Sterile Bioprocess Filtration Market Summary

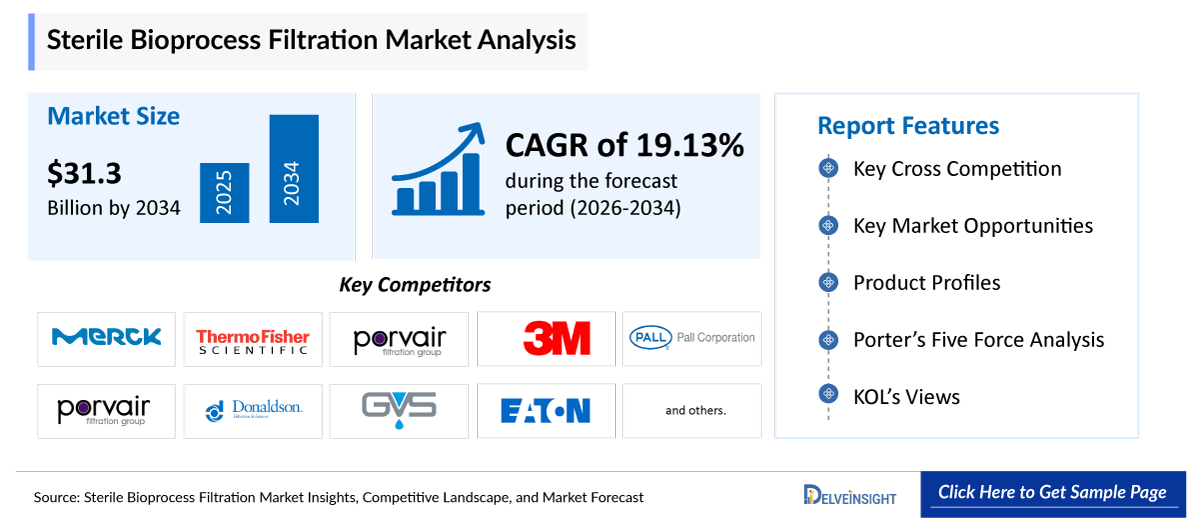

- The global sterile bioprocess filtration market size is expected to increase from USD 6,509.84 million in 2025 to USD 31,337.98 million by 2034, reflecting strong and sustained growth.

- The global sterile bioprocess filtration market is growing at a CAGR of 19.13% during the forecast period from 2026 to 2034.

- The sterile bioprocess filtration market is being strongly driven by the combined impact of rising biopharmaceutical demand, vaccine production expansion, growing outsourcing to CMOs/CDMOs, and continuous advancements in filtration technologies. The increasing development of biologics such as monoclonal antibodies, recombinant proteins, and cell and gene therapies requires highly efficient and contamination-free processing, where sterile filtration is essential. At the same time, global vaccine manufacturing capacity is expanding rapidly, further increasing the need for reliable sterile filtration systems for media preparation, downstream purification, and final fill-finish operations. In parallel, pharmaceutical companies are outsourcing production to CMOs and CDMOs to improve scalability and reduce costs, which is boosting demand for flexible and standardized filtration solutions across multiple facilities. Additionally, innovations in membrane materials such as high-performance PES and virus-retentive filters are improving filtration efficiency, product yield, and process safety. Together, these factors are significantly accelerating the adoption and growth of sterile bioprocess filtration technologies across the biopharmaceutical industry.

- The leading companies operating in the sterile bioprocess filtration market include Merck KGaA, Sartorius AG, Cytiva, Pall Corporation, Thermo Fisher Scientific Inc., 3M Company, Meissner Filtration Products, Porvair Filtration Group, Donaldson Company, Inc., GVS Group, Eaton Corporation plc, Parker Hannifin Corporation, Saint-Gobain Life Sciences™, Amazon Filters Ltd., Cobetter Filtration, Repligen Corporation, GEA Group AG, Alfa Laval AB, Koch Separation Solutions, GE Healthcare, and others.

- North America is expected to dominate the Sterile Bioprocess Filtration market due to its strong and well-established biopharmaceutical industry, particularly in the United States. The region hosts a high concentration of leading biologics and vaccine manufacturers, along with advanced R&D infrastructure and early adoption of single-use and high-efficiency filtration technologies. Supportive regulatory frameworks from agencies like the FDA further encourage innovation and ensure stringent quality standards in bioprocessing. Additionally, significant investments in biologics, cell and gene therapies, and continuous biomanufacturing are driving demand for sterile filtration solutions. The presence of major global players and continuous technological advancements also reinforces North America’s leading position in this market.

