Needle Safety Devices Market Summary

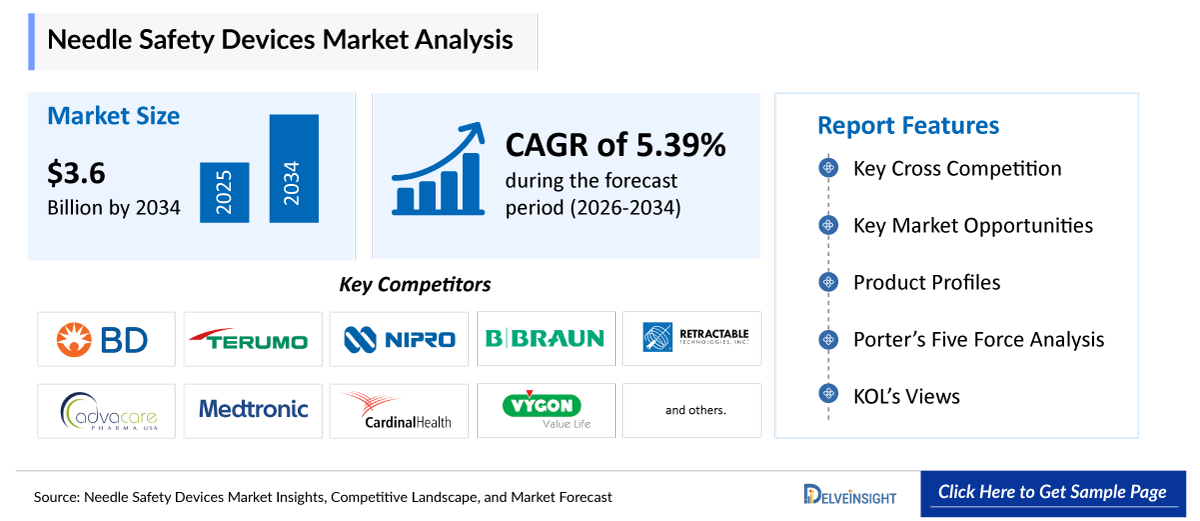

- The global needle safety devices market size is expected to increase from USD 2,284.15 million in 2025 to USD 3,637.49 million by 2034, reflecting strong and sustained growth.

- The global needle safety devices market is growing at a CAGR of 5.39% during the forecast period from 2026 to 2034.

- The growth of the needle safety devices market is largely attributed to the increasing number of accidental needlestick injuries and the heightened concern over the transmission of blood-borne infections among healthcare professionals. The rising burden of chronic conditions that require repeated injections, along with expanding vaccination initiatives and higher healthcare spending, is further contributing to market expansion. Moreover, the shift toward home healthcare and self-administration of injectable therapies is creating additional demand for safer devices. Continuous innovations in passive and auto-retractable technologies are also improving safety, ease of use, and regulatory compliance, thereby driving overall market growth.

- The leading companies operating in the needle safety devices market include BD, Terumo Corporation, Nipro, ICU Medical, B.Braun, Retractable Technologies, AdvaCare Pharma, Medtronic, Hindustan Syringes & Medical Devices Ltd., Cardinal Health, Vygon SA, Gerresheimer AG, West Pharamaceuticak Services, Inc., UltiMed, Inc., Argon Medical Devices, Inc., Novo Nordisk A/S, Kindly (KDL) Meditech, Weigao Group, Jiangsu Jichun Medical Devices Co., Ltd., Sarstedt AG & CO. KG and others.

