Developmental and Epileptic Encephalopathies Market Summary

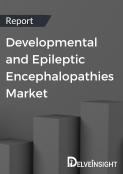

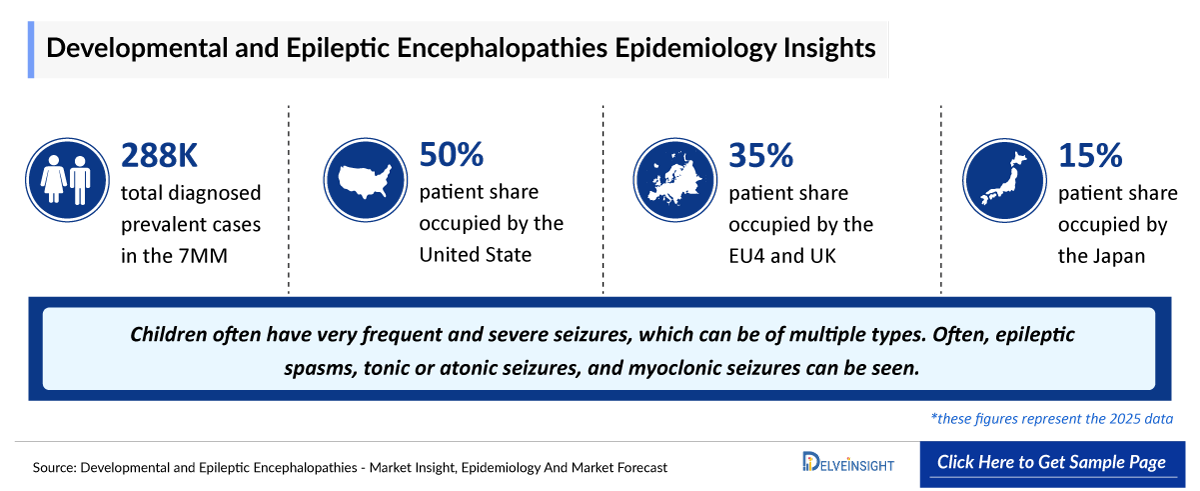

- The Developmental and Epileptic Encephalopathy market is projected to grow from approximately USD 2.23 billion in 2025 to nearly USD 7.18 billion by 2036, registering a CAGR of 11.7% during the forecast period from 2026 to 2036.

- The leading Developmental and Epileptic Encephalopathy companies developing therapies in the treatment market include - Marinus Pharmaceuticals, UCB, Jazz Pharmaceuticals, Novartis, Stoke Therapeutics and others.

Developmental and Epileptic Encephalopathy Market & Epidemiology Insights

- In 2025, the United States accounted for the maximum share of the total market in the 7MM, i.e., approximately 80%.

- The treatment paradigm for DEE has progressively evolved from symptomatic seizure management toward disease-modifying approaches aimed at improving long-term neurological, cognitive, and developmental outcomes.

- Over the past decade, significant progress has been made in expanding treatment options for DEE, with approvals of syndrome-specific therapies such as cannabidiol (EPIDIOLEX), fenfluramine (FINTEPLA), ganaxolone (ZTALMY), and everolimus (AFINITOR/VOTUBIA) for indications including Dravet syndrome, LGS, CDD, and TSC. Notably, everolimus represents a precision-based approach targeting the mTOR pathway in TSC, reflecting the broader transition toward mechanism-driven therapies in DEE.

- In parallel, fenfluramine continues to expand its clinical application beyond Dravet syndrome and Lennox Gastaut Syndrome, with ongoing evaluation in additional DEE indications such as CDD, reflecting a broader effort to extend its therapeutic utility across genetically defined epileptic encephalopathies.

- Currently approved therapies also associated with important safety and monitoring considerations. Fenfluramine includes a boxed warning for VHD and Pulmonary Arterial Hypertension, requiring structured REMS-based cardiac monitoring, while cannabidiol is associated with elevated liver enzyme risk necessitating routine hepatic function monitoring.

- Despite these advancements, the DEE landscape remains significantly underserved, with numerous genetically defined DEE subtypes continuing to lack approved targeted therapies, thereby representing substantial unmet clinical need.

- Consequently, the development landscape is increasingly prioritizing precision medicine approaches, including Antisense Oligonucleotides (ASOs), gene therapies, and mutation-specific therapies designed to directly target the underlying molecular and genetic drivers of disease progression.

