Gastroesophageal Reflux Disease (GERD) Market Summary

Gastroesophageal Reflux Disease (GERD) Insights and Trends

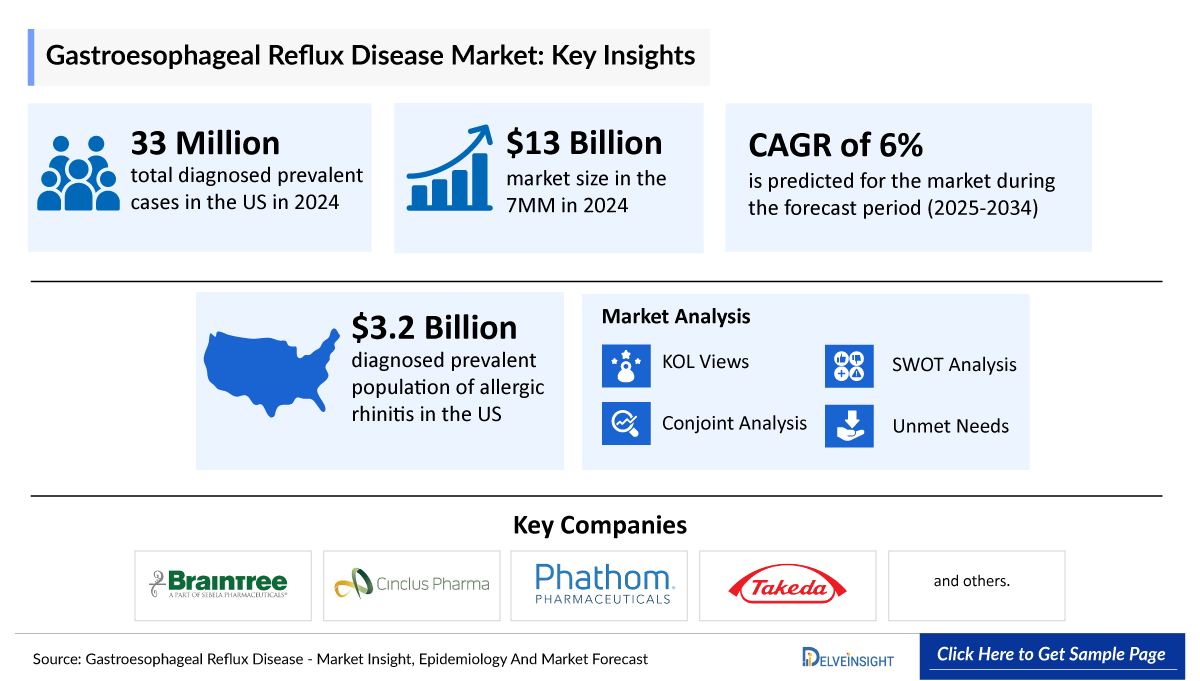

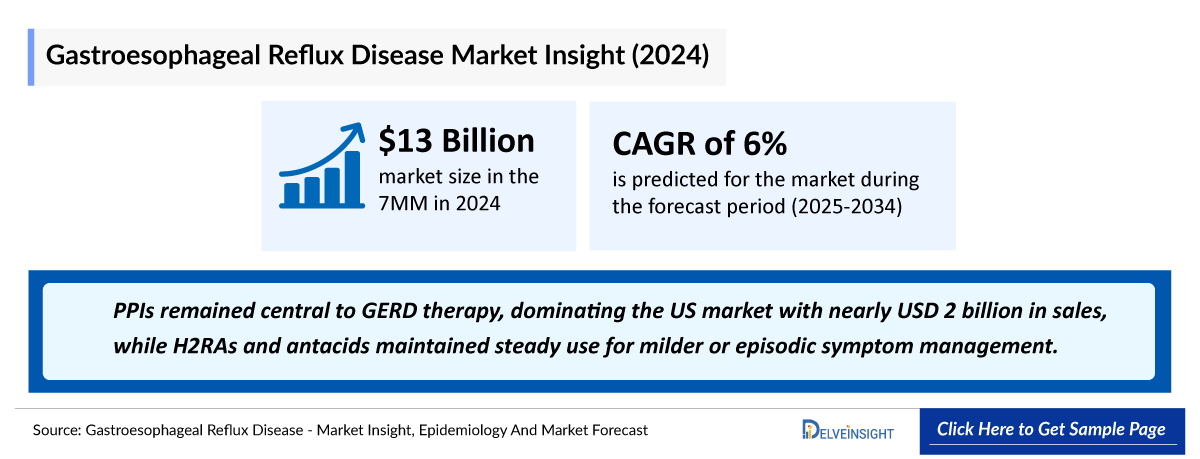

- According to DelveInsight’s analysis, the GERD market size was found to be ~USD 3,400 million in the United States, in 2025.

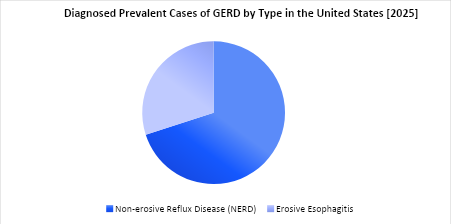

- Non-Erosive GERD is the largest subcategory of GERD and is characterized by reflux-related symptoms in the absence of esophageal mucosal erosions.

- Night time GERD symptoms are highly prevalent, affecting up to an estimated 80% of patients with GERD which can be associated with impaired sleep, reduced work productivity, and increased risk of esophageal and respiratory complications.

- The gold standard for diagnosing GERD is impedance-pH monitoring. This test is particularly valuable when endoscopy doesn't reveal esophagitis yet patients continue to experience refractory or recurrent symptoms or require invasive therapy.

- Vonoprazan (VOQUEZNA), the first and only branded Potassium-Competitive Acid Blocker (P-CAB) for GERD in the US, represents a major therapeutic advancement by delivering faster onset, more consistent 24-h acid control, and superior early healing in erosive disease compared with lansoprazole.

- Phathom Pharmaceuticals surpassed 1 million vonoprazan prescriptions dispensed in the US by Q4 2025, highlighting strong physician adoption and growing confidence in the P-CAB class for GERD management.

- The emerging GERD pipeline remains relatively limited but is supported by differentiated therapies, including tegoprazan (BLI5100) and ISOT-101, which aim to improve outcomes through novel mechanisms and enhanced symptom control.

