2023 ; EU: 2024 |

|

Note: Detailed marketed therapies assessment will be provided in the final report. | ||||||

Hematopoietic Stem cell transplantation (HSCT) Pipeline Analysis

OTL-203: Orchard Therapeutics

OTL-203 is an investigational Phase III ex vivo autologous HSCT-based gene therapy for MPS-IH, designed to deliver sustained systemic and central nervous system enzyme expression after a single administration, aiming to address both somatic and neurocognitive manifestations while overcoming limitations of allogeneic HSCT.

- In July 2025, Orchard Therapeutics reported that the last patient had been treated in the registrational HURCULES trial, which is evaluating the efficacy and safety of OTL-203 in patients with mucopolysaccharidosis type I, MPS-IH, compared with the standard of care using allogeneic HSCT.

- In November 2023, Orchard Therapeutics reported that the US FDA granted Fast Track Designation (FTD) to OTL-203 for mucopolysaccharidosis type I, Hurler syndrome.

- In October 2023, Orchard Therapeutics reported interim outcomes from its proof-of-concept study of OTL-203 in mucopolysaccharidosis type I, Hurler syndrome (MPS-IH), presented at the European Society of Gene and Cell Therapy (ESGCT) 30th Annual Congress.

|

Competitive Landscape of Pipeline Drugs | ||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Anticipated Launch in the US |

|

OTL-203 |

Orchard Therapeutics |

III |

Mucopolysaccharidosis type I |

IV infusion |

Gene replacement |

2029 |

|

Orca-T |

Orca Biosystems |

III |

GvHD in patients with AML |

IV |

Cell therapy |

Information is available in the full report. |

|

Iomab-B (I-131 apamistamab) |

Actinium Pharmaceuticals |

III |

Relapsed or Refractory AML |

IV infusion |

Targeted radio immunotherapy |

Information is available in the full report. |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | ||||||

HSCT Key Players, Market Leaders and Emerging Companies

- Medac GmbH

- Medexus Pharma

- Gamida Cell

- Vertex Pharmaceuticals

- ExCellThera

- Ayrmid Pharma

- BioLineRx

- Orchard Therapeutics

- Orca Biosystems

- Bristol-Myers Squibb

- MaaT Pharma

- Actinium Pharmaceuticals

HSCT Drug Updates

- In December 2025, the FDA approved OMISIRGE for a second indication in Severe Aplastic Anemia, making it the first cellular therapy licensed for this condition and expanding use to patients aged 6 years and older following reduced intensity conditioning when a compatible donor is not available.

- Orca-T has a PDUFA date of April 6, 2026, as reported by Orca Bio, marking a key regulatory milestone that could support its potential approval and entry into the HSCT landscape.

- Orchard Therapeutics reported that the last patient was treated in the registrational HURCULES trial evaluating OTL-203 in MPS-IH versus allogeneic HSCT.

- Actinium Pharmaceuticals reported that it will present two abstracts at the AACR Annual Meeting 2026, scheduled for April 2026 in San Diego, California.

Hematopoietic Stem cell transplantation (HSCT) Market Outlook

Today’s HSCT paradigm delivers powerful disease control for a small, high-need population but depends on intensive conditioning, broad immune suppression, and prolonged supportive frameworks. This positions HSCT as a high-value yet high-burden platform, with future innovation expected to focus on safer conditioning, precision immune modulation, and faster functional recovery rather than incremental procedural refinement alone.

Key marketed therapies shaping current management

Treosulfan (GRAFAPEX/TRECONDI; Medexus Pharma): Reduced-toxicity conditioning agent enabling reliable myeloablation with improved safety, expanding HSCT eligibility.

- Dorocubicel (ZEMCELPRO; ExCellThera): UM171-expanded cord blood–derived CD34+ product enhancing engraftment and immune recovery in HSCT.

- Omidubicel-onlv (OMISIRGE; Gamida Cell): Nicotinamide-expanded cord blood product improving engraftment speed and immune reconstitution.

