Non-invasive Prenatal Testing Market

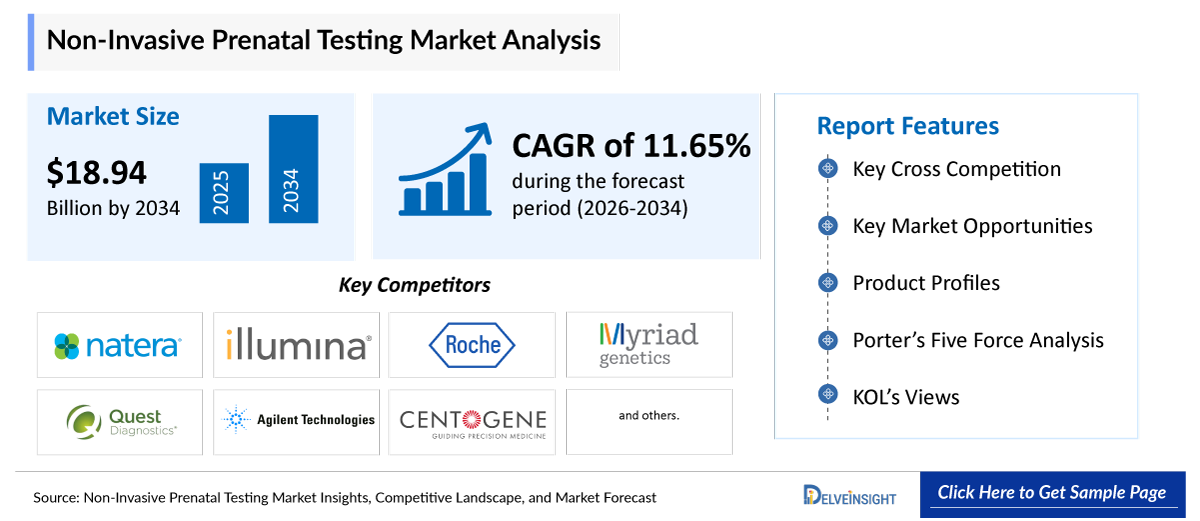

- The global non-invasive prenatal testing (NIPT) market was valued at USD 7.2 billion in 2025 and is projected to reach USD 18.94 billion by 2034, driven by rising global maternal age, increasing awareness of chromosomal abnormality risk, rapid advances in next-generation sequencing technologies, and expanding insurance reimbursement coverage across major markets.

- The global non-invasive prenatal testing market is growing at a CAGR of 11.65% during the forecast period from 2026 to 2034.

- The global trend of rising average maternal age creating higher chromosomal abnormality risk with the Centers for Disease Control and Prevention (CDC) reporting that 1 in 33 babies born in the United States has a birth defect, the World Health Organization (WHO) estimating that 1 in every 160 children is born with a congenital anomaly, expanding coverage and reimbursement for NIPT with UnitedHealthcare removing prior authorization requirements for NIPT in April 2025, rapid advances in next-generation sequencing (NGS) technology reducing costs and improving detection accuracy to over 99% sensitivity and specificity for common trisomies per peer-reviewed literature (PubMed/NCBI), and expanding geographic access to NIPT services through new laboratory partnerships and at-home testing innovations are collectively driving exceptional and sustained growth in the NIPT market through the forecast period.

- The leading companies operating in the non-invasive prenatal testing market include Natera, Inc., Illumina, Inc. (Verinata Health, Inc.), F. Hoffmann-La Roche Ltd. (Ariosa Diagnostics), Laboratory Corp. of America Holdings (LabCorp), Myriad Women's Health, Inc. (Counsyl, Inc.), Quest Diagnostics, Inc., Agilent Technologies, Inc., Centogene N.V., Qiagen N.V., Thermo Fisher Scientific, Inc., Eurofins LifeCodexx GmbH, MedGenome Labs Ltd., Progenity, Inc., BGI Genomics Co., Ltd., and Berry Genomics Co., Ltd.

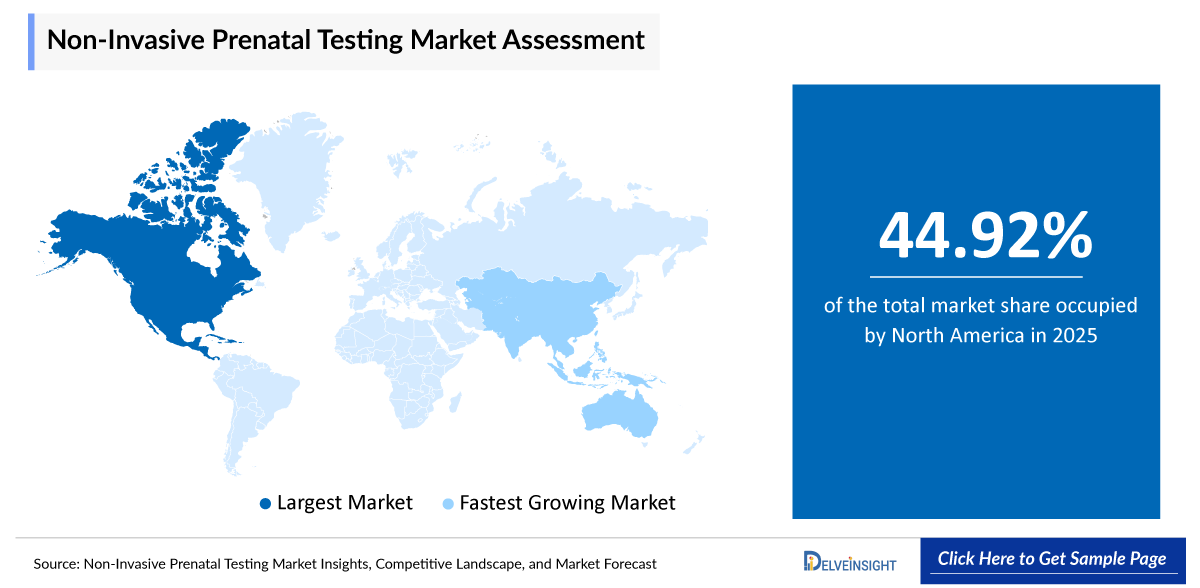

- North America is expected to dominate the non-invasive prenatal testing market with 44.92% of global market revenue in 2025, driven by the United States' advanced healthcare infrastructure, favorable insurance reimbursement frameworks with UnitedHealthcare's April 2025 removal of prior authorization for NIPT across commercial and community plans, the presence of global NIPT market leaders Natera, Illumina, Roche, LabCorp, and Quest Diagnostics headquartered in the United States, and strong awareness programs for prenatal genetic screening among obstetric care providers and expectant parents.

