Pharmaceutical Filtration Market Summary

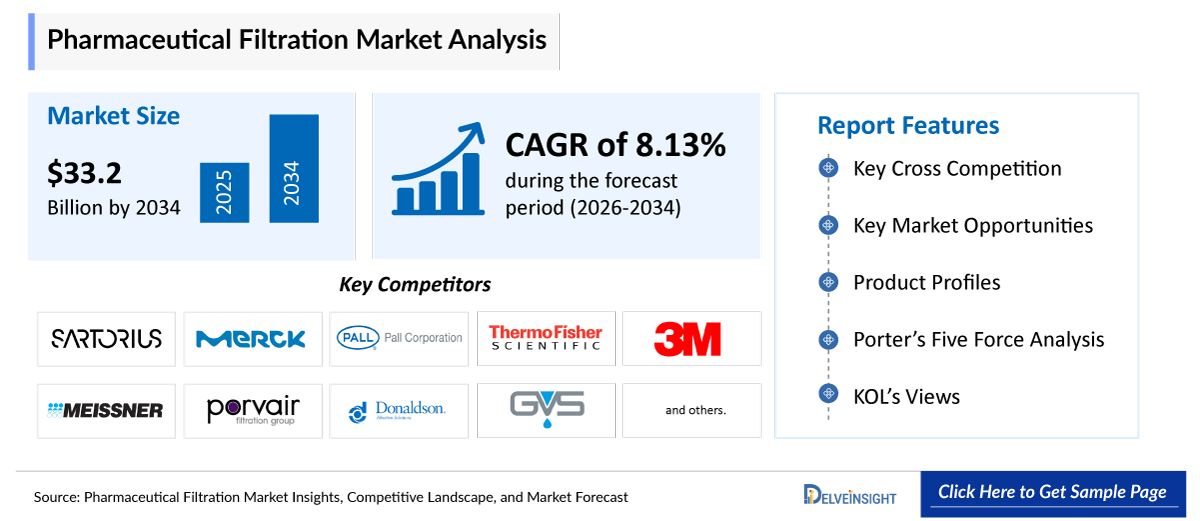

- The global pharmaceutical filtration market is expected to increase from USD 16,509.84 million in 2025 to USD 33,203.40 million by 2034, reflecting strong and sustained growth.

- The global pharmaceutical filtration market is growing at a CAGR of 8.13% during the forecast period from 2026 to 2034.

- The pharmaceutical filtration market is being strongly driven by the combined impact of rising demand for biopharmaceuticals, growth in sterile drug manufacturing, and the expansion of contract manufacturing organizations (CDMOs). The increasing production of biologics such as monoclonal antibodies, vaccines, and cell & gene therapies requires highly efficient filtration systems to ensure purity, safety, and regulatory compliance. At the same time, the surge in sterile drug manufacturing, particularly injectables, has intensified the need for advanced sterile filtration technologies for final product processing. Additionally, the rapid growth of outsourcing to CDMOs is boosting demand for scalable, flexible, and high-performance filtration solutions across multiple production stages. Together, these factors are significantly accelerating the adoption of pharmaceutical filtration technologies and driving overall market growth.

- The leading companies operating in the pharmaceutical filtration market include Sartorius AG, Merck KGaA (MilliporeSigma), Pall Corporation, Thermo Fisher Scientific Inc., 3M Company, Meissner Filtration Products, Inc., Porvair Filtration Group Ltd., Donaldson Company, Inc., GVS S.p.A., Eaton Corporation plc, Parker-Hannifin Corporation, Saint-Gobain Life Sciences, Amazon Filters Ltd., Cobetter Filtration Equipment Co., Ltd., Repligen Corporation, GEA Group Aktiengesellschaft, Alfa Laval AB, Asahi Kasei Corporation, Koch Separation Solutions, Sterlitech Corporation, and others.

