Viral Vector CDMO Market Summary

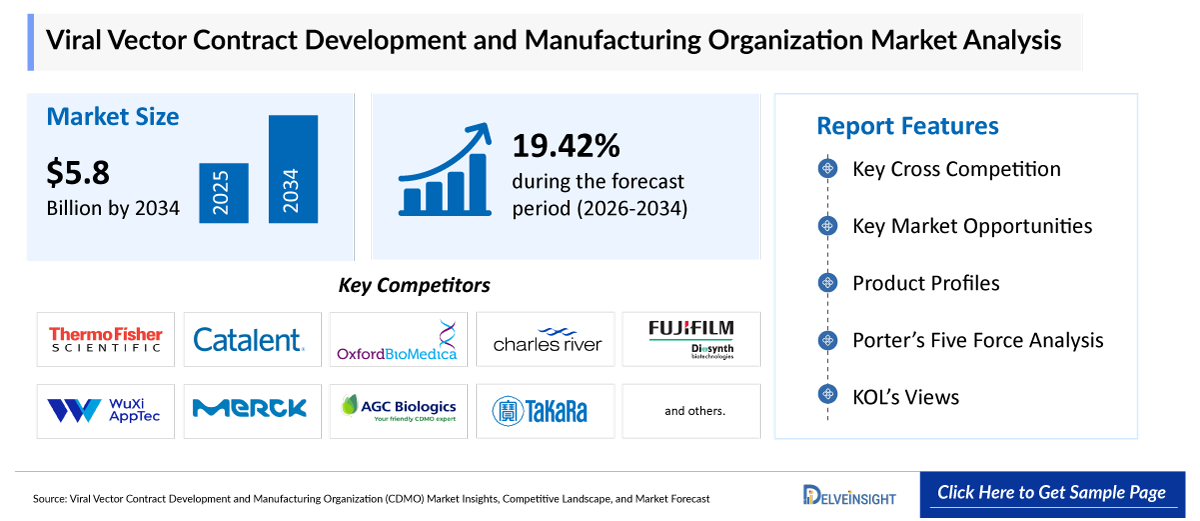

- The global viral vector contract development and manufacturing organization market is expected to increase from USD 1,186.16 million in 2025 to USD 5,832.21 million by 2034, reflecting strong and sustained growth.

- The global viral vector contract development and manufacturing organization market is growing at a CAGR of 19.42% during the forecast period from 2026 to 2034.

- The rapid expansion of gene and cell therapy pipelines, increasing outsourcing by biotech and pharmaceutical companies, rising investment in biotechnology and gene therapy R&D, and the growing use of viral vectors in vaccine and infectious disease applications are collectively driving strong growth in the viral vector CDMO market. As more advanced therapies progress through clinical development, demand for scalable, high-quality GMP manufacturing of viral vectors is increasing significantly. Since most biotech firms lack in-house manufacturing capabilities, they rely on CDMOs for end-to-end production, accelerating outsourcing trends. At the same time, sustained funding in gene therapy innovation and the expansion of vaccine platforms are further broadening the application scope of viral vectors, making CDMOs a critical enabler in the commercialization of next-generation therapies.

- The leading companies operating in the viral vector contract development and manufacturing organization market include Lonza Group, Thermo Fisher Scientific, Catalent, Oxford Biomedica, Charles River Laboratories, FUJIFILM Diosynth Biotechnologies, WuXi AppTec, Merck KGaA, AGC Biologics, Takara Bio, Samsung Biologics, Curia Global, GenScript ProBio, Creative Biogene, VectorBuilder, Aldevron, FinVector, Yposkesi, VGXI, Genezen, and others.

- North America is expected to dominate the viral vector contract development and manufacturing organization market due to its strong concentration of leading biotechnology and pharmaceutical companies, advanced gene and cell therapy pipeline, and high levels of R&D investment. The region also benefits from well-established manufacturing infrastructure, favorable regulatory support from agencies such as the FDA for accelerated approvals of advanced therapies, and a robust ecosystem of specialized CDMOs and academic research institutions. In addition, increasing clinical trials for gene therapies and growing outsourcing activities by biopharma companies further strengthen North America’s leading position in this market.

- In the vector type segment of the viral vector contract development and manufacturing organization market, the Adeno-Associated Virus (AAV) category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Viral Vector Contract Development and Manufacturing Organization Market

Viral Vector Contract Development and Manufacturing Organization Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 1,186.16 million |

|

2034 Projected Market Size |

USD 5,832.21 million |

|

Growth Rate (2026-2034) |

19.42% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Viral Vector Contract Development and Manufacturing Organization Market

Rapid expansion of gene and cell therapy pipelines leading to a surge in viral vector contract development and manufacturing organization: The single biggest driver is the surging number of gene therapies, cell therapies, and gene-modified vaccines entering clinical trials and commercialization.