- In the product type segment of the sterile bioprocess filtration market, the membrane filters category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Sterile Bioprocess Filtration Market Insights

Sterile Bioprocess Filtration Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 6,509.84 million |

|

2034 Projected Market Size |

USD 31,337.98 million |

|

Growth Rate (2026-2034) |

19.13% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Sterile Bioprocess Filtration Market

- Rising demand for biopharmaceuticals leading to a surge in Sterile Bioprocess Filtration: The rising demand for biopharmaceuticals is significantly boosting the sterile bioprocess filtration market as it increases the need for highly efficient and contamination-free production processes. Biologics such as monoclonal antibodies, vaccines, and cell and gene therapies require strict sterility throughout manufacturing, making advanced filtration systems essential for removing microbes, particulates, and impurities. As global healthcare demand grows and more biologic drugs enter development pipelines, manufacturers are expanding production capacity, which in turn drives greater adoption of sterile filtration technologies to ensure product safety, regulatory compliance, and consistent quality.

- Expansion of vaccine production: The expansion of vaccine production is boosting the sterile bioprocess filtration market by increasing the need for highly controlled and contamination-free manufacturing environments. Large-scale vaccine development, especially for mRNA, viral vector, and recombinant vaccines, requires multiple filtration steps to ensure sterility, purity, and safety of the final product. Growing global immunization programs and preparedness for emerging infectious diseases are driving the rapid scale-up of vaccine manufacturing facilities. This, in turn, is accelerating the adoption of advanced sterile filtration systems that support high-volume, reliable, and regulatory-compliant vaccine production.

- Increasing biomanufacturing outsourcing to CMOs and CDMOs: The increasing biomanufacturing outsourcing to CMOs and CDMOs is boosting the sterile bioprocess filtration market by driving higher demand for flexible, scalable, and single-use filtration systems. As pharmaceutical and biotech companies outsource production to reduce costs and accelerate time-to-market, CMOs/CDMOs are expanding their manufacturing capacities and investing in advanced sterile filtration technologies to meet diverse client requirements. These facilities often handle multiple biologics and production batches, making contamination control and process efficiency critical. As a result, the need for reliable sterile filtration solutions that ensure product safety, regulatory compliance, and operational flexibility is significantly increasing.

- Technological advancements in filtration materials: Technological advancements in filtration materials are boosting the sterile bioprocess filtration market by improving efficiency, safety, and process reliability in biologics manufacturing. Innovations such as high-performance membranes, advanced polymer materials, and nanofiber-based filters enhance contaminant removal while maintaining high flow rates and product recovery. These improved materials also offer greater chemical compatibility, scalability, and durability, making them suitable for complex biopharmaceutical processes. As a result, manufacturers are increasingly adopting next-generation filtration solutions to meet strict regulatory standards and support the growing demand for high-quality sterile biologics production.

Sterile Bioprocess Filtration Market Report Segmentation

This sterile bioprocess filtration market report offers a comprehensive overview of the global sterile bioprocess filtration market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Products Type (Membrane Filters, Depth Filters, Cartridge Filters, and Others), Workflow (Upstream Processing, Downstream Processing, and Aseptic Filling/Fill-Finish Fermentation), MaterialType (Polyethersulfone (PES), Polyvinylidene Fluoride (PVDF), Polytetrafluoroethylene (PTFE), and Nylon), Application (Biologics Manufacturing, Vaccine Production, Cell & Gene Therapy Manufacturing, and Others), End-Users (Biopharmaceutical & Biotechnology Companies, Contract Manufacturing Organizations (CMOs), Contract Research Organizations (CROs), and Others), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing sterile bioprocess filtration market.

Sterile bioprocess filtration is a critical step in biopharmaceutical manufacturing that involves removing microorganisms, particulates, and other contaminants from biological fluids to ensure sterility and product safety. It is widely used in the production of biologics such as vaccines, monoclonal antibodies, and gene therapies. This process typically uses specialized membrane filters to maintain product integrity while achieving high levels of purity, helping manufacturers meet strict regulatory requirements and ensure safe final drug products.

The sterile bioprocess filtration market is being strongly driven by the combined impact of rising biopharmaceutical demand, vaccine production expansion, growing outsourcing to CMOs/CDMOs, and continuous advancements in filtration technologies. The increasing development of biologics such as monoclonal antibodies, recombinant proteins, and cell and gene therapies requires highly controlled, contamination-free manufacturing environments, where sterile filtration plays a crucial role in ensuring product safety, purity, and regulatory compliance. As these therapies become more widely adopted, production volumes are scaling up, further intensifying the need for reliable and high-performance filtration systems across upstream and downstream processes.

