Cervical Cancer Diagnostics Market Summary

- The global cervical cancer treatment market size is expected to increase from USD 8,965.42 million in 2025 to USD 14,433.40 million by 2034, reflecting strong and sustained growth.

- The global cervical cancer treatment market is growing at a CAGR of 5.48% during the forecast period from 2026 to 2034.

- The growth of the cervical cancer treatment market is being collectively driven by the rising global disease burden, widespread Human Papillomavirus (HPV) Infection, and rapid advancements in innovative therapies. The increasing incidence of cervical cancer, particularly in developing regions, is expanding the patient pool and creating sustained demand for effective treatment options. At the same time, the high prevalence of HPV, the primary causative factor, continues to contribute to new cases, ensuring a consistent need for therapeutic interventions. Complementing this demand, breakthroughs in targeted therapies and immunotherapies, such as Bevacizumab and Pembrolizumab, are improving survival outcomes and expanding treatment possibilities, especially for advanced and recurrent cases. Together, these factors are significantly accelerating market growth by increasing both the number of patients requiring treatment and the adoption of advanced, high-value therapies.

- The leading companies operating in the cervical cancer treatment market include F. Hoffmann-La Roche Ltd, Amgen Inc., Pfizer Inc., Merck & Co., Inc., Seagen Inc., Bristol-Myers Squibb, AstraZeneca plc, Eli Lilly and Company, Sanofi, Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Cipla Limited, GlaxoSmithKline plc, Novartis AG, Johnson & Johnson, Takeda Pharmaceutical Company, Gilead Sciences, Inc., Regeneron Pharmaceuticals, BeiGene Ltd.,, and others.

- North America is expected to dominate the Cervical Cancer treatment market due to its advanced healthcare infrastructure, high adoption of innovative therapies, and strong presence of leading pharmaceutical and biotechnology companies. The region benefits from widespread access to screening and early diagnosis, which increases the number of patients receiving timely treatment. Additionally, the rapid uptake of advanced treatment options such as immunotherapies like Pembrolizumab and targeted therapies such as Bevacizumab, along with favorable reimbursement policies and ongoing clinical research, further contribute to the region’s market leadership.

- In the cancer type segment of the cervical cancer treatment market, the squamous cell carcinoma category is estimated to account for the largest market share in 2025.

