Hip Replacement Devices Market Summary

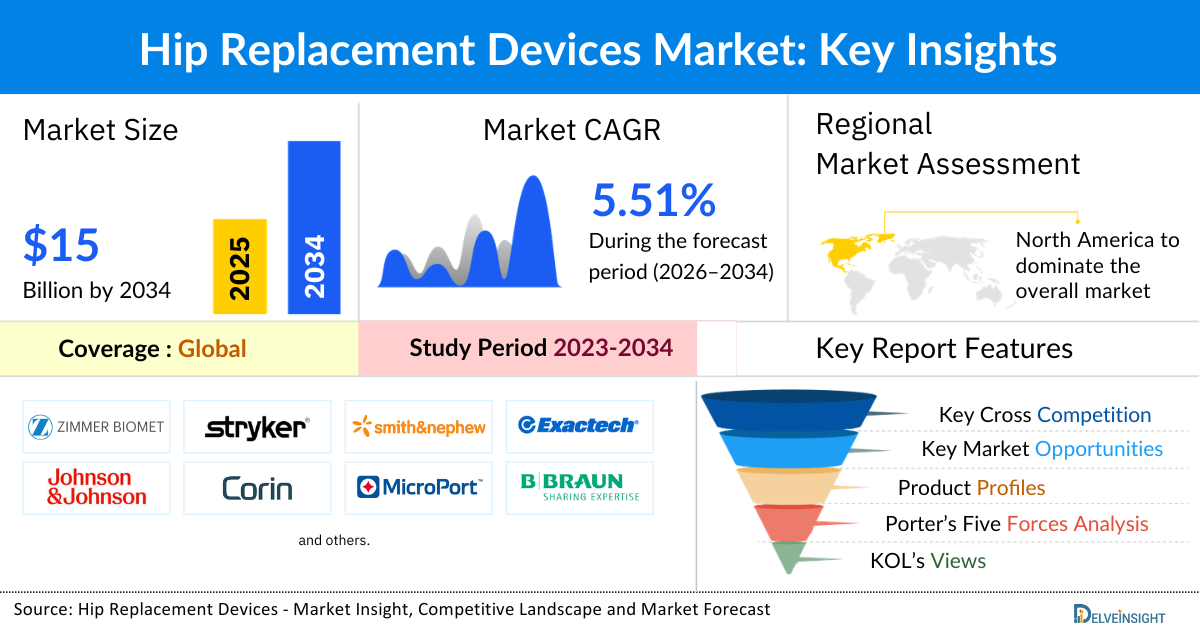

- The global hip reconstruction/replacement devices market is expected to increase from USD 9,254.50 million in 2025 to USD 14,917.71 million by 2034, reflecting strong and sustained growth.

- The global hip reconstruction/replacement devices market is growing at a CAGR of 5.51% during the forecast period from 2026 to 2034.

- The global hip reconstruction and replacement devices market is growing rapidly due to the rising prevalence of bone-related disorders, increasing hip fracture cases, and continuous technological advancements. Conditions like osteoarthritis and osteoporosis are driving the need for effective joint restoration solutions, while the surge in age-related fractures further boosts surgical demand. In parallel, innovations such as 3D-printed implants, hybrid fixation systems, and robotic-assisted procedures are enhancing implant performance and surgical precision. Together, these factors are propelling market expansion and reinforcing the critical role of hip reconstruction/replacement devices in modern orthopedic care.

- The leading companies operating in the Hip Reconstruction/Replacement Devices market include Zimmer Biomet, Stryker Corporation, Smith & Nephew, Exactech, Inc, Johnson & Johnson Services, Inc, Corin, Microport Scientific Corporation, Conformis, B. Braun Melsungen AG, Medacta International, DJO LLC, United Orthopedic Corporation, Meril Life Sciences Pvt. Ltd, Advin Health Care, Auxein Medical, MatOrtho Limited, Surgival, Amplitude, DEDIENNE SANTÉ, Merete GmbH, and Others.

- North America is expected to remain a dominant force in the hip reconstruction/replacement devices market. This is due to the high incidence of hip fractures and avascular necrosis. Escalating healthcare costs, advancements in product development, and the introduction of innovative technologies by key market players in the region are expected to drive the market for hip reconstruction/replacement devices in the forthcoming years.

