Injectable Drug Delivery Devices Market

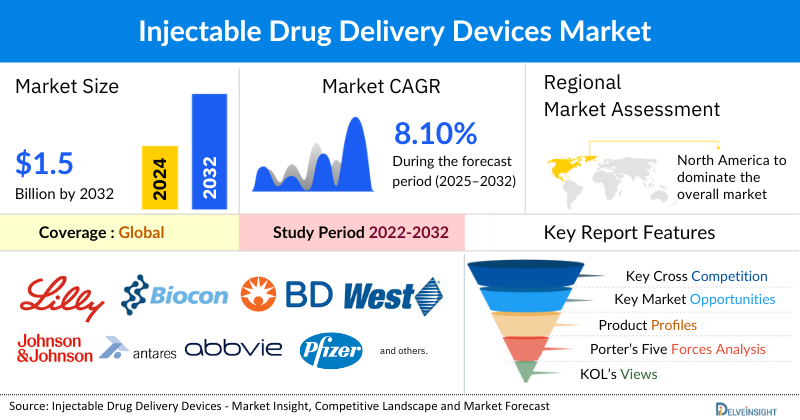

- The global injectable drug delivery devices market size is expected to increase from USD 570.77 billion in 2024 to USD 1,056.10 billion by 2032, reflecting strong and sustained growth.

- The global injectable drug delivery devices market is growing at a CAGR of 8.10% during the forecast period from 2025 to 2032.

- The global injectable drug delivery devices market is driven by the growing prevalence of chronic diseases, the rapid expansion of biologics and biosimilars requiring advanced delivery systems, and continuous innovations in smart injectors, wearable devices, and needle-free technologies that enhance patient compliance and treatment outcomes.

- The leading companies operating in the injectable drug delivery devices market include Eli Lilly and Company, Biocon, BD, West Pharmaceutical Services, Inc., Johnson & Johnson Services, Inc., Antares Pharma, AbbVie Inc., Pfizer Inc., Mylan N.V., Vetter Pharma-Fertigung GmbH & Co.KG, Emperra GmbH, Gerresheimer AG, SCHOTT AG, Terumo Corporation, Teva Pharmaceutical Industries Ltd., and others.

- The North America injectable drug delivery devices market is driven by the rising prevalence of chronic diseases such as diabetes, autoimmune disorders, and cancer, fueling demand for devices like autoinjectors, insulin pens, pre-filled syringes, and wearable injectors. Growth is further supported by technological innovation, patient-centric care, strong healthcare infrastructure, and favorable reimbursement policies.

- In the product type segment of the injectable drug delivery devices market, the insulin pens category is estimated to account for the largest market share in 2024.

Request for unlocking the report of the @ Injectable Drug Delivery Devices Market Forecast

Injectable Drug Delivery Devices Market Size and Forecasts

|

Report Metrics |

Details |

|

2024 Market Size |

USD 570.77 billion |

|

2032 Projected Market Size |

USD 1,056.10 billion |

|

Growth Rate (2025-2032) |

8.10% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Consolidated |

Factors Contributing to the Growth of the Injectable Drug Delivery Devices Market

- Growing prevalence of chronic disorders leading to a surge in the injectable drug delivery devices market: The rising incidence of chronic diseases such as diabetes, cancer, cardiovascular disorders, and autoimmune conditions is one of the strongest drivers of demand for injectable drug delivery devices. These conditions often require long-term or lifelong medication, much of which is administered through injections. With aging populations in developed regions and lifestyle-related health burdens increasing in emerging markets, the need for reliable, easy-to-use, and safe delivery systems is growing rapidly. Injectable devices such as insulin pens, autoinjectors, and wearable injectors are becoming essential for maintaining treatment adherence and improving quality of life. This trend is expected to continue as chronic diseases remain a leading healthcare challenge worldwide.