At the same time, global vaccine manufacturing capacity is expanding rapidly, supported by both routine immunization programs and preparedness for emerging infectious diseases. This has significantly increased the use of sterile filtration in critical stages such as media and buffer preparation, bioreactor feed streams, and final fill-finish operations to maintain sterility and consistency at large scale. In parallel, pharmaceutical and biotechnology companies are increasingly outsourcing manufacturing activities to CMOs and CDMOs to reduce capital investment, enhance flexibility, and accelerate time-to-market. These service providers often manage multiple products and clients simultaneously, which further drives demand for standardized, scalable, and single-use compatible filtration solutions.

Additionally, continuous innovations in filtration materials and membrane technologies, such as advanced polyethersulfone (PES) membranes, high-flux filters, and virus-retentive systems, are improving filtration efficiency, throughput, and product recovery while minimizing fouling and process variability. These advancements not only enhance operational efficiency but also strengthen compliance with stringent global regulatory standards. Collectively, these factors are significantly accelerating the adoption and growth of sterile bioprocess filtration technologies across the expanding biopharmaceutical manufacturing landscape.

Get More Insights into the Report @ Sterile Bioprocess Filtration Market Trends

What are the latest sterile bioprocess filtration market dynamics and trends?

The sterile bioprocess filtration market is experiencing strong and sustained growth as the rising demand for biopharmaceuticals, expansion of vaccine production, and increasing outsourcing to CMOs/CDMOs collectively intensify the need for reliable, high-performance filtration systems that ensure sterility, product safety, and regulatory compliance across complex manufacturing workflows. The surge in biologics such as monoclonal antibodies, recombinant proteins, and advanced cell and gene therapies is driving large-scale adoption of sterile filtration in both upstream and downstream processing. In parallel, global vaccine production capacity has expanded significantly following increased immunization programs and pandemic preparedness, further strengthening demand for high-efficiency membranes and single-use filtration technologies. Additionally, the growing reliance on CMOs and CDMOs, as reflected in their rapidly expanding market share in biologics manufacturing, has accelerated the need for flexible, scalable, and multi-product compatible filtration solutions, as these facilities handle diverse client pipelines and must maintain strict sterility standards. Supporting this growth, recent industry developments highlight continuous consolidation and capacity expansion. For instance, in February 2025, Thermo Fisher Scientific announced a ~$4.1 billion acquisition of Solventum’s purification and filtration business, significantly strengthening its bioprocess filtration portfolio and expanding its capabilities in high-growth biologics manufacturing markets.

Similarly, in July 2024, Sartorius expanded its bioprocess filtration portfolio with modular single-use assemblies optimized for mRNA vaccine manufacturing, supporting rapid scale-up and regulatory compliance for vaccine producers.

Thus, the factors mentioned above are expected to boost the overall market of sterile bioprocess filtration during the forecast period.

However, high operational and consumable costs, along with frequent filter clogging and fouling issues, act as significant limiting factors for the sterile bioprocess filtration market by increasing both production expenses and process inefficiencies. The high cost of advanced membrane filters and their frequent replacement, especially in single-use systems, raises overall manufacturing costs for biopharmaceutical companies. At the same time, fouling caused by complex biological fluids reduces filtration efficiency, leads to downtime, and requires additional maintenance or filter changes, disrupting continuous production. Together, these challenges reduce process productivity, increase operational complexity, and can limit adoption in cost-sensitive manufacturing environments.

Sterile Bioprocess Filtration Market Segment Analysis

Sterile Bioprocess Filtration Market by Products Type (Membrane Filters, Depth Filters, Cartridge Filters, and Others), Workflow (Upstream Processing, Downstream Processing, and Aseptic Filling/Fill-Finish Fermentation), MaterialType (Polyethersulfone (PES), Polyvinylidene Fluoride (PVDF), Polytetrafluoroethylene (PTFE), and Nylon), Application (Biologics Manufacturing, Vaccine Production, Cell & Gene Therapy Manufacturing, and Others), End-Users (Biopharmaceutical & Biotechnology Companies, Contract Manufacturing Organizations (CMOs), Contract Research Organizations (CROs), and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product Type: Membrane filters in sterile bioprocess filtration are expected to dominate the market with the largest revenue share.