- In the product type segment of the hip reconstruction/replacement devices market, the total hip replacement implants category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @Hip Reconstruction/Replacement Devices Market

Hip Reconstruction/Replacement Devices Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 9,254.50 million |

|

2034 Projected Market Size |

USD 14,917.71 million |

|

Growth Rate (2026-2034) |

5.51% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Highly Consolidated |

Factors Contributing to the Growth of the Hip Reconstruction/Replacement Devices Market

-

The increasing cases of bone-related disorders leading to a surge in the hip reconstruction/replacement devices market

The growing prevalence of bone-related disorders such as osteoarthritis, rheumatoid arthritis, osteoporosis, and avascular necrosis is a major factor driving the demand for hip reconstruction and replacement devices. These chronic conditions cause progressive joint degeneration, pain, and mobility loss, necessitating surgical intervention to restore normal hip function. With an aging global population and lifestyle factors contributing to musculoskeletal deterioration, the number of patients requiring hip joint reconstruction continues to rise. Consequently, the demand for advanced implant materials, minimally invasive procedures, and durable prosthetic designs is boosting the overall growth of the hip reconstruction/replacement devices market.

-

The rising product development activities among key market players

Ongoing technological innovations and increased research and development activities are significantly propelling the hip reconstruction/replacement devices market. Manufacturers are focusing on developing next-generation implants that offer enhanced biocompatibility, longevity, and mechanical performance. Innovations such as 3D-printed implants, hybrid fixation systems, and bioresorbable materials are transforming surgical outcomes by improving fit, reducing wear, and minimizing postoperative complications. Additionally, the integration of digital surgical planning tools and robotic-assisted systems further supports precision in implant placement. These advancements, coupled with regulatory approvals and product launches, continue to strengthen market growth and adoption globally.

-

Increasing cases of hip fractures

The rising incidence of hip fractures, particularly among the elderly population, is another key factor accelerating the hip reconstruction/replacement devices market. Age-related bone weakening due to osteoporosis and accidental falls are leading causes of such injuries, often necessitating partial or total hip replacement surgeries. According to global health estimates, millions of hip fractures occur annually, with the number expected to increase substantially as life expectancy rises. This growing patient pool drives consistent demand for reliable and durable implant solutions, spurring innovation in cemented and non-cemented fixation systems and expanding the market for hip reconstruction and replacement devices worldwide.

Hip Reconstruction/Replacement Devices Market Report Segmentation

This hip reconstruction/replacement devices market report offers a comprehensive overview of the global hip reconstruction/replacement devices market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product Type (Total Hip Replacement System, Partial Hip Replacement System, Hip Revision System, and Hip Resurfacing System), Fixation (Cemented and Non-Cemented), End-User (Hospitals, Orthopedic Clinics, and Others), and Geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing hip reconstruction/replacement devices market.

The hip reconstruction/replacement devices are specialized orthopedic implants and instruments designed to restore mobility and relieve pain in patients with damaged or diseased hip joints, typically due to arthritis, fractures, or other degenerative conditions. These devices include components such as femoral stems, acetabular cups, liners, and fixation systems, which together replace or reconstruct the natural joint structure. By replicating normal hip biomechanics, they enable improved function, stability, and long-term durability following total or partial hip replacement or revision surgeries.

The hip reconstruction and replacement devices market is witnessing robust growth driven by several interrelated factors, including the increasing prevalence of bone-related disorders, rising cases of hip fractures, and ongoing advancements in product development. The growing incidence of conditions such as osteoarthritis, rheumatoid arthritis, and osteoporosis has led to a surge in surgical interventions aimed at restoring joint mobility and alleviating pain, thereby fueling demand for advanced implant solutions.

Simultaneously, the global rise in hip fractures, particularly among the elderly population due to age-related bone fragility and falls, has further amplified the need for effective reconstructive and replacement procedures. In response, manufacturers are accelerating research and development efforts to introduce innovative technologies such as 3D-printed implants, hybrid fixation systems, and bioresorbable materials that enhance implant longevity, fit, and biocompatibility. The integration of digital planning tools and robotic-assisted systems has also improved surgical precision and outcomes. Collectively, these trends are strengthening the adoption and global expansion of hip reconstruction/replacement devices, positioning the market for sustained growth in the coming years.

Get More Insights into the Report @Hip Reconstruction/Replacement Devices Market

What are the latest Hip Reconstruction/Replacement Devices Market Dynamics and Trends?

