Lab Automation Market

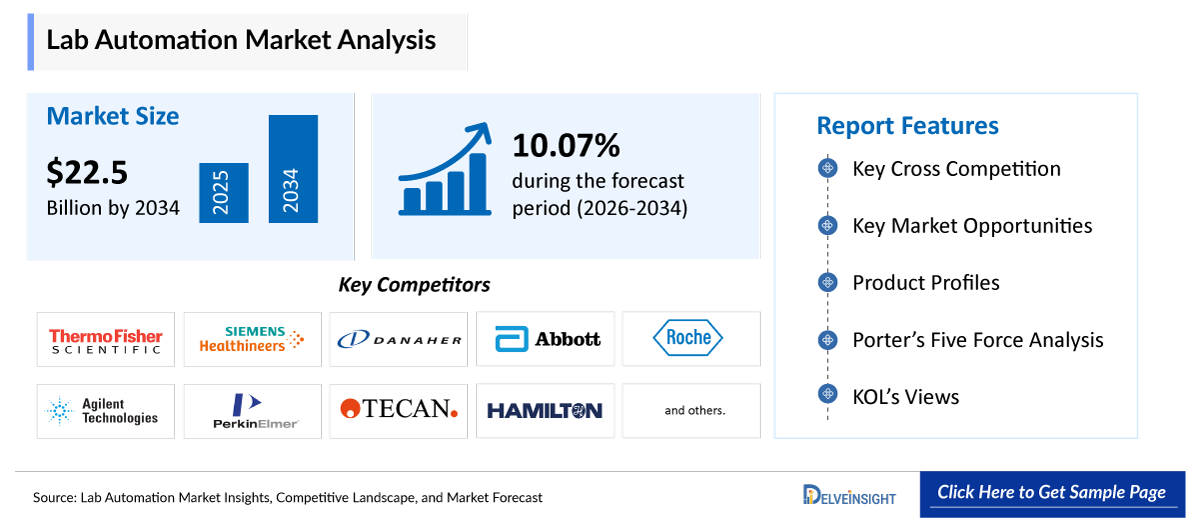

- The global lab automation market is expected to increase from USD 9,571.12 million in 2025 to USD 22,501.13 million by 2034, reflecting strong and sustained growth.

- The global lab automation market is growing at a CAGR of 10.07% during the forecast period from 2026 to 2034.

- Labor shortages and workforce pressure, accelerated biopharmaceutical R&D, and rising demand for high-throughput diagnostics are collectively accelerating the adoption of lab automation by addressing both capacity and efficiency gaps in modern laboratories. As skilled laboratory personnel become increasingly limited and operational costs rise, automation helps reduce dependency on manual workflows while improving productivity and consistency. At the same time, rapid expansion in biopharma pipelines and complex drug discovery processes requires faster experimentation, scalable screening, and higher data accuracy, which automated systems can deliver. Similarly, the growing need for high-throughput diagnostic testing, especially in genomics, infectious disease, and personalized medicine, further drives demand for automated platforms capable of processing large sample volumes with speed and precision, ultimately strengthening overall market growth.

- The leading companies operating in the lab automation market include Thermo Fisher Scientific, Danaher Corporation, Siemens Healthineers, Abbott, F. Hoffmann-La Roche Ltd, Agilent Technologies, PerkinElmer (Revvity), Tecan Group, Hamilton Company, SPT Labtech, Hudson Lab Automation, Qiagen N.V., Benchling, LabVantage Solutions, Biosero, Inc., Opentrons, Scispot, Clinisys, Ginkgo Bioworks, LabWare, and others.

- North America is expected to dominate the lab automation market due to the strong presence of major pharmaceutical, biotechnology, and diagnostic companies, along with advanced healthcare and research infrastructure. The region has high adoption of robotic systems, AI-enabled laboratory platforms, and digital workflow technologies across drug discovery, clinical diagnostics, and genomics research. In addition, increasing investments in biopharmaceutical R&D, growing demand for high-throughput testing, and the presence of leading market players such as Thermo Fisher Scientific, Danaher Corporation, and Agilent Technologies are further supporting regional market growth.

- In the offering segment of the lab automation market, the product category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Lab Automation Market

Lab Automation Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 9,571.12 million |

|

2034 Projected Market Size |

USD 22,501.13 million |

|

Growth Rate (2026-2034) |

10.07% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Lab Automation Market

-

Labor shortages & workforce pressure leading to a surge in lab automation:

The growing shortage of skilled laboratory professionals and increasing workforce costs are significantly boosting the demand for lab automation. Automated systems help laboratories reduce manual workloads, improve operational efficiency, minimize human errors, and maintain consistent productivity even with limited staff availability.

