Neurostimulation Devices Market Summary

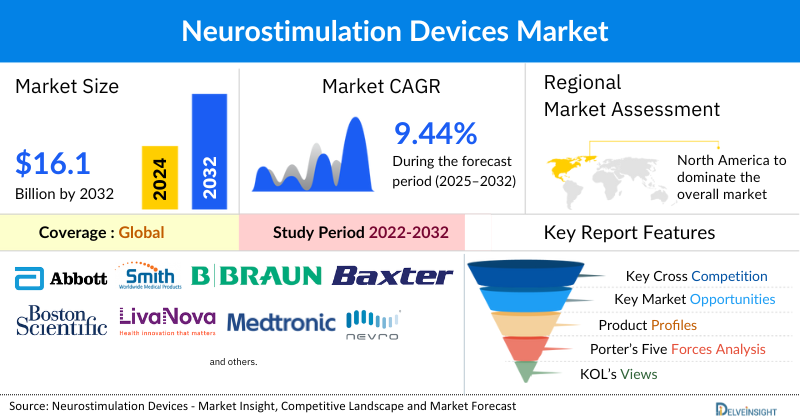

- The global neurostimulation devices market size is expected to increase from USD 7,862.04 million in 2024 to USD 16,111.10 million by 2032, reflecting strong and sustained growth.

- The global neurostimulation devices market is growing at a CAGR of 9.44% during the forecast period from 2025 to 2032.

- The market for neurostimulation devices is growing rapidly, fueled by the rising global prevalence of chronic diseases like pain, epilepsy, and depression. This growth is also driven by significant technological advancements that have made devices smaller, smarter, and more effective. Favorable regulatory policies and better reimbursement coverage are also making these treatments more accessible. Overall, the increasing demand for effective, long-term therapeutic options for neurological and chronic conditions is creating a strong and sustained market.

- The leading companies operating in the neurostimulation devices market include Abbott Laboratories, Smith’s Medical, B. Braun Melsungen AG, Baxter International Inc., Boston Scientific Corp., LivaNova PLC., Medtronic, Nevro Corp., Abbott, Stryker, Omron Corporation, Stimwave LLC, Koninklijke Philips NV, Kimberly Clark Corporation, EndoStim Inc., Aleva neurotherapeutics SA, Cyberonics, DyAnsys, Inc., NanoVibronix, Inc., ElectroCore Inc., and Others.

- North America is expected to remain a dominant force in the neurostimulation devices market, driven by the high burden of chronic pain and neurological disorders, increasing awareness initiatives, supportive government programs, and continuous product innovations with frequent FDA approvals.

- In the device type segment of the neurostimulation devices market, the spinal cors stimulators devices category is estimated to account for the largest market share in 2024.

Request for unlocking the report of the @ Neurostimulation Devices Market Forecast

Neurostimulation Devices Market Size and Forecasts

|

Report Metrics |

Details |

|

2024 Market Size |

USD 7,862.04 million |

|

2032 Projected Market Size |

USD 16,111.10 million |

|

Growth Rate (2025-2032) |

9.44% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Consolidated |

Factors Contributing to the Growth of the Neurostimulation Devices Market

- Rising Prevalence of Chronic and Neurological Disorders leading to a Surge in the Neurostimulation Devices Market: There is a growing global burden of conditions that neurostimulation devices are designed to treat. This includes the increasing incidence of chronic pain, epilepsy, Parkinson's disease, and treatment-resistant depression. As these conditions become more widespread, the demand for effective, long-term therapeutic solutions has surged.

- Technological Advancements: continuous innovation is acting as a powerful catalyst for market expansion. Recent advances include the development of smaller, more powerful, and rechargeable devices, which reduce surgical burden and extend device lifespan, enhancing patient convenience. The emergence of “closed-loop” neurostimulation systems, such as adaptive deep brain stimulation, represents a paradigm shift by enabling real-time monitoring of neural activity and delivering stimulation only when required. This not only enhances therapeutic efficacy but also minimizes side effects and optimizes energy use. Moreover, the expanding application of neurostimulation in conditions beyond movement disorders, such as depression, chronic pain, epilepsy, and even sleep disorders, broadens the addressable market significantly. Collectively, the convergence of rising disease prevalence and rapid technological progress is reinforcing neurostimulation’s role as a transformative solution in managing complex, long-term neurological and chronic conditions.

