Artificial Intelligence (AI) in Healthcare Market Summary

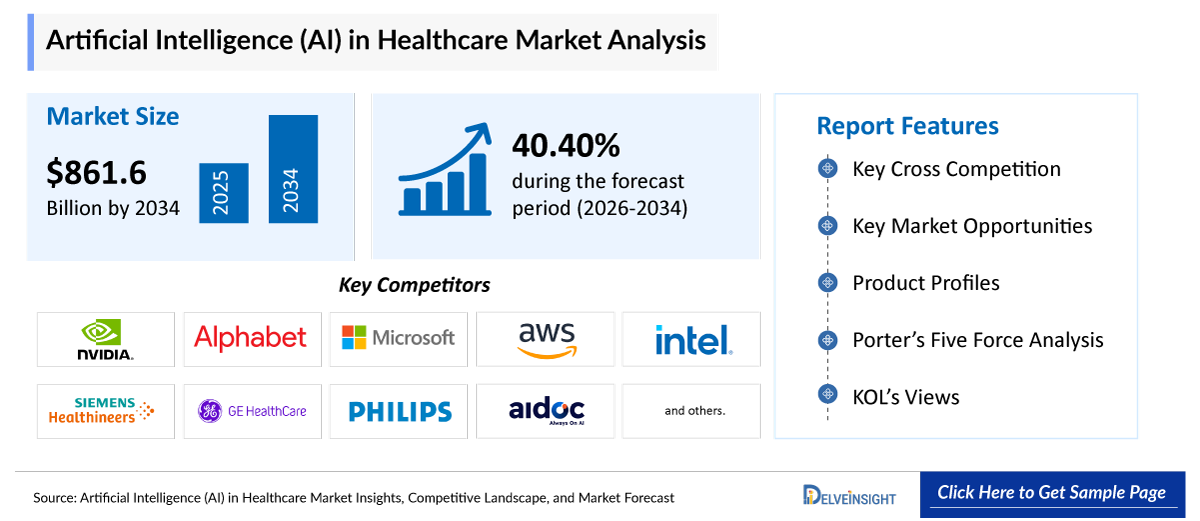

The global artificial intelligence in healthcare market is expected to increase from USD 40,809.25 million in 2025 to USD 861,636.63 million by 2034, reflecting strong and sustained growth.

The global artificial intelligence in healthcare market is growing at a CAGR of 40.40% during the forecast period from 2026 to 2034.

The rising prevalence of chronic diseases is increasing the demand for continuous monitoring, early diagnosis, and personalized treatment, which AI-powered tools can efficiently support. At the same time, the accelerating adoption of AI and advanced analytics in healthcare is improving clinical decision-making, operational efficiency, and predictive insights across hospitals and research settings. The expansion of digital health, telemedicine, and remote patient monitoring is further generating large volumes of real-time patient data, enabling AI systems to deliver timely interventions and virtual care solutions. Additionally, advances in machine learning, deep learning, and generative AI are enhancing diagnostic accuracy, drug discovery, and personalized medicine capabilities. Collectively, these factors are significantly driving the growth and transformation of the AI in healthcare market.

The leading companies operating in the artificial intelligence in healthcare market include NVIDIA, Google (Alphabet), Microsoft, Amazon (AWS), Intel Corporation, Siemens Healthineers, GE HealthCare, Koninklijke Philips N.V., Aidoc, Viz.ai, Inc, Qure.ai, Recursion, Insilico Medicine, Abridge AI, Inc., Waystar, IBM, CitiusTech Inc, Tempus AI, Inc., Hippocratic AI, Solventum, and others.

North America is expected to dominate the artificial intelligence in healthcare market due to its strong healthcare infrastructure, early adoption of advanced digital technologies, and significant investments in AI research and development. The region is also home to major technology companies and healthcare innovators, which accelerates the development and deployment of AI-driven solutions. Additionally, supportive government initiatives, increasing healthcare data availability, and growing demand for improved patient outcomes and cost efficiency further strengthen the market growth in North America.

In the component segment of the artificial intelligence in healthcare market, the software category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Artificial Intelligence (AI) in Healthcare Market Insight

Artificial Intelligence (AI) in Healthcare Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 40,809.25 million |

|

2034 Projected Market Size |

USD 861,636.63 million |

|

Growth Rate (2026-2034) |

40.40% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of Artificial Intelligence (AI) in Healthcare Market

Rising prevalence of chronic diseases leading to a surge in artificial intelligence in healthcare: The increasing burden of chronic diseases such as diabetes, cardiovascular disorders, and cancer is driving the demand for continuous monitoring, early diagnosis, and personalized treatment. AI in healthcare enables predictive analytics and risk stratification, helping clinicians manage patients more effectively and reduce complications, thereby boosting market growth.

Accelerating adoption of AI and advanced analytics in healthcare: Healthcare providers are increasingly integrating AI and advanced analytics into clinical workflows to improve diagnostic accuracy, optimize treatment plans, and enhance operational efficiency. This growing adoption is expanding the use of AI-based tools across hospitals, diagnostics, and research, fueling market expansion.

Expansion of digital health, telemedicine, and remote patient monitoring: The rapid growth of digital health platforms, telemedicine services, and remote patient monitoring is generating large volumes of real-time patient data. AI technologies analyze this data to provide timely insights, virtual care support, and early intervention, significantly driving the demand for AI in healthcare solutions.