-

Accelerated R&D in biopharmaceuticals:

Rapid growth in biopharmaceutical research and drug development is increasing the need for automated laboratory workflows. Lab automation enables faster sample processing, high-throughput screening, and improved data accuracy, helping pharmaceutical and biotechnology companies accelerate drug discovery and development timelines.

-

Demand for high-throughput diagnostics:

The rising need for large-scale diagnostic testing in areas such as genomics, infectious diseases, and personalized medicine is driving adoption of lab automation systems. Automated diagnostic platforms can process high sample volumes quickly and accurately, improving turnaround times and supporting efficient clinical laboratory operations.

Lab Automation Market Report Segmentation

This lab automation market report offers a comprehensive overview of the global lab automation market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Offering (Product {Automated Liquid Handling Systems, Robotic Laboratory Automation Systems, Detection & Analytical Automation Systems, and Others}, Software {Laboratory Informatics & Software, Electronic Lab Notebooks (ELN), Scientific Data Management Systems (SDMS), and Others} and Services), Automation Type (Task-targeted Automation (TTA, Modular Automation, Total Laboratory Automation (TLA), and Others), Workflow (Sample Preparation, Liquid Handling & Dispensing, Sample Transport & handling, and Others), Application (Drug Discovery & Development, Clinical Diagnostics, Genomics & Proteomics, Cell Biology & Cell-based Assays, and Others), End-Users (Pharma & biotech companies, Diagnostic labs, Academic & Research Institutes, and CRO/CDMOs), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing lab automation market.

The lab automation market refers to the comprehensive ecosystem of automated hardware, specialized software, and integrated robotic platforms designed to perform laboratory tasks with minimal human intervention, thereby enhancing throughput, precision, and data integrity across clinical diagnostics and research workflows.

Labor shortages and workforce pressure, accelerated biopharmaceutical R&D, and rising demand for high-throughput diagnostics are collectively driving strong growth in the lab automation market by helping laboratories overcome operational, efficiency, and scalability challenges. As the availability of skilled laboratory professionals continues to decline in many regions, laboratories are increasingly adopting automation solutions to reduce reliance on manual processes, improve workflow consistency, minimize human error, and maintain productivity despite staffing constraints. Automated liquid handling systems, robotic sample processors, and AI-enabled workflow platforms allow laboratories to perform repetitive and complex tasks with greater speed and accuracy.

At the same time, the rapid expansion of biopharmaceutical research, including biologics, cell and gene therapies, vaccines, and personalized medicines, is creating a growing need for faster and more efficient research workflows. Pharmaceutical and biotechnology companies are investing heavily in automated laboratory technologies to accelerate drug discovery, high-throughput screening, sample preparation, and data analysis. Automation not only shortens R&D timelines but also improves reproducibility and supports large-scale experimentation required for modern drug development.

In addition, the increasing demand for high-throughput diagnostics is further boosting the adoption of lab automation systems across clinical and diagnostic laboratories. Rising testing volumes in genomics, infectious disease detection, molecular diagnostics, and precision medicine require laboratories to process thousands of samples rapidly while maintaining high accuracy and regulatory compliance. Automated diagnostic platforms help improve turnaround times, optimize laboratory efficiency, and enable scalable testing capabilities, making lab automation an essential component of modern healthcare and life sciences infrastructure.

Get More Insights into the Report @ Lab Automation Market

What are the latest Lab Automation market dynamics and trends?

Labor shortages and workforce pressure have emerged as one of the primary drivers accelerating growth in the global Laboratory Automation market. In 2026, laboratories worldwide are facing a significant imbalance between rapidly rising testing volumes and the declining availability of skilled professionals, including medical laboratory technologists, molecular biologists, clinical laboratory scientists, and automation specialists. The situation has intensified following the COVID-19 pandemic, which increased diagnostic testing demand while simultaneously contributing to burnout, early retirements, and workforce attrition across healthcare systems. According to workforce projections discussed by Roche Diagnostics, the global healthcare sector could face a shortage of nearly 11 million healthcare workers by 2030, with laboratory professionals representing a critical portion of this gap.

