Pain Management Devices Market Summary

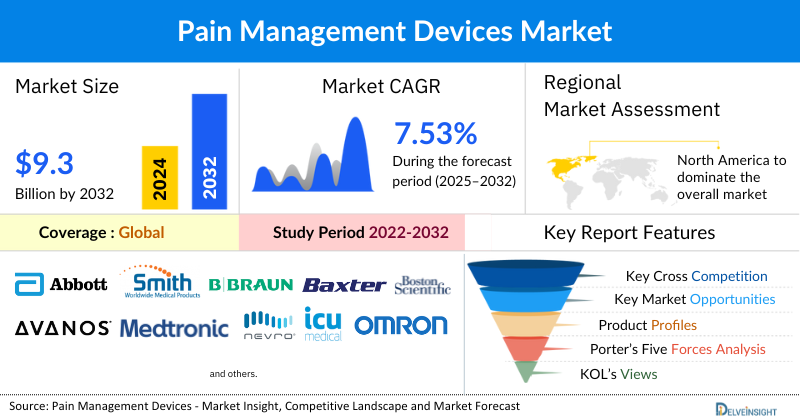

- The global pain management devices market is expected to increase from USD 5,277.30 million in 2024 to USD 9,350.72 million by 2032, reflecting strong and sustained growth.

- The global pain management devices market is growing at a CAGR of 7.53% during the forecast period from 2025 to 2032.

Pain Management Devices Market Insights & Analysis

- The global pain management devices market is set to grow rapidly from 2025 to 2032, driven by the rising prevalence of chronic pain, frequent product launches, and increasing awareness of pain management solutions. Growing demand for minimally invasive devices and supportive awareness campaigns are boosting adoption, creating strong opportunities for innovation and improved patient outcomes.

- The leading companies operating in the pain management devices market include Abbott Laboratories, Smith’s Medical, B. Braun SE, Baxter International, Boston Scientific Corp., Avanos Medical, Inc., Medtronic, Nevro Corp., ICU Medical, Inc., Omron Corporation, Stimwave LLC, Nipro, O&M Halyard, EndoStim Inc., Nalu Medical, Inc., Micrel Medical Devices SA, DyAnsys, Inc., NanoVibronix, Inc., Zynex Inc., and others.

- North America is expected to remain a dominant force in the pain management devices market, driven by the high burden of chronic pain, increasing awareness initiatives, supportive government programs, and continuous product innovations with frequent FDA approvals.

- In the device type segment of the pain management devices market, the Neurostimulation devices category is estimated to account for the largest market share in 2024.

Request for unlocking the report of the @ Pain Management Devices Market Insights

Pain Management Devices Market Size and Forecasts

Pain Management Devices Market Size and Forecasts

|

Report Metrics |

Details |

|

2024 Market Size |

USD 5,277.30 million |

|

2032 Projected Market Size |

USD 9,350.72 million |

|

Growth Rate (2025-2032) |

7.53% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Consolidated |

Factors Contributing to the Growth of the Pain Management Devices Market

- The Growing Prevalence of Chronic Pain and Related Conditions Leading to a Surge in the Pain Management Devices Market: This is not a single, isolated factor but rather a complex issue stemming from several interconnected demographic and health trends.

- Aging Population: As life expectancy increases worldwide, the proportion of the population aged 65 and over is growing. This demographic shift is directly linked to a higher prevalence of chronic pain. Older adults are more susceptible to age-related conditions that cause persistent pain, such as:

- Osteoarthritis: A degenerative joint disease that becomes more common with age.

- Musculoskeletal disorders: Including back pain, which is one of the leading causes of disability globally.

- Neuropathic pain: Nerve-related pain that can result from age-related nerve damage.

- Chronic Diseases: The rising global burden of chronic diseases like diabetes and cancer contributes to a higher prevalence of neuropathic pain and other forms of pain that require long-term management. For instance:

- Diabetes: Can lead to a type of nerve damage called diabetic neuropathy, which causes chronic pain, tingling, and numbness.

- Cancer: Both the disease itself and its treatments (e.g., chemotherapy, radiation) can cause severe and persistent pain.

- Obesity: Places added stress on joints and the skeletal system, leading to a higher incidence of back, knee, and hip pain.

- Lifestyle Changes: Sedentary lifestyles and occupational factors are leading to a rise in conditions like back pain and other musculoskeletal issues, fueling the demand for non-pharmacological pain relief.

- Sedentary Lifestyles: Long hours spent sitting at desks or in front of screens can lead to poor posture and chronic back and neck pain.