- Viral vectors (AAV, lentivirus, adenovirus) are essential delivery systems for these therapies.

- Increasing approvals in oncology, rare genetic disorders, and ophthalmology are pushing demand for large-scale GMP vector production.

- As more therapies move from Phase I to Phase III commercialization, CDMOs are heavily relied upon for scale-up manufacturing.

- Increasing outsourcing by biotech and pharma companies: Most biotech companies lack in-house GMP manufacturing capability for viral vectors.

- High capital cost and technical complexity make internal manufacturing difficult.

- Companies prefer outsourcing to CDMOs to focus on R&D and clinical development.

- This has made outsourcing a structural, long-term growth driver for the industry.

- Rising investment in biotechnology and gene therapy R&D: There is a sustained inflow of capital into:

- Gene therapy startups

- Cell therapy platforms (CAR-T, CAR-NK)

- Viral vector innovation technologies

Public funding, venture capital, and pharma partnerships are accelerating development pipelines, which increases demand for CDMO services.

- Expansion of vaccine and infectious disease applications: Post-COVID and ongoing infectious disease concerns have increased.

- Use of viral vectors in vaccine platforms

- Need for rapid, scalable production systems

- Government preparedness programs for pandemic response

This strengthens long-term CDMO demand beyond gene therapy alone.

Viral Vector Contract Development and Manufacturing Organization Market Report Segmentation

This viral vector contract development and manufacturing organization market report offers a comprehensive overview of the global viral vector contract development and manufacturing organization market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Vector Type (Adeno-Associated Virus (AAV), Lentivirus, Adenovirus, Retrovirus, and Other), Application (Gene Therapy, Cell Therapy, Vaccine Development, Antisense & RNAi Therapy, and Others), Workflow Stage (Upstream Processing and Downstream Processing), End-Users (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, and Others), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing viral vector contract development and manufacturing organization market.

A Viral Vector Contract Development and Manufacturing Organization (CDMO) is a specialized service provider that supports biotechnology and pharmaceutical companies in the development, production, and large-scale manufacturing of viral vectors used in gene and cell therapies. These organizations offer end-to-end services, including process development, scale-up, GMP-compliant manufacturing, and quality testing for viral delivery systems such as adeno-associated viruses (AAV), lentiviruses, and adenoviruses. By leveraging advanced manufacturing technologies and regulatory expertise, viral vector CDMOs enable faster and more efficient production of complex therapies, allowing biotech companies to focus on research and clinical development.

The rapid expansion of gene and cell therapy pipelines, increasing outsourcing by biotech and pharmaceutical companies, rising investment in biotechnology and gene therapy R&D, and the growing use of viral vectors in vaccine and infectious disease applications are collectively driving robust growth in the viral vector CDMO market. As a large number of advanced therapies progress from early-stage research to late-stage clinical trials and commercialization, the need for scalable, high-quality, and GMP-compliant viral vector manufacturing has increased significantly. Viral vectors play a critical role in delivering genetic material in therapies such as CAR-T, gene replacement treatments, and next-generation vaccines, further strengthening their demand across therapeutic areas.

Since most biotech firms and emerging players lack the infrastructure, technical expertise, and regulatory capability required for in-house large-scale viral vector production, they increasingly depend on CDMOs for end-to-end services, including process development, scale-up, manufacturing, and quality control. This growing reliance has accelerated outsourcing trends across the industry. Additionally, sustained funding from venture capital, government initiatives, and pharmaceutical collaborations in gene therapy innovation is expanding the global development pipeline. The increasing application of viral vectors in both therapeutic and preventive vaccine development is further broadening their use case, positioning CDMOs as essential partners in enabling the efficient, cost-effective, and compliant commercialization of next-generation advanced therapies.

Get More Insights into the Report @ Viral Vector Contract Development and Manufacturing Organization Market

What are the latest viral vector contract development and manufacturing organization market dynamics and trends?

The rapid expansion of gene and cell therapy pipelines, increasing outsourcing by biotech and pharmaceutical companies, rising investment in biotechnology and gene therapy R&D, and the growing use of viral vectors in vaccine and infectious disease applications are collectively driving strong growth in the viral vector CDMO market.