- The DEE emerging pipeline includes zorevunersen (STK-001), EPX-100 (clemizole), relutrigine (PRAX-562), bexicaserin (LP352), carisbamate, elsunersen (PRAX-222), tricaprilin, rugonersen (RO7248824), obudanersen (ION582), apazunersen (GTX-102), and others, reflecting growing industry focus on rare and genetically defined epileptic encephalopathies.

- The DEE pipeline remains robust, with several companies actively advancing novel therapies for the treatment of DEE. Key players include Marinus Pharmaceuticals, UCB, Jazz Pharmaceuticals, Novartis, Stoke Therapeutics, Harmony Biosciences/Epygenix, Longboard Pharmaceuticals, Praxis Precision Medicines, Neurocrine Biosciences, Bright Minds Biosciences, Encoded Therapeutics, Ultragenyx Pharmaceutical, and others.

Developmental and Epileptic Encephalopathy Market size and forecast in the 7MM

- 2025 Developmental and Epileptic Encephalopathy Market Size: ~USD 2,230 million

- 2036 Projected Developmental and Epileptic Encephalopathy Market Size: ~USD 7,180 million

- Developmental and Epileptic Encephalopathy Growth Rate (2026–2036): 11.7% CAGR

DelveInsight's ‘Developmental and Epileptic Encephalopathy (DEE) Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of DEE, historical and forecasted epidemiology, as well as the DEE therapeutics market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The DEE market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates, DEE patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment, and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in DEE and maps the competitive and clinical landscape to uncover high-value opportunities, providing a clear outlook on future market growth potential.

Scope of the Developmental and Epileptic Encephalopathy Market Report | |

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

DEE Market CAGR (Forecast period) |

11.7% (2026–2036) |

|

DEE Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

DEE Companies |

|

|

DEE Therapies |

|

|

DEE Market |

Segmented by

|

|

Analysis |

|

Key Factors Driving the Alcohol Use Disorder Market

Increasing shift toward precision medicine and disease-modifying therapies in DEEs

The DEE pipeline is increasingly focused on precision medicine and disease-modifying approaches targeting underlying genetic drivers through modalities such as antisense oligonucleotides, gene therapies, and RNA-targeted treatments across syndromes including Dravet syndrome, Angelman syndrome, SCN2A-DEE, and CDD.

Strong pipeline innovation in rare DEE subtypes

Robust innovation across rare DEE subtypes is strengthening the development pipeline, with emerging therapies such as zorevunersen (STK-001), elsunersen, ETX101, and BMB-101 advancing targeted approaches including ASOs, gene therapies, and novel small molecules for disorders associated with SCN1A, SCN2A, and CDKL5 mutations.

Developmental and Epileptic Encephalopathy Disease Understanding

Developmental and Epileptic Encephalopathy Overview and Diagnosis

Developmental and Epileptic Encephalopathy (DEE) is a group of severe, often drug-resistant epilepsies characterized by frequent seizures and significant developmental delay or regression caused by underlying genetic or structural abnormalities, with abnormal brain activity further worsening outcomes; it includes syndromes such as Dravet, Lennox–Gastaut, CDKL5 deficiency, and SCN-related disorders. Diagnosis is based on clinical history, neurological examination, EEG, imaging (MRI/CT), and genetic or blood tests to confirm epilepsy type, identify the underlying cause, guide treatment selection, and assess associated developmental or behavioral impairments.

Further details are provided in the report...

Developmental and Epileptic Encephalopathy Treatment

The epilepsy syndromes at high risk are a group of conditions characterized by epileptic seizures that are difficult to treat and have developmental delays. The approach to the treatment of epileptic encephalopathy has some of the general principles and approaches to pediatric epilepsy treatment. The most appropriate anti-epileptic treatment is selected based on the type of epilepsy syndrome.

Anti-seizure medications are routinely used, but some types of seizures are usually difficult to control. It is the primary way in which epileptic seizures are controlled and is almost always the first class of therapy medications which include: Clobazam , Vigabatrin, Topiramate, Levetiracetam, Zonisamide, Phenobarbital, Cannabidiol, Stiripentol, Ethosuximide, Carbamazepine, Lamotrigine, Benzodiazapines, Clonazepam, Diazepam, Lorazepam, Nitrazepam, Phenobarbitone, Succinimides, Valproic acid, Rufinamide, and Felbamate.