- Despite the availability of PPIs and newer P-CAB therapies, a substantial proportion of patients continue to experience persistent symptoms, particularly those with non-erosive reflux disease (NERD) and PPI-refractory GERD, underscoring significant unmet clinical needs.

Gastroesophageal Reflux Disease (GERD) Market Size and Forecast in the United States

- 2025 GERD Market Size: ~USD 3,400 million

- 2036 Projected GERD Market Size: USD ~6,500 million

- GERD Growth Rate (2026–2036): 6.3% CAGR

DelveInsight's ‘Gastroesophageal Reflux Disease (GERD) Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of the GERD, historical and forecasted epidemiology, as well as the GERD market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The GERD market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates GERD patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment, and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in GERD and maps the competitive and clinical landscape to uncover high‑value opportunities, providing a clear outlook on future market growth potential.

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

Gastroesophageal Reflux Disease (GERD) US Market CAGR (Forecast period) |

~6.3% (2026–2036) |

|

Gastroesophageal Reflux Disease (GERD) Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

Gastroesophageal Reflux Disease (GERD) Companies |

|

|

Gastroesophageal Reflux Disease (GERD) Therapies |

|

|

Gastroesophageal Reflux Disease (GERD) Market |

Segmented by

|

|

Analysis |

|

Key Factors Driving the Gastroesophageal Reflux Disease (GERD) Market

- Rising Prevalence of GERD

Increasing rates of obesity, sedentary lifestyles, unhealthy dietary habits, and an aging population are contributing to a growing global burden of GERD, expanding the treatable patient pool.

