Hepatitis Testing Market Summary

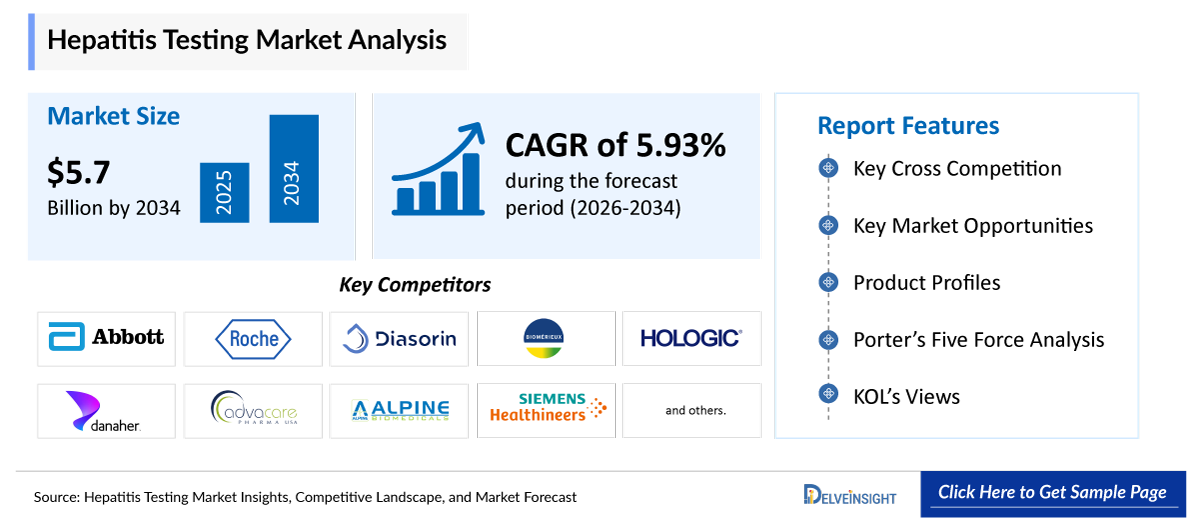

- The global hepatitis testing market is expected to increase from USD 3,470.08 million in 2025 to USD 5,785.24 million by 2034, reflecting strong and sustained growth.

- The global hepatitis testing market is growing at a CAGR of 5.93% during the forecast period from 2026 to 2034.

- The hepatitis testing market is primarily driven by the rising prevalence of hepatitis infections and their associated risk factors, such as chronic liver disease, lifestyle-related conditions, and high-risk populations. As awareness of early detection grows, healthcare providers are increasingly adopting point-of-care testing, which allows for rapid, on-site diagnosis and timely treatment decisions. Additionally, continuous product development and innovation by diagnostic companies, including the introduction of advanced molecular assays, rapid diagnostic kits, and automated testing platforms, is expanding the availability and efficiency of hepatitis testing, further fueling market growth.

- The leading companies operating in the hepatitis testing market include Abbott, F. Hoffmann-La Roche Ltd., Diasorin S.p.A, Bio-Merieux, Hologic Inc., Danaher Corporation, AdvaCare Pharma, Alpine Biomedicals Pvt Ltd., Siemens Healthineers, SD Biosensor, Inc., OraSure Technologies, Inc., Creative Diagnostics, SSI Diagnsotica A/S, InTec Products, Inc., BTNX Inc., ACON Laboratories, Inc., Altona Diagnostics GmbH, Bruker Corporation, Mikrogen GmbH, Fortress Diagnostics and others.