Steroid therapy with Adrenocorticotropic hormone (ACTH) or prednisone has been helpful in some children. Steroids are often an effective treatment for the West’s syndrome. There have been few reports of steroid use in children with epilepsy outside the first year of life. Several studies suggest that the intravenous methylprednisolone pulse therapy regimen induces a statistically significant reduction of seizure frequency in children with epileptic encephalopathy.

Epilepsy surgery is carried out on the brain to treat epilepsy. This may involve removing a specific area of the brain that might have caused the epilepsy. There are different types of surgery, which are: Respective surgery, Disconnection surgery, and Laser Interstitial Thermal Therapy (LITT).

Further details related to country-based variations are provided in the report...

Developmental and Epileptic Encephalopathy Unmet Needs

The section “unmet needs of DEE” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Beyond Seizures: Neurodevelopmental and Comorbid Burdens

- Refractory Seizure Control and Treatment Limitations

- Quality of life and care complexity and others…..

Note: Comprehensive unmet needs insights in DEE and their strategic implications are provided in the full report...

Developmental and Epileptic Encephalopathy Epidemiology

The Developmental and Epileptic Encephalopathy epidemiology section provides insights about the historical and current Developmental and Epileptic Encephalopathy patient pool and forecasted trends for individual seven major countries. It helps to recognize the causes of current and forecasted trends by exploring numerous studies and views of key opinion leaders. This part of the Developmental and Epileptic Encephalopathy market report also provides the diagnosed patient pool and their trends along with assumptions undertaken.

Key Findings from DEE Epidemiological Analysis and Forecast

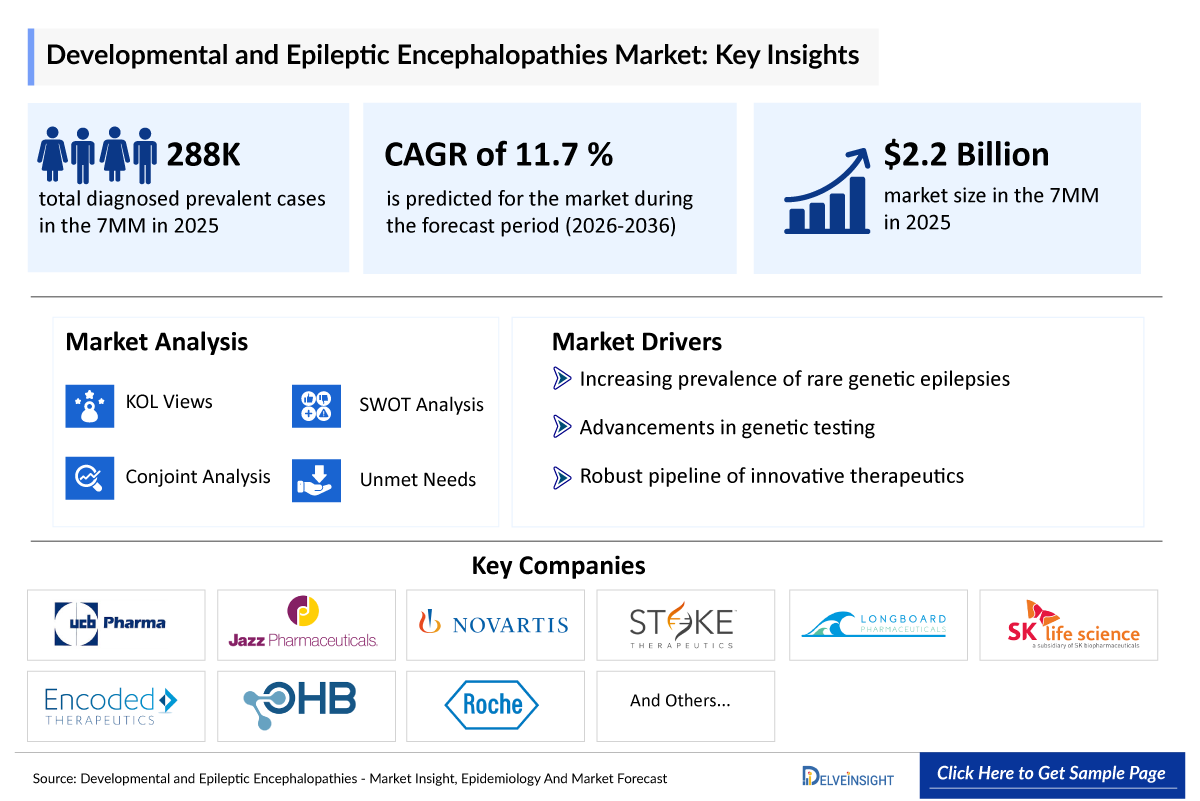

- In the 7MM, the total diagnosed prevalent population of DEE is expected to rise from ~287,800 (2025) to ~326,500 (2036).