In the product type segment of the sterile bioprocess filtration market, the membrane filters category is contributing to 33.6% of total market revenue in 2025, due to their essential role in ensuring sterility, high filtration efficiency, and broad applicability across biopharmaceutical manufacturing. These filters are widely used for removing bacteria, particulates, and other contaminants from biologics such as monoclonal antibodies, vaccines, recombinant proteins, and cell and gene therapy products, making them indispensable in both upstream and downstream processing. For example, Merck KGaA (MilliporeSigma) offers its Durapore® and Millipore Express® PES membrane filters, which are extensively used in monoclonal antibody purification and vaccine production due to their high flow rates and low protein-binding characteristics. Similarly, Cytiva (Danaher) provides Whatman™ and Supor™ membrane filters, widely adopted in viral vector and recombinant protein manufacturing, while Sartorius AG supplies Sartopore® PES membrane filters, which are commonly used in sterile final filtration and bioreactor feed applications in large-scale biologics production. Pall Corporation (Danaher) also plays a key role with its Pall Fluorodyne® and Supor® membrane technologies, which are extensively used in cell culture media filtration and sterile filling processes, particularly in vaccine manufacturing.

Additionally, the technological advancements in membrane materials such as polyethersulfone (PES), polyvinylidene fluoride (PVDF), and mixed cellulose ester (MCE) have further enhanced performance by improving flow rates, reducing fouling, and increasing protein recovery efficiency. Additionally, the growing adoption of single-use systems in biomanufacturing, especially among CMOs and CDMOs handling multiple biologics simultaneously, is accelerating demand for these membrane filters due to their disposability, ease of integration, and reduced risk of cross-contamination. Collectively, these factors reinforce membrane filters as a dominant and high-growth segment within the sterile bioprocess filtration market.

By Workflow: Upstream processing category dominates the market

Within the workflow segment of the sterile bioprocess filtration market, the upstream category is anticipated to dominate, accounting for around 35% of the market share in 2025, due to its critical role in the earliest and most contamination-sensitive stages of biopharmaceutical manufacturing, such as cell culture, media preparation, inoculum development, and bioreactor feed preparation. Since any contamination introduced at this stage can compromise entire production batches, upstream processes require highly reliable sterile filtration systems to ensure optimal sterility, nutrient purity, and consistent cell growth performance. The increasing global production of biologics, including monoclonal antibodies, recombinant proteins, and advanced therapies, has significantly amplified filtration demand in upstream operations, especially with the widespread adoption of single-use bioreactors and high-density cell culture systems. Industry reports also confirm that the upstream segment held the largest share in 2024, driven by its extensive use in media and buffer filtration and its high sensitivity to contamination risks in early-stage processing workflows. Furthermore, upstream bioprocessing remains the foundation of biologics manufacturing, involving initial cell expansion and culture steps that determine overall product yield and quality, which further reinforces its dominance in filtration demand. Recent developments also support this trend, for example, in January 2023, Sartorius AG partnered with RoosterBio to develop integrated downstream and upstream purification solutions for exosome-based therapies, highlighting growing investment in advanced sterile processing platforms. Additionally, the continued expansion of biologics manufacturing capacity and rising investments in vaccine production facilities have led to increased adoption of high-performance sterile filters in upstream workflows to support large-scale, contamination-free production. Collectively, these factors make upstream filtration the most dominant and strategically important segment within the sterile bioprocess filtration market.

By Material Type: Polyethersulfone (PES) category dominates the market

Within the material type segment of the sterile bioprocess filtration market, the Polyethersulfone (PES) category is anticipated to dominate, accounting for around 36.2% of the market share in 2025, due to its superior performance characteristics, high compatibility with biologics, and widespread adoption across both upstream and downstream processing. PES membranes are highly preferred because they are hydrophilic, exhibit low protein binding, and provide high flow rates and throughput, making them ideal for filtering sensitive biological products such as monoclonal antibodies, vaccines, recombinant proteins, and cell & gene therapies. Their ability to efficiently remove microorganisms and particulates while maintaining product integrity significantly enhances yield and process efficiency. For instance, Sartorius AG offers Sartopore® and Sartopore Evo® PES membrane filters, which are widely used for sterilizing-grade filtration in final fill-finish operations due to their low adsorption and high throughput performance, helping reduce product loss and improve productivity. Similarly, Sartopore® Platinum PES filters are designed with modified membranes that provide excellent wettability and extremely low protein adsorption, maximizing product recovery in high-value biologics manufacturing. In prefiltration applications, Sartoguard PES filters use asymmetric double-layer PES membranes to achieve high bioburden reduction and protect downstream filtration systems, improving overall process efficiency and reducing costs. Beyond Sartorius, companies such as Merck KGaA (MilliporeSigma), Pall Corporation, and Cytiva also offer PES-based membrane filters (e.g., Millipore Express®, Supor® membranes) that are extensively used in sterile filtration of cell culture media, buffers, and drug substances. The dominance of PES is further reinforced by its excellent chemical and thermal stability, gamma sterilization compatibility, and scalability across single-use systems, which are increasingly adopted by CMOs/CDMOs. Additionally, compared to alternative materials like PVDF, PES membranes often deliver higher flow rates and reduced fouling, enabling faster processing and lower operational costs. Collectively, these advantages, combined with strong product portfolios from leading manufacturers and growing demand for high-efficiency biologics production, position PES as the leading material segment driving the sterile bioprocess filtration market.