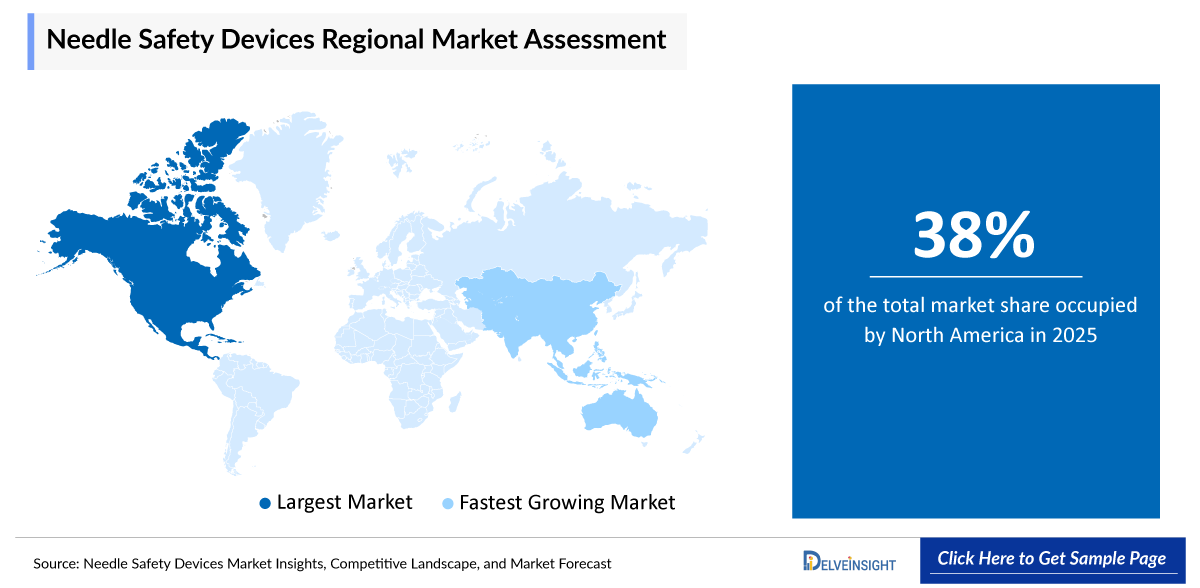

- North America is expected to remain a leading region in the global needle safety devices market due to strong awareness about needlestick injuries and the importance of reducing infection risks in healthcare settings. Strict safety regulations and workplace protection policies support the widespread use of safety-engineered injection devices. The rising number of patients with chronic diseases, increasing vaccination programs, and growing use of home-based treatments are also driving demand. Additionally, continuous improvements in automatic shielding and needle-retraction technologies are enhancing safety and supporting steady market growth in the region.

- In the product type segment of the needle safety devices market, under the safety needles segment, safety hypodermic needles category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Needle Safety Devices Market Trends

Needle Safety Devices Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 2,284.15 million |

|

2034 Projected Market Size |

USD 3,637.49 million |

|

Growth Rate (2026-2034) |

5.39% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Needle Safety Devices Market

- Rising incidence of needlestick injuries: The increasing occurrence of needlestick injuries is significantly driving the growth of the needle safety devices market, as accidental sharps injuries continue to pose serious occupational hazards in healthcare settings. Needlestick injuries expose healthcare workers to bloodborne pathogens such as HIV, hepatitis B, and hepatitis C, leading to serious health risks, psychological stress, and increased healthcare costs. The growing volume of injections administered for vaccinations, chronic disease management, and emergency care has increased routine exposure to needles among healthcare professionals. As a result, healthcare institutions are prioritizing the adoption of safety-engineered devices with built-in protective features to reduce accidental exposure. This heightened focus on prevention and risk management is creating strong and sustained demand for needle safety technologies worldwide.

- Increasing chronic conditions such as diabetes, cancer, autoimmune disorders requiring frequent injections: The increasing prevalence of chronic conditions such as diabetes, cancer, and autoimmune disorders is significantly driving the growth of the needle safety devices market, as these diseases often require long-term and repeated injectable treatments. Patients undergoing insulin therapy, chemotherapy, biologic drug administration, and hormone treatments depend on frequent injections in hospitals, specialty clinics, and home-care settings. The growing adoption of self-administration therapies, particularly for diabetes and autoimmune diseases, has increased the need for safer and more user-friendly injection devices to minimize accidental injuries. Additionally, the expanding geriatric population, which is more prone to chronic illnesses, is further contributing to higher injection volumes worldwide. This sustained rise in injectable treatments is creating strong demand for advanced safety syringes and protective needle technologies, thereby supporting overall market expansion.

- Increase in vaccination & immunization programs: The increase in vaccination and immunization programs is a significant driver of the needle safety devices market, as large-scale vaccine administration requires safe and reliable injection practices. Government-led public health initiatives, routine childhood immunization schedules, and mass vaccination campaigns for infectious diseases have substantially increased the volume of injections administered worldwide. This high usage creates a strong need for safety syringes and auto-disable devices to prevent needle reuse and cross-contamination. Additionally, global efforts to improve immunization coverage in developing regions and preparedness for emerging disease outbreaks are further boosting procurement of safety-engineered injection products. As a result, the expanding scope of vaccination programs continues to generate consistent demand for needle safety devices across healthcare systems.