- North America is expected to dominate the pharmaceutical filtration market due to its strong presence of leading biopharmaceutical companies, advanced manufacturing infrastructure, and high adoption of innovative filtration technologies. The region benefits from stringent regulatory standards set by bodies like the U.S. Food and Drug Administration, which drive consistent demand for high-quality filtration systems. Additionally, increasing investments in biologics, vaccine production, and research & development, along with the growing role of contract manufacturing organizations (CDMOs), further support market growth in the region.

- In the product type segment of the pharmaceutical filtration market, the membrane filters category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @Pharmaceutical Filtration Market

Pharmaceutical Filtration Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 16,509.84 million |

|

2034 Projected Market Size |

USD 33,203.40 million |

|

Growth Rate (2026-2034) |

8.13% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Pharmaceutical Filtration Market

Rising demand for biopharmaceuticals is leading to a surge in Pharmaceutical Filtration:

The increasing production of biologics such as monoclonal antibodies, vaccines, and cell & gene therapies is a major driver. These products are highly sensitive and require advanced filtration (sterile, ultrafiltration, virus filtration) to ensure purity and safety.

Growth in sterile drug manufacturing:

There is a strong increase in demand for injectable drugs and sterile formulations, especially in oncology and biologics. Filtration is essential for final product sterilization, particularly for heat-sensitive drugs, thereby boosting the market of pharmaceuticals filteration.

Growth of Contract Manufacturing (CDMOs):

The rise of Contract Development and Manufacturing Organizations (CDMOs) has increased the outsourcing of drug production. These facilities require scalable and flexible filtration solutions, boosting market growth.

Pharmaceutical Filtration Market Report Segmentation

This pharmaceutical filtration market report offers a comprehensive overview of the global pharmaceutical filtration market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Products Type (Membrane Filters, Depth Filters, Cartridge Filters, Syringe Filters, and Other Consumables), Technology (Microfiltration, Ultrafiltration, Nanofiltration, and Others), Application (Final Product Processing, Raw Material Filtration, and Cell Separation), Scale of Operation (R&D Scale, Pilot-scale, and Commercial Scale), End-Users (Pharmaceutical & Biotechnology Companies, Research and Academic Institutions, and Others), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing Pharmaceutical Filtration market.

Pharmaceutical filtration is a critical process used in drug manufacturing to remove particles, microorganisms, and impurities from liquids and gases to ensure product safety, purity, and quality. It involves the use of specialized filters such as membrane, depth, and cartridge filters across various stages of production, including raw material preparation, bioprocessing, and final sterile filtration. This process is essential for meeting strict regulatory standards and is widely applied in the production of biologics, vaccines, and injectable drugs.

The pharmaceutical filtration market is being strongly driven by the combined impact of rising demand for biopharmaceuticals, growth in sterile drug manufacturing, and the expansion of contract manufacturing organizations (CDMOs). The increasing production of biologics such as monoclonal antibodies, vaccines, and cell & gene therapies requires highly efficient and specialized filtration systems, including microfiltration, ultrafiltration, and virus filtration to maintain product integrity and meet strict quality standards. These biologics are highly sensitive to contamination, making advanced filtration an essential part of both upstream and downstream processing.

At the same time, the rapid growth in sterile drug manufacturing, particularly injectable formulations, has intensified the need for reliable sterile filtration technologies during final fill-finish operations. Since many of these drugs are heat-sensitive, filtration becomes the primary method for ensuring sterility, further increasing its importance in pharmaceutical production.

Additionally, the expansion of CDMOs is accelerating market growth as pharmaceutical companies increasingly outsource manufacturing to reduce costs and improve flexibility. CDMOs require scalable, single-use, and high-throughput filtration solutions that can support multiple products and production scales. This has led to greater adoption of advanced and disposable filtration systems across facilities.

Together, these factors, biologics growth, sterile manufacturing demand, and outsourcing trends, are significantly increasing the reliance on high-performance filtration technologies, thereby driving sustained growth in the pharmaceutical filtration market.