The rapid expansion of gene and cell therapy pipelines is significantly boosting the viral vector CDMO market by increasing the demand for reliable, scalable, and GMP-compliant manufacturing of viral vectors. As a growing number of gene therapies (such as AAV-based treatments for rare genetic disorders) and cell therapies (including CAR-T and CAR-NK therapies using lentiviral vectors) advance from early-stage research to late-stage clinical trials and commercialization, the need for consistent and high-quality vector supply rises sharply. This growing pipeline intensity places pressure on biotech and pharmaceutical companies, most of which lack in-house manufacturing capabilities, leading them to increasingly outsource production to specialized CDMOs. As a result, CDMOs are becoming critical partners in process development, scale-up, clinical supply, and commercial manufacturing of viral vectors. Recent developments clearly reflect this trend. For instance, in December 2024, the U.S. FDA approved Autolus’ CAR-T therapy using lentiviral vectors manufactured by AGC Biologics, further reinforcing CDMOs’ role in commercial gene therapy supply chains.

On the capacity expansion side, in June 2025, ProBio launched its 128,000 sq. ft. GMP viral vector and plasmid DNA manufacturing facility in New Jersey, designed specifically to support increasing demand from expanding gene therapy pipelines. In addition, in August 2025, ProBio also initiated GMP AAV manufacturing services at the same facility, further scaling its ability to support clinical-to-commercial viral vector production.

Furthermore, rising investment in biotechnology and gene therapy R&D is significantly boosting the viral vector CDMO market by accelerating the development of advanced gene and cell therapy pipelines that depend on viral vectors for delivery. Increased funding from venture capital firms, pharmaceutical partnerships, and government-backed innovation programs is enabling a higher number of biotech companies to progress from discovery to clinical-stage programs, particularly in AAV and lentiviral-based therapies. This surge in capital inflow is directly translating into greater outsourcing demand for CDMO services, as companies require specialized expertise for vector design, process development, and GMP manufacturing. Recent developments highlight this trend clearly. In September 2025, Kriya Therapeutics raised $320 million in Series D funding to advance its gene therapy pipeline and strengthen its manufacturing capabilities, reflecting strong investor confidence in scalable gene therapy platforms. Thus, the factors mentioned above are expected to boost the overall market of viral vector contract development and manufacturing organizations during the forecast period.

However, the high manufacturing complexity and stringent regulatory requirements are key limiting factors for the viral vector CDMO market. The production of viral vectors such as AAV and lentivirus involves highly specialized, multi-step processes that require precise control of cell culture, purification, and quality testing, making scale-up difficult and time-consuming. Even minor variations in process conditions can impact yield, potency, and safety, increasing the risk of batch failures. In addition, strict regulatory standards imposed by agencies such as the FDA and EMA require extensive documentation, validation, and compliance with GMP guidelines, which further lengthen development timelines and increase operational costs. Together, these challenges restrict manufacturing efficiency and slow down the overall commercialization of gene and cell therapies.

Viral Vector Contract Development and Manufacturing Organization Market Segment Analysis

Viral Vector Contract Development and Manufacturing Organization Market by Vector Type (Adeno-Associated Virus (AAV), Lentivirus, Adenovirus, Retrovirus, and Other), Application (Gene Therapy, Cell Therapy, Vaccine Development, Antisense & RNAi Therapy, and Others), Workflow Stage (Upstream Processing and Downstream Processing), End-Users (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Vector Type: Adeno-Associated Virus (AAV) is expected to dominate the market with the largest revenue share.

In the vector type segment of the viral vector contract development and manufacturing organization market, the Adeno-Associated Virus (AAV) category is contributing to 47% of total market revenue in 2025, due to its strong safety profile, low immunogenicity, and high efficiency in long-term gene expression. AAV vectors are widely used in gene therapies targeting rare genetic disorders, ophthalmic diseases, neurological conditions, and certain metabolic diseases, making them one of the most clinically advanced and commercially viable viral vector platforms. Their ability to deliver genetic material without integrating into the host genome significantly reduces the risk of insertional mutagenesis, further increasing their preference in therapeutic development. Additionally, the rapid expansion of AAV-based clinical pipelines and increasing regulatory approvals are driving substantial demand for large-scale, GMP-compliant manufacturing services. This has led biotech and pharmaceutical companies to heavily rely on CDMOs for process optimization, scalable production, and high-quality vector supply. Continuous advancements in AAV production technologies, including improved yield systems and suspension-based manufacturing, are further strengthening its dominance in the viral vector CDMO market.

