-market.png&w=256&q=75)

IgA Nephropathy Market Summary

IgA Nephropathy (IgAN) Insights and Trends

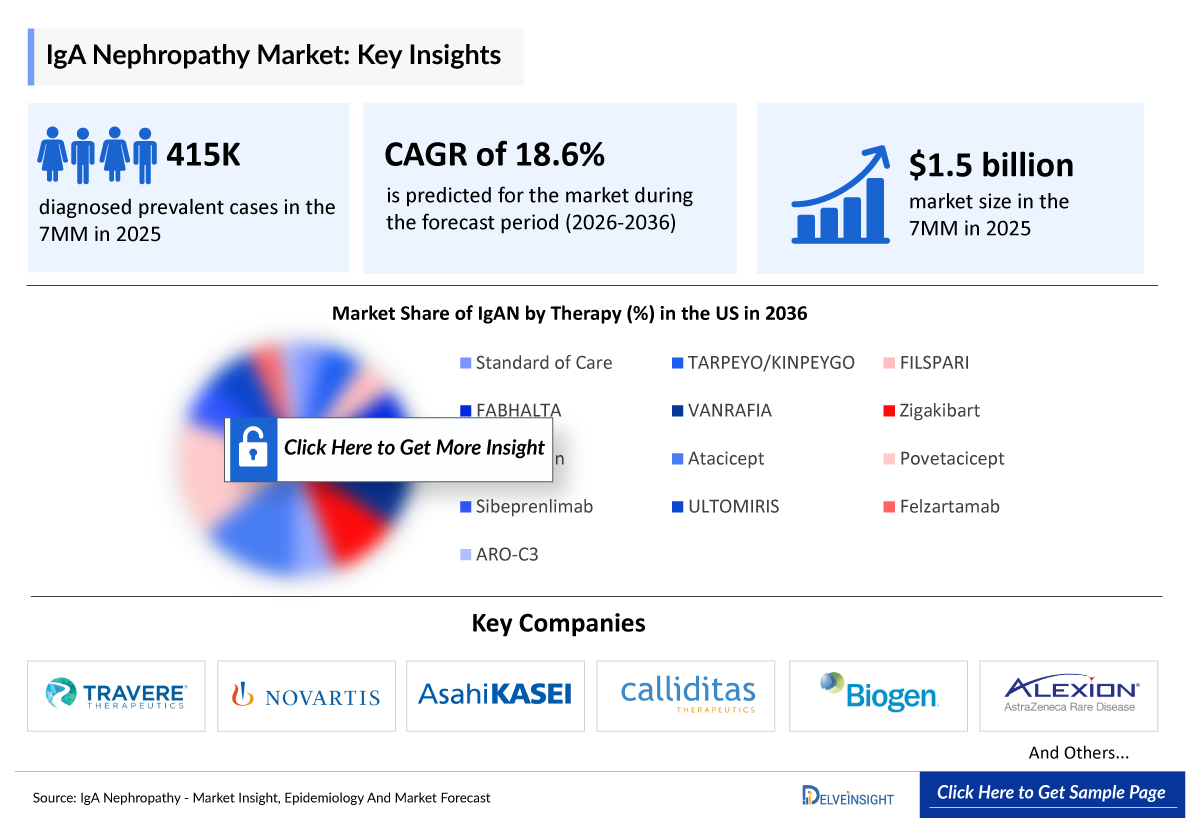

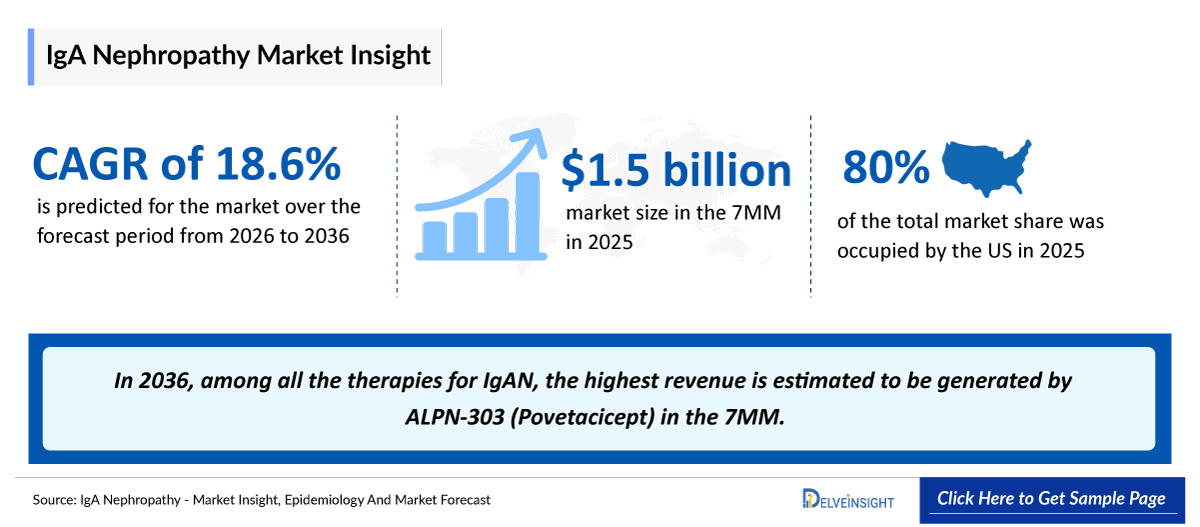

- According to DelveInsight’s analysis, IgA Nephropathy (IgAN) market size was found to be ~USD 1.5 billion in the leading markets (the United States, the EU4 (Germany, France, Italy, and Spain), the United Kingdom, and Japan) in 2025.

- IgAN reported approximately 135,000 diagnosed prevalent cases in the US. Improved diagnostic practices, greater disease awareness, and wider use of kidney biopsies is expected to drive the growing prevalence of IgAN.

- There is no cure for IgAN, and treatment focuses on reducing proteinuria, controlling blood pressure, and slowing disease progression. Standard therapies include ACEis, ARBs, and SGLT2 inhibitors, while newer approaches target underlying disease mechanisms, offering precision, disease-modifying strategies that go beyond supportive care and aim to improve long-term renal outcomes.

- The IgAN-approved drugs include iptacopan (FABHALTA), atrasentan (VANRAFIA), budesonide (TARPEYO/KINPEYGO), sparsentan (FILSPARI), and sibeprenlimab (VOYXACT). Among these, VOYXACT has recently received US FDA approval, providing a first-in-class APRIL-blocking therapy that offers a novel, disease-modifying option to reduce proteinuria and slow disease progression.

- The IgAN pipeline includes several late-stage therapies targeting key disease mechanisms. Major Phase III candidates include BAFF/APRIL dual inhibitors (povetacicept, atacicept), anti-CD38 antibodies (felzartamab, mezagitamab), complement inhibitors (ravulizumab, ARO-C3), anti-APRIL therapy (zigakibart), and the gene-silencing agent sefaxersen. These biologics, monoclonal antibodies, and RNA-based therapies aim to modify disease progression and expand treatment options beyond supportive care.