The shortage of qualified personnel is forcing laboratories to shift from manual and task-oriented workflows toward automated and digitally integrated operations. Automation technologies such as automated liquid handling systems, robotic workstations, AI-enabled workflow software, and Total Laboratory Automation (TLA) platforms enable laboratories to process significantly higher test volumes with fewer personnel while improving accuracy, reproducibility, and turnaround times. These systems reduce dependence on repetitive manual activities such as pipetting, sample sorting, labeling, centrifugation, aliquoting, and data entry, allowing laboratories to sustain productivity despite chronic understaffing.

A major factor strengthening automation demand is the ongoing generational turnover within the laboratory workforce. A large proportion of experienced laboratory professionals are approaching retirement age, creating concerns around the loss of specialized institutional knowledge and technical expertise. Automation helps standardize complex laboratory procedures into reproducible digital workflows, ensuring operational continuity and minimizing variability in diagnostic and research outputs. At the same time, laboratories are increasingly using automation to reduce employee burnout associated with repetitive high-volume testing and staff shortages.

The workforce crisis is also reshaping laboratory roles globally. Instead of performing repetitive manual tasks, laboratory professionals are increasingly transitioning toward supervisory and analytical responsibilities, including automation oversight, workflow management, and data interpretation. Modern automation platforms allow a single technician to oversee workflows that previously required multiple personnel, significantly improving operational efficiency and turnaround time predictability. As a result, major companies are increasingly positioning automation systems as direct solutions to labor shortages and operational bottlenecks.

Several industry surveys highlight the scale of workforce-related challenges driving automation adoption. According to a survey conducted by Siemens Healthineers and the Harris Poll, approximately 39% of laboratory professionals identified limited staffing as the biggest operational challenge facing laboratories, while laboratory vacancy rates range between 7% and 11%, reaching nearly 25% in certain regions and specialties. In addition, the U.S. Bureau of Labor Statistics projects approximately 22,600 annual openings for medical laboratory technologists through 2034, further highlighting the widening workforce gap. Similarly, the 2025 MLO State of the Industry Survey found that nearly 71% of laboratory professionals consider staffing shortages a major operational concern, accelerating investment in laboratory informatics, workflow optimization software, robotics, and AI-driven automation tools.

Overall, labor shortages and workforce pressure are expected to remain long-term structural drivers for the global laboratory automation market. As laboratories continue to face increasing test complexity, higher regulatory requirements, growing patient volumes, and limited access to skilled professionals, automation technologies will play an increasingly critical role in improving scalability, operational efficiency, quality control, and long-term workforce sustainability. Thus, the factors mentioned above are expected to boost the overall market of lab automation during the forecast period.

However, the high financial barriers, integration and technical complexity, and regulatory and security concerns are collectively limiting the growth of the lab automation market by creating challenges in adoption and implementation. Advanced automation systems often require significant initial investments in robotic platforms, software integration, infrastructure upgrades, and maintenance, making them difficult for small and mid-sized laboratories to afford. In addition, integrating automated systems with existing laboratory workflows, instruments, and data management platforms can be technically complex and time-consuming. Furthermore, strict regulatory requirements related to data integrity, patient safety, and cybersecurity increase compliance burdens for laboratories, slowing the adoption of fully automated solutions across healthcare and research environments.

Lab Automation Market Segment Analysis

Lab Automation Market by Offering (Product {Automated Liquid Handling Systems, Robotic Laboratory Automation Systems, Detection & Analytical Automation Systems, and Others}, Software {Laboratory Informatics & Software, Electronic Lab Notebooks (ELN), Scientific Data Management Systems (SDMS), and Others} and Services), Automation Type (Task-targeted Automation (TTA, Modular Automation, Total Laboratory Automation (TLA), and Others), Workflow (Sample Preparation, Liquid Handling & Dispensing, Sample Transport & handling, and Others), Application (Drug Discovery & Development, Clinical Diagnostics, Genomics & Proteomics, Cell Biology & Cell-based Assays, and Others), End-Users (Pharma & biotech companies, Diagnostic labs, Academic & Research Institutes, and CRO/CDMOs), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Offering: Automated liquid handling system under the product category is expected to dominate the market with the largest revenue share

In the offering segment of the lab automation market, the automated liquid handling system under the product category is contributing to 31% of total market revenue in 2025. Automated Liquid Handling Systems represent the largest product category within the global Laboratory Automation market and are being driven by the growing demand for high-throughput workflows, precision, and operational efficiency across pharmaceutical, biotechnology, diagnostics, and genomics laboratories.

These systems automate repetitive liquid transfer tasks such as pipetting, dispensing, dilution, aliquoting, and sample preparation, helping laboratories reduce manual errors, improve reproducibility, and significantly increase processing speed. The segment has become a core component of modern laboratory infrastructure, particularly in drug discovery, molecular diagnostics, next-generation sequencing (NGS), and cell biology workflows.