- Shift Towards Minimally Invasive Procedures: Both patients and healthcare providers are increasingly favoring less invasive treatment options, a trend that strongly supports the adoption of neurostimulation devices. Implantable neurostimulation procedures are often regarded as a less invasive alternative to traditional surgeries for managing chronic pain, movement disorders, or urological conditions. Compared with open surgical interventions, they typically offer smaller incisions, shorter hospital stays, faster recovery times, and reduced postoperative complications, which translates into improved patient satisfaction and lower healthcare costs.

Beyond these procedural benefits, innovations such as percutaneous implantation techniques, miniaturized leads, and MRI-compatible devices have further reduced surgical risks while making these procedures more accessible to a broader patient population. Importantly, minimally invasive neurostimulation is also gaining traction in outpatient and ambulatory surgical settings, aligning with the healthcare industry’s shift toward value-based care and cost efficiency. As reimbursement policies in many markets expand to include neurostimulation therapies, and as device manufacturers continue refining delivery methods, the less invasive nature of these interventions is expected to remain a major adoption driver across both developed and emerging healthcare systems.

Neurostimulation Devices Market Report Segmentation

This neurostimulation devices market report offers a comprehensive overview of the global neurostimulation devices market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by by Device Type (Spinal Cord Stimulators, Deep Brain Stimulators, Sacral Nerve Stimulators, Vagus Nerve Stimulators, and Others), Application (Pain Management, Bowel and Bladder Control, Parkinson's Disease, Epilepsy, and Others), Type (Invasive, Non-Invasive), End-Users (Hospitals, Specialty Clinics, and Others), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing neurostimulation devices market.

Neurostimulation devices, also known as neurostimulators or neuromodulation devices, are medical technologies that use electrical impulses to purposefully modulate or change the activity of the nervous system. By delivering mild electrical signals to specific nerves or areas of the brain or spinal cord, these devices can disrupt pain signals, alter brain activity, or restore lost function.

The market for neurostimulation devices is experiencing substantial growth, driven by a combination of factors. The rising global prevalence of chronic diseases such as chronic pain, neurological disorders like Parkinson's disease, epilepsy, and essential tremor, and mental health conditions like treatment-resistant depression is a primary driver. This increased disease burden has created a greater demand for effective, long-term therapeutic options. Furthermore, significant technological advancements have made these devices more effective and user-friendly. Innovations such as smaller, rechargeable implants, "closed-loop" systems that respond to neural activity in real time, and the development of non-invasive options like Transcranial Magnetic Stimulation (TMS) are expanding their adoption. Additionally, a more favorable regulatory environment and improved reimbursement policies are making these treatments more accessible to patients. This includes regulatory bodies approving a wider range of neurostimulators for new applications and insurers providing better coverage. Finally, the aging global population, which has a higher incidence of age-related neurological disorders and chronic pain, further contributes to the market's strong growth trajectory.

Get More Insights into the Report @ Neurostimulation Devices Market Trends

What are the latest Neurostimulation Devices Market Dynamics and Trends?

The growing market for neurostimulation devices is primarily driven by the escalating prevalence of various neurological conditions and the continuous introduction of innovative products by key industry players.

According to a major analysis from the Global Burden of Disease (GBD) Study 2021, published in The Lancet Neurology, neurological conditions collectively affected 3.4 billion people worldwide in 2021, representing 43% of the global population. This made them the leading cause of ill health and disability globally. The most prevalent of these conditions were tension-type headaches (affecting around 2 billion people) and migraines (affecting approximately 1.1 billion). Neurostimulation devices, such as those targeting the occipital nerves, are effective in managing chronic headaches and migraines by interrupting pain signals. Furthermore, the number of people with diabetic neuropathy has more than tripled since 1990, reaching 206 million in 2021, and neurostimulation devices are increasingly used to treat the nerve damage and associated pain.

The World Health Organization (WHO) reports that epilepsy affects around 50 million people globally. Neurostimulation devices like vagus nerve stimulators and responsive neurostimulators offer a critical treatment option, especially for patients with drug-resistant epilepsy, by reducing the frequency and severity of seizures.

The rise in cancer cases also contributes to the market. According to the latest GLOBOCAN 2022 estimates, there were about 20 million new cancer cases and 9.7 million deaths worldwide, with a 5-year prevalence of 53.5 million cases. The most common cancers were lung (2.48M cases), breast (2.30M), colorectal (1.93M), prostate (1.47M), and stomach (0.97M). Overall, 1 in 5 people will develop cancer during their lifetime, and 1 in 9 men and 1 in 12 women will die from it. While incidence is higher in high-income countries, mortality rates remain disproportionately high in low- and middle-income regions due to limited access to early detection and treatment. Looking ahead, global cancer cases are projected to rise to 35 million by 2050, a 77% increase from 2022. Many cancer patients experience neuropathic pain, which is often difficult to manage with conventional treatments. Advanced neurostimulation devices are being used to provide significant pain relief for these patients.