- Growth in self-administration & home healthcare: The growth in self-administration and home healthcare is significantly driving the needle safety devices market, as an increasing number of patients are managing long-term conditions outside traditional hospital settings. Treatments for diabetes, autoimmune disorders, hormonal deficiencies, and other chronic illnesses often require regular injectable medications, prompting patients to use insulin pens, prefilled syringes, and biologic injectables at home. This shift toward convenient and cost-effective care has increased the demand for easy-to-use, reliable, and protective injection devices that minimize accidental injuries. Additionally, the rising elderly population, preference for outpatient care, and advancements in drug delivery systems are further accelerating the adoption of safety-integrated needles and pen devices in home environments, thereby contributing to sustained market expansion.

- Increase in product development activites: The increase in product development activities is significantly driving the growth of the needle safety devices market, as manufacturers focus on introducing more efficient, user-friendly, and compliant safety solutions. Companies are investing in research and development to design innovative devices with improved ergonomic features, enhanced shielding mechanisms, and integrated safety technologies that reduce activation errors. The shift toward passive safety systems, compact designs for home healthcare use, and compatibility with prefilled syringes and biologics is further accelerating innovation. In addition, collaborations, strategic partnerships, and regulatory approvals for next-generation products are expanding product portfolios and strengthening competitive positioning. These continuous advancements are improving clinical efficiency and encouraging faster adoption across healthcare settings, thereby supporting overall market expansion.

Needle Safety Devices Market Report Segmentation

This needle safety devices market report offers a comprehensive overview of the global needle safety devices market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product Type (Safety Needles {Safety Hypodermic Needles, Safety Pen Needles, Safety Blood Collection Needles, and Others} Safety IV Catheters, and Safety Syringes), Safety Mechanism (Active Safety Devices and Passive Safety Devices), End-Users (Hospitals & Clinics, Ambulatory Surgical Centers, Homecare Settings, and Others), and Geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing needle safety devices market.

Needle safety devices are medical instruments designed with built-in protective mechanisms that reduce the risk of accidental needlestick injuries during and after the use of needles. These devices incorporate safety features such as retractable needles, sliding shields, protective sheaths, or automatic locking systems that cover or withdraw the needle immediately after use.

The global needle safety devices market is being propelled by several interrelated factors that are collectively strengthening product adoption across healthcare systems worldwide. One of the primary drivers is the rising incidence of needlestick injuries among healthcare professionals. Hospitals and clinical laboratories are increasingly prioritizing occupational safety to reduce the risk of transmission of bloodborne infections such as HIV and hepatitis. Moreover, another growth factor is the expanding volume of surgical procedures, vaccinations, and chronic disease treatments. The increasing prevalence of diabetes, cancer, and cardiovascular disorders has led to a higher frequency of injections, IV therapies, and blood sampling procedures, thereby driving the need for safer needle technologies.

Technological advancements are further contributing to market expansion. Manufacturers are introducing passive safety mechanisms, auto-retractable syringes, and user-friendly designs that enhance efficiency while minimizing manual handling. These innovations are improving product reliability and encouraging broader adoption across healthcare facilities.

Collectively, these factors are driving sustained growth in the global needle safety devices market by aligning regulatory compliance, technological innovation, and occupational safety priorities with increasing healthcare demand.

Get More Insights into the Report @ Needle Safety Devices Market Insights

What are the latest needle safety devices market dynamics and trends?

The needle safety devices market has grown due to the rising incidence of needlestick injuries and concerns over blood-borne infections among healthcare workers. Increasing chronic disease prevalence, expanding vaccination programs, higher healthcare spending, and the shift toward home-based therapies have further driven demand.

According to the World Health Organization (2022), needlestick injuries were among the most serious occupational hazards for healthcare workers (HCWs), with over 2 million occupational exposures occurring annually among 35 million HCWs. Needlestick injuries are a key driver of the needle safety devices market, as they expose healthcare workers to serious blood-borne infections such as HIV, Hepatitis B, and Hepatitis C. The frequent occurrence of these injuries in hospitals, clinics, and laboratories has created a pressing demand for devices designed to prevent accidental needle pricks and enhance occupational safety.

Moreover, according to the International Diabetes Federation (2025), approximately 589 million adults (aged 20–79 years) were living with diabetes globally. Individuals with diabetes frequently require multiple daily injections, increasing needle usage in both clinical and home settings. This higher exposure raises the risk of accidental needlestick injuries for patients, caregivers, and healthcare professionals, underscoring the essential need for safety-engineered injection devices and driving the growth of the needle safety devices market.

