Plasmid DNA Manufacturing Market Summary

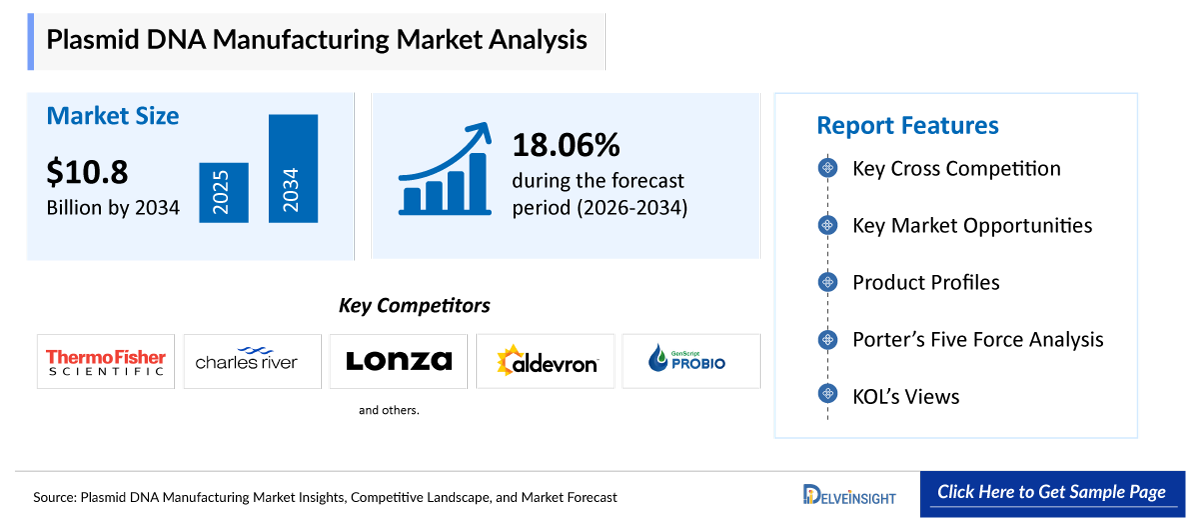

- The global plasmid DNA manufacturing market is expected to increase from USD 2,456.46 million in 2025 to USD 10,858.12 million by 2034, reflecting strong and sustained growth.

- The global plasmid DNA manufacturing market is growing at a CAGR of 18.06% during the forecast period from 2026 to 2034.

- The rapid expansion of gene therapy pipelines, rising demand for mRNA vaccines and RNA-based therapeutics, growth of cell and gene therapy (CGT) manufacturing, and increasing prevalence of genetic and chronic diseases are collectively driving strong growth in the plasmid DNA manufacturing market. Gene and cell therapies rely on plasmid DNA as a critical starting material for viral vector production and genetic engineering, while mRNA vaccines depend on plasmids as templates for in vitro transcription. As more therapies advance from clinical trials to commercialization and patient populations requiring advanced treatments expand, the need for high-quality GMP-grade plasmid DNA is increasing significantly, making it a foundational component of next-generation biopharmaceutical development.

- The leading companies operating in the plasmid DNA manufacturing market include Thermo Fisher Scientific, Charles River Laboratories, Lonza, Aldevron (Danaher), GenScript ProBio, AGC Biologics, Cobra Biologics (Charles River), Catalent, WuXi AppTec, WuXi Advanced Therapies, Eurogentec, Sartorius (BIA Separations), ProBio, PharmaCell, Pharmaron, Esco Aster, AGTC (Applied Genetic Technologies Corp.), VGXI (GeneOne Life Science), PlasmidFactory, VectorBuilder, and others.