- Adoption of Novel potassium-competitive acid blockers (P-CABs) Therapies

The introduction of P-CABs, particularly vonoprazan and emerging agents such as tegoprazan, is driving market growth by offering faster, more potent, and sustained acid suppression compared with conventional PPIs.

-

Persistent Unmet Need in PPI-Refractory Patients

A substantial proportion of patients continue to experience symptoms despite standard PPI therapy, creating demand for more effective and differentiated treatment options.

Gastroesophageal Reflux Disease (GERD) Understanding and Treatment Algorithm

Gastroesophageal Reflux Disease (GERD) Overview and Diagnosis

GERD is a chronic digestive disorder characterized by the reflux of stomach contents into the esophagus, resulting in troublesome symptoms and/or complications. The condition primarily occurs due to dysfunction of the lower esophageal sphincter, which normally prevents gastric contents from flowing back into the esophagus. Common symptoms include heartburn, acid regurgitation, chest discomfort, dysphagia, chronic cough, hoarseness, and sleep disturbances. GERD is one of the most prevalent gastrointestinal disorders worldwide and can significantly impair quality of life. If left untreated, chronic reflux may lead to complications such as erosive esophagitis, esophageal strictures, Barrett’s esophagus, and an increased risk of esophageal adenocarcinoma.

GERD is typically diagnosed based on clinical symptoms, particularly the presence of frequent heartburn and regurgitation. In patients with typical symptoms and no alarm features, an empirical trial of acid-suppressive therapy is often used to support the diagnosis. For individuals with persistent symptoms, atypical presentations, or suspected complications, diagnostic investigations may include upper gastrointestinal endoscopy to assess mucosal damage, ambulatory esophageal pH monitoring to quantify acid exposure, and esophageal impedance-pH testing to detect both acid and non-acid reflux. Esophageal manometry may also be performed to evaluate esophageal motility disorders and lower esophageal sphincter function.

Further details are provided in the report.

Current Gastroesophageal Reflux Disease (GERD) Treatment Landscape

The management of GERD involves a combination of lifestyle modifications and pharmacological therapy. Lifestyle interventions include weight reduction, dietary adjustments, smoking cessation, limiting alcohol intake, and elevating the head of the bed during sleep. Pharmacologic treatment is primarily centered on PPIs, such as omeprazole and esomeprazole, which remain the standard of care for symptom control and healing of erosive esophagitis. Histamine-2 receptor antagonists (H2RAs) may be used in selected patients with milder disease. More recently, P-CABs, such as vonoprazan, have emerged as effective alternatives offering rapid and sustained acid suppression.

Further details related to country-based variations are provided in the report.

Gastroesophageal Reflux Disease (GERD) Unmet Needs

The section “unmet needs of GERD” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Underdiagnosed and misdiagnosed because its symptoms resemble those of allergic and gastrointestinal conditions

- Incomplete symptom control with PPIs

- Limited long-term solutions for chronic disease management

- Limited options for PPI-refractory GERD, and others…..

Note: Comprehensive unmet needs insights in GERD and their strategic implications are provided in the full report.

