Colorectal Cancer Diagnostics and Therapeutics Market Summary

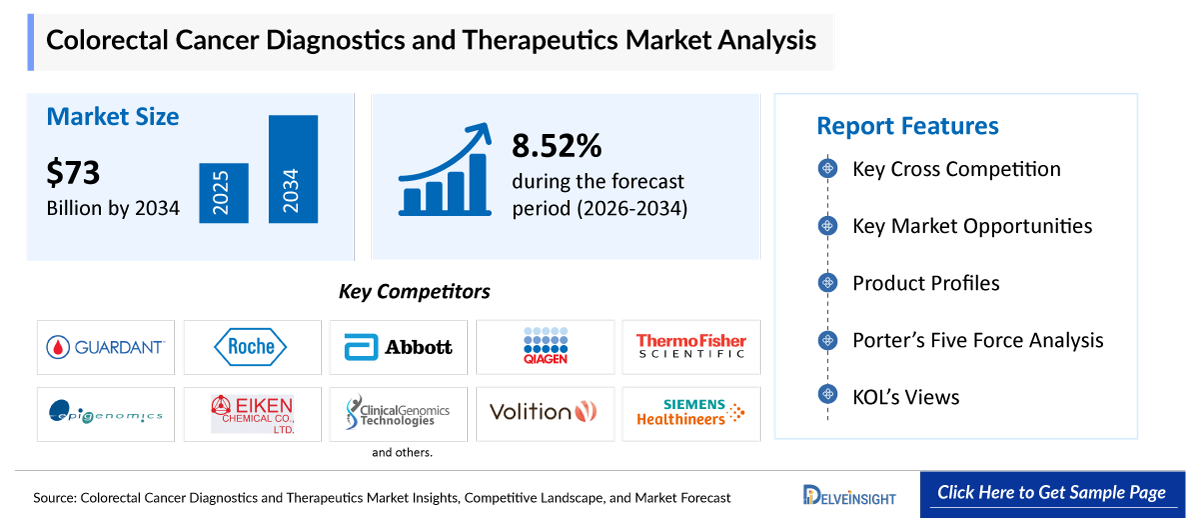

- The Global Colorectal Cancer Diagnostics and Therapeutics Market is expected to increase from USD 35,146.54 million in 2025 to USD 73,021.39 million by 2034, reflecting strong and sustained growth.

- The Global Colorectal Cancer Diagnostics and Therapeutics Market is growing at a CAGR of 8.52% during the forecast period from 2026 to 2034.

Colorectal Cancer Diagnostics and Therapeutics Market Insights & Forecast

- The rising prevalence of Colorectal Cancer is significantly increasing the demand for both early detection and effective treatment solutions, creating a strong foundation for market growth. At the same time, advancements in molecular diagnostics and precision medicine are enabling more accurate identification of genetic mutations and tumor characteristics, allowing clinicians to tailor personalized treatment strategies.

- This is further complemented by the increasing use of targeted therapies and immunotherapies, such as Pembrolizumab, which offer improved efficacy and better patient outcomes compared to conventional treatments. Additionally, continuous technological advancements in diagnostic modalities including liquid biopsy, AI-driven imaging, and next-generation sequencing are enhancing early detection, accuracy, and convenience. Collectively, these factors are driving higher adoption of integrated diagnostic and therapeutic approaches, thereby accelerating the overall Colorectal Cancer Diagnostics and Therapeutics market growth.

- The leading Colorectal Cancer Diagnostics and Therapeutics Companies such as Exact Sciences Corporation, Guardant Health, F. Hoffmann-La Roche Ltd., Abbott Laboratories, QIAGEN, Illumina, Inc., Thermo Fisher Scientific, Epigenomics AG, Eiken Chemical Co., Ltd., Clinical Genomics Technologies, VolitionRx Ltd., Siemens Healthineers, Olympus Corporation, Fujifilm Holdings Corporation, Medtronic plc, Merck & Co., Inc., Bristol-Myers Squibb, Amgen Inc., Eli Lilly and Company, F. Hoffmann-La Roche Ltd, Sanofi, Pfizer Inc., Bayer AG, Johnson & Johnson, Taiho Pharmaceutical, and others.