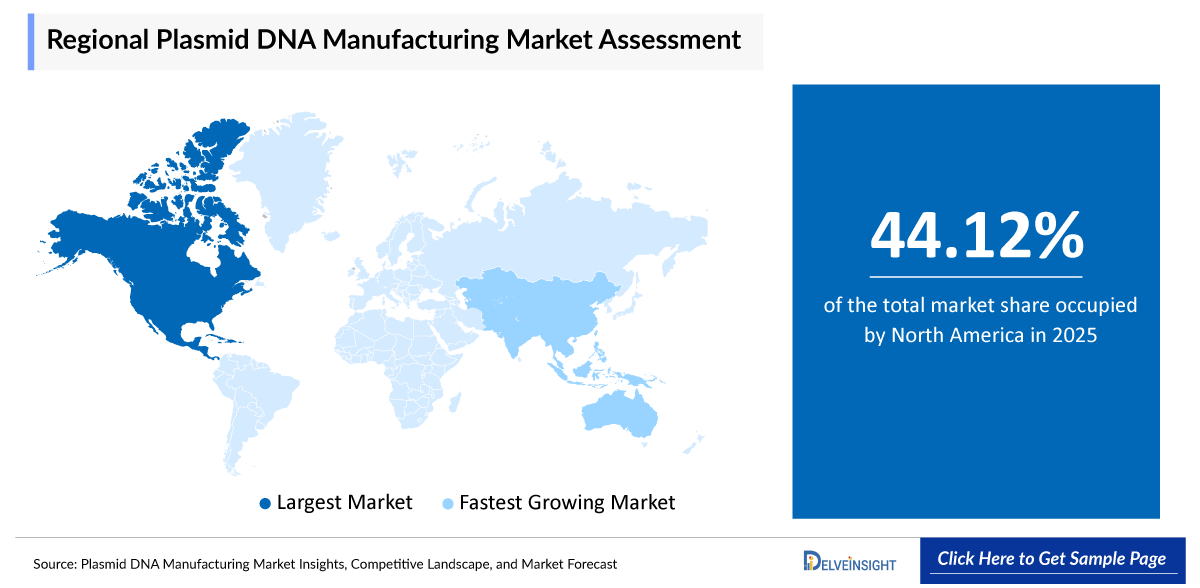

- North America is expected to dominate the plasmid DNA manufacturing market due to the presence of advanced healthcare infrastructure, strong investment in regenerative medicine, and a high number of ongoing clinical trials and product approvals. Additionally, the region benefits from increasing prevalence of chronic diseases, well-established research institutions, and the presence of key market players, all of which contribute to early adoption and commercialization of innovative stem cell therapies.

- In the product type segment of the plasmid DNA manufacturing market, the GMP-grade plasmid DNA category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Plasmid DNA Manufacturing Market

Plasmid DNA Manufacturing Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 2,456.46 million |

|

2034 Projected Market Size |

USD 10,858.12 million |

|

Growth Rate (2026-2034) |

18.06% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Plasmid DNA Manufacturing Market

Rapid expansion of gene therapy pipelines leading to a surge in plasmid DNA manufacturing:

The strongest driver of the plasmid DNA manufacturing market is the rapid and explosive growth in gene therapy development. Plasmid DNA serves as the core starting material for the production of viral vectors such as adeno-associated virus (AAV) and lentivirus, which are essential for delivering therapeutic genes into target cells. These therapies are increasingly being developed for rare and genetic disorders, where conventional treatments are limited or ineffective. In addition, the rising number of clinical trials across oncology, neurology, and metabolic diseases is further accelerating demand for high-quality plasmid DNA, reinforcing its critical role in advanced therapeutic development.

Rising demand for mRNA vaccines and RNA-based therapeutics:

Plasmid DNA is essential for mRNA production, where it acts as a template for in-vitro transcription (IVT) to synthesize mRNA molecules used in advanced therapeutics. It plays a crucial role in the development of vaccines for infectious diseases such as COVID-19, influenza, and RSV, enabling rapid and scalable vaccine production. Additionally, the use of mRNA technology is expanding into cancer immunotherapy, where it is being explored to stimulate targeted immune responses against tumor cells. As mRNA platforms continue to grow across infectious disease and oncology applications, the demand for high-purity GMP-grade plasmid DNA is increasing significantly, making it a critical enabling component in next-generation vaccine and therapeutic manufacturing.

Growth of Cell and Gene Therapy (CGT) manufacturing:

Cell therapies such as CAR-T rely heavily on plasmid DNA for the genetic engineering of immune cells and for the production of viral vectors used in the transduction process. These therapies depend on plasmids to encode the necessary genetic constructs that enable T-cells to recognize and attack cancer cells. The market is being further driven by the increasing number of FDA and EMA approvals for CAR-T therapies, which is accelerating their clinical adoption and commercialization. In addition, the expansion of allogeneic (off-the-shelf) cell therapies is enhancing scalability and accessibility, while a growing oncology pipeline continues to boost demand for advanced cell-based treatments, thereby strengthening the overall need for plasmid DNA manufacturing.

Rising prevalence of genetic and chronic diseases:

The increasing burden of diseases worldwide is significantly expanding the demand for advanced therapeutic solutions, thereby driving the plasmid DNA manufacturing market. The rising prevalence of rare genetic disorders, cancer, cardiovascular conditions, and metabolic diseases is accelerating the development of innovative gene and cell therapies aimed at addressing unmet medical needs. As the patient population grows, pharmaceutical and biotechnology companies are investing more heavily in research and development of advanced genetic treatments. This ultimately leads to greater reliance on plasmid DNA as a foundational material, since it is essential for gene delivery systems, viral vector production, and next-generation therapeutic development, thereby increasing overall market demand.