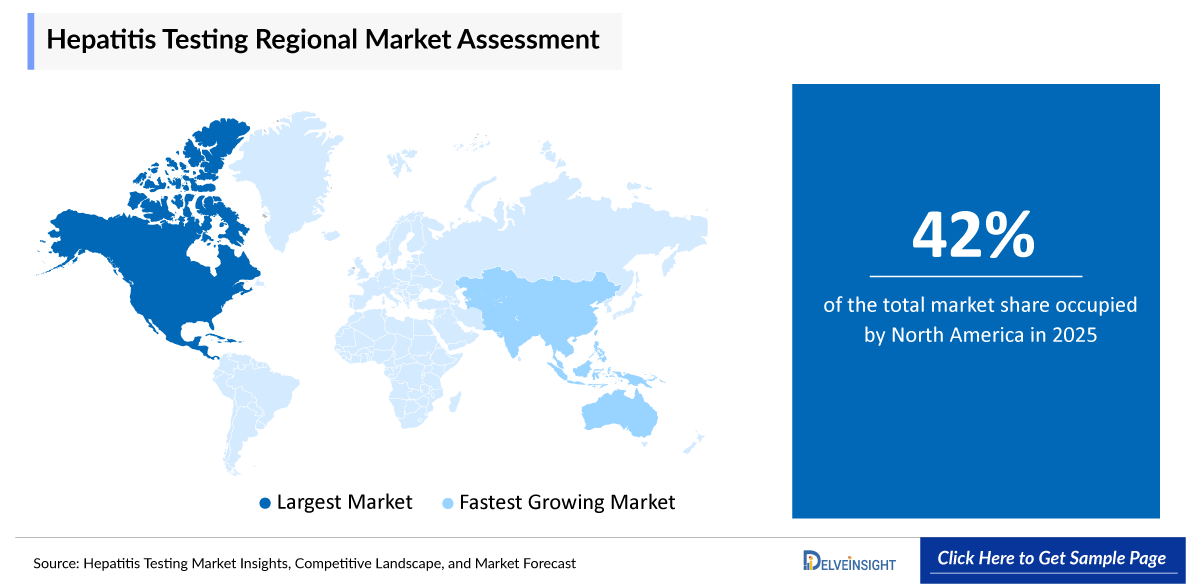

- North America’s hepatitis testing market is primarily driven by the high prevalence of chronic Hepatitis B and Hepatitis C, which continues to increase the demand for early diagnosis and routine disease monitoring. In addition, technological advancements such as molecular diagnostics, automated immunoassays, and rapid point-of-care testing have significantly improved testing accuracy, efficiency, and accessibility. Mandatory blood donor screening programs and rising public awareness regarding liver health also contribute to sustained testing demand. Collectively, these factors are strengthening and accelerating the growth of the hepatitis testing market across North America.

- In the product type segment of the hepatitis testing market, regents & kits category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Hepatitis Testing Market

Hepatitis Testing Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 3,470.08 million |

|

2034 Projected Market Size |

USD 5,785.24 million |

|

Growth Rate (2026-2034) |

5.93% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Hepatitis Testing Market

- Rising prevalence of hepatitis infections and associated risk factors: The hepatitis testing market is strongly fueled by the increasing prevalence of hepatitis infections and their serious complications, such as liver cancer and liver cirrhosis. Chronic infections with Hepatitis B and Hepatitis C can cause progressive liver damage over time, significantly raising the risk of cirrhosis and liver cancer. This growing health burden has created a critical need for early detection and routine screening, enabling timely intervention and better disease management. As a result, there is an increasing demand for advanced hepatitis diagnostic tools, including molecular assays, serological tests, and rapid diagnostic kits, which is driving the overall expansion of the hepatitis testing market globally.

- Growth in blood donation and blood screening programs: The growth in blood donation and blood screening programs is significantly boosting the hepatitis testing market as donated blood must be thoroughly screened to prevent the transmission of infectious diseases such as hepatitis B and hepatitis C. Blood banks and transfusion centers routinely conduct mandatory screening tests to detect hepatitis antigens, antibodies, or viral nucleic acids before blood is approved for transfusion. As the number of blood donations increases due to rising healthcare needs, surgical procedures, and emergency treatments, the demand for reliable hepatitis testing methods such as ELISA, rapid diagnostic tests, and nucleic acid testing (NAT) also increases. In addition, government regulations and public health initiatives that mandate strict blood safety protocols further drive the adoption of hepatitis diagnostic kits and reagents, thereby contributing to the overall growth of the hepatitis testing market.

- Increasing awareness and screening programs: Increasing awareness and screening programs are significantly boosting the hepatitis testing market as governments and healthcare organizations are actively promoting early detection of hepatitis infections. Public health campaigns, community screening initiatives, and national hepatitis control programs encourage people to undergo routine testing, especially high-risk populations. Early diagnosis helps in timely treatment and prevents the spread of the disease, which increases the demand for various hepatitis diagnostic tests such as ELISA, rapid tests, and molecular assays. As a result, the expansion of awareness campaigns and large-scale screening programs is driving the growth of the hepatitis testing market.

- Increasing adoption of point-of-care testing: The growing availability of point-of-care hepatitis testing kits is making diagnostic services more accessible, particularly in developing countries and remote healthcare settings. Rapid diagnostic tests allow healthcare professionals to obtain results within minutes without requiring advanced laboratory infrastructure. This expansion of decentralized testing is helping to increase screening coverage and accelerate market growth.