A major technological driver is the industry-wide shift toward miniaturization. Modern liquid handlers are increasingly capable of non-contact dispensing, allowing laboratories to significantly reduce assay volumes. By shrinking the scale of experiments, labs can realize a massive reduction in reagent consumption, often up to 90%, which not only lowers the cost per data point but also aligns with corporate sustainability initiatives by minimizing plastic waste from disposable tips.

This "low-volume, high-density" approach enables scientists to run more trials simultaneously, effectively accelerating the pace of scientific discovery without a linear increase in costs.

Labor shortages and workforce pressure are also contributing significantly to market growth. Laboratories worldwide are facing shortages of skilled laboratory professionals while testing volumes continue to rise. Automated liquid handling systems help laboratories maintain productivity with fewer personnel by reducing dependence on repetitive manual tasks and minimizing fatigue-related human errors. Growing regulatory emphasis on workflow standardization, traceability, and data integrity is further supporting adoption across clinical and research laboratories.

Technological advancements and increasing digitalization are further strengthening the segment. Modern liquid handling platforms are increasingly integrated with AI-enabled software, Laboratory Information Management Systems (LIMS), robotic scheduling tools, and cloud-based analytics platforms to improve workflow automation and laboratory connectivity.

The market is also witnessing continuous product innovation. In 2025, Tecan Group launched the Veya™ liquid handling platform featuring AI-enhanced workflow optimization and scalable automation capabilities for multi-omics applications. Similarly, Beckman Coulter introduced the Biomek i3 Benchtop Liquid Handler, designed for genomics, sequencing, and drug discovery applications in low- to medium-throughput laboratories. These product launches reflect the growing industry focus on improving automation accessibility, workflow flexibility, and operational efficiency across laboratories of all sizes.

Thus, all the aforementioned factors are expected to drive the segmental growth of the lab automation market during the forecasted period from 2026 to 2034.

By Automation Type: The Total Laboratory Automation (TLA) category dominates the market

Within the automation type segment of the lab automation market, the Total Laboratory Automation (TLA) category is anticipated to dominate, accounting for around 55% of the market share in 2025. Total Laboratory Automation (TLA) is significantly boosting the overall lab automation market by enabling laboratories to achieve fully integrated, high-efficiency workflows across pre-analytical, analytical, and post-analytical processes. TLA systems automate critical laboratory functions such as sample transportation, sorting, centrifugation, testing, storage, and data management, which helps reduce manual intervention, minimize human error, improve turnaround times, and increase testing capacity. The growing demand for high-throughput diagnostics, rising laboratory workloads, and shortages of skilled professionals are further accelerating the adoption of TLA solutions across clinical diagnostics, pharmaceutical research, and biotechnology laboratories. In addition, TLA supports better standardization, regulatory compliance, and operational scalability, making it highly attractive for large laboratories handling complex and high-volume testing environments. Recent technological advancements integrating AI, robotics, machine learning, and IoT-enabled laboratory systems are also strengthening the capabilities of TLA platforms.

Several companies have recently introduced advanced TLA solutions to expand laboratory automation capabilities. In June 2024, F. Hoffmann-La Roche Ltd introduced new cobas® pro integrated solution analytical units designed to improve laboratory throughput, automation efficiency, and workflow capacity. Additionally, in October 2024, Siemens Healthineers expanded its Atellica Integrated Automation platform to help laboratories automate up to 25 manual tasks and reduce workflow burden caused by staffing shortages.

Thus, the factors mentioned above are expected to boost the overall market of Total Laboratory Automation (TLA) and thereby escalate the overall market of lab automation during the forecast period.

By Workflow: The liquid handling & dispensing category dominates the market.

Within the workflow segment of the lab automation market, the liquid handling & dispensing category is anticipated to dominate, accounting for around 35% of the market share in 2025. Liquid Handling & Dispensing is playing a critical role in boosting the overall lab automation market by enabling laboratories to perform precise, rapid, and high-throughput sample processing with minimal manual intervention. These systems automate repetitive pipetting and reagent dispensing tasks, significantly improving workflow accuracy, reproducibility, and operational efficiency across pharmaceutical research, biotechnology, genomics, proteomics, clinical diagnostics, and molecular biology applications. As laboratories increasingly handle large sample volumes and complex workflows, automated liquid handling platforms help reduce human errors, minimize reagent waste, lower labor dependency, and accelerate experimental timelines. The growing adoption of next-generation sequencing (NGS), PCR-based diagnostics, drug discovery screening, and personalized medicine is further driving demand for advanced liquid handling solutions capable of supporting scalable and standardized workflows. In addition, the integration of AI, robotics, cloud connectivity, and no-code software platforms is making liquid handling automation more accessible and efficient for modern laboratories.