Plasmid DNA Manufacturing Market Report Segmentation

This plasmid DNA manufacturing market report offers a comprehensive overview of the global plasmid DNA manufacturing market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product Type (GMP-grade Plasmid DNA and Research-grade Plasmid DNA), Application (Cell Therapy Manufacturing, Gene Therapy Manufacturing, DNA / RNA Vaccine Development, Viral Vector Manufacturing, and Others), Production Scale (Commercial, Clinical, and Preclinical), End-Users (Pharmaceutical & Biotechnology Companies, Contract Development & Manufacturing Organizations (CDMOs), and Others), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing plasmid DNA manufacturing market.

Plasmid DNA manufacturing is the biotechnological process of producing and purifying circular DNA molecules called plasmids, typically using engineered bacteria such as E. coli. These plasmids are amplified through fermentation and then purified to high-quality standards, especially GMP-grade, for use in gene therapy, DNA vaccines, mRNA production, and cell therapy applications. It serves as a critical starting material for advanced genetic and biologic therapies.

The rapid expansion of gene therapy pipelines, rising demand for mRNA vaccines and RNA-based therapeutics, growth of cell and gene therapy (CGT) manufacturing, and the increasing prevalence of genetic and chronic diseases are collectively driving robust growth in the plasmid DNA manufacturing market. Gene and cell therapies depend on plasmid DNA as a critical foundational material for the production of viral vectors and for enabling precise genetic engineering of therapeutic constructs. Similarly, mRNA vaccines rely on high-quality plasmid DNA as a template for in-vitro transcription (IVT), which is essential for producing stable and effective mRNA molecules. As more therapies progress from early-stage clinical trials to late-stage development and commercialization, the demand for scalable and GMP-compliant plasmid production continues to rise. Additionally, the growing global patient population affected by rare genetic disorders, cancer, and chronic diseases is accelerating the need for advanced treatment modalities. This convergence of technological advancement and rising disease burden is significantly increasing the requirement for high-purity GMP-grade plasmid DNA, establishing it as a fundamental and indispensable component of next-generation biopharmaceutical manufacturing.

Get More Insights into the Report @Plasmid DNA Manufacturing Market

What are the latest plasmid DNA manufacturing market dynamics and trends?

The global market for plasmid DNA manufacturing has witnessed significant growth in recent years. This expansion is driven primarily by the rapid expansion of gene therapy pipelines, rising demand for mRNA vaccines and RNA-based therapeutics, growth of Cell and Gene Therapy (CGT) manufacturing, and rising prevalence of genetic and chronic diseases such as Duchenne Muscular Dystrophy (DMD), Spinal Muscular Atrophy (SMA), and Huntington’s disease.

The rapid expansion of gene therapy pipelines is one of the most powerful drivers of the plasmid DNA manufacturing market because plasmid DNA serves as the fundamental starting material for producing viral vectors (such as AAV and lentivirus) used in gene delivery systems. As the number of gene therapy candidates increases across oncology, rare genetic disorders, and neurology, demand for scalable and GMP-grade plasmid DNA has risen sharply. According to data provided by the American Cancer Society of Cell and Gene Therapy (2025), of the 80 gene therapy trials initiated in Q2, 64% targeted oncology indications, marking the highest proportion in the past year. In the cell therapy pipeline, oncology and rare diseases remained dominant, while 76% of the 33 newly initiated cell therapy trials were for non-oncology indications. In RNA therapies, 38 new trials were initiated in Q2, up from 35 in the previous quarter, with 74% focused on non-oncology applications.

In parallel, the broader gene and cell therapy ecosystem is rapidly advancing, with increasing regulatory approvals and large-scale commercialization efforts, further accelerating the need for reliable plasmid supply chains. For example, in January 2026, Eli Lilly signed an agreement worth up to $1.12 billion with Seamless Therapeutics, a Germany-based startup, to develop and commercialize treatments for hearing loss using the biotech's gene-editing platform. Collectively, this surge in clinical development, regulatory momentum, and high-value investments is driving the continuous expansion of plasmid DNA manufacturing capacity, making it a critical enabling infrastructure for next-generation therapeutics.