- Exagamglogene autotemcel (CASGEVY; Vertex/CRISPR Therapeutics): Gene-edited autologous HSCT therapy delivering curative potential without donor dependence.

- In the US, conditioning strategies for allogeneic HSCT remain heavily weighted toward myeloablative regimens, representing ~92% of reported use, driven by younger patients and aggressive or high-risk disease where higher toxicity is accepted to maximize disease control. Reduced-intensity or non-myeloablative conditioning is used in a small minority (~7%), largely in patients aged =50 years, those with multiple myeloma or chronic leukemia’s, or when minimizing transplant-related mortality takes precedence over intensive cytoreduction. Total body irradiation is frequently incorporated in acute lymphoid leukemia particularly in pediatric populations but is uncommon in other indications, highlighting a conditioning approach shaped primarily by age and disease biology.

Overall, the advancement of innovative cell therapies, improved transplant protocols, and increasing clinical adoption are expected to drive steady growth in the 7MM HSCT market from 2022–2036, with significant implications for both existing therapies and emerging pipeline products.

- Among the 7MM, the US accounted for the largest market size of HSCT. i.e., USD ~ 555 million in 2025.

- In 2036, Orca-T is projected to generate the highest revenue among emerging HSCT therapies in the 7MM.

- The most meaningful recent shift in HSCT has been the approval of advanced cell and gene-based therapies with improved efficacy profiles. Products such as OMISIRGE and CASGEVY have gained regulatory approval across key markets, offering enhanced engraftment, faster recovery, and reduced donor dependence, thereby reshaping the HSCT landscape.

Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in HSCT (2022–2036 Forecast)

The HSCT landscape comprises conditioning agents, graft sources, immunomodulators, mobilization agents, and gene-edited therapies, each addressing different aspects of the transplant process.

Conditioning agents: Used prior to HSCT to enable myeloablation and immune suppression. Agents such as treosulfan (GRAFAPEX/TRECONDI) offer effective conditioning with improved safety profiles, though toxicity and patient eligibility remain key considerations.

Cord blood–derived products: Advanced graft sources such as OMISIRGE and ZEMCELPRO enhance engraftment and immune recovery. While they address limitations of traditional cord blood transplantation, access and scalability can be challenges.

Immunomodulators: Agents like MABCAMPATH and THYMOGLOBULIN are used to reduce immune-mediated complications and support engraftment, though they may increase infection risk and delay immune reconstitution.

Mobilization agents: Products such as APHEXDA improve stem cell mobilization and collection efficiency, but variability in response and procedural complexity persist.

Gene-edited therapies: Innovative options like CASGEVY enable autologous, gene-modified HSCT approaches, reducing donor dependence and offering transformative potential, though long-term durability and accessibility remain under evaluation.

Hematopoietic Stem cell transplantation (HSCT) Drug Uptake

This section focuses on the uptake rate of potential therapies expected to enter the HSCT landscape during the forecast period (2026–2036). The analysis covers uptake dynamics, peak performance, key factors influencing adoption, and the anticipated contribution of each therapy to overall market growth.

Currently, HSCT utilization is driven by a combination of conditioning agents, graft sources, and supportive pharmacologic interventions. Conventional approaches, including conditioning regimens and immunomodulators such as THYMOGLOBULIN and MABCAMPATH, remain widely used, while advanced graft sources like OMISIRGE and ZEMCELPRO are gaining traction due to improved engraftment and recovery profiles. Mobilization agents such as APHEXDA and gene-edited therapies like CASGEVY are also contributing to evolving clinical adoption, though uptake varies based on accessibility, cost, and clinical outcomes.

The emergence of next-generation pipeline therapies, including OTL-203, Orca-T, and Iomab-B, is reshaping the HSCT landscape by introducing gene therapy, precision-engineered grafts, and targeted conditioning approaches. These innovations are expected to enhance transplant outcomes, expand eligibility, and drive sustained market growth, supporting long-term advancement and diversification within the HSCT space.