By Application: The biologics manufacturing category dominates the market.

Within the application segment of the sterile bioprocess filtration market, the biologics manufacturing category is anticipated to dominate, accounting for around 43% of the market share in 2025, due to the rapidly increasing demand for complex biological drugs and the stringent sterility requirements associated with their production. Biologics such as monoclonal antibodies, recombinant proteins, vaccines, and cell and gene therapies require highly controlled manufacturing environments, where sterile filtration is essential at multiple stages, including media preparation, cell culture, purification, and final fill-finish. The growing global pipeline of biologic drugs and the rising number of regulatory approvals are significantly increasing production volumes, thereby driving higher adoption of sterile filtration systems to ensure product safety, purity, and compliance with strict regulatory standards. Additionally, biologics manufacturing processes are more sensitive to contamination compared to small-molecule drugs, making advanced filtration technologies indispensable. The increasing shift toward single-use systems and continuous bioprocessing, along with expanding manufacturing capacities by pharmaceutical companies and CMOs/CDMOs, is further strengthening the demand for efficient and scalable sterile filtration solutions. As a result, the biologics manufacturing segment continues to lead the market, supported by ongoing innovation, high investment in biopharmaceutical production, and the critical need for contamination control throughout the production lifecycle.

By End-Users: The biopharmaceutical & biotechnology companies category dominates the market.

In the end-users segment of the sterile bioprocess filtration market, the biopharmaceutical & biotechnology companies category dominates due to their extensive involvement in the development and large-scale production of biologics such as monoclonal antibodies, vaccines, and cell and gene therapies. These companies require highly efficient sterile filtration systems across multiple stages of manufacturing to ensure product safety, purity, and compliance with stringent regulatory standards. Additionally, their continuous investment in R&D, expansion of biologics pipelines, and adoption of advanced bioprocessing technologies such as single-use systems and continuous manufacturing further drive the demand for sterile filtration solutions, solidifying their leading position in the market.

Sterile Bioprocess Filtration Market Regional Analysis

North America Sterile Bioprocess Filtration Market Trends

North America is expected to account for the highest proportion of 36.45% of the Sterile Bioprocess Filtration market in 2025, out of all regions. North America is expected to dominate the sterile bioprocess filtration market due to its highly advanced biopharmaceutical ecosystem, strong presence of leading industry players, robust regulatory framework, and continuous investments in biologics manufacturing and innovation. The region, particularly the United States, is supported by extensive R&D activities, early adoption of single-use and high-efficiency filtration technologies, and a high volume of biologics and biosimilars approvals.

Additionally, the presence of major companies such as Thermo Fisher Scientific, Danaher (Cytiva and Pall), and Merck Millipore further strengthens the region’s leadership through continuous innovation and large-scale manufacturing capabilities. Furthermore, strict regulatory standards imposed by agencies like the FDA ensure high adoption of sterile filtration systems to maintain product quality and compliance, while the growing focus on personalized medicine, cell and gene therapies, and mRNA-based products continues to accelerate demand for advanced filtration solutions.

Recent developments in North America further reinforce this dominance. More recently, in April 2026, Thermo Fisher opened an expanded bioprocessing facility in Plainville, Massachusetts, designed to provide advanced upstream and downstream processing support, including filtration solutions, for biopharmaceutical manufacturers.

Additionally, as pharmaceutical and biotechnology companies in the U.S. and Canada increasingly rely on outsourcing to reduce capital expenditure, accelerate drug development timelines, and manage complex biologics pipelines, CMOs/CDMOs are rapidly expanding their upstream and downstream manufacturing capacities. This expansion directly increases the consumption of sterile filtration products, especially membrane filters, single-use assemblies, and virus-retentive systems, since outsourced facilities must maintain strict sterility standards while handling multiple products simultaneously. For instance, in April 2025, Sartorius Stedim Biotech partnered with Tulip Interfaces to launch the Biobrain Operate digital platform, which integrates with single-use bioprocessing systems to optimize upstream operations, reduce variability, and improve process control in biologics manufacturing environments.