- In the 7MM, the United States contributed to the largest diagnosed prevalent population of DEE, acquiring ~50% of the 7MM in 2025. The total diagnosed prevalent population of DEE in the United States is expected to rise from ~146,500 in 2025 to ~167,000 by 2036. Whereas, EU4 and the UK accounted for ~35% and Japan for ~15% of the total prevalent population, in 2025.

- In 2025, the total diagnosed prevalent cases of DEE in Japan were ~33,500, which is anticipated to increase by 2036.

- In 2025, the total diagnosed prevalent population of DEE in EU4 and the UK was ~107,500, which is projected to increase to ~121,000 by 2036. Germany accounted for the highest number of diagnosed prevalent cases of DEE, i.e.~35,000 cases, while Spain accounted for the least number of cases in 2025.

Developmental and Epileptic Encephalopathy Epidemiology Segmentation

- Total Diagnosed Prevalent Cases of DEE

- Diagnosed Prevalent Cases of DEE by Subtypes

- Total Treated Cases of DEE

Recent Developments in the Developmental and Epileptic Encephalopathy Treatment Landscape

- In April 2026, Jazz pharmaceuticals presented research on cannabidiol at the 2026 American Academy of Neurology Annual Meeting.

- In March 2026, Praxis Precision Medicines announced that the US FDA has accepted for Priority Review its NDA for relutrigine for the treatment of SCN2A and SCN8A DEEs. The FDA has set a target action date under the PDUFA of September 27, 2026.

- As per Praxis Precision Medicines’ 2026 Presentation, the company anticipates a pivotal readout from the EMBOLD study in SCN2A/SCN8A gain-of-function DEEs in the first half of 2026, followed by a subsequent pivotal readout from the EMERALD study to enable expansion into broader DEEs.

- In October 2025, UCB announced that the final analysis of an open-label extension study of fenfluramine in LGS was published in Epilepsy and Behavior. Treatment in patients aged 2–35 years resulted in sustained reductions in drop seizure frequency from Month 2 through study end, alongside improvements in global functioning as reported by caregivers and investigators. No new or unexpected treatment-emergent adverse events were observed. Caregivers also reported improvements in social functioning, quality of life, stigma, and anxiety. These findings were consistent with earlier OLE results in Dravet syndrome, which demonstrated sustained reductions in convulsive seizure frequency and favorable long-term tolerability.

Developmental and Epileptic Encephalopathy Drug Analysis & Competitive Landscape

The DEE drug chapter provides a detailed, market-focused review of approved therapies and the emerging pipeline across Phase I–III Developmental and Epileptic Encephalopathy clinical trials. It covers mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, strategic partnerships upcoming Key catalyst for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the DEE treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the DEE market.

Approved Therapies for Developmental and Epileptic Encephalopathy

Cannabidiol (EPIDIOLEX): Jazz Pharmaceuticals

Cannabidiol (EPIDIOLEX), also known as EPIDYOLEX in Europe, is the first prescription, plant-derived cannabis oral formulation developed by GW Pharmaceuticals. It is a novel class of antiepileptic medications with a different mechanism of action. The drug is the first FDA-approved drug that contains a purified drug substance derived from marijuana, and the active ingredient is cannabidiol (CBD). Under the Controlled Substances Act (CSA), CBD is classified as a Schedule I substance; thus, GW Pharmaceuticals conducted nonclinical and clinical studies to assess the abuse potential of CBD to support its usage. An ongoing Phase III trial in Japan evaluating the efficacy and safety of cannabidiol in patients with LGS, DS and TSC.