The growing prevalence of musculoskeletal and degenerative joint diseases continues to significantly boost the demand for hip reconstruction and replacement devices worldwide. As per DelveInsight estimates (2024), approximately 345 million individuals are affected by osteoarthritis globally on average. Amongst this population, 73% of people living with osteoarthritis are older than 55 years, and 60% are female. Moreover, as per the same source, 13.5 million people are living with rheumatoid arthritis globally. Hip reconstruction and replacement devices are essential in alleviating pain and restoring mobility for individuals with advanced joint degeneration. Employed in surgical interventions, these devices help improve the quality of life and functionality, making them crucial in managing the increasing demand for effective solutions in arthritic conditions.

Additionally, estimates also suggest that more than 50-60% of all osteoporotic hip fractures will occur in Asia by the year 2050. In addition to this, it is also projected that the global incidence of hip fractures will rise from 7 to 21 million by 2050. The anticipated surge in hip fractures globally highlights a growing need for hip reconstruction and replacement devices. These devices play a vital role in managing the increasing number of hip injuries, offering effective solutions for restoring mobility and function, and addressing the rising demand driven by the higher incidence of fractures.

Increased product development activities by market key players are also slated to witness the market growth of hip replacement devices. For example, in February 2024, Stryker Corporation announced to showcase new joint-replacement technology and updates to its Mako surgical robotic platform. The company also aimed to reduce intraoperative fluoroscopy in certain hip-replacement procedures.

Additionally, in August 2023, Smith and Nephew, the global medical technology company, announced the launch of its OR3O Dual Mobility System for primary and revision hip arthroplasty in India. Compared to traditional solutions, the dual mobility implants featured a small-diameter femoral head that locked into a larger polyethylene insert, enhancing stability, reducing the risk of dislocation, and providing an improved range of motion.

Therefore, the factors stated above collectively will drive the overall hip reconstruction/replacement devices market during the forecast period.

However, the growth of the global hip reconstruction/replacement devices market faces notable restraints related to postoperative complications and implant-associated risks. Surgical procedures involving hip reconstruction or replacement carry the potential for nerve and blood vessel injuries, leading to bleeding, stiffness, and compromised mobility around the operated joint. Additionally, nerve damage during implantation can result in long-term numbness, muscle weakness, and persistent pain, adversely affecting patient recovery and satisfaction. These complications not only impact clinical outcomes but also increase the need for revision surgeries and postoperative care, thereby elevating overall healthcare costs. Such risks pose a significant challenge to market growth, as both patients and healthcare providers demand safer, more reliable implant technologies with minimal adverse effects.

Hip Reconstruction/Replacement Devices Market Segment Analysis

Hip Reconstruction/Replacement Devices Market by Product Type (Total Hip Replacement System, Partial Hip Replacement System, Hip Revision System, and Hip Resurfacing System), Fixation (Cemented and Non-Cemented), End-User (Hospitals, Orthopedic Clinics, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product Type: Total Hip Replacement System Category Dominates the Market

In the hip reconstruction/replacement devices market, the total hip replacement system category is expected to hold the market share of 40% in 2025. The rapid growth of this product category can be attributed to the features of the total hip replacement system category. These are designed to address severe hip joint damage. The total hip replacement system includes a femoral component and an acetabular component. The femoral component consists of a metal stem that is inserted into the thigh bone, a metal or ceramic ball that replaces the damaged hip socket, and a neck that connects the ball to the stem. The acetabular component is a cup-shaped device that fits into the pelvic bone socket, often lined with a durable material such as polyethylene, ceramic, or metal to reduce friction.

Total hip replacement systems are engineered to replicate the natural movement of the hip joint, providing stability and flexibility. The materials used are selected for their durability and biocompatibility, ensuring that the implant integrates well with the surrounding bone and minimizes the risk of rejection or complications.

An increase in product development activities by the market player is likely to drive the market for this category. For example, in August 2022, Exactech, a developer and producer of innovative implants, instrumentation, and smart technologies for joint replacement surgery, announced the successful completion of the first surgeries using the Spartan™ Stem and Logical™ Cup System for total hip replacement.

Therefore, owing to the above-mentioned factors, the demand for the total hip replacement system category upsurges, thereby the category is expected to witness considerable growth, eventually contributing to the overall growth of the hip reconstruction/replacement devices market during the forecast period.

