T-cell Malignancies Market Summary

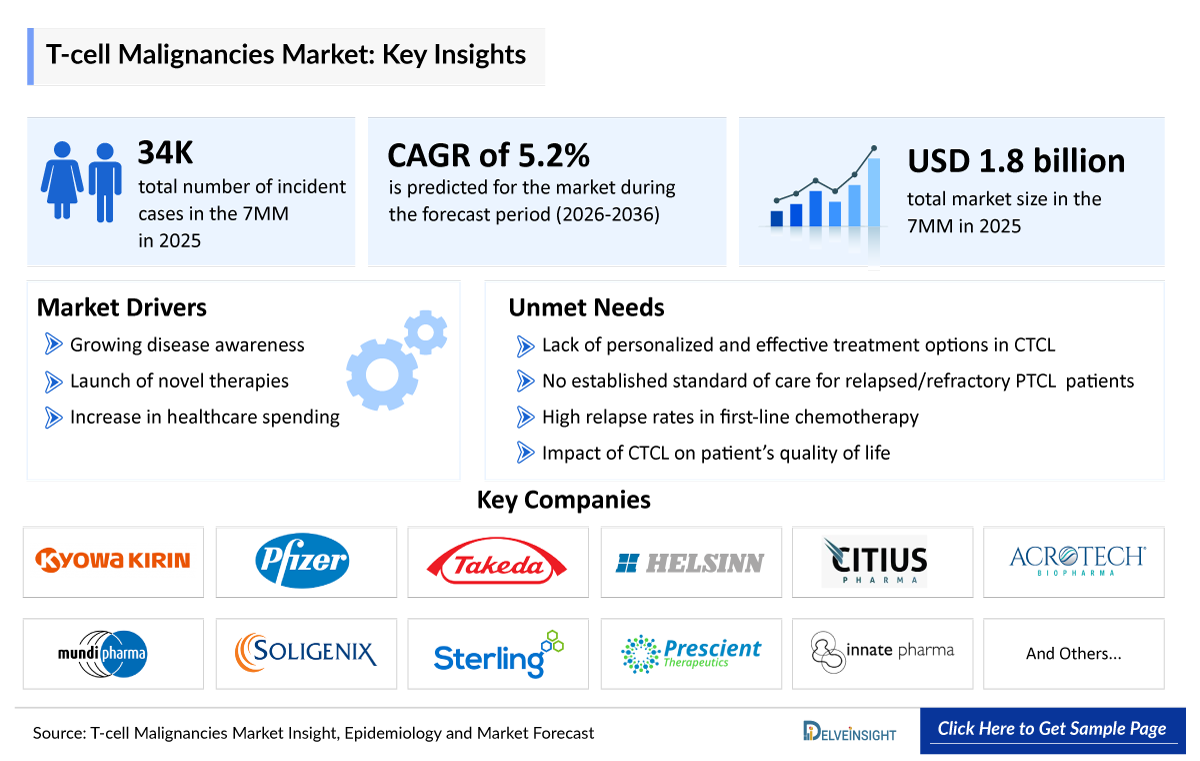

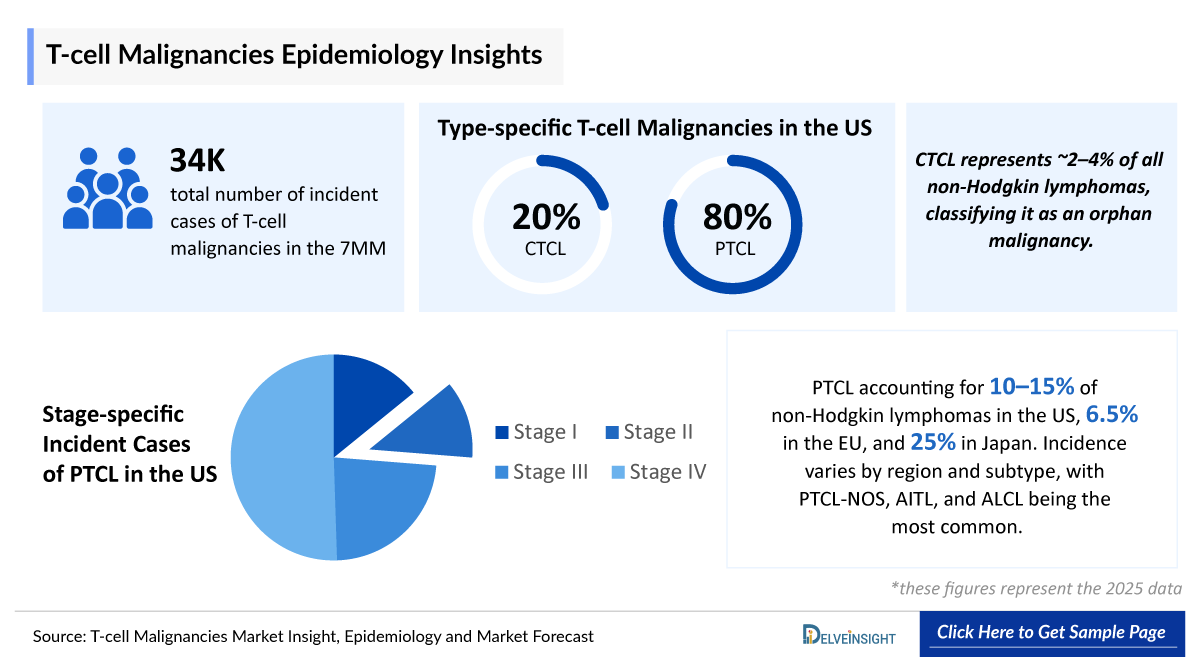

- The T-cell Malignancies market size was valued at approximately USD 1.8 billion in 2025 and is projected to reach nearly USD 3.17 billion by 2036, expanding at a CAGR of 5.2% during the forecast period from 2026 to 2036.

- The leading T-cell Malignancies companies developing therapies in the treatment market include - Kyowa Hakko Kirin, Pfizer (Seagen), Takeda, Helsinn Therapeutics, Citius Pharmaceuticals, HUYA Bioscience International (HUYABIO), Acrotech Biopharma, Mundipharma, Soligenix, Sterling Pharma Solutions, Prescient Therapeutics, Innate Pharma, and others.

T-cell Malignancies Market & Epidemiology Insights

- According to DelveInsight’s analysis, T-cell Malignancies market size was found to be ~USD 1,800 million in the leading markets (the United States, the EU4 (Germany, France, Italy, and Spain), the United Kingdom, and Japan) in 2025.

- T-cell malignancies, encompassing Peripheral T-cell Lymphomas (PTCL) and cutaneous subtypes such as Cutaneous T-cell lymphoma (CTCL), represent a clinically heterogeneous and aggressive group of cancers with generally poorer outcomes than B-cell malignancies.

- In CTCL, about 60% of patients are diagnosed at early Stages (IA/IB), which are typically indolent with near-normal life expectancy. However, ~30% may progress to advanced-stage disease, significantly worsening prognosis.