- In the method segment of the non-invasive prenatal testing market, the cell-free DNA in maternal plasma tests category accounted for 45.15% of total global market revenue in 2025, driven by its established clinical superiority in detecting chromosomal abnormalities, safety profile eliminating procedural miscarriage risk associated with invasive alternatives, ability to be performed as early as 9-10 weeks of gestation, and demonstrated sensitivity and specificity exceeding 99% for trisomy 21 detection in large-scale clinical validation studies published in peer-reviewed literature.

Request for unlocking the report of the @Non-Invasive Prenatal Testing (NIPT) Market

Non-Invasive Prenatal Testing Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 7.2 billion |

|

2034 Projected Market Size |

USD 18.94 billion |

|

Growth Rate (2026-2034) |

11.65% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Non-Invasive Prenatal Testing Market

-

Rising global maternal age is creating expanding high-risk pregnancy populations: The global trend toward delayed childbearing is the most significant structural growth driver for the NIPT market. Advanced maternal age is the primary established risk factor for chromosomal abnormalities, including Down syndrome (trisomy 21), Edwards syndrome (trisomy 18), and Patau syndrome (trisomy 13). The Centers for Disease Control and Prevention (CDC) reports that 1 in 33 babies born in the United States has a birth defect, with chromosomal abnormalities representing a major category. The risk of trisomy 21 rises significantly with maternal age, increasing from 1 in 1,500 at age 25 to 1 in 100 at age 40. According to CDC vital statistics data, births to women aged 35 and older have increased significantly as societal trends toward career development and educational advancement delay family formation globally. This demographic shift creates a structural and expanding demand for reliable, non-invasive chromosomal screening that NIPT uniquely provides without the procedural risks of amniocentesis or chorionic villus sampling.

-

Technological advances in next-generation sequencing are improving accuracy and reducing costs: Rapid advances in next-generation sequencing (NGS) technology are simultaneously improving NIPT clinical performance and reducing per-test costs, creating a virtuous cycle of expanding clinical adoption. According to peer-reviewed research published in PubMed/NCBI, NGS-based NIPT has demonstrated sensitivity and specificity exceeding 98.89% for trisomy 21, trisomy 18, and trisomy 13, with failure rates below 0.72% in large multicenter validation studies, representing diagnostic performance that substantially exceeds conventional maternal serum screening. The decreasing cost of NGS-based sequencing is making NIPT economically accessible beyond the high-risk population segment into average-risk pregnancies, dramatically expanding the total addressable market. Myriad Women's Health's Prequel Prenatal Screen with AMPLIFY technology enables accurate cfDNA screening as early as 8 weeks of gestation with a failure rate of only 0.1% - the lowest in the industry - including in patients with high BMI who represent a historically challenging testing population.

-

Expanding insurance reimbursement and healthcare policy support broadening market access: The progressive expansion of insurance reimbursement coverage for NIPT from high-risk-only populations to average-risk pregnancies is the most commercially impactful near-term market expansion mechanism. In April 2025, UnitedHealthcare removed prior authorization requirements for non-invasive prenatal testing, including cell-free fetal DNA tests, across various commercial and community plans - substantially reducing administrative barriers to NIPT access for millions of covered patients. The National Institutes of Health (NIH) continues to fund research supporting the clinical utility and cost-effectiveness of NIPT, strengthening the evidence base supporting payer coverage decisions. The Society for Maternal-Fetal Medicine (SMFM) and the American College of Obstetricians and Gynecologists (ACOG) have published guidelines recommending NIPT as a first-tier screening option for all pregnant women, regardless of age or risk level, providing the clinical endorsement framework that drives payer coverage expansion. The National Health Service (NHS) in the United Kingdom has progressively expanded NIPT availability within its national prenatal screening program.

Non-Invasive Prenatal Testing Market Report Segmentation

This non-invasive prenatal testing market report offers a comprehensive overview of the global NIPT market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Component (Kits and Reagents, Instruments, and Software and Services), Method (Cell-Free DNA in Maternal Plasma Tests, Fetal Cell Isolation, and Others), Application (Trisomy Detection [Down Syndrome/Trisomy 21, Edwards Syndrome/Trisomy 18, and Patau Syndrome/Trisomy 13], Sex Chromosome Aneuploidies, Microdeletion Syndromes, and Others), Gestation Period (0-12 Weeks, 13-24 Weeks, and 25-36 Weeks), End-User (Diagnostic Laboratories, Hospitals, and Others), Technology (Next-Generation Sequencing [NGS], Polymerase Chain Reaction [PCR], Microarray, and Others), and Geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific.

Non-invasive prenatal testing (NIPT), also known as cell-free DNA screening or non-invasive prenatal screening (NIPS), is a method of screening for certain chromosomal abnormalities and genetic conditions in a developing fetus using a simple blood sample from the pregnant person, typically from 9 to 10 weeks of gestation onward. Unlike traditional invasive prenatal diagnostic procedures such as amniocentesis (involving needle insertion into the amniotic sac) or chorionic villus sampling (CVS, involving tissue sampling from the placenta) - both of which carry a small but meaningful risk of pregnancy loss estimated at 0.1% to 0.5% per procedure - NIPT is entirely non-invasive and carries no procedural risk to the fetus or pregnancy. The test analyzes cell-free fetal DNA (cfDNA) fragments that naturally circulate in maternal blood, originating primarily from placental cells (trophoblasts), to detect numerical chromosomal abnormalities (aneuploidies) including trisomy 21 (Down syndrome), trisomy 18 (Edwards syndrome), trisomy 13 (Patau syndrome), sex chromosome aneuploidies (Turner syndrome, Klinefelter syndrome), and increasingly microdeletion syndromes and single-gene disorders.