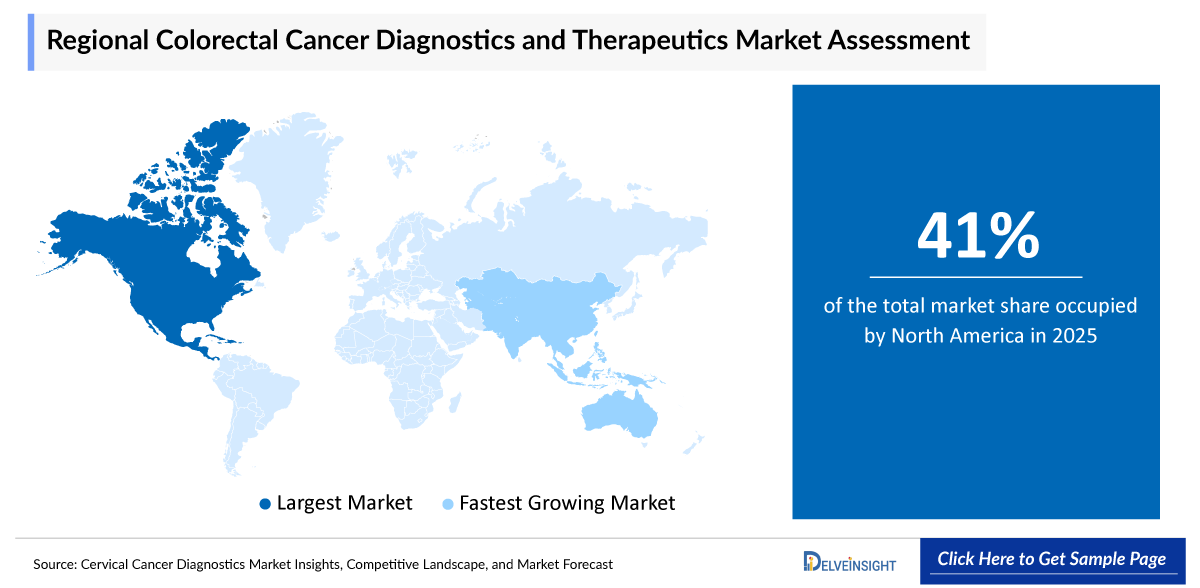

- North America is expected to dominate the Colorectal Cancer Diagnostics and Therapeutics market due to the high prevalence of colorectal cancer, well-established healthcare infrastructure, and strong presence of leading pharmaceutical and diagnostic companies. The region also benefits from widespread adoption of advanced screening technologies, such as molecular diagnostics and targeted therapies, along with favorable reimbursement policies. Additionally, increasing awareness programs and government initiatives promoting early cancer detection further contribute to market growth in North America.

- In the modality segment of the Colorectal Cancer Diagnostics and Therapeutics market, the diagnostic category is estimated to account for the largest market share in 2025.

Request for Unlocking the report of the @ Colorectal Cancer Diagnostics and Therapeutics Market

Colorectal Cancer Diagnostics and Therapeutics Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size | |

|

2034 Projected Market Size | |

|

Growth Rate (2026-2034) | |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Colorectal Cancer Diagnostics and Therapeutics Market

-

Rising prevalence of colorectal cancer leading to a surge in Colorectal Cancer Diagnostics and Therapeutics

The increasing global burden of colorectal cancer is a major growth driver. Sedentary lifestyles, unhealthy diets, obesity, and aging populations are contributing to higher incidence rates. As more cases are diagnosed each year, the demand for both early diagnostic tools and advanced treatment options continues to rise.

-

Advancements in molecular diagnostics & precision medicine

Innovations in genetic profiling (KRAS, NRAS, BRAF, MSI) are transforming treatment selection. The rise of personalized medicine enables clinicians to tailor therapies based on tumor biology, increasing demand for companion diagnostics and biomarker testing platforms. This trend is accelerating the integration of diagnostics with therapeutics.

-

Increasing use of targeted therapy and immunotherapy

The shift from traditional chemotherapy to advanced therapies is boosting the therapeutics segment. Targeted drugs (EGFR, VEGF Inhibitors) and immunotherapies like Pembrolizumab and Nivolumab therapies offer improved outcomes and fewer side effects, driving higher adoption and market growth.

-

Technological advancements in diagnostic modalities

Continuous innovation in diagnostic tools is enhancing accuracy and convenience. Liquid biopsy (minimally invasive testing), AI-powered imaging and colonoscopy, and Next-generation sequencing (NGS) technologies are improving early detection rates and boosting market expansion.

Colorectal Cancer Diagnostics and Therapeutics Market Report Segmentation

This Colorectal Cancer Diagnostics and Therapeutics market report offers a comprehensive overview of the global Colorectal Cancer Diagnostics and Therapeutics market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Modality (Diagnostics {Blood Test, Stool Test, Imaging Test, Biopsy, and Others} and Therapeutics {Chemotherapy, Immunotherapy, Targeted Therapy, and Others}), End-Users (Hospitals, Diagnostic Laboratories, Cancer Research Institutes, and Others), and geography.