By Fixation: Non-cemented Category Dominates the Market

The non-cemented category dominates the hip reconstruction/replacement devices market, contributing nearly 52% of global revenue in 2025, due to a convergence of several critical factors, including its superior long-term outcomes, enhanced biological fixation, and growing preference among both surgeons and patients. Unlike cemented implants, which rely on bone cement for immediate stability, non-cemented or press-fit implants achieve fixation through bone ingrowth into specially designed porous or coated implant surfaces. This biological integration provides durable stability, reduces the risk of loosening, and enhances implant longevity, particularly in younger, more active patients. Advances in biomaterials such as titanium alloys, porous coatings, and hydroxyapatite layers have further improved osseointegration and load transfer between the implant and bone.

Additionally, non-cemented fixation methods align well with minimally invasive surgical techniques and modern implant designs, offering reduced surgical time, faster recovery, and easier revision if needed. Orthopedic surgeons increasingly prefer these systems for their ability to preserve bone stock and accommodate future interventions. The shift toward value-based care and long-term implant performance has also encouraged wider adoption, especially in developed markets with aging but active populations. As a result, the non-cemented fixation segment continues to dominate the market, driven by advancements in material science, improved implant design, and growing clinical confidence in biologically stable, long-lasting hip reconstruction outcomes.

By End-User: Hospitals Dominate the Market

The hospitals category dominated the global hip reconstruction/replacement devices market in 2025, due to several key factors, including their advanced surgical infrastructure, multidisciplinary expertise, and capacity to handle complex orthopedic procedures. Hospitals serve as the primary centers for total hip replacement, partial replacement, and revision surgeries, which require specialized equipment, sterile environments, and integrated postoperative care facilities. These institutions benefit from the presence of highly skilled orthopedic surgeons, anesthesiologists, and rehabilitation specialists, enabling them to provide comprehensive patient management from diagnosis through recovery. Moreover, hospitals are leading adopters of cutting-edge technologies such as robotic-assisted surgical systems, computer navigation platforms, and AI-based preoperative planning tools, which enhance surgical accuracy, minimize complications, and improve long-term implant outcomes.

Favorable reimbursement policies and insurance coverage further contribute to hospitals’ leading position, as most hip replacement procedures are covered under inpatient care benefits. Large tertiary and specialty hospitals often have established partnerships with top medical device manufacturers, ensuring access to the latest implants, materials, and surgical innovations. Their ability to perform a high volume of surgeries also promotes operational efficiency and cost optimization, making them attractive both to patients and payers. Additionally, hospitals play a vital role in clinical research and surgeon training, fostering continuous innovation and best practices in orthopedic surgery. Altogether, the combination of advanced resources, technological integration, skilled expertise, and supportive reimbursement structures solidifies hospitals as the cornerstone of the hip reconstruction and replacement devices market.

Hip Reconstruction/Replacement Devices Market Regional Analysis

North America Hip Reconstruction/Replacement Devices Market Trends

North America, led by the U.S., accounted for a dominant share of 43% in the global Hip Reconstruction/Replacement Devices market in 2025. This is due to the high incidence of hip fractures and avascular necrosis. Escalating healthcare costs, advancements in product development, and the introduction of innovative technologies by key market players in the region are expected to drive the market for hip reconstruction/replacement devices in the forthcoming years.

According to DelveInsight analysis (2024), annually, over 30,500 individuals in the U.S. experience a hip fracture, with the majority occurring in those aged 65 and older due to falls in the home or community. Moreover, the estimates suggest that a patient incurs costs of approx USD 40,000 in the first year after a hip fracture, with the annual expense for hip fracture care in the U.S. exceeding USD 17 billion. Hip reconstruction and replacement devices play a crucial role in managing hip fractures, especially among older adults. They are used to restore mobility and function, significantly impacting recovery and reducing long-term healthcare costs.

Additionally, the estimates reported that in the United States, avascular necrosis of the femoral head is estimated to affect between 20,000 and 30,000 new patients each year. This condition contributes to the overall number of total hip arthroplasties performed annually, which totals approximately 250,000 procedures.

Rising product development activities by regulatory bodies in the region will further boost the market for hip reconstruction/replacement devices. For example, in addition to this, in March 2022, Stryker announced the launch of the Insignia hip stem for total hip and hemiarthroplasty procedures. The Insignia stem was designed to be compatible with Stryker’s Mako SmartRobotics platform, which utilizes Total Hip 4.1 software. This integration allowed surgeons to use data from a 3D, CT-based plan to capture each patient’s unique anatomy.