- Expansion of the biologics and biosimilars market: Biologics, including monoclonal antibodies, vaccines, and gene or cell therapies, have become critical in treating complex diseases that small-molecule drugs cannot address. Since most biologics are large molecules that cannot be taken orally, they must be delivered via injections, fueling the demand for advanced delivery devices. At the same time, the growing pipeline of biosimilars is making biologic therapies more affordable and accessible, further increasing their use across therapeutic areas. This expansion has created significant opportunities for innovative injectable platforms such as prefilled syringes and autoinjectors tailored for high-viscosity biologics. As biologics gain dominance in pharmaceutical pipelines, device manufacturers are aligning strategies to support safe, effective, and patient-friendly delivery solutions.

- Rising innovation and technological advancements among the key market players: The injectable drug delivery devices market is experiencing rapid innovation, with new technologies transforming how patients and healthcare providers manage treatments. Smart injectors equipped with sensors and connectivity features now allow real-time dose tracking, adherence monitoring, and integration with mobile health platforms. Wearable injectors capable of delivering large volumes subcutaneously are addressing the challenges of complex biologics, while needle-free injectors and microneedle systems are improving patient comfort. Additionally, advances in materials such as biocompatible plastics and biodegradable polymers are enhancing safety and sustainability. These technological advancements are not only improving treatment outcomes but also shaping the future of patient-centric, digitally connected healthcare.

Injectable Drug Delivery Devices Market Report Segmentation

This injectable drug delivery devices market report offers a comprehensive overview of the global Injectable Drug Delivery Devices market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation Injectable Drug Delivery Devices Market by Product Type (Self-injectors, Needle-free Injectors, Auto-Injectors, Wearable Injectors, and Insulin Pens), Drug Loading (Pre-filled Devices and Fillable Devices), Reusability (Reusable Devices and Disposable Devices), On-Site Delivery (Intramuscular, Intradermal, and Subcutaneous), End-User (Hospitals, Specialty Clinics, and Home Care Settings), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing injectable drug delivery devices market.

The injectable drug delivery devices are medical tools and systems specifically designed to administer drugs into the body through various injection routes such as subcutaneous, intramuscular, or intravenous delivery. These devices include a wide range of products such as syringes, prefilled syringes, safety syringes, autoinjectors, pen injectors, needle-free injectors, and wearable injectors. Their primary role is to ensure accurate dosing, maintain sterility, and enhance patient safety while improving convenience and compliance in both clinical and home-care settings. With the growing use of biologics, vaccines, and long-term therapies for chronic diseases, injectable drug delivery devices have become essential in modern healthcare by bridging pharmaceutical formulations with safe, effective, and user-friendly administration methods.

The injectable drug delivery devices market is witnessing steady growth, propelled by several influential factors. The growing prevalence of chronic disorders such as diabetes, cancer, and autoimmune conditions has significantly increased the demand for reliable and user-friendly injectable systems that support long-term treatment adherence. At the same time, the rapid expansion of the biologics and biosimilars market is fueling the adoption of advanced delivery platforms, as most biologics require injection-based administration for efficacy. This trend is further supported by rising innovations and technological advancements, including the development of smart connected injectors, wearable large-volume devices, and needle-free technologies designed to enhance patient comfort and safety. Together, these factors are reshaping the landscape of drug administration, positioning injectable delivery devices as a critical enabler of modern therapies and accelerating their adoption worldwide.

Get More Insights into the Report @ Injectable Drug Delivery Devices Market Trends

What are the latest Injectable Drug Delivery Devices Market Dynamics and Trends?

The injectable drug delivery devices market is undergoing a significant transformation, driven by evolving healthcare needs and rapid technological advancements. A major factor shaping this growth is the rising demand for patient-friendly solutions, as the prevalence of chronic conditions such as diabetes, cancer, and autoimmune disorders continues to climb. This trend has fueled sustained reliance on self-administration devices, including autoinjectors, pen injectors, and wearable pumps.