The continuous stream of new product introductions and regulatory approvals is a significant driver of the neurostimulation devices market. A notable example is the FDA approval in February 2025 of Medtronic’s BrainSense Adaptive Deep Brain Stimulation (aDBS) system for Parkinson’s disease, the first adaptive or “closed-loop” DBS technology to reach the market. Unlike conventional DBS systems that deliver fixed, continuous stimulation, the aDBS platform monitors patients’ brain activity in real time, focusing on local field potentials (LFPs) and beta-band oscillations, which are biomarkers of Parkinson’s motor symptoms. The system then dynamically adjusts stimulation parameters to align with the patient’s neurological state across various conditions, such as medication cycles, rest, and physical activity. This capability not only enhances therapeutic precision but also reduces unnecessary stimulation, potentially improving outcomes while minimizing side effects like dyskinesia. Moreover, the addition of the BrainSense Electrode Identifier simplifies programming and enables clinicians to personalize therapy more efficiently, setting a new benchmark in the evolution of brain modulation technologies.

The neurostimulation devices market faces significant restraints and challenges despite its growth. A primary obstacle is the high cost of both the devices and the surgical procedures required for implantation, which limits accessibility, particularly in developing countries. This issue is compounded by a shortage of trained professionals, as the successful application of this therapy requires a specialized, multidisciplinary team, and the lack of such expertise can lead to suboptimal patient outcomes. Furthermore, the market is constrained by stringent regulatory frameworks; neurostimulation devices are classified as high-risk, leading to a long and complex approval process that can delay the commercialization of new innovations. Finally, patient and physician hesitation also serves as a barrier. Patients may be apprehensive about undergoing an invasive surgery, while some physicians may lack awareness or prefer traditional, more familiar treatment methods over neurostimulation.

Neurostimulation Devices Market Segment Analysis

Neurostimulation Devices Market by Device Type (Spinal Cord Stimulators, Deep Brain Stimulators, Sacral Nerve Stimulators, Vagus Nerve Stimulators, and Others), Application (Pain Management, Bowel and Bladder Control, Parkinson's Disease, Epilepsy, and Others), Type (Invasive, Non-Invasive), End-Users (Hospitals, Specialty Clinics, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Device Type: Spinal Cord Stimulator Dominates the Market

The spinal cord stimulator category accounted for over 45% of the global neurostimulation devices market share in 2024, driven largely by mainstream adoption. According to the World Health Organization (2023), there were approximately 619 million cases of lower back pain (LBP), a figure expected to climb to 843 million by 2050. In parallel, the European Pain Federation (2023) reported that around 740 million people globally experience at least one episode of severe pain during their lifetime, with nearly 20% developing chronic pain lasting more than three months. This growing burden of chronic pain highlights the urgent need for effective and sustainable pain management solutions.

Spinal cord stimulators (SCS) have gained traction as they provide a minimally invasive, drug-free, and reversible therapy option. By delivering targeted electrical impulses to the spinal cord, these devices block pain signals before they reach the brain, significantly improving patient quality of life. The rising incidence of chronic pain disorders is, therefore, expected to be a major driver of SCS adoption worldwide.

Furthermore, findings published by the NIH (2023) revealed that Failed Back Surgery Syndrome (FBSS) affects 10-40% of patients following spinal surgeries. With the growing volume of spinal procedures for conditions such as herniated discs, spinal stenosis, and degenerative disc disease, the prevalence of FBSS continues to rise. Since repeated surgeries carry higher risks and often fail to deliver lasting pain relief, spinal cord stimulators are increasingly being recognized as an effective alternative. Their ability to reduce dependency on opioids, improve functional outcomes, and lower long-term healthcare costs makes them a preferred treatment choice, particularly for patients with FBSS and chronic neuropathic pain.

Emerging regulatory approvals are catalyzing market growth by enabling easier access to advanced SCS technologies:

In April 2024, Medtronic gained FDA approval for Inceptiv™, the first closed-loop SCS system to automatically adjust stimulation using real-time biological feedback (evoked compound action potentials, or ECAPs), maintaining optimal therapy even during daily movement. It is also the only FDA-approved closed-loop system offering full-body 3T MRI access with no restrictions, and is touted as the smallest and thinnest fully implantable SCS device.