Additionally, the presence of key players such as Zimmer, Stryker, Johnson and Johnson Services, Inc., Exactech, Inc, among others, in the region is also a driving factor for the hip reconstruction/replacement devices market as they hold significant revenue shares.

Therefore, the interplay of all the aforementioned factors would provide a conducive growth environment for the North America region in the hip reconstruction/replacement devices market.

Europe Hip Reconstruction/Replacement Devices Market Trends

The Europe hip reconstruction and replacement devices market is witnessing steady growth, supported by an aging population, high prevalence of musculoskeletal disorders, and a strong tradition of advanced orthopedic care. Western European countries such as Germany, the U.K., France, and Italy remain key demand centers due to their well-established healthcare infrastructure, high procedural volumes, and widespread adoption of technologically advanced implants. The region’s growing elderly population, coupled with lifestyle factors such as obesity and increased participation in physical activities, continues to drive the need for both primary and revision hip replacement surgeries. Additionally, favorable reimbursement frameworks and government-supported healthcare systems contribute to high accessibility and procedural uptake across most European nations.

Technological advancement remains a defining trend in the European market. The adoption of minimally invasive surgical approaches, robotic-assisted hip replacement, and computer-navigated systems is enhancing procedural accuracy and improving postoperative outcomes. Moreover, manufacturers are increasingly focusing on biomaterial innovation, with growing use of advanced ceramics, titanium alloys, and porous coatings designed to enhance osseointegration and implant longevity. The emergence of 3D printing and patient-specific implant design is also gaining traction, allowing for greater customization and biomechanical precision in complex reconstructions.

The market is further shaped by a strong emphasis on research collaborations, clinical evidence generation, and digital transformation. Many hospitals and orthopedic centers in Europe are integrating AI-based surgical planning, data analytics, and outcome-tracking systems to optimize implant performance and support value-based care initiatives. Sustainability is also becoming a key strategic focus, with manufacturers adopting eco-friendly production processes and recyclable materials to meet the region’s stringent environmental standards.

Hence, the Europe hip reconstruction and replacement devices market is advancing toward greater precision, personalization, and sustainability. Supported by high healthcare standards, continuous innovation, and a growing focus on digital and robotic-assisted orthopedic solutions, Europe remains a mature yet evolving hub for next-generation hip replacement technologies.

Asia-Pacific Hip Reconstruction/Replacement Devices Market Trends

The Asia-Pacific hip reconstruction and replacement devices market is experiencing strong and sustained growth, driven by rapid population aging, a rising incidence of osteoarthritis and hip fractures, and expanding access to advanced orthopedic care. Countries such as Japan, China, and India are witnessing a sharp increase in joint replacement procedures as older adults seek to maintain mobility and improve quality of life. The region’s healthcare infrastructure is evolving rapidly, supported by higher disposable incomes and growing awareness of modern surgical solutions. Medical tourism has also become a significant growth catalyst, with India, Thailand, and Malaysia emerging as leading destinations for high-quality yet cost-effective hip replacement surgeries that attract patients from across the globe.

Technological innovation is playing a pivotal role in shaping the market’s evolution. The adoption of minimally invasive surgical techniques, cementless fixation, dual-mobility cup systems, and 3D-printed patient-specific implants is enhancing surgical precision, shortening recovery times, and improving long-term outcomes. Furthermore, global manufacturers are expanding their regional presence through localized production facilities, strategic partnerships, and collaborations with healthcare providers to address growing demand efficiently. Simultaneously, domestic players in countries such as China, India, and South Korea are strengthening their competitive position by offering affordable, high-performance implant solutions tailored to local needs.

Therefore, the Asia-Pacific hip reconstruction and replacement devices market is poised for substantial expansion as demographic trends, technological advancement, and regional manufacturing initiatives converge. With continuous innovation, improved healthcare accessibility, and the growing adoption of smart and personalized implant technologies, the region is set to become a major hub for orthopedic excellence and next-generation joint reconstruction solutions.

Who are the major players in the Hip Reconstruction/Replacement Devices Market?

The following are the leading companies in the hip reconstruction/replacement devices market. These companies collectively hold the largest market share and dictate industry trends.