Gastroesophageal Reflux Disease (GERD) Epidemiology

Key Findings from GERD Epidemiological Analysis and Forecast

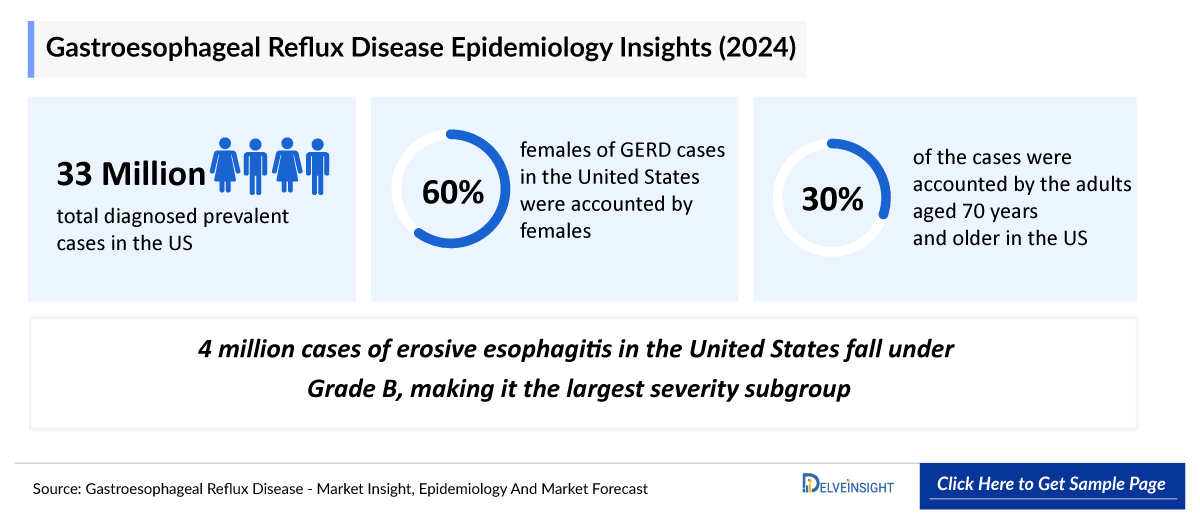

- GERD remains one of the most common chronic gastrointestinal disorders in the United States, with ~33,724,000 diagnosed prevalent cases in 2025.

- Among gender-specific cases of GERD, females (~60%) had highest number of cases than men in United States in 2025.

- In 2025, age group of more than 70 years had the highest (~30%) number of GERD cases followed by the age group of 60-69 (~22%), while the lowest number of cases were observed in age group less than 19 in United States.

- Among the EU4 and the UK, the UK had the highest prevalent cases of GERD in 2025 folllowed by Italy, while Spain accounted for the least number fo cases.

- Among individuals with erosive esophagitis, disease severity is similarly skewed toward the milder end of the spectrum: Grade B represents the single largest subgroup, followed by Grade A, while severe mucosal damage (Grade D) remains relatively uncommon. This distribution highlights a core challenge in GERD management—most patients present with symptom-driven, non-erosive disease or mild mucosal changes, yet still experience significant and often persistent symptom burden that may not align with endoscopic findings.

Gastroesophageal Reflux Disease (GERD) Drug Analysis & Competitive Landscape

The GERD drug chapter provides a detailed, market-focused review of the emerging pipeline across Phase II-III clinical trials and preclinical trials. It covers the mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, and strategic partnerships for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the GERD treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the GERD therapeutics market.

Approved Therapies for Gastroesophageal Reflux Disease (GERD)

Vonoprazan (VOQUEZNA): Phathom Pharmaceuticals and Takeda Pharmaceutical

Vonoprazan is a first-in-class P-CAB, a novel class of medicines that block acid secretion in the stomach. The therapy is approved in the US for the treatment of adults with Erosive Esophagitis, also known as Erosive GERD, the relief of heartburn associated with Erosive GERD, the relief of heartburn associated with Non-Erosive GERD. Phathom in-licensed the US rights to vonoprazan from Takeda, which markets the product in Japan and numerous other countries in Asia and Latin America. As per Phathom’s April 2026 corporate overview, VOQUEZNA reported ~USD 58 millions in revenue in Q1 2026.

Competitive Landscape of Gastroesophageal Reflux Disease (GERD) Marketed/Approved Therapies | ||||||

|

Drug/Therapy |

Company |

Indication |

Molecule Type |

MoA |

RoA |

Marketed Region |

|

Vonoprazan (VOQUEZNA) |

Phathom Pharmaceuticals and Takeda Pharmaceutical |

GERD |

Small molecule |

P-CAB |

Oral |

US: 2023 |

Note: Detailed marketed therapies assessment will be provided in the final report.