Additionally, the increasing product development activities are further escalating the overall market of the category in viral vector contract development and manufacturing organization markets. For instance, in May, 2024, Catalent entered a strategic partnership with Siren Biotechnology to support AAV-based immuno-gene therapy development and GMP manufacturing, strengthening its role in clinical-stage AAV vector supply for oncology programs. Additionally, in November 2025, AGC Biologics signed a manufacturing agreement for dual AAV vector gene therapies targeting inherited retinal disorders, using advanced AAV platforms to address gene size limitations and improve delivery efficiency.

As a result, the AAV segment not only supports the adoption of viral vector contract development and manufacturing organizations but also acts as a key revenue generator, thereby significantly boosting the overall growth of the viral vector contract development and manufacturing organization market.

By Application: Gene Therapy category dominates the market

Within the application segment of the viral vector contract development and manufacturing organization market, the gene therapy category is anticipated to dominate, accounting for around 46% of the market share in 2025, due to its extensive and rapidly expanding clinical pipeline targeting a wide range of genetic, rare, and chronic diseases. Gene therapy relies heavily on viral vectors, particularly AAV and lentiviral vectors, to deliver functional genes into patient cells, making it the largest and most critical application area driving demand for CDMO services. The increasing number of gene therapy candidates progressing from preclinical research to late-stage clinical trials and commercialization is significantly boosting the need for scalable, GMP-compliant viral vector manufacturing.

Additionally, rising approvals of gene therapies for conditions such as inherited retinal disorders, hemophilia, and spinal muscular atrophy are further accelerating market growth. For instance, in November 2024, AGC Biologics supported the FDA approval of Autolus Therapeutics’ CAR-T gene therapy (AUCATZYL®), where its Milan facility manufactured the required lentiviral vectors, highlighting how late-stage gene therapy approvals depend on CDMO-produced viral vectors.

Since most biotech and pharmaceutical companies lack in-house manufacturing capabilities, they depend on CDMOs for end-to-end services, including process development, scale-up, and commercial production. Continuous advancements in vector engineering and manufacturing technologies, along with strong investment inflows into gene therapy R&D, are further reinforcing gene therapy’s dominance within the viral vector CDMO market.

By Workflow Stage: The downstream processing category dominates the market.

Within the workflow stage segment of the viral vector contract development and manufacturing organization market, the downstream processing category is anticipated to dominate, accounting for around 55% of the market share in 2025, due to the high complexity associated with viral vector purification and quality assurance. After the viral vectors are produced during upstream processing, they must undergo multiple purification and concentration steps to remove impurities such as host cell proteins, residual DNA, plasmids, cell debris, and empty capsids. These purification requirements are particularly critical for vectors such as adeno-associated viruses (AAVs) and lentiviruses, where even minor impurities can impact therapeutic efficacy and patient safety. As a result, CDMOs invest heavily in advanced downstream technologies, including chromatography, ultrafiltration, and tangential flow filtration systems, making downstream processing the most resource-intensive stage of manufacturing.

Another key factor supporting the dominance of downstream processing is the stringent regulatory environment surrounding gene and cell therapies. Regulatory agencies such as the FDA and EMA require extremely high levels of purity, consistency, and product characterization before approving viral vector-based therapies. This has increased the need for sophisticated analytical testing and robust purification workflows, significantly raising the cost contribution of downstream activities compared to upstream production. In many cases, downstream purification and quality control together account for the majority of total manufacturing expenses, particularly in commercial-scale production.

The growing commercialization of gene therapies is also driving demand for scalable downstream processing capabilities. As more therapies transition from clinical trials to commercial manufacturing, CDMOs are required to produce larger batches while maintaining vector integrity, potency, and yield. However, viral vectors are highly sensitive biologics, and substantial product loss can occur during purification. Therefore, companies are increasingly focusing on optimizing downstream recovery rates and improving process efficiency, further increasing investments in this segment.

In addition, AAV-based therapies, which currently dominate the viral vector market, require complex separation of full and empty capsids during purification. This step is technically challenging and requires advanced downstream processing platforms, contributing significantly to overall manufacturing costs. Consequently, the increasing adoption of AAV vectors in gene therapy pipelines continues to strengthen the market share of downstream processing within the Viral Vector CDMO industry.

By End-Users: Pharmaceutical & Biotechnology Companies category dominates the market

In the end-users segment of the viral vector contract development and manufacturing organization market, the pharmaceutical & biotechnology companies category dominates due to their central role in developing and commercializing gene and cell therapies that rely on viral vectors. These companies account for the majority of demand as they have extensive pipelines of advanced therapies requiring scalable, high-quality viral vector manufacturing. However, most small and mid-sized biotech firms, and even many large pharmaceutical companies, lack the specialized infrastructure, technical expertise, and regulatory capabilities needed for in-house production. As a result, they heavily depend on CDMOs for end-to-end services, including process development, clinical manufacturing, and commercial-scale production. Additionally, increasing R&D investments, strategic collaborations, and a growing focus on outsourcing to reduce costs and accelerate time-to-market are further strengthening the dominance of pharmaceutical and biotechnology companies in this segment.