Advances in machine learning, deep learning, and generative AI technologies: Continuous advancements in machine learning, deep learning, and generative AI are improving the capabilities of healthcare applications such as medical imaging, drug discovery, and personalized medicine. These technological innovations are enhancing accuracy, speed, and scalability, thereby accelerating the overall growth of the AI in healthcare market.

Artificial Intelligence (AI) in Healthcare Market Report Segmentation

This artificial intelligence in healthcare market report offers a comprehensive overview of the global artificial intelligence in healthcare market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Component (Hardware, Software Solutions, and Services), Technology (Deep Learning, Natural Language Processing, Machine Learning, Computer Vision & Image Recognition, and Others), Deployment Models (On-Premises Models, Cloud-Based Models, and Hybrid Deployment Models), Solution Type (Diagnosis & Early Detection, Treatment Planning & Personalization, Patient Engagement & Remote Monitoring, Administrative Workflow Automation, Data Management & Analytics, and Others), Application (Medical Imaging and Diagnostics, Robot-Assisted Surgery & Surgical AI, Clinical Trial Acceleration & Drug Discovery, Virtual Assistants & Chatbots, Telemedicine & Remote Care, and Others), End-Users (Hospitals & Healthcare Providers, Pharmaceutical & Biotechnology Firms, Healthcare Payers & Insurance, Diagnostic Centers & Labs, Research & Academic Institutions, and Patients & Caregivers), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing artificial intelligence in healthcare market.

The Artificial Intelligence (AI) in Healthcare refers to the global ecosystem of AI-enabled software, platforms, services, and solutions designed to support and enhance healthcare delivery, clinical decision-making, operational efficiency, and patient outcomes. This market encompasses technologies such as machine learning, deep learning, natural language processing, computer vision, and generative AI that analyze complex healthcare data from medical imaging, electronic health records, genomics, and connected devices to enable diagnostics, treatment planning, disease prevention, population health management, and administrative automation across healthcare systems.

The rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, cancer, and respiratory conditions is significantly increasing the need for continuous patient monitoring, early and accurate diagnosis, and highly personalized treatment approaches. In this context, AI-powered healthcare solutions are becoming essential, as they can analyze large and complex patient datasets in real time to support clinicians in making faster and more informed decisions.

At the same time, the accelerating adoption of artificial intelligence and advanced analytics across healthcare ecosystems is transforming clinical workflows by improving decision-making accuracy, optimizing hospital operations, and enabling predictive insights for better disease management and resource allocation. Hospitals, diagnostic centers, and research institutions are increasingly integrating data-driven tools to enhance efficiency and reduce diagnostic errors.

Furthermore, the rapid expansion of digital health ecosystems, including Telemedicine and Remote Patient Monitoring, is generating vast volumes of real-time patient data from wearable devices, mobile applications, and connected medical systems. This continuous data flow is enabling AI systems to deliver proactive alerts, timely interventions, and more effective virtual care delivery, especially for patients in remote or underserved regions.

In addition, advancements in Machine Learning, Deep Learning, and Generative AI are further strengthening the capabilities of healthcare AI solutions. These technologies are improving diagnostic precision in medical imaging, accelerating drug discovery processes, and enabling highly personalized treatment plans based on patient-specific genetic, clinical, and behavioral data.

Collectively, these converging factors are not only driving strong growth in the AI in healthcare market but are also fundamentally transforming the way healthcare is delivered, making it more predictive, personalized, and efficient across the entire care continuum.

Get More Insights into the Report @Artificial Intelligence (AI) in Healthcare Market

What are the latest artificial intelligence in healthcare market dynamics and trends?

The accelerating adoption of artificial intelligence (AI) and advanced analytics is clearly reflected in multiple recent industry developments and regulatory milestones, which collectively demonstrate how rapidly these technologies are being embedded into clinical and operational healthcare workflows.

The accelerating adoption of artificial intelligence (AI) and advanced analytics is becoming one of the most influential forces driving growth in the global AI in healthcare market. Healthcare systems worldwide are increasingly relying on data-driven technologies to improve clinical outcomes, optimize operations, and address growing cost and workforce pressures. AI enables healthcare organizations to extract meaningful insights from vast volumes of structured and unstructured medical data, which traditional analytics tools are unable to process efficiently.

One of the key drivers of AI adoption is its expanding role in clinical decision-making and diagnostics. Advanced analytics and machine learning algorithms are being integrated into medical imaging, pathology, and diagnostic workflows to support early disease detection and improve diagnostic accuracy. For instance, in October 2023, Microsoft expanded its Nuance DAX Copilot solution, an AI-powered clinical documentation tool using ambient listening and generative AI to automate physician notes, significantly reducing administrative burden and improving workflow efficiency. In medical imaging, in December 2024, GE Healthcare announced expanded deployment of its AI-based imaging platform AIR Recon DL, enhancing MRI image reconstruction quality and reducing scan times. Similarly, Siemens Healthineers strengthened its AI portfolio in June 2024 through upgrades to its AI-Rad Companion platform, which supports radiologists in detecting abnormalities in CT and MRI scans, improving diagnostic consistency and reducing interpretation time. In clinical AI decision support, Viz.ai received expanded FDA clearances in August 2023 for AI-powered stroke and pulmonary embolism detection systems, enabling real-time identification of critical conditions and faster clinical response. Likewise, Aidoc secured additional FDA clearances in February 2025 for AI algorithms detecting multiple acute conditions such as rib fractures and intracranial hemorrhage, reinforcing trust in AI-driven radiology triage systems.