Additionally, the rising demand for mRNA vaccines and RNA-based therapeutics is significantly boosting the plasmid DNA manufacturing market because plasmid DNA is the essential starting template for producing mRNA through in vitro transcription (IVT). High-quality GMP-grade plasmid DNA is first linearized and then used to synthesize mRNA molecules, which are further formulated into vaccines and therapeutics for infectious diseases. The global expansion of mRNA platforms driven by rapid vaccine innovation post-COVID-19 has therefore created sustained demand for scalable plasmid DNA supply chains and high-purity production systems. For instance, in November 2025, Moderna announced the $140 million investment to strengthen its end-to-end mRNA manufacturing network in the U.S., aimed at supporting both clinical and commercial production of mRNA medicines across infectious diseases and oncology applications. In parallel, industry analyses emphasize that plasmid DNA is now a critical bottleneck and enabling raw material for RNA vaccine production, with increasing emphasis on GMP-grade quality and scalable fermentation-based manufacturing to meet growing clinical demand. Collectively, the rapid expansion of mRNA vaccine pipelines and RNA therapeutics is accelerating investments in plasmid DNA manufacturing capacity, positioning it as a foundational pillar of next-generation vaccine and drug production ecosystems.

Furthermore, the increasing product development activities among the key market players are further escalating the overall market of plasmid DNA manufacturing. For instance, in January 2023, Charles River expanded its portfolio by launching the eXpDNA™ plasmid manufacturing platform in order to offer efficient and accelerated GMP plasmid manufacturing and supply services to ATMP developers.

Thus, the factors mentioned above are expected to boost the overall market of plasmid DNA manufacturing during the forecasted period.

However, high manufacturing complexity and strict regulatory requirements together act as major limiting factors for the plasmid DNA manufacturing market. The production of plasmid DNA involves multiple sensitive steps such as bacterial fermentation, plasmid extraction, purification, and quality control, where even minor variations can affect yield, supercoiling efficiency, and overall product purity. At the same time, stringent regulatory standards imposed by agencies like the FDA and EMA require extensive testing for contaminants, endotoxins, and genetic stability, significantly increasing compliance burden. These combined challenges not only raise production costs and extend development timelines but also create bottlenecks in scaling up GMP-grade plasmid DNA, thereby limiting the overall speed and efficiency of market growth.

Plasmid DNA Manufacturing Market Segment Analysis

Plasmid DNA Manufacturing Market by Product Type (GMP-grade Plasmid DNA and Research-grade Plasmid DNA), Application (Cell Therapy Manufacturing, Gene Therapy Manufacturing, DNA / RNA Vaccine Development, Viral Vector Manufacturing, and Others), Production Scale (Commercial, Clinical, and Preclinical), End-Users (Pharmaceutical & Biotechnology Companies, Contract Development & Manufacturing Organizations (CDMOs), and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product Type: GMP-grade Plasmid DNA in the Plasmid DNA Manufacturing Category is Expected to Dominate the Market with the Largest Revenue Share

In the product type segment of the plasmid DNA manufacturing market, the GMP-grade Plasmid DNA category is contributing to 86.34% of total market revenue in 2025, because it is the only grade suitable for clinical and commercial therapeutic use, including gene therapies, mRNA vaccines, and viral vector production. GMP-grade plasmid DNA is manufactured under strict regulatory standards with validated processes, high traceability, and rigorous quality control, ensuring safety and consistency for human applications. It serves as a critical starting material for viral vectors (AAV and lentivirus) and as a template for in-vitro transcription (IVT) in mRNA vaccine production, making it indispensable for advanced biopharmaceutical development. As gene and cell therapy pipelines expand and more products move from clinical trials to commercialization, demand for GMP-grade plasmid DNA has increased significantly, supported by rising outsourcing to CDMOs and scaling of manufacturing capacity. Recent industry developments highlight this trend, such as in December 2025, Aldevron announced the continued expansion of GMP plasmid DNA manufacturing capabilities to support growing gene and cell therapy demand. Additionally, GMP plasmid DNA is now a key bottleneck material in advanced therapies, driving heavy investments in scalable, high-purity production platforms across leading CDMOs. Together, these factors reinforce GMP-grade plasmid DNA as the dominant and fastest-growing segment in the market.