- Repetitive Strain Injuries: Certain occupations involve repetitive motions that can lead to conditions like carpal tunnel syndrome or other forms of tendonitis.

- Aging Population: As life expectancy increases worldwide, the proportion of the population aged 65 and over is growing. This demographic shift is directly linked to a higher prevalence of chronic pain. Older adults are more susceptible to age-related conditions that cause persistent pain, such as:

- The Shift Away from Opioid-Based Pain Management: It is a critical factor driving the growth of the pain management devices market, and it is a direct response to a global public health crisis.

- The Opioid Crisis and Its Impact: The global opioid crisis has highlighted the dangers of addiction, misuse, and abuse associated with traditional pain medications. This has prompted healthcare providers, patients, and regulators to actively seek safer, non-addictive alternatives. Also, the over-prescription of opioid painkillers for both acute and chronic pain led to a public health crisis in many countries, most notably the United States. Key issues include:

- Addiction and Abuse: Many individuals who were prescribed opioids for pain management developed a dependence or addiction, which can lead to substance use disorder and, in some cases, a transition to more dangerous illicit opioids like heroin or fentanyl.

- Overdose Deaths: A staggering number of overdose deaths have been attributed to both prescription and illicit opioids, making it a leading cause of unintentional injury deaths.

- Public and Professional Concern: The scale of the crisis has generated widespread concern among the general public, healthcare providers, and policymakers, leading to a strong push for non-pharmacological alternatives.

- Reduced Side Effects: Pain management devices, particularly non-invasive ones, offer a way to alleviate pain without the systemic side effects (e.g., drowsiness, nausea, constipation) of oral pain medications.

- The Rise of Multimodal Pain Management: The shift away from opioids has accelerated the adoption of a multimodal approach to pain management. This involves using a combination of different therapies to achieve optimal pain relief. Pain management devices fit perfectly into this model, as they can be used alongside non-opioid medications (e.g., NSAIDs), physical therapy, and other interventions. For example, a patient recovering from surgery might use a TENS unit to manage their post-operative pain, reducing their need for oral opioids.

- The Opioid Crisis and Its Impact: The global opioid crisis has highlighted the dangers of addiction, misuse, and abuse associated with traditional pain medications. This has prompted healthcare providers, patients, and regulators to actively seek safer, non-addictive alternatives. Also, the over-prescription of opioid painkillers for both acute and chronic pain led to a public health crisis in many countries, most notably the United States. Key issues include:

In summary, the opioid crisis has acted as a powerful catalyst, forcing a fundamental change in the way pain is treated. This has created a significant market opportunity for pain management devices, which are positioned as a safer, non-addictive, and effective alternative to traditional drug-based pain relief.

- Technological Advancements and Innovation:

- Neuromodulation Technologies: Breakthroughs in neurostimulation, such as closed-loop systems and miniaturized implantable devices, are making these treatments more effective, personalized, and less invasive.

- Smart and Wearable Devices: The development of portable, user-friendly, and wearable devices (like TENS units) allows for convenient, at-home pain management, reducing the need for frequent clinical visits.

- Integration with Digital Health: The incorporation of artificial intelligence (AI), remote monitoring, and digital health platforms allows for more precise and data-driven pain management, improving patient outcomes.

Pain Management Devices Market Report Segmentation

This pain management devices market report offers a comprehensive overview of the global pain management devices market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Device Type {Electrical Stimulation Devices [Neurostimulation Devices, (Spinal Cord Stimulators, Deep Brain Stimulators, Sacral Nerve Stimulators, and Others), Transcutaneous Electrical Nerve Stimulation (TENS), and Others], Analgesic Infusion Pumps (Intrathecal Infusion Pumps, External Infusion Pumps), Ablation Devices (Radiofrequency Ablation Devices, Cryoablation Devices), and Others}, Application (Musculoskeletal Pain, Cancer Pain, Neuropathic Pain, and Others), End-Users (Hospitals, Specialty Clinics, Rehabilitation Centers/Physiotherapy Centers, Homecare Settings, and Others), and Geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing pain management devices market.

Pain management devices are a category of medical equipment designed to alleviate pain without the need for or as an alternative to oral medications, particularly opioids. They work by either stimulating the body's natural pain-relieving mechanisms or by blocking pain signals from reaching the brain. These devices are used to manage a wide range of chronic and acute pain conditions, including those related to musculoskeletal disorders, neuropathic pain, and post-surgical recovery.