Viral Vector Contract Development and Manufacturing Organization Market Regional Analysis

North America Viral Vector Contract Development and Manufacturing Organization Market Trends

North America is expected to account for the highest proportion of 35% of the viral vector contract development and manufacturing organization market in 2025, out of all regions. In North America, the rapid expansion of gene and cell therapy pipelines, increasing outsourcing by biotech and pharmaceutical companies, rising investment in biotechnology R&D, and the growing use of viral vectors in vaccine and infectious disease applications are collectively driving strong growth in the viral vector CDMO market.

The region benefits from a high concentration of clinical-stage gene therapy programs and advanced research infrastructure, which significantly increases the demand for scalable viral vector manufacturing. As many companies lack in-house production capabilities, outsourcing to CDMOs has become essential, especially for complex therapies such as CAR-T and AAV-based treatments. At the same time, recent developments further demonstrate this trend. For instance, in October 2025, Oxford Biomedica expanded its U.S. footprint by acquiring a commercial-scale viral vector manufacturing facility in North Carolina, supported by a £60 million investment to strengthen CDMO capacity and production capabilities. Similarly, in July 2025, AstraZeneca announced a $50 billion investment plan to expand U.S. manufacturing and R&D infrastructure, including cell and gene therapy capabilities, reinforcing demand for advanced manufacturing services.

Collectively, these factors, such as strong clinical pipelines, heavy investment inflows, increasing outsourcing, and continuous facility expansion, are positioning North America as the leading region in the viral vector CDMO market, with sustained growth driven by innovation and commercialization of advanced therapies.

Europe Viral Vector Contract Development and Manufacturing Organization Market Trends

The viral vector Contract Development and Manufacturing Organization (CDMO) market in Europe is witnessing strong and sustained growth due to the region’s robust gene and cell therapy ecosystem, increasing government and private funding, and the presence of well-established CDMO players with advanced manufacturing capabilities. Countries such as Germany, the U.K., Italy, and Denmark are emerging as key hubs for viral vector production, supported by strong academic research networks and favorable regulatory frameworks for advanced therapy medicinal products (ATMPs). The rising number of gene therapy clinical trials and growing reliance on outsourcing by biotech companies are significantly increasing demand for specialized CDMO services, particularly for AAV and lentiviral vector manufacturing. Additionally, Europe’s focus on innovation, quality compliance, and cross-border collaborations is further accelerating market expansion.

Recent developments highlight this growth trajectory. For instance, in October 2024, AGC Biologics began operations at its new state-of-the-art manufacturing facility in Copenhagen, Denmark, strengthening its European production capacity following regulatory inspection and licensing. Furthermore, in April 2025, AGC Biologics launched a dedicated Cell and Gene Technologies Division to enhance its CDMO capabilities and support increasing demand from gene therapy developers across Europe.

Collectively, these developments demonstrate that increasing investments, expanding infrastructure, and strategic collaborations are positioning Europe as a key growth region in the viral vector CDMO market, with sustained momentum driven by innovation and commercialization of advanced gene therapies.

Asia-Pacific Viral Vector Contract Development and Manufacturing Organization Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the viral vector Contract Development and Manufacturing Organization (CDMO) market due to its rapidly expanding biotechnology ecosystem, increasing investment in gene and cell therapy R&D, and growing focus on building local manufacturing capabilities. Countries such as China, Japan, South Korea, and India are witnessing a surge in clinical research activities and government support for advanced therapies, which is significantly increasing the demand for viral vector production. Additionally, the region offers cost-effective manufacturing, a skilled workforce, and improved regulatory frameworks, making it an attractive destination for outsourcing by global pharmaceutical and biotech companies. As a result, many international CDMOs are expanding their presence in APAC, while local players are scaling up capabilities to meet rising demand.

Recent developments further highlight this growth momentum. For instance, in June 2025, AGC Biologics expanded its cell and gene therapy development operations in Yokohama, Japan, strengthening its regional manufacturing footprint to support growing clinical demand. Furthermore, in September 2025, Thermo Fisher Scientific partnered with South Korea-based Dr. Park CDMO to enable large-scale viral vector production using advanced bioprocessing technologies, enhancing manufacturing capacity in the region. Additionally, in September 2025, eXmoor Pharma collaborated with Siam Bioscience in Thailand to establish a major cell and gene therapy development and manufacturing hub in Southeast Asia. More recently, in March 2026, Merck signed an MoU with Cyto-Facto to strengthen lentiviral vector production platforms and accelerate CDMO capabilities across APAC.