- Increase in product development activities among key market players: Diagnostic companies are continuously investing in research and innovation to develop advanced testing solutions that are faster, more accurate, and easier to use. This includes the introduction of high-sensitivity molecular assays, rapid diagnostic kits, automated testing platforms, and multiplex testing technologies. Such developments not only improve the efficiency of hepatitis detection but also expand the availability of testing options across hospitals, laboratories, and point-of-care settings. The ongoing focus on innovation by key players is thus enhancing market competitiveness and fueling the overall growth of the hepatitis testing market.

Hepatitis Testing Market Report Segmentation

This hepatitis testing market report offers a comprehensive overview of the global hepatitis testing market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product Type (Reagents & Kits and Instruments), Technology (Enzyme Linked Immunosorbent Assay (ELISA), Rapid Diagnostic Test, Polymerase Chain Reaction (PCR), Chemiluminescence Immunoassay (CLIA), and Others), Disease Type (Hepatitis B, Heaptitis C, Hepatitis A, Hepatitis D, and Hepatitis E), Test Type (Antigen Test, Antibody Test, Nucleic Acid Test and Genotype Test), End-Users (Hospitals & Clinics, Diagnostic Laboratories, and Others), and Geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing hepatitis testing market.

Hepatitis testing is a set of medical diagnostic procedures used to detect the presence of hepatitis viruses or liver damage caused by them. It typically involves blood tests that identify viral antigens, antibodies, or genetic material (DNA/RNA) to determine whether a person has a current, past, or chronic infection. These tests help in early diagnosis, monitoring disease progression, guiding treatment decisions, and preventing transmission of hepatitis.

The hepatitis testing market is primarily driven by the rising prevalence of hepatitis infections and their severe complications, such as liver cirrhosis and liver cancer, which has increased the need for early diagnosis and routine screening. Additionally, the growth in blood donation and mandatory blood screening programs has significantly increased the demand for hepatitis diagnostic tests to ensure the safety of blood transfusions. Increasing awareness initiatives and national screening programs are also encouraging individuals, particularly high-risk populations, to undergo early testing, thereby supporting market growth. Furthermore, the expanding adoption of point-of-care testing is improving access to rapid and reliable diagnostics, especially in remote and resource-limited settings. At the same time, continuous product development and technological advancements by diagnostic companies, including the introduction of molecular assays, automated immunoassays, and rapid diagnostic kits, are enhancing testing accuracy and efficiency, ultimately driving the overall growth of the hepatitis testing market.

Get More Insights into the Report @ Hepatitis Testing Market

What are the latest hepatitis testing market dynamics and trends?

The hepatitis testing market is driven by the rising prevalence of hepatitis B and C and the increasing demand for early diagnosis and routine monitoring.

According to the Centers for Disease Control and Prevention (2025), viral hepatitis had affected more than 300 million people globally.

Additionally, as per the same source, in 2022, 1.2 million people were newly infected with hepatitis B virus (HBV) and 1 million people were newly infected with hepatitis C virus (HCV). Approximately 254 million people were living with chronic hepatitis B, while nearly 50 million people had chronic hepatitis C. As the number of people affected by hepatitis B and C has grown, the demand for early diagnosis, routine screening, and ongoing disease monitoring has increased substantially. Rising infection rates, especially among high-risk populations, have led governments and healthcare providers to expand screening programs and implement targeted public health initiatives. Moreover, the availability of effective antiviral treatments has made early detection essential for timely intervention, further encouraging widespread testing and collectively driving the growth of the hepatitis testing market.

Moreover, India’s National Viral Hepatitis Control Program, which was launched in 2018 with the mission to combat hepatitis and eliminate hepatitis C by 2030, had significantly expanded hepatitis screening and treatment efforts in the country. Reports indicated that by July 2024, the program had screened approximately 10.34 crore individuals for hepatitis B and C and had provided treatment to around 3.3 lakh patients since its inception. As the program has screened millions of individuals for hepatitis B and C, it has created substantial demand for diagnostic tests, reagents, and testing kits used in hospitals, laboratories, and community health centers. Such government-led screening programs encourage routine testing, improve disease detection rates, and expand the use of hepatitis diagnostic technologies, thereby contributing to the overall growth of the hepatitis testing market.

Furthermore, the growth in blood donation and blood screening programs is significantly boosting the hepatitis testing market because all donated blood must be carefully screened to prevent the transmission of infectious diseases such as hepatitis B and hepatitis C. According to the data provided by the World Health Organization (2026), approximately, 118.5 million blood donations were collected globally. Thus, as the number of blood donations increases worldwide, the demand for reliable hepatitis diagnostic tests, including ELISA, nucleic acid testing (NAT), and rapid diagnostic kits, also rises.