According to DelveInsight, approximately 537.5 million adults aged 20–79 were living with diabetes, representing roughly one in ten individuals. This number is projected to rise to 643 million by 2030 and 783.5 million by 2045, with over 75% of adults with diabetes residing in low- and middle-income countries. In addition, around 13.5 million people worldwide are affected by rheumatoid arthritis, while multiple sclerosis (MS) impacts over 2 million individuals globally, affecting cognitive, emotional, motor, sensory, and visual functions.

The expansion of biologics and biosimilars is another key driver, as these therapies necessitate specialized delivery systems capable of handling high-viscosity and large-volume formulations. Concurrently, technological innovations are reshaping the market, with connected and smart injectors enabling real-time monitoring, data integration, and improved patient adherence. Sustainability is increasingly influencing the industry, prompting manufacturers to adopt eco-friendly materials and reusable designs in response to regulatory requirements and environmental goals.

Strategic collaborations between pharmaceutical companies and device manufacturers are further accelerating the development of integrated drug-device solutions, enhancing both therapeutic outcomes and the patient experience. Collectively, these factors are not only fueling market growth but also steering the injectable drug delivery devices sector toward a more patient-centric, digitally enabled, and sustainable future.

Consequently, these trends are expected to drive robust growth in the injectable drug delivery devices market throughout the forecast period from 2025 to 2032.

Despite the growing demand for injectable drug delivery devices, the market faces notable challenges that could hinder its growth. One key restraint is the stringent regulatory approval process, as injectable devices are often classified as combination products and must undergo rigorous testing to ensure safety, efficacy, and compatibility with the drug, leading to longer timelines and higher development costs. Another concern arises from certain side effects associated with the use of nanoparticles in advanced drug delivery systems, which may trigger toxicity, immune responses, or other unforeseen complications, thereby raising safety concerns among patients and regulators. These factors collectively create hurdles for manufacturers, slowing down innovation and market entry while shaping the competitive dynamics of the industry.

Injectable Drug Delivery Devices Market Segment Analysis

Product Type (Self-injectors, Needle-free Injectors, Auto-Injectors, Wearable Injectors, and Insulin Pens), Drug Loading (Pre-filled Devices and Fillable Devices), Reusability (Reusable Devices and Disposable Devices), On-Site Delivery (Intramuscular, Intradermal, and Subcutaneous), End-User (Hospitals, Specialty Clinics, and Home Care Settings), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product Type: Insulin Pens Category Dominates the Market

The insulin pens category is the dominant force in the injectable drug delivery devices market. In 2024, insulin pens accounted for a significant share of approximately 35%. The insulin pen segment is a dominant force in the injectable drug delivery devices market due to its convenience, accuracy, and ability to improve patient adherence in managing diabetes. Unlike traditional vial-and-syringe methods, insulin pens are compact, prefilled, and easy to use. They allow patients to administer insulin independently with minimal training and significantly reduce the risk of dosing errors. These features make insulin pens especially beneficial for elderly patients, children, and individuals who require multiple daily injections.

The segment’s leadership is strengthened by well-established products such as Novo Nordisk’s NovoPen series, Sanofi’s SoloStar, and Eli Lilly’s KwikPen. These devices are known for their precision, reliability, and ergonomic design. Some models also include advanced features like adjustable dosing, memory functions, and connectivity options, which help patients monitor their treatment more effectively and maintain adherence.

The rising prevalence of diabetes worldwide, combined with increasing awareness of self-management and the growing focus on patient-centric care, has made insulin pens the preferred choice for millions of people. Their ease of use, safety, and ability to enhance quality of life continue to drive growth in the injectable drug delivery devices market, establishing insulin pens as a cornerstone of this industry.