Cervical Cancer Diagnostics Market Size and Forecasts

|

Report Metrics |

Details |

|

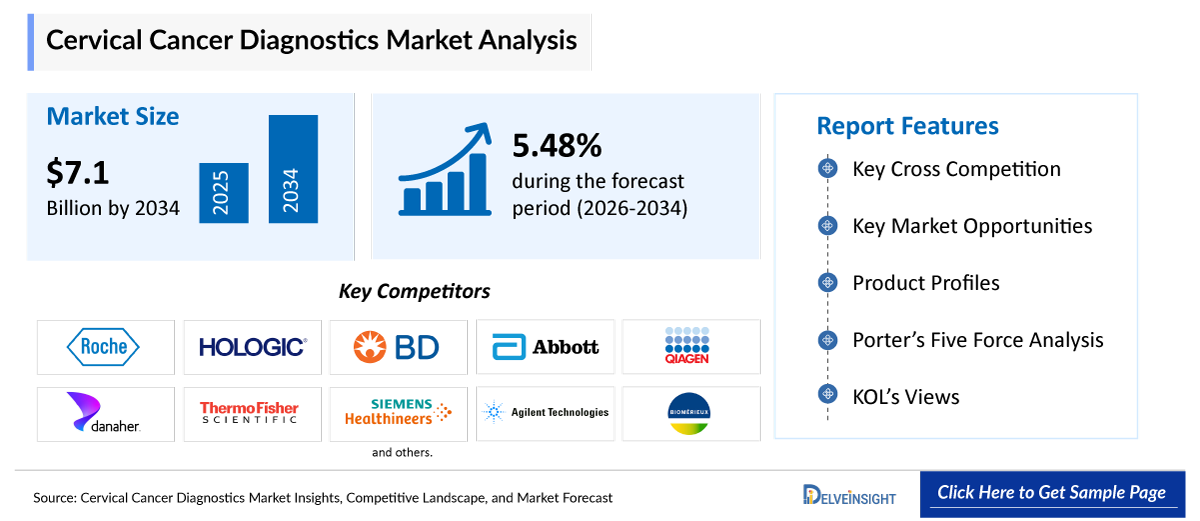

2025 Market Size |

USD 4,432.40 million |

|

2034 Projected Market Size |

USD 7,135.70 million |

|

Growth Rate (2026-2034) |

5.48% CAGR |

|

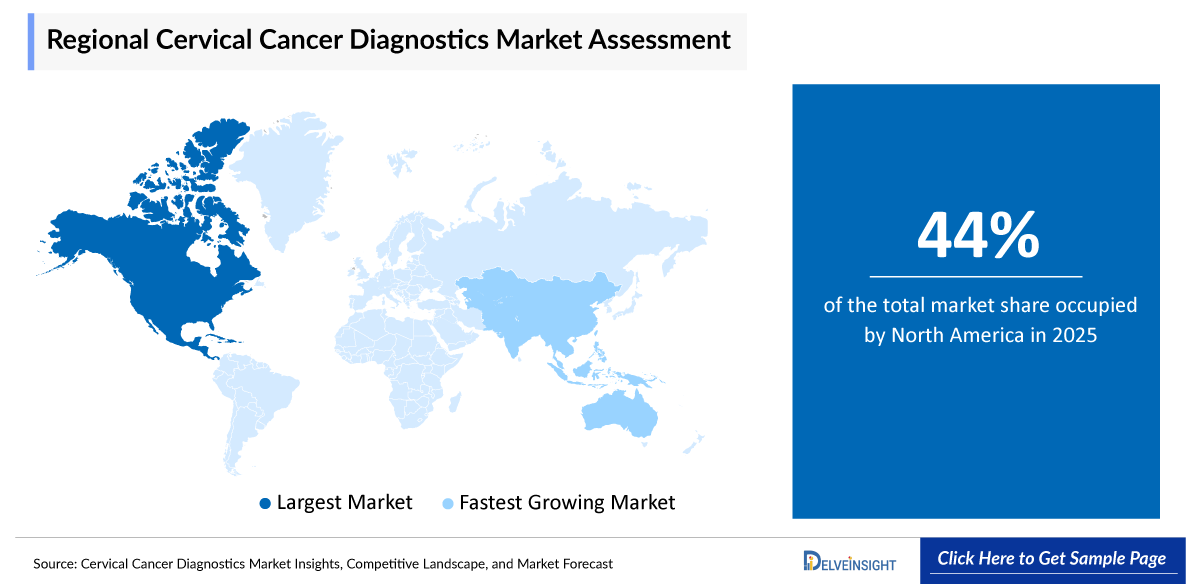

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Cervical Cancer Diagnostics Market

- Rising prevalence of cervical cancer leading to a surge in cervical cancer diagnostics: The increasing incidence of cervical cancer globally is a primary driver for diagnostics. Persistent infection with high-risk HPV strains remains the leading cause, especially in developing regions. According to the World Health Organization, cervical cancer is among the most common cancers in women worldwide. This growing disease burden is directly increasing demand for early screening, diagnostic confirmation, and monitoring tests, thereby boosting the market.

- Increasing adoption of HPV testing: There is a strong shift from conventional cytology (Pap tests) to HPV DNA and mRNA testing, which offer higher sensitivity and earlier detection. Regulatory bodies and screening guidelines now recommend primary HPV screening, especially for women aged 25–65. This transition is driving demand for molecular diagnostic kits, instruments, and automated platforms, significantly expanding market revenue.

- Government screening programs & awareness initiatives: Governments and global organizations are actively promoting cervical cancer screening through national programs. Initiatives such as mass screening campaigns, free Pap/HPV tests, and vaccination drives are increasing screening coverage. For example, the World Health Organization aims to eliminate cervical cancer through widespread screening and vaccination. Such initiatives are significantly increasing the volume of diagnostic tests performed globally.