In April 2023, Biotronik received FDA approval for its Prospera SCS System, featuring RESONANCE, the first multiphase stimulation paradigm, and Embrace One, a patient-centric care model offering automatic, objective, daily remote monitoring, ongoing management, and support. The system also includes HomeStream remote management, rechargeable implants, and full-body MRI compatibility

Each of these advancements highlights the trajectory of the SCS market, shifting from traditional, fixed-output devices requiring routine in-clinic adjustments, to intelligent, adaptive systems that emphasize remote care, personalization, and workflow efficiency.

By Application: Pain Management Categroy Dominate the Market

The pain management segment dominates the neurostimulation devices market, contributing nearly 58% of global revenue in 2024. This domicance is primarily due to the vast and growing population suffering from chronic pain, a condition that poses a significant global health and economic burden. The escalating opioid crisis has propelled a major shift in healthcare, favoring non-addictive, drug-free alternatives like neurostimulation. These devices are increasingly seen as a safe and effective long-term solution. This trend is further amplified by significant technological advancements, including the development of more sophisticated, user-friendly, and effective devices such as spinal cord stimulators. These innovations, coupled with favorable reimbursement policies and increasing awareness among both patients and healthcare providers, have solidified pain management's leading position in the market.

By Type: Invasive Categroy Dominate the Market

In 2024, the invasive neurostimulation devices category accounted for over 95% of the global market share due to their established clinical effectiveness, broad adoption, and strong support from regulatory approvals and reimbursement frameworks. Invasive devices such as spinal cord stimulators, deep brain stimulators, vagus nerve stimulators, and sacral nerve stimulators are widely used for chronic pain, Parkinson’s disease, epilepsy, depression, and urinary incontinence, with proven outcomes that drive physician and patient confidence.

Recent technological advancements, including closed-loop stimulation, multiphase waveforms, miniaturized and MRI-compatible implants, and remote monitoring, have further enhanced their safety, efficacy, and usability. Chronic pain remains the largest driver, with spinal cord stimulators dominating given the rising prevalence of lower back pain and failed back surgery syndrome. Additionally, major players such as Medtronic, Abbott, Boston Scientific, Nevro, Biotronik, and Saluda continue to invest heavily in invasive solutions, unlike the fragmented non-invasive segment, which remains limited by narrower clinical validation and adoption. Together, these factors solidified the dominance of invasive neurostimulation devices in the global market in 2024.

By End-Users: Hospitals Dominate the Market

Hospitals dominated the global neurostimulation devices market in 2024, accounting for over 85% of the market share, and are expected to maintain leadership in terms of both revenue growth and CAGR during the forecast period. This dominance stems from the fact that hospitals serve as the primary centers for conducting complex surgical implantations of devices such as spinal cord stimulators, deep brain stimulators, and vagus nerve stimulators, which require advanced infrastructure, skilled neurosurgeons, and multidisciplinary care teams. Hospitals also provide comprehensive pre-operative evaluation, intraoperative monitoring, and post-operative rehabilitation, making them the preferred treatment setting for both patients and physicians. Furthermore, hospitals benefit from better reimbursement frameworks, enabling greater adoption of high-cost implantable neurostimulation devices. The rising burden of chronic pain, neurological disorders, and failed back surgery syndrome has increased hospital admissions and surgical volumes, further driving utilization. In addition, continuous technological upgrades, partnerships with MedTech companies, and participation in clinical trials strengthen hospitals’ role as the central hubs for neurostimulation therapies. In contrast, outpatient centers and clinics, while growing, are largely limited to follow-up care or non-invasive neurostimulation, which contributes to their smaller market share. These factors collectively explain why hospitals remain the dominant end user in the neurostimulation devices market.

Neurostimulation Devices Market Regional Analysis

North America Neurostimulation Devices Market Trends

North America, led by the U.S., accounted for a dominant ~55% share of the global neurostimulation devices market in 2024, due to a combination of factors that create a highly favorable environment for the development, adoption, and commercialization of these technologies.

According to the CDC (2023), in 2021, 20.9% of U.S. adults (51.6M) reported chronic pain, with 6.9% (17.1M) experiencing high-impact chronic pain that limits daily activities. Additionally, around 2.9 million adults were living with active epilepsy (CDC, 2024), while the Alzheimer’s Association (2024) reported 6.9 million Americans aged 65+ with Alzheimer’s disease. Parkinson’s disease prevalence is also rising, with nearly 90,000 new cases annually and over 1 million people affected, expected to reach 1.2 million by 2030 (Parkinson’s Foundation, 2022).