By Drug Loading: Pre-filled Devices Dominate the Market

The prefilled devices category is the dominant force in the injectable drug delivery devices market. In 2024, prefilled devices accounted for a significant share of approximately 67%. The pre-filled injectable devices segment has established itself as a key growth driver in the injectable drug delivery devices market, owing to its convenience, safety, and efficiency in administering a wide range of therapies. These devices come preloaded with a fixed dose of medication, eliminating the need for manual preparation and significantly reducing the risk of dosing errors, contamination, or needle-stick injuries. Their ease of use makes them particularly suitable for patients requiring long-term or self-administered treatments, such as biologics for autoimmune disorders, monoclonal antibodies, and hormone therapies.

Prominent products in this segment, such as BD Ultra-Fine™ prefilled syringes, Sanofi’s prefilled Lantus® SoloStar®, and Amgen’s prefilled Neulasta® devices, are designed for accuracy, reliability, and patient comfort. Features like ergonomic design, clear dosing indicators, and safety-engineered needles enhance the user experience, making pre-filled devices a preferred choice for both healthcare professionals and patients.

The rising prevalence of chronic conditions, including rheumatoid arthritis, multiple sclerosis, and diabetes, combined with increasing demand for self-administration, adherence support, and patient-centric care, has propelled the widespread adoption of pre-filled injectables. Thus, this segment continues to play a crucial role in driving innovation and growth in the injectable drug delivery devices market, offering both clinical and practical advantages over traditional administration methods.

By Reusability: Disposable Devices Dominate the Market

The disposable devices category is the dominant force in the injectable drug delivery devices market. In 2024, disposable devices accounted for a significant share of approximately 60%. The disposable injectable devices segment is a significant contributor to the growth of the injectable drug delivery devices market, primarily due to its focus on safety, convenience, and cost-effectiveness. Designed for single-use applications, these devices minimize the risk of contamination and cross-infection, making them particularly suitable for both hospital and home settings. Their pre-assembled, ready-to-use format eliminates the need for complex preparation, reducing administration errors and streamlining the overall treatment process.

Leading products in this category include BD SafetyGlide™ disposable syringes, Ypsomed’s UnoPen® disposable devices, and Owen Mumford’s Autopen® disposable injectors, which are engineered to ensure precision, patient comfort, and safety. Many of these devices incorporate safety features such as retractable needles or auto-disable mechanisms, aligning with stringent regulatory standards and enhancing user confidence.

The growing prevalence of chronic diseases, the increasing adoption of self-administered therapies, and the emphasis on infection control and patient safety are key factors driving the demand for disposable injectable devices. Additionally, the rising trend toward short-term treatment regimens and the expansion of biologics and vaccines further bolster this segment. Collectively, disposable devices are recognized not only for their clinical reliability but also for their ability to improve patient adherence, convenience, and overall treatment outcomes, cementing their position as a vital component of the injectable drug delivery devices market.

By On-Site Delivery: Subcutaneous Dominates the Market

In the injectable drug delivery devices market, the subcutaneous category held the largest market share, capturing nearly 39% of the global market in 2024. The subcutaneous injectable devices segment has become a vital part of the injectable drug delivery devices market, driven by the increasing adoption of self-administered therapies for chronic conditions such as diabetes, autoimmune disorders, and cancer. These devices are designed to deliver medication beneath the skin, enabling rapid absorption while minimizing discomfort, making them highly suitable for frequent dosing and long-term treatment regimens. Their user-friendly design allows patients to administer therapy at home, reducing hospital visits and improving overall treatment adherence.

Leading products in this category include BD’s Sub-Q™ Safety Plus, Ypsomed’s YpsoMate®, and Sanofi’s prefilled subcutaneous Lantus® SoloStar®, which are engineered for precision, ease of use, and patient comfort. Many devices incorporate features such as dose-lock mechanisms, ergonomic grips, and safety-engineered needles to enhance safety and convenience, particularly for elderly patients or those with limited dexterity.