However, the increase in product development activities is further boosting the overall market of respiratory care devices. For instance, in June 2024, Cepheid announced that it had received FDA De Novo marketing authorization and Clinical Laboratory Improvement Amendments (CLIA) Waiver approval for Xpert® HCV, making it the only molecular test in the U.S. capable of detecting hepatitis C virus RNA directly from a human capillary whole blood (fingerstick) sample. The Xpert HCV test was performed on the GeneXpert Xpress System.

Thus, the factors mentioned above are expected to boost the overall market of hepatitis testing during the forecast period from 2026 to 2034.

However, the hepatitis testing market encounters several challenges that may hinder its growth. Technical limitations in serological assays, including cross-reactivity, low sensitivity during early infection, or interference from other biological factors, can result in inaccurate or inconclusive outcomes, impacting diagnosis and patient care. Furthermore, the rigorous regulatory approval process requiring extensive clinical validation and adherence to regional and international standards can delay product launches and increase development costs. Collectively, these factors create significant obstacles for manufacturers and healthcare providers, potentially restricting the widespread adoption and timely availability of hepatitis testing solutions.

Hepatitis Testing Market Segment Analysis

Hepatitis Testing Market by Product Type (Reagents & Kits and Instruments), Technology (Enzyme Linked Immunosorbent Assay (ELISA), Rapid Diagnostic Test, Polymerase Chain Reaction (PCR), Chemiluminescence Immunoassay (CLIA), and Others), Disease Type (Hepatitis B, Heaptitis C, Hepatitis A, Hepatitis D, and Hepatitis E), Test Type (Antigen Test, Antibody test, Nucleic Acid Test and Genotype Test), End-Users (Hospitals & Clinics, Diagnostic Laboratories, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World).

By Product Type: Reagents & Kits are projected to account for the highest revenue share in the global market.

Within the product type segmentation of the hepatitis testing market, reagents & kits are projected to hold the largest revenue share, accounting for an estimated 68% of the market in 2025. Reagents and kits played a crucial role in boosting the overall hepatitis testing market because they form the core consumables required for detecting hepatitis infections in clinical laboratories, hospitals, blood banks, and diagnostic centers. These products include antibody detection kits, antigen detection reagents, nucleic acid amplification reagents, and genotyping kits, which are essential for identifying hepatitis A, B, and C infections through various technologies such as ELISA, chemiluminescence immunoassays, and PCR-based molecular testing.

Additionally, the growing demand for routine screening, early diagnosis, and monitoring of hepatitis infections significantly increased the consumption of these reagents and kits, as they must be used for every diagnostic test performed. In addition, large-scale screening programs and blood safety initiatives implemented by organizations such as the World Health Organization further accelerated the need for reliable testing consumables to screen blood donations and detect infections at early stages.

Furthermore, the increasing adoption of automated diagnostic platforms in laboratories required specialized reagents and assay kits designed for high-throughput systems, which further expanded their demand. Leading diagnostics companies, including Abbott Laboratories, F. Hoffmann‑La Roche, and Bio‑Rad Laboratories, have continuously introduced advanced hepatitis testing reagents and kits to support large-scale testing and monitoring programs.

Continuous technological advancements also contributed to the development of highly sensitive and specific reagent kits that enabled faster and more accurate detection of viral markers, thereby improving clinical outcomes and disease management. However, the increase in product development activities is further boosting the overall market of hepatitis testing. For example, in December 2025, Altona launched the AltoStar® HDV RT‑PCR Kit 1.5 (CE‑IVD), completing its CE‑IVD PCR portfolio for all five hepatitis viruses.

As a result, the repeated usage, technological innovation, and increasing global screening initiatives associated with reagents and kits significantly contributed to the expansion of the hepatitis testing market.

By Technology: Enzyme Linked Immunosorbent Assay (ELISA) Category Dominates the Market

Enzyme-Linked Immunosorbent Assay (ELISA) dominates the hepatitis testing market with a market share of 60% in 2025, due to its high sensitivity, specificity, and cost-effectiveness in detecting hepatitis antigens and antibodies in blood samples. ELISA is widely used for screening and diagnosing infections such as hepatitis A, hepatitis B, and hepatitis C because it allows laboratories to process a large number of samples simultaneously with reliable and reproducible results. The technology is commonly adopted in hospitals, diagnostic laboratories, and blood banks for routine screening, particularly for detecting markers such as hepatitis B surface antigen (HBsAg) and hepatitis C antibodies. In addition, ELISA kits are relatively easy to use and compatible with automated laboratory systems, which improves testing efficiency and reduces manual errors. Several diagnostic companies manufacture ELISA-based hepatitis testing kits. For example, Bio‑Rad Laboratories offers the Monolisa™ HBsAg ULTRA ELISA kit for the detection of hepatitis B surface antigen, while Dia.Pro Diagnostic Bioprobes provides HCV Ab ELISA kits for hepatitis C antibody detection. Similarly, Abbott Laboratories develops ELISA-based assays used in hepatitis screening programs. The widespread use of these ELISA kits for routine screening, blood donor testing, and large-scale diagnostic programs has therefore led to the dominance of ELISA technology in the hepatitis testing market.