The growing prevalence of chronic pain, coupled with an increasing number of product launches and rising awareness of pain management solutions, is expected to drive significant growth in the global pain management devices market. As patient demand for effective and minimally invasive treatments rises, leading companies are introducing advanced devices that expand treatment options while intensifying market competition and innovation. Moreover, awareness campaigns and patient advocacy are fostering greater acceptance and adoption of these technologies worldwide. Collectively, these factors are creating a favorable environment for market expansion, promising improved patient outcomes and enhanced quality of life for individuals suffering from chronic pain during the forecast period of 2025 to 2032.

Get More Insights into the Report @ Pain Management Devices Market Trends

What are the latest Pain Management Devices Market Dynamics and Trends?

The global pain management devices market is experiencing robust growth, driven by the rising prevalence of chronic pain conditions across oncology, musculoskeletal, and neurological disorders. A significant contributor is cancer-related pain, particularly neuropathic cancer pain, which often remains inadequately managed with conventional therapies. With cancer cases surging worldwide, including breast, lung, and prostate cancers, the demand for advanced pain management solutions continues to climb. According to DelveInsight (2024), there were approximately 102,000 incident cases of triple-negative breast cancer (TNBC) in the 7MM in 2023. Global breast cancer incidence, which reached 2.3 million cases in 2022, is projected to escalate to 3.36 million by 2045. This expanding patient pool underscores the critical role of innovative devices in delivering effective pain relief and improving quality of life.

The growing burden of musculoskeletal diseases is another major growth driver. According to the Global Burden of Disease (2023), nearly one billion people are projected to have osteoarthritis by 2050, with steep increases anticipated in the knee (+74.9%), hip (+78.6%), hand (+48.6%), and other joints such as the elbow and shoulder (+95.1%). This sharp rise highlights the urgent need for accessible and effective pain-relieving technologies, positioning pain management devices as indispensable in addressing the long-term impact of osteoarthritis.

Neurological conditions further amplify market demand. The Global Burden of Disease Study 2021, published in The Lancet Neurology, reported that neurological disorders affected 3.4 billion people globally, 43% of the world’s population, making them the leading cause of disability and ill health. Among these, tension-type headaches (≈2 billion cases) and migraines (≈1.1 billion cases) remain highly prevalent. Devices such as neurostimulation systems, including those targeting occipital nerves, have proven effective in interrupting pain signals and providing relief for chronic headaches and migraines. Meanwhile, the diabetic neuropathy population has more than tripled since 1990, reaching 206 million in 2021, fueling further adoption of devices designed to alleviate nerve-related pain.

Collectively, the rising incidence of cancer, osteoarthritis, and neurological conditions, coupled with continuous product innovations by leading players, is creating a highly favorable environment for the expansion of the global pain management devices market.

However, the growth of the global pain management devices market is significantly hampered by three main restraints: the high cost of devices and procedures, a stringent and complex regulatory framework, and the inherent risks and complications of implantable devices. The high cost is a major barrier, as advanced devices like neurostimulators are expensive to produce, and their associated surgical costs are prohibitive for many patients and healthcare systems, often compounded by inconsistent insurance reimbursement. Furthermore, the regulatory environment is challenging; a lengthy and costly approval process for high-risk devices stifles innovation and slows the entry of new technologies into the market. Finally, patient and physician adoption is limited by concerns over surgical risks and the potential for device-specific complications, such as lead migration or a loss of efficacy over time, which may necessitate further, costly surgeries. These combined factors create significant hurdles that restrain the market's full potential despite the rising need for non-opioid pain management solutions.

Pain Management Devices Market Segment Analysis

Pain Management Devices Market by Device Type {Electrical Stimulation Devices [Neurostimulation Devices, (Spinal Cord Stimulators, Deep Brain Stimulators, Sacral Nerve Stimulators, and Others), Transcutaneous Electrical Nerve Stimulation (TENS), and Others], Analgesic Infusion Pumps (Intrathecal Infusion Pumps, External Infusion Pumps), Ablation Devices (Radiofrequency Ablation Devices, Cryoablation Devices), and Others}, Application (Musculoskeletal Pain, Cancer Pain, Neuropathic Pain, and Others), End-Users (Hospitals, Specialty Clinics, Rehabilitation Centers/Physiotherapy Centers, Homecare Settings, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Device Type: Neurostimulation Device Category Dominates the Market

Within the neurostimulation devices segment, which leads the overall pain management devices market with a share of about 55%, the spinal cord stimulator (SCS) category accounted for more than 45% of the neurostimulation market in 2024. This dominance is primarily attributed to the widespread clinical adoption of SCS as a standard treatment option for chronic and refractory pain.