The Colorectal Cancer Diagnostics and Therapeutics Market Report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing Colorectal Cancer Diagnostics and Therapeutics market.

Colorectal Cancer Diagnostics and Therapeutics refer to the range of medical approaches used to detect, diagnose, and treat cancers of the colon and rectum. Diagnostics include screening and testing methods such as colonoscopy, imaging, and molecular or genetic tests to identify cancer at an early stage. Therapeutics involve treatment options like surgery, chemotherapy, radiation therapy, targeted therapy, and immunotherapy aimed at eliminating cancer cells and improving patient outcomes. Together, these solutions play a crucial role in early detection, effective treatment, and management of colorectal cancer.

The rising prevalence of colorectal cancer is significantly increasing the demand for both early detection and effective treatment solutions, thereby creating a strong foundation for sustained market growth. As the global burden of the disease continues to rise driven by aging populations, sedentary lifestyles, and dietary factors there is a growing emphasis on routine screening and timely diagnosis to reduce mortality rates. At the same time, advancements in molecular diagnostics and precision medicine are transforming the clinical landscape by enabling more accurate identification of genetic mutations, biomarkers, and tumor-specific characteristics. This allows clinicians to design highly personalized treatment strategies tailored to individual patient profiles, improving treatment effectiveness.

Furthermore, the increasing adoption of targeted therapies and immunotherapies, such as Pembrolizumab, is revolutionizing colorectal cancer treatment by offering higher efficacy, fewer side effects, and improved survival outcomes compared to traditional chemotherapy. These therapies specifically target cancer cells or enhance the body’s immune response, making them a preferred option in many advanced cases. In parallel, continuous technological advancements in diagnostic modalities including liquid biopsy, AI-driven imaging, and next-generation sequencing are significantly enhancing early detection, diagnostic accuracy, and procedural convenience. These innovations also support non-invasive or minimally invasive testing, further encouraging patient compliance.

Collectively, the convergence of increasing disease prevalence, rapid technological innovation, and the shift toward personalized and targeted treatment approaches is driving the widespread adoption of integrated diagnostic and therapeutic solutions. This, in turn, is accelerating the overall growth and evolution of the Colorectal Cancer Diagnostics and Therapeutics market.

Get More Insights into the Report @ Colorectal Cancer Diagnostics and Therapeutics Market

What are the latest Colorectal Cancer Diagnostics and Therapeutics Market Dynamics and Trends?

The rising prevalence of colorectal cancer and increasing adoption of targeted therapies and immunotherapies, among others are boosting the overall market of colorectal cancer diagnostic and therapeutics market.

According to the data provided by the International Agency for Research on Cancer (2025), in 2025, the global estimated new cases of colorectal cancer was 2.06 million, and the projections further estimated that these cases would rise upto 3.29 million by 2045. The increasing Incidence of Colorectal Cancer is a key factor driving the growth of the Colorectal Cancer Diagnostics and Therapeutics market. As more patients are diagnosed each year, there is a rising demand for early screening tools such as colonoscopy, molecular diagnostics, and imaging technologies to enable timely detection.

At the same time, the growing patient pool is increasing the need for effective treatment options, including surgery, chemotherapy, targeted therapy, and immunotherapy. This continuous demand for both advanced diagnostic solutions and innovative treatment approaches is significantly boosting the overall market growth.

Additionally, the advancements in molecular diagnostics and precision medicine are significantly boosting the Colorectal Cancer Diagnostics and Therapeutics market by enabling highly accurate, personalized, and targeted approaches to disease management. Modern molecular diagnostic techniques such as next-generation sequencing (NGS), biomarker testing, and liquid biopsy allow clinicians to identify specific genetic mutations (e.g., KRAS, MSI-H/dMMR), which helps in selecting the most effective therapy for each patient.

For instance, liquid biopsy has emerged as a minimally invasive tool that can detect circulating tumor DNA and monitor disease progression in real time, improving early detection and treatment decision-making. These advancements are closely integrated with precision medicine, where therapies are tailored based on an individual’s tumor profile, leading to improved clinical outcomes and reduced unnecessary treatments.

In addition, several recent development activities are accelerating market growth. In July 2024, the FDA approved Shield, a groundbreaking blood-based screening test developed by Guardant Health for the early detection of colorectal cancer. On the therapeutic side, in June 2024, accelerated approval was granted for adagrasib (KRAS G12C inhibitor) in combination with cetuximab for advanced colorectal cancer, highlighting the shift toward targeted therapies.

Furthermore, in January 2025, Lumakras (sotorasib) in combination with Vectibix was approved for treating KRAS-mutated colorectal cancer, reinforcing the importance of molecular profiling in guiding treatment decisions. Additionally, companion diagnostics such as MMR IHC panels received approvals in August 2025, enabling better identification of patients eligible for immunotherapies.