By Application: Cell Therapy Manufacturing Category Dominates the Market

Within the application segment of the plasmid DNA manufacturing market, the cell therapy manufacturing category is anticipated to dominate, accounting for around 34.54% of the market share in 2025, because plasmid DNA is a critical raw material used for genetic engineering of immune cells and for producing viral vectors required in cell-based therapies such as CAR-T and other engineered cell therapies. The expansion of cell therapy pipelines across oncology and rare diseases has significantly increased demand for high-quality GMP-grade plasmid DNA, especially as more therapies progress from early-stage research to clinical and commercial manufacturing. Recent industry developments further reinforce this trend. For example, in November 2025, Bharat Biotech announced the launch of its new subsidiary “Nucelion Therapeutics,” which includes a GMP-compliant facility capable of producing plasmids and viral vectors to support cell and gene therapy development. This expansion highlights the growing investment in integrated manufacturing ecosystems for advanced therapies, where plasmid DNA serves as a foundational input. Additionally, regulatory updates from the U.S. FDA in February 2026, including new draft guidance on individualized and gene-based therapies, emphasize streamlined development pathways for cell and gene therapy products, further accelerating clinical translation and indirectly boosting demand for plasmid DNA as a key enabling material. Together, these developments show how rising clinical activity, manufacturing expansion, and regulatory support are collectively strengthening the role of cell therapy manufacturing in driving the plasmid DNA manufacturing market.

By Production Scale: Clinical Category Dominates the Market

In the production scale segment of the plasmid DNA manufacturing market, the clinical category is projected to dominate because most gene therapy, cell therapy, and mRNA vaccine programs are currently concentrated in Phase I, II, and III clinical trials, where GMP-grade plasmid DNA is required in moderate but highly regulated quantities. Clinical-scale manufacturing acts as a critical bridge between preclinical research and full commercial production, enabling biopharma companies to generate consistent, high-purity plasmid DNA batches for safety testing, dose optimization, and regulatory submissions. The rising number of clinical-stage gene and cell therapy programs globally has directly increased demand for flexible, scalable clinical manufacturing capacity. For instance, in August 2025, Bionova Scientific opened a new plasmid DNA development and production facility in Texas, specifically designed to support cell and gene therapy development and clinical-scale manufacturing needs, strengthening the U.S. supply chain for early- and mid-stage therapeutic programs. Similarly, multiple CDMO expansions have focused on increasing clinical and GMP manufacturing flexibility, reflecting the surge in ongoing clinical trials across oncology, rare diseases, and RNA-based therapies.

Collectively, these developments show that the clinical production scale segment is becoming the most active growth driver in plasmid DNA manufacturing due to its central role in advancing therapies from research into commercialization.

By End-Users: Pharmaceutical & Biotechnology Companies Category Dominates the Market

In the end-user segment of the plasmid DNA manufacturing market, pharmaceutical and biotechnology companies dominate the overall market due to their central role in the research, development, and commercialization of advanced therapeutics such as gene therapies, cell therapies, and mRNA-based vaccines. These companies generate the highest demand for plasmid DNA as it is a critical starting material for viral vector production, genetic engineering, and in-vitro transcription processes. With the rapid expansion of pipelines targeting rare genetic disorders, cancer, and infectious diseases, pharma and biotech firms are increasingly investing in both in-house capabilities and outsourcing partnerships with CDMOs to secure a reliable supply of GMP-grade plasmid DNA. Additionally, the growing number of clinical trials and regulatory approvals is pushing these companies to scale up production from preclinical to commercial levels, further strengthening their dominance. Their strong financial resources, continuous R&D investments, and focus on innovation in next-generation therapies collectively position pharmaceutical and biotechnology companies as the leading end users driving demand in the plasmid DNA manufacturing market.

Plasmid DNA Manufacturing Market Regional Analysis

North America Plasmid DNA Manufacturing Market Trends

North America is expected to account for the highest proportion of 44.12% of the plasmid DNA manufacturing market in 2025, out of all regions. North America is expected to dominate the plasmid DNA manufacturing market due to its strong presence of leading biotechnology and pharmaceutical companies, advanced biomanufacturing infrastructure, and high concentration of CDMOs specializing in gene and cell therapy production. The region also benefits from significant R&D investments, rapid adoption of advanced therapies such as gene therapy, CAR-T, and mRNA vaccines, and supportive regulatory approvals from agencies like the FDA. Additionally, the increasing number of clinical trials and commercialization of advanced biologics further strengthen North America’s leadership position in the global plasmid DNA manufacturing market.

According to the Centers for Disease Control and Prevention (2025), about 1 in every 5,000 males aged 5-9 years in the United States has Duchenne Muscular Dystrophy (DMD).