Get More Insights into the Report @Pharmaceutical Filtration Market

What are the latest pharmaceutical filtration market dynamics and trends?

The pharmaceutical filtration market is being strongly propelled by the combined impact of rising biopharmaceutical demand, expansion of sterile drug manufacturing, and the rapid growth of contract development and manufacturing organizations (CDMOs), which together are reshaping production scale and complexity. The surge in biologics such as monoclonal antibodies, vaccines, and cell & gene therapies has significantly increased reliance on advanced filtration technologies because these products are highly sensitive and require multiple sterile processing steps; this trend is a primary driver of filtration demand globally. At the same time, the expansion of sterile drug manufacturing, especially injectable and parenteral formulations, has intensified the need for high-performance membrane, microfiltration, and virus filtration systems to ensure regulatory compliance and product safety, with sterile filtration dominating key regional markets in 2024. Parallelly, the rapid rise of CDMOs is amplifying filtration consumption because outsourced manufacturing requires scalable, flexible, and compliant filtration solutions across multiple clients and drug types; the CDMO segment itself is growing strongly, with increasing investments and a rising share in pharmaceutical manufacturing revenues.

Recent developments further highlight how these factors are converging to boost the market. In February 2025, Thermo Fisher Scientific announced a $4.1 billion acquisition of Solventum’s purification and filtration business, strengthening its position in bioprocess filtration and expanding capabilities for biologics manufacturing. Furthermore, in December 2024, Lonza restructured its operations to focus more on its CDMO business, launching new platforms in biologics and advanced modalities from 2025 onward, reinforcing demand for specialized filtration systems.

Thus, the factors mentioned above are expected to boost the overall market of pharmaceutical filtration during the forecast period.

However, high operational and consumable costs, along with frequent filter clogging and fouling issues, act as significant limiting factors for the Pharmaceutical Filtration market by increasing both production expenses and process inefficiencies. The high cost of advanced membrane filters and their frequent replacement, especially in single-use systems, raises overall manufacturing costs for biopharmaceutical companies. At the same time, fouling caused by complex biological fluids reduces filtration efficiency, leads to downtime, and requires additional maintenance or filter changes, disrupting continuous production. Together, these challenges reduce process productivity, increase operational complexity, and can limit adoption in cost-sensitive manufacturing environments.

Pharmaceutical Filtration Market Segment Analysis

Pharmaceutical Filtration Market by Products Type (Membrane Filters, Depth Filters, Cartridge Filters, Syringe Filters, and Other Consumables), Technology (Microfiltration, Ultrafiltration, Nanofiltration, and Others), Application (Final Product Processing, Raw Material Filtration, and Cell Separation), Scale of Operation (R&D Scale, Pilot-scale, and Commercial Scale), End-Users (Pharmaceutical & Biotechnology Companies, Research and Academic Institutions, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product Type: Membrane filters in pharmaceutical filtration are expected to dominate the market with the largest revenue share.

In the product type segment of the pharmaceutical filtration market, the membrane filters category is contributing to 37.25% of total market revenue in 2025, as they serve as the backbone of sterile and high-precision filtration across both upstream and downstream bioprocessing. These filters, commonly made from materials such as polyethersulfone (PES), polyvinylidene fluoride (PVDF), and nylon, are essential for applications like sterilizing filtration, microfiltration, ultrafiltration, and virus removal, all of which are critical in the production of biologics, vaccines, and injectable drugs. Their ability to provide high retention efficiency, consistent pore size distribution, low protein binding, and strong chemical compatibility makes them indispensable in ensuring product purity and regulatory compliance, especially under stringent guidelines from agencies like the U.S. Food and Drug Administration and the European Medicines Agency. The rapid expansion of biologics and cell & gene therapies has further amplified demand for advanced membrane technologies, particularly single-use membrane systems that reduce contamination risk and improve operational flexibility. In addition, continuous innovations such as high-throughput membranes, pre-sterilized capsule filters, and next-generation virus-retentive membranes are improving processing efficiency and lowering manufacturing costs, encouraging wider adoption. Leading companies like Merck KGaA (MilliporeSigma), Sartorius AG, Pall Corporation, and Thermo Fisher Scientific are heavily investing in membrane innovation and capacity expansion, further strengthening this segment. As a result, membrane filters dominate the product landscape and act as a critical enabler of scalability, sterility assurance, and efficiency, collectively boosting the overall pharmaceutical filtration market.