The NIPT market operates within the broader prenatal care ecosystem, where it is positioned as the primary first-tier screening option offering superior accuracy over conventional maternal serum screening (double marker, triple marker, and quadruple marker tests) while remaining non-invasive and therefore accessible to all pregnant populations without procedural risk counseling requirements. The market encompasses the full diagnostic value chain from test kit and reagent manufacturing through NGS instrument sales, laboratory services, bioinformatics software, and genetic counseling services.

The NIPT market growth is collectively driven by the structural demographic force of rising maternal age expanding high-risk pregnancy populations, the technological advancement of NGS enabling progressively higher diagnostic accuracy at lower cost, and the healthcare policy evolution of expanding insurance reimbursement converting NIPT from a specialty-population diagnostic into a standard prenatal care offering. These forces ensure that the NIPT addressable market grows continuously as average-risk reimbursement coverage expands and diagnostic panel breadth extends from common trisomies into microdeletion syndromes and ultimately single-gene disorder screening.

Get More Insights into the Report @Non-Invasive Prenatal Testing Market.

What are the Latest Non-Invasive Prenatal Testing Market Dynamics and Trends?

Rising global maternal age is creating expanding high-risk chromosomal abnormality populations, technological advances in NGS are achieving over 99% detection sensitivity for common trisomies, expanding insurance reimbursement with UnitedHealthcare's April 2025 prior authorization removal, and geographic expansion of NIPT services through laboratory partnerships and at-home testing innovations are collectively driving exceptional growth in the global NIPT market.

According to the Centers for Disease Control and Prevention (CDC), approximately 1 in 33 babies born in the United States has a birth defect, with chromosomal abnormalities representing a major and highly prevalent subset. The World Health Organization (WHO) estimates that approximately 1 in 160 children is born with a congenital anomaly globally, underscoring the scale of the preventable birth defect burden that prenatal screening programs, including NIPT, address. The CDC further documents that advanced maternal age, defined as 35 years or older at delivery, is the primary established risk factor for chromosomal aneuploidies, with Down syndrome risk increasing dramatically from 1 in 1,500 at age 25 to approximately 1 in 100 at age 40. The U.S. trend toward delayed childbearing documented by the National Center for Health Statistics (NCHS/CDC) is directly expanding the proportion of pregnancies at elevated chromosomal risk, creating a growing structural demand base for NIPT services across the country and in similarly age-delayed childbearing populations across Europe, East Asia, and Australia.

The technological performance of NGS-based NIPT has reached clinical validation thresholds that support its recommendation as a first-tier screening option by major obstetric professional societies. A 2021 peer-reviewed study published in PubMed/NCBI based on 13,607 cases concluded that NGS-based NIPT offers sensitivities and specificities exceeding 98.89% for aneuploidy conditions, including trisomy 21, trisomy 18, trisomy 13, and monosomy X, with failure rates below 0.72%. Natera's Panorama test, based on single-nucleotide polymorphism (SNP) analysis technology, is documented in peer-reviewed literature as the only NIPT capable of differentiating between maternal and fetal DNA in chromosomes of interest, providing an additional layer of specificity that reduces maternal cell contamination false-positive rates. Myriad Women's Health's Prequel with AMPLIFY technology demonstrates accurate cfDNA screening as early as 8 weeks of gestation with only a 0.1% failure rate, including in high-BMI patients where conventional cfDNA tests historically fail at higher rates. These validated performance differentiators are driving clinician and payer adoption of NIPT as standard prenatal care across all risk populations.

The most significant near-term commercial market development is the expansion of insurance reimbursement from high-risk-only to all-risk pregnancy coverage. In April 2025, UnitedHealthcare removed prior authorization requirements for NIPT, including cell-free fetal DNA tests, across various commercial and community plans, substantially reducing the administrative barrier to NIPT access for millions of covered patients and directly expanding the addressable testing population. The Society for Maternal-Fetal Medicine (SMFM) and the American College of Obstetricians and Gynecologists (ACOG) have both published consensus statements recommending NIPT as a first-tier screening option for all pregnant women, regardless of age or prior risk designation, providing the clinical endorsement framework that enables and accelerates payer coverage expansion. In January 2024, Natera, Inc. acquired Invitae Corporation's non-invasive prenatal screening and carrier screening business assets for USD 10 million plus up to USD 42.5 million in milestone payments, consolidating market leadership and transitioning Invitae's prenatal customer base to Natera's platform.

Innovation in NIPT platform capabilities is continuously expanding the clinical utility and commercial scope of the market. NIPT panels are progressively expanding beyond common trisomies and sex chromosome aneuploidies into microdeletion syndrome screening, including DiGeorge syndrome (22q11.2 deletion), Wolf-Hirschhorn syndrome, and Cri-du-chat syndrome. In May 2024, Natera launched a new cfDNA-based fetal RhD blood test to address severe shortages of Rho(D) immune globulin treatment in the United States, demonstrating how cfDNA technology is expanding beyond chromosomal screening into maternal-fetal medicine blood group diagnostics. In June 2025, Myriad Genetics introduced a new at-home NIPT kit, reflecting the broader healthcare trend toward decentralized and home-based testing that dramatically expands geographic access to NIPT services. In February 2025, Yourgene Health launched the IONA Care + non-invasive prenatal screening service in the UK. In June 2025, BGI Genomics and Prom-Test Laboratories launched the first localized NIPT project in Armenia using the NIFTY test following technology transfer. In May 2025, Roche partnered with Broad Clinical Labs to expand NIPT services. In January 2025, Myriad Genetics published clinical data demonstrating accurate cfDNA screening at 8 weeks of gestation.