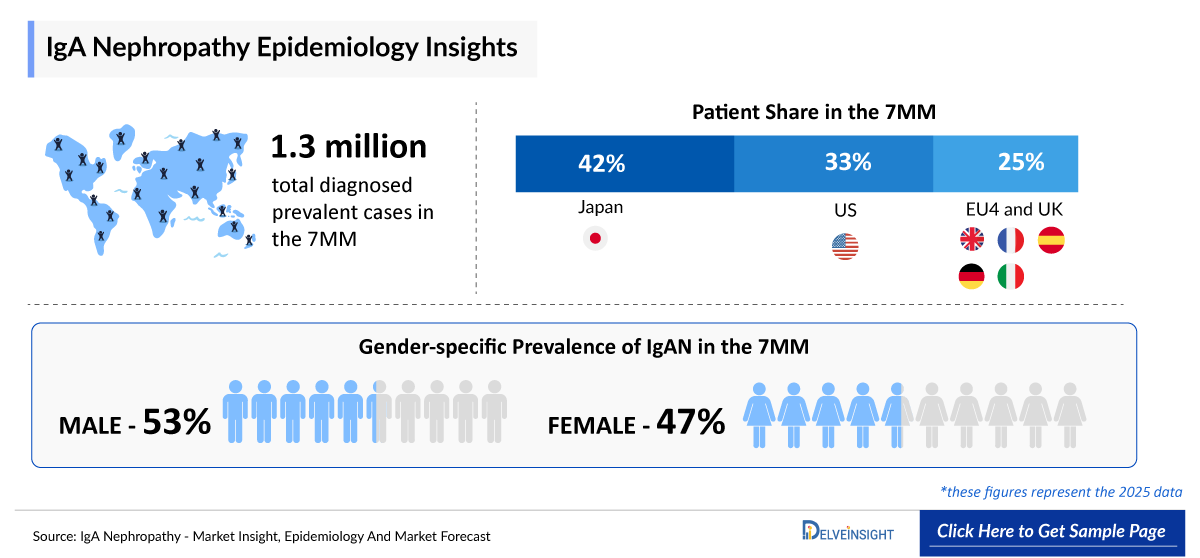

- IgAN is more prevalent in men than in women. In most studies, except for Japan and Brazil, IgAN was over-represented in male patients compared with female patients.

- Vera Therapeutics reported positive Phase III ORIGIN atacicept data in IgAN, presented at ASN Kidney Week 2025 and published in the New England Journal of Medicine.

- In June 2025, 100-week Phase I/II data for zigakibart presented at the ERA Congress showed sustained proteinuria remission, stable kidney function, and a favorable safety profile in patients with IgAN, supporting its continued clinical advancement.

- Heterogeneity in IgAN phenotypes and variable disease progression complicate patient stratification and therapy selection, often delaying initiation of optimal targeted treatments.

- The total IgAN market size is expected to expand over the forecast period. Growth is primarily driven by an increasing diagnosed and treated patient population across the 7MM, supported by earlier detection through routine urine screening, wider adoption of renal biopsy, and enhanced disease awareness—collectively contributing to a steady expansion of the addressable treatment pool.

IgAN Market size and forecast

- 2025 IgAN Market Size: USD 1.5 billion

- 2036 Projected IgAN Market Size: USD 11.6 billion

- IgAN Growth Rate (2026–2036): 18.6% CAGR

DelveInsight's ‘IgA Nephropathy (IgAN)– Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of IgAN, historical and forecasted epidemiology, as well as the IgAN market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The IgAN market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates, IgAN patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment, and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in IgAN and maps the competitive and clinical landscape to uncover high‑value opportunities, providing a clear outlook on future market growth potential.

Geography Covered

- North America: The United States ;

- Europe: Germany, France, Italy, Spain and the UK;

- Asia-Pacific: Japan

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2025 |

|

Geographies Covered |

|

|

IgAN Market CAGR (Study period/Forecast period) |

18.6% (2022-2036) |

|

IgAN Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

IgAN Companies |

And more |

|

IgAN Therapies |

and more |

|

IgAN Market |

Segmented by

|

|

Analysis |

|

IgAN Understanding and Treatment Algorithm

IgAN Overview and Diagnosis

IgAN also known as Berger disease is an autoimmune disease that attacks the kidneys and affects blood filtration in the kidneys’ small blood vessels. IgAN occurs when an abnormal protein damages the filtering unit (glomerulus) inside the kidneys. It is estimated that 20–40% of people with IgAN will develop ESKD, which means they will need dialysis or kidney transplantation to survive.

The diagnosis of IgAN relies entirely on a histopathologic evaluation of renal biopsy, demonstrating mesangial hypercellularity and predominant or co-dominant glomerular deposition of IgAN, usually with complement C3 and variable amounts of IgG and/or IgM.