By Technology: Microfiltration category dominates the market.

Within the technology segment of the pharmaceutical filtration market, the microfiltration category is anticipated to dominate, accounting for around 38.2% of the market share in 2025, due to its critical role in ensuring product purity, sterility, and process efficiency across pharmaceutical manufacturing. Microfiltration operates using membranes with pore sizes typically ranging from 0.1 to 1.0 µm, enabling the effective removal of bacteria, suspended particles, and other contaminants without altering the biological integrity of sensitive drug molecules such as proteins and vaccines. This makes it indispensable in key applications such as cell culture clarification, buffer filtration, sterile filtration of injectables, and final product processing. The segment holds a leading market share due to its widespread use across both upstream and downstream bioprocessing workflows. Its dominance is further strengthened by advantages such as low operating pressure, cost-effectiveness, scalability, and compatibility with single-use systems, which are increasingly adopted in modern biopharmaceutical manufacturing. Additionally, the rapid growth of biologics, biosimilars, vaccines, and cell & gene therapies has significantly increased the need for reliable contamination control, where microfiltration plays a foundational role in meeting stringent regulatory standards for sterility and product safety. Continuous advancements in membrane materials, improved fouling resistance, and enhanced performance efficiency further support its large-scale adoption, collectively positioning microfiltration as the dominant and most essential technology in the pharmaceutical filtration market.

By Application: The final product processing category dominates the market.

Within the application segment of the pharmaceutical filtration market, the final product processing category is anticipated to dominate, accounting for around 43.45% of the market share in 2025, due to its critical role in ensuring drug safety, sterility, and regulatory compliance before products reach patients. This stage represents the last and most stringent filtration step in pharmaceutical manufacturing, where finished formulations such as injectables, vaccines, biologics, and ophthalmic solutions must undergo sterile filtration to remove any remaining microorganisms and particulate contaminants. Given that regulatory authorities like the U.S. Food and Drug Administration and the European Medicines Agency mandate strict sterility assurance levels, pharmaceutical companies heavily rely on high-performance membrane filters (typically 0.2 µm) during final fill-finish operations. The dominance of this segment is further driven by the rapid growth of biologics and parenteral drugs, which cannot undergo terminal sterilization and therefore depend entirely on aseptic filtration. Additionally, the increasing demand for prefilled syringes, large-volume injectables, and ready-to-use formulations has intensified the need for robust final product filtration systems that ensure product integrity without altering drug composition. Technological advancements such as low protein-binding membranes, high-throughput filter cartridges, and integrity testing systems have further enhanced the reliability and efficiency of this process. Coupled with the expansion of contract manufacturing organizations (CMOs/CDMOs) and global vaccine production capacity, these factors collectively position final product processing as the leading application segment in the pharmaceutical filtration market.

By Scale of Operation: Commercial Scale category dominates the market

Within the scale of operation segment of the pharmaceutical filtration market, the commercial scale category is anticipated to dominate, accounting for around 57% of the market share in 2025, due to the large-volume production requirements of approved drugs and biologics. Once a product receives regulatory approval from authorities such as the U.S. Food and Drug Administration and the European Medicines Agency, manufacturing shifts from pilot or clinical-scale batches to full commercial production, where filtration becomes a continuous, high-throughput, and mission-critical operation. Commercial-scale manufacturing involves the production of vast quantities of vaccines, monoclonal antibodies, injectables, and other therapeutics, all of which require robust and scalable filtration systems to ensure sterility, consistency, and compliance with stringent quality standards. This segment dominates because it generates recurring and high-volume demand for filtration consumables such as membrane filters, depth filters, and single-use assemblies, which need frequent replacement during large production runs. Additionally, the rapid expansion of biologics, biosimilars, and contract manufacturing organizations (CMOs/CDMOs) has significantly increased commercial manufacturing activities worldwide. Pharmaceutical companies are also investing heavily in large-scale bioprocessing facilities and continuous manufacturing technologies, further driving the need for efficient, high-capacity filtration solutions. The combination of high production volumes, strict regulatory requirements, and ongoing demand for life-saving drugs firmly positions the commercial-scale segment as the leading contributor to the pharmaceutical filtration market.