Furthermore, the expansion of vaccination and immunization programs is driving growth in the needle safety devices market by increasing syringe and needle usage, which raises the risk of needlestick injuries. According to the data provided by the World Health Organization (2025), the global coverage for the first dose of HPV vaccine in girls grew from 27% in 2023 to 31% in 2024. The increasing uptake of human papillomavirus (HPV) vaccination is significantly boosting the overall market for needle safety devices by driving sustained demand for safe injectable delivery tools as countries expand immunization beyond infancy to include adolescents and young adults. HPV vaccines administered typically in two or three intramuscular injections are now being integrated into national immunization schedules across low-, middle-, and high-income countries to prevent cervical and other HPV-related cancers. As more governments and global health partners scale up school-based and community vaccination campaigns, the volume of administered injections rises, creating a proportional need for safety syringes and needles.

However, the increase in product development activities is further boosting the overall market of respiratory care devices. For instance, in January 2026, Terumo Medical Corporation, a wholly owned subsidiary of Terumo Corporation, announced the U.S. launch of its SurTract™ Safety Syringe, featuring SafeR® passive safety technology developed by Roncadelle Operations S.r.l.

Thus, the factors mentioned above are expected to boost the overall market of respiratory care devices during the forecast period from 2023 to 2034.

However, the needle safety devices market faces challenges related to environmental and waste management concerns, as the widespread use of single-use syringes and needles generates large volumes of medical sharps waste that require safe disposal. Improper handling and disposal can lead to environmental pollution and pose health risks. Additionally, increasing product recalls due to manufacturing defects, safety issues, or regulatory non-compliance can disrupt supply chains, affect market confidence, and hinder adoption. Together, these factors act as restraints on market growth and emphasize the need for improved waste management and quality control measures.

Needle Safety Devices Market Segment Analysis

Needle Safety Devices Market by Product Type (Safety Needles {Safety Hypodermic Needles, Safety Pen Needles, Safety Blood Collection Needles, and Others} Safety IV Catheters, and Safety Syringes), Safety Mechanism (Active Safety Devices and Passive Safety Devices), End-Users (Hospitals & Clinics, Ambulatory Surgical Centers, Homecare Settings, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World).

By Product Type: Under the safety needles segment, safety hypodermic needles are projected to account for the highest revenue share in the global market.

Within the product type segmentation of the needle safety devices market, under the safety needles segment, safety hypodermic needles are projected to hold the largest revenue share, accounting for an estimated 28% of the market in 2025. Their dominance is due to their widespread use in healthcare facilities for injections, vaccinations, and blood sampling.

Safety hypodermic needles are advanced injection devices equipped with built-in protective mechanisms, such as retractable needles or shielding systems, to significantly reduce the risk of accidental needlestick injuries. They are widely used for routine injections, vaccinations, and blood collection, making them a critical component of healthcare safety protocols. Key advantages of safety hypodermic needles include enhanced protection for healthcare workers, compliance with stringent regulatory standards, minimized risk of bloodborne infection transmission, and ease of use in high-volume clinical procedures.

Leading manufacturers in this segment include BD (Becton, Dickinson and Company), which offers BD SafetyGlide™ Hypodermic Needles; Terumo Corporation, known for its SurTract™ Safety Syringe; and ICU Medical, with the Hypodermic Needle‑Pro® EDGE™ Safety Device combined with low dead-space syringes. For instance, in May, 2024, the U.S. Food and Drug Administration (FDA) cleared a modified version of the Smiths Medical (now ICU Medical) Hypodermic Needle‑Pro® EDGE™ Safety Device integrated with a new low dead-space (LD) syringe, highlighting ongoing innovation in this space.

Thus, the combination of strong regulatory support, increasing prevalence of chronic diseases that require frequent injections, and continuous technological advancements by leading companies has made safety hypodermic needles the highest revenue-generating segment within the global needle safety devices market. Their widespread adoption in hospitals, clinics, and diagnostic laboratories underscores their role as a preferred and essential choice in healthcare, driving significant market growth.

As a result , the safety hypodermic needles category is projected to witness substantial growth within the overall needle safety devices market throughout the forecast period.