Thus, the factors mentioned above are expected to boost the overall North America market of sterile bioprocess filteration across the region during the forecast period.

Europe Sterile Bioprocess Filtration Market Trends

The sterile bioprocess filtration market in Europe is witnessing strong and sustained growth due to the region’s well-established biopharmaceutical industry, stringent regulatory framework, and increasing focus on high-quality, contamination-free drug manufacturing. Countries such as Germany, the UK, and France are leading this growth, supported by robust R&D infrastructure, expanding biologics pipelines, and rising production of biosimilars, vaccines, and advanced therapies such as cell and gene therapies. The European market is also benefiting from strict regulatory standards imposed by agencies such as the European Medicines Agency (EMA), which require high sterility assurance levels, thereby increasing the adoption of advanced membrane filtration and single-use technologies.

Additionally, the increasing presence of CMOs/CDMOs and the shift toward flexible manufacturing are further accelerating demand for sterile filtration solutions across upstream and downstream workflows. Recent developments in Europe further highlight this strong growth trajectory. For example, in June, 2025, Sartorius AG expanded its bioprocessing manufacturing and R&D facility in Illkirch, France, strengthening its capacity to support sterile filtration and upstream bioprocessing solutions across the region.

Thus, the factors mentioned above are expected to boost the overall market of sterile bioprocess filtration in Europe during the forecast period.

Asia-Pacific Sterile Bioprocess Filtration Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the sterile bioprocess filtration market due to its rapidly expanding biopharmaceutical manufacturing base, increasing government support, and growing demand for cost-effective biologics production. Countries such as China, India, South Korea, and Japan are investing heavily in biomanufacturing infrastructure, supported by rising healthcare expenditure, favorable regulatory reforms, and strong demand for vaccines, biosimilars, and advanced therapies. The region is also benefiting from lower production costs and a rapidly expanding network of CMOs/CDMOs, which is attracting global pharmaceutical companies to establish manufacturing hubs in APAC.

As a result, the adoption of sterile filtration technologies, especially membrane filters and single-use filtration systems, is increasing significantly across upstream and downstream processes to ensure contamination-free production. According to recent industry insights, the Asia Pacific is the fastest-growing market for pharmaceutical and bioprocess filtration, driven by the expansion of biologics manufacturing, increasing R&D activities, and strong government initiatives supporting life sciences infrastructure. Additionally, the region’s growing role as a global vaccine supplier and the rising number of biologics approvals further amplify the need for high-performance sterile filtration systems in large-scale production environments.

Recent developments in the region further reinforce this growth trajectory. For instance, in March 2024, Merck KGaA expanded its M Lab™ Collaboration Center in Shanghai, China, adding a new upstream application lab and training facility to support bioprocess development and single-use filtration adoption in Asia.

Thus, the factors mentioned above are expected to boost the overall market of sterile bioprocess filtration across the Asia-Pacific region during the forecast period.

Who are the major players in the sterile bioprocess filtration market?

The following are the leading companies in the sterile bioprocess filtration market. These companies collectively hold the largest market share and dictate industry trends.

- Merck KGaA

- Sartorius AG

- Cytiva

- Pall Corporation

- Thermo Fisher Scientific Inc.

- 3M Company

- Meissner Filtration Products

- Porvair Filtration Group

- Donaldson Company, Inc.

- GVS Group

- Eaton Corporation plc

- Parker Hannifin Corporation

- Saint-Gobain Life Sciences™

- Amazon Filters Ltd.

- Cobetter Filtration

- Repligen Corporation

- GEA Group AG

- Alfa Laval AB

- Koch Separation Solutions

- GE Healthcare, and others

How is the competitive landscape shaping the sterile bioprocess filtration market?

The competitive landscape of the sterile bioprocess filtration market is highly dynamic and moderately consolidated, characterized by the strong presence of global leaders alongside emerging and niche players, all competing through innovation, strategic partnerships, and capacity expansion. Major companies such as Merck KGaA, Danaher Corporation, Sartorius AG, Thermo Fisher Scientific, and 3M dominate the market due to their extensive product portfolios, strong global distribution networks, and continuous investments in advanced membrane and single-use filtration technologies. These players are actively focusing on mergers and acquisitions, product launches, and technological advancements to strengthen their market position and expand capabilities. For example, the industry has seen ongoing M&A activity and collaborations aimed at enhancing filtration technologies and expanding bioprocessing solutions portfolios. At the same time, emerging companies such as Repligen Corporation, Meissner Filtration Products, and Asahi Kasei Corporation are gaining traction by offering specialized, high-performance, and customizable filtration systems tailored to advanced biologics and cell & gene therapy applications. The market is also witnessing intense competition driven by rapid innovation, including next-generation membrane materials, nanofiber filters, and smart/automated filtration systems integrated with digital monitoring technologies. Additionally, stringent regulatory requirements and the growing demand for high-purity biologics are pushing companies to invest heavily in R&D and quality compliance, further intensifying competition. Overall, the competitive landscape is shaped by a combination of technological innovation, strategic consolidation, and increasing focus on scalable, single-use, and high-efficiency filtration solutions, making it both highly competitive and innovation-driven.

