Plaque Modification Devices Market Summary

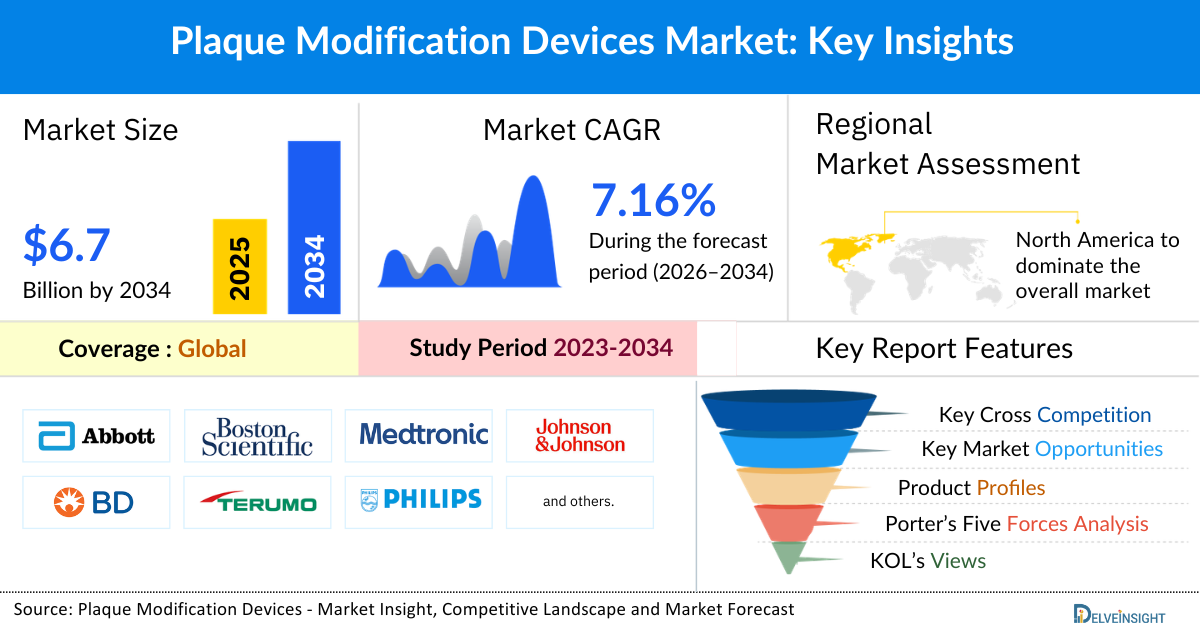

- The global plaque modification devices market is expected to increase from USD 3,622.27 million in 2025 to USD 6,725.92 million by 2034, reflecting strong and sustained growth.

- The global plaque modification devices market is growing at a CAGR of 7.16% during the forecast period from 2026 to 2034.

- The market of plaque modification devices is being primarily driven by the rising cases of atherosclerosis and calcified CAD/PAD, increasing the need for effective vessel-preparation tools during interventions. At the same time, the shift toward minimally invasive endovascular procedures is driving demand for advanced devices that ensure safer and more efficient treatment of complex, calcified lesions. Alongside this, key manufacturers are rapidly introducing new technologies and improving existing products, further boosting clinical adoption. Together, rising disease prevalence, expanding minimally invasive treatments, and continuous product innovation are collectively accelerating the overall growth of the plaque modification devices market.

- The leading companies operating in the plaque modification devices market include Abbott, Boston Scientific Corporation, Medtronic, Johnson & Johnson Services Inc., BD, Terumo Corporation, Koninklijke Philips N.V., Nipro Corporation, AngioDynamics, Inc., Elixir Medical, Avinger Inc., SIS Medical, BrosMed Medical Co., Ltd., OrbusNeich, MicroPort Scientific Corporation., Cagent Vascular, INVAMED, Cordis, Sonosemi Medical Co., Ltd., APR Medtech Ltd., and others.

- North America is expected to dominate the overall plaque modification devices market due to a combination of factors, including the region's advanced healthcare infrastructure, high adoption of technologically advanced medical devices, and increasing prevalence of peripheral artery disease (PAD) and coronary artery disease (CAD). Additionally, the presence of key market players involved in product development activites are further driving demand for plaque modification devices across hospitals in North America. These factors collectively position the region as a leading contributor to the global market.

- In the product type segment of the plaque modification devices market, the specialized balloons category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Plaque Modification Devices Market

Plaque Modification Devices Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 3,622.27 million |

|

2034 Projected Market Size |

USD 6,725.92 million |

|

Growth Rate (2026-2034) |

7.16% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Plaque Modification Devices Market

- Rising prevalence of atherosclerosis and calcified coronary/peripheral artery disease (CAD & PAD) leading to a surge in plaque modification devices: The rising prevalence of atherosclerosis and calcified coronary and peripheral artery disease (CAD & PAD) is one of the strongest forces driving the growth of the plaque modification devices market, as these conditions increasingly lead to complex and heavily calcified arterial blockages that cannot be effectively treated with standard balloon angioplasty or stents alone.

- Rising adoption of minimally invasive endovascular procedures esclating the market of plaque modification devices: The rising adoption of minimally invasive endovascular procedures is significantly boosting the market for plaque modification devices, as healthcare systems worldwide increasingly favor catheter-based interventions over traditional open surgeries due to their lower complication rates, shorter hospital stays, and faster recovery times. With cardiovascular diseases continuing to rise globally, clinicians are treating a growing number of complex arterial blockages using percutaneous techniques, which naturally increases the demand for tools that can effectively prepare calcified or fibrotic vessels for stent delivery and optimal expansion.

- The increase in product development activities among the key market players: The increase in product development activities is playing a pivotal role in boosting the overall market for plaque modification devices by driving innovation, expanding clinical applicability, improving procedural outcomes, and increasing physician confidence in using these tools. The increased product development activities are significantly boosting the plaque modification device market by making devices safer, more effective, easier to use, and suitable for a wider range of lesions. Innovations such as intravascular lithotripsy, super high-pressure balloons, and next-gen