By End-Users: Pharmaceutical & biotechnology companies category dominates the market

In the end-users segment of the pharmaceutical filtration market, pharmaceutical and biotechnology companies dominate the overall market due to their central role in large-scale drug development and manufacturing. These companies extensively use filtration technologies at every stage of production, from raw material purification to final product processing, to ensure sterility, product quality, and regulatory compliance set by authorities such as the U.S. Food and Drug Administration and the European Medicines Agency. The dominance of this segment is driven by the rising production of biologics, vaccines, and complex therapies, which require advanced and high-frequency filtration processes. Additionally, continuous investments in biopharmaceutical R&D, expansion of manufacturing capacities, and increasing outsourcing to contract manufacturing organizations further boost filtration demand within this segment, solidifying its leading position in the market.

Pharmaceutical Filtration Market Regional Analysis

North America Pharmaceutical Filtration Market Trends

North America is expected to account for the highest proportion of XX% of the pharmaceutical filtration market in 2025, out of all regions. North America dominates the overall pharmaceutical filtration market due to its highly advanced biopharmaceutical manufacturing infrastructure, strong regulatory environment, and the presence of leading industry players such as Thermo Fisher Scientific, Danaher Corporation (through Pall and Cytiva), Merck KGaA, and Sartorius AG that have a significant operational footprint in the region. The region benefits from extensive investments in biologics, vaccines, and advanced therapies, supported by a strong pipeline of monoclonal antibodies, gene therapies, and mRNA-based drugs, all of which require high-performance filtration technologies at multiple stages of production.

Additionally, strict regulatory standards enforced by agencies such as the U.S. Food and Drug Administration ensure the mandatory use of advanced sterile filtration systems, particularly in aseptic processing and final fill-finish operations. North America’s leadership is further reinforced by the widespread presence of contract manufacturing organizations (CMOs/CDMOs), robust R&D capabilities, and early adoption of innovative technologies such as single-use filtration systems and continuous bioprocessing, which enhance efficiency and contamination control.

Recent company-specific developments further strengthen the region’s dominance. For instance, in February, 2025, Thermo Fisher Scientific announced the acquisition of Solventum’s purification and filtration business for approximately $4.1 billion, aiming to expand its capabilities in bioprocessing filtration and strengthen its position in drug manufacturing solutions. Additionally, in June 2025, Cytiva completed major global expansion projects as part of a long-term investment strategy to enhance filtration and bioprocessing capacity, including significant developments supporting North American supply chains.

These strategic acquisitions, capacity expansions, and product innovations by key companies collectively enhance supply capabilities, technological advancement, and large-scale production efficiency, thereby reinforcing North America’s leading position in the pharmaceutical filtration market.

Europe Pharmaceutical Filtration Market Trends

The pharmaceutical filtration market in Europe is witnessing strong and sustained growth due to its well-established pharmaceutical manufacturing base, stringent regulatory standards, and continuous advancements in biopharmaceutical production. Countries such as Germany, France, and the United Kingdom serve as major hubs for biologics, biosimilars, and vaccine manufacturing, driving significant demand for advanced filtration technologies. The region’s strict quality and safety regulations for sterile drug production, coupled with increasing adoption of biologics and personalized medicines, are key factors accelerating the use of membrane filtration, microfiltration, and virus filtration systems. Additionally, the strong presence of leading companies such as Merck KGaA, Sartorius AG, and Eaton Corporation further strengthens the regional market by driving innovation and ensuring a consistent supply of high-performance filtration products. The expansion of CDMOs, increasing R&D investments, and rising focus on sterile injectables and advanced therapies continue to support long-term market growth across Europe.