Advancements in targeted therapies have broadened the therapeutic landscape. Sparsentan, a dual endothelin and angiotensin receptor antagonist, and targeted-release budesonide offer effective non-immunosuppressive options for patients with residual proteinuria. SGLT2 inhibitors, initially developed for diabetes, have demonstrated renal benefits in IgAN subgroups within broader Chronic Kidney Disease (CKD) trials. While mycophenolate shows promise in Asian populations, global efficacy remains uncertain. Other immunosuppressants, such as rituximab and calcineurin inhibitors, have shown limited benefit, and combination regimens with corticosteroids yield mixed results. Tonsillectomy remains a regionally applied adjunct in Japan. For patients progressing to end-stage renal disease, kidney transplantation remains viable, with relatively low recurrence-related graft loss.

Further details are provided in the report.

Current IgAN Treatment Landscape

The IgAN treatment pipeline appears robust, with several therapies expected to launch during the forecast period. These include ravulizumab (ULTOMIRIS), ARO-C3, Atacicept, Sefaxersen (RG6299; IONIS-FB-LRx), and others.

Long-term market growth will depend on payer recognition of clinical value, as reimbursement decisions increasingly rely on demonstrated reduction in proteinuria, delayed progression to end-stage kidney disease, and real-world safety outcomes.

Further details related to country-based variations are provided in the report.

IgAN Unmet Needs

The section “unmet needs of IgAN” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Delayed and complex diagnosis of IgAN

- Inadequate long-term solutions for high-risk groups

- Safer therapeutic alternatives with improved tolerability

- Integrated management of comorbidities in IgAN

and others…..

Note: Comprehensive unmet needs insights in IgAN and their strategic implications are provided in the full report.

IgAN Epidemiology

Key Findings from IgAN epidemiological Analysis and Forecast

- The total number of diagnosed prevalent cases of IgAN in the 7MM is ~415,000 in 2025.

- According to DelveInsight’s estimates, in 2025, the US reported nearly 135,000 diagnosed prevalent cases of IgAN.

- In 2025, IgAN diagnoses across Spain showed a gender disparity, with 67% of cases occurring in males and 33% in females, highlighting a greater susceptibility among women. Germany emerged as the leading contributor to the regional disease burden, recording the highest number of diagnosed cases in both sexes.

- The 18–45 years age group accounted for the highest number of IgAN cases in Japan, with nearly 70,000 diagnosed cases. This figure is projected to rise due to improved diagnostic recognition and evolving demographic trends.

- In 2025, individuals aged 18-45 years accounted for the largest share of diagnosed IgAN cases in EU4 and the UK, comprising 41% of the total across all age groups, followed by the 46–65 years cohort. In contrast, the <18 years age group represented the smallest proportion of the overall case burden.

IgAN Drug Analysis & Competitive Landscape

The IgAN drug chapter provides a detailed, market-focused review of approved therapies and the emerging pipeline across Phase I-III clinical trials. It covers mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, strategic partnerships upcoming Key catalyst for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the IgAN treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the IgAN therapeutics market.

Approved Therapies for IgAN

Budesonide (TARPEYO/KINPEYGO): Asahi Kasei (Calliditas Therapeutics)

Budesonide delayed-release capsules (TARPEYO) are a gut-targeted oral corticosteroid for primary IgAN, designed for targeted ileal release. By modulating mucosal immune responses and suppressing Gd-IgA1 production from Peyer’s patch B cells, the therapy significantly reduces proteinuria and helps stabilize kidney function, representing a disease-modifying approach that addresses the underlying immune dysregulation in IgAN.

In July 2024, Calliditas Therapeutics reported that its partner, Viatris Pharmaceutical, had initiated a Phase III clinical trial in Japan for NEFECON, marketed locally as VR-205, in Japanese patients diagnosed with IgAN, with the Phase III readout expected in 2026.