Detailed insights of emerging therapies' drug uptake is included in the report

Market Access and Reimbursement of Approved therapies in Hematopoietic Stem cell transplantation (HSCT)

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of approved therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

EU4 and the UK

|

EU4 and the UK Reimbursement of Therapies Approved for HSCT | |

|

AEMPS Assessment for HSCT Therapies | |

|

Drug Name |

Deduction |

|

TRECONDI 5 g |

4% |

Reimbursement is a crucial factor that affects the drug’s access to the market. Often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

NOTE: Further Details are provided in the final report….

Hematopoietic Stem cell transplantation (HSCT) therapies Price Scenario & Trends

Pricing and analogue assessment of HSCT therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, closest and most approproiate analogue selection for emerging therapies, and understanding of how pricing influences market access, adherence, and long-term uptake.

Pricing of Hematopoietic Stem cell transplantation (HSCT) Approved Drugs

Treosulfan (GRAFAPEX/TRECONDI) offers the CORE Connection program, which helps reduce administrative burden and accelerate patient access by supporting healthcare providers with insurance precertification, prior authorization, and denial appeals, including relevant documentation and medical necessity processes. The estimated treatment cost is approximately USD 31,500 in the US.

Industry Experts and Physician Views for Hematopoietic Stem cell transplantation (HSCT)

To keep up with HSCT market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry Experts were contacted for insights on the HSCT emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in HSCT, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 8+ KOLs to gather insights at country level. Centers such as the Memorial Sloan Kettering Cancer Center, University of California San Francisco, State University of New York Upstate Medical University, etc. were contacted.

Their opinion helps understand and validate current and emerging HSCT therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in HSCT.

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“HSCT plays a central consolidative role in pediatric patients with contemporarily defined high-risk AML in first complete remission. With modern risk stratification incorporating cytogenetic, molecular, and MRD features, HSCT is consistently associated with lower relapse rates and superior disease-free survival compared with chemotherapy alone. These data support HSCT as a key component of risk-adapted therapy in pediatric AML.” |

|

Germany |

“HSCT activity continues to expand, driven by rising use in AML in first complete remission, myeloproliferative neoplasms, and marrow failure, alongside declining use in CLL due to effective targeted therapies. Donor practices are shifting, with rapid adoption of haploidentical family donors offsetting slower growth in unrelated donor transplants and reduced reliance on cord blood.” |

Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of HSCT, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are majorly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Report

- The report covers a segment of key events, an executive summary, a descriptive overview of HSCT, explaining their causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the HSCT market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM HSCT market.

Report Insights

- HSCT Patient population forecast

- HSCT therapeutics market size

- HSCT pipeline analysis

- HSCT market size and trends

- HSCT market opportunity (Current and forecasted)

Report Key Strengths

- Epidemiology-based (Epi-based) bottom-up forecasting

- Artificial Intelligence (AI) - enabled market research report

- 11-year forecast

- HSCT market outlook (North America, Europe, Asia-Pacific)

- Patient Burden trends (by geography)

- HSCT Treatment addressable Market (TAM)

- HSCT Competitive Landscape

- HSCT major companies Insights

- HSCT Price trends and analogue assessment

- HSCT Therapies Drug Adoption/Uptake

- HSCT Therapies Peak Patient Share analysis

- Report Assessment

- HSCT Current treatment practices

- HSCT Unmet needs

- HSCT Clinical development Analysis

- HSCT emerging drugs product profiles

- HSCT Market attractiveness

- HSCT Qualitative analysis (SWOT and conjoint analysis)

FAQs

Market Insights

- What was the HSCT market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of HSCT?

- What are the disease risks, burdens, and unmet needs of HSCT? What will be the growth opportunities across the 7MM concerning the patient population with HSCT?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of HSCT? What are the current guidelines for treating HSCT in the US, Europe, and Japan?

Reasons to Buy

- The report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the HSCT market.

- Bottom up forecasting builds from the affected population to product forecasts, delivering a robust, data driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease prevalence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI) enabled report summarize and simplify complex datasets within the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data driven decisions.