Recent Developmental Activities in the Sterile Bioprocess Filtration Market

- In April 2026, Thermo Fisher opened an expanded bioprocessing facility in Plainville, Massachusetts, designed to provide advanced upstream and downstream processing support, including filtration solutions, for biopharmaceutical manufacturers.

- In April 2025, Sartorius Stedim Biotech partnered with Tulip Interfaces to launch the Biobrain Operate digital platform, which integrates with single-use bioprocessing systems to optimize upstream operations, reduce variability, and improve process control in biologics manufacturing environments.

- In June 2025, Sartorius AG expanded its bioprocessing manufacturing and R&D facility in Illkirch, France, strengthening its capacity to support sterile filtration and upstream bioprocessing solutions across the region.

- In February 2025, Thermo Fisher Scientific announced a ~$4.1 billion acquisition of Solventum’s purification and filtration business, significantly strengthening its bioprocess filtration portfolio and expanding its capabilities in high-growth biologics manufacturing markets.

- In July 2024, Sartorius expanded its bioprocess filtration portfolio with modular single-use assemblies optimized for mRNA vaccine manufacturing, supporting rapid scale-up and regulatory compliance for vaccine producers.

- In March 2024, Merck KGaA expanded its M Lab™ Collaboration Center in Shanghai, China, adding a new upstream application lab and training facility to support bioprocess development and single-use filtration adoption in Asia.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Sterile Bioprocess Filtration Market CAGR |

19.13% |

|

Key Companies in the Sterile Bioprocess Filtration Market |

Merck KGaA, Sartorius AG, Cytiva, Pall Corporation, Thermo Fisher Scientific Inc., 3M Company, Meissner Filtration Products, Porvair Filtration Group, Donaldson Company, Inc., GVS Group, Eaton Corporation plc, Parker Hannifin Corporation, Saint-Gobain Life Sciences™, Amazon Filters Ltd., Cobetter Filtration, Repligen Corporation, GEA Group AG, Alfa Laval AB, Koch Separation Solutions, GE Healthcare, and others. |

|

Sterile Bioprocess Filtration Market Segments |

by Product Type, by Workflow, by Material Type, by Application, by End-Users, and by Geography |

|

Sterile Bioprocess Filtration Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Sterile Bioprocess Filtration Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Sterile Bioprocess Filtration Market Segmentation

- Sterile Bioprocess Filtration Product Type Exposure

- Sterile Bioprocess Filtration Cell Type Exposure

- Mammalian

- Bacterial

- Others

- Sterile Bioprocess Filtration by Workflow Exposure

- Upstream Processing

- Downstream Processing

- Aseptic Filling / Fill-Finish

- Fermentation

- Sterile Bioprocess Filtration Material Type Exposure

- Polyethersulfone (PES)

- Polyvinylidene Fluoride (PVDF)

- Polytetrafluoroethylene (PTFE)

- Nylon

- Sterile Bioprocess Filtration Application Exposure

- Biologics Manufacturing

- Vaccine Production

- Cell & gene Therapy Manufacturing

- Others

- Sterile Bioprocess Filtration End-Users Exposure

- Biopharmaceutical & Biotechnology Companies

- Contract Manufacturing Organizations (CMOs)

- Contract Research Organizations (CROs)

- Others

Sterile Bioprocess Filtration Geography Exposure

- North America Sterile Bioprocess Filtration Market

- United States Sterile Bioprocess Filtration Market

- Canada Sterile Bioprocess Filtration Market

- Mexico Sterile Bioprocess Filtration Market

- Europe Sterile Bioprocess Filtration Market

- United Kingdom Sterile Bioprocess Filtration Market

- Germany Sterile Bioprocess Filtration Market

- France Sterile Bioprocess Filtration Market

- Italy Sterile Bioprocess Filtration Market

- Spain Sterile Bioprocess Filtration Market

- Rest of Europe Sterile Bioprocess Filtration Market

- Asia-Pacific Sterile Bioprocess Filtration Market

- China Sterile Bioprocess Filtration Market

- Japan Sterile Bioprocess Filtration Market

- India Sterile Bioprocess Filtration Market

- Australia Sterile Bioprocess Filtration Market

- South Korea Sterile Bioprocess Filtration Market

- Rest of Asia-Pacific Sterile Bioprocess Filtration Market

- Rest of the World Sterile Bioprocess Filtration Market

- South America Sterile Bioprocess Filtration Market

- Middle East Sterile Bioprocess Filtration Market

- Africa Sterile Bioprocess Filtration Market

Sterile Bioprocess Filtration Market Recent Industry Trends and Milestones (2023-2026):