- PTCL accounting for 10–15% of non-Hodgkin lymphomas in the US, 6.5% in EU and 25% in Japan. Incidence varies by region and subtype, with PTCL-NOS, AITL, and ALCL being the most common. Patients face poor prognosis, high relapse rates, and limited durable treatment options, contributing to significant clinical and quality-of-life burden.

- CHOP remains the standard first-line therapy for PTCL, yet substantial unmet need persists for patients who cannot tolerate cytotoxic chemotherapy. ADCETRIS is the only approved first-line agent, reflecting limited therapeutic progress, while CHOP-based combination strategies have largely failed due to increased toxicity and lack of biologically guided approaches.

- Currently, mechlorethamine (VALCHLOR), bexarotene (TARGRETIN), brentuximab vedotin (ADCETRIS), mogamulizumab (POTELIGEO), denileukin diftitox-cxdl (LYMPHIR), and others are approved therapies available for the treatment of CTCL, offering valuable options for both patients and healthcare providers in managing the disease.

- The approved PTCL treatment landscape is led by agents such as brentuximab vedotin (ADCETRIS; Takeda) in CD30-positive disease, romidepsin (ISTODAX; Bristol Myers Squibb), belinostat (BELEODAQ; Acrotech BioPharma), mogamulizumab (POTELIGEO; Kyowa Kirin), crizotinib (XALKORI; Pfizer), and valemetostat tosilate (EZHARMIA; Daiichi Sankyo) in select subtypes, all of which provide modest, subtype-restricted benefit.