Collectively, these innovations in molecular diagnostics and precision medicine are transforming colorectal cancer care by improving early detection, enabling targeted therapies, and enhancing patient outcomes, thereby driving strong growth in the overall Colorectal Cancer Diagnostics and Therapeutics market.

Thus, the factors mentioned above are expected to boost the overall Colorectal Cancer Diagnostics and Therapeutics Market during the forecast period.

However, complex regulatory approval processes and the presence of side effects and resistance to therapies are collectively acting as significant restraints on the Colorectal Cancer Diagnostics and Therapeutics market. Stringent regulatory requirements often lead to prolonged approval timelines for new diagnostic tools and targeted treatments, delaying their commercialization and limiting patient access. At the same time, the risk of adverse effects and the development of resistance to therapies—particularly in targeted and immunotherapy treatments—can reduce treatment effectiveness and patient compliance. Together, these factors hinder the rapid adoption of innovative solutions and slow down overall market growth..

Colorectal Cancer Diagnostics and Therapeutics Market Segment Analysis

Colorectal Cancer Diagnostics and Therapeutics Market by Modality (Diagnostics {Blood Test, Stool Test, Imaging Test, Biopsy, and Others} and Therapeutics {Chemotherapy, Immunotherapy, Targeted Therapy, and Others}), End-Users (Hospitals, Diagnostic Laboratories, Cancer Research Institutes, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Modality: Imaging Test under the diagnostic category in Colorectal Cancer Diagnostics and Therapeutics is expected to dominate the market with the largest revenue share

In the modality segment of the Colorectal Cancer Diagnostics and Therapeutics market, the imaging test under the diagnostic category, is contributing to 48% of total market revenue in 2025, due to their ability to provide accurate visualization, early detection, and disease staging. Imaging modalities such as CT colonography (virtual colonoscopy), MRI, and advanced endoscopic imaging are increasingly being adopted as they offer non-invasive or minimally invasive alternatives to conventional procedures.

Recent advancements, including AI-assisted imaging and deep learning–based detection systems, have significantly improved the accuracy of polyp and tumor detection, reduced missed lesions, and enhanced diagnostic efficiency. For instance, AI-assisted colonoscopy systems have demonstrated a notable increase in adenoma detection rates, thereby improving early diagnosis and clinical outcomes. Additionally, technological improvements in CT imaging such as dual-energy CT, spectral imaging, and deep-learning reconstruction have enhanced image quality, reduced radiation exposure, and enabled better differentiation between benign and malignant lesions.

Furthermore, recent development activities are accelerating the adoption of imaging-based diagnostics.

For instance, in May 2024, Geneoscopy, Inc., a life sciences company focused on developing diagnostic tests for the advancement of gastrointestinal health, announced that the U.S. Food and Drug Administration (FDA) approved its noninvasive colorectal cancer screening test, ColoSense. ColoSense is indicated as a screening test for adults, 45 years of age or older, who are at typical average risk for developing CRC.

Thus, the factors mentioned above are expected to boost the market of segment thereby boosting the overall market of Colorectal Cancer Diagnostics and Therapeutics.

By End-Users: Hospitals category dominates the market

Within the end-users segment of the Colorectal Cancer Diagnostics and Therapeutics market, the hospitals category is anticipated to dominate due to the availability of advanced diagnostic infrastructure, specialized oncology departments, and skilled healthcare professionals. Hospitals handle a high volume of colorectal cancer cases, ranging from screening and diagnosis to complex surgical procedures and advanced therapies such as chemotherapy, targeted therapy, and immunotherapy. Additionally, the presence of multidisciplinary care teams and better reimbursement support further strengthens the preference for hospital-based treatment, thereby driving the dominance of this segment.

Colorectal Cancer Diagnostics and Therapeutics Market Regional Analysis

North America Colorectal Cancer Diagnostics and Therapeutics Market Trends

North America is expected to account for the highest proportion of 41% of the Colorectal Cancer Diagnostics and Therapeutics Market in 2025, out of all regions. North America is expected to dominate the Colorectal Cancer Diagnostics and Therapeutics market due to the high prevalence of colorectal cancer, well-established healthcare infrastructure, and strong presence of leading pharmaceutical and diagnostic companies. The region also benefits from widespread adoption of advanced screening technologies, such as molecular diagnostics and targeted therapies, along with favorable reimbursement policies. Additionally, increasing awareness programs and government initiatives promoting early cancer detection further contribute to market growth in North America.