Cervical Cancer Treatment Market Report Segmentation

This cervical cancer treatment market report offers a comprehensive overview of the global cervical cancer treatment market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Cancer Type (Squamous Cell Carcinoma, Adenocarcinoma, Adenosquamous Carcinoma, and Others), Treatment Type (Radiation Therapy, Chemotherapy, Targeted Therapy, and Immunotherapy), End-Users (Hospitals & Clinics, Cancer Research Institutes, and Others), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing cervical cancer treatment market.

Cervical cancer treatment refers to the range of medical therapies used to manage and eliminate Cervical Cancer, depending on its stage and severity. It typically includes a combination of surgery, radiation therapy, chemotherapy, targeted therapy, and immunotherapy aimed at destroying cancer cells, preventing disease progression, and improving patient survival outcomes. The choice of treatment is influenced by factors such as tumor size, extent of spread, and the patient’s overall health.

The growth of the Cervical Cancer treatment market is being collectively driven by the rising global disease burden, the widespread prevalence of Human Papillomavirus (HPV) Infection, and continuous advancements in innovative therapeutic approaches. The increasing incidence of cervical cancer, particularly in low- and middle-income countries where screening and vaccination coverage remain limited, is significantly expanding the patient pool and generating sustained demand for effective and accessible treatment options. In parallel, the high prevalence of HPV, which is the primary etiological factor responsible for the majority of cervical cancer cases, continues to drive new diagnoses each year, thereby ensuring a consistent and long-term need for therapeutic interventions across different stages of the disease.

Furthermore, rapid advancements in oncology, especially in targeted therapy and immunotherapy, are transforming the treatment landscape. Novel agents such as Bevacizumab, which inhibits tumor angiogenesis, and Pembrolizumab, which enhances the body’s immune response against cancer cells, have demonstrated improved clinical outcomes, particularly in advanced and recurrent cervical cancer cases. These therapies not only extend survival rates but also offer more personalized and effective treatment options, thereby increasing their adoption among healthcare providers. Collectively, these factors are accelerating market growth by simultaneously increasing the number of patients requiring treatment and driving the shift toward advanced, high-value, and combination-based therapeutic regimens.

What are the latest cervical cancer treatment market dynamics and trends?

The rising burden of cervical cancer and HPV Infections worldwide is significantly boosting the overall market of cervical cancer treatment.

According to the data provided by the International Agency for Research on Cancer (2025), in 2025, the estimated new cases of cervical cancer were 7,02,616, and the projections further estimated that these cases would rise to 9,08,612 by 2045.

Additionally, as per the data provided by the World Health Organization (2024), in 2019, HPV caused an estimated 6,20,000 cancer cases in women and 70,000 cancer cases in men. Persistent infection with high-risk HPV strains is the primary cause of most cervical cancer cases, leading to a continuous inflow of newly diagnosed patients who require medical intervention. This growing disease burden, especially in regions with limited screening and vaccination coverage, is driving demand for a wide range of treatment options. As the number of cases rises, there is increased utilization of chemotherapy drugs such as Cisplatin and Paclitaxel, which remain standard treatments across various stages. Additionally, the growing adoption of advanced therapies like Bevacizumab for inhibiting tumor blood vessel formation and Pembrolizumab for enhancing immune response is further expanding treatment possibilities, particularly in advanced or recurrent cases.

Additionally, the increasing product development activities, such as product launch, approvals, and successful clinical trials, are further escalating the overall market of cervical cancer treatment. For instance, in January, 2024, the FDA approved pembrolizumab (Keytruda) combined with chemoradiotherapy (CRT) for treating FIGO 2014 Stage III–IVA cervical cancer.

Thus, the factors mentioned above are expected to boost the overall market of cervical cancer treatment during the forecast period.