- The lack of reliable, disease-specific biomarkers in Cutaneous T-cell lymphoma leads to delayed and uncertain diagnosis, reliance on repeated biopsies, and suboptimal treatment decisions, highlighting a critical need for biomarkers that enable early detection, accurate differentiation, and more durable, personalized therapy selection.

T-cell Malignancies Market Size and Forecast in the 7MM

- 2025 T-cell Malignancies Market Size: ~USD 1,800 million

- 2036 Projected T-cell Malignancies Market Size: ~USD 3,170 million

- T-cell Malignancies Growth Rate (2026–2036): 5.2% CAGR

Request a sample to unlock the CAGR for "T-cell Malignancies Market Forecast"

Key Factors Driving the T-cell Malignancies Market

- Rising T-cell Malignancies Incidence: The increasing incidence of T-cell malignancies, particularly among older adults, is a key driver of market expansion. In the US, approximately 15,500 incident cases of T-cell malignancis were reported in 2025, with incidence expected to further increase over the forecast period, driven by an aging population and improved diagnosis through better molecular classification and diagnostic tools.

- Rising Opportunities in GGT1-Targeted Therapies: Emerging evidence of PTX-100’s superior efficacy and safety over LYMPHIR highlights a growing opportunity for drug developers to focus on therapies targeting GGT1 inhibition.

- Robust and diversified pipeline (next-gen & multi-target approaches): The pipeline is rapidly evolving toward dual-target, multi-antigen, and next-generation therapies, designed to overcome relapse, antigen escape, and durability limitations. These innovations are expected to significantly expand efficacy across heterogeneous tumors and improve long-term outcomes.

DelveInsight's ‘T-cell Malignancies Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of the T-cell Malignancies, historical and forecasted epidemiology, as well as the T-cell Malignancies therapeutics market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The T-cell malignancies market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates, T-cell malignancies patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment, and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in T-cell malignancies and maps the competitive and clinical landscape to uncover high-value opportunities, providing a clear outlook on future market growth potential.

Scope of the T-cell Malignancies Market Report | |

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

T-cell Malignancies Market CAGR (Forecast period) |

5.2% (2026–2036) |

|

T-cell Malignancies Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

T-cell Malignancies Companies |

|

|

T-cell Malignancies Therapies |

|

|

T-cell Malignancies Market |

Segmented by

|

|

Analysis |

• Addressable patient population • Market drivers and Market barriers • Cost assumptions and Pricing analogues • KOL views • SWOT analysis • Reimbursement • Conjoint analysis • Unmet need |

T-cell Malignancies Disease Understanding

T-cell Malignancies Overview

T cell malignancies encompass a heterogeneous group of diseases, each reflecting a clonal evolution of dysfunctional T cells at various stages of development. T-cell lymphomas comprise approximately 10-15% of all Non-Hodgkin’s Lymphomas (NHLs). The main subsets are peripheral T-cell lymphoma (PTCL) and cutaneous T-cell lymphoma (CTCL).

PTCLs refers to the nodal or systemic T-cell lymphomas and comprises 19 different entities with varying clinical and pathologic presentation including PTCL-not otherwise specified (NOS), angioimmunoblastic T-cell lymphoma (AITL), anaplastic large cell lymphoma (ALCL) and adult T-cell Leukemia/lymphoma (ATLL), a rare and aggressive T-cell lymphoma linked to human T-cell lymphotropic virus type 1 (HTLV-1). CTCL originates in the skin, including the main subtype’s mycosisfungoides (MF) and Sézary syndrome. The various subtypes have distinct pathophysiology and molecular profiles. Beyond this, there is geographic diversity.