Gastroesophageal Reflux Disease (GERD) Pipeline Analysis

Tegoprazan (BLI5100): Braintree Laboratories (Sebela Pharmaceuticals)

Tegoprazan is a novel P-CAB being developed by Braintree, a part of Sebela Pharmaceuticals for the treatment of acid-related gastrointestinal diseases. The therapy has completed its Phase III clinical program in GERD, and a New Drug Application (NDA) was submitted to the FDA in January 2026, with approval anticipated in January 2027. Already approved in 21 countries, tegoprazan is positioned to address a significant multi-billion-dollar GERD market opportunity and is projected to have blockbuster potential, with peak US sales expected to exceed USD 1 billion.

ISOT-101: ISOThrive

ISOT-101 is a novel microbiome-based therapy for the treatment of GERD, particularly in patients with persistent symptoms despite proton pump inhibitor (PPI) therapy. The therapy consists of a proprietary digestion-resistant prebiotic carbohydrate, maltosyl-isomalto-oligosaccharides (MIMO), designed to selectively modulate the gastrointestinal and esophageal microbiome rather than suppress gastric acid production.

Competitive Landscape of Pipeline Drugs | ||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Anticipated Launch in the US |

|

Tegoprazan (BLI5100) |

Braintree Laboratories (Sebela Pharmaceuticals) |

III |

GERD |

Oral |

P-CAB |

Information is available in the full report |

|

ISOT-101 |

ISOThrive |

II |

GERD |

Oral |

Microbiome-based therapy |

Information is available in the full report |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | ||||||

Note: Detailed emerging therapies assessment will be provided in the final report.

Gastroesophageal Reflux Disease (GERD) Key Players, Market Leaders and Emerging Companies

- Phathom Pharmaceuticals

- Takeda Pharmaceutical

- Braintree Laboratories

- Sebela Pharmaceuticals

- ISOThrive, and others

Gastroesophageal Reflux Disease (GERD) Drug Updates

- In May 2026, Phathom Pharmaceuticals presented new GERD data from the Phase III pHalcon-NERD-301 study, at Digestive Disease Week (DDW) 2026, with one poster receiving DDW's poster of distinction recognition. The meeting also featured multiple investigator-initiated abstracts evaluating vonoprazan in GERD, further supporting its clinical utility and growing scientific interest in the P-CAB class for acid-related disorders.

- In May 2026, Braintree Laboratories announced that positive results from the Phase III TRIUMpH-EE clinical program evaluating tegoprazan were presented in two oral abstract sessions at DDW 2026.

- In October 2025, Phathom Pharmaceuticals announced that additional data from Phathom’s Phase III pHalcon-NERD-301 trial were recently published in the American Journal of Gastroenterology showing vonoprazan improved nocturnal GERD symptoms in patients with Non-Erosive Reflux Disease.

- In January 2026, Braintree Laboratories announced that it submitted a New Drug Application (NDA) to the US FDA for tegoprazan for the treatment of adults with GERD. The NDA submission is supported by robust data from the pivotal Phase III TRIUMpH clinical program.

- In August 2025, Braintree Laboratories announced positive topline results from the 24-week maintenance phase of the pivotal Phase III TRIUMpH clinical program evaluating tegoprazan in GERD.

- In June 2025, Phathom Pharmaceuticals announced that the US FDA had updated the Orange Book to accurately reflect the full 10-year period of non-patent New Chemical Entity (NCE) exclusivity for vonoprazan 10 mg and 20 mg tablets.

- In May 2025, Cinclus Pharma announced an agreement with Zentiva for the commercialization and manufacturing of linaprazan glurate in Europe.

Gastroesophageal Reflux Disease (GERD) Market Outlook

The GERD treatment landscape is evolving beyond traditional PPIs, with the emergence of P-CABs and microbiome-targeted therapies designed to provide faster symptom control, improved acid suppression, and enhanced patient outcomes.

Vonoprazan is expected to play a significant role in reshaping GERD management due to its potent and sustained acid suppression, rapid onset of action, and efficacy in both erosive and non-erosive forms of reflux disease. Its growing adoption in major markets is anticipated to drive increased use of P-CABs as an alternative to traditional PPIs, particularly among patients with persistent symptoms despite standard therapy.