Recent company-specific developments further highlight this growth trajectory. In May 2024, Sartorius AG completed the acquisition of a filtration business from a subsidiary of Merck KGaA, strengthening its filtration portfolio and market position in Europe.

These strategic acquisitions and capacity expansions, along with continuous innovation by key European players, are enhancing manufacturing capabilities, improving filtration efficiency, and reinforcing Europe’s position as a major growth region in the pharmaceutical filtration market.

Asia-Pacific Pharmaceutical Filtration Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the pharmaceutical filtration market due to its rapidly expanding pharmaceutical and biopharmaceutical manufacturing base, increasing healthcare investments, and strong government support for life sciences infrastructure. Countries such as China, India, South Korea, and Singapore are witnessing a surge in biologics, biosimilars, and vaccine production, which significantly increases the demand for advanced filtration technologies across upstream and downstream processes. The region benefits from a large patient population, rising prevalence of chronic and infectious diseases, and growing demand for high-quality medicines, all of which are accelerating drug development and manufacturing activities. In addition, improving healthcare infrastructure, increasing R&D expenditure, and favorable regulatory initiatives are attracting global pharmaceutical companies to establish manufacturing facilities and outsource production to regional contract development and manufacturing organizations (CDMOs). The rapid expansion of biopharmaceutical manufacturing and strong growth in research activities are key factors positioning the Asia Pacific as the fastest-growing region in the pharmaceutical filtration market. Furthermore, increasing investments in emerging economies and advancements in filtration technologies, including nanofiltration and single-use systems, are enhancing production efficiency and scalability, thereby supporting sustained market growth.

Recent company-specific developments further reinforce this growth trajectory in the region. In December 2024, Ahlstrom announced the acquisition of ErtelAlsop, a manufacturer of liquid depth filtration media, strengthening its life sciences filtration portfolio and expanding its presence in global and Asia-focused pharmaceutical markets. Additionally, leading global players such as Thermo Fisher Scientific, Sartorius AG, and Danaher (Cytiva and Pall) have been actively expanding their manufacturing capabilities and supply networks across the Asia Pacific through strategic investments and partnerships, aimed at meeting the rising regional demand for high-performance filtration solutions. These developments, combined with increasing localization of drug manufacturing and continuous technological advancements, are collectively positioning the Asia Pacific as a key growth engine for the pharmaceutical filtration market.

Who are the major players in the pharmaceutical filtration market?

The following are the leading companies in the pharmaceutical filtration market. These companies collectively hold the largest market share and dictate industry trends.

- Sartorius AG

- Merck KGaA (MilliporeSigma)

- Pall Corporation

- Thermo Fisher Scientific Inc.

- 3M Company

- Meissner Filtration Products, Inc.

- Porvair Filtration Group Ltd.

- Donaldson Company, Inc.

- GVS S.p.A.

- Eaton Corporation plc.

- Parker-Hannifin Corporation

- Saint-Gobain Life Sciences

- Amazon Filters Ltd.

- Cobetter Filtration Equipment Co., Ltd.

- Repligen Corporation

- GEA Group Aktiengesellschaft

- Alfa Laval AB

- Asahi Kasei Corporation

- Koch Separation Solutions

- Sterlitech Corporation

- Others

How is the competitive landscape shaping the pharmaceutical filtration market?