The growing prevalence of chronic diseases, the expanding pipeline of biologics requiring subcutaneous administration, and the emphasis on patient-centric care are key factors propelling the adoption of subcutaneous injectable devices. By facilitating safe, accurate, and convenient self-administration, these devices not only improve therapeutic outcomes but also support better patient engagement and adherence, establishing them as a critical segment of the global injectable drug delivery devices market.

By End-User: Hospitals Dominate the Market

The hospitals category represents a critical application area for injectable drug delivery devices, driven by the need for safe, precise, and high-volume medication administration in clinical settings. Hospitals serve as primary sites for delivering complex therapies, including biologics, chemotherapy, vaccines, and critical care medications, where accuracy, sterility, and patient safety are of utmost importance. Injectable devices in hospitals range from conventional syringes to advanced autoinjectors, infusion systems, and safety-engineered devices designed to minimize errors and prevent needlestick injuries among healthcare professionals.

The increasing prevalence of chronic diseases, rising hospital admissions, and the expanding use of injectable biologics and specialty drugs are key factors propelling growth in this segment. Additionally, the adoption of advanced, safety-focused, and automated delivery systems is improving operational efficiency and patient outcomes in healthcare facilities worldwide. Consequently, the hospital segment remains a cornerstone of the injectable drug delivery devices market, highlighting the critical role of these devices in modern clinical care.

Injectable Drug Delivery Devices Market Regional Analysis

North America Injectable Drug Delivery Devices Market Trends

North America, led by the United States, dominates the global injectable drug delivery devices market, accounting for approximately 43% of the total market share in 2024. The North America injectable drug delivery devices market is marked by rapid technological innovation, increasing adoption of self-administered therapies, and a strong emphasis on patient-centric care. The region benefits from a well-established healthcare infrastructure, favorable reimbursement policies, and high awareness among patients and healthcare providers regarding advanced drug delivery solutions. Key trends driving market growth include the rising prevalence of chronic diseases such as diabetes, autoimmune disorders, and cancer, which continue to sustain demand for devices like autoinjectors, insulin pens, pre-filled syringes, and wearable injectors.

According to DelveInsight analysis (2024), in the United States, approximately 38.4 million people of all ages, approximately 11.6% of the population, are affected by diabetes. Among adults aged 18 years and older, 38.1 million (14.7%) are affected. Additionally, 8.7 million adults who meet the laboratory criteria for diabetes are either unaware of or do not report having the disease, representing 3.4% of all U.S. adults and 22.8% of adults with diabetes. Diabetes prevalence rises with age, reaching 29.2% among individuals aged 65 and older. Furthermore, over 8.5 million people in the U.S. are diagnosed with psoriasis, with roughly 30% of these individuals developing psoriatic arthritis.

Regulatory approvals and product development strategies in the region have also significantly bolstered market growth. For instance, U.S. FDA approval for the supplemental Biologics License Application for Xolair® (omalizumab) prefilled syringes, enabling self-injection across all approved U.S. indications. Additionally, ongoing product launches and strategic initiatives by market players targeting North America are expected to further propel market expansion.

Collectively, the combination of technological advancements, high disease prevalence, supportive regulatory frameworks, and focused product development is creating a highly conducive environment for growth in the North America injectable drug delivery devices market, with robust expansion anticipated during the forecast period from 2025 to 2032.

Europe Injectable Drug Delivery Devices Market Trends

The Europe injectable drug delivery devices market is witnessing steady growth, driven by the rising prevalence of chronic diseases such as diabetes, cancer, and autoimmune disorders, along with the region’s strong focus on biologics and biosimilars. European healthcare systems place a high emphasis on patient safety and treatment adherence, which is fueling the adoption of advanced devices such as autoinjectors, wearable injectors, and safety-engineered syringes. Regulatory support from agencies like the EMA has further encouraged the development and approval of innovative combination products that integrate drugs with delivery devices.