Additionally, the rapid expansion of telemedicine, digital health platforms, and remote patient monitoring (RPM) is significantly accelerating the adoption of AI in healthcare, as these ecosystems continuously generate large volumes of real-time patient data that require intelligent analysis for early detection, triaging, and personalized care delivery. In recent years, leading healthcare technology companies have intensified efforts to integrate AI into virtual care workflows. For example, in September 2025, Royal Philips and Masimo extended their long-standing partnership to jointly develop next-generation patient monitoring solutions that combine wearable devices, RPM systems, and AI-powered clinical decision support tools to improve both hospital and home-based care delivery. This collaboration specifically focuses on embedding AI algorithms into connected monitoring platforms to enable faster interpretation of patient vitals and proactive intervention in deteriorating conditions.

Thus, the factors mentioned above are expected to boost the overall market of AI in healthcare during the forecast period.

However, the concerns around data privacy, security, and regulatory compliance, along with limited digital literacy and resistance to technology adoption, and high implementation costs with scalability challenges, are collectively acting as key restraints for the AI in healthcare market. Healthcare systems handle highly sensitive patient data, making them vulnerable to cybersecurity risks and strict regulatory requirements such as HIPAA and GDPR, which slow down AI deployment. At the same time, many patients and even healthcare providers lack sufficient digital literacy, leading to hesitation in fully adopting AI-driven tools, especially in telemedicine and remote monitoring settings. Additionally, the high upfront costs of AI infrastructure, integration with legacy hospital systems, and ongoing maintenance create significant financial burdens, particularly for smaller healthcare providers, limiting large-scale and uniform adoption across regions.

Artificial Intelligence (AI) in Healthcare Market Segment Analysis

Artificial Intelligence (AI) in Healthcare Market by Component (Hardware, Software Solutions, and Services), Technology (Deep Learning, Natural Language Processing, Machine Learning, Computer Vision & Image Recognition, and Others), Deployment Models (On-Premises Models, Cloud-Based Models, and Hybrid Deployment Models), Solution Type (Diagnosis & Early Detection, Treatment Planning & Personalization, Patient Engagement & Remote Monitoring, Administrative Workflow Automation, Data Management & Analytics, and Others), Application (Medical Imaging and Diagnostics, Robot-Assisted Surgery & Surgical AI, Clinical Trial Acceleration & Drug Discovery, Virtual Assistants & Chatbots, Telemedicine & Remote Care, and Others), End-Users (Hospitals & Healthcare Providers, Pharmaceutical & Biotechnology Firms, Healthcare Payers & Insurance, Diagnostic Centers & Labs, Research & Academic Institutions, and Patients & Caregivers), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Component: The software category in artificial intelligence in healthcare is expected to dominate the market with the largest revenue share

In the component segment of the artificial intelligence in healthcare market, the software category is contributing to 47.68% of total market revenue in 2025, as it enables hospitals and digital health platforms to deploy AI capabilities such as clinical decision support, automated diagnostics, predictive analytics, and workflow optimization across telemedicine and remote care ecosystems. The increasing integration of AI-powered software into electronic health records (EHRs), imaging platforms, and virtual care solutions is making healthcare delivery more efficient, scalable, and data-driven. A key recent development supporting this trend is the launch of Microsoft Dragon Copilot in March 2025, an AI-powered clinical assistant that combines ambient listening, voice dictation, and generative AI to automate documentation, surface clinical insights, and streamline physician workflows within healthcare systems, significantly strengthening the role of software-driven AI in clinical environments.

Similarly, in October 2025, Microsoft further expanded its software ecosystem by extending Dragon Copilot capabilities to nursing workflows and enabling third-party AI applications through an extensible platform, allowing deeper integration of AI agents directly into clinical systems for tasks such as documentation, care coordination, and revenue cycle support. In addition, Nuance DAX Copilot (integrated with Epic EHR in January 2024) continues to demonstrate strong adoption across healthcare providers by using AI software to automatically generate clinical notes from patient interactions, reducing administrative burden and improving physician productivity.

Overall, these continuous software innovations highlight how AI-enabled platforms are becoming central to healthcare transformation, as they allow seamless integration of AI into existing hospital IT systems, enhance real-time clinical decision-making, and drive widespread adoption across telehealth, RPM, and hospital workflows, thereby making software the most influential component in accelerating the AI in healthcare market.

By Technology: Machine Learning Category Dominates the Market

Within the technology segment of the artificial intelligence in healthcare market, the machine learning category is anticipated to dominate, accounting for around 47.37% of the market share in 2025, due to its broad applicability across nearly all major healthcare use cases. Unlike other AI technologies that are often confined to specific domains, ML is widely used in predictive analytics, clinical decision support, medical imaging, hospital workflow optimization, and drug discovery. over 60% of healthcare AI use cases are centered around predictive analytics, which is fundamentally powered by ML algorithms. This wide applicability enables ML to capture the largest share of the technology segment.