Thus, the factors mentioned above are expected to boost th eoverall market of viral vector CDMO market across the APAC region.

Who are the major players in the viral vector contract development and manufacturing organization market?

The following are the leading companies in the viral vector contract development and manufacturing organization market. These companies collectively hold the largest market share and dictate industry trends.

- Lonza Group

- Thermo Fisher Scientific

- Catalent

- Oxford Biomedica

- Charles River Laboratories

- FUJIFILM Diosynth Biotechnologies

- WuXi AppTec

- Merck KGaA

- AGC Biologics

- Takara Bio

- Samsung Biologics

- Curia Global

- GenScript ProBio

- Creative Biogene

- VectorBuilder

- Aldevron

- FinVector

- Yposkesi

- VGXI

- Genezen

- Others

How is the competitive landscape shaping the viral vector contract development and manufacturing organization market?

The competitive landscape of the viral vector Contract Development and Manufacturing Organization (CDMO) market is highly dynamic and moderately consolidated, characterized by the presence of a few large global players alongside numerous specialized niche providers. Leading companies such as Thermo Fisher Scientific, Lonza, Catalent, Charles River Laboratories, and Oxford Biomedica dominate a significant share of the market, collectively accounting for a large portion of global viral vector manufacturing revenues.

Competition in this market is primarily driven by technical expertise, manufacturing capacity, regulatory compliance, and the ability to provide end-to-end services, as clients increasingly prefer integrated CDMO partners capable of supporting the entire value chain from process development to commercial production. Companies are differentiating themselves through advanced platform technologies (such as AAV and lentiviral systems), process innovation, and large-scale GMP facility expansions, while also investing in automation and cost-efficient manufacturing solutions to gain a competitive edge.

Additionally, the market is witnessing intense strategic activity, including mergers and acquisitions, partnerships with gene therapy developers, and geographic expansion to strengthen global footprints. Large CDMOs are acquiring specialized capabilities to enhance service portfolios, while smaller players compete by offering niche expertise, flexibility, and customized solutions. The increasing complexity of gene and cell therapies is further intensifying competition, as companies race to improve scalability, reduce costs, and meet stringent regulatory standards. Overall, the competitive landscape is evolving rapidly, with innovation, capacity expansion, and strategic collaborations shaping market leadership in the viral vector CDMO industry.

Recent Developmental Activities in the Viral Vector Contract Development and Manufacturing Organization Market

- In March 2026, Merck signed an MoU with Cyto-Facto to strengthen lentiviral vector production platforms and accelerate CDMO capabilities across APAC.

- In November 2025, AGC Biologics signed a manufacturing agreement for dual AAV vector gene therapies targeting inherited retinal disorders, using advanced AAV platforms to address gene size limitations and improve delivery efficiency.

- In September 2025, eXmoor Pharma collaborated with Siam Bioscience in Thailand to establish a major cell and gene therapy development and manufacturing hub in Southeast Asia.

- In September 2025, Thermo Fisher Scientific partnered with South Korea-based Dr. Park CDMO to enable large-scale viral vector production using advanced bioprocessing technologies, enhancing manufacturing capacity in the region.

- In September 2025, Kriya Therapeutics raised $320 million in Series D funding to advance its gene therapy pipeline and strengthen its manufacturing capabilities, reflecting strong investor confidence in scalable gene therapy platforms.

- In July 2025, AGC Biologics supported the European Commission approval of Autolus Therapeutics’ CAR-T therapy (AUCATZYL®), where its Milan facility was responsible for manufacturing the lentiviral vectors used in production, highlighting how late-stage gene therapy approvals depend on CDMO-supplied viral vectors.

- In June 2025, AGC Biologics expanded its cell and gene therapy development operations in Yokohama, Japan, strengthening its regional manufacturing footprint to support growing clinical demand.

- In June 2025, ProBio launched its 128,000 sq. ft. GMP viral vector and plasmid DNA manufacturing facility in New Jersey in June 2025, designed specifically to support increasing demand from expanding gene therapy pipelines.

- In April 2025, AGC Biologics launched a dedicated Cell and Gene Technologies Division to enhance its CDMO capabilities and support increasing demand from gene therapy developers across Europe.