According to the data provided by the International Agency for Research on Cancer (2026), in 2025, the estimated new cases of colorectal cancer was 195,000 and the projections further estimated that these new cases would rise upto 250,000 by 2045 in North America. As more patients are diagnosed each year, there is a rising demand for early screening tools such as colonoscopy, molecular diagnostics, and imaging technologies to enable timely detection. At the same time, the growing patient pool is increasing the need for effective treatment options, including surgery, chemotherapy, targeted therapy, and immunotherapy, thus boosting the overall market of colorectal cancer diagnostic and therapeutic market across the region.

Additionally, the increasing use of targeted therapy and immunotherapy, along with rapid technological advancements in diagnostic modalities, is significantly boosting the Colorectal Cancer Diagnostics and Therapeutics market. The growing adoption of precision-based treatments such as immune checkpoint inhibitors and targeted biologics has improved survival rates and treatment outcomes, encouraging wider clinical use. These therapies rely heavily on advanced diagnostic tools, including molecular testing, next-generation sequencing, and biomarker analysis, to identify specific mutations (e.g., MSI-H/dMMR), thereby driving demand for sophisticated diagnostic platforms.

At the same time, technological advancements such as AI-powered imaging, liquid biopsy, and high-resolution endoscopy are enhancing early detection, diagnostic accuracy, and real-time disease monitoring. This strong integration between advanced diagnostics and personalized therapeutics is accelerating treatment efficiency and increasing adoption across healthcare systems in North America.

Furthermore, recent development activities are reinforcing this growth. In April, 2025, the U.S. FDA approved the combination of Nivolumab (Opdivo) and Ipilimumab (Yervoy) as a first-line treatment for unresectable or metastatic MSI-H/dMMR colorectal cancer, marking a significant advancement in immunotherapy-based treatment options. This approval demonstrated superior progression-free survival compared to conventional therapies, establishing immunotherapy combinations as a new standard of care.

In addition, the continued expansion of immunotherapy formulations, such as the subcutaneous version of Pembrolizumab approved in September 2025, is improving treatment convenience and accessibility for patients. These approvals and innovations are accelerating the shift toward personalized and minimally invasive cancer management, thereby significantly driving the growth of the Colorectal Cancer Diagnostics and Therapeutics market in North America.

Collectively, these factors are expected to significantly drive the growth of the Colorectal Cancer Diagnostics and Therapeutics Market in the U.S. throughout the forecast period of 2026 to 2034.

Europe Colorectal Cancer Diagnostics and Therapeutics Market Trends

The Colorectal Cancer Diagnostics and Therapeutics Market in Europe is witnessing strong and sustained growth due to the rising disease burden, aging population, and continuous advancements in healthcare infrastructure and oncology research. Europe has a well-established healthcare system with widespread access to screening programs, including colonoscopy and molecular diagnostics, which supports early detection and timely treatment. Additionally, increasing adoption of targeted therapies, immunotherapies, and precision medicine approaches is significantly improving patient outcomes and driving demand for advanced diagnostic tools.

The presence of leading pharmaceutical companies and strong clinical research networks such as collaborative initiatives across multiple European countries further accelerates innovation and adoption of new technologies. Moreover, growing awareness programs and government-supported cancer screening initiatives are encouraging early diagnosis, thereby contributing to consistent market expansion. The market is also supported by steady growth projections, with increasing investment in oncology care and evolving treatment practices across countries like Germany, France, and the UK.

Furthermore, recent development activities are reinforcing this growth trajectory. In June 2024, the European Commission approved fruquintinib, a targeted therapy, for patients with metastatic colorectal cancer who have previously received standard treatments, highlighting the shift toward advanced precision-based therapies. Additionally, in December 2024, a novel immunotherapy-based combination regimen received approval in Europe as a first-line treatment for advanced colorectal cancer, further strengthening the role of immunotherapy in clinical practice.

On the diagnostic front, in September 2025, the EU certified the MMR IHC Panel pharmDx as a companion diagnostic to identify patients eligible for immunotherapy combinations such as nivolumab and ipilimumab, enhancing personalized treatment selection. Moreover, companies are expanding their presence in Europe, as seen in June 2025, Sakar Healthcare received its second European Union (EU) marketing authorization for an oncology injection product, specifically targeting colorectal cancer treatment.

These approvals and product launches are strengthening the integration of diagnostics and therapeutics, thereby significantly driving the growth of the Colorectal Cancer Diagnostics and Therapeutics market in Europe.

Asia-Pacific Colorectal Cancer Diagnostics and Therapeutics Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the Colorectal Cancer Diagnostics and Therapeutics Market due to the rapidly increasing disease burden, improving healthcare infrastructure, and growing awareness of early cancer screening. Countries such as China, India, and Japan are witnessing a steady rise in colorectal cancer cases, largely driven by aging populations, urbanization, and lifestyle changes.