Among emerging therapies, tegoprazan represents another promising P-CAB with the potential to expand therapeutic options in GERD. Clinical studies have demonstrated effective acid control and symptom improvement, supporting its potential use across a broad spectrum of reflux disease patients. ISOT-101 introduces a differentiated microbiome-based approach to GERD treatment by targeting gastrointestinal microbial balance rather than acid secretion alone. If ongoing clinical development demonstrates meaningful symptom improvement and durable benefits, ISOT-101 could emerge as a complementary therapy for patients inadequately controlled with acid-suppressive agents or those seeking non-acid-focused treatment strategies. This novel mechanism may help address persistent unmet needs in GERD management and support expansion into broader gastrointestinal disorders.

Collectively, these therapies have the potential to transform the GERD treatment paradigm by offering improved efficacy, faster symptom relief, and novel mechanisms of action. Their successful commercialization and clinical adoption are expected to drive market growth, intensify competition within the reflux disease space.

Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in GERD (2022–2036 Forecast)

The GERD market (2022–2036 forecast) consists of next-generation acid-suppressive agents and microbiome-focused therapies designed to provide faster symptom relief, improved healing rates, and more durable disease control..

- P-CABs: Vonoprazan and tegoprazan belong to the P-CAB class, which inhibits gastric H+/K+-ATPase through reversible potassium-competitive binding. Unlike PPIs, P-CABs provide rapid, potent, and sustained acid suppression without requiring acid activation.

- Microbiome-Based Therapies: ISOT-101 represents a novel microbiome-focused therapeutic approach aimed at restoring gastrointestinal microbial balance and improving digestive health. Rather than directly suppressing gastric acid secretion, microbiome-based therapies seek to address underlying gastrointestinal dysfunction that may contribute to persistent reflux symptoms.

For GERD, innovation is primarily being driven by next-generation P-CABs and microbiome-targeted therapies, which aim to overcome the limitations of conventional PPIs. P-CABs and microbiome-based candidates seek to address underlying disease mechanisms beyond gastric acid production.

Gastroesophageal Reflux Disease (GERD) Drug Uptake

This section focuses on the uptake rate of potential drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the GERD drug’s uptake, performance at peak, factors affecting performance during prime years of growth, patient uptake by therapy, and anticipated sales generated by each drug.

Since the approval of vonoprazan, GERD treatment landscape has begun shifting from traditional PPIs toward next-generation acid suppression therapies. Vonoprazan has established itself as a leading innovative treatment due to its rapid, potent, and sustained acid suppression, addressing several limitations of conventional PPIs. Uptake has been strong in the United States, with Phathom Pharmaceuticals surpassing one million prescriptions dispensed since launch by Q4 2025, reflecting growing physician confidence and patient adoption. In addition, confirmation of NCE exclusivity through May 2032 strengthens the product’s long-term commercial outlook. As awareness of the P-CAB class increases, vonoprazan is expected to continue gaining share, particularly among patients with erosive esophagitis and inadequate response to PPIs.

Among emerging therapies, tegoprazan is expected to be a key competitor within the P-CAB class, offering rapid symptom relief and effective healing of erosive esophagitis. Its potential approval in major western markets could intensify competition with vonoprazan and further drive the shift away from traditional PPIs, particularly among patients with inadequate symptom control. Meanwhile, ISOT-101 represents a differentiated, microbiome-based approach that targets underlying dysbiosis and inflammation rather than gastric acid secretion. If clinical development is successful, it could address unmet needs in patients with NERD and PPI-refractory GERD.

The uptake is expected to be driven by therapies that provide faster symptom control, more durable acid suppression, improved convenience, and novel mechanisms addressing disease pathways beyond gastric acid production.