- In December 2024, the U.S. FDA approved Autolus’ CAR-T therapy using lentiviral vectors manufactured by AGC Biologics, further reinforcing CDMOs’ role in commercial gene therapy supply chains.

- In November 2024, AGC Biologics supported the FDA approval of Autolus Therapeutics’ CAR-T gene therapy (AUCATZYL®), where its Milan facility manufactured the required lentiviral vectors, highlighting how late-stage gene therapy approvals depend on CDMO-produced viral vectors.

- In October 2024, AGC Biologics began operations at its new state-of-the-art manufacturing facility in Copenhagen, Denmark, strengthening its European production capacity following regulatory inspection and licensing.

- In May, 2024, Catalent entered a strategic partnership with Siren Biotechnology to support AAV-based immuno-gene therapy development and GMP manufacturing, strengthening its role in clinical-stage AAV vector supply for oncology programs.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Viral Vector Contract Development and Manufacturing Organization Market CAGR |

19.42% |

|

Key Companies in the Viral Vector Contract Development and Manufacturing Organization Market |

Lonza Group, Thermo Fisher Scientific, Catalent, Oxford Biomedica, Charles River Laboratories, FUJIFILM Diosynth Biotechnologies, WuXi AppTec, Merck KGaA, AGC Biologics, Takara Bio, Samsung Biologics, Curia Global, GenScript ProBio, Creative Biogene, VectorBuilder, Aldevron, FinVector, Yposkesi, VGXI, Genezen, SIRION Biotech, Exothera, VIVEbiotech, Novasep, BioVectra, Batavia Biosciences, Kaneka Eurogentec, Miltenyi Biotec, uniQure, RoslinCT, Cobra Biologics, MassBiologics, and others. |

|

Viral Vector Contract Development and Manufacturing Organization Market Segments |

by Vector Type, by Application, by Workflow Stage, by End-Users, and by Geography |

|

Viral Vector Contract Development and Manufacturing Organization Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Viral Vector Contract Development and Manufacturing Organization Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Viral Vector Contract Development and Manufacturing Organization Market Segmentation

- Viral Vector Contract Development and Manufacturing Organization by Vector Type Exposure

- Adeno-Associated Virus (AAV)

- Lentivirus

- Adenovirus

- Retrovirus

- Other

- Viral Vector Contract Development and Manufacturing Organization Application Exposure

- Gene Therapy

- Cell Therapy

- Vaccine Development

- Antisense & RNAi Therapy

- Others

- Viral Vector Contract Development and Manufacturing Organization Workflow Stage Exposure

- Upstream Processing

- Downstream Processing

- Viral Vector Contract Development and Manufacturing Organization End-Users Exposure

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Others

- Viral Vector Contract Development and Manufacturing Organization Geography Exposure

- North America Viral Vector Contract Development and Manufacturing Organization Market

- United States Viral Vector Contract Development and Manufacturing Organization Market

- Canada Viral Vector Contract Development and Manufacturing Organization Market

- Mexico Viral Vector Contract Development and Manufacturing Organization Market

- Europe Viral Vector Contract Development and Manufacturing Organization Market

- United Kingdom Viral Vector Contract Development and Manufacturing Organization Market

- Germany Viral Vector Contract Development and Manufacturing Organization Market

- France Viral Vector Contract Development and Manufacturing Organization Market

- Italy Viral Vector Contract Development and Manufacturing Organization Market

- Spain Viral Vector Contract Development and Manufacturing Organization Market

- Rest of Europe Viral Vector Contract Development and Manufacturing Organization Market

- Asia-Pacific Viral Vector Contract Development and Manufacturing Organization Market

- China Viral Vector Contract Development and Manufacturing Organization Market

- Japan Viral Vector Contract Development and Manufacturing Organization Market

- India Viral Vector Contract Development and Manufacturing Organization Market

- Australia Viral Vector Contract Development and Manufacturing Organization Market

- South Korea Viral Vector Contract Development and Manufacturing Organization Market

- Rest of Asia-Pacific Viral Vector Contract Development and Manufacturing Organization Market

- Rest of the World Viral Vector Contract Development and Manufacturing Organization Market

- South America Viral Vector Contract Development and Manufacturing Organization Market

- Middle East Viral Vector Contract Development and Manufacturing Organization Market

- Africa Viral Vector Contract Development and Manufacturing Organization Market

Viral Vector Contract Development and Manufacturing Organization Market Recent Industry Trends and Milestones (2023-2026)

|

Category |

Key Developments |

|

Viral Vector Contract Development and Manufacturing Organization Product Partnership |