Another key reason for ML’s dominance is that deep learning, one of the fastest-growing AI technologies, is a subset of machine learning. Many advanced applications, such as radiology image analysis, pathology detection, and oncology diagnostics, rely on deep learning models, but these are often classified within the broader ML category. As a result, even as deep learning adoption accelerates, it reinforces ML’s dominance rather than competing with it.

A critical real-world validation of ML’s dominance comes from regulatory approvals. The U.S. Food and Drug Administration has authorized a rapidly growing number of AI-enabled medical devices, the majority of which are based on machine learning techniques. According to FDA data, hundreds to over 1,000 AI-enabled medical devices have already received approval or clearance, with a significant concentration in radiology and cardiology.

This is a strong indicator that ML is not just theoretical; it is clinically validated and commercially deployed at scale.

Several companies have already received FDA approvals for ML-enabled devices, particularly in imaging and diagnostics:

iSchemaView – FDA-cleared stroke imaging solutions (e.g., RapidAI) using ML for real-time brain scan analysis

VideaHealth – FDA-cleared AI for dental radiograph analysis

Quantib – ML-based neuroimaging tools for brain disease detection

Butterfly Network – FDA-cleared AI-powered ultrasound solutions for automated diagnostics

AIRS Medical – AI-based MRI enhancement tools

These examples clearly show that ML is already embedded in commercially approved and deployed medical devices, particularly in high-value areas like imaging.

Machine learning also has strong penetration in clinical decision support systems (CDSS), which are among the most widely adopted AI applications in healthcare. Hospitals increasingly rely on ML models for early disease detection, risk stratification, and treatment recommendations. Studies indicate that ML-based systems can reduce hospital readmissions by 15-25% and lower sepsis-related mortality by 20-30%, demonstrating clear clinical and economic value.

Another major driver is ML’s dominance in predictive analytics, which represents the largest revenue-generating function in healthcare AI. ML models are used to predict patient deterioration, disease progression, hospital length of stay, and operational risks such as fraud detection. This segment alone accounts for approximately 35-45% of total AI spending in healthcare, further reinforcing ML’s leading position.

From a technical standpoint, ML offers a lower barrier to adoption compared to other AI technologies. It works effectively with structured and semi-structured data such as electronic health records (EHRs), claims data, and lab results. Given that nearly 80% of healthcare data is structured or semi-structured, ML is naturally better suited for widespread deployment compared to technologies like NLP (focused on text) or computer vision (focused on images).

Finally, ML’s dominance is reinforced by strong investment and ecosystem support from major technology players such as IBM, Google, Microsoft, and NVIDIA. These companies have built large-scale healthcare AI platforms centered around ML capabilities, particularly in predictive analytics and clinical decision-making.

By Deployment Mode: Cloud Category Dominates the Market

Within the deployment mode segment of the AI in healthcare market, the cloud-based category is projected to dominate, accounting for around 54.65% of the market share in 2025, due to its ability to provide scalable infrastructure, real-time data access, seamless integration with telemedicine and remote monitoring systems, and faster deployment of AI models without heavy upfront IT investments. Cloud platforms enable healthcare providers to store and analyze vast volumes of patient data securely while supporting advanced AI applications such as predictive analytics and clinical decision support. This trend is reinforced by recent developments among key players. For instance, in March, 2025, Microsoft introduced new AI-powered capabilities within its healthcare cloud portfolio, enhancing data interoperability, analytics, and AI-driven clinical workflows on cloud infrastructure.

Similarly, during Google Cloud Next 2025 (April, 2025), Google Cloud announced multiple innovations, including upgrades to Vertex AI and new AI agent development tools designed to help healthcare organizations build and deploy AI solutions at scale on the cloud. In another notable development, in March 2026, CVS Health partnered with Google Cloud to launch an AI-enabled cloud-based platform (Health100) that integrates patient data from multiple sources to support real-time health management and personalized care delivery.

Collectively, these advancements highlight how cloud deployment is becoming the backbone of AI in healthcare by enabling flexibility, interoperability, and large-scale adoption across healthcare systems.

By Solution Type: Diagnosis & Early Detection Category Dominates the Market

In the solution type segment of the AI in healthcare market, the diagnosis & early detection category dominates, accounting for around 33.75% of the market share in 2025, due to its critical role in improving clinical outcomes through timely and accurate identification of diseases. AI technologies, particularly machine learning and deep learning, are extensively used to analyze medical imaging, pathology slides, and patient data to detect conditions such as cancer, cardiovascular diseases, and neurological disorders at an early stage, often with higher precision than traditional methods. The growing burden of chronic diseases and the increasing demand for faster, cost-effective diagnostic solutions have further accelerated the adoption of AI-driven diagnostic tools across hospitals and diagnostic centers. Additionally, continuous advancements in AI algorithms and their integration into imaging systems and clinical workflows are enhancing diagnostic efficiency, reducing human error, and enabling proactive treatment decisions, thereby driving the dominance of this segment in the overall market.

By Application: Medical Imaging and Diagnostics Category Dominates the Market

In the application segment of the AI in healthcare market, the medical imaging and diagnostics category dominates the overall market, accounting for around 14.86% of the market share in 2025, due to the extensive use of AI, particularly deep learning, in analyzing radiology images, detecting abnormalities, and improving diagnostic accuracy and workflow efficiency. Imaging generates vast volumes of complex data, making it highly suitable for AI-driven interpretation, which helps clinicians achieve faster and more precise diagnoses across conditions such as cancer, cardiovascular, and neurological disorders. This dominance is further supported by the large number of regulatory approvals, as medical imaging accounts for the majority of AI-enabled medical devices authorized by the U.S. FDA, highlighting its leading position in AI adoption.