Key drivers of growth include:

- Robust Healthcare Infrastructure: The United States and Canada have highly developed healthcare systems with advanced surgical centers, specialized neurological clinics, and a strong network of hospitals. This infrastructure facilitates the early adoption of innovative medical devices and provides a setting where complex procedures, such as implanting neurostimulators, can be performed safely and effectively.

- Favorable Regulatory and Reimbursement Landscape: The presence of regulatory bodies like the U.S. Food and Drug Administration (FDA) and a relatively streamlined process for device approvals, especially for breakthrough therapies, accelerates market entry. Crucially, favorable reimbursement policies from both private and public insurers in the region provide financial coverage for these expensive procedures. This ensures that the high cost of neurostimulation devices and their implantation does not become a significant barrier for patients, driving demand.

- High Incidence of Neurological Disorders: North America has a significant patient population suffering from a wide array of neurological and chronic pain conditions. The high prevalence of chronic pain, Parkinson's disease, epilepsy, and treatment-resistant depression creates a large and consistent demand for alternative and advanced treatment options.

- Early Adoption of Technology and High Awareness: Patients and healthcare providers in North America have a high level of awareness regarding the latest medical technologies. There is a strong willingness to adopt innovative therapies that offer improved outcomes and a better quality of life, particularly for conditions that are difficult to manage with conventional medication.

- Presence of Key Market Players: The region is home to many of the world's leading neurostimulation device manufacturers, including Medtronic, Abbott, and Boston Scientific. These companies are at the forefront of research and development, continuously introducing new, more advanced, and patient-friendly products. Their strong presence and focus on innovation further solidify North America's market dominance

Europe Neurostimulation Devices Market Trends

The neurostimulation devices market in Europe is dynamic and expanding, ranking second only to North America and accounting for approximately 21% of the global market share in 2024. This growth is driven by several key trends, including the rising prevalence of chronic conditions and an aging population, which together create a significant patient pool for conditions like Parkinson's disease, chronic pain, and epilepsy. Technological advancements are also a major catalyst, with the market seeing a rise in "smart," closed-loop systems, as well as smaller, rechargeable, and non-invasive devices that improve patient outcomes and comfort. Furthermore, while the regulatory and reimbursement landscape can be complex, many major European countries have established frameworks that support the adoption of these technologies. This growth is further propelled by the strong presence of global industry leaders, which drives continuous innovation and new product launches in the region.

- Germany: Germany is the dominant market leader in Europe, holding the largest market share in 2024. This is driven by its robust and well-funded healthcare system, a large aging population susceptible to neurological conditions, and a strong focus on advanced, effective pain management solutions. The country's strong reimbursement policies also play a crucial role in supporting the adoption of these expensive devices.

- United Kingdom: The UK market is a significant contributor to the European sector. It is projected to experience a strong CAGR of over 11% from 2025 to 2032. The growth is fueled by a high prevalence of chronic pain and neurological disorders like epilepsy and Parkinson's disease, as well as government initiatives aimed at improving treatments for neurodegenerative diseases. However, the lack of widespread NHS funding for some neurostimulation therapies can present a challenge.

- France: France is another key market with a growing demand for neurostimulation devices, particularly for pain management, which accounts for the largest segment. The country is seeing a rise in neurological disorders and has a growing geriatric population, which are major drivers. Government initiatives to digitize and modernize the healthcare system are also expected to fuel the market. In 2022, France saw over 8,700 neuromodulation procedures performed, with Spinal Cord Stimulation being the most common.

- Italy: The Italian market is also contributing to the overall growth trend in Europe. Key drivers include the increasing incidence of neurological disorders, an aging population, and technological advancements. While it is a smaller market compared to Germany and the UK, it is experiencing a steady growth rate, with a projected CAGR of 7.8% from 2025 to 2032.

Asia-Pacific Neurostimulation Devices Market Trends

The Asia-Pacific region is emerging as the fastest-growing market for neurostimulation devices globally, with a projected compound annual growth rate (CAGR) of over 12%. This rapid expansion is driven by a unique set of regional trends and dynamics.

Key Market Trends

- Increasing Prevalence of Neurological Disorders and Chronic Pain: Similar to Western nations, the Asia-Pacific region is grappling with a rising burden of neurological diseases, including epilepsy, Parkinson's disease, and chronic pain. The aging population in countries like Japan and China is a significant factor, as these conditions are more common in older adults.