Additionally, increasing investment in digital health and the integration of connected injectors with mobile health platforms are supporting the shift toward home-based care, reducing the burden on hospitals and improving patient convenience. Sustainability is also becoming a key trend in Europe, with manufacturers prioritizing eco-friendly materials and reusable designs in response to environmental regulations and healthcare providers’ growing preference for green solutions. Together, these trends position Europe as a progressive market where innovation, patient-centric design, and regulatory alignment are shaping the future of injectable drug delivery.

Asia-Pacific Injectable Drug Delivery Devices Market Trends

The Asia-Pacific injectable drug delivery devices market is witnessing rapid expansion, reflecting a robust CAGR of 9.4% during the forecast period from 2025 to 2032, driven by rising healthcare expenditure, expanding access to advanced therapies, and a growing burden of chronic diseases such as diabetes, cancer, and autoimmune disorders. Countries like China, India, and Japan are at the forefront, with large patient populations fueling strong demand for insulin pens, autoinjectors, and prefilled syringes. Increasing adoption of biologics and biosimilars in the region is further accelerating the shift toward advanced injectable platforms that ensure safety, accuracy, and patient convenience. Local manufacturing initiatives and government support for cost-effective drug delivery solutions are also strengthening market penetration, particularly in price-sensitive markets.

Moreover, global players are forging strategic partnerships with regional firms to expand distribution networks and adapt devices to local needs, while domestic companies are increasingly investing in innovation to compete with international brands. Alongside affordability, growing interest in connected health technologies and wearable injectors is shaping future adoption patterns, positioning Asia-Pacific as one of the fastest-growing and most dynamic regions in the injectable drug delivery devices market.

Who are the major players in the Injectable Drug Delivery Devices Market?

The following are the leading companies in the injectable drug delivery devices market. These companies collectively hold the largest market share and dictate industry trends.

- Eli Lilly and Company

- Biocon

- BD

- West Pharmaceutical Services, Inc.

- Johnson & Johnson Services, Inc.

- Antares Pharma

- AbbVie Inc

- Pfizer Inc.

- Mylan N.V.

- Vetter Pharma-Fertigung GmbH & Co.KG

- Emperra GmbH

- Gerresheimer AG

- SCHOTT AG

- Terumo Corporation

- Teva Pharmaceutical Industries Ltd.

How is the competitive landscape shaping the Injectable Drug Delivery Devices Market?

The competitive landscape of the injectable drug delivery devices market is evolving rapidly, shaped by a mix of established multinational corporations and emerging innovators. The market is moderately concentrated, with a few leading players such as BD, West Pharmaceutical Services, and Gerresheimer holding significant market shares due to their broad product portfolios, global distribution networks, and strong regulatory expertise. These companies dominate areas like prefilled syringes, safety devices, autoinjectors, and connected insulin delivery systems, leveraging their scale and R&D capabilities to maintain leadership.

At the same time, smaller and mid-sized firms, particularly startups such as Enable Injections, Portal Instruments, and Crossject, are driving niche innovation with wearable injectors, needle-free devices, and AI-enabled smart injectors. Strategic collaborations between pharmaceutical companies and device manufacturers are becoming increasingly common, as drug developers seek to integrate delivery systems into their therapeutic offerings to enhance patient adherence and differentiate biologics and biosimilars. Partnerships focusing on digital health integration, sustainability, and patient-centric design are further intensifying competition.

Thus, the moderately concentrated nature of the market creates a balance: established players provide stability and large-scale capacity, while agile innovators push the boundaries of technology. This dynamic competition is accelerating product launches, regulatory approvals, and investments in next-generation delivery systems, positioning the market for sustained growth while keeping barriers high for new entrants.