By Disease Type : Hepatitis B Category Dominates the Market

The increasing prevalence of Hepatitis B is significantly boosting the overall hepatitis testing market due to the growing need for early detection, diagnosis, and continuous monitoring of the infection. Hepatitis B is one of the most widespread viral liver infections globally and can lead to severe complications such as Liver Cirrhosis and Liver Cancer if not diagnosed and treated at an early stage. As per the data provided by the European Centre for Disease Prevention and Control (2024), in 2022, the global prevalence was estimated at 257 million people living with HBV infection. As a result, healthcare systems across the world are increasingly implementing routine screening programs for high-risk populations, including pregnant women, blood donors, and individuals with weakened immune systems.

The diagnosis of hepatitis B typically involves several tests such as HBsAg detection, antibody tests, and nucleic acid testing (NAT) to identify viral DNA and monitor viral load. The growing number of screening initiatives, hospital testing procedures, and blood safety programs has significantly increased the demand for hepatitis diagnostic reagents, kits, and automated testing systems. In addition, government initiatives and global health organizations are promoting early diagnosis and treatment of hepatitis B to reduce disease transmission and long-term liver complications. Consequently, the rising disease burden and the need for continuous monitoring of infected patients are driving the adoption of advanced diagnostic technologies, thereby boosting the overall growth of the hepatitis testing market.

By Test Type: Antibody Test Category Dominates the Market

The antibody test category dominates the hepatitis testing market due to its critical role in detecting past or current infections and assessing immunity. These tests are widely used to screen for hepatitis B and C by identifying specific antibodies, such as HBsAb for hepatitis B and anti-HCV for hepatitis C, which indicate exposure or immune response. Their high accuracy, reliability, and relatively low cost make them a preferred choice in hospitals, laboratories, and point-of-care settings. Additionally, antibody tests are non-invasive, easy to perform, and provide rapid results, which further supports their widespread adoption. The combination of these factors efficiency, accessibility, and diagnostic value ensures the antibody test category remains a leading segment in the global hepatitis testing market.

By End-Users: Hospitals & Clinics Category Dominates the Market

Hospitals and clinics dominate the hepatitis testing market as they serve as the primary points of care for patient screening, diagnosis, and disease management. These settings handle a large volume of patients, including high-risk populations, making them central to routine and preventive hepatitis testing. The dominance of hospitals and clinics is driven by factors such as the availability of advanced laboratory infrastructure, access to trained medical personnel, and integration with automated diagnostic platforms that allow high-throughput and accurate testing. Additionally, these facilities benefit from established patient trust, health insurance coverage, and government-supported screening programs, which encourage regular testing and follow-up. The combination of advanced infrastructure, trained medical personnel, integration of cutting-edge diagnostic technologies, and easy patient access ensures that hospitals and clinics continue to lead and dominate the hepatitis testing market.

Hepatitis Testing Market Regional Analysis

North America Hepatitis Testing Market Trends

North America is expected to account for the highest proportion of 42% of the hepatitis testing market in 2025, out of all regions. This dominance is fueled by the high prevalence of hepatitis B and C, extensive screening initiatives, well-developed healthcare infrastructure, technological advancements in diagnostics, and mandatory blood donor testing.

According to the Centers for Disease Control and Prevention, in 2023, the United States had recorded 1,643 new cases of hepatitis A, 2,212 new cases of hepatitis B, and 5,538 new cases of hepatitis C. With the global rise in hepatitis B and C infections, the demand for early diagnosis, routine screening, and continuous disease monitoring has grown substantially. High infection rates, particularly among high-risk populations, have led governments and healthcare providers to expand screening programs and implement targeted public health initiatives. Furthermore, the availability of effective antiviral treatments has made early detection crucial, driving wider adoption of testing and collectively fueling growth in the hepatitis testing market.

Moreover, according to Blue Faery: The Adrienne Wilson Liver Cancer Association, in 2024 an estimated 41,630 new cases of liver cancer were reported, including 28,000 cases in men and 13,630 cases in women. Chronic infections caused by Hepatitis B and Hepatitis C are major risk factors for the development of liver cancer. Long-term viral hepatitis can lead to liver inflammation, fibrosis, and cirrhosis, increasing the risk of cancer. As a result, the growing emphasis on early diagnosis and monitoring has increased the demand for advanced diagnostic tools such as serological assays, molecular tests, and rapid diagnostic kits, thereby boosting the hepatitis testing market globally.