T-cell Malignancies Diagnosis

Diagnosis of T-cell malignancies involves a stepwise approach integrating clinical evaluation, histopathology, and advanced laboratory testing. The initial step includes assessment of presenting symptoms such as skin lesions in CTCL or lymphadenopathy and systemic symptoms in PTCL. This is followed by tissue biopsy (skin, lymph node, or bone marrow), which remains the gold standard for diagnosis. Immunophenotyping using immunohistochemistry or flow cytometry is then performed to confirm T-cell lineage and characterize antigen expression. Molecular testing, including T-cell receptor (TCR) gene rearrangement and next-generation sequencing, is used to establish clonality and identify relevant mutations. Imaging techniques such as CT Scans or PET-CT scans are further utilized to determine disease extent and staging, while bone marrow evaluation may be required in certain cases.

Further details are provided in the report...

Current T-cell Malignancies Treatment Landscape

The current treatment of T-cell malignancies is based on a combination of chemotherapy, targeted therapies, immunotherapy, and, in select cases, stem cell transplantation, depending on disease subtype and stage. First-line management for aggressive subtypes such as PTCL typically involves multi-agent chemotherapy (e.g., CHOP-based regimens), while indolent conditions like CTCL may be treated with skin-directed and systemic therapies. Targeted agents such as brentuximab vedotin (ADCETRIS) and mogamulizumab (POTELIGEO) are increasingly used, particularly in relapsed or refractory settings, alongside small molecules including HDAC Inhibitors and PI3K inhibitors. Treatment is highly individualized, with transplantation considered for eligible high-risk or relapsed patients.

Further details related to country-based variations are provided in the report...

T-cell Malignancies Unmet Needs

The section “unmet needs of T-cell malignancies” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Lack of personalized and effective treatment options in CTCL

- No established standard of care for relapsed/refractory PTCL patients

- High relapse rates in first-line chemotherapy

- Impact of CTCL on patient’s quality of life, and others…..

Note: Comprehensive unmet needs insights in T-cell malignancies and their strategic implications are provided in the full report.

T-cell Malignancies Epidemiology

The T-cell Malignancies epidemiology section provides insights about the historical and current T-cell Malignancies patient pool and forecasted trends for individual seven major countries. It helps to recognize the causes of current and forecasted trends by exploring numerous studies and views of key opinion leaders. This part of the T-cell Malignancies market report also provides the diagnosed patient pool and their trends along with assumptions undertaken.

Key Findings from T-cell Malignancies Epidemiological Analysis and Forecast

- According to DelveInsight’s estimates, in 2025, the total number of incident cases of T-cell malignanacies in the 7MM were ~15,500.

- In the US, among type-specific T-cell malignancies, pTCL accounted for the majority of cases (~12,330) in 2025, whereas CTCL represented a smaller share with ~3,100 cases.

- In Japan, the age-specific incident cases of CTCL in 2025 were higher in males (~890 cases), whereas females accounted for a comparatively lower number of cases (~560).

- CTCL represents approximately 2–4% of all non-Hodgkin lymphomas, classifying it as an orphan malignancy. Mycosis fungoides is the predominant subtype, accounting for ~55–65% of CTCL cases. The disease is typically diagnosed in older adults, with a median age at onset of 55–65 years, and around 60-70% of patients present with early-stage disease at diagnosis.

T-cell Malignancies Epidemiology Segmentation

- Total Incident Cases of T-cell Malignancies

- PTCL-specific Incident Cases

- Total Incident Cases of PTCL

- Stage-specific Incident Cases of PTCL

- Subtype-specific Incident Cases of PTCL

- Line-wise Treated Cases of PTCL

- CTCL-specific Incident Cases

- Total Incident Cases of CTCL

- Type-specific Cases of CTCL

- Gender-specific Cases of CTCL

- Stage-specific Cases of CTCL

- Treatment-eligible Pool for Early and Advanced Stages

Recent Developments in the T-cell Malignancies Treatment Landscape:

- In March 2026, Prescient Therapeutics is advancing enrolment in its Phase II clinical trial for lead asset PTX-100, with new research highlighting steady progress across trial execution, regulatory milestones and funding, while pointing to valuation upside from current levels.

- In December 2025, Corvus Pharmaceuticals announced the presentation of final data from its Phase I/Ib trial of soquelitinib in patients with T-cell lymphoma at ASH 2025. These results provide the foundation for the ongoing registration Phase III trial in r/r PTCL.

- In November 2025, Innate announced that the US FDA has completed its review of the confirmatory Phase III protocol for lacutamab in CTCL, with no further comments, clearing the trial to proceed.