However, the NIPT market faces several growth constraints. The relatively high cost of NIPT testing - typically ranging from USD 400 to USD 800 per test in the United States before insurance - creates access barriers in markets without comprehensive reimbursement coverage. Ethical and regulatory challenges surrounding genetic testing, including concerns about sex selection and discrimination based on genetic information, have led to restrictions or prohibitions on certain NIPT applications in multiple countries. The complexity of genetic counseling required to interpret NIPT results, including the challenge of communicating risk probabilities rather than definitive diagnoses to expectant parents, creates a workforce bottleneck that can limit service expansion. The classification of NIPT as a screening rather than a diagnostic test means that positive results require confirmatory invasive testing, which can generate confusion and anxiety among patients. Limited testing infrastructure in lower-income countries restricts market growth in developing regions with the highest birth rates globally.

Non-Invasive Prenatal Testing Market Segment Analysis

Non-Invasive Prenatal Testing Market by Component (Kits and Reagents, Instruments, and Software and Services), Method (Cell-Free DNA in Maternal Plasma Tests, Fetal Cell Isolation, and Others), Application (Trisomy Detection [Down Syndrome, Edwards Syndrome, Patau Syndrome], Sex Chromosome Aneuploidies, Microdeletion Syndromes, and Others), Gestation Period (0-12 Weeks, 13-24 Weeks, and 25-36 Weeks), End-User (Diagnostic Laboratories, Hospitals, and Others), Technology (Next-Generation Sequencing, PCR, Microarray, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World).

By Component: The Kits and Reagents segment is expected to dominate the market with the largest revenue share.

In the component segment of the non-invasive prenatal testing market, the kits and reagents category accounted for 45% of total global market revenue in 2025. Kits and reagents hold the dominant revenue position in the NIPT component segment, as the high-volume consumable driving recurring revenue across every NIPT test performed globally. Every NIPT procedure requires specialized blood collection tubes containing cell-free fetal DNA stabilizing reagents, cfDNA extraction kits, sequencing library preparation reagents, and hybridization probes or SNP arrays, depending on the technology platform. The consumable nature of kits and reagents ensures that revenue generation scales directly and proportionally with NIPT test volumes, creating the most reliable and predictable revenue stream in the NIPT market ecosystem. As NIPT testing volumes expand from high-risk to average-risk population coverage, the kits and reagents demand multiply proportionally across all technology platforms.

The instruments segment is expected to grow at the fastest CAGR of 12.7% through 2034, driven by laboratory infrastructure investment as new NIPT laboratories are established in Asia-Pacific and developing markets to reduce dependence on sample shipment to established reference laboratories in the United States and Europe. Next-generation sequencing instruments from Illumina represent the dominant instrument platform in the NIPT workflow, with Illumina's leadership in NGS sequencer manufacturing giving it a dual commercial advantage as both a NIPT test developer and the instrument supplier to the broader NIPT laboratory ecosystem. Software and services represent the third component category, encompassing bioinformatics analysis pipelines, physician reporting platforms, and genetic counseling service networks that are increasingly being offered as integrated service bundles alongside physical test kits.

By Method: The Cell-Free DNA in Maternal Plasma Tests category dominates with 45.15% market share.

In the method segment of the non-invasive prenatal testing market, the cell-free DNA (cfDNA) in maternal plasma tests category accounted for 45.15% of total global market revenue in 2025. cfDNA in maternal plasma testing dominates the NIPT method segment by virtue of its established clinical validation, technological maturity, operational simplicity of sample collection through a standard maternal blood draw, and comprehensive range of chromosomal abnormality targets detectable from a single test. The cfDNA method analyzes cell-free fetal DNA fragments naturally circulating in maternal blood originating primarily from placental trophoblasts to detect chromosomal copy number variations and sequence abnormalities with sensitivity and specificity exceeding 98.89% for major trisomies per PubMed/NCBI validated research.

Within the cfDNA method segment, two major analytical approaches compete: whole-genome sequencing analysis (used by Illumina's VeriSeq platform, Roche's Harmony/Ariosa, and LabCorp's MaterniT21) and targeted SNP-based analysis (used exclusively by Natera's Panorama platform). The SNP-based approach enables differentiation between maternal and fetal DNA sources, providing a specificity advantage in detecting true fetal chromosomal abnormalities versus maternal mosaicism false-positives. Natera's clinical validation documented in peer-reviewed literature shows 100% specificity and sensitivity for common non-mosaic autosomal aneuploidies using the SNP method in single-laboratory validation data. The fetal cell isolation method segment holds a smaller but emerging share, with companies including Genoptix developing next-generation approaches to isolate intact fetal cells from maternal blood for direct genomic analysis, potentially enabling higher resolution genomic assessment than cfDNA testing alone.

By Application: The Trisomy Detection segment dominated with 55.10% of market revenue in 2025.

In the application segment of the non-invasive prenatal testing market, the trisomy detection category encompassing Down syndrome (trisomy 21), Edwards syndrome (trisomy 18), and Patau syndrome (trisomy 13) accounted for 55.10% of total global market revenue in 2025. Trisomy detection holds the dominant application segment position because it represents the original, most clinically validated, and most widely reimbursed NIPT indication, with over a decade of large-scale clinical deployment supporting its safety, accuracy, and clinical utility across both high-risk and average-risk pregnancy populations. Down syndrome remains the most common chromosomal condition compatible with long-term survival, affecting approximately 1 in 700 live births per CDC data, creating the greatest single-target demand for prenatal chromosomal screening globally.