- Technological Adoption and Innovation: While historically a more conservative market, there is a growing willingness to adopt advanced medical technologies. This trend is supported by an increasing focus on R&D and a shift towards minimally invasive procedures. The integration of "smart" features, such as AI and machine learning, into neurostimulation devices for personalized therapy is a key trend.

- Improving Healthcare Infrastructure and Access: Rapid economic development in key countries like China and India is leading to increased healthcare spending, the establishment of modern hospitals, and a growing number of skilled medical professionals. This improves access to advanced treatments that were previously unavailable.

- Favorable Government Initiatives and Policies: Governments in the region are recognizing the need for better neurological care and are implementing supportive policies. This includes increased funding for research, simplified regulatory pathways, and initiatives to improve public health and medical technology.

Key Countries and Statistics

- China: As the largest country in the region, China is a major market driver. It has a high prevalence of neurological conditions, with some reports indicating the country has the largest number of Parkinson's disease patients in the world. The combination of a massive population and rising healthcare expenditure makes it a primary target for international device manufacturers. China is also rapidly developing its own medical device industry, making it a significant player in the global market.

- Japan: Japan holds a dominant position in the Asia-Pacific market due to its well-established healthcare infrastructure and a highly advanced medical technology sector. The country's very large and rapidly aging population creates a strong, sustained demand for neurostimulation devices, particularly for managing age-related conditions.

- India: India is one of the fastest-growing markets in the region. The growth is fueled by a large patient population, increasing awareness of neurostimulation therapies, and rising healthcare expenditures. While the market is still developing, the potential for growth is immense, with both international and domestic companies investing in the country.

- Australia: Australia has a mature and well-regulated healthcare system, with a high per-capita adoption rate of neurostimulation devices. It is often a key market for new product launches by international companies and serves as a benchmark for trends in the region.

Who are the major players in the Neurostimulation Devices Market?

The following are the leading companies in the Neurostimulation Devices market. These companies collectively hold the largest market share and dictate industry trends.

- Abbott Laboratories

- Smith’s Medical

- B. Braun Melsungen AG

- Baxter International Inc.

- Boston Scientific Corp.

- LivaNova PLC.

- Medtronic

- Nevro Corp.

- Abbott

- Stryker

- Omron Corporation

- Stimwave LLC

- Koninklijke Philips NV

- Kimberly Clark Corporation

- EndoStim Inc.

- Aleva neurotherapeutics SA

- Cyberonics

- DyAnsys, Inc.

- NanoVibronix, Inc.

- ElectroCore Inc., and others

How is the competitive landscape shaping the neurostimulation devices market?

The competitive landscape of the neurostimulation devices market is moderately consolidated, with a few major players holding a significant market share. Companies such as Medtronic, Boston Scientific, and Abbott Laboratories are the key industry leaders, leveraging their extensive R&D investments, broad product portfolios, and strong global distribution networks to maintain their dominance. The market's competitive dynamics are shaped by a continuous push for innovation, with companies focusing on developing more advanced technologies like closed-loop and wireless systems to improve patient outcomes and address a wider range of conditions. Strategic activities, including mergers, acquisitions, and collaborations, are common as established players seek to expand their product offerings and geographical reach, while smaller, specialized firms often enter the market with niche, technologically advanced products, such as next-generation spinal cord stimulators or non-invasive wearables. This combination of established giants and agile innovators creates a landscape where product differentiation, clinical evidence, and strategic partnerships are crucial for success.

Recent Developmental Activities in the Neurostimulation Devices Market

- In February 2025, the U.S. FDA has approved Medtronic's BrainSense Adaptive Deep Brain Stimulation (aDBS) system, which is the first of its kind for treating Parkinson's disease.

- In December 2024, Nyxoah launched its Genio neurostimulator in England for the treatment of moderate to severe obstructive sleep apnea (OSA), with the first implants performed at University College London Hospitals (UCLH).

- In December 2024, Onward’s ARC-EX received FDA de novo classification and U.S. market authorization.

- In April 2024, FDA-approved Medtronic’s first closed-loop rechargeable Inceptiv™ Closed-Loop Spinal Cord Stimulator.

- In February 2024, the FDA approved an expanded indication for the WaveWriter SCS Systems to treat chronic low back and leg pain in patients without prior back surgery (non-surgical back pain).