T-cell Malignancies Drug Analysis & Competitive Landscape

The T-cell malignancies drug chapter provides a detailed, market-focused review of approved therapies and the emerging pipeline across Phase I–III T-cell Malignancies clinical trials. It covers mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, and strategic partnerships upcoming Key catalyst for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the T-cell malignancies treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the T-cell malignancies therapeutics market.

Approved Therapies for T-cell Malignancies

Denileukin diftitox (LYMPHIR): Citius Pharmaceuticals

Denileukin diftitox is an IL-2 receptor-directed cytotoxin and designed to direct the cytocidal action of Diphtheria Toxin (DT) to cells that express the IL-2 receptor. After uptake into the cell, the DT fragment is cleaved, and the free DT fragments inhibit protein synthesis, resulting in cell death. It is approved in August 2024 for the treatment of adult patients with relapsed or refractory stage I-III CTCL after at least one prior systemic therapy.

T-cell Malignancies Marketed/Approved Therapies | ||||||

|

Drug/Therapy |

Company |

Indication |

Molecule Type |

MoA |

RoA |

Marketed Region |

|

Denileukin diftitox (LYMPHIR) |

Citius Pharmaceuticals |

r/r Stage I–III CTCL after at least one prior systemic therapy |

Recombinant engineered fusion protein |

Protein synthesis inhibitors |

IV infusion |

US: 2024 |

|

Brentuximab vedotin (ADCETRIS) |

Pfizer (Seagen) and Takeda |

Adult patients with pcALCL or CD30-expressing mycosis fungoides who have received at least one prior systemic therapy |

ADC |

CD30-directed antibody and microtubule inhibitor |

IV infusion |

US: 2017 |

T-cell Malignancies Pipeline Analysis

Duvelisib (COPIKTRA): Secura Bio

Duvelisib (COPIKTRA) is an oral dual PI3K-d/? inhibitor being actively evaluated in clinical development for T-cell malignancies, particularly PTCL. PI3K signaling may lead to the proliferation of malignant cells and is thought to play a role in the formation and maintenance of a supportive tumor microenvironment.

Competitive Landscape of T-cell Malignancies Pipeline Drugs | ||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Anticipated Launch in the US |

|

Duvelisib |

Secura Bio |

III |

r/r PTCL |

Oral |

Phosphoinositide 3-kinase inhibitor |

2029 |

|

Golidocitinib |

Dizal Pharmaceuticals |

III |

r/r PTCL |

Oral |

JAK1 inhibitor |

Information is available in the full report |

|

PTX-100 |

Prescient Therapeutics |

II |

r/r CTCL |

IV infusion |

Geranylgeranyl Transferase-1 (GGT-1) inhibitor |

Information is available in the full report |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | ||||||

T-cell Malignancies Key Players, Market Leaders and Emerging Companies

- Kyowa Hakko Kirin

- Pfizer (Seagen)

- Takeda

- Helsinn Therapeutics

- Citius Pharmaceuticals

- HUYA Bioscience International (HUYABIO)

- Acrotech Biopharma

- Mundipharma

- Soligenix

- Sterling Pharma Solutions

- Prescient Therapeutics

- Innate Pharma, and others

T-cell Malignancies Market Outlook

The T-cell malignancies market is undergoing a progressive transformation, shifting from historically chemotherapy-driven and non-specific immunosuppressive approaches toward targeted and immunotherapy-based treatment paradigms. Established agents such as brentuximab vedotin (ADCETRIS) and mogamulizumab (POTELIGEO) have already demonstrated the clinical value of precision targeting (e.g., CD30 and CCR4), while immune checkpoint inhibitors such as pembrolizumab (KEYTRUDA) have further expanded the role of immuno-oncology in select T-cell lymphoma settings.

Recent years have seen increasing integration of antibody-drug conjugates (ADCs), monoclonal antibodies, and small-molecule targeted therapies, including agents such as duvelisib and crizotinib, which inhibit key oncogenic signaling pathways involved in T-cell proliferation and survival. This diversification of mechanisms reflects a broader shift toward biology-driven treatment strategies, particularly in relapsed or refractory disease where unmet need remains high.