The competitive landscape of the pharmaceutical filtration market is characterized by the strong presence of global leaders alongside a range of regional and niche players, creating a moderately consolidated yet highly competitive environment. Major companies such as Merck KGaA, Danaher Corporation (through Cytiva and Pall), Sartorius AG, and Thermo Fisher Scientific dominate the market due to their extensive product portfolios, global distribution networks, and strong technological capabilities. These companies offer a wide range of filtration solutions, including membrane filters, depth filters, and single-use systems, enabling them to cater to diverse applications across upstream and downstream bioprocessing. At the same time, small and mid-sized players contribute to market competitiveness by providing specialized, cost-effective, and application-specific filtration products, particularly in emerging markets. Competition in this space is driven not only by pricing but also by product quality, regulatory compliance, innovation in membrane materials, and the ability to deliver integrated and scalable solutions for complex biologics and advanced therapies. Additionally, increasing focus on sustainability, efficiency, and customization is pushing companies to continuously enhance their offerings, making the market dynamic, innovation-driven, and highly competitive.

Recent Developmental Activities in the Pharmaceutical Filtration Market

- In February, 2025, Thermo Fisher Scientific announced the acquisition of Solventum’s purification and filtration business for approximately $4.1 billion, aiming to expand its capabilities in bioprocessing filtration and strengthen its position in drug manufacturing solutions.

- In June 2025, Cytiva completed major global expansion projects as part of a long-term investment strategy to enhance filtration and bioprocessing capacity, including significant developments supporting North American supply chains.

- In September, 2025, Sartorius AG expanded its manufacturing and R&D capabilities, strengthening its global filtration portfolio and supporting demand from North American biopharma companies.

- In July 2024, IDEX Corporation acquired Mott, a microfiltration business, to enhance its filtration offerings.

- In May 2024, Sartorius AG completed the acquisition of a filtration business from a subsidiary of Merck KGaA, strengthening its filtration portfolio and market position in Europe.

- In September 2023, Repligen Corporation collaborated with Sartorius to integrate advanced upstream filtration technologies, reflecting the growing trend of partnerships and technology integration.

Pharmaceutical Filtration Market Segmentation

- Pharmaceutical Filtration Product Type Exposure

- Membrane Filters

- Depth Filters

- Cartridge Filters

- Syringe Filters

- Other Consumables

- Pharmaceutical Filtration by Technology Exposure

- Microfiltration

- Ultrafiltration

- Nanofiltration

- Others

- Pharmaceutical Filtration Application Exposure

- Final Product Processing

- Raw Material Filtration

- Cell Separation

- Pharmaceutical Filtration Scale of Operation Exposure

- R&D Scale

- Pilot-scale

- Commercial Scale

- Pharmaceutical Filtration End-Users Exposure

- Pharmaceutical & Biotechnology Companies

- Research and Academic Institutions

- Others

- Pharmaceutical Filtration Geography Exposure

- North America Pharmaceutical Filtration Market

- United States Pharmaceutical Filtration Market

- Canada Pharmaceutical Filtration Market

- Mexico Pharmaceutical Filtration Market

- Europe Pharmaceutical Filtration Market

- United Kingdom Pharmaceutical Filtration Market

- Germany Pharmaceutical Filtration Market

- France Pharmaceutical Filtration Market

- Italy Pharmaceutical Filtration Market

- Spain Pharmaceutical Filtration Market

- Rest of Europe Pharmaceutical Filtration Market

- Asia-Pacific Pharmaceutical Filtration Market

- China Pharmaceutical Filtration Market

- Japan Pharmaceutical Filtration Market

- India Pharmaceutical Filtration Market

- Australia Pharmaceutical Filtration Market

- South Korea Pharmaceutical Filtration Market

- Rest of Asia-Pacific Pharmaceutical Filtration Market

- Rest of the World Pharmaceutical Filtration Market

- South America Pharmaceutical Filtration Market

- Middle East Pharmaceutical Filtration Market

- Africa Pharmaceutical Filtration Market

- North America Pharmaceutical Filtration Market

Pharmaceutical Filtration Market Recent Industry Trends and Milestones (2023-2026)

|

Category |

Key Developments |

|

Pharmaceutical Filtration Product Acquisitions |

Thermo Fisher Scientific announced the acquisition of Solventum, Sartorius AG completed the acquisition of a filtration business from a subsidiary of Merck KGaA, and IDEX Corporation acquired Mott, a microfiltration business. |

|

Company Strategy |

Merck KGaA

Sartorius AG

|

|

Emerging Technology |

Nanotechnology-based Drug Delivery Systems, Lipid Nanoparticles (LNPs), 3D Printing in Pharmaceuticals, Hot Melt Extrusion (HME), and others |