By Safety Mechanism: Active Safety Devices Category Dominates the Market

Active safety devices hold the largest share of 65% in 2025 and playing a dominant role in the global needle safety devices market due to their effectiveness in reducing needlestick injuries while offering flexibility and control to healthcare professionals. Unlike passive devices that activate automatically, active safety devices require manual engagement, such as sliding a protective sheath or pressing a button to cover the needle after use. This feature allows users to maintain precision during injections, blood collection, or IV procedures, making them particularly suitable for complex or high-risk clinical settings. The dominance of active safety devices is further supported by their compatibility with a wide range of medical procedures, cost-effectiveness compared to some fully passive systems, and strong regulatory encouragement for the adoption of safety-engineered devices. The combination of proven safety, procedural adaptability, and technological enhancements has positioned active safety devices as a key revenue-driving segment within the needle safety devices market.

By End-Users: Hospitals & Clinics Category Dominates the Market

Hospitals and clinics, as the primary end-user segment, are significantly boosting the overall market of needle safety devices due to the high volume of injectable procedures performed in these settings, including vaccinations, diagnostic blood draws, intravenous therapies, surgeries, and chronic disease management treatments such as diabetes care. These healthcare facilities handle a continuous flow of patients, which increases exposure risk to needlestick injuries and blood-borne infections among healthcare professionals. As a result, regulatory mandates, occupational safety guidelines, and infection prevention protocols increasingly require the use of safety-engineered devices such as retractable needles, auto-disable syringes, and needle shields. Hospitals, in particular, operate under strict compliance standards and accreditation requirements, prompting large-scale procurement of advanced safety devices to protect staff and patients. Additionally, the rising prevalence of chronic diseases, expansion of surgical procedures, growth in emergency care services, and increased vaccination activities within hospital and clinic networks further elevate injection volumes. This consistent and high-intensity usage environment makes hospitals and clinics the dominant drivers of demand, thereby accelerating adoption and sustained growth in the needle safety devices market globally.

Needle Safety Devices Market Regional Analysis

North America Needle Safety Devices Market Trends

North America is expected to account for the highest proportion of 38% of the needle safety devices market in 2025, out of all regions. This dominance is driven by increasing number of surgical procedures, large-scale vaccination programs, and widespread treatment of chronic diseases requiring injectable therapies significantly boost the demand for safety syringes and retractable needle devices in the region.

According to the Centers for Disease Control and Prevention (2024), an estimated 385,000 needlestick and other sharps-related injuries were sustained annually by hospital-based healthcare personnel in the United States. The increasing occurrence of accidental needlestick injuries among healthcare professionals has intensified concerns about the transmission of blood-borne infections such as HIV, hepatitis B, and hepatitis C. Consequently, hospitals and clinics are progressively adopting safety-engineered devices, including retractable syringes and shielded needles, to comply with occupational safety standards and safeguard medical staff. This growing emphasis on workplace protection is significantly driving the expansion of the needle safety devices market.

Moreover, according to the International Agency for Research on Cancer, the estimated number of new cancer cases in the United States was projected to reach 2.54 million in 2025 and was expected to increase further to 3.38 million by 2045. The increasing prevalence of cancer is substantially driving the growth of the needle safety devices market, as patients require frequent injectable therapies and blood-related procedures. Treatments such as chemotherapy, immunotherapy, targeted therapy, blood transfusions, and routine diagnostic blood tests involve repeated needle use, heightening the need for safer injection practices. This growing demand for protective and safety-engineered devices is consequently accelerating the expansion of the needle safety devices market. However, the increase in product development activities is further boosting the overall market of needle safety devices. For instance, in January 2026, Terumo Medical Corporation, a wholly owned subsidiary of Terumo Corporation, announced the U.S. launch of its SurTract™ Safety Syringe, featuring SafeR® passive safety technology developed by Roncadelle Operations S.r.l.

Thus, all the above-mentioned factors are anticipated to propel the market for needle safety devices in North America during the forecast period.

Europe Needle Safety Devices Market Trends

In Europe, the needle safety devices market is primarily driven by the rising volume of surgical procedures, extensive immunization initiatives, and the growing prevalence of chronic diseases that require regular injectable treatments.

According to the International Diabetes Federation (2025), the number of adults aged 20–79 years living with diabetes in Europe was estimated at 65.6 million in 2024 and was projected to rise to 72.4 million by 2050. A significant proportion of individuals with diabetes require daily insulin injections, routine blood glucose monitoring, and, in some cases, injectable GLP-1 receptor agonists. The frequent and long-term use of needles heightens the risk of accidental needlestick injuries for both healthcare providers and patients, especially in home-care environments. This growing need for safer injection practices is consequently driving the expansion of the needle safety devices market.