Merck signed an MoU with Cyto-Facto to strengthen lentiviral vector production platforms and accelerate CDMO capabilities across APAC. Thermo Fisher Scientific partnered with South Korea-based Dr. Park CDMO to enable large-scale viral vector production using advanced bioprocessing technologies. |

|

Viral Vector Contract Development and Manufacturing Organization Product Launch |

ProBio launched its 128,000 sq. ft. GMP viral vector and plasmid DNA manufacturing facility in New Jersey, AGC Biologics launched a dedicated Cell and Gene Technologies Division to enhance its CDMO capabilities and support increasing demand from gene therapy developers across Europe. |

|

Viral Vector Contract Development and Manufacturing Organization Product Approval |

The FDA approved Otarmeni (lunsotogene parvec-cwha), the first dual AAV vector-based gene therapy for genetic hearing loss. The European Commission approved Autolus Therapeutics’ CAR-T therapy, AUCATZYL®, which relies on lentiviral vector manufacturing. |

|

Viral Vector Contract Development and Manufacturing Organization Product Collaboration |

eXmoor Pharma collaborated with Siam Bioscience in Thailand |

|

Company Strategy |

Lonza Group

Thermo Fisher Scientific

|

|

Emerging Technology |

Single-use bioreactor systems (SUBs), Suspension cell culture and stable producer cell lines, Digital biomanufacturing (AI, automation, and digital twins), Advanced upstream technologies (high-efficiency transfection & vector design), Innovative downstream purification technologies, Automation and closed-system manufacturing, Modular and flexible GMP facility design, and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are increasingly transforming the viral vector CDMO market by enhancing efficiency, scalability, and product quality across the manufacturing workflow. Artificial intelligence and machine learning are being used to optimize upstream processes such as cell culture conditions, transfection efficiency, and vector yield through predictive modeling and real-time data analysis. In downstream processing, AI helps improve purification strategies, including chromatography optimization and impurity removal, ensuring higher purity and consistency of viral vectors. Additionally, digital twin technology is enabling virtual simulation of manufacturing processes, allowing CDMOs to predict outcomes, reduce batch failures, and accelerate process development. AI is also being applied in quality control through advanced analytics for rapid detection of deviations and ensuring compliance with stringent regulatory standards. Furthermore, automation integrated with AI-driven monitoring systems supports closed and continuous manufacturing, reducing human error and operational costs. Overall, these AI-powered applications are enabling CDMOs to deliver faster, more cost-effective, and scalable viral vector production, strengthening their role in supporting the growing demand for gene and cell therapies.

U.S. Tariff Impact Analysis on Viral Vector Contract Development and Manufacturing Organization Market:

The U.S. tariff environment is having a mixed but increasingly important impact on the viral vector CDMO market, acting both as a challenge and a strategic reshaping force. On the negative side, tariffs on imported pharmaceutical products, raw materials, and critical inputs such as plasmids, reagents, and single-use bioprocessing components are raising manufacturing costs and disrupting global supply chains, which directly affects viral vector production economics. Since advanced therapies rely heavily on globally sourced, highly specialized inputs, tariffs increase procurement complexity, delay timelines, and inflate overall project costs for CDMOs and their clients.

At the same time, tariffs are driving a shift toward domestic manufacturing in the United States, which is creating growth opportunities for local CDMOs. Pharmaceutical and biotech companies are increasingly reshoring production or expanding U.S.-based facilities to avoid high import duties sometimes as high as 100% on certain patented drug imports announced in 2026. This trend is boosting demand for U.S.-based viral vector CDMOs, as outsourcing partners with domestic capacity become more attractive. Industry observations indicate that tariffs are encouraging companies to reduce dependence on global supply chains and increase outsourcing to domestic CDMOs, thereby expanding their market share.

Overall, while tariffs increase operational costs and supply chain risks in the short term, they are simultaneously accelerating local capacity expansion, strategic partnerships, and long-term demand for U.S.-based viral vector CDMO services, reshaping the competitive and geographic dynamics of the market.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Key Takeaways from the viral vector contract development and manufacturing organization market report study

- Market size analysis for the current viral vector contract development and manufacturing organization market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the viral vector contract development and manufacturing organization market.

- Various opportunities available for the other competitors in the viral vector contract development and manufacturing organization market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current viral vector contract development and manufacturing organization market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the viral vector contract development and manufacturing organization market growth in the future.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Vector BioMed |

$15 million |

Early-stage / Seed round |

Lentiviral vector manufacturing, vector design & GMP production |

Algorithm-optimized high-titer lentiviral vector production platforms. |