- Zimmer Biomet

- Stryker Corporation

- Smith & Nephew,

- Exactech, Inc

- Johnson & Johnson Services, Inc

- Corin

- Microport Scientific Corporation

- Conformis

- B. Braun Melsungen AG

- Medacta International

- DJO LLC

- United Orthopedic Corporation

- Meril Life Sciences Pvt. Ltd

- Advin Health Care

- Auxein Medical

- MatOrtho Limited

- Surgival

- Amplitude

- DEDIENNE SANTÉ

- Merete GmbH

How is the competitive landscape shaping the Hip Reconstruction/Replacement Devices market?

The competitive landscape of the hip reconstruction and replacement devices market is shaped by a mix of technological innovation, strategic consolidation, and growing emphasis on value-based care. The market is highly concentrated, dominated by a few key players such as Stryker, Zimmer Biomet, DePuy Synthes (Johnson & Johnson), and Smith+Nephew, which collectively account for a major share of global revenue. These companies leverage extensive product portfolios, global distribution networks, and continuous R&D investment to maintain a competitive advantage. Innovation remains a key differentiator; firms are focusing on AI-driven preoperative planning, robotic-assisted surgery platforms, and advanced biomaterials such as titanium alloys, ceramics, and bioresorbable composites to improve implant longevity and patient outcomes.

Strategic partnerships and acquisitions are further reshaping competition, enabling companies to expand technological capabilities and geographic reach while enhancing their position in fast-growing segments like minimally invasive and outpatient hip procedures. Smaller and emerging players are contributing niche innovations, especially in 3D printing, patient-specific implants, and smart sensor-enabled prosthetics, but face challenges in scaling production and navigating stringent regulatory pathways.

Additionally, competition is intensifying around service models, with manufacturers offering data-driven support, digital surgical ecosystems, and outcome-based reimbursement frameworks to strengthen customer loyalty.

Overall, the market’s competitive dynamics are evolving toward technology integration, portfolio diversification, and cost optimization. Large incumbents are consolidating their dominance through innovation and partnerships, while agile new entrants are driving niche advancements, collectively pushing the hip reconstruction and replacement devices market toward a more intelligent, connected, and outcomes-focused future.

Recent Developmental Activities in the Hip Reconstruction/Replacement Devices Market

- In July 2025, MatOrtho® announced that the ReCerf® Hip Resurfacing Arthroplasty (HRA) received the CE mark, confirming compliance with European safety and performance standards.

- In July 2025, a novel hip implant developed by spin-out Embody Orthopaedic of Imperial College London received the CE Mark, marking a significant milestone in hip arthroplasty. The device, known as the H1 implant, is designed to extend the option of hip resurfacing surgery to women and smaller-built men groups previously excluded from this treatment due to anatomical and wear-related issues.

- In July 2024, Smith & Nephew announced that it received 510(k) clearance from the United States Food and Drug Administration for its new CATALYSTEM Primary Hip System. The system was designed to meet the evolving needs of primary hip surgery, including the growing adoption of anterior approach procedures and the expanding role of Ambulatory Surgery Centers (ASCs).

- In March 2024, Ortho Development Corporation, a designer and manufacturer of orthopedic implants and instruments for hip and knee joint replacement surgery, announced the receipt of U.S. Food and Drug Administration (FDA) 510(k) clearance for the Trivicta™ Hip System. The clearance was granted for the triple-taper femoral stem, which was designed to provide an optimal fit within the canal for a wide range of patient anatomies.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Hip Reconstruction/Replacement Devices Market CAGR |

5.51% |

|

Key Companies in the Hip Reconstruction/Replacement Devices Market |

Zimmer Biomet, Stryker Corporation, Smith & Nephew, Exactech, Inc, Johnson & Johnson Services, Inc, Corin, Microport Scientific Corporation, Conformis, B. Braun Melsungen AG, Medacta International, DJO LLC, United Orthopedic Corporation, Meril Life Sciences Pvt. Ltd, Advin Health Care, Auxein Medical, MatOrtho Limited, Surgival, Amplitude, DEDIENNE SANTÉ, Merete GmbH, and Others. |

|

Hip Reconstruction/Replacement Devices Market Segments |

by Product Type, by Fixation, by End-Users, and by Geography |

|

Hip Reconstruction/Replacement Devices Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Hip Reconstruction/Replacement Devices Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Hip Reconstruction/Replacement Devices Market Segmentation