Several companies have recently introduced advanced liquid handling innovations to strengthen laboratory automation capabilities. In February 2024, SPT Labtech launched the firefly®+ automated genomics liquid handling platform with integrated thermocycling and hands-free NGS library preparation capabilities to improve workflow efficiency in genomics laboratories. In February 2024, Opentrons introduced a new AI-powered protocol library and generative AI tools designed to simplify and accelerate automated liquid handling workflows across genomics, proteomics, and synthetic biology applications. Additionally, in September 2024, Opentrons launched the Flex Prep robot, a no-code automated liquid handling platform that enables scientists to program pipetting tasks through an intuitive touchscreen interface, improving accessibility and workflow automation in laboratories.

Thus, the factors mentioned above are expected to boost the overall market of lab automation.

By Application: Drug discovery & development category dominates the market.

Within the application segment of the lap automation market, the drug discovery & development category is anticipated to dominate, accounting for around 40% of the market share in 2025. Drug Discovery & Development is significantly boosting the overall lab automation market as pharmaceutical and biotechnology companies increasingly rely on automated technologies to accelerate research workflows, improve efficiency, and reduce drug development timelines. Modern drug discovery involves large-scale compound screening, high-throughput testing, genomics analysis, cell-based assays, and complex data generation, all of which require highly precise and scalable laboratory operations. Lab automation systems such as robotic liquid handlers, automated sample preparation platforms, AI-enabled screening systems, and integrated data management software help laboratories process thousands of samples rapidly while minimizing human error and improving reproducibility. The growing focus on biologics, biosimilars, cell and gene therapies, and precision medicine is further increasing the complexity of R&D workflows, making automation essential for efficient experimentation and standardized results. In addition, pharmaceutical companies are increasingly integrating artificial intelligence, machine learning, and robotic process automation into drug discovery pipelines to improve target identification, optimize lead compounds, and enhance predictive analysis. Rising investments in biopharmaceutical R&D, increasing clinical trial activity, and the need for faster therapeutic innovation are therefore driving strong adoption of automated laboratory technologies, ultimately accelerating the growth of the overall lab automation market.

By End-Users: The Pharma & Biotech Companies category dominates the market.

Within the end-user segment of the lab automation market, pharma and biotech companies dominate due to their extensive use of automated systems in drug discovery, biologics development, genomics research, and high-throughput screening applications. These companies heavily invest in robotic platforms, automated liquid handling systems, AI-driven analytics, and integrated laboratory workflows to accelerate R&D processes, improve experimental accuracy, reduce operational costs, and shorten drug development timelines. The growing focus on precision medicine, cell and gene therapy, and large-scale biopharmaceutical production is further strengthening the adoption of lab automation technologies across the pharmaceutical and biotechnology industries.

Lab Automation Market Regional Analysis

North America Lab Automation Market Trends

North America is expected to account for the highest proportion of 41% of the lab automation market in 2025, out of all regions, driven by the strong presence of pharmaceutical and biotechnology companies, advanced healthcare and research infrastructure, rising laboratory testing volumes, and rapid adoption of digital and AI-enabled laboratory technologies. The country accounts for the largest share of global laboratory automation spending due to increasing demand for high-throughput drug discovery, genomics research, molecular diagnostics, and precision medicine applications. In addition, growing workforce shortages across clinical and research laboratories are accelerating investments in automated workflows, robotic systems, and laboratory informatics platforms to improve operational efficiency and reduce dependence on manual processes.

The country is home to several major market players, including Thermo Fisher Scientific, Danaher Corporation, Agilent Technologies, Revvity, and Bio-Rad Laboratories, all of which continue to launch next-generation automation platforms in the U.S. market before broader global expansion. For instance, in 2025, Tecan Group launched its Veya™ automated liquid handling platform designed for scalable multi-omics workflows, while Beckman Coulter introduced the Biomek i3 Benchtop Liquid Handler for genomics and drug discovery applications.

The country is also witnessing the rapid adoption of Total Laboratory Automation (TLA) systems across hospital laboratories, reference laboratories, and pharmaceutical research facilities. Major players such as Siemens Healthineers and Roche Diagnostics continue to expand integrated clinical laboratory automation platforms in the U.S. to address growing diagnostic workloads and workforce shortages. Increasing integration of robotics, cloud-based laboratory informatics, AI-driven analytics, and Laboratory Information Management Systems (LIMS) is further strengthening the country’s leadership position in smart laboratory transformation.