However, the late-stage diagnosis of cervical cancer, particularly in low- and middle-income countries, acts as a major limiting factor for the treatment market, as patients are often identified when the disease has already advanced, reducing the effectiveness of standard therapies and increasing dependence on complex, high-cost treatments that are not widely accessible. This not only lowers treatment success rates but also restricts overall market penetration due to limited affordability and infrastructure. In addition, stringent regulatory requirements and lengthy clinical trial timelines delay the approval and commercialization of new therapies, slowing the entry of innovative drugs into the market. As a result, despite ongoing advancements, these factors collectively hinder timely access to effective treatments and restrain the overall growth of the cervical cancer treatment market.

Cervical Cancer Treatment Market Segment Analysis

Cervical Cancer Treatment Market by Cancer Type (Squamous Cell Carcinoma, Adenocarcinoma, Adenosquamous Carcinoma, and Others), Treatment Type (Radiation Therapy, Chemotherapy, Targeted Therapy, and Immunotherapy), End-Users (Hospitals & Clinics, Cancer Research Institutes, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Cancer Type: Squamous cell carcinoma in cervical cancer treatment is expected to dominate the market with the largest revenue share

In the cancer type segment of the Cervical Cancer Treatment market, the Squamous Cell Carcinoma category is contributing to 67% of total market revenue in 2025, due to its high prevalence of all cervical cancer cases worldwide. According to recent studies (2023), Cervical squamous cell carcinoma (SCC) accounts for approximately 75% of all cervical cancer cases, with 662,301 new global cases in 2022. This dominance creates a large and consistent patient pool requiring diagnosis and treatment, thereby driving demand across multiple therapeutic segments. Squamous cell carcinoma is strongly associated with persistent Human Papillomavirus (HPV) Infection, particularly high-risk strains such as HPV-16, leading to a steady incidence rate, especially in developing regions. As a result, there is widespread use of standard chemotherapy regimens involving drugs like Cisplatin and Paclitaxel, often in combination with radiation therapy for locally advanced disease. Additionally, the growing adoption of advanced therapies such as Bevacizumab for inhibiting tumor angiogenesis and Pembrolizumab for immunotherapy in recurrent or metastatic cases is further contributing to market expansion. The high disease burden, combined with the availability and increasing use of both conventional and innovative treatment options, makes squamous cell carcinoma a key driver of growth in the cervical cancer treatment market.

Thus, the factors mentioned above are expected to boost the category and thereby escalate the overall market of cervical cancer treatment during the forecast period.

By Treatment Type: Chemotherapy category dominates the market

Within the treatment type segment of the cervical cancer treatment market, the chemotherapy category is anticipated to dominate, accounting for around 37% of the market share in 2025, due to its extensive use as the standard and foundational treatment across all stages of the disease. Chemotherapy remains the primary therapeutic approach for both early-stage patients requiring adjuvant therapy and for those with locally advanced or metastatic disease, where it is commonly used in combination with radiation therapy (chemoradiation). Its dominance is largely driven by its broad clinical applicability, established efficacy, and relatively lower cost compared to newer biologics, making it widely accessible, especially in developing regions with a high disease burden. Commonly used chemotherapy agents include Cisplatin, which is considered the gold standard in concurrent chemoradiation, as well as Paclitaxel and Carboplatin, which are frequently used in combination regimens for advanced or recurrent cervical cancer. Other drugs such as Topotecan and Gemcitabine are also utilized in second-line or combination therapies, further expanding the chemotherapy segment.

Additionally, even with the rapid advancement of targeted therapy and immunotherapy, chemotherapy continues to play a central and indispensable role in combination-based treatment regimens, where newer agents are often administered alongside traditional cytotoxic drugs rather than replacing them. This ensures sustained high demand for chemotherapy drugs within clinical practice. The large patient population, frequent treatment cycles, and integration into multi-modality treatment protocols collectively reinforce chemotherapy’s leading position, making it the most dominant segment in the cervical cancer treatment market.