Fenfluramine (FINTEPLA): UCB

Fenfluramine is an oral medication that is a low-dose solution of fenfluramine hydrochloride. It prevents the entry of calcium ions into nerve cells, lowering their over-excitability and reducing seizure episodes. It also activates serotonin receptors, which contribute to the overall antiepileptic action. In the United States, Fenfluramine is available only through a restricted distribution program called the Fenfluramine REMS program. Fenfluramine is currently in Phase III development for CDKL5 deficiency disorder and has demonstrated positive Phase III results. Following these findings, the company plans to submit the data for regulatory approval to make this potential treatment available to patients with CDD.

Competitive Landscape of Developmental and Epileptic Encephalopathy Marketed Therapies | ||||||

|

Product |

Company |

Mechanism of Action |

Indication |

ROA |

Molecule Type |

Initial Approval |

|

ZTALMY (ganaxolone) |

Marinus Pharmaceuticals |

GABAA receptor modulator |

CDKL5 deficiency disorder |

Oral |

Recombinant fusion proteins |

US: 2022 EU: 2023 |

|

FINTEPLA (fenfluramine) |

UCB |

Serotonin 5HT-2 receptor agonist |

Dravet syndrome, LGS |

Oral |

Recombinant fusion proteins |

US: Dravet syndrome: 2020 LGS: 2022 EU: Dravet syndrome: 2020 JP LGS: 2023 Dravet syndrome: 2022 LGS: 2024 |

|

EPIDIOLEX (cannabidiol) |

Jazz Pharmaceuticals |

Enhancement of adenosine-mediated signaling |

LGS, Dravet syndrome, TSC |

Oral |

Recombinant fusion proteins |

US: LGS, Dravet syndrome: June 2018, TSC: July 2020 EU: LGS, Dravet syndrome: September 2019, TSC: April 2021 |

Developmental and Epileptic Encephalopathy Pipeline Analysis

Zorevunersen (STK-001): Stoke Therapeutics

Zorevunersen is an investigational new medicine for the treatment of Dravet syndrome. It is a proprietary antisense oligonucleotide (ASO) and has the potential to be the first disease-modifying therapy to address the genetic cause of Dravet syndrome. The drug is designed to upregulate NaV1.1 protein expression by leveraging the non-mutant copy of the SCN1A gene to restore physiological NaV1.1 levels, thereby reducing both occurrences of seizures and significant non-seizure comorbidities. This RNA-based approach is not gene therapy but rather RNA modulation, as it does not manipulate nor insert genetic deoxyribonucleic acid (DNA). STK-001 has been granted orphan drug designation by the FDA and the EMA and rare pediatric disease designation by the FDA as a potential new treatment for Dravet syndrome. The drug is currently being evaluated in Phase III clinical trial for Patient with Dravet syndrome.

Bexicaserin (LP352): Longboard Pharmaceuticals

Bexicaserin is an oral, centrally acting, 5-HT2c superagonist in development for the potential treatment of seizures associated with DEEs such as Dravet syndrome, LGS, tuberous sclerosis complex (TSC), CDKL5 deficiency disorder (CDD), and other epileptic disorders. LP352 is designed to modulate GABA and, as a result, suppress the central hyperexcitability that is characteristic of seizures. LP352 is the only 5-HT2c receptor superagonist being dose-optimized for the refractory epilepsy population. The drug is currently being evaluated in Phase III clinical trials

Competitive Landscape of Emerging Developmental and Epileptic Encephalopathy Therapies | ||||||

|

Product |

Company |

Highest Phase |

Indication |

Molecule Type |

RoA |

Anticipated Launch in the US |

|

Zorevunersen (STK-001) |

Stoke Therapeutics |

III |

Dravet syndrome |

ASO |

Intrathecal injection |

2028 |

|

Bexicaserin (LP352) |

Longboard Pharmaceuticals (acquired by Lundbeck) |

III |

DEEs (Dravet syndrome, LGS, TSC, CDD, and other epileptic disorders) |

Small molecule |

Oral |

Information is available in the full report |

|

Elsunersen (PRAX-222) |

Praxis Precision Medicines |

III |

Early onset SCN2A DEE |

ASO |

Intrathecal injection |

Information is available in the full report |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | ||||||

Developmental and Epileptic Encephalopathy Key Players, Market Leaders and Emerging Companies

- Marinus Pharmaceuticals

- UCB

- Jazz Pharmaceuticals

- Novartis

- Stoke Therapeutics and others

Developmental and Epileptic Encephalopathy Market Outlook

The current treatment landscape in DEE is largely driven by a limited number of indications with approved therapies, including LGS, Dravet Syndrome, TSC, and CDKL5 Deficiency Disorder. For these conditions, the US FDA has approved targeted therapies such as Ganaxolone, Fenfluramine, Cannabidiol, and Everolimus, which form the basis of disease-specific treatment approaches within this segment.