The increasing prevalence of chronic diseases and rising adoption of molecular diagnostics are further supporting market growth. According to the Centers for Disease Control and Prevention (CDC), chronic diseases account for nearly 90% of annual healthcare expenditures in the U.S., significantly increasing demand for advanced laboratory testing and automation. Additionally, ongoing workforce shortages remain a major growth catalyst, with laboratory vacancy rates ranging between 7% and 11% across the country. In addition, the U.S. Bureau of Labor Statistics projected approximately 22,600 annual openings for medical laboratory technologists through 2034, further highlighting the widening workforce gap.

Collectively, strong R&D investments, early technology adoption, expanding genomics and precision medicine applications, and the presence of leading automation companies position the U.S. as the dominant regional market for laboratory automation globally.

Europe Lab Automation Market Trend

The lab automation market in Europe is witnessing strong and sustained growth due to increasing investments in pharmaceutical research, clinical diagnostics, genomics, and precision medicine, along with rising demand for efficient and standardized laboratory workflows. European laboratories are rapidly adopting robotic systems, AI-enabled automation platforms, automated liquid handling technologies, and cloud-based laboratory management systems to improve productivity, reduce human error, and address shortages of skilled laboratory professionals. In addition, supportive government initiatives for healthcare modernization, growing biopharmaceutical R&D activities, and increasing focus on high-throughput testing are further accelerating market expansion across countries such as Germany, the United Kingdom, France, and Switzerland. According to recent studies, up to 28% of lab technicians were over 55, and some regions in Europe reported as much as a 24% vacancy rate in hospital laboratories, placing extreme pressure on remaining staff.

Additionally, several recent developments are further strengthening the European lab automation ecosystem. In January 2025, Agilent Technologies partnered with ABB Robotics to co-develop advanced robotic laboratory automation solutions aimed at improving laboratory speed, efficiency, and workflow integration across pharmaceutical and biotechnology applications. Additionally, European laboratories are increasingly integrating AI-driven and robotics-enabled “trackless automation” systems to enhance sample handling and laboratory logistics. Siemens Healthineers has also been actively expanding robotic laboratory workflow solutions across Europe to automate tasks such as sample transport, reagent retrieval, and laboratory process management. Furthermore, Germany continues to remain a major regional growth hub due to its strong pharmaceutical infrastructure, advanced research ecosystem, and high adoption of smart laboratory technologies.

Asia-Pacific Lab Automation Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the lab automation market due to the rapid expansion of the pharmaceutical, biotechnology, and clinical diagnostics industries across countries such as China, India, Japan, South Korea, and Singapore. Increasing healthcare investments, growing biopharmaceutical manufacturing activities, and rising adoption of advanced laboratory technologies are significantly accelerating demand for automated laboratory systems in the region. In addition, the increasing prevalence of chronic and infectious diseases, expanding genomics research, and rising focus on precision medicine are encouraging laboratories to adopt high-throughput and AI-enabled automation platforms to improve efficiency and diagnostic accuracy. Governments across APAC are also supporting healthcare modernization and life sciences innovation through funding initiatives and research infrastructure development. Furthermore, the presence of cost-effective manufacturing capabilities, expanding CRO and CDMO activities, and growing investments by global pharmaceutical companies are further strengthening the adoption of robotic liquid handling systems, automated analyzers, and integrated laboratory workflows, making APAC one of the fastest-growing regions in the global lab automation market.

Who are the major players in the lab automation market?

The following are the leading companies in the lab automation market. These companies collectively hold the largest market share and dictate industry trends.

- Thermo Fisher Scientific

- Danaher Corporation

- Siemens Healthineers

- Abbott

- F. Hoffmann-La Roche Ltd.

- Agilent Technologies

- PerkinElmer (Revvity)

- Tecan Group

- Hamilton Company

- SPT Labtech

- Hudson Lab Automation

- Qiagen N.V.

- Benchling, LabVantage Solutions

- Biosero, Inc.

- Opentrons

- Scispot

- Clinisys

- Ginkgo Bioworks

- LabWare

- Others

How is the competitive landscape shaping the lab automation market?