- In January 2024, FDA-approved Abbott Liberta RC DBS system, a rechargeable deep brain stimulator, notable for being the smallest DBS device with the longest battery life.

|

Report Metrics |

Details |

| Study Period | 2022 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2032 |

| Neurostimulation Devices Market CAGR | 9.44% |

| Key Companies in the Neurostimulation Devices Market | Abbott Laboratories, Smith’s Medical, B. Braun Melsungen AG, Baxter International Inc., Boston Scientific Corp., LivaNova PLC., Medtronic, Nevro Corp., Abbott, Stryker, Omron Corporation, Stimwave LLC, Koninklijke Philips NV, Kimberly Clark Corporation, EndoStim Inc., Aleva neurotherapeutics SA, Cyberonics, DyAnsys, Inc., NanoVibronix, Inc., ElectroCore Inc., and Others. |

| Neurostimulation Devices Market Segments | by Device Type, by Application, by Type, by End-Users, and by Geography |

| Neurostimulation Devices Regional Scope | North America, Europe, Asia Pacific, Middle East, Africa, and South America |

| Neurostimulation Devices Country Scope | U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Neurostimulation Devices Market Segmentation

Neurostimulation Devices Device Type Exposure

- Spinal Cord Stimulators

- Deep Brain Stimulators

- Sacral Nerve Stimulators

- Vagus Nerve Stimulators

- Others

Neurostimulation Devices Application Exposure

- Pain Management

- Bowel and Bladder Control

- Parkinson's Disease

- Epilepsy

- Others

Neurostimulation Devices Type Exposure

- Invasive

- Non-Invasive

Neurostimulation Devices End-Users Exposure

- Hospitals

- Specialty Clinics

- Others

Neurostimulation Devices Geography Exposure

- North America Neurostimulation Devices Market

-

- United States Neurostimulation Devices Market

- Canada Neurostimulation Devices Market

- Mexico Neurostimulation Devices Market

- Europe Neurostimulation Devices Market

- United Kingdom Neurostimulation Devices Market

- Germany Neurostimulation Devices Market

- France Neurostimulation Devices Market

- Italy Neurostimulation Devices Market

- Spain Neurostimulation Devices Market

- Rest of Europe Neurostimulation Devices Market

- Asia-Pacific Neurostimulation Devices Market

- China Neurostimulation Devices Market

- Japan Neurostimulation Devices Market

- India Neurostimulation Devices Market

- Australia Neurostimulation Devices Market

- South Korea Neurostimulation Devices Market

- Rest of Asia-Pacific Neurostimulation Devices Market

- Rest of the World Neurostimulation Devices Market

- South America Neurostimulation Devices Market

- Middle East Neurostimulation Devices Market

- Africa Neurostimulation Devices Market

Neurostimulation Devices Market Recent Industry Trends and Milestones (2022-2025):

| Category | Key Developments |

| Neurostimulation Devices Product Launches | Medtronic's BrainSense Adaptive Deep Brain Stimulation (aDBS) system, Medtronic ‘s Inceptiv™ Spinal Cord Stimulator, Nyxoah launched its Genio neurostimulator, Abbott Liberta RC DBS system |

| Neurostimulation Devices Regulatory Approvals | Medtronic - BrainSense Adaptive Deep Brain Stimulation (aDBS) system (FDA), Boston and Scientific - WaveWriter SCS System (FDA), Onward’s ARC-EX (FDA) |

| Partnerships in the Neurostimulation Devices Market |

|

| Acquisitions in the Neurostimulation Devices Market |

|

| Company Strategy |

|

| Emerging Technology |

|

Impact Analysis:

AI-Powered Innovations and Applications:

The integration of artificial intelligence (AI) is having a transformative impact on the neurostimulation devices market, moving the field from static, one-size-fits-all treatments to dynamic, personalized, and highly effective therapies. AI's core application lies in the development of closed-loop systems, which use machine learning algorithms to analyze a patient's neural and physiological data in real-time. This allows the device to automatically adjust stimulation parameters, such as intensity and frequency, to a patient's specific needs, thereby optimizing therapeutic effects and minimizing side effects. For example, in spinal cord stimulation (SCS), AI-powered devices can identify pain signals and deliver targeted stimulation only when needed, leading to more sustained pain relief and better patient outcomes. Furthermore, AI is being used in predictive modeling to help clinicians identify which patients are most likely to respond to a specific neurostimulation therapy, improving patient selection and reducing the burden of costly and invasive procedures that may not be effective. This paradigm shift, driven by AI, is making treatments more precise, efficient, and personalized, ultimately expanding the market's potential by improving the quality of life for a broader range of patients with chronic pain, epilepsy, and movement disorders.