The trisomy segment growth is supported by the progressive recommendation of NIPT as a first-tier trisomy screening option by SMFM, ACOG, and international obstetric societies, replacing conventional maternal serum screening (double marker, triple marker, quadruple marker tests) that offer substantially lower sensitivity and higher false-positive rates. The trisomy segment is anticipated to maintain its dominant position through 2034 as average-risk reimbursement expansion progressively multiplies the eligible testing population. The sex chromosome aneuploidies segment is growing alongside trisomy detection, as most commercial NIPT panels include sex chromosome analysis as a standard add-on to common trisomy screening. The microdeletion syndromes segment represents the fastest-growing application, with panels increasingly including DiGeorge syndrome (22q11.2 deletion), Wolf-Hirschhorn syndrome, and other microdeletions that individually affect 1 in 4,000 to 1 in 10,000 pregnancies but collectively represent a significant birth defect burden. The Turner syndrome segment is anticipated to grow at the fastest CAGR within the sex chromosome aneuploidy sub-segment.

By End-User: The Diagnostic Laboratories segment dominates with 63% of market revenue.

In the end-user segment of the non-invasive prenatal testing market, diagnostic laboratories accounted for 63% of total global market revenue in 2025. Diagnostic laboratories dominate the NIPT end-user segment because of their specialized infrastructure, NGS sequencing platforms, bioinformatics pipelines, CLIA-certified quality systems, certified genetic counselors, and FDA-compliant reporting frameworks that enable high-throughput, high-accuracy NIPT processing at the economies of scale required for commercially sustainable operations. Leading NIPT laboratory operators, including LabCorp, Quest Diagnostics, Natera, and Roche's Ariosa Diagnostics, process tens of thousands of NIPT samples monthly, leveraging their scale to achieve per-test economics that individually operating hospital laboratories cannot match.

The high diagnostic laboratory market share reflects the centralized laboratory model that has historically dominated clinical NIPT delivery: blood samples collected in obstetric offices and maternal-fetal medicine practices are shipped to central reference laboratories for NGS processing and bioinformatics analysis, with results typically returned within 5-7 business days. The hospitals segment is expected to grow at the fastest CAGR of 13.9% through 2034, driven by hospital-based prenatal care program expansion, the integration of in-house NIPT services in major academic medical centers with NGS infrastructure, and growing patient preference for receiving NIPT results within the same healthcare system providing obstetric care for integrated follow-up management of positive screening results. The shift toward at-home testing exemplified by Myriad Genetics' June 2025 at-home NIPT kit launch represents an emerging end-user segment that could capture a growing share of average-risk NIPT volume.

Non-Invasive Prenatal Testing Market Regional Analysis

Non-Invasive Prenatal Testing Market Regional Analysis

North America Non-Invasive Prenatal Testing Market Trends

North America accounted for 44.92% of the global non-invasive prenatal testing market revenue in 2025, representing the highest regional market share globally. North America's dominant position is anchored by the United States, representing the world's largest national NIPT market. The United States benefits from the highest concentration of NIPT market leaders, including Natera, Illumina, Roche Ariosa Diagnostics, LabCorp, Quest Diagnostics, and Myriad Women's Health, all headquartered in the country and serving the world's most commercially developed NIPT market. The U.S. regulatory framework administered by the FDA, NIH genomics research investment, and healthcare policy infrastructure administered by the Centers for Medicare and Medicaid Services (CMS) collectively provide a supportive environment for rapid NIPT adoption.

The April 2025 UnitedHealthcare prior authorization removal for NIPT, covering cell-free fetal DNA tests across commercial and community plans, represents the most significant single commercial expansion event in the U.S. NIPT market in recent years, directly expanding the covered testing population and reducing administrative burden on ordering physicians. The U.S. Department of Health and Human Services has launched programs supporting genetic testing infrastructure that benefit NIPT service availability. Investment trends in North America are strongly supportive of continued market leadership, with Natera's January 2024 acquisition of Invitae's NIPT and carrier screening business consolidating market share and demonstrating active M&A investment in the sector.

Europe Non-Invasive Prenatal Testing Market Trends

Europe accounted for 30% of the global non-invasive prenatal testing market revenue in 2025, representing the second-largest regional market globally. Europe's NIPT market is characterized by progressive national health system integration, with the UK National Health Service (NHS) expanding NIPT coverage within its national prenatal screening program, and multiple European countries offering government-funded NIPT for high-risk pregnancies. Germany, France, the United Kingdom, and the Nordic countries lead European NIPT adoption, supported by well-developed prenatal genetic counseling infrastructure and favorable regulatory frameworks under European guidelines for prenatal screening. In February 2025, Yourgene Health launched the IONA Care + non-invasive prenatal screening service in the United Kingdom, expanding access to advanced cfDNA-based NIPT services within the British healthcare market. The European Society of Human Genetics (ESHG) guidelines recommend NIPT as a first-tier prenatal screening option for trisomies, providing the clinical endorsement that drives payer coverage expansion across European markets.

The Eurofins LifeCodexx GmbH platform and Centogene N.V. provide European-headquartered NIPT service infrastructure, while Roche's Ariosa Diagnostics Harmony test and Illumina's VeriSeq NIPT Solution serve European laboratories through established diagnostics distribution channels. The European NIPT market benefits from an aging maternal population in Western Europe, generating expanding high-risk pregnancy cohorts requiring chromosomal screening. However, regulatory heterogeneity across EU member states regarding the scope of permissible NIPT applications creates market fragmentation challenges for service providers operating across multiple national systems.

Asia-Pacific Non-Invasive Prenatal Testing Market Trends

Asia-Pacific is the fastest-growing regional non-invasive prenatal testing market, expected to register a CAGR of 12.6% through 2034, the highest of any global region. The region's rapid growth is driven by the world's largest birth volumes, rising healthcare expenditure, expanding private healthcare networks, growing awareness of prenatal genetic screening among urban middle-class populations, increasing average maternal age, particularly in East Asian countries, and government-backed maternal health programs in China and India supporting prenatal care infrastructure development. BGI Genomics Co., Ltd. and Berry Genomics Co., Ltd., both headquartered in China, provide locally manufactured NIPT solutions that compete effectively with Western platforms on cost in Asian markets.