Additionally, the growth of cell and gene therapy (CGT) manufacturing in North America is significantly boosting the plasmid DNA manufacturing market, as plasmid DNA serves as a critical upstream raw material for viral vector production and genetic engineering processes used in these therapies. The rapid expansion of CGT pipelines with more than 4,000 therapies in development and over 2,000 active clinical trials globally as of January 2026 has sharply increased demand for high-quality GMP-grade plasmid DNA. This surge is further supported by continuous regulatory momentum. For instance, in May 2025, the U.S. FDA approved multiple advanced therapies, including gene therapies for rare diseases such as hemophilia B, expanding treatment availability and accelerating commercialization pathways. As more therapies move through clinical stages and toward commercialization, manufacturers are scaling up plasmid DNA production capacity to meet rising demand. Additionally, increasing investments in CGT manufacturing infrastructure across the U.S. are strengthening integrated supply chains, where plasmid DNA acts as a foundational input. Collectively, the growing CGT ecosystem, regulatory support, and expanding clinical pipeline in North America are driving sustained demand for plasmid DNA, positioning it as a critical enabler of next-generation therapeutic manufacturing.

Thus, the factors mentioned above are expected to boost the overall market of plasmid DNA manufacturing across the region.

Europe Plasmid DNA Manufacturing Market Trends

The plasmid DNA manufacturing market in Europe is experiencing robust growth due to the region’s strong biotechnology ecosystem, increasing investments in gene and cell therapy development, and expanding demand for GMP-grade plasmid DNA in clinical and commercial applications. Countries such as Germany, the U.K., and France are emerging as key hubs, supported by advanced research infrastructure, favorable regulatory frameworks, and growing CDMO capabilities. The market is witnessing significant momentum from the rising number of clinical trials and the increasing adoption of plasmid DNA in gene therapies, DNA vaccines, and immunotherapies. Additionally, continuous technological advancements in plasmid production, including automation and high-yield fermentation systems, are improving scalability and efficiency across European facilities. Recent developments further highlight this growth trajectory. For instance, in November 2025, Kaneka’s subsidiary Eurogentec expanded its GMP plasmid DNA and biologics manufacturing capabilities in Belgium to support increasing demand from gene therapy and vaccine developers, strengthening Europe’s position in the global supply chain.

Moreover, the rising investments by CDMOs and biopharma companies across Europe to enhance plasmid DNA production capacity and integrate end-to-end gene therapy manufacturing solutions reflect the growing need for localized and scalable supply chains. With market projections showing Europe’s plasmid DNA manufacturing sector expanding significantly over the next decade, driven by increasing R&D activities and clinical advancements, the region is poised to remain a key contributor to global market growth.

Asia-Pacific Plasmid DNA Manufacturing Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the plasmid DNA manufacturing market due to rapidly expanding biotechnology capabilities, increasing investments in gene and cell therapy research, and the growing presence of contract development and manufacturing organizations (CDMOs) across countries such as China, Japan, South Korea, and India. The region is witnessing strong demand for plasmid DNA as a key raw material for gene therapies, DNA vaccines, and mRNA-based therapeutics, supported by a rising burden of chronic and genetic diseases and an aging population. Additionally, governments and private players are heavily investing in local biomanufacturing infrastructure, which is accelerating clinical trial activity and the commercialization of advanced therapies.

Recent developments further highlight this growth trajectory. For instance, in June 2024, Asahi Kasei (through its subsidiary Bionova Scientific) announced a $100 million investment to expand into plasmid DNA manufacturing, including the development of large-scale facilities to support gene and cell therapy pipelines.

Furthermore, leading manufacturers such as FUJIFILM Holdings Corporation and WuXi Biologics are continuously expanding their biologics and advanced therapy manufacturing capabilities in Asia, strengthening integrated supply chains for plasmid DNA production.

Thus, the factors mentioned above are expected to boost the overall market of plasmid DNA manufacturing across the region.

Who are the major players in the plasmid DNA manufacturing market?

The following are the leading companies in the plasmid DNA manufacturing market. These companies collectively hold the largest market share and dictate industry trends.

- Thermo Fisher Scientific

- Charles River Laboratories

- Lonza

- Aldevron (Danaher)

- GenScript ProBio

- AGC Biologics

- Cobra Biologics (Charles River)

- Catalent

- WuXi AppTec

- WuXi Advanced Therapies

- Eurogentec

- Sartorius (BIA Separations)

- ProBio

- PharmaCell

- Pharmaron

- Esco Aster

- AGTC (Applied Genetic Technologies Corp.)

- VGXI (GeneOne Life Science)

- PlasmidFactory

- VectorBuilder

- Others

How is the competitive landscape shaping the plasmid DNA manufacturing market?

The competitive landscape of the plasmid DNA manufacturing market is characterized by a moderately consolidated structure with increasing concentration among a few key players, primarily large contract development and manufacturing organizations (CDMOs) and specialized biotech firms. Leading companies such as Thermo Fisher Scientific, Lonza, Charles River Laboratories, and Aldevron dominate the market due to their strong GMP manufacturing capabilities, global infrastructure, and integrated service offerings. Market data indicates that over 45–60% of the industry is controlled by top manufacturers, reflecting a relatively high level of concentration and the presence of established leaders with significant technological and regulatory expertise.