|

Report Metrics |

Details |

|

Study Period |

2022 to 2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2032 |

|

Injectable Drug Delivery Devices Market CAGR |

8.10% |

|

Key Companies in the Injectable Drug Delivery Devices Market |

Eli Lilly and Company, Biocon, BD, West Pharmaceutical Services, Inc., Johnson & Johnson Services, Inc., Antares Pharma, AbbVie Inc., Pfizer Inc., Mylan N.V., Vetter Pharma-Fertigung GmbH & Co.KG, Emperra GmbH, Gerresheimer AG, SCHOTT AG, Terumo Corporation, Teva Pharmaceutical Industries Ltd., and others |

|

Injectable Drug Delivery Devices Market Segments |

by Product Type, by Drug Loading, by Reusability, by On-Site Delivery, by End-User, and by Geography |

|

Injectable Drug Delivery Devices Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Injectable Drug Delivery Devices Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Injectable Drug Delivery Devices Market Segmentation

Injectable Drug Delivery Devices by Product Type Exposure

- Self-injectors

- Needle-free Injectors

- Auto-Injectors

- Wearable Injectors

- Insulin Pens

Injectable Drug Delivery Devices by Drug Loading Exposure

- Pre-filled Devices

- Fillable Devices

Injectable Drug Delivery Devices by Reusability Exposure

- Reusable Devices

- Disposable Devices

Injectable Drug Delivery Devices by On-Site Delivery Exposure

- Intramuscular

- Intradermal

- Subcutaneous

Injectable Drug Delivery Devices End-User Exposure

- Hospitals

- Specialty Clinics

- Home care settings

Injectable Drug Delivery Devices Geography Exposure

- North America Injectable Drug Delivery Devices Market

- United States Injectable Drug Delivery Devices Market

- Canada Injectable Drug Delivery Devices Market

- Mexico Injectable Drug Delivery Devices Market

- Europe Injectable Drug Delivery Devices Market

- United Kingdom Injectable Drug Delivery Devices Market

- Germany Injectable Drug Delivery Devices Market

- France Injectable Drug Delivery Devices Market

- Italy Injectable Drug Delivery Devices Market

- Spain Injectable Drug Delivery Devices Market

- Rest of Europe Injectable Drug Delivery Devices Market

- Asia-Pacific Injectable Drug Delivery Devices Market

- China Injectable Drug Delivery Devices Market

- Japan Injectable Drug Delivery Devices Market

- India Injectable Drug Delivery Devices Market

- Australia Injectable Drug Delivery Devices Market

- South Korea Injectable Drug Delivery Devices Market

- Rest of Asia-Pacific Injectable Drug Delivery Devices Market

- Rest of the World Injectable Drug Delivery Devices Market

- South America Injectable Drug Delivery Devices Market

- Middle East Injectable Drug Delivery Devices Market

- Africa Injectable Drug Delivery Devices Market

Injectable Drug Delivery Devices Market Recent Industry Trends and Milestones (2022-2025)

|

Category |

Key Developments |

|

Injectable Drug Delivery Devices Product Launches |

Becton Dickinson (BD) launched the NOVA™ prefillable syringe platform designed for advanced biologics; West Pharmaceutical unveiled smart connected drug delivery platforms to support patient adherence. |

|

Injectable Drug Delivery Devices Regulatory Approvals |

EMA clearance for Insulet’s Omnipod® 5 automated wearable injector |

|

Partnerships in the Injectable Drug Delivery Devices Market |

Sanofi partnered with Delfu Medical to expand access to autoinjectors in emerging markets; AstraZeneca and Enable Injections collaborated on wearable injector delivery for biologics. |

|

Acquisitions in the Injectable Drug Delivery Devices Market |

BD acquired CUBIC Health’s connected solutions division to strengthen its digital drug delivery offerings; Gerresheimer acquired Medimop Medical Projects to expand capabilities in prefillable syringes and safety devices. |

|

Company Strategy |

Eli Lilly invested in smart insulin delivery systems and connected pens; Novo Nordisk is expanding its digital ecosystem for injectable diabetes therapies; West Pharmaceutical is increasing its focus on sustainability and eco-friendly injection devices. |

|

Setbacks in the Injectable Drug Delivery Devices Market |

Reports of supply chain disruptions for medical-grade plastics and glass syringes; device recalls linked to mechanical malfunctions in certain autoinjectors; rising scrutiny over the environmental impact of single-use devices. |

|

Emerging Technology |

Growth of needle-free jet injectors and microneedle-based patches; increasing integration of AI and IoT in smart injectors; rising adoption of biodegradable materials in prefilled syringes; development of large-volume wearable injectors for biologics. |