However, the increase in product development activities is further boosting the overall market of needle safety devices. For instance, In January 2024, Medmix Drug Delivery (Haselmeier) launched its passive needle safety device, SicuroJect™, at Pharmapack Europe held in Paris, further expanding its product portfolio in drug delivery solutions.

Hence, all the factors mentioned above are expected to drive the market for needle safety devices in Europe during the forecast period.

Asia-Pacific Needle Safety Devices Market Trends

In the Asia Pacific region, the needle safety devices market is driven by the growing number of surgical procedures, large-scale vaccination programs, and the increasing prevalence of chronic diseases requiring regular injections.

According to the International Agency for Research on Cancer, the estimated number of cancer cases in Japan was projected to reach 1.04 million in 2025 and is expected to increase to approximately 1.06 million by 2045. The increasing prevalence of cancer is playing a major role in driving the needle safety devices market, as oncology care relies heavily on injectable therapies and diagnostic needle-based procedures. Patients undergoing cancer treatment often receive chemotherapy, immunotherapy, targeted therapies, supportive injections, blood transfusions, and frequent blood tests. The continuous and intensive use of needles in these treatments elevates the risk of accidental needlestick injuries for healthcare workers, thereby reinforcing the need for advanced safety devices.

Moreover, according to the International Diabetes Federation (2025), the number of adults aged 20–79 years living with diabetes in Japan was estimated at 10.8 million in 2024 and is projected to decline to 9.4 million by 2050. A significant number of individuals with diabetes depend on daily insulin injections, routine blood glucose testing, and, in some cases, injectable non-insulin medications. The frequent and long-term use of needles elevates the likelihood of accidental needlestick injuries for both healthcare providers and patients, especially in home-care and self-administration settings. This increasing need for safer injection practices is consequently driving the growth of the needle safety devices market.

Thus, the factors mentioned above are expected to boost the market of needle safety devices across the Asia-Pacific region.

Who are the major players in the needle safety devices market?

The following are the leading companies in the needle safety devices market. These companies collectively hold the largest market share and dictate industry trends.

- BD

- Terumo Corporation

- Nipro

- ICU Medical

- B.Braun

- Retractable Technologies, Inc

- AdvaCare Pharma

- Medtronic

- Hindustan Syringes & Medical Devices Ltd

- Cardinal Health

- Vygon SA

- Gerresheimer AG

- West Pharmaceutical Services, Inc.

- UltiMed, Inc.

- Argon Medical Devices, Inc

- NOVO NORDISK A/S

- Kindly (KDL) Meditech

- Weigao Group

- Jiangsu Jichun Medical Devices Co., Ltd.

- Sarstedt AG & Co. KG, and others

How is the competitive landscape shaping the needle safety devices market?

The competitive landscape of the needle safety devices market is increasingly dynamic, characterized by intense innovation, strategic partnerships, and product diversification among key players. Companies are focusing on developing advanced safety-engineered devices, including passive and auto-retractable needles, safety syringes, and needle-free injection systems, to meet growing regulatory requirements and healthcare facility demands. Strategic collaborations, mergers, and acquisitions are enabling manufacturers to expand their product portfolios, strengthen global distribution networks, and enhance market penetration, particularly in emerging regions.

In addition to technological advancements, competition is driven by the emphasis on ergonomic designs, ease of use, and cost-effectiveness, as healthcare providers prioritize devices that enhance safety without compromising workflow efficiency. Leading players are also investing in research and development to introduce environmentally sustainable products, such as recyclable or eco-friendly syringes, catering to increasing demand for green healthcare solutions. The competitive environment is further shaped by regional expansion strategies, localized manufacturing, and proactive engagement with regulatory bodies to accelerate approvals and adoption.

Overall, the needle safety devices market is witnessing robust competition, where innovation, compliance, and strategic growth initiatives are the primary factors enabling companies to differentiate themselves, capture market share, and meet the evolving needs of healthcare providers globally.

Recent Developmental Activities in the Needle Safety Devices Market

- In January 2026, Terumo Medical Corporation, a wholly owned subsidiary of Terumo Corporation, announced the U.S. launch of its SurTract™ Safety Syringe, featuring SafeR® passive safety technology developed by Roncadelle Operations S.r.l.