According to the data provided by the International Agency for Research on Cancer (2026), in 2025, the estimated new cases of colorectal cancer was 1.05 million and the projections further estimated that these new cases would rise upto 1.71 million by 2045 in Asia.

At the same time, governments across the region are expanding cancer screening programs and investing in healthcare facilities, which is improving access to diagnostic technologies such as colonoscopy, imaging, and molecular testing. Additionally, the increasing adoption of targeted therapies, immunotherapies, and precision medicine approaches is enhancing treatment outcomes and driving demand for advanced therapeutics. The presence of a large patient pool, growing medical tourism, and rising healthcare expenditure are further supporting market expansion, making APAC the fastest-growing region globally.

Who are the major players in the Colorectal Cancer Diagnostics and Therapeutics Market?

The following are the leading companies in the Colorectal Cancer Diagnostics and Therapeutics market. These Colorectal Cancer Diagnostics and Therapeutics Companies collectively hold the largest market share and dictate industry trends.

- Exact Sciences Corporation

- Guardant Health

- F. Hoffmann-La Roche Ltd.

- Abbott Laboratories

- QIAGEN

- Illumina, Inc.

- Thermo Fisher Scientific

- Epigenomics AG

- Eiken Chemical Co., Ltd.

- Clinical Genomics Technologies

- VolitionRx Ltd.

- Siemens Healthineers

- Olympus Corporation

- Fujifilm Holdings Corporation

- Medtronic plc

- Merck & Co., Inc.

- Bristol-Myers Squibb

- Amgen Inc.

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd

- Sanofi

- Pfizer Inc.

- Bayer AG

- Johnson & Johnson

- Taiho Pharmaceutical

- Others

How is the competitive landscape shaping the Colorectal Cancer Diagnostics and Therapeutics market?

The competitive landscape of the Colorectal Cancer Diagnostics and Therapeutics market is highly dynamic and moderately consolidated, characterized by the presence of leading global pharmaceutical, biotechnology, and diagnostic companies competing through innovation, strategic collaborations, and portfolio expansion. Major Colorectal Cancer Diagnostics and Therapeutics Companies such as F. Hoffmann-La Roche Ltd, Pfizer Inc., Bristol-Myers Squibb, Exact Sciences Corporation, and Guardant Health hold a significant share of the market, collectively driving advancements in both diagnostics and therapeutics.

Competition is largely driven by continuous innovation in molecular diagnostics, liquid biopsy, and targeted/immunotherapy development, as companies aim to improve early detection and treatment outcomes. Firms are heavily investing in research and development, clinical trials, and next-generation technologies such as AI-based diagnostics and genomics to differentiate their offerings. Additionally, strategic partnerships, mergers, and acquisitions play a crucial role in strengthening market positions—for example, large companies acquiring diagnostic firms to expand their oncology portfolios and integrate screening with treatment solutions.

Moreover, the Colorectal Cancer Diagnostics and Therapeutics Market is witnessing the entry of numerous emerging biotech companies and startups, intensifying competition by focusing on niche areas such as biomarker discovery, multi-omics, and personalized medicine. At the same time, collaborations between pharmaceutical companies and diagnostic firms are enabling the development of companion diagnostics, which are essential for targeted therapies.

Overall, the competitive landscape is shaping the market by fostering innovation, accelerating product development, and enhancing the integration of diagnostics and therapeutics, ultimately leading to improved patient outcomes and sustained market growth.

Colorectal Cancer Diagnostics and Therapeutics Market Recent Breakthroughs and Developments

- In September 2025, the EU certified the MMR IHC Panel pharmDx as a companion diagnostic to identify patients eligible for immunotherapy combinations such as nivolumab and ipilimumab, enhancing personalized treatment selection.

- In August 2025, companion diagnostics such as MMR IHC panels received FDA approvals, enabling better identification of patients eligible for immunotherapies.

- In April, 2025, the U.S. FDA approved the combination of Nivolumab (Opdivo) and Ipilimumab (Yervoy) as a first-line treatment for unresectable or metastatic MSI-H/dMMR colorectal cancer, marking a significant advancement in immunotherapy-based treatment options.

- In June 2025, Sakar Healthcare received its second European Union (EU) marketing authorization for an oncology injection product, specifically targeting colorectal cancer treatment.

- In January 2025, Lumakras (sotorasib) in combination with Vectibix was approved for treating KRAS-mutated colorectal cancer, reinforcing the importance of molecular profiling in guiding treatment decisions.

- In December 2024, a novel immunotherapy-based combination regimen received approval in Europe as a first-line treatment for advanced colorectal cancer, further strengthening the role of immunotherapy in clinical practice.