The market for neurostimulation devices is experiencing substantial growth, driven by a combination of factors. The rising global prevalence of chronic diseases, such as chronic pain. This increased disease burden has created a greater demand for effective, long-term therapeutic options. Furthermore, significant technological advancements have made these devices more effective and user-friendly. Innovations such as smaller, rechargeable implants, "closed-loop" systems that respond to neural activity in real time, and the development of non-invasive options like Transcranial Magnetic Stimulation are expanding their adoption. Additionally, a more favorable regulatory environment and improved reimbursement policies are making these treatments more accessible to patients. This includes regulatory bodies approving a wider range of neurostimulators for new applications and insurers providing better coverage. Finally, the aging global population, which has a higher incidence of age-related neurological disorders and chronic pain, further contributes to the market's strong growth trajectory.

According to the World Health Organization (2023), there were approximately 619 million cases of lower back pain (LBP), a figure expected to climb to 843 million by 2050. In parallel, the European Pain Federation (2023) reported that around 740 million people globally experience at least one episode of severe pain during their lifetime, with nearly 20% developing chronic pain lasting more than three months. This growing burden of chronic pain highlights the urgent need for effective and sustainable pain management solutions.

Spinal cord stimulators (SCS) have gained traction as they provide a minimally invasive, drug-free, and reversible therapy option. By delivering targeted electrical impulses to the spinal cord, these devices block pain signals before they reach the brain, significantly improving patients' quality of life. The rising incidence of chronic pain disorders is, therefore, expected to be a major driver of SCS adoption worldwide.

Furthermore, findings published by the NIH (2023) revealed that Failed Back Surgery Syndrome (FBSS) affects 10-40% of patients following spinal surgeries. With the growing volume of spinal procedures for conditions such as herniated discs, spinal stenosis, and degenerative disc disease, the prevalence of Failed Back Surgery Syndrome continues to rise. Since repeated surgeries carry higher risks and often fail to deliver lasting pain relief, spinal cord stimulators are increasingly being recognized as an effective alternative. Their ability to reduce dependency on opioids, improve functional outcomes, and lower long-term healthcare costs makes them a preferred treatment choice, particularly for patients with FBSS and chronic neuropathic pain.

Emerging regulatory approvals are catalyzing market growth by enabling easier access to advanced SCS technologies: In April 2024, Medtronic gained FDA approval for Inceptiv™, the first closed-loop SCS system to automatically adjust stimulation using real-time biological feedback (evoked compound action potentials, or ECAPs), maintaining optimal therapy even during daily movement. It is also the only FDA-approved closed-loop system offering full-body 3T MRI access with no restrictions, and is touted as the smallest and thinnest fully implantable SCS device.

In April 2023, Biotronik received FDA approval for its Prospera SCS System, featuring RESONANCE, the first multiphase stimulation paradigm, and Embrace One, a patient-centric care model offering automatic, objective, daily remote monitoring, ongoing management, and support. The system also includes HomeStream remote management, rechargeable implants, and full-body MRI compatibility.

Each of these advancements highlights the trajectory of the Spinal cord stimulators market, shifting from traditional, fixed-output devices requiring routine in-clinic adjustments to intelligent, adaptive systems that emphasize remote care, personalization, and workflow efficiency.

By Application: Neuropathetic Pain Category Dominates the Market

The neuropathic pain application category dominates the pain management devices market, contributing nearly 35% of global revenue in 2024, due to a convergence of several critical factors. Neuropathic pain is not a disease itself but a symptom of an underlying condition. It is commonly associated with an increasing number of chronic diseases, such as diabetes (diabetic neuropathy), cancer (chemotherapy-induced peripheral neuropathy), shingles (postherpetic neuralgia), and multiple sclerosis. The global rise in the prevalence of these chronic conditions, driven by factors like aging populations and lifestyle changes, directly increases the incidence of neuropathic pain. Neuropathic pain and the chronic conditions that cause it become more common with age. As the global population ages, the number of individuals suffering from these painful nerve conditions continues to grow, creating a massive and expanding patient base for pain management solutions.

Simultaneously, limitations of traditional oral medications, which often provide inadequate relief and come with undesirable side effects, and the ongoing global opioid crisis have created a strong demand for safer, non-pharmacological alternatives. This need is being met by significant technological advancements in pain management devices, particularly with the development of effective, minimally invasive neurostimulation devices like spinal cord stimulators and user-friendly, non-invasive TENS units. These devices offer targeted and drug-free pain relief, making them a highly attractive option for patients and healthcare providers. Favorable market dynamics, including robust research and development and growing awareness and acceptance, further solidify the segment's dominant position.