By End-Users: Hospitals & Clinics Category Dominates the Market

In the end-users segment of the cervical cancer treatment market, the hospitals & clinics category dominates due to the availability of advanced diagnostic infrastructure, skilled healthcare professionals, and the ability to provide comprehensive cervical cancer screening and follow-up care in a single setting. Hospitals are well-equipped to perform Cervical Cancer Treatment, along with confirmatory procedures such as colposcopy and biopsy for patients diagnosed with abnormalities related to Human papillomavirus. Additionally, the high patient inflow, integration with government screening programs, and access to reimbursement facilities further strengthen the dominance of hospitals in delivering large-scale and reliable screening services, thereby making hospitals a dominant category in the end-users segment.

Cervical Cancer Treatment Market Regional Analysis

North America Cervical Cancer Treatment Market Trends

North America is expected to account for the highest proportion of 41% of the cervical cancer treatment market in 2025, out of all regions. North America is expected to dominate the cervical cancer treatment market due to its advanced healthcare infrastructure, high adoption of innovative therapies, and strong presence of leading pharmaceutical and biotechnology companies. The region benefits from widespread access to screening and early diagnosis, which increases the number of patients receiving timely treatment. Additionally, the rapid uptake of advanced treatment options such as immunotherapies like Pembrolizumab and targeted therapies such as Bevacizumab, along with favorable reimbursement policies and ongoing clinical research, further contribute to the region’s market leadership.

According to the data provided by the American Cancer Society (2026), in 2026, about 13,490 new cases of invasive cervical cancer will be diagnosed in 2026, in the United States, and 4,200 women will die from cervical cancer.

Additionally, according to the data provided by the Centre for Disease Control and Prevention (2025), 39,300 cancers (79%) were attributable to HPV each year during 2018 to 2022 in the United States.

Moreover, growing awareness and government screening programs are significantly boosting the Cervical Cancer Treatment market in North America by increasing participation in routine cervical cancer screening and improving early detection rates. Initiatives such as Cervical Cancer Awareness Month (January 2026) in Canada actively encourage women to stay up to date with screening and highlight the importance of early treatment. In the United States, updated guidelines by organizations like the American Cancer Society in 2025 promoting HPV treatment have further improved screening accessibility and compliance.

However, the increase in product development activities among the key market players is further boosting the overall market. For instance, in April 2024, the FDA granted full approval to Tisotumab Vedotin (Tivdak) for patients with recurrent or metastatic cervical cancer progressing after chemotherapy.

Collectively, these factors are expected to significantly drive the growth of the cervical cancer treatment market in the U.S. throughout the forecast period of 2026 to 2034.

Europe Cervical Cancer Treatment Market Trends

The cervical cancer treatment market in Europe is witnessing strong and sustained growth due to the rising burden of cervical cancer. According to the data provided by the HPV Information Centre (2023), the estimates indicated that every year, 58,169 women were diagnosed with cervical cancer, and 25,989 would die from the disease in Europe.

Additionally, the Cervical Cancer treatment market in Europe is witnessing strong and sustained growth driven by advanced healthcare infrastructure, increasing adoption of innovative therapies, and continuous regulatory support for novel oncology drugs. The region benefits from well-established screening programs, high awareness levels, and strong reimbursement frameworks, which facilitate early diagnosis and timely access to treatment. Moreover, the growing burden of cervical cancer, particularly among aging female populations, is further increasing demand for effective therapies. A major contributor to this growth is the rapid expansion of immunotherapy and targeted treatment options approved by regulatory authorities such as the European Commission. For instance, in March 2025, Tisotumab Vedotin (Tivdak) received marketing authorization in the European Union for recurrent or metastatic cervical cancer, further expanding treatment options. Furthermore, in November, 2025, a subcutaneous formulation of Pembrolizumab was approved across Europe, improving administration convenience and patient compliance. These continuous approvals and innovations, combined with strong clinical research activity and healthcare accessibility, are collectively driving robust growth in the cervical cancer treatment market across Europe.

Asia-Pacific Cervical Cancer Treatment Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the Cervical Cancer treatment market due to a combination of rising disease burden, improving healthcare systems, and increasing government initiatives. According to the data provided by the International Agency for Research on Cancer (2026), in 2025, the estimated new cases of cervical cancer in India were 1,38,871, and the projections further estimated that these cases would rise to 2,12,623 by 2045.