- In July 2024, the FDA approved Shield, a groundbreaking blood-based screening test developed by Guardant Health for the early detection of colorectal cancer.

- In June 2024, accelerated approval was granted for adagrasib (KRAS G12C inhibitor) in combination with cetuximab for advanced colorectal cancer, highlighting the shift toward targeted therapies.

- In June 2024, the European Commission approved fruquintinib, a targeted therapy, for patients with metastatic colorectal cancer who have previously received standard treatments, highlighting the shift toward advanced precision-based therapies.

- In May 2024, Geneoscopy, Inc., a life sciences company focused on developing diagnostic tests for the advancement of gastrointestinal health, announced that the U.S. Food and Drug Administration (FDA) approved its noninvasive colorectal cancer screening test, ColoSense. ColoSense is indicated as a screening test for adults, 45 years of age or older, who are at typical average risk for developing CRC.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Colorectal Cancer Diagnostics and Therapeutics Market CAGR |

8.52% |

|

Key Companies in the Colorectal Cancer Diagnostics and Therapeutics Market |

Exact Sciences Corporation, Guardant Health, F. Hoffmann-La Roche Ltd., Abbott Laboratories, QIAGEN, Illumina, Inc., Thermo Fisher Scientific, Epigenomics AG, Eiken Chemical Co., Ltd., Clinical Genomics Technologies, VolitionRx Ltd., Siemens Healthineers, Olympus Corporation, Fujifilm Holdings Corporation, Medtronic plc, Merck & Co., Inc., Bristol-Myers Squibb, Amgen Inc., Eli Lilly and Company, F. Hoffmann-La Roche Ltd, Sanofi, Pfizer Inc., Bayer AG, Johnson & Johnson, Taiho Pharmaceutical, and others. |

|

Colorectal Cancer Diagnostics and Therapeutics Market Segments |

by Modality, by End-Users, and by Geography |

|

Colorectal Cancer Diagnostics and Therapeutics Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Colorectal Cancer Diagnostics and Therapeutics Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Colorectal Cancer Diagnostics and Therapeutics Market Segmentation

- Colorectal Cancer Diagnostics and Therapeutics by Modality Exposure

- Diagnostics

- Blood Test

- Stool Test

- Imaging Test

- Biopsy

- Others

- Therapeutics

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Others

- Diagnostics

- Colorectal Cancer Diagnostics and Therapeutics End-Users Exposure

- Hospitals

- Diagnostic Laboratories

- Cancer Research Institutes

- Others

- Colorectal Cancer Diagnostics and Therapeutics Geography Exposure

- North America Colorectal Cancer Diagnostics and Therapeutics Market

- United States Colorectal Cancer Diagnostics and Therapeutics Market

- Canada Colorectal Cancer Diagnostics and Therapeutics Market

- Mexico Colorectal Cancer Diagnostics and Therapeutics Market

- Europe Colorectal Cancer Diagnostics and Therapeutics Market

- United Kingdom Colorectal Cancer Diagnostics and Therapeutics Market

- Germany Colorectal Cancer Diagnostics and Therapeutics Market

- France Colorectal Cancer Diagnostics and Therapeutics Market

- Italy Colorectal Cancer Diagnostics and Therapeutics Market

- Spain Colorectal Cancer Diagnostics and Therapeutics Market

- Rest of Europe Colorectal Cancer Diagnostics and Therapeutics Market

- Asia-Pacific Colorectal Cancer Diagnostics and Therapeutics Market

- China Colorectal Cancer Diagnostics and Therapeutics Market

- Japan Colorectal Cancer Diagnostics and Therapeutics Market

- India Colorectal Cancer Diagnostics and Therapeutics Market

- Australia Colorectal Cancer Diagnostics and Therapeutics Market

- South Korea Colorectal Cancer Diagnostics and Therapeutics Market

- Rest of Asia-Pacific Colorectal Cancer Diagnostics and Therapeutics Market

- Rest of the World Colorectal Cancer Diagnostics and Therapeutics Market

- South America Colorectal Cancer Diagnostics and Therapeutics Market

- Middle East Colorectal Cancer Diagnostics and Therapeutics Market

- Africa Colorectal Cancer Diagnostics and Therapeutics Market

- North America Colorectal Cancer Diagnostics and Therapeutics Market

Colorectal Cancer Diagnostics and Therapeutics Market Recent Industry Trends and Milestones (2023-2026)

|

Category |

Key Developments |

|

Colorectal Cancer Diagnostics and Therapeutics Product Approval |

Guardant Health - Shield (FDA), Geneoscopy, Inc. - ColoSense (FDA), Sakar Healthcare - oncology injection (EMA) |