Recent developments from key manufacturers reinforce this trend. For instance, in November 2025, Siemens Healthineers launched its AI-enabled radiology services and Optiq AI imaging chain, designed to enhance image quality, automate workflows, and support clinical decision-making across the entire imaging process. Furthermore, at RSNA in December 2025, major players, including GE HealthCare and Philips, showcased next-generation AI-powered MRI and imaging platforms that integrate AI across scanning, image reconstruction, and interpretation workflows.

In July 2026, a bio-native AI company took steps to patent the foundational data layer underlying its life sciences models, capitalizing on the shift of AI models toward commodities. Recognizing that raw data quality drives competitive advantage, the firm’s filing protects proprietary datasets optimized specifically for biological and chemical applications. This strategic move aims to secure their market position by safeguarding the foundational training inputs rather than the rapidly evolving algorithms themselves.

Overall, the continuous launch of AI-powered imaging platforms, increasing regulatory approvals, and growing reliance on automated diagnostics are key factors driving the dominance of the medical imaging and diagnostics segment in the AI in healthcare market.

By End-Users: Hospitals & Healthcare Providers Category Dominates the Market

In the end-users segment of the AI in healthcare market, the hospitals & healthcare providers category dominates the overall market due to their central role in patient care delivery and their strong need for advanced technologies to improve clinical efficiency, accuracy, and outcomes. Hospitals generate vast amounts of patient data from imaging systems, electronic health records (EHRs), and monitoring devices, making them the primary adopters of AI solutions such as clinical decision support, workflow automation, and predictive analytics. Additionally, the growing pressure to reduce operational costs, manage increasing patient volumes, and enhance quality of care is encouraging hospitals to integrate AI across diagnostics, treatment planning, and administrative functions. The availability of better infrastructure, higher investment capacity, and ongoing digital transformation initiatives further strengthen the adoption of AI among hospitals and healthcare providers, thereby driving their dominance in the overall market.

-in-Healthcare-Market-Assessment.png)

Artificial Intelligence (AI) in Healthcare Market Regional Analysis

North America Artificial Intelligence (AI) in Healthcare Market Trends

North America is expected to account for the highest proportion of 45.47% of the artificial intelligence in healthcare market in 2025, out of all regions. North America is expected to dominate the artificial intelligence in healthcare market due to its strong healthcare infrastructure, early adoption of advanced digital technologies, and significant investments in AI research and development. The region is also home to major technology companies and healthcare innovators, which accelerates the development and deployment of AI-driven solutions. Additionally, supportive government initiatives, increasing healthcare data availability, and growing demand for improved patient outcomes and cost efficiency further strengthen the market growth in North America.

A key growth driver is the widening gap between healthcare demand and the availability of trained specialists, particularly in areas such as mental health, maternal health, and primary care. Large segments of the U.S. population reside in regions facing critical shortages of mental and maternal health professionals, limiting access to timely and specialized care. AI-enabled virtual care platforms, digital therapeutics, and remote monitoring solutions are increasingly being deployed to address these access challenges by expanding care reach, supporting early intervention, and enabling continuous monitoring beyond traditional clinical settings.

Regulatory support and increasing acceptance of software-based medical interventions are further reinforcing market momentum. The U.S. Food and Drug Administration (FDA) has demonstrated growing openness toward AI-driven solutions, including digital therapeutics and clinical decision support tools. Regulatory clearances and approvals for AI-powered healthcare applications are helping validate their clinical effectiveness, build provider confidence, and accelerate adoption across healthcare systems.

Artificial intelligence has rapidly transitioned from an experimental technology to a core operational capability within U.S. healthcare organizations. Advanced AI systems are now embedded across clinical, administrative, and financial workflows. The emergence of agent-based and autonomous AI systems capable of executing tasks such as insurance prior authorizations, patient scheduling, and revenue cycle management is improving operational efficiency. At the clinical level, ambient clinical documentation and generative AI tools are increasingly used to automate medical note creation, significantly reducing administrative burden and helping address clinician burnout.

The adoption of AI-enabled digital health solutions continues to expand across disease management and post-acute care. Remote patient monitoring, AI-driven virtual consultations, medication adherence platforms, and digitally enabled rehabilitation programs are increasingly used to improve care continuity, enhance patient engagement, and reduce hospital readmissions. These technologies are particularly impactful for elderly populations and patients with cardiovascular, metabolic, and respiratory conditions.

The large patient base, combined with rising healthcare costs and workforce shortages, has encouraged artificial intelligence in healthcare companies to expand their U.S. presence through innovative service models and product launches. For example, in November 2025, ODDITY Tech Ltd. launched METHODIQ in the United States, an artificial intelligence in healthcare platform offering personalized treatments through online diagnosis, eliminating the need for in-person physician visits or pharmacy trips.

Overall, the convergence of high disease burden, supportive regulatory pathways, rapid technological innovation, and growing acceptance of digital and AI-driven care models is expected to sustain the growth of the North America artificial intelligence in healthcare market over the forecast period. The United States is anticipated to remain a global leader in AI healthcare adoption, innovation, and commercialization.