At the same time, the market remains highly competitive and innovation-driven, with companies differentiating themselves through scalable GMP production, advanced purification technologies, and end-to-end solutions (plasmid to viral vector manufacturing). Increasing mergers, acquisitions, and strategic partnerships are further consolidating the market, as firms aim to expand capacity, enhance technological capabilities, and secure long-term contracts with biopharma clients. Additionally, the growing trend of outsourcing, where more than 70% of plasmid DNA production in mature markets is handled by CDMOs, has intensified competition among service providers while reinforcing the dominance of established players.

Overall, the competitive landscape is evolving into a concentrated yet dynamic market, where a few global leaders hold significant share, but continuous innovation, capacity expansion, and the entry of niche and regional players are maintaining competitive intensity and shaping long-term market growth.

Recent Developmental Activities in the Plasmid DNA Manufacturing Market

- In December 2025, Aldevron announced the continued expansion of GMP plasmid DNA manufacturing capabilities to support growing gene and cell therapy demand.

- In November 2025, Bharat Biotech announced the launch of its new subsidiary, “Nucelion Therapeutics,” which includes a GMP-compliant facility capable of producing plasmids and viral vectors to support cell and gene therapy development.

- In April 2025, Thermo Fisher Scientific expanded its plasmid DNA manufacturing capacity in the United States, introducing enhanced single-use bioreactors and automated purification systems to support large-scale production for gene therapy and mRNA vaccine applications. This expansion was aimed at addressing growing demand from clinical and commercial gene therapy pipelines.

- In January 2023, Charles River expanded its portfolio by launching the eXpDNA™ plasmid manufacturing platform in order to offer efficient and accelerated GMP plasmid manufacturing and supply services to ATMP developers.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Plasmid DNA Manufacturing Market CAGR |

18.06% |

|

Key Companies in the Plasmid DNA Manufacturing Market |

Thermo Fisher Scientific, Charles River Laboratories, Lonza, Aldevron (Danaher), GenScript ProBio, AGC Biologics, Cobra Biologics (Charles River), Catalent, WuXi AppTec, WuXi Advanced Therapies, Eurogentec, Sartorius (BIA Separations), ProBio, PharmaCell, Pharmaron, Esco Aster, AGTC (Applied Genetic Technologies Corp.), VGXI (GeneOne Life Science), PlasmidFactory, VectorBuilder, and others. |

|

Plasmid DNA Manufacturing Market Segments |

by Product Type, by Application, by Production Scale, by End-Users, and by Geography |

|

Plasmid DNA Manufacturing Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Plasmid DNA Manufacturing Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Plasmid DNA Manufacturing Market Segmentation

- Plasmid DNA Manufacturing by Product Type Exposure

- GMP-grade Plasmid DNA

- Research-grade Plasmid DNA

- Plasmid DNA Manufacturing Application Exposure

- Cell Therapy Manufacturing

- Gene Therapy Manufacturing

- DNA / RNA Vaccine Development

- Viral Vector Manufacturing

- Others

- Plasmid DNA Manufacturing Production Scale Exposure

- Commercial

- Clinical

- Preclinical

- Ambulance End-Users Exposure

- Pharmaceutical & Biotechnology Companies

- Contract Development & Manufacturing Organizations (CDMOs)

- Others

- Plasmid DNA Manufacturing Geography Exposure

- North America Plasmid DNA Manufacturing Market

- United States Plasmid DNA Manufacturing Market

- Canada Plasmid DNA Manufacturing Market

- Mexico Plasmid DNA Manufacturing Market

- Europe Plasmid DNA Manufacturing Market

- United Kingdom Plasmid DNA Manufacturing Market

- Germany Plasmid DNA Manufacturing Market

- France Plasmid DNA Manufacturing Market

- Italy Plasmid DNA Manufacturing Market

- Spain Plasmid DNA Manufacturing Market

- Rest of Europe Plasmid DNA Manufacturing Market

- Asia-Pacific Plasmid DNA Manufacturing Market

- China Plasmid DNA Manufacturing Market

- Japan Plasmid DNA Manufacturing Market

- India Plasmid DNA Manufacturing Market

- Australia Plasmid DNA Manufacturing Market

- South Korea Plasmid DNA Manufacturing Market

- Rest of Asia-Pacific Plasmid DNA Manufacturing Market

- Rest of the World Plasmid DNA Manufacturing Market

- South America Plasmid DNA Manufacturing Market

- Middle East Plasmid DNA Manufacturing Market

- Africa Plasmid DNA Manufacturing Market

- North America Plasmid DNA Manufacturing Market

Plasmid DNA Manufacturing Market Recent Industry Trends and Milestones (2022-2026)