The competitive landscape of the lab automation market is highly fragmented and innovation-focused, with major global companies competing through advanced robotics, automated liquid handling systems, laboratory informatics, AI-enabled workflow platforms, and integrated automation solutions. Leading players such as Thermo Fisher Scientific, Danaher Corporation, Siemens Healthineers, Agilent Technologies, Tecan Group, and F. Hoffmann-La Roche Ltd. are focusing on expanding their product portfolios, strengthening R&D capabilities, and improving laboratory workflow integration to maintain market competitiveness. The market is also witnessing growing competition from emerging automation and software-focused companies offering flexible, modular, and cost-effective laboratory solutions. Increasing demand for high-throughput testing, precision medicine, genomics, and biopharmaceutical research is encouraging companies to invest in AI, cloud connectivity, robotic automation, and digital laboratory ecosystems. In addition, strategic collaborations, customized automation platforms, and scalable laboratory solutions are becoming key competitive strategies as vendors aim to improve laboratory efficiency, reproducibility, and operational scalability across pharmaceutical, biotechnology, clinical diagnostics, and research laboratories worldwide.

Recent Developmental Activities in the Lab Automation Market

- In January 2025, Agilent Technologies partnered with ABB Robotics to co-develop advanced robotic laboratory automation solutions aimed at improving laboratory speed, efficiency, and workflow integration across pharmaceutical and biotechnology applications.

- In October 2024, Siemens Healthineers expanded its Atellica Integrated Automation platform to help laboratories automate up to 25 manual tasks and reduce workflow burden caused by staffing shortages.

- In September 2024, Opentrons launched the Flex Prep robot, a no-code automated liquid handling platform that enables scientists to program pipetting tasks through an intuitive touchscreen interface, improving accessibility and workflow automation in laboratories.

- In June 2024, F. Hoffmann-La Roche Ltd introduced new cobas® pro integrated solution analytical units designed to improve laboratory throughput, automation efficiency, and workflow capacity.

- In May 2024, Abbott launched its GLP systems Track automation solution in India to support high-volume laboratory operations and reduce manual workflow steps by nearly 80%.

- In February 2024, SPT Labtech launched the firefly®+ automated genomics liquid handling platform with integrated thermocycling and hands-free NGS library preparation capabilities to improve workflow efficiency in genomics laboratories.

- In February 2024, Opentrons introduced a new AI-powered protocol library and generative AI tools designed to simplify and accelerate automated liquid handling workflows across genomics, proteomics, and synthetic biology applications.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Lab Automation Market CAGR |

10.07% |

|

Key Companies in the Lab Automation Market |

Thermo Fisher Scientific, Danaher Corporation, Siemens Healthineers, Abbott, F. Hoffmann-La Roche Ltd, Agilent Technologies, PerkinElmer (Revvity), Tecan Group, Hamilton Company, SPT Labtech, Hudson Lab Automation, Qiagen N.V., Benchling, LabVantage Solutions, Biosero, Inc., Opentrons, Scispot, Clinisys, Ginkgo Bioworks, LabWare, and others. |

|

Lab Automation Market Segments |

by Offering, by Automation Type, by Workflow, by Application, by End-Users, and by Geography |

|

Lab Automation Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Lab Automation Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Lab Automation Market Segmentation

-

Lab Automation by Offering Exposure

-

Product

-

Automated Liquid Handling Systems

-

Robotic Laboratory Automation Systems

-

Detection & Analytical Automation Systems

-

Others

-

Software

-

Laboratory Informatics & Software

-

Electronic Lab Notebooks (ELN)

-

Scientific Data Management Systems (SDMS)

-

Others

-

Services

-

Lab Automation by Automation Type Exposure

-

Task-targeted Automation (TTA)

-

Modular Automation

-

Total Laboratory Automation (TLA)

-

Others

-

Lab Automation Workflow Exposure

-

Sample Preparation

-

Liquid Handling & Dispensing

-

Sample Transport & Handling

-

Others

-

Lab Automation Application Exposure

-

Drug Discovery & Development

-

Clinical Diagnostics

-

Genomics & Proteomics

-

Cell Biology & Cell-based Assays

-

Others

-

Lab Automation End-Users Exposure

-

Pharma & biotech Companies

-

Diagnostic labs

-

Academic & Research Institutes

-

CRO/CDMOs

-

Lab Automation Geography Exposure

-

North America Lab Automation Market

-

United States Lab Automation Market

-

Canada Lab Automation Market

-

Mexico Lab Automation Market

-

Europe Lab Automation Market

-

United Kingdom Lab Automation Market

-

Germany Lab Automation Market

-

France Lab Automation Market

-

Italy Lab Automation Market

-

Spain Lab Automation Market

-

Rest of Europe Lab Automation Market

-

Asia-Pacific Lab Automation Market

-

China Lab Automation Market

-

Japan Lab Automation Market

-

India Lab Automation Market

-

Australia Lab Automation Market

-

South Korea Lab Automation Market

-

Rest of Asia-Pacific Lab Automation Market

-

Rest of the World Lab Automation Market

-

South America Lab Automation Market

-

Middle East Lab Automation Market

-

Africa Lab Automation Market

Lab Automation Market Recent Industry Trends and Milestones (2023-2026)