China is the largest national NIPT market in Asia-Pacific, reflecting the country's enormous birth volume, rapidly rising disposable incomes, expanding private maternity care infrastructure, and government focus on reducing birth defect rates under the Healthy China 2030 initiative. In June 2025, BGI Genomics and Prom-Test Laboratories launched the first localized NIPT project in Armenia through technology transfer, demonstrating BGI's geographic expansion strategy beyond China into neighboring regional markets. India represents a high-growth emerging NIPT market, with the MedGenome Labs Ltd. platform providing localized NIPT services across Indian healthcare networks. Japan, South Korea, and Australia contribute sophisticated NIPT markets with high per-capita adoption rates driven by elevated average maternal ages among their populations.

Rest of World Non-Invasive Prenatal Testing Market Trends

The Rest of World region, encompassing the Middle East, Africa, and South America, accounted for 13% of global non-invasive prenatal testing market revenue in 2025 and represents a growing long-term opportunity as healthcare infrastructure develops, awareness of prenatal genetic screening expands, and testing costs decline with NGS technology maturation. Latin America's growing private healthcare sector, particularly in Brazil, Mexico, and Colombia, is creating new NIPT market entry opportunities for established testing platforms. The Middle East's expanding private healthcare networks and growing awareness of genetic disorders in populations with higher consanguinity rates are supporting NIPT adoption. Africa represents a long-term development opportunity as maternal healthcare infrastructure develops with support from international health organizations.

Who are the Major Players in the Non-Invasive Prenatal Testing Market?

The following are the leading companies in the non-invasive prenatal testing market. These companies collectively hold the largest market share and dictate industry trends.

- Natera, Inc.

- Illumina, Inc. (Verinata Health, Inc.)

- F. Hoffmann-La Roche Ltd. (Ariosa Diagnostics)

- Laboratory Corp. of America Holdings (LabCorp)

- Myriad Women's Health, Inc. (Counsyl, Inc.)

- Quest Diagnostics, Inc.

- Agilent Technologies, Inc.

- Centogene N.V.

- Qiagen N.V.

- Thermo Fisher Scientific, Inc.

- Eurofins LifeCodexx GmbH

- MedGenome Labs Ltd.

- Progenity, Inc.

- BGI Genomics Co., Ltd.

- Berry Genomics Co., Ltd.

- Others

How is the Competitive Landscape Shaping the Non-Invasive Prenatal Testing Market?

The competitive landscape of the non-invasive prenatal testing market is Moderately Concentrated, with Natera, Illumina, Roche (Ariosa Diagnostics), LabCorp, and Quest Diagnostics collectively dominating the global market through differentiated technology platforms, established clinical laboratory networks, and strong physician and payer relationships. Natera, Inc. has emerged as the commercial market leader through its proprietary SNP-based Panorama test platform, which uniquely differentiates between maternal and fetal DNA chromosomes to reduce false-positive rates, combined with its January 2024 acquisition of Invitae's NIPT and carrier screening business, consolidating additional market share and customer relationships. Natera also expanded its cfDNA diagnostic portfolio in May 2024 with the launch of a new fetal RhD blood test addressing a specific clinical unmet need, demonstrating its strategy of leveraging its cfDNA technology platform competence into adjacent diagnostic applications.

Illumina, Inc. occupies a uniquely powerful competitive position in the NIPT market as both the manufacturer of the VeriSeq NIPT Solution test kit and the dominant supplier of the NGS sequencing instruments and reagents used by the majority of independent NIPT laboratory operators globally. This dual vertical positioning gives Illumina commercial exposure to the NIPT market growth at both the kit/test level and the instrument/reagent infrastructure level. Roche's Ariosa Diagnostics Harmony test is one of the most widely deployed NIPT platforms globally, backed by Roche's comprehensive clinical laboratory relationships and international regulatory clearance portfolio. Myriad Women's Health differentiates through its Prequel Prenatal Screen with AMPLIFY technology's industry-leading 0.1% failure rate and 8-week gestational testing capability. Myriad Genetics introduced an at-home NIPT kit in June 2025, representing product innovation targeting the growing direct-to-consumer and home-based testing segment.

BGI Genomics and Berry Genomics have established competitive positions in Asian and emerging markets through cost-effective NGS-based NIPT platforms manufactured in China at price points below established Western platforms, enabling market penetration in price-sensitive healthcare environments without compromising NGS-based analytical capabilities. Geographic reach differentiates leading players substantially: Natera and Illumina maintain global commercial operations, while BGI Genomics' June 2025 Armenia launch through technology transfer demonstrates the company's strategy of geographic expansion through local laboratory partnership and technology licensing. Pipeline strength is converging on microdeletion syndrome panel expansion, single-gene disorder NIPT development, earlier gestational window testing capability, and at-home test collection innovation. M&A activity, including Natera's acquisition of Invitae's NIPT business in January 2024, reflects ongoing market consolidation as established players acquire specialized testing capabilities and customer relationships.

Recent Developmental Activities in the Non-Invasive Prenatal Testing Market

- In June 2026, published research demonstrated ongoing clinical adoption of expanded NIPT panels including microdeletion syndrome screening across major academic prenatal diagnostic centers, with clinical validation studies confirming diagnostic performance of expanded panels for 22q11.2 deletion, Wolf-Hirschhorn syndrome, and Cri-du-chat syndrome across multicenter patient cohorts. Strategic significance: Establishes the clinical evidence base supporting expanded NIPT panel reimbursement and adoption, creating the next expansion frontier for the market beyond common trisomy screening.

- In June 2025, Myriad Genetics, Inc. introduced a new at-home NIPT kit, allowing expectant parents to conduct testing from home using a simple blood collection device aligned with the growing telemedicine and home-based healthcare trend. Strategic significance: Positions Myriad as the first major NIPT provider to commercially deploy at-home collection, dramatically expanding geographic access to NIPT and reducing access barriers for patients in underserved areas or those with mobility limitations.