|

Category |

Key Developments |

|

Plasmid DNA Manufacturing Product Launch |

Bharat Biotech announced the launch of its new subsidiary, “Nucelion Therapeutics,” which includes a GMP-compliant facility capable of producing plasmids and viral vectors. Bionova Scientific (Asahi Kasei Group) launched a 10,000 sq. ft. plasmid DNA development and manufacturing facility in The Woodlands, Texas, |

|

Plasmid DNA Manufacturing Partnership |

VGXI entered a multi-year agreement with a vaccine developer to manufacture plasmid DNA for a next-generation DNA-based influenza vaccine. Wacker Biotech partners with Gearbox Biosciences to focus on next-generation plasmid DNA manufacturing, including antibiotic-free production systems. |

|

Company Strategy |

Aldevron is focusing on a phase-appropriate plasmid strategy, aligning plasmid grade (research vs GMP) with each development stage to reduce cost and timelines. Thermo Fisher is expanding its GeneArt plasmid DNA services as part of a broader integrated CGT manufacturing platform, and Lonza is strengthening its viral vector manufacturing network, which directly increases internal demand for plasmid DNA. |

|

Emerging Technology |

Enzymatic DNA synthesis (Cell-Free DNA Technology), rolling circle amplification (RCA)-based DNA production, automation & robotic bioprocessing, synthetic biology & modular DNA platforms, high-yield fermentation technologies (next-gen bioprocessing), and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are increasingly transforming plasmid DNA manufacturing by enhancing efficiency, precision, and scalability across the entire workflow. Artificial intelligence and machine learning algorithms are being used to optimize plasmid design, enabling rapid identification of ideal gene sequences, promoters, and vector backbones for specific therapeutic applications such as gene therapy and mRNA production. In upstream processing, AI helps optimize fermentation conditions by analyzing large datasets to predict optimal growth parameters, improve plasmid yield, and reduce batch variability. During downstream processing, AI-driven models support purification optimization, improving separation efficiency and ensuring higher purity levels by predicting contaminant profiles and process outcomes. Additionally, AI is enabling predictive quality control and real-time monitoring, allowing manufacturers to detect deviations early, reduce failure rates, and ensure compliance with GMP standards. Digital twins and smart manufacturing systems are also being adopted to simulate plasmid production processes, enabling faster scale-up from laboratory to commercial levels. Overall, the integration of AI is helping reduce production timelines, lower costs, and improve consistency, making plasmid DNA manufacturing more robust and responsive to the growing demands of advanced therapeutics.

U.S. Tariff Impact Analysis on Plasmid DNA Manufacturing Market

The U.S. tariff impact on the plasmid DNA manufacturing market is multifaceted, acting both as a cost burden and a strategic driver for domestic capacity expansion. Tariffs imposed on imported bioprocessing equipment (e.g., bioreactors, chromatography systems) and critical raw materials such as reagents and cell culture components have significantly increased the overall cost of establishing and operating plasmid DNA manufacturing facilities in the U.S. These cost pressures are particularly impactful because nearly 90% of U.S. biotech companies rely on imported components, making the supply chain highly sensitive to trade policies. Additionally, newer tariff measures introduced in 2025 have imposed duties ranging from 15% to 25% on key inputs, further increasing production expenses and potentially extending lead times for sourcing alternatives.

However, these tariffs also have a dual positive effect by encouraging local manufacturing and supply chain localization. To mitigate tariff risks, many biopharmaceutical companies are increasing investments in domestic production infrastructure, which is strengthening the U.S. plasmid DNA manufacturing ecosystem and reducing long-term dependency on imports. Overall, while tariffs raise short-term costs and create operational challenges, they are simultaneously driving strategic reshoring, capacity expansion, and supply chain resilience, ultimately shaping a more self-reliant but higher-cost plasmid DNA manufacturing market in the United States.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Bionova Scientific |

$100 million |

- |

large-scale plasmid DNA manufacturing facility |

To initiate a persistent unmet need for high-quality, timely, and reliable pDNA supply among developers of novel cell and gene therapies (CGT). |

Key takeaways from the Plasmid DNA Manufacturing market report study

- Market size analysis for the current plasmid DNA manufacturing market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the plasmid DNA manufacturing market.

- Various opportunities available for the other competitors in the plasmid DNA manufacturing market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current plasmid DNA manufacturing market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the plasmid DNA manufacturing market growth in the future?