However, the increase in product development activities is further boosting the overall market of hepatitis testing. For instance, in June 2024, Cepheid announced that it had received FDA De Novo marketing authorization and Clinical Laboratory Improvement Amendments (CLIA) Waiver approval for Xpert® HCV, making it the only molecular test in the U.S. capable of detecting hepatitis C virus RNA directly from a human capillary whole blood (fingerstick) sample.

Thus, all the above-mentioned factors are anticipated to propel the market for hepatitis testing in North America during the forecast period.

Europe Hepatitis Testing Market Trends

In Europe, the hepatitis testing market is primarily driven by ongoing prevalence of hepatitis B and hepatitis C infections which has heightened the demand for early detection and routine monitoring. At the same time, technological advancements including molecular diagnostics, automated immunoassays, and rapid point-of-care tests have enhanced both the accuracy and accessibility of hepatitis testing.

According to the European Centre for Disease Prevention and Control, in 2023, the European Union/European Economic Area (EU/EEA) had reported 37,766 cases of hepatitis B virus (HBV) infection, corresponding to a crude rate of 8.1 cases per 100,000 population. Of these cases, 6.3% were classified as acute, 40.5% as chronic, 46.1% as unknown, and 7.1% could not be classified. With the growing number of hepatitis B and C cases, the need for early diagnosis, regular screening, and continuous disease monitoring has risen significantly. The availability of effective antiviral treatments has further emphasized the importance of early detection, driving greater adoption of testing and, in turn, fueling the growth of the hepatitis testing market.

Moreover, according to the International Agency for Research on Cancer, the estimated number of new cases of liver and intrahepatic bile duct cancer in Europe was 91,200 in 2025 and is projected to reach 113,000 by 2045. Early detection of hepatitis infections is essential to prevent progression to severe liver diseases, including liver and bile duct cancers. Growing awareness of this link has led governments and healthcare organizations to implement large-scale screening programs, boosting demand for serological, molecular, and rapid point-of-care tests, and driving growth in the global hepatitis testing market.

Hence, all the factors mentioned above are expected to drive the market for hepatitis testing in Europe during the forecast period.

Asia-Pacific Hepatitis Testing Market Trends

In the Asia Pacific region, the hepatitis testing market is driven by the growing prevalence of hepatitis B and C infections along with increasing government initiatives aimed at early diagnosis and disease control. Moreover, the adoption of advanced diagnostic technologies such as molecular testing and rapid point-of-care assays has improved the accessibility and efficiency of hepatitis detection.

According to the Global Hepatitis Elimination Initiative, the 2022 survey report indicated that the prevalence of chronic HBV infection in Japan was estimated at 0.77%. As per the same source (2023), an estimated 7.6 million people in China were living with chronic hepatitis C. As the number of infected individuals continues to increase, the demand for early diagnosis, routine screening, and continuous disease monitoring has grown significantly. Early detection enables timely initiation of antiviral treatment and helps prevent serious complications such as liver cirrhosis and liver cancer. Consequently, the growing need for early and accurate diagnosis is accelerating the expansion of the hepatitis testing market.

Moreover, according to the International Agency for Research on Cancer, the estimated number of new cases of liver and intrahepatic bile duct cancers in Japan was 390,000 in 2025 and is projected to reach 541,000 by 2045. Long-term hepatitis infections can lead to liver inflammation, cirrhosis, and eventually cancer, which has increased the need for early detection and routine screening of hepatitis viruses. As a result, healthcare providers increasingly conduct hepatitis testing to identify infected individuals at an early stage and monitor disease progression, thereby escalating the overall market of hepatitis testing across the region.

However, the increase in product development activities is further boosting the overall market of hepatitis testing. For example, in October 2025, Reszon Diagnostics International, a subsidiary of Hextar Healthcare and manufacturer of innovative rapid diagnostic tests, launched the RESZON HBsAg Rapid Test commercially. The test provided a fast and reliable method for detecting the Hepatitis B surface antigen (HBsAg) in serum, plasma, or whole-blood samples.

Thus, the factors mentioned above are expected to boost the market of hepatitis testing across the Asia-Pacific region.

Who are the major players in the hepatitis testing market?

The following are the leading companies in the hepatitis testing market. These companies collectively hold the largest market share and dictate industry trends.

- Abbott

- F. Hoffmann-La Roche Ltd

- DiaSorin S.p.A

- Bio-Merieux

- Hologic, Inc.