Additionally, the region has a significantly large and growing patient population, with countries such as India, China, and Southeast Asian nations reporting high incidence rates, largely driven by widespread Human Papillomavirus (HPV) Infection and limited early screening in rural areas. This expanding patient pool is creating strong demand for both conventional therapies and advanced treatment options. Furthermore, improving healthcare infrastructure, rising healthcare expenditure, and expanding access to oncology services are enabling greater adoption of treatments, including chemotherapy, targeted therapy, and immunotherapy. Governments across the region are also actively promoting HPV vaccination programs, awareness campaigns, and national screening initiatives, which are increasing diagnosis rates and subsequently driving treatment demand. Furthermore, economic development and growing awareness among women are encouraging early medical intervention, while the introduction of advanced technologies and therapies is transforming treatment outcomes.

Who are the major players in the cervical cancer diagnostics market?

- F. Hoffmann-La Roche Ltd.

- Hologic, Inc.

- Becton, Dickinson and Company

- Abbott Laboratories

- Qiagen N.V.

- Danaher Corporation

- Thermo Fisher Scientific

- Siemens Healthineers

- Agilent Technologies

- bioMérieux SA

- Bio-Rad Laboratories

- Illumina, Inc.

- Myriad Genetics

- PerkinElmer, Inc.

- Sysmex Corporation

- Olympus Corporation

- Carl Zeiss Meditec AG

- Leisegang GmbH

- CooperSurgical Inc.

- MobileODT Ltd, and others

How is the competitive landscape shaping the cervical cancer diagnostics market?

Recent Developmental Activities in the Cervical Cancer Diagnostics Market

- In April 2026, Waters Corporation announced that the U.S. Food and Drug Administration (FDA) had cleared the Onclarity HPV Self-Collection Kit and approved the BD Onclarity HPV Assay with extended genotyping for at-home use, marking a significant milestone in expanding access to cervical cancer screening and removing barriers that currently prevent many individuals from receiving routine screening.

- In February 2026, Hologic, Inc. announced that its Aptima® HPV Assay received FDA approval for clinician-collected HPV primary screening. Hologic’s human papillomavirus (HPV) test is the only FDA-approved mRNA-based assay, designed specifically to detect infections most likely to lead to cervical cancer.

- In January 2026, Teal Health, a virtual women’s health company on a mission to eliminate cervical cancer in the U.S., announced the national availability of its at-home cervical cancer screening (PAP Test), which included the FDA-authorized Teal WandTM self-collection device and comprehensive telehealth platform. Cervical cancer screening, often referred to as the Pap smear, is a recommended screening for women ages 25-65.

- In April, 2025, Quest Diagnostics launched an FDA-cleared HPV self-collection service, allowing women to collect their own samples for high-risk HPV testing within clinical settings.

- In May, 2024, the U.S. Food and Drug Administration (FDA) approved a significant expansion for F. Hoffmann-La Roche’s cobas® HPV test, allowing it to be used with self-collected vaginal samples for cervical cancer screening.

- In May, 2024, the U.S. Food and Drug Administration (FDA) approved a significant expansion to the indications for use (IFU) of the BD Onclarity™ HPV Assay (PMA P160037/S017). This update allows for vaginal self-collection of specimens in a clinical setting (such as a pharmacy or doctor's office) when traditional clinician-collected cervical samples are not possible.

- In May 2024, the U.S. FDA expanded approvals for HPV tests, such as those from Becton Dickinson and F. Hoffmann-La Roche, to include self-collected samples, increasing overall screening participation and subsequently driving the need for follow-up Pap cytology.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Cervical Cancer Diagnostics Market CAGR |

5.48% |

|

Key Companies in the Cervical Cancer Diagnostics Market |

F. Hoffmann-La Roche Ltd, Hologic, Inc., Becton, Dickinson and Company, Abbott Laboratories, Qiagen N.V., Danaher Corporation, Thermo Fisher Scientific, Siemens Healthineers, Agilent Technologies, bioMérieux SA, Bio-Rad Laboratories, Illumina, Inc., Myriad Genetics, PerkinElmer, Inc., Sysmex Corporation, Olympus Corporation, Carl Zeiss Meditec AG, Leisegang GmbH, CooperSurgical Inc., MobileODT Ltd., and others. |

|

Cervical Cancer Diagnostics Market Segments |

by Test Type, by Product Type, by Age Group, by End-Users, and by Geography |

|

Cervical Cancer Diagnostics Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Cervical Cancer Diagnostics Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Cervical Cancer Diagnostics Market Segmentation