By End-Users: Hospitals Dominate the Market

Hospitals dominated the global pain management devices market in 2024, due to their access to and primary adoption of high-cost, advanced technologies like spinal cord stimulators for complex, invasive procedures requiring specialized medical expertise and comprehensive care programs. Hospitals offer integrated pain management programs, which combine device therapy with other treatments like physical therapy, rehabilitation, and pharmacological management. This holistic approach is essential for many patients with complex and severe chronic pain conditions.

Hospitals see a large number of patients with acute and chronic pain stemming from various conditions, including post-surgical pain, cancer-related pain, and severe neuropathic pain. This consistent patient flow drives the high volume of device usage. Additionally, in many developed nations, insurance and public health systems offer more favorable reimbursement for procedures and devices administered in a hospital setting, which incentivizes their use.

However, the Homecare Settings segment is projected to grow the fastest, fueled by a major shift toward convenient, cost-effective, and continuous at-home care. This growth is driven by the increasing availability of user-friendly, portable devices such as TENS units, which align with the growing preference for non-pharmacological, at-home pain management solutions.

Pain Management Devices Market Regional Analysis

North America Pain Management Devices Market Trends

North America, led by the U.S., accounted for a dominant ~45% share of the global pain management devices market in 2024. The North American pain management devices market is experiencing robust growth, driven by a trifecta of factors: the increasing burden of chronic pain, a surge in recent product innovations and approvals, and supportive government initiatives.

A key driver is the alarming prevalence of chronic pain across the region. According to recent data from the Centers for Disease Control and Prevention (CDC), in 2021, an estimated 51.6 million U.S. adults, or 20.9% of the population, were living with chronic pain. A significant subset of this group, 17.1 million individuals, experienced high-impact chronic pain that severely limits daily activities. This is further compounded by the aging demographic, which is more susceptible to chronic conditions like arthritis. The CDC highlights that in 2022, the age-adjusted prevalence of diagnosed arthritis in the U.S. was 18.9%, with a sharp increase to 53.9% in adults aged 75 and older. This widespread prevalence of chronic, debilitating pain creates an immense and sustained demand for effective, long-term pain management solutions beyond traditional pharmaceuticals.

The market's growth is also being fueled by a flurry of recent product approvals and launches that are transforming the treatment landscape. These new devices are often minimally invasive, incorporating advanced technologies like artificial intelligence (AI) and closed-loop systems to offer more personalized and effective therapy. For instance, in September 2024, Nevro launched HFX AdaptivAI, an AI-driven spinal cord stimulation (SCS) system that uses real-time patient feedback to personalize therapy. Similarly, in December 2022, Abbott received FDA approval for its Eterna™ SCS system, the smallest implantable, rechargeable SCS available for chronic pain treatment. It uses proprietary low-dose BurstDR™ stimulation, which has shown a 23% greater reduction in pain compared to traditional SCS. Furthermore, recent innovations are also targeting specific conditions, such as SetPoint Medical's SetPoint System, which received FDA approval in July 2025 as the first neuroimmune modulation device for rheumatoid arthritis, offering a non-pharmaceutical alternative for patients with inadequately managed disease.

Finally, increasing government initiatives and public awareness campaigns are further propelling market growth. These efforts, such as the designation of September as Pain Awareness Month in the U.S., aim to educate the public on the importance of early intervention and the availability of non-opioid pain relief methods. This shift in focus is a direct response to the opioid crisis, with institutions like the National Institutes of Health (NIH) and the FDA promoting safer alternatives. The robust regulatory framework and favorable reimbursement policies for advanced procedures also incentivize the adoption of these innovative devices, making them more accessible to a wider patient population.

Europe Pain Management Devices Market Trends

The pain management devices market in Europe is a dynamic and growing sector, driven by trends that are both similar to and distinct from those in North America. The market is projected to grow at a significant compound annual growth rate (CAGR) in the coming years, with key drivers and trends shaping its trajectory.

Key Drivers and Market Trends

- Aging Population and Chronic Pain Prevalence: Like other developed regions, Europe is grappling with an aging population, which is directly correlated with a rise in chronic conditions. The European Pain Federation (EFIC) and other studies have highlighted that a significant portion of the adult population in European countries, such as Germany and the UK, lives with chronic pain. This persistent and widespread need for effective, long-term pain management is the fundamental driver of the market.

- Shift from Opioids to Non-Invasive Solutions: Europe has a strong focus on public health and patient safety, which is fueling a clear shift away from a reliance on opioid-based pain management. This has created a fertile ground for the adoption of non-pharmacological alternatives. Devices like Transcutaneous Electrical Nerve Stimulation (TENS) units, neurostimulation devices, and radiofrequency ablation are gaining traction as preferred options for their effectiveness and reduced risk of addiction.