Note: Detailed marketed therapies assessment will be provided in the final report.

|

IgAN Marketed/Approved Therapies | ||||||

|

Drug/Therapy |

Company |

Indication |

Molecule Type |

MoA |

RoA |

Marketed Region |

|

(budesonide) (TARPEYO/KINPEYGO) |

Asahi Kasei/Calliditas Therapeutics |

IgAN |

Small molecule |

Glucocorticoid receptor agonists |

Oral |

US: 2021, 2023 EU: 2022, 2024 UK: 2023 |

|

(Sparsentan) (FILSPARI) |

Travere Therapeutics |

IgAN |

Small molecule |

ETAR antagonist, AT1R antagonist |

Oral |

US: 2023, 2024 EU: 2024 UK: 2025 |

IgAN Pipeline Analysis

Zigakibart (FUB523): Novartis

Zigakibart (FUB523; formerly BION-1301) is a subcutaneously administered monoclonal antibody that selectively targets APRIL, a key driver of pathogenic IgA production. The therapy is currently in Phase III clinical development for IgAN, with Novartis planning regulatory submissions in 2027.

In June 2025, 100-week Phase I/II data for zigakibart presented at the ERA Congress showed sustained proteinuria remission, stable kidney function, and a favorable safety profile in patients with IgAN, supporting its continued clinical advancement.

|

Competitive Landscape of Pipeline Drugs | ||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Anticipated Launch in the US |

|

FUB523; formerly known as BION-1301 (Zigakibart) |

Novartis |

III |

IgAN |

SC |

Anti-A proliferation inducing ligand (APRIL) |

Information is available in the full report |

|

ALPN-303 (Povetacicept) |

Vertex Pharmaceuticals |

III |

IgAN |

SC |

Dual antagonist of BAFF and APRIL |

Information is available in the full report |

|

MOR202 (Felzartamab) |

Biogen |

III |

IgAN |

IV |

Anti-CD38 |

2028 |

|

Atacicept |

Vera Therapeutics |

III |

IgAN |

SC |

B cell activating factor (BAFF) and APRIL dual inhibitor |

Information is available in the full report |

IgAN Key Players, Market Leaders and Emerging Companies

- Travere Therapeutics

- Otsuka Pharmaceutical/ PANTHERx Rare

- Novartis

- Vertex Pharmaceuticals

- Takeda Pharmaceutical

- and others

IgAN Drug Updates

- Renalys Pharma reported positive topline Phase III results for sparsentan in Japanese patients with IgAN, supporting efficacy and advancing the program toward regulatory submission in Japan.

- Takeda reported new data showing mezagitamab (TAK-079) achieved sustained preservation of kidney function through 18 months in patients with primary IgAN.

- PANTHERxRare Pharmacy was selected by Otsuka as the exclusive specialty pharmacy for VOYXACT, an APRIL blocker approved under accelerated approval to reduce proteinuria in adults with primary IgAN.

IgAN Market Outlook

The expanding IgAN market is driven by improved disease recognition among nephrologists, broader use of renal biopsy enabling earlier diagnosis, and growing focus on slowing progression to end-stage kidney disease. In parallel, the emergence of next-generation pipeline therapies—including povetacicept, atacicept, felzartamab, zigakibart, TAK-079, sefaxersen, ARO-C3, ULTOMIRIS and others—is broadening the therapeutic landscape by targeting diverse disease mechanisms, sustaining long-term market growth and treatment innovation.

Key marketed therapies shaping current management

VOYXACT (sibeprenlimab, Otsuka Pharmaceutical)

- Recently FDA-approved in November 2025, VOYXACT is an APRIL-blocking IgG2 monoclonal antibody.

- Mechanism: Neutralizes oligomeric APRIL, a key driver of IgA production, reducing pathogenic IgA deposition in the kidney.

- Clinical impact: Offers a disease-targeting, proteinuria-reducing therapy, representing the first major approval in the emerging APRIL-inhibition class.

TARPEYO/KINPEYGO (budesonide, Calliditas Therapeutics)

- FDA approval: December 2023; EU approval: July 2024; UK: June 2024.

- Mechanism: Glucocorticoid receptor agonists

- Key point: Targets a disease driver with minimal systemic steroid exposure, helping preserve kidney function.

FILSPARI (sparsentan, Travere Therapeutics)

- FDA full: September 2024; EU: April 2025

- Mechanism: ETAR antagonist; AT1R antagonist

- Clinical nuance: Boxed warnings for hepatotoxicity and teratogenicity necessitate REMS monitoring.