- In June 2025, BGI Genomics Co., Ltd. and Prom-Test Laboratories launched the first localized NIPT project in Armenia using the NIFTY test following technology transfer, making prenatal chromosomal screening accessible locally for the first time. Strategic significance: Demonstrates BGI's geographic expansion strategy through technology transfer partnerships, expanding NIPT access to new national markets and establishing BGI's platform as the entry-level NIPT standard in emerging Eastern European and Central Asian markets.

- In May 2025, F. Hoffmann-La Roche Ltd. partnered with Broad Clinical Labs to expand NIPT services and access across new laboratory network partnerships. Strategic significance: Expands Roche Ariosa Diagnostics' NIPT service reach through new laboratory network partnerships, diversifying service delivery channels, and increasing test accessibility beyond Roche's direct laboratory operations.

- In April 2025, UnitedHealthcare removed prior authorization requirements for non-invasive prenatal testing, including cell-free fetal DNA tests, across various commercial and community plans, substantially reducing administrative barriers to NIPT access for covered patients. Strategic significance: Represents the most commercially significant U.S. payer policy change for the NIPT market in recent years, directly expanding the addressable testing population for all U.S. commercial NIPT providers.

- In February 2025, Yourgene Health launched the IONA Care + non-invasive prenatal screening service in the United Kingdom, providing expectant parents with expanded access to advanced cfDNA-based NIPT screening services within the British healthcare market. Strategic significance: Expands NIPT service availability in the UK market and positions Yourgene as a growing independent NIPT service provider competing alongside NHS-integrated pathways.

- In January 2025, Myriad Genetics, Inc. revealed clinical study results demonstrating that its Prequel Prenatal Screen with AMPLIFY technology enables accurate cfDNA screening as early as 8 weeks of gestation with only a 0.1% failure rate, including in high-BMI patients - the earliest gestational testing window and lowest failure rate commercially available. Strategic significance: Establishes a significant clinical differentiation advantage for Myriad's Prequel platform over competitors in clinical settings serving high-BMI obstetric populations and providers seeking the earliest possible gestational testing windows.

- In January 2024, Natera, Inc. acquired Invitae Corporation's non-invasive prenatal screening and carrier screening business assets for USD 10 million upfront plus up to USD 42.5 million in milestone payments, consolidating Invitae's prenatal testing customer base within Natera's growing platform ecosystem. Strategic significance: Significantly expanded Natera's NIPT market share by absorbing a competitor's entire prenatal testing customer base and strengthened Natera's position as the dominant independent NIPT commercial operator in the United States.

- In May 2024, Natera, Inc. launched a new cfDNA-based fetal RhD blood test to address severe national shortages of Rho(D) immune globulin treatment in the United States, performing fetal RhD status determination, including analysis of complex pseudogene and RhD-CE-D hybrid variants from maternal blood as early as 9 weeks of gestation. Strategic significance: Demonstrates Natera's strategy of leveraging established cfDNA platform competence into adjacent maternal-fetal medicine diagnostic applications beyond chromosomal screening, expanding the total diagnostic revenue potential of the cfDNA technology platform.

- In January 2024, Illumina, Inc. partnered with a leading healthcare provider to expand access to NIPT services in underserved regions, aiming to improve maternal health outcomes by increasing awareness and availability of non-invasive testing options in communities with historically limited access to advanced prenatal screening. Strategic significance: Reflects Illumina's commitment to geographic access expansion for NIPT and demonstrates the company's dual strategy of growing both its direct test kit sales and its NGS instrument infrastructure customer base.

- In January 2023, Juno Diagnostics (JunoDxTM) launched Juno Hazel Plus, a non-invasive prenatal screening solution using finger-prick blood samples rather than venous blood draws, and established an Early Access Program to broaden its innovative minimal-blood NIPT product portfolio. Strategic significance: Represents a significant sample collection innovation, reducing the patient experience barrier for NIPT by enabling finger-prick rather than venipuncture sample collection, potentially expanding NIPT accessibility in settings without phlebotomy infrastructure.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Non-Invasive Prenatal Testing Market CAGR |

11.65% |

|

Key Companies |

Natera, Inc., Illumina, Inc. (Verinata Health, Inc.), F. Hoffmann-La Roche Ltd. (Ariosa Diagnostics), Laboratory Corp. of America Holdings (LabCorp), Myriad Women's Health, Inc. (Counsyl, Inc.), Quest Diagnostics, Inc., Agilent Technologies, Inc., Centogene N.V., Qiagen N.V., Thermo Fisher Scientific, Inc., Eurofins LifeCodexx GmbH, MedGenome Labs Ltd., Progenity, Inc., BGI Genomics Co., Ltd., Berry Genomics Co., Ltd., and others. |

|

Market Segments |

By Component, By Method, By Application, By Gestation Period, By End-User, By Technology, and By Geography |

|

Regional Scope |

North America, Europe, Asia Pacific, the Middle East, Africa, and South America |

|

Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key countries |

Non-Invasive Prenatal Testing Market Segmentation

Non-Invasive Prenatal Testing Market by Component

- Kits and Reagents

- Instruments

- Software and Services

Non-Invasive Prenatal Testing Market by Method

- Cell-Free DNA in Maternal Plasma Tests

- Fetal Cell Isolation

- Others

Non-Invasive Prenatal Testing Market by Application

- Trisomy Detection

- Down Syndrome (Trisomy 21)

- Edwards Syndrome (Trisomy 18)

- Patau Syndrome (Trisomy 13)

- Sex Chromosome Aneuploidies

- Microdeletion Syndromes

- Others

Non-Invasive Prenatal Testing Market by Gestation Period

- 0-12 Weeks

- 13-24 Weeks

- 25-36 Weeks

Non-Invasive Prenatal Testing by End-User

- Diagnostic Laboratories

- Hospitals

- Others

Non-Invasive Prenatal Testing Market by Technology

- Next-Generation Sequencing (NGS)