U.S. Tariff Impact Analysis on the Neurostimulation Devices Market:

The implementation of U.S. tariffs has introduced significant volatility and uncertainty into the global neurostimulation devices market. The impact is felt through several key channels:

First, tariffs directly increase the cost of imported neurostimulation devices and their components, which can lead to higher prices for U.S. healthcare providers and patients. This economic pressure is particularly acute for countries with significant medical device exports to the U.S., such as India and the European Union, which have faced duties of 20% or more. While these tariffs are designed to encourage domestic production, they can also disrupt existing supply chains and make it more difficult for foreign companies to compete, potentially limiting the availability of certain devices and increasing the financial burden on the U.S. healthcare system.

Second, the tariffs are prompting a reshaping of global supply chains. Companies are now considering diversifying their manufacturing and sourcing strategies to mitigate the risks associated with these trade barriers. This could involve relocating production to countries with more favorable trade agreements with the U.S., or expanding domestic manufacturing capacity within the U.S. to avoid tariffs altogether. This shift, while a long-term strategic move, creates near-term disruptions and investment uncertainty.

Finally, the tariffs have created a complex and challenging environment for market access. For companies in tariff-hit nations, the high duties act as a non-tariff barrier, making it more difficult to penetrate the lucrative U.S. market. This dynamic not only affects the profitability of these exporters but also influences their long-term growth and investment strategies, potentially redirecting their focus toward other global markets with more stable trade relationships.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends:

| Company Name | Total Funding | Main Products | Stage of Development | Core Technology |

| SetPoint Medical | $140 million | SetPoint System | Seed D and C | Neuroimmune modulation therapy for adults living with moderate-to-severe rheumatoid arthritis (RA), as well as advancement of the company’s pipeline in other autoimmune conditions. |

| Neuros Medical | $56 million | Altius nerve stimulation system | Series D | For the development and commercialization of its neurostimulation therapy for chronic neuropathic pain, especially post-amputation pain. |

| Phagenesis | $42 million | Phagenyx® neurostimulation system | Series D | To treat swallowing dysfunction (dysphagia) resulting from brain injury, such as stroke. The technology uses pharyngeal electrical stimulation (PES) to restore neurological control of swallowing. |

Key takeaways from the neurostimulation devices market report study

- Market size analysis for the current neurostimulation devices market size (2024), and market forecast for 8 years (2025 to 2032)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the neurostimulation devices market.

- Various opportunities available for the other competitors in the neurostimulation devices market space.

- What are the top-performing segments in 2024? How these segments will perform in 2032?

- Which are the top-performing regions and countries in the current neurostimulation devices market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the neurostimulation devices market growth in the future?

Frequently Asked Questions for the Neurostimulation Devices Market

1.What is the growth rate of the neurostimulation devices market?

The neurostimulation devices market is estimated to grow at a CAGR of 9.44% during the forecast period from 2025 to 2032.

2. What is the market size for neurostimulation devices?

The neurostimulation devices market size was valued at USD 7,862.04 million in 2024, and is expected to reach USD 16,111.10 million by 2032.

3. Which region has the highest share in the neurostimulation devices market?

North America is expected to remain a dominant force in the neurostimulation devices market, driven by the high burden of chronic pain and neurological disorders, increasing awareness initiatives, supportive government programs, and continuous product innovations with frequent FDA approvals.

4. What are the drivers for the neurostimulation devices market?

The market for neurostimulation devices is growing rapidly, fueled by the rising global prevalence of chronic diseases like pain, epilepsy, and depression. This growth is also driven by significant technological advancements that have made devices smaller, smarter, and more effective. Favorable regulatory policies and better reimbursement coverage are also making these treatments more accessible. Overall, the increasing demand for effective, long-term therapeutic options for neurological and chronic conditions is creating a strong and sustained market.

5. Who are the key neurostimulation devices companies operating in the market landscape?

Some of the key neurostimulation devices compnaies companies operating in the market include Abbott Laboratories, Smith’s Medical, B. Braun Melsungen AG, Baxter International Inc., Boston Scientific Corp., LivaNova PLC., Medtronic, Nevro Corp., Abbott, Stryker, Omron Corporation, Stimwave LLC, Koninklijke Philips NV, Kimberly Clark Corporation, EndoStim Inc., Aleva neurotherapeutics SA, Cyberonics, DyAnsys, Inc., NanoVibronix, Inc., ElectroCore Inc., and Others.