Europe Artificial Intelligence (AI) in Healthcare Market Trends

The artificial intelligence in healthcare market in Europe is experiencing robust growth due to strong government support, increasing digital health adoption, and a well-defined regulatory framework that promotes safe and scalable AI deployment. A key driver is the implementation of the EU Artificial Intelligence Act (enforced on August 1, 2024), which establishes clear guidelines for high-risk healthcare AI systems, boosting industry confidence and accelerating innovation across diagnostics, imaging, and clinical decision support. In addition, Europe is actively investing in AI-driven healthcare transformation; for instance, in October 2025, the European Commission launched a €1 billion “Apply AI” strategy to expand AI adoption across sectors, including healthcare, with a strong focus on clinical applications and digital infrastructure.

Recent developments further highlight this momentum. In June 2025, the European Commission initiated stakeholder consultations on high-risk AI systems to refine regulatory pathways and support faster commercialization of AI-based medical technologies. Moreover, healthcare systems are increasingly deploying AI solutions at scale; for example, the UK’s NHS announced in June 2025 the rollout of an AI-based early warning system to detect patient safety risks using real-time hospital data, marking a major step toward AI-driven population health management. Additionally, in April 2026, researchers in the UK developed an advanced AI tool capable of predicting heart failure up to five years in advance, demonstrating ongoing innovation in early diagnosis and preventive care.

Overall, the combination of supportive regulations, significant public and private investments, and continuous product innovations is driving strong adoption of AI technologies across European healthcare systems, thereby fueling market growth.

Asia-Pacific Artificial Intelligence (AI) in Healthcare Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the artificial intelligence in healthcare market due to rapid digital transformation, increasing healthcare investments, large patient populations, and rising adoption of telemedicine and AI-enabled diagnostic solutions. Countries such as China, India, Japan, and South Korea are actively investing in AI-driven healthcare infrastructure, supported by high smartphone penetration, expanding health data ecosystems, and strong government initiatives aimed at improving access and efficiency of care delivery. The region is also witnessing a surge in innovation and strategic collaborations among key players. For instance, in December 2025, Bristol Myers Squibb, in collaboration with Accenture, launched the AI-powered “Mosaic” medical content hub in Mumbai, designed to enhance real-time, data-driven healthcare communication and commercialization.

Additionally, in February 2026, the Government of India introduced a national AI healthcare blueprint and testing platform to standardize and accelerate the safe deployment of AI solutions across public healthcare systems, reflecting strong policy support in the region. In another development, February 2026 saw Innovaccer expand its AI capabilities through partnerships and launch initiatives like its Healthcare AI Center of Excellence, aimed at scaling enterprise AI adoption across healthcare providers. Moreover, regional innovation continues to grow, as seen in April 2026, when South Korean companies showcased advanced AI-driven healthcare technologies at WHX Bangkok 2026, highlighting increasing commercialization and cross-border expansion of AI solutions in APAC.

Overall, the combination of strong government initiatives, rapid technological advancements, and continuous product launches and collaborations among key industry players is positioning APAC as one of the fastest-growing and most dynamic regions in the AI in healthcare market.

Who are the major players in the artificial intelligence in healthcare market?

The following are the leading companies in the artificial intelligence in healthcare market. These companies collectively hold the largest market share and dictate industry trends.

NVIDIA

Google (Alphabet)

Microsoft

Amazon (AWS)

Intel Corporation

Siemens Healthineers

GE HealthCare

Koninklijke Philips N.V.

Aidoc

Viz.ai, Inc.

Qure.ai

Recursion

Insilico Medicine

Abridge AI, Inc.

Waystar

IBM

CitiusTech Inc.

Tempus AI, Inc.

Hippocratic AI

Solventum

Others

How is the competitive landscape shaping the artificial intelligence in healthcare market?

The competitive landscape of the artificial intelligence in healthcare market is characterized by intense competition, strategic collaborations, and continuous innovation, with a mix of large technology companies and specialized healthcare AI startups shaping the industry. Major players such as Microsoft, Google, IBM, and NVIDIA dominate through strong R&D capabilities, cloud infrastructure, and integrated AI platforms, while emerging companies focus on niche areas like imaging diagnostics, clinical decision support, and population health management. The market shows a moderately consolidated structure, with leading companies holding a significant share while startups drive innovation and agility.

Additionally, mergers, acquisitions, and partnerships play a crucial role as companies aim to expand technological capabilities, enhance product portfolios, and strengthen global presence. At the same time, there is a surge in investments from venture capital and private equity firms, reflecting strong confidence in AI’s potential to transform healthcare delivery and drug discovery. The competition is further intensified by the shift toward platform-based ecosystems and SaaS models, where companies compete on scalability, interoperability, and real-world clinical integration. Overall, the interplay between established tech giants and innovative startups, combined with high investment activity and rapid technological advancements, is creating a highly competitive and fast-evolving market landscape.

Recent Developmental Activities in the Artificial Intelligence (AI) in Healthcare Market

In April 2026, GE HealthCare received FDA clearance for a new deep learning-based CT imaging solution, designed to enhance image quality and diagnostic accuracy using advanced AI reconstruction techniques.

In September 2025, Royal Philips and Masimo extended their long-standing partnership to jointly develop next-generation patient monitoring solutions that combine wearable devices, RPM systems, and AI-powered clinical decision support tools to improve both hospital and home-based care delivery.