|

Category |

Key Developments |

|

Sterile Bioprocess Filtration Product Partnership |

Sartorius Stedim Biotech partnered with Tulip Interfaces |

|

Sterile Bioprocess Filtration Product Expansion |

Thermo Fisher opened an expanded bioprocessing facility in Plainville, Massachusetts, designed to provide advanced upstream and downstream processing support. Sartorius AG expanded its bioprocessing manufacturing and R&D facility in Illkirch, France, strengthening its capacity to support sterile filtration and upstream bioprocessing solutions. |

|

Company Strategy |

Merck KGaA · Focuses on an end-to-end integrated bioprocessing platform, combining filtration, chromatography, and digital analytics. · Invests heavily in low protein-binding membranes and advanced filtration materials to improve product yield. · Expands globally through capacity expansion and partnerships with biopharma and CDMOs.

Sartorius AG

· Offers end-to-end solutions from lab to commercial scale, strengthening customer retention. |

|

Emerging Technology |

Single-use (disposable) filtration systems, Advanced membrane materials (next-generation membranes), Nanofiber and nano-structured filtration technologies, Nanofiber and nano-structured filtration technologies, and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are increasingly transforming sterile bioprocess filtration by enabling smarter, more efficient, and highly controlled filtration operations across biopharmaceutical manufacturing. Advanced machine learning (ML) and artificial intelligence (AI) algorithms are now being used to analyze large volumes of process data, such as pressure, flow rate, and membrane performance, to optimize filtration parameters in real time, improving throughput and reducing failures. For instance, AI models can predict membrane fouling, pressure drops, and filter lifespan, allowing operators to take proactive actions and minimize downtime during critical filtration steps. Additionally, AI-driven systems support process optimization and adaptive control, where algorithms continuously adjust operating conditions (e.g., transmembrane pressure and flux rates) to maintain optimal filtration efficiency and product quality.

Another key innovation is the use of digital twins and soft sensors, which create virtual replicas of bioprocess systems and enable real-time monitoring and predictive control of filtration processes, improving consistency and reducing variability. AI is also being integrated with automated filtration platforms and IoT-enabled sensors, enabling continuous monitoring, anomaly detection, and predictive maintenance to reduce human intervention and operational risks. In downstream processing, AI helps optimize filtration and clarification steps by modeling fouling behavior and improving filter sizing and selection, ensuring higher yield and reduced product loss. Furthermore, AI-powered analytics link upstream conditions with downstream filtration performance, enabling end-to-end process optimization and quality prediction.

U.S. Tariff Impact Analysis on Sterile Bioprocess Filtration Market:

The U.S. tariff impact on the sterile bioprocess filtration market is creating a mix of short-term cost challenges and long-term growth opportunities. On one hand, increased tariffs on pharmaceutical imports, raw materials, and related components are raising overall manufacturing costs, which can put pressure on biopharmaceutical companies and limit immediate spending on filtration systems and consumables. These cost increases may also lead to supply chain disruptions, delays, and pricing volatility, especially for companies that rely on globally sourced filtration materials. On the other hand, tariffs are encouraging the reshoring and localization of biomanufacturing in the United States, as companies aim to reduce dependency on imports and avoid additional duties. This shift is driving investments in domestic production facilities, which in turn is increasing demand for sterile bioprocess filtration technologies used across upstream, downstream, and fill-finish processes. As a result, while tariffs may create near-term constraints, they are also supporting long-term market growth by strengthening local manufacturing infrastructure and boosting demand for advanced filtration solutions.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends:

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Cytiva |

~$1.5 billion |

- |

Xcellerex stirred-tank Sterile Bioprocess Filtration (50 L–2000 L+) |

Integrated single-use bioprocessing, digital automation, and AI-enabled monitoring |

Key takeaways from the Sterile Bioprocess Filtration market report study

- Market size analysis for the current sterile bioprocess filtration market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the sterile bioprocess filtration market.

- Various opportunities available for the other competitors in the sterile bioprocess filtration market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current sterile bioprocess filtration market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the sterile bioprocess filtration market growth in the future.