- Favorable Reimbursement and Regulatory Frameworks: While North America is a major market, Europe's market is supported by well-established healthcare systems and increasingly favorable reimbursement policies. These policies, especially in key markets like Germany, the UK, and France, are making advanced pain management devices more accessible to a broader patient base. This support from public and private health insurers is crucial for overcoming the high cost of advanced implantable devices.

- Strategic Initiatives by Market Players: Major players in the pain management device market, many of which are headquartered or have a strong presence in Europe (e.g., Medtronic), are heavily invested in R&D and strategic partnerships. They are actively launching new products and focusing on clinical evidence to support the use of their devices, thereby strengthening their market position and driving adoption.

Asia-Pacific Pain Management Devices Market Trends

The Asia-Pacific pain management devices market is a high-growth region, poised to outpace North America and Europe in terms of compound annual growth rate (CAGR). This rapid expansion is driven by a unique set of demographic and economic trends.

Key Market Trends

Massive and Growing Patient Population: The Asia-Pacific region is home to a vast and rapidly aging population, particularly in countries like Japan, China, and South Korea. This demographic shift is leading to a significant increase in the prevalence of chronic pain conditions such as arthritis, diabetic neuropathy, and musculoskeletal disorders. For example, a study on chronic pain prevalence in Japan found a rate of 17.5%, while India's adult population has an estimated prevalence of 19.3%. This immense patient base represents a huge, and in many areas, an underserved market.

- Improving Healthcare Infrastructure: Significant investments in healthcare infrastructure across emerging economies like China and India are making advanced pain management devices more accessible. Governments are increasing healthcare spending, building new hospitals and clinics, and modernizing existing facilities. This improved infrastructure facilitates the adoption and use of both complex implantable devices and more common non-invasive devices.

- Increasing Disposable Income and Awareness: As economies in the region grow, so does the disposable income of a rising middle class. This enables a greater number of patients to afford advanced medical treatments and devices that may not be covered by public healthcare systems. Simultaneously, public awareness campaigns and a greater focus on pain management in medical training are changing the historical tendency to under-report or tolerate chronic pain.

- Shift to Non-Opioid Therapies: Similar to global trends, there is a growing recognition of the risks associated with long-term opioid use. This is driving a shift in clinical practice and patient preference toward non-pharmacological alternatives. Non-invasive devices like TENS and more advanced technologies like radiofrequency ablation are gaining traction as safe and effective solutions.

- Rise of Homecare and Portable Devices: The Asia-Pacific market is seeing a strong trend toward home-based care. The availability of portable and user-friendly devices, such as wearable neurostimulation devices, allows patients to manage their pain conveniently and reduce the burden on crowded hospital systems. This trend is particularly popular in countries like Japan and South Korea, where there is a cultural preference for minimally invasive and at-home treatments.

- Regulatory Developments: While the regulatory landscape can be complex and varies by country, some nations like Japan and Australia have well-established frameworks that are beginning to facilitate faster product approvals. As regulatory pathways become clearer and more efficient, international and domestic manufacturers are more incentivized to launch new products in the region.

Who are the major players in the Pain Management Devices Market?

The following are the leading companies in the pain management devices market. These companies collectively hold the largest market share and dictate industry trends.

- Abbott Laboratories

- Smith’s Medical

- B. Braun SE

- Baxter International

- Boston Scientific Corp.

- Avanos Medical, Inc.

- Medtronic

- Nevro Corp.

- ICU Medical, Inc.

- Omron Corporation

- Stimwave LLC

- Nipro

- O&M Halyard

- EndoStim Inc.

- Nalu Medical, Inc.

- Micrel Medical Devices SA

- DyAnsys, Inc.

- NanoVibronix, Inc.

- Zynex Inc, and others

How is the competitive landscape shaping the pain management devices market?

The competitive landscape of the pain management devices market is defined by a moderate degree of concentration, with a handful of major multinational corporations dominating the high-value, neurostimulation segment. Companies like Medtronic, Boston Scientific, and Abbott Laboratories are the key players, leveraging their extensive R&D capabilities, strong clinical evidence, and established global distribution networks to maintain a significant market share, particularly in implantable devices like spinal cord stimulators (SCS). However, this dynamic is evolving as the market is also populated by a growing number of smaller, innovative players and startups, such as Nevro and Saluda Medical, which are introducing disruptive technologies like high-frequency and closed-loop stimulation systems. These new entrants are driving innovation and challenging the dominance of the larger firms by focusing on specific niches and offering advanced, more personalized solutions. The non-invasive and over-the-counter (OTC) segments are more fragmented, with companies like Omron and Zynex competing with a broad range of portable, user-friendly devices, reflecting a shift towards at-home and remote care that is reshaping competitive strategies across the entire market.