Impact Analysis

AI-Powered Innovations and Applications:

Artificial intelligence is rapidly transforming pharmaceutical formulation by enabling faster, more precise, and data-driven development of drug products. AI-powered platforms are used to predict physicochemical properties such as solubility, stability, and bioavailability, helping formulators select optimal excipients and design effective drug delivery systems with fewer experimental trials. Machine learning algorithms can analyze vast datasets from past formulations to identify patterns and recommend ideal composition and process parameters, significantly reducing development time and cost. AI is also being applied in optimizing complex formulations such as nanoparticles, liposomes, and controlled-release systems by simulating drug–excipient interactions and release profiles. In manufacturing, AI supports real-time process monitoring and control through predictive analytics, ensuring consistent product quality and minimizing batch failures, especially in continuous manufacturing environments. Additionally, AI-driven digital twins and modeling tools allow virtual testing of formulations under different conditions, improving scalability from lab to commercial production. In the context of personalized medicine, AI enables the design of patient-specific formulations by integrating clinical, genetic, and pharmacokinetic data. Overall, AI-powered innovations are enhancing efficiency, accuracy, and flexibility across the entire pharmaceutical formulation lifecycle, from early-stage design to large-scale manufacturing.

U.S. Tariff Impact Analysis on Pharmaceutical Filtration Market:

The U.S. tariff impact on the pharmaceutical filtration market is increasingly significant, as recent trade policies are reshaping cost structures, supply chains, and manufacturing strategies across the pharmaceutical and bioprocessing industries. In April 2026, the U.S. government introduced Section 232 tariffs imposing up to 100% duties on patented pharmaceuticals and associated inputs, including active pharmaceutical ingredients (APIs), with implementation beginning from July, 2026. Since pharmaceutical filtration systems are extensively used in the production of these drugs and APIs, any increase in raw material and production costs directly impacts demand patterns and procurement strategies for filtration technologies. The U.S. pharmaceutical sector is highly dependent on global supply chains for raw materials and intermediates, and tariffs can lead to supply chain disruptions, increased manufacturing costs, and margin pressures for drug manufacturers. As a result, companies may reduce operational expenditures or renegotiate supplier contracts, which can moderately affect short-term demand for filtration consumables and systems.

At the same time, these tariffs are encouraging reshoring and domestic manufacturing expansion, as companies seek to avoid import duties and qualify for tariff exemptions tied to U.S.-based production. This shift is expected to create long-term growth opportunities for pharmaceutical filtration within the U.S., as new and expanded manufacturing facilities require advanced sterile filtration technologies across upstream, downstream, and final product processing stages. However, in the near term, the market may face pricing pressures, increased capital costs, and operational uncertainties, particularly for companies reliant on imported components or global production networks. Overall, the U.S. tariff environment presents a dual impact on the pharmaceutical filtration market, posing short-term challenges related to cost and supply chain disruption, while simultaneously driving long-term domestic capacity expansion and demand for high-performance filtration solutions.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Key takeaways from the pharmaceutical filtration market report study

- Market size analysis for the current pharmaceutical filtration market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the pharmaceutical filtration market.

- Various opportunities available for the other competitors in the pharmaceutical filtration market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current pharmaceutical filtration market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the pharmaceutical filtration market growth in the future.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Alioth Biotech |

RMB 100 million |

Series A |

Pharmaceutical process filtration membranes and filter products |

Advanced membrane material engineering for biopharmaceutical separation and purification |