The primary treatment approach for DEE remains AEDs, which are typically initiated early in patients presenting with recurrent seizures. These therapies aim to control seizures by stabilizing neuronal activity and reducing excessive, abnormal electrical signaling in the brain. While AEDs can achieve seizure control in a significant proportion of general epilepsy cases (~70%), outcomes in DEEs are often more limited due to the highly refractory nature of these disorders. Treatment selection is individualized and depends on factors such as seizure type, underlying syndrome, patient age, comorbidities, potential drug–drug interactions, and tolerability. In clinical practice, therapy may involve monotherapy initially (e.g., valproate), but most DEE patients ultimately require combination regimens with multiple AEDs (e.g., valproate + clobazam) following recurrent or drug-resistant seizures.

- The total market size of DEE in the United States was around USD 1,750 million in 2025, which is projected to rise by 2036 driven by a robust and mechanistically diverse late-stage, high-cost ASO and gene therapies.

- In 2025, EPIDIOLEX/EPIDYOLEX achieved “blockbuster” status, generating approximately USD 1.1 billion in net sales, reflecting sustained commercial uptake across its approved indications and reinforcing its position as a key therapy within the DEE treatment landscape.

- Fenfluramine has emerged as the most differentiated marketed therapy within the DEE space, supported by strong efficacy in reducing convulsive and drop seizures across Dravet syndrome and LGS, broad global approvals including Japan, and growing physician confidence in its long-term clinical benefit.

- By 2036, zorevunersen is anticipated to lead the emerging DEE market in the 7MM, followed by bexicaserin and relutrigine.

Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in Developmental and Epileptic Encephalopathy (2022–2036 Forecast)

The DEE market comprises targeted small molecules, and Antisense oligonucleotides (ASOs), alongside conventional therapies, each addressing distinct immunologic pathways and mechanisms underlying DEE.

Small molecules and gene-based therapies: Emerging candidates such as relutrigene (a gene therapy approach) and bexicaserin (a next-generation serotonergic small molecule) are being developed specifically for DEE, moving beyond older, broad-spectrum anti-seizure drugs. Relutrigene aims to address the underlying genetic drivers of DEE by restoring or modifying gene function, offering potential disease-modifying benefits. In contrast, bexicaserin is designed to selectively target serotonin pathways implicated in seizure regulation, with the goal of improving efficacy while minimizing off-target effects.

Antisense oligonucleotides (ASOs): Antisense therapies are emerging as a targeted approach for DEE, designed to modulate gene expression at the RNA level and address the underlying genetic causes of disease. Candidates such as elsunersen and zorevunersen exemplify this strategy, aiming to correct aberrant splicing or regulate pathogenic gene activity associated with specific DEE subtypes. By directly targeting disease-causing mutations, these ASOs offer the potential for precision, disease-modifying treatment, moving beyond symptomatic seizure control toward addressing the root molecular pathology.

Further details will be provided in the report….

Developmental and Epileptic Encephalopathy Drug Uptake

This section focuses on the uptake rate of potential Developmental and Epileptic Encephalopathy drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the DEE drug’s uptake, performance at peak, factors affecting performance during prime years of growth, patient uptake by therapy, and anticipated sales generated by each drug.

The uptake of therapies in DEE is likely to vary depending on clinical positioning, mechanism of action, and maturity of clinical evidence. Emerging candidates for SCN8A/2A-DEE such as Relutrigine (PRAX-562) may achieve relatively faster uptake, particularly if supported by strong efficacy data and potential first-in-class positioning, while Elsunersen (PRAX-222) is expected to see moderate adoption as evidence and clinician confidence build over time

Detailed insights of emerging therapies' drug uptake is included in the report...

Developmental and Epileptic Encephalopathy Market Access and Reimbursement of Approved therapies

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of approved therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

The United States

US Reimbursement of Therapies Approved for DEE | |

|

Drug/Therapy |

Access Program |

|

EPIDIOLEX |

|

Reimbursement is a crucial factor that affects the drug’s access to the market. Often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

NOTE: Further Details are provided in the final report….