Impact Analysis

AI-Powered Innovations and Applications:

Artificial intelligence is increasingly shaping the future of injectable drug delivery devices by enhancing efficiency, personalization, and patient safety. AI-powered systems enable smart injectors and connected autoinjectors to monitor dosing patterns, detect errors, and provide real-time feedback, improving adherence and reducing the risk of complications associated with incorrect administration. Machine learning algorithms can analyze patient data to optimize injection schedules and personalize treatment regimens, particularly for chronic conditions such as diabetes, rheumatoid arthritis, and multiple sclerosis, where long-term self-administration is common.

In addition, AI applications in predictive maintenance help manufacturers ensure device reliability by identifying potential failures before they occur, thereby extending product lifespan and enhancing user confidence. Integration of AI with mobile health platforms and wearable injectors also supports remote patient monitoring, giving healthcare providers actionable insights while empowering patients to take greater control of their therapy. Collectively, these innovations are transforming injectable drug delivery from a simple mode of administration into an intelligent, patient-centric system that bridges the gap between pharmaceuticals, devices, and digital health.

U.S. Tariff Impact Analysis on the Injectable Drug Delivery Devices Market:

U.S. tariff policies have a significant influence on the injectable drug delivery devices market as they increase the overall cost of imported components and finished products, putting pressure on manufacturers and potentially raising prices for both healthcare providers and patients. Since many companies in this sector depend on internationally sourced materials such as medical-grade plastics, silicon, electronic sensors, and specialized subassemblies, any increase in tariffs directly raises production expenses. Manufacturers are often left with the choice of absorbing these higher costs, which reduces their margins, or passing them on to the market, which can slow the adoption of advanced devices such as wearable injectors and connected autoinjectors. In addition, tariffs create uncertainty across supply chains, leading some companies to delay product launches or postpone investments in new technologies until the financial implications are clearer.

The broader impact of tariffs also extends to long-term industry strategies. Higher import duties encourage companies to explore domestic manufacturing and local sourcing, which may strengthen supply chain resilience and support local economic growth, but often requires substantial capital investment and longer timelines to implement. This can be particularly challenging for startups and smaller innovators with limited resources. On the other hand, trade tensions with major production hubs can prompt global firms to restructure supply networks, which may temporarily disrupt availability and alter pricing trends in different regions. To navigate these challenges, manufacturers are increasingly turning to diversified sourcing, closer supplier partnerships, and greater investment in vertical integration. Policymakers, in turn, can play a role by creating stable and predictable tariff frameworks, offering incentives for domestic production of critical inputs, and pursuing trade agreements that minimize uncertainty. Thus, tariffs may offer some protection to domestic industries, but they also increase costs and complexity, making it vital for both manufacturers and regulators to find a balance that supports innovation and accessibility in the injectable drug delivery devices market.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Main Products |

Stage of Development |

Core Technology |

|

Crossject (France) |

USD 120M |

ZENEO® needle-free autoinjector for emergency medications |

Late clinical/market approval stage |

Needle-free prefilled single-use autoinjector |

Key takeaways from the Injectable Drug Delivery Devices market report study

- Market size analysis for the current injectable drug delivery devices market size (2024), and market forecast for 8 years (2025 to 2032)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the injectable drug delivery devices market.

- Various opportunities available for the other competitors in the injectable drug delivery devices market space.

- What are the top-performing segments in 2024? How these segments will perform in 2032?

- Which are the top-performing regions and countries in the current injectable drug delivery devices market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the injectable drug delivery devices market growth in the future?