|

Colorectal Cancer Diagnostics and Therapeutics Partnership |

Guardant Health & Quest Diagnostic, Abbott Laboratories & Exact Sciences, BioNTech & Triastek. |

|

Company Strategy |

Exact Sciences Corporation- Focuses on expanding non-invasive cancer screening through products like Cologuard, Strong investment in R&D and multi-cancer early detection (MCED) technologies, Uses strategic acquisitions and collaborations to strengthen genomic and molecular testing capabilities, Expanding into blood-based screening and AI-integrated diagnostics platforms. Guardant Health- Strategy centered on liquid biopsy innovation (ctDNA-based tests) for early detection and monitoring, expanding product portfolio with Guardant360, Guardant Reveal, and Shield screening test, focus on minimally invasive blood-based diagnostics to improve patient compliance, Investing heavily in clinical validation and regulatory approvals to gain market share |

|

Emerging Technology |

Liquid Biopsy (Non-invasive Diagnostics), Artificial Intelligence (AI) & Machine Learning, Next-Generation Sequencing (NGS) & Multi-Omics, Precision Medicine & Biomarker-Driven Therapies, and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are transforming the Colorectal Cancer Diagnostics and Therapeutics market by significantly improving early detection, diagnostic accuracy, and personalized treatment planning. In diagnostics, artificial intelligence particularly machine learning and deep learning algorithms is widely used in colonoscopy and imaging analysis to detect polyps and early-stage tumors with higher precision and reduced miss rates. AI-based computer-aided detection (CADe) and diagnosis (CADx) systems assist clinicians in real time, enhancing adenoma detection rates and minimizing human error.

Additionally, AI is being applied to radiology and pathology workflows, where it can analyze CT, MRI, and histopathology images to identify subtle abnormalities and classify tumor types more efficiently. In therapeutics, AI supports precision medicine by analyzing large datasets, including genomic and clinical data, to identify biomarkers and predict patient responses to targeted therapies and immunotherapies. It also plays a key role in drug discovery and clinical trial optimization, accelerating the development of new treatments and improving patient selection. Furthermore, AI-driven tools enable predictive analytics and disease monitoring, helping clinicians track disease progression and adjust treatment strategies in real time. Overall, these AI-powered applications are enhancing clinical decision-making, improving patient outcomes, and driving the advancement of the Colorectal Cancer Diagnostics and Therapeutics market.

U.S. Tariff Impact Analysis on Colorectal Cancer Diagnostics and Therapeutics Market

The U.S. tariff impact on the Colorectal Cancer Diagnostics and Therapeutics market is largely characterized by increased costs, supply chain disruptions, and strategic shifts in manufacturing and sourcing. The introduction of tariffs on imported medical devices, diagnostic equipment, and pharmaceutical components has significantly raised production and procurement costs, as a large proportion of these products and raw materials are sourced internationally. For instance, a substantial share of medical devices used in the U.S. is manufactured overseas, making the sector highly vulnerable to tariff-induced price increases . These higher costs are often passed on to healthcare providers and patients, thereby affecting affordability and adoption of advanced colorectal cancer diagnostics and therapies.

In addition, tariffs on critical inputs such as semiconductors, polymers, and active pharmaceutical ingredients have disrupted global supply chains, leading to delays in product availability and increased operational complexity . This can hinder timely diagnosis and treatment, particularly for advanced technologies like molecular diagnostics and targeted therapies. Moreover, retaliatory tariffs from other countries may reduce export opportunities for U.S.-based companies, further impacting revenue growth and global competitiveness. While tariffs may encourage domestic manufacturing in the long term, the high cost and complexity of establishing local production facilities limit immediate benefits. Overall, U.S. tariffs act as a market restraint in the short term by increasing costs and limiting accessibility, but they may also drive long-term strategic realignment and localization within the Colorectal Cancer Diagnostics and Therapeutics market.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Mercy BioAnalytics |

$59 million |

Series B |

Liquid biopsy assay platform for early cancer detection |

ctDNA-based liquid biopsy technology. |

Key Takeaways from the Colorectal Cancer Diagnostics and Therapeutics Market Report Study

- Market size analysis for the current Colorectal Cancer Diagnostics and Therapeutics Market Size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the Colorectal Cancer Diagnostics and Therapeutics market.

- Various opportunities available for the other competitors in the Colorectal Cancer Diagnostics and Therapeutics market space.

- What are the top-performing segments in 2025? How will these segments perform in 2034?

- Which are the top-performing regions and countries in the current Colorectal Cancer Diagnostics and Therapeutics market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the Colorectal Cancer Diagnostics and Therapeutics market growth in the future?

Stay updated with us for Recent Articles @ New DelveInsight Blogs