Recent Developmental Activities in the Pain Management Devices Market

- In August 2025, the FDA cleared NeuroOne OneRF™ Radiofrequency Ablation System targeting trigeminal neuralgia via RF ablation, a minimally invasive alternative to traditional interventions. Planned commercial launch in fall 2025.

- In May 2025, electroCore, Inc., a commercial-stage bioelectronic technology company, completed its merger with NeuroMetrix, Inc., positioning itself as a diversified leader in non-invasive health and wellness solutions. The addition of NeuroMetrix’s Quell® Fibromyalgia Solution broadens electroCore’s portfolio of bioelectronic therapies, enhances its presence within the VA Hospital System, and significantly expands its addressable market in chronic pain and wellness management.

- In April 2025, Globus Medical, Inc., a leading musculoskeletal technology company, announced the completion of its previously disclosed acquisition of Nevro Corp., a global innovator in medical devices focused on delivering transformative solutions for chronic pain management.

- In September 2024, Endorphin Stimulator Wristband became the first Class IIa CE-marked medical device specifically approved for fibromyalgia symptom relief in Europe. It uses millimeter-wave neuromodulation technology.

- In September 2024, Nevro launched this AI-driven spinal cord stimulation (SCS) system. It's the first of its kind to be FDA-cleared, using real-time patient data to personalize and optimize therapy, aiming to provide more consistent and effective pain relief.

- In April 2024, FDA-approved Medtronic’s first closed-loop rechargeable Inceptiv™ Closed-Loop Spinal Cord Stimulator.

- In February 2024, Zynex received FDA clearance for its next-generation M-Wave neuromuscular electrical stimulation (NMES) device. This non-invasive device is designed for both chronic pain management and enhancing exercise performance, reflecting the growing demand for user-friendly, non-pharmacological solutions.

- In February 2024, the FDA approved an expanded indication for the WaveWriter SCS Systems to treat chronic low back and leg pain in patients without prior back surgery (non-surgical back pain).

|

Report Metrics |

Details |

|

Study Period |

2022 to 2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2032 |

|

Pain Management Devices Market CAGR |

7.53% |

|

Key Companies in the Pain Management Devices Market |

Abbott Laboratories, Smith’s Medical, B. Braun SE, Baxter International, Boston Scientific Corp., Avanos Medical, Inc., Medtronic, Nevro Corp., Abbott, ICU Medical, Inc., Omron Corporation, Stimwave LLC, Nipro, O&M Halyard, EndoStim Inc., Nalu Medical, Inc., Micrel Medical Devices SA, DyAnsys, Inc., NanoVibronix, Inc., Zynex Inc., and Others. |

|

Pain Management Devices Market Segments |

by Device Type, by Application, by Type, by End-Users, and by Geography |

|

Pain Management Devices Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Pain Management Devices Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Pain Management Devices Market Segmentation

- Pain Management Devices by Device Market by Type Exposure

- Electrical Stimulation Devices

- Neurostimulation Devices

- Spinal Cord Stimulators

- Deep Brain Stimulators

- Sacral Nerve Stimulators

- Others

- Transcutaneous Electrical Nerve Stimulation (TENS)

- Others

- Pain Management Devices Market By Analgesic Infusion Pumps

- Intrathecal Infusion Pumps

- External Infusion Pumps

- Pain Management Devices Market By Ablation Devices

- Radiofrequency Ablation Devices

- Cryoablation Devices

- Others

- Pain Management Devices Market by Application Exposure

- Musculoskeletal Pain

- Cancer Pain

- Neuropathic Pain

- Others

- Pain Management Devices Market By End-Users Exposure

- Hospitals

- Specialty Clinics

- Rehabilitation Centers / Physiotherapy Centers

- Homecare Settings

- Others

Pain Management Devices Geography Exposure

- North America Pain Management Devices Market

- United States Pain Management Devices Market

- Canada Pain Management Devices Market

- Mexico Pain Management Devices Market

- Europe Pain Management Devices Market

- United Kingdom Pain Management Devices Market

- Germany Pain Management Devices Market

- France Pain Management Devices Market

- Italy Pain Management Devices Market

- Spain Pain Management Devices Market

- Rest of Europe Pain Management Devices Market

- Asia-Pacific Pain Management Devices Market

- China Pain Management Devices Market

- Japan Pain Management Devices Market

- India Pain Management Devices Market

- Australia Pain Management Devices Market

- South Korea Pain Management Devices Market

- Rest of Asia-Pacific Pain Management Devices Market

- Rest of the World Pain Management Devices Market

- South America Pain Management Devices Market

- Middle East Pain Management Devices Market

- Africa Pain Management Devices Market

Pain Management Devices Market Recent Industry Trends and Milestones (2022-2025):