Detailed insights of emerging therapies' drug uptake is included in the report

Market Access and Reimbursement of Approved therapies in Gastroesophageal Reflux Disease (GERD)

Reimbursement is a crucial factor that affects the drug’s access to the market. Often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

The United States

US Reimbursement of Therapies Approved for Gastroesophageal Reflux Disease (GERD) | |

|

Drug/Therapy |

Access Program |

|

VOQUEZNA |

VOQUEZNA Savings Program |

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of approved therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

NOTE: Further Details are provided in the final report….

Gastroesophageal Reflux Disease (GERD) Therapies Price Scenario & Trends

Pricing and analogue assessment of GERD therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, closest and most appropriate analogue selection for emerging therapies, and understanding of how pricing influences market access, adherence, and long-term uptake.

Industry Experts and Physician Views for Gastroesophageal Reflux Disease (GERD)

To keep up with GERD market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry experts were contacted for insights on the GERD emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in GERD, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 15+ KOLs to gather insights at the country level. Centers such as Johns Hopkins University School of Medicine, Cedars-Sinai Medical Center, and UniversityHospital Heidelberg etc. were contacted. Their opinion helps understand and validate current and emerging GERD therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in GERD.

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“Approximately 40–50% of GERD patients continue to experience symptoms despite daily use of the standard-of-care PPIs, which are designed to suppress stomach acid. Concerningly, long-term studies indicate that PPIs fail to prevent the progression of reflux-related diseases and malignancies.” |

|

Germany |

“GERD is oftentimes dismissed and treated medically even with patients who have a paraesophageal hernia who should really have an operation.” |

Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of GERD, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are majorly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Report

- The report covers a segment of key events, an executive summary, a descriptive overview of GERD, explaining their causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the GERD market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM GERD market.

Report Insights

- Gastroesophageal Reflux Disease (GERD) Patient Population Forecast

- Gastroesophageal Reflux Disease (GERD) Therapeutics Market Size

- Gastroesophageal Reflux Disease (GERD) Pipeline Analysis

- Gastroesophageal Reflux Disease (GERD) Market Size and Trends

- Gastroesophageal Reflux Disease (GERD) Market Opportunity (Current and Forecasted)

Report Key Strengths

- Epidemiology‑based (Epi‑based) Bottom‑up Forecasting

- Artificial Intelligence (AI)-Enabled Market Research Report

- 11-Year Forecast

- Gastroesophageal Reflux Disease (GERD) Market Outlook (North America, Europe, Asia-Pacific)

- Patient Burden Trends (By Geography)

- Gastroesophageal Reflux Disease (GERD) Treatment Addressable Market (TAM)

- Gastroesophageal Reflux Disease (GERD) Competitve Landscape

- Gastroesophageal Reflux Disease (GERD)) Major Companies Insights

- Gastroesophageal Reflux Disease (GERD) Price Trends and Analogue Assessment

- Gastroesophageal Reflux Disease (GERD) Therapies Drug Adoption/Uptake

- Gastroesophageal Reflux Disease (GERD) Therapies Peak Patient Share Analysis

Report Assessment

- Gastroesophageal Reflux Disease (GERD) Current Treatment Practices

- Gastroesophageal Reflux Disease (GERD) Unmet Needs

- Gastroesophageal Reflux Disease (GERD) Clinical Development Analysis

- Gastroesophageal Reflux Disease (GERD) Emerging Drugs Product Profiles

- Gastroesophageal Reflux Disease (GERD) Market attractiveness

- Gastroesophageal Reflux Disease (GERD) Qualitative Analysis (SWOT and Conjoint Analysis)

FAQs

Market Insights

- What was the GERD market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of GERD?

- What are the disease risks, burdens, and unmet needs of GERD? What will be the growth opportunities across the 7MM concerning the patient population with GERD?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of GERD? What are the current guidelines for treating GERD in the US, Europe, and Japan?

Reasons to Buy

- The report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the GERD market.

- Bottom-up forecasting builds from the affected population to product forecasts, delivering a robust, data-driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI)-enabled report summarize and simplify complex datasets with in the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data-driven decisions.

-pipeline.png&w=256&q=75)