- In January 2024, medmix Drug Delivery (Haselmeier) launched its passive needle safety device SicuroJect™ at Pharmapack Europe in Paris, further expanding its product portfolio.

- In May 2023, Nipro Medical Corporation received FDA approval for the Nipro SafeTouch Needle and the Nipro SafeTouch Needle with Syringe.

- In February 2023, Zephyrus Innovations (Zephyrus), a privately owned medical device company specializing in the design and manufacture of safety syringes and Closed System Transfer Devices (CSTDs), received its first 510(k) marketing clearance from the U.S. Food and Drug Administration (FDA) for its Aeroject™ 3 ml safety syringe.

- In January 2023, MTD Group, a global leader in medical devices, announced that its affiliate Pikdare S.p.A. had obtained FDA clearance for the DropSafe™ Sicura™ passive safety needle for intramuscular and subcutaneous administration of vaccines and other drugs.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Needle Safety Devices Market CAGR |

5.39% |

|

Key Companies in the Needle Safety Devices Market |

BD, Terumo Corporation, Nipro, ICU Medical, B.Braun, Retractable Technologies, AdvaCare Pharma, Medtronic, Hindustan Syringes & Medical Devices Ltd., Cardinal Health, Vygon SA, Gerresheimer AG, West Pharamaceuticak Services, Inc., UltiMed, Inc., Argon Medical Devices, Inc., Novo Nordisk A/S, Kindly (KDL) Meditech, Weigao Group, Jiangsu Jichun Medical Devices Co., Ltd., Sarstedt AG & CO. KG and others. |

|

Needle Safety Devices Market Segments |

by Product Type, by Safety Mechanism, by End-Users, and by Geography |

|

Needle Safety Devices Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Needle Safety Devices Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Needle Safety Devices Market Segmentation

Needle Safety Devices by Product Type Exposure

Safety Needles

Safety Hypodermic Needles

Safety Pen Needles

Safety Blood Collection Needles

Others

Safety IV Catheters

Safety Syringes

Needle Safety Devices Safety Mechanism Exposure

Active Safety Devices

Passive Safety Devices

Needle Safety Devices End-Users Exposure

Hospitals & Clinics

Ambulatory Surgical Centers

Homecare Settings

Others

Needle Safety Devices Geography Exposure

North America Needle Safety Devices Market

United States Needle Safety Devices Market

Canada Needle Safety Devices Market

Mexico Needle Safety Devices Market

Europe Needle Safety Devices Market

United Kingdom Needle Safety Devices Market

Germany Needle Safety Devices Market

France Needle Safety Devices Market

Italy Needle Safety Devices Market

Spain Needle Safety Devices Market

Rest of Europe Needle Safety Devices Market

Asia-Pacific Needle Safety Devices Market

China Needle Safety Devices Market

Japan Needle Safety Devices Market

India Needle Safety Devices Market

Australia Needle Safety Devices Market

South Korea Needle Safety Devices Market

Rest of Asia-Pacific Needle Safety Devices Market

Rest of the World Needle Safety Devices Market

South America Needle Safety Devices Market

Middle East Needle Safety Devices Market

Africa Needle Safety Devices Market

Needle Safety Devices Market Recent Industry Trends and Milestones (2022-2026):

|

Category |

Key Developments |

|

Needle Safety Devices Product Approvals |

Zephyrus Innovations- Aeroject™ 3ml safety syringe (FDA), MTD Group - DropSafeTM SicuraTM passive safety needle (FDA), Nipro - Nipro SafeTouch Needle and Nipro SafeTouch Needle with Syringe (FDA). |

|

Needle Safety Devices Product Launch |

Medmix launched SicuroJect™, Terumo launched SurTract™ Safety Syringe. |

|

Acquisition in the Needle Safety Devices Market |

Cardinal Health (US) acquired Advanced Diabetes Supply Group. |

|

Company Strategy |

BD - the company aims to drive sustainable growth by introducing new and improved medical devices, expanding manufacturing capacity, and enhancing supply chain resilience to ensure eliable delivery of critical products such as syringes, needles, and safety‑engineered solutions. Terumo Coproration- the company focuses on addressing challenges within medical settings by enhancing access to high-value healthcare solutions and advancing delivery technologies. Terumo also leverages digital innovations to optimize patient outcomes over the long term and emphasizes the development of cutting-edge drug-delivery systems, combination products, and integrated healthcare ecosystems across international markets. |

|

Emerging Technology |

Needle-Free Injection Technology, Smart and Digital Needle Technologies, Retractable IV Catheters and Safety Blood Collection Systems, Auto-Retractable Needles, Eco-Friendly and Recyclable Safety Devices and others. |