- Polymerase Chain Reaction (PCR)

- Microarray

- Others

Non-Invasive Prenatal Testing Market by Geography

- North America Non-Invasive Prenatal Testing Market

- United States Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Canada Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Mexico Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Europe Non-Invasive Prenatal Testing Market

- Germany Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- United Kingdom Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- France Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Italy Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Spain Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Rest of Europe Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Asia-Pacific Non-Invasive Prenatal Testing Market

- China Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Japan Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- India Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Australia Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- South Korea Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Rest of Asia-Pacific Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Rest of the World (RoW) Non-Invasive Prenatal Testing Market

- Middle East Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- Africa Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

- South America Non-Invasive Prenatal Testing Market Size in USD million (2023-2034)

Non-Invasive Prenatal Testing Market Recent Industry Trends and Milestones (2023-2026)

|

Category |

Key Developments |

|

Non-Invasive Prenatal Testing Market Product Approval |

Myriad Genetics at-home NIPT kit launch (June 2025); Yourgene Health IONA Care + NIPT service UK launch (February 2025); Myriad Genetics Prequel AMPLIFY 8-week gestational testing clinical validation data (January 2025); Natera fetal RhD cfDNA blood test launch addressing U.S. RhIg shortage (May 2024); Juno Diagnostics Juno Hazel Plus finger-prick NIPT launch and Early Access Program (January 2023) |

|

Non-Invasive Prenatal Testing Market Product Expansion |

UnitedHealthcare removed NIPT prior authorization across commercial and community plans (April 2025); BGI Genomics and Prom-Test Armenia NIFTY NIPT localized launch through technology transfer (June 2025); Roche partnership with Broad Clinical Labs for expanded NIPT service access (May 2025); Illumina partnership for NIPT access expansion in underserved regions (January 2024); BGI Genomics expanded geographic NIPT service access across Asia-Pacific and Central Asian markets. |

|

Non-Invasive Prenatal Testing Market Product Investment |

Natera acquired Invitae's NIPT and carrier screening business assets for USD 10 million plus USD 42.5 million in milestones (January 2024); MedGenome Labs USD 45 million Series C investment (Sequoia Capital, Sofina) for India NIPT expansion; NGS sequencing cost reduction enabling average-risk NIPT economic viability across broader payer populations; expanded microdeletion syndrome panel clinical validation investments across leading NIPT providers. |

|

Company Strategy |

Natera, Inc.: SNP-based Panorama platform differentiation plus Invitae acquisition consolidating market share plus cfDNA diagnostic expansion into fetal RhD testing and oncology. Illumina, Inc.: Dual strategy as NIPT test kit provider (VeriSeq) and NGS instrument supplier to independent NIPT laboratory operators globally. Roche Ariosa Diagnostics: Global Harmony test deployment through established clinical laboratory distribution network. Myriad Women's Health: Prequel AMPLIFY technology differentiation for high-BMI patients plus at-home testing innovation. BGI Genomics/Berry Genomics: Cost-competitive NGS NIPT platforms for Asia-Pacific and emerging market penetration. |

|

Emerging Technologies |

AI/ML integration for cfDNA sequencing data analysis, improving chromosomal aneuploidy detection accuracy and reducing no-call rates; whole-genome sequencing NIPT enabling incidental finding detection beyond targeted chromosomal panels; finger-prick and at-home blood collection devices eliminating venipuncture barriers; expanded microdeletion syndrome panels covering 22q11.2 deletion and other conditions; single-gene disorder NIPT development enabling monogenic disease screening from maternal blood; cfDNA platform expansion into fetal RhD typing and maternal oncology screening applications |

Key Takeaways from the Non-Invasive Prenatal Testing Market Report Study

- Market size analysis for the current non-invasive prenatal testing market size (2025), and market forecast for 9 years (2026 to 2034).

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures that happened over the last 3 years.

- Key companies dominating the global non-invasive prenatal testing market.

- Various opportunities available for competitors in the non-invasive prenatal testing market space.

- What are the top-performing segments in 2025? How will these segments perform in 2034?

- Which are the top-performing regions and countries in the current non-invasive prenatal testing market scenario?

- Which are the regions and countries where companies should concentrate their opportunities for the non-invasive prenatal testing market growth in the future?

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Funding Stage |

Main Product |

Core Technology |

|

Juno Diagnostics (JunoDxTM) |

USD 13 million (Series A) |

Series A (2023) |

Juno Hazel Plus - non-invasive prenatal screening using finger-prick blood samples rather than venous blood draw for NIPT and chromosomal abnormality screening |

Minimal-volume cfDNA extraction and NGS analysis from finger-prick blood samples, eliminating venipuncture requirement and enabling at-home or remote NIPT collection without phlebotomy infrastructure |

|

Yourgene Health plc (UK) |

GBP 8 million (growth financing) |

Established Growth Stage |

IONA Care, a non-invasive prenatal screening service, launched in the UK (February 2025), and IONA Calc risk calculation software for prenatal screening laboratory workflows |

Proprietary cfDNA-based NIPT platform with integrated laboratory software enabling NHS-compatible prenatal screening service delivery across UK maternity networks |

|

Progenity, Inc. |

USD 85 million (Series D equivalent through IPO) |

Growth Stage / Post-IPO |

Innatal Prenatal Screen - cfDNA-based NIPT for common chromosomal aneuploidies and microdeletion syndromes with advanced fetal fraction optimization |

Single-molecule counting technology applied to maternal plasma cfDNA provides high-sensitivity NIPT with advanced quality metrics for low fetal fraction samples. |

|

MedGenome Labs Ltd. (India) |

USD 45 million (Series C) |

Series C (Investors: Sequoia Capital, Sofina) |

India-specific NIPT platform providing localized cfDNA-based prenatal chromosomal screening optimized for South Asian genetic backgrounds and clinical infrastructure |

Indigenous NGS-based cfDNA NIPT laboratory service providing chromosomal aneuploidy screening optimized for Indian clinical workflows and ethnic-specific reference population databases |