- Hip Reconstruction/Replacement Devices by Component Exposure

- Total Hip Replacement Implants

- Partial Hip Replacement Implants

- Hip Revision Implants

- Hip Resurfacing Implants

- Hip Reconstruction/Replacement Devices Application Exposure

- Cemented

- Non-cemented

- Hip Reconstruction/Replacement Devices End-User Exposure

- Hospitals

- Orthopedic Clinics

- Others

- Hip Reconstruction/Replacement Devices Geography Exposure

- North America Hip Reconstruction/Replacement Devices Market

- United States Hip Reconstruction/Replacement Devices Market

- Canada Hip Reconstruction/Replacement Devices Market

- Mexico Hip Reconstruction/Replacement Devices Market

- Europe Hip Reconstruction/Replacement Devices Market

- United Kingdom Hip Reconstruction/Replacement Devices Market

- Germany Hip Reconstruction/Replacement Devices Market

- France Hip Reconstruction/Replacement Devices Market

- Italy Hip Reconstruction/Replacement Devices Market

- Spain Hip Reconstruction/Replacement Devices Market

- Rest of Europe Hip Reconstruction/Replacement Devices Market

- Asia-Pacific Hip Reconstruction/Replacement Devices Market

- China Hip Reconstruction/Replacement Devices Market

- Japan Hip Reconstruction/Replacement Devices Market

- India Hip Reconstruction/Replacement Devices Market

- Australia Hip Reconstruction/Replacement Devices Market

- South Korea Hip Reconstruction/Replacement Devices Market

- Rest of Asia-Pacific Hip Reconstruction/Replacement Devices Market

- Rest of the World Hip Reconstruction/Replacement Devices Market

- South America Hip Reconstruction/Replacement Devices Market

- Middle East Hip Reconstruction/Replacement Devices Market

- Africa Hip Reconstruction/Replacement Devices Market

- North America Hip Reconstruction/Replacement Devices Market

Hip Reconstruction/Replacement Devices Market Recent Industry Trends and Milestones (2022-2025)

|

Category |

Key Developments |

|

Hip Reconstruction/Replacement Devices Product Launches & Approvals |

Embody Orthopaedic received CE Mark (2025) for its H1 hip resurfacing implant, the world’s first non-metal resurfacing device, extending treatment options to women and smaller patients. Smith & Nephew launched the OR3O Dual Mobility System (2023) in India for primary and revision hip arthroplasty, enhancing stability and reducing dislocation risks. Stryker Corporation unveiled new updates to its Mako SmartRobotics™ platform (2024), featuring improved joint-replacement workflows and reduced intraoperative fluoroscopy. Osteal Therapeutics advanced late-stage trials for its VT-X7 local antibiotic implant (2024), targeting infection prevention in joint replacements. |

|

Partnerships in the Hip Reconstruction/Replacement Devices Market |

Zimmer Biomet entered strategic investment partnerships, including participation in the $50 million Series D funding of Osteal Therapeutics to strengthen infection-prevention technology in arthroplasty. Embody Orthopaedic partnered with Zimmer Biomet for the development and distribution of its CE-marked H1 implant across Europe and global markets. Garland Surgical Ltd received €1.4 million grant from Malta Enterprise (2024) and established partnerships with local research facilities to advance the MaltaHip total hip replacement implant. Insight Surgery collaborated with orthopedic centers in the U.S. (2024) to integrate AI-driven surgical planning systems in hip and knee replacement procedures. |

|

Company Strategy |

Zimmer Biomet expanded its robotic surgery and joint reconstruction portfolio through strategic acquisitions and partnerships (2024–2025), including the Paragon 28 acquisition, strengthening its global orthopedic presence. Stryker enhanced Mako robotics integration and focused on improving intraoperative imaging precision and smart surgical workflow automation. Smith & Nephew focused on product localization strategies in Asia-Pacific and emerging markets to meet the rising demand for hip implants. Startups such as Osteal Therapeutics and Garland Surgical secured targeted funding to advance clinical trials and regulatory pathways, reflecting investor confidence in innovation-led growth. |

|

Emerging Technology |

Robotics and Smart OR Integration: OEMs such as Stryker and Zimmer Biomet advanced integration of AI-driven robotic-assisted systems for enhanced surgical precision. Advanced Implant Materials: Non-metal and dual mobility implants (Embody’s H1 and Smith & Nephew’s OR3O) introduced improved biocompatibility and stability. |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are transforming the hip reconstruction and replacement devices market by driving precision, personalization, and efficiency across the care continuum. Machine learning and predictive analytics enable the design of patient-specific implants by analyzing anatomical and biomechanical data, improving fit, alignment, and long-term durability. These AI-driven customizations reduce complications such as dislocation or loosening, enhance mobility restoration, and minimize revision surgeries.