DEE therapies Price Scenario & Trends

Pricing and analogue assessment of DEE therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, closest and most approproiate analogue selection for emerging therapies, and understanding of how pricing influences market access, adherence, and long-term uptake.

Pricing of DEE Approved Drugs

The list price of EPIDIOLEX in 2022 was USD 1,420 per 100 ml bottle, corresponding to an average annual treatment cost of approximately USD 32,500.

Industry Experts and Physician Views for Developmental and Epileptic Encephalopathy

To keep up with DEE market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry Experts were contacted for insights on the DEE emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in DEE, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 10+ KOLs to gather insights at country level. Centers such as the University of California, Imperial College London, Hokkaido University, and Cholangiocarcinoma Foundation, etc. were contacted. Their opinion helps understand and validate current and emerging DEE therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in DEE.

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“Rare epilepsies, particularly those that constitute developmental and epileptic encephalopathy, are characterized by high etiological polymorphism, high clinical complexity and chronicity, thus leading to significant diagnostic difficulties and requiring the implementation of treatment and management based on a multi-professional approach, consolidated integration between hospital and territory and between services dedicated to pediatric age and those for adults.” |

|

Italy |

“Patients affected by drug-resistant epilepsies represent a challenge for the neurologist, not only for the diagnostic and therapeutic complexity, but also for the significant impact of drug resistance on the quality of life, among which the discrepancy of treatments from the neuro-pediatric field to the adult neurological field, the need for centers dedicated to the management of rare diseases and knowledge of them, in order to implement therapeutic strategies as early as possible.” |

Developmental and Epileptic Encephalopathy Report Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of DEE, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are majorly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided..

Scope of the Developmental and Epileptic Encephalopathy Market Report

- The report covers a segment of key events, an executive summary, a descriptive overview of DEE, explaining their causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the DEE market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM DEE market.

Developmental and Epileptic Encephalopathy Market Report Insights

- Developmental and Epileptic Encephalopathy Patient Population Forecast

- Developmental and Epileptic Encephalopathy Therapeutics Market Size

- Developmental and Epileptic Encephalopathy Pipeline Analysis

- Developmental and Epileptic Encephalopathy Market Size And Trends

- Developmental and Epileptic Encephalopathy Market Opportunity (current and forecasted)

Developmental and Epileptic Encephalopathy Market Report Key Strengths

- Epidemiology-based (Epi-based) bottom-up forecasting

- Artificial Intelligence (AI)-enabled market research report

- 11-year forecast

- Developmental and Epileptic Encephalopathy market outlook (North America, Europe, Asia-Pacific)

- Patient Burden trends (by geography)

- Developmental and Epileptic Encephalopathy Treatment addressable Market (TAM)

- Developmental and Epileptic Encephalopathy Competitve Landscape

- Developmental and Epileptic Encephalopathy major companies Insights

- Developmental and Epileptic Encephalopathy price trends and analogue assessment

- Developmental and Epileptic Encephalopathy therapies and Drug Adoption/Uptake

- Developmental and Epileptic Encephalopathy therapies Peak Patient Share Analysis

Developmental and Epileptic Encephalopathy Market Report Assessment

- Developmental and Epileptic Encephalopathy Current treatment practices

- Developmental and Epileptic Encephalopathy Unmet needs

- Developmental and Epileptic Encephalopathy Clinical development Analysis

- Developmental and Epileptic Encephalopathy Emerging drugs product profiles

- Developmental and Epileptic Encephalopathy Market attractiveness

- Developmental and Epileptic Encephalopathy Qualitative analysis (SWOT and conjoint analysis)

- Developmental and Epileptic Encephalopathy Market Drivers

- Developmental and Epileptic Encephalopathy Market Barriers

FAQs Related to the Developmental and Epileptic Encephalopathy Market Report:

Developmental and Epileptic Encephalopathy Market Insights

- What was the DEE market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of DEE?

- What are the disease risks, burdens, and unmet needs of DEE? What will be the growth opportunities across the 7MM concerning the DEE patient population?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of DEE? What are the current guidelines for treating DEE in the US, Europe, and Japan?

Reasons to Buy Developmental and Epileptic Encephalopathy Market Forecast Report

- The report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the DEE market.

- Bottom up forecasting builds from the affected population to product forecasts, delivering a robust, data driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI) enabled report summarize and simplify complex datasets withing the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data driven decisions.