FABHALTA (iptacopan, Novartis)

- FDA approval: August 2024

- Mechanism: Complement Factor B inhibitors

- Clinical relevance: Offers an oral option for complement-mediated IgAN, though REMS is required due to infection risk.

And more…

In 2025, the total IgAN market size across the US was estimated at USD 1.2 billion. Driven by a projected CAGR of 16.1% during the forecast period (2026–2036), the market is anticipated to grow significantly, reaching USD 8.1 billion by 2036.

- Overall, the launch of first-in-class therapies, improved testing, and rising disease awareness are expected to drive steady growth in the 7MM IgAN market from 2022–2036, with strong commercial implications for both marketed products and emerging pipelines.

- Among the 7MM, the US accounted for the largest market size of IgAN. i.e., USD ~ 1.2 billion in 2025.

- In 2036, among all the therapies for IgAN, the highest revenue is estimated to be generated by ALPN-303 (Povetacicept) in the 7MM.

- The IgAN market is entering a pivotal decade (2026–2036), marked by a transition from conventional supportive care toward targeted, mechanism-based therapies. Recent approvals, led by VOYXACT, and a robust pipeline spanning APRIL/BAFF inhibition, anti-CD38 antibodies, and complement-targeted therapies, signal potentially disease-modifying impact, improved long-term renal outcomes, and more individualized management. Commercial success will hinge on clinical efficacy, chronic safety, payer adoption, and physician education to shorten diagnosis delays and optimize patient access.

Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in IgAN (2022–2036 Forecast)

Treatment today emphasizes optimized supportive care, aiming to slow disease progression, reduce proteinuria, and preserve renal function

RASB: ACE inhibitors and ARBs are first-line, recommended even in normotensive patients with proteinuria >0.5 g/day, with dose escalation to maximize benefit.

SGLT2 inhibitors: Provide additional renal protection, particularly in patients with persistent proteinuria.

Short-term corticosteroids: Used selectively to reduce IgA production, balancing efficacy against systemic side effects.

Immunosuppressive therapy: Reserved for high-risk or rapidly progressive patients; mycophenolate mofetil may benefit select populations, while cyclophosphamide is limited to severe crescentic disease.

Nonpharmacologic strategies: Lifestyle modification, sodium restriction, weight management, exercise, smoking cessation, protein intake moderation, statins for hyperlipidemia, and fluid management through diuretics. Rare interventions include tonsillectomy or plasma exchange for rapid progression.

IgAN Drug Uptake

This section focuses on the uptake rate of potential drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the IgAN drug’s uptake, performance at peak, factors affecting performance during prime years of growth, patient uptake by therapy, and anticipated sales generated by each drug.

Several emerging therapies are expected to reshape the IgA nephropathy (IgAN) treatment landscape. Povetacicept (Vertex Pharmaceuticals) and atacicept (Vera Therapeutics) neutralize BAFF and APRIL to suppress B-cell activity, while felzartamab from Biogen and mezagitamab from Takeda Pharmaceutical Company target CD38-positive plasma cells to reduce pathogenic IgA production. Other approaches include zigakibart (Novartis) targeting APRIL signaling, sefaxersen (Roche) suppressing hepatic IgA synthesis via RNA interference, and complement inhibitors such as ARO-C3 (Arrowhead Pharmaceuticals) and ULTOMIRIS (ravulizumab) from AstraZeneca. Collectively, these mechanisms reflect a shift toward disease-modifying strategies aimed at reducing proteinuria and slowing disease progression.

Collectively, marketed and advanced-stage pipeline therapies reflect a strong industry shift toward precision immunologic and complement-directed interventions in IgAN, offering multiple points of intervention across immune dysregulation, complement activation, and renal injury pathways. This expanding therapeutic landscape enables deeper proteinuria control, sustained renal preservation, and the potential to delay progression to end-stage kidney disease, and is expected to transform long-term disease management, improve patient outcomes, and redefine standards of care in the years ahead.