In surgery, AI-assisted planning tools, robotic systems, and computer vision technologies are revolutionizing accuracy and consistency. They optimize implant positioning, guide real-time decisions, and standardize complex procedures, leading to shorter operating times, fewer errors, and faster recovery. Meanwhile, in manufacturing, AI streamlines design and production through generative modeling, predictive maintenance, and automated quality control, enabling the development of lighter, stronger, and more biocompatible implants.

From a market perspective, AI integration enhances value by improving outcomes and reducing healthcare costs, strengthening competitiveness for manufacturers. However, challenges such as high implementation costs, data security, model transparency, and regulatory hurdles may slow adoption. Ensuring diverse, unbiased datasets and ethical AI use will be vital to prevent disparities in outcomes.

Looking ahead, the convergence of AI with smart biomaterials and sensor-enabled implants could enable continuous postoperative monitoring and predictive maintenance of joint health. As validation and regulation mature, AI-powered hip reconstruction is poised to become a cornerstone of personalized orthopedics, delivering safer surgeries, superior outcomes, and greater long-term efficiency.

U.S. Tariff Impact Analysis on the Hip Reconstruction/Replacement Devices Market:

U.S. tariffs on hip reconstruction and replacement devices would raise costs and squeeze margins across the supply chain, particularly for manufacturers that rely on imported raw materials, specialized components (e.g., cobalt-chromium alloys, custom bearings), or finished implants. Higher import duties increase landed cost for devices and implantable components, likely translating to higher list prices or reduced manufacturer margins. Hospital and ambulatory surgery center procurement teams would face tougher budget trade-offs, potentially slowing purchasing cycles or favoring domestic suppliers where available.

Supply-chain disruption and reshoring incentives would be amplified. Tariffs make vertically integrated or U.S.-based manufacturing more attractive, encouraging capital investment in local production and additive manufacturing, but those shifts take time and raise near-term capital and operating costs. Smaller OEMs that lack scale or capital access would be disproportionately affected. They may outsource more, consolidate, or exit niche segments, reducing competition and innovation variety.

Reimbursement and payer dynamics would magnify the impact. Medicare, Medicaid, and private insurers are cost-sensitive; persistent price increases could prompt tighter formularies, stricter value-based procurement, or pressure on hospitals to substitute lower-cost implants, compressing volumes for higher-priced premium devices. Conversely, stronger “buy American” incentives or procurement preferences could shift market share toward U.S. manufacturers if cost gaps narrow.

Regulatory and compliance burdens would interact with tariff effects. Manufacturers choosing to localize production must navigate FDA device registration, quality systems, and supply validation, adding time and expense before tariff-driven savings are realized. Tariffs may also spur increased vertical integration (component to finished device) to avoid duty exposure, but that requires regulatory oversight and investment in quality infrastructure.

Mitigation strategies and market responses are likely: strategic sourcing diversification, long-term supplier contracts, tariff engineering (reclassifying inputs where lawful), price hedging, and increased adoption of domestic contract manufacturers (CDMOs). Payers and health systems may negotiate bundled pricing or adopt stricter value assessments to contain total episode-of-care costs. Policymakers could counterbalance tariffs with incentives for onshoring or exemptions for critical medical supplies to preserve access and innovation.

Outlook: in the short term, tariffs raise costs, disrupt suppliers, and squeeze smaller players; in the medium-to-long term, they could accelerate domestic manufacturing and consolidation, shifting competitive dynamics but not eliminating demand. The ultimate effect depends on tariff magnitude, duration, availability of domestic capacity, and parallel policy responses (procurement rules, incentives, or exemptions).

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Main Products |

Stage of Development |

Core Technology |

|

Garland Surgical Ltd |

EURO 1.4 million |

MaltaHip Total Hip Replacement Implant |

Pre-commercial / Regulatory preparation |

Advanced hip reconstruction system with improved implant geometry and enhanced biocompatible materials |

Key takeaways from the Hip Reconstruction/Replacement Devices market report study

- Market size analysis for the current hip reconstruction/replacement devices market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the hip reconstruction/replacement devices market.

- Various opportunities available for the other competitors in the hip reconstruction/replacement devices market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the hip reconstruction/replacement devices market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the hip reconstruction/replacement devices market growth in the future?