- Danaher Corporation

- AdvaCare Pharma

- Alpine Biomedicals Pvt Ltd

- Siemens Healthineers

- SD Biosensor, Inc.

- OraSure Technologies, Inc.

- Creative Diagnostics

- SSI Diagnostica A/S

- InTec Products, Inc

- BTNX Inc.

- ACON Laboratories, Inc.

- Altona Diagnostics GmbH

- Bruker Corporation

- Mikrogen GmbH

- Fortress Diagnostics

- Others

How is the competitive landscape shaping the hepatitis testing market?

The competitive landscape of the hepatitis testing market is shaped by the presence of a mix of global diagnostics leaders and emerging regional players, all striving to innovate and expand their market reach. Established companies such as Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, and Bio-Rad Laboratories dominate through extensive product portfolios that include ELISA kits, molecular assays, and rapid point-of-care tests, supported by strong distribution networks and regulatory approvals across multiple regions. Competition is intensified by continuous technological advancements, with companies investing heavily in next-generation diagnostics that offer higher sensitivity, faster turnaround times, and automation to meet growing clinical demands. Additionally, strategic collaborations, mergers, acquisitions, and partnerships are increasingly being used to expand geographic presence, strengthen R&D capabilities, and improve access to emerging markets. Smaller or regional players focus on niche segments such as affordable rapid tests or specialized molecular kits, creating diverse options for end-users. This dynamic competitive environment drives innovation, improves testing accuracy, broadens product availability, and ultimately shapes the growth trajectory of the global hepatitis testing market.

Overall, the hepatitis testing market is witnessing robust competition, where innovation, compliance, and strategic growth initiatives are the primary factors enabling companies to differentiate themselves, capture market share, and meet the evolving needs of healthcare providers globally.

Recent Developmental Activities in the Hepatitis Testing Market

- In December 2025, Altona launched the AltoStar® HDV RT‑PCR Kit 1.5 (CE‑IVD), completing its CE‑IVD PCR portfolio for all five hepatitis viruses.

- In August 2025, HiMedia Laboratories received Central Drugs Standard Control Organisation (CDSCO) approval in India for its Hi‑PCR® Hepatitis B and C molecular diagnostic kits (quantitative), marking a significant milestone for the company’s hepatitis testing portfolio.

- In June 2024, Cepheid announced that it had received FDA De Novo marketing authorization and Clinical Laboratory Improvement Amendments (CLIA) Waiver approval for Xpert® HCV, making it the only molecular test in the U.S. capable of detecting hepatitis C virus RNA directly from a human capillary whole blood (fingerstick) sample. The Xpert HCV test was performed on the GeneXpert Xpress System.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Hepatitis Testing Market CAGR |

5.93% |

|

Key Companies in the Hepatitis Testing Market |

Abbott, F. Hoffmann-La Roche Ltd., Diasorin S.p.A, Bio-Merieux, Hologic Inc., Danaher Corporation, AdvaCare Pharma, Alpine Biomedicals Pvt Ltd., Siemens Healthineers, SD Biosensor, Inc., OraSure Technologies, Inc., Creative Diagnostics, SSI Diagnsotica A/S, InTec Products, Inc., BTNX Inc., ACON Laboratories, Inc., Altona Diagnostics GmbH, Bruker Corporation, Mikrogen GmbH, Fortress Diagnostics and others. |

|

Hepatitis Testing Market Segments |

by Product Type, by Technology, by Disease Type, by Test Type, by End-Users, and by Geography |

|

Hepatitis Testing Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Hepatitis Testing Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Hepatitis Testing Market Segmentation

- Hepatitis Testing by Product Type Exposure

- Reagents & Kits

- Instruments

- Hepatitis Testing Technology Exposure

- Enzyme-Linked Immunosorbent Assay (ELISA)

- Rapid Diagnostic Test

- Chemiluminescence Immunoassay (CLIA)

- Polymerase Chain Reaction (PCR)