Detailed insights of emerging therapies' drug uptake is included in the report

Market Access and Reimbursement of Approved therapies in IgAN

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of approved therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

The United States

|

US Reimbursement of Therapies Approved for IgAN | |

|

Drug/Therapy |

Access Program |

|

FILSPARI |

|

Reimbursement is a crucial factor that affects the drug’s access to the market. Often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

NOTE: Further Details are provided in the final report….

IgAN therapies Price Scenario & Trends

Pricing and analogue assessment of IgAN therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, closest and most appropriate analogue selection for emerging therapies, and understanding of how pricing influences market access, adherence, and long-term uptake.

Pricing of IgAN Approved Drugs

Travere’s FILSPARI was granted conditional approval on February 17, 2023. FILSPARI has been set to have a list price is USD 9,900 per month, ~USD 120,000 annually. For the EU4, the annual therapy price was derived from the G-BA–listed price in Germany, estimated at EUR 56,639.97 per year. Based on this benchmark, an annual cost of USD 66,000 was assumed for the EU4. For the UK, an annual price of USD 55,000 was incorporated into the model, based on a list price of GBP 3,401 for a pack of 30 tablets (400 mg each). Standard regional price-adjustment ratios benchmarked to the US, and further refined through internal assumptions, were then applied, resulting in an estimated annual cost of USD 48,000 for Japan.

Industry Experts and Physician Views for IgAN

To keep up with IgAN market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry Experts were contacted for insights on the IgAN emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in IgAN, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 8+ KOLs to gather insights at country level. Centers such as the Stanford University Medical Center, Division of Nephrology and Rheumatology, RWTH Aachen University, Department of Nephrology, Sorbonne Université , Nephropathy Laboratories, etc. were contacted.

Their opinion helps understand and validate current and emerging IgAN therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in IgAN.

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“Even after a kidney transplant, disease recurrence is a risk because IgAN has a systemic immune component; circulating aberrant IgA can affect the new organ. The targeted approaches signify a paradigm change in IgAN. The traditional strategy was to preserve kidney structure and function with broad therapy. Now, we can and should impact the disease process more directly.” |

|

Germany |

“IgAN is recognized as the most common primary glomerulonephritis, yet its incidence and detection are influenced by biopsy practices and referral patterns. This epidemiologic observation highlights the need for more standardized screening to capture early disease stages.” |

Qualitative Analysis: SWOT and Conjoint Analysis

- We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

- In the SWOT analysis of IgAN, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

- Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

- The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are majorly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Report

- The report covers a segment of key events, an executive summary, a descriptive overview of IgAN, explaining their causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the IgAN market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM IgAN market.

Report Insights

- IgAN Patient population forecast

- IgAN therapeutics market size

- IgAN pipeline analysis

- IgAN market size and trends

- IgAN market opportunity (Current and forecasted)

Report Key Strengths

- Epidemiology‑based (Epi‑based) bottom‑up forecasting

- Artificial Intelligence (AI)-enabled market research report

- 11-year forecast

- IgAN market outlook (North America, Europe, Asia-Pacific)

- Patient Burden trends (by geography)

- IgAN Treatment addressable Market (TAM)

- IgAN Competitive Landscape

- IgAN major companies Insights

- IgAN Price trends and analogue assessment

- IgAN Therapies Drug Adoption/Uptake

- IgAN Therapies Peak Patient Share analysis

Report Assessment

- IgAN Current treatment practices

- IgAN Unmet needs

- IgAN Clinical development Analysis

- IgAN emerging drugs product profiles

- IgAN Market attractiveness

- IgAN Qualitative analysis (SWOT and conjoint analysis)

FAQs

Market Insights

- What was the IgAN market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of IgAN?

- What are the disease risks, burdens, and unmet needs of IgAN? What will be the growth opportunities across the 7MM concerning the patient population with IgAN?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of IgAN? What are the current guidelines for treating IgAN in the US, Europe, and Japan?

Reasons to Buy

- The report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the IgAN market.

- Bottom up forecasting builds from the affected population to product forecasts, delivering a robust, data driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI) enabled report summarize and simplify complex datasets within the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data driven decisions.