In July 2025, GE HealthCare announced that it has consistently led the industry in AI innovation, reaching over 100 FDA-authorized AI-enabled devices, many of which leverage deep learning to improve clinical workflows and diagnostic confidence.

In February 2025, Aidoc secured additional FDA clearances for AI algorithms detecting multiple acute conditions such as rib fractures and intracranial hemorrhage, reinforcing trust in AI-driven radiology triage systems.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Artificial Intelligence (AI) in Healthcare Market CAGR |

40.40% |

|

Key Companies in the Artificial Intelligence (AI) in Healthcare Market |

NVIDIA, Google (Alphabet), Microsoft, Amazon (AWS), Intel Corporation, Siemens Healthineers, GE HealthCare, Koninklijke Philips N.V., Aidoc, Viz.ai, Inc, Qure.ai, Recursion, Insilico Medicine, Abridge AI, Inc., Waystar, IBM, CitiusTech Inc, Tempus AI, Inc., Hippocratic AI, Solventum, and others. |

|

Artificial Intelligence (AI) in Healthcare Market Segments |

by Component, by Technology, by Deployment Mode, by Solution Type, by Application, by End-Users, and by Geography |

|

Artificial Intelligence (AI) in Healthcare Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Artificial Intelligence (AI) in Healthcare Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Artificial Intelligence (AI) in Healthcare Market Segmentation

Artificial Intelligence (AI) in Healthcare by Component Exposure

Hardware

Software Solutions

Services

Artificial Intelligence (AI) in Healthcare Technology Exposure

Deep Learning

Natural Language Processing

Machine Learning

Computer Vision & Image Recognition

Others

Artificial Intelligence (AI) in Healthcare Deployment Modes Exposure

On-Premises Models

Cloud-Based Models

Hybrid Deployment Models

Artificial Intelligence (AI) in Healthcare Solution Type Exposure

Diagnosis & Early Detection

Treatment Planning & Personalization

Patient Engagement & Remote Monitoring

Administrative Workflow Automation

Data Management & Analytics

Others

Artificial Intelligence (AI) in Healthcare Application Exposure

Medical Imaging and Diagnostics

Robot-Assisted Surgery & Surgical AI

Clinical Trial Acceleration & Drug Discovery

Virtual Assistants & Chatbots

Telemedicine & Remote Care

Others

Artificial Intelligence (AI) in Healthcare End-Users Exposure

Hospitals & Healthcare Providers

Pharmaceutical & Biotechnology Firms

Healthcare Payers & Insurance

Diagnostic Centers & Labs

Research & Academic Institutions

Patients & Caregivers

Artificial Intelligence (AI) in Healthcare Geography Exposure

North America Artificial Intelligence (AI) in Healthcare Market

United States Artificial Intelligence (AI) in Healthcare Market

Canada Artificial Intelligence (AI) in Healthcare Market

Mexico Artificial Intelligence (AI) in Healthcare Market

Europe Artificial Intelligence (AI) in Healthcare Market

United Kingdom Artificial Intelligence (AI) in Healthcare Market

Germany Artificial Intelligence (AI) in Healthcare Market

France Artificial Intelligence (AI) in Healthcare Market

Italy Artificial Intelligence (AI) in Healthcare Market

Spain Artificial Intelligence (AI) in Healthcare Market

Rest of Europe Artificial Intelligence (AI) in Healthcare Market

Asia-Pacific Artificial Intelligence (AI) in Healthcare Market

China Artificial Intelligence (AI) in Healthcare Market

Japan Artificial Intelligence (AI) in Healthcare Market

India Artificial Intelligence (AI) in Healthcare Market

Australia Artificial Intelligence (AI) in Healthcare Market

South Korea Artificial Intelligence (AI) in Healthcare Market

Rest of Asia-Pacific Artificial Intelligence (AI) in Healthcare Market

Rest of the World Artificial Intelligence (AI) in Healthcare Market

South America Artificial Intelligence (AI) in Healthcare Market

Middle East Artificial Intelligence (AI) in Healthcare Market

Africa Artificial Intelligence (AI) in Healthcare Market

Artificial Intelligence (AI) in Healthcare Market Recent Industry Trends and Milestones (2022-2026)

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Artificial Intelligence (AI) in Healthcare Market CAGR |

40.40% |

|

Key Companies in the Artificial Intelligence (AI) in Healthcare Market |

NVIDIA, Google (Alphabet), Microsoft, Amazon (AWS), Intel Corporation, Siemens Healthineers, GE HealthCare, Koninklijke Philips N.V., Aidoc, Viz.ai, Inc, Qure.ai, Recursion, Insilico Medicine, Abridge AI, Inc., Waystar, IBM, CitiusTech Inc, Tempus AI, Inc., Hippocratic AI, Solventum, and others. |

|

Artificial Intelligence (AI) in Healthcare Market Segments |

by Component, by Technology, by Deployment Mode, by Solution Type, by Application, by End-Users, and by Geography |