|

Category |

Key Developments |

|

Lab Automation Product Expansion |

Siemens Healthineers expanded its Atellica Integrated Automation platform |

|

Lab Automation Product Partnership |

Agilent Technologies partnered with ABB Robotics to co-develop advanced robotic laboratory automation solutions. |

|

Lab Automation Product Launch |

Opentrons launched the Flex Prep robot, a no-code automated liquid handling platform that enables scientists to program pipetting tasks through an intuitive touchscreen interface, improving accessibility and workflow automation in laboratories. |

|

Company Strategy |

Thermo Fisher Scientific

Danaher Corporation

|

|

Emerging Technology |

AI and machine learning–driven Lab Automation, robotics and collaborative robots (cobots), Cloud-based Laboratory Information Management Systems (LIMS), Internet of Things (IoT) and smart sensor technologies, self-driving laboratories and AI-powered biofoundries, and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are transforming the lab automation market by enabling laboratories to become more intelligent, efficient, and data-driven. Artificial intelligence and machine learning technologies are increasingly being integrated into automated laboratory systems for applications such as predictive analytics, workflow optimization, automated data interpretation, anomaly detection, and real-time decision-making. In drug discovery and biopharmaceutical research, AI-powered automation platforms help accelerate target identification, compound screening, assay optimization, and lead candidate selection by rapidly analyzing large biological datasets with greater accuracy. In clinical diagnostics and genomics, AI-enabled systems improve sample classification, image analysis, disease detection, and diagnostic accuracy while reducing manual errors and turnaround times. AI is also being used in robotic liquid handling systems, self-driving laboratories, and smart laboratory management platforms to automate experimental design, optimize resource utilization, and improve reproducibility. Additionally, AI-integrated cloud-based laboratory informatics systems support predictive maintenance, remote monitoring, and automated workflow coordination, helping laboratories enhance productivity, scalability, and operational efficiency across pharmaceutical, biotechnology, and clinical research environments.

U.S. Tariff Impact Analysis on Lab Automation Market:

U.S. tariff policies are creating a mixed impact on the lab automation market by increasing operational costs and supply chain pressures while also encouraging domestic manufacturing and supply chain diversification. Many lab automation systems depend on imported electronic components, robotics hardware, semiconductors, sensors, laboratory instruments, and consumables sourced from countries such as China, Japan, and members of the European Union. Rising tariffs on these imported products are increasing procurement and manufacturing costs for laboratory automation vendors, which can lead to higher prices for automated instruments, liquid handling systems, analyzers, and laboratory software platforms.

In addition, tariffs are contributing to supply chain disruptions, longer lead times, and uncertainty in sourcing critical automation components, making it more difficult for laboratories and manufacturers to maintain stable procurement cycles and budget planning. Clinical and diagnostic laboratories are particularly vulnerable because changes in validated instruments or reagents often require additional regulatory validation and compliance procedures.

However, the tariff environment is also encouraging companies to strengthen domestic manufacturing capabilities, regionalize supply chains, and invest in local production facilities to reduce dependence on imports. This shift may support long-term growth opportunities for U.S.-based automation manufacturers and suppliers. At the same time, laboratories are increasingly adopting AI-driven inventory management, predictive procurement tools, and digital supply chain monitoring systems to mitigate tariff-related risks and improve operational resilience. Overall, while tariffs may temporarily increase costs and slow purchasing decisions, they are also accelerating strategic restructuring and localization efforts within the U.S. lab automation industry.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Key takeaways from the lab automation market report study

- Market size analysis for the current lab automation market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the lab automation market.

- Various opportunities available for the other competitors in the lab automation market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current lab automation market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the lab automation market growth in the future.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Unnatural Products (UNP) |

~$77M (including $45M Series B in March 2026) |

Pre-Commercial (Advancing lead programs through IND-enabling studies) |

Integrated Drug Discovery Platform for Macrocyclic Peptides |

Closed-Loop Automation: Combines computational design, automated chemistry, and high-throughput biological testing. |