- Cervical Cancer Diagnostics by Test Type Exposure

- Pap Test

- HPV Testing

- Colposcopy

- Cervical Biopsy

- Others

- Cervical Cancer Diagnostics Product Type Exposure

- Instruments

- Consumables

- Software

- Cervical Cancer Diagnostics Age Group Exposure

- 20–40 Years

- Above 40 Years

- Cervical Cancer Diagnostics End-Users Exposure

- Hospitals

- Diagnostic Centres

- Others

- Cervical Cancer Diagnostics Geography Exposure

- North America Cervical Cancer Diagnostics Market

- United States Cervical Cancer Diagnostics Market

- Canada Cervical Cancer Diagnostics Market

- Mexico Cervical Cancer Diagnostics Market

- Europe Cervical Cancer Diagnostics Market

- United Kingdom Cervical Cancer Diagnostics Market

- Germany Cervical Cancer Diagnostics Market

- France Cervical Cancer Diagnostics Market

- Italy Cervical Cancer Diagnostics Market

- Spain Cervical Cancer Diagnostics Market

- Rest of Europe Cervical Cancer Diagnostics Market

- Asia-Pacific Cervical Cancer Diagnostics Market

- China Cervical Cancer Diagnostics Market

- Japan Cervical Cancer Diagnostics Market

- India Cervical Cancer Diagnostics Market

- Australia Cervical Cancer Diagnostics Market

- South Korea Cervical Cancer Diagnostics Market

- Rest of Asia-Pacific Cervical Cancer Diagnostics Market

- Rest of the World Cervical Cancer Diagnostics Market

- South America Cervical Cancer Diagnostics Market

- Middle East Cervical Cancer Diagnostics Market

- Africa Cervical Cancer Diagnostics Market

- North America Cervical Cancer Diagnostics Market

Cervical Cancer Diagnostics Market Recent Industry Trends and Milestones (2023-2026)

|

Category |

Key Developments |

|

Cervical Cancer Diagnostics Product Approval |

Hologic, Inc.: Aptima® HPV Assay (FDA approval), F. Hoffmann-La Roche: cobas® HPV test (FDA approval) |

|

Cervical Cancer Diagnostics Partnership |

Roche Diagnostics partnered with Metropolis Healthcare, Hologic Inc. partnered with Clinton Health Access Initiative, and MedAccess. |

|

Company Strategy |

F. Hoffmann-La Roche: Focusing on global partnerships and accessibility expansion, collaborating with healthcare systems in over 55 countries to scale cervical cancer screening programs. Hologic Inc.: Strengthening its leadership through end-to-end cervical health solutions, combining Pap and HPV testing (co-testing) into integrated workflows. |

|

Emerging Technology |

Self-Sampling HPV Testing, Artificial Intelligence (AI)-Based Cytology, Next-Generation Sequencing (NGS), CRISPR-Based Diagnostics, Liquid Biopsy (Non-Invasive Testing), Isothermal Amplification (LAMP Technology), and others |

Impact Analysis

AI-Powered Innovations and Applications:

U.S. Tariff Impact Analysis on Cervical Cancer Diagnostics Market:

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Phase Scientific |

$34M |

Series A |

Urine-based HPV test (Indicaid platform) |

Urine-based diagnostics + Phasify biomarker amplification technology. |

Key takeaways from the cervical cancer diagnostics market report study

- Market size analysis for the current cervical cancer diagnostics market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the cervical cancer diagnostics market.

- Various opportunities available for the other competitors in the cervical cancer diagnostics market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current cervical cancer diagnostics market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the cervical cancer diagnostics market growth in the future?