|

Artificial Intelligence (AI) in Healthcare Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Artificial Intelligence (AI) in Healthcare Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations and applications in healthcare are transforming the entire care continuum by enabling more accurate, efficient, and personalized medical services. AI is widely used in diagnostics and medical imaging, where advanced algorithms analyze X-rays, MRIs, and CT scans to detect diseases such as cancer and cardiovascular conditions at early stages with high precision. In clinical decision support, AI helps physicians interpret complex patient data and recommend optimized treatment plans, improving outcomes and reducing errors. AI is also revolutionizing drug discovery and development by accelerating target identification, predicting molecule behavior, and streamlining clinical trials, significantly reducing time and costs. Additionally, virtual health assistants and chatbots are enhancing patient engagement by providing real-time medical guidance, appointment scheduling, and symptom checking. In the area of remote patient monitoring and telemedicine, AI enables continuous tracking of patient health through wearable devices and predicts potential health risks for timely intervention. Furthermore, AI-driven workflow automation is reducing administrative burdens by automating tasks such as medical coding, billing, and clinical documentation. Emerging applications like personalized medicine, where AI tailors treatments based on genetic and clinical data, and robot-assisted surgeries, which enhance precision and minimize invasiveness, are further advancing healthcare delivery. Overall, these innovations are driving a shift toward more proactive, data-driven, and patient-centric healthcare systems.

U.S. Tariff Impact Analysis on Artificial Intelligence (AI) in Healthcare Market:

The U.S. tariff impact on the artificial intelligence (AI) in healthcare market is creating a mixed effect, but overall, it acts as a restraining and restructuring factor for market growth. Tariffs on imported medical devices, electronic components, and healthcare technologies significantly increase the cost of AI infrastructure, including imaging systems, sensors, and high-performance computing hardware required for AI applications. Since a large share of medical devices and components used in the U.S. are imported, these tariffs raise procurement and operational costs for hospitals and AI solution providers, thereby slowing adoption.

Additionally, tariffs are disrupting global supply chains, leading to delays in the availability of advanced AI-enabled medical technologies and forcing companies to reconsider sourcing and manufacturing strategies. At the same time, increased costs of semiconductors and computing hardware critical for AI model training and deployment are reducing investment efficiency and limiting the scalability of AI solutions, especially for startups and smaller healthcare providers.

However, these challenges are also pushing companies toward localized manufacturing, supply chain diversification, and greater adoption of digital and cloud-based AI solutions to reduce dependency on imported hardware. Overall, U.S. tariffs are acting as both a short-term barrier through increased costs and supply disruptions and a long-term structural driver, encouraging innovation, resilience, and strategic transformation within the AI in healthcare market.

How This Analysis Helps Clients

Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Abridge |

USD 250 million |

Late-stage (growth round) |

AI-powered medical documentation platform |

Natural Language Processing (NLP) & Generative AI for converting doctor–patient conversations into structured clinical notes |

Key takeaways from the artificial intelligence in Healthcare market report study

Market size analysis for the current artificial intelligence in healthcare market size (2025), and market forecast for 8 years (2026 to 2034)

Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

Key companies dominating the artificial intelligence in healthcare market.

Various opportunities available for the other competitors in the artificial intelligence in healthcare market space.

What are the top-performing segments in 2025? How these segments will perform in 2034?

Which are the top-performing regions and countries in the current artificial intelligence in healthcare market scenario?

Which are the regions and countries where companies should have concentrated on opportunities for artificial intelligence in healthcare market growth in the future?

Frequently Asked Questions for the Artificial Intelligence (AI) in Healthcare Market

1. What is the growth rate of artificial intelligence in healthcare market?

The artificial intelligence in healthcare market is estimated to grow at a CAGR of 40.40% during the forecast period from 2026 to 2034.

2. What is the market for artificial intelligence in healthcare?

The global artificial intelligence in healthcare market is expected to increase from USD 40,809.25 million in 2025 to USD 861,636.63 million by 2034.

3. Which region has the highest share in the artificial intelligence in healthcare market?

North America is expected to dominate the artificial intelligence in healthcare market due to its strong healthcare infrastructure, early adoption of advanced digital technologies, and significant investments in AI research and development. The region is also home to major technology companies and healthcare innovators, which accelerates the development and deployment of AI-driven solutions. Additionally, supportive government initiatives, increasing healthcare data availability, and growing demand for improved patient outcomes and cost efficiency further strengthen the market growth in North America.

4. What are the drivers for the artificial intelligence in healthcare market?

The rising prevalence of chronic diseases is increasing the demand for continuous monitoring, early diagnosis, and personalized treatment, which AI-powered tools can efficiently support. At the same time, the accelerating adoption of AI and advanced analytics in healthcare is improving clinical decision-making, operational efficiency, and predictive insights across hospitals and research settings. The expansion of digital health, telemedicine, and remote patient monitoring is further generating large volumes of real-time patient data, enabling AI systems to deliver timely interventions and virtual care solutions. Additionally, advances in machine learning, deep learning, and generative AI are enhancing diagnostic accuracy, drug discovery, and personalized medicine capabilities. Collectively, these factors are significantly driving the growth and transformation of the AI in healthcare market.

5. Who are the key players operating in the artificial intelligence in healthcare market?

Some of the key market players operating in the artificial intelligence in healthcare market include NVIDIA, Google (Alphabet), Microsoft, Amazon (AWS), Intel Corporation, Siemens Healthineers, GE HealthCare, Koninklijke Philips N.V., Aidoc, Viz.ai, Inc, Qure.ai, Recursion, Insilico Medicine, Abridge AI, Inc., Waystar, IBM, CitiusTech Inc, Tempus AI, Inc., Hippocratic AI, Solventum, and others.