Impact Analysis

AI-Powered Innovations and Applications:

Artificial intelligence (AI) is increasingly transforming the needle safety devices market by enhancing device functionality, improving safety compliance, and optimizing healthcare workflows. AI-powered innovations enable features such as real-time monitoring of needle usage, automatic verification of safety mechanism activation, and predictive analytics to identify high-risk procedures or user errors. These applications not only reduce the incidence of needlestick injuries but also provide valuable data for hospital administrators to track device utilization, ensure regulatory compliance, and implement targeted training programs for healthcare professionals. Additionally, AI integration facilitates the development of smarter safety devices, such as connected syringes and catheters, which can alert users if the needle is not properly shielded or retracted. By combining advanced safety mechanisms with AI-driven insights, these innovations are improving operational efficiency, enhancing occupational safety, and driving greater adoption of needle safety devices across hospitals, clinics, and diagnostic laboratories, thereby strengthening market growth and technological advancement in the sector.

U.S. Tariff Impact Analysis on Needle Safety Devices Market:

The imposition of tariffs in the United States has had a notable impact on the needle safety devices market, influencing pricing, supply chains, and overall market dynamics. Increased import duties on medical devices and raw materials have raised the cost of production for manufacturers relying on overseas components, leading to higher prices for end-users, including hospitals, clinics, and diagnostic laboratories. These tariffs have also prompted companies to reassess their supply chains, with many seeking to source materials locally or diversify manufacturing locations to mitigate cost pressures. Despite these challenges, the growing demand for safety-engineered needles, driven by regulatory compliance, rising healthcare expenditure, and the need to prevent occupational injuries, has helped sustain market growth. Companies such as BD (Becton, Dickinson and Company), Terumo Corporation, and ICU Medical have adopted strategic measures, including regional production expansions and pricing adjustments, to offset tariff-related impacts, ensuring continued availability and adoption of needle safety devices in the U.S. market.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Key takeaways from the needle safety devices market report study

- Market size analysis for the current needle safety devices market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the needle safety devices market.

- Various opportunities available for the other competitors in the needle safety devices market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current needle safety devices market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the needle safety devices market growth in the future?

Frequently Asked Questions for the Needle Safety Devices Market

1. What is the growth rate of the needle safety devices market?

The needle safety devices market is estimated to grow at a CAGR of 5.39% during the forecast period from 2026 to 2034.

2. What is the market size for needle safety devices?

The global needle safety devices market sie is expected to increase from USD 2,284.15 million in 2025 to USD 3,637.49 million by 2034, reflecting strong and sustained growth.

3. Which region has the highest share in the needle safety devices market?

North America is expected to lead the global needle safety devices market due to strong awareness of needlestick injuries, strict safety regulations, and widespread adoption of safety-engineered injection devices. Market growth is supported by the rising prevalence of chronic diseases, expanding vaccination programs, and increasing demand for home-based treatments. Additionally, advancements in automatic needle shielding and retractable technologies are enhancing safety and usability, driving steady growth in the region.

4. What are the drivers for the needle safety devices market?

The growth of the needle safety devices market is largely attributed to the increasing number of accidental needlestick injuries and the heightened concern over the transmission of blood-borne infections among healthcare professionals. The rising burden of chronic conditions that require repeated injections, along with expanding vaccination initiatives and higher healthcare spending, is further contributing to market expansion. Moreover, the shift toward home healthcare and self-administration of injectable therapies is creating additional demand for safer devices. Continuous innovations in passive and auto-retractable technologies are improving safety, ease of use, and regulatory compliance, thereby driving overall market growth.

5. Who are the key players operating in the needle safety devices market?

Some of the key needle safety devices companies operating in the needle safety devices market include - BD, Terumo Corporation, Nipro, ICU Medical, B.Braun, Retractable Technologies, AdvaCare Pharma, Medtronic, Hindustan Syringes & Medical Devices Ltd., Cardinal Health, Vygon SA, Gerresheimer AG, West Pharamaceuticak Services, Inc., UltiMed, Inc., Argon Medical Devices, Inc., Novo Nordisk A/S, Kindly (KDL) Meditech, Weigao Group, Jiangsu Jichun Medical Devices Co., Ltd., Sarstedt AG & CO. KG and others.