- Others

- Hepatitis Testing Disease Type Exposure

- Hepatitis B

- Hepatitis C

- Hepatitis A

- Hepatitis D

- Hepatitis E

- Hepatitis Testing Test Type Exposure

- Antigen Test

- Antibody Test

- Nucleic Acid

- Genotype Test

- Hepatitis Testing End-Users Exposure

- Hospitals & Clinics

- Diagnostic Laboratories

- Others

- Hepatitis Testing Geography Exposure

- North America Hepatitis Testing Market

- United States Hepatitis Testing Market

- Canada Hepatitis Testing Market

- Mexico Hepatitis Testing Market

- Europe Hepatitis Testing Market

- United Kingdom Hepatitis Testing Market

- Germany Hepatitis Testing Market

- France Hepatitis Testing Market

- Italy Hepatitis Testing Market

- Spain Hepatitis Testing Market

- Rest of Europe Hepatitis Testing Market

- Asia-Pacific Hepatitis Testing Market

- China Hepatitis Testing Market

- Japan Hepatitis Testing Market

- India Hepatitis Testing Market

- Australia Hepatitis Testing Market

- South Korea Hepatitis Testing Market

- Rest of Asia-Pacific Hepatitis Testing Market

- Rest of the World Hepatitis Testing Market

- South America Hepatitis Testing Market

- Middle East Hepatitis Testing Market

- Africa Hepatitis Testing Market

- North America Hepatitis Testing Market

Hepatitis Testing Market Recent Industry Trends and Milestones (2022-2026)

|

Category |

Key Developments |

|

Hepatitis Testing Product Approvals |

Cepheid- Xpert® HCV (FDA), HiMedia Labs- Hi-PCR® Hepatitis B and C molecular diagnostic kits (CDSCO) |

|

Hepatitis Testing Product Launch |

Altona Diagnostics launched AltoStar® HDV RT-PCR Kit 1.5 (CE-IVD) |

|

Company Strategy |

Abbott - focuses on innovating advanced diagnostics and expanding global access to healthcare solutions. The company emphasizes developing high-accuracy immunoassays, molecular tests, and point-of-care platforms while leveraging strong distribution networks to reach hospitals, laboratories, and remote regions. Bio-Merieux - focuses on innovation, global expansion, and operational efficiency, investing in R&D to enhance the speed, reliability, and clinical value of its infectious disease and molecular diagnostics, while collaborating with academic, biotech, and public health partners to advance technology development. |

|

Emerging Technology |

CRISPR-Based Diagnostics, Point-of-Care (POC) Molecular Assays, Next-Generation Sequencing (NGS), Biosensors, Artificial Intelligence (AI) and Machine Learning and others . |

Impact Analysis

AI-Powered Innovations and Applications:

AI‑powered innovations are increasingly influencing the hepatitis testing market by enhancing diagnostic accuracy, operational efficiency, and clinical decision‑making. Artificial intelligence (AI) and machine learning algorithms can analyze complex data from imaging, laboratory results, and patient records to identify patterns that may be difficult for human interpretation alone. In hepatitis testing, AI supports improved interpretation of molecular and serological assay data, reducing false positives and negatives and enabling earlier detection of infection. AI also accelerates workflow automation in high‑volume laboratory environments by optimizing sample processing, result validation, and quality control, which reduces turnaround times and operational costs. When integrated with next‑generation diagnostic platforms, such as digital immunoassays and PCR systems, AI tools help laboratories tailor testing protocols based on patient history and risk factors, improving personalized diagnostics and treatment planning. Additionally, AI facilitates predictive analytics and population health management by identifying trends in hepatitis incidence and testing patterns, enabling health systems to allocate resources more effectively and target screening programs to high‑risk groups. AI‑driven software can also support telemedicine and remote testing interpretations, expanding access in underserved or resource‑limited regions. Overall, the integration of AI into the hepatitis testing ecosystem is enhancing efficiency, accuracy, and scalability, positioning AI as a transformative factor that is likely to support future market growth and innovation.

U.S. Tariff Impact Analysis on Hepatitis Testing Market:

The U.S. tariff impact on the hepatitis testing market centers on how broader trade duties on imported medical and diagnostic products can influence costs, supply chains, and competitive dynamics within the in vitro diagnostics (IVD) sector that includes hepatitis testing kits and related reagents. Since many diagnostic components and complete test kits are produced outside the United States, tariffs on imports—ranging from baseline duties to elevated trade penalties on goods from key manufacturing hubs—can increase the cost of goods sold for companies that rely on foreign production, potentially prompting higher prices for laboratories, clinics, and patients. Diagnostic manufacturers may respond by absorbing costs, relocating manufacturing to the U.S., or shifting supply chains, which could influence product pricing and availability in the hepatitis testing segment. Higher input costs and supply chain disruptions caused by tariffs can also strain operational budgets of healthcare providers by making essential supplies more expensive and less predictable to source, which in turn may affect testing volumes and overall market growth dynamics. Companies with primarily domestic manufacturing could benefit if imported competitors face tariff‑induced cost increases, while ongoing tariff uncertainty may deter investment and complicate long‑term planning for both suppliers and buyers in the hepatitis testing market.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Key takeaways from the hepatitis testing market report study

- Market size analysis for the current hepatitis testing market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the hepatitis testing market.

- Various opportunities available for the other competitors in the hepatitis testing market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current hepatitis testing market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the hepatitis testing market growth in the future?