Concurrently, the pipeline is expanding with next-generation immunotherapies and novel targeted agents, including checkpoint inhibitors, anti-KIR and anti-CD47 approaches, and epigenetic modulators, many of which are being evaluated in early- to mid-stage clinical trials. Combination strategies (e.g., ADCs with checkpoint inhibitors) are also being explored to enhance response durability and overcome resistance, signaling a move toward rational combination regimens in future treatment algorithms.

Overall, the T-cell malignancies market is expected to witness steady evolution rather than rapid disruption, driven by incremental innovation, increasing biomarker-driven patient stratification, and improved disease awareness. While the rarity and heterogeneity of T-cell malignancies may limit large-scale clinical development, the continued entry of targeted and immunotherapeutic agents is anticipated in the gradually reshape the treatment landscape across 7MM T-cell maliganancies market from 2022–2036, with strong commercial implications for both marketed products and emerging pipelines.

- Among the 7MM, the US accounted for the largest market size of T-cell malignanacies. i.e., USD ~1,250 million in 2025.

- In 2036, among all the therapies for T-cell malignancies, the highest revenue is estimated to be generated by brentuximab vedotin (ADCETRIS), in the US.

- The entry of late-stage candidates such as linperlisib, golidocitinib, and PTX-100 are expected to intensify competition in the T-cell malignanices treatment landscape during the latter half of the forecast period.

Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in T-cell Malignancies (2022–2036 Forecast)

The T-cell malignanacies market comprises monoclonal antibodies, ADCs, and small molecules, each targeting types of T-cell Malignancies.

Monoclonal antibodies: Therapies such as brentuximab vedotin (ADCETRIS), an ADC targeting CD30, and mogamulizumab (POTELIGEO), a CCR4-directed monoclonal antibody, are key approved options in T-cell lymphomas. In addition, immune checkpoint inhibitors like pembrolizumab (KEYTRUDA) target the PD-1 pathway to enhance anti-tumor immunity, while emerging agents such as sugemalimab further expand the immunotherapy landscape.

Small molecules: This class includes targeted and epigenetic therapies such as crizotinib (XALKORI), tucidinostat (HIYASTA), and duvelisib, which inhibit oncogenic signaling pathways critical for tumor survival. Other treatments like mechlorethamine (VALCHLOR/LEDAGA) provide skin-directed chemotherapy for cutaneous T-cell lymphoma, while emerging agents such as golidocitinib are being developed to further address unmet needs through novel mechanisms of action.

Small molecules defines the core innovation landscape, with radioligand therapies currently commercially validated and small molecules driving pipeline growth.

T-cell Malignancies Drug Uptake

This section focuses on the uptake rate of potential T-cell Malignancies drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the T-cell Malignancies drug’s uptake, performance at peak, factors affecting performance during prime years of growth, patient uptake by therapy, and anticipated sales generated by each drug.

The uptake of therapies in T-cell malignancies is expected to vary based on clinical positioning, mechanism of action, and stage of development. Approved therapies such as denileukin diftitox (LYMPHIR) are projected to demonstrate a medium-fast uptake, supported by their established clinical profile, targeted mechanism, and the high unmet need in relapsed or refractory settings.

Emerging therapies such as Lacutamab (IPH4102), PTX-100, and AUTO4 are anticipated to follow a moderate uptake trajectory, reflecting their investigational status and the gradual build-up of clinical evidence, alongside cautious adoption in clinical practice.

Meanwhile, agents like Linperlisib are expected to show a slow-to-medium uptake, as their positioning within the treatment landscape, differentiation from existing therapies, and long-term efficacy and safety data will play a key role in influencing adoption.

Detailed insights of emerging therapies' drug uptake is included in the report...

T-cell Malignancies Market Access and Reimbursement Scenario

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of approved therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

The United States

US Reimbursement of Therapies Approved for T-cell Malignancies | |

|

Drug/Therapy |

Access Program |

|

XALKORI |

|

Reimbursement is a crucial factor that affects the drug’s access to the market. often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

T-cell Malignancies Therapies Price Scenario & Trends

Pricing and analogue assessment of T-cell malignancies therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, closest and most approproiate analogue selection for emerging therapies, and understanding of how pricing influences market access, adherence, and long-term uptake.