|

Category |

Key Developments |

|

Pain Management Devices Product Launches & Approvals |

Medtronic Inceptiv Closed-Loop SCS, Zynex TensWave (Prescription TENS Device), Remedee Labs Endorphin Stimulator Wristband, NeuroOne OneRF Trigeminal Nerve Ablation System |

|

Partnerships in the Pain Management Devices Market |

|

|

Acquisitions in the Pain Management Devices Market |

|

|

Company Strategy |

|

|

Emerging Technology |

|

Pain Management Devices Market Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are set to revolutionize the pain management devices market by transitioning it from a reactive to a proactive and personalized model of care. This transformation is primarily driven by the development of closed-loop systems, such as those from Nevro and Medtronic, which use AI to analyze real-time patient data and automatically adjust neurostimulation therapy for more effective and consistent pain relief. Furthermore, AI is enhancing diagnostics by analyzing medical images and wearable sensor data to more accurately identify the source of pain and predict future flare-ups, allowing for timely intervention. The technology also supports the rise of smart and wearable devices, enabling remote patient monitoring and personalized therapy in home care settings, a trend that is gaining significant traction. Additionally, AI holds promise in addressing healthcare disparities by objectively quantifying pain through the analysis of facial expressions and body movements, offering a more unbiased assessment than traditional subjective methods. Despite challenges related to validation and data privacy, AI's role is not merely as a feature but as a fundamental component that will shape the future of pain management devices, making them more intelligent and effective in combating chronic pain.

U.S. Tariff Impact Analysis on the Pain Management Devices Market:

The U.S. government's tariffs have had a complex and disruptive impact on the pain management devices market, primarily by raising costs for manufacturers and consumers. Tariffs on imports from key suppliers, notably China and the EU, have forced companies to either absorb costs, thus reducing profit margins, or pass them on to healthcare providers, potentially limiting patient access to care. This has also exposed the fragility of global supply chains, prompting a strategic shift toward diversification, with companies relocating manufacturing to countries with more favorable trade agreements or re-shoring production to the U.S. Furthermore, while tariffs may offer a temporary advantage to some domestic producers, they also create a climate of uncertainty that can deter foreign investment and lead to a re-evaluation of research and development budgets, ultimately impacting the pace of innovation within the market.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends:

|

Company Name |

Total Funding |

Main Products |

Stage of Development |

Core Technology |

|

Presidio Medical |

$72M+ (Series C) |

ULF™ spinal cord neuromodulation for nociceptive low back pain |

FDA IDE approved; starting pivotal RCT (FULFILL) |

Ultra-low-frequency (ULF) spinal cord stimulation platform. |

|

Neuros Medical |

$56 million |

Altius nerve stimulation system |

Series D |

For the development and commercialization of its pain management therapy for chronic neuropathic pain, especially post-amputation pain. |

|

Theranica |

$86 million (total) |

Wearable device for migraine pain |

Commercialized in some markets, but continues R&D for new applications and indications |

Remote electrical neuromodulation via a wearable patch |

|

ShiraTronics |

$66M (Series B) |

Implantable neurostimulation for chronic migraine |

FDA-approved IDE pivotal trial underway (RELIEV-CM2) |

Minimally invasive cranial neuromodulation targeting occipital/supraorbital nerves. |

|

Neuronoff |

$9.1M (grants) |

Injectrode™ for peripheral nerve stimulation (pain & autonomic targets) |

Early clinical; first-in-human completed; multiple NIH/DoD grants |

Injectable, in-body–curing electrode placed via needle (“Injectrode”). |

|

Remedee Labs |

$30M (multiple rounds incl. €12.2M in 2022) |

Millimeter-wave wristband for fibromyalgia |

CE-marked (EU) in 2024; France launch planned 2025; pre-commercial in many markets. |

Millimeter-wave endorphin stimulation wearable + coaching. |

Key takeaways from the pain management devices market report study

- Market size analysis for the current pain management devices market size (2024), and market forecast for 8 years (2025 to 2032)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the pain management devices market.

- Various opportunities available for the other competitors in the pain management devices market space.

- What are the top-performing segments in 2024? How these segments will perform in 2032?

- Which are the top-performing regions and countries in the current pain management devices market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the pain management devices market growth in the future?