Pricing of T-cell Malignancies Approved Drugs

Belinostat (BELEODAQ) is administered at a recommended dose of 1,000 mg/m², delivered as a 30-minute intravenous infusion once daily on Days 1–5 of a 21-day cycle. Based on current pricing and treatment duration, the estimated total cost of therapy is approximately USD 516,556.

Industry Experts and Physician Views for T-cell Malignancies

To keep up with T-cell malignancies market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry Experts were contacted for insights on the T-cell malignancies emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in T-cell malignancies, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 15+ KOLs to gather insights at country level. Centers such as the University of Colorado School of Medicine, Padua University Hospital, University College London Hospitals NHS Foundation Trust, and Humboldt-Universität zu Berlin, etc. were contacted. Their opinion helps understand and validate current and emerging T-cell malignancies therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in T-cell malignancies.

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“Early diagnosis is essential to prevent treatment delay, mistreatment, and a deleterious effect on quality of life due to itching, pain, and disfigurement. For patients with advanced-stage disease, rapid diagnosis is critical, particularly for SS and for stage IVA2-IVB patients who have a median survival of just 12 to 36 months from the time of diagnosis. No individual treatments are curative and eligible patients should be referred for assessment for allogeneic bone marrow transplant because that is their best chance for long-term survival.” |

|

Germany |

“The LibrA T1 study of AUTO4 is a novel approach using a CAR T-cell designed to selectively target and eliminate T cells that include the malignant clone which harbors the TRBC1 receptor, while preserving the T-cell compartment with the TRBC2 receptor which helps to maintain immune-competence. AUTO4 is well tolerated and the data to date in this early phase study are very promising.” |

T-cell Malignancies Report Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of T-cell malignancies, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are majorly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the T-cell Malignancies Market Report

- The report covers a segment of key events, an executive summary, a descriptive overview of T-cell malignancies, explaining their causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the T-cell malignancies market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM T-cell malignancies market.

T-cell Malignancies Market Report Insights

- T-cell Malignancies Patient Population Forecast

- T-cell Malignancies Therapeutics Market Size

- T-cell Malignancies Pipeline Analysis

- T-cell Malignancies Market Size and Trends

- T-cell Malignancies Market Opportunity (Current and forecasted)

T-cell Malignancies Market Report Key Strengths

- T-cell Malignancies Epidemiology-based (Epi-based) Bottom-up Forecasting

- Artificial Intelligence (AI)-Enabled Market Research Report

- 11-Year Forecast

- T-cell Malignancies Market Outlook (North America, Europe, Asia-Pacific)

- T-cell Malignancies Patient Burden Trends (By Geography)

- T-cell Malignancies Treatment Addressable Market (Tam)

- T-cell Malignancies Competitve Landscape

- T-cell Malignancies Major Companies Insights

- T-cell Malignancies Price Trends and Analogue Assessment

- T-cell Malignancies Therapies Drug Adoption/Uptake

- T-cell Malignancies Therapies Peak Patient Share Analysis

T-cell Malignancies Market Report Assessment

- T-cell Malignancies Current Treatment Practices

- T-cell Malignancies Unmet Needs

- T-cell Malignancies Clinical Development Analysis

- T-cell Malignancies Emerging Drugs Product Profiles

- T-cell Malignancies Market attractiveness

- T-cell Malignancies Qualitative Analysis (SWOT and conjoint analysis)

- T-cell Malignancies Market Drivers

- T-cell Malignancies Market Barrriers

FAQs Related to the T-cell Malignancies Market Report:

T-cell Malignancies Market Insights

- What was the T-cell malignancies market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of T-cell malignancies?

- What are the disease risks, burdens, and unmet needs of T-cell malignancies? What will be the growth opportunities across the 7MM concerning the T-cell Malignancies patient population?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of T-cell malignancies? What are the current guidelines for treating T-cell malignancies in the US, Europe, and Japan?

Reasons to Buy T-cell Malignancies Market Forecast Report

- The report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the T-cell malignancies market.

- Bottom up forecasting builds from the affected population to product forecasts, delivering a robust, data driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI) enabled report summarize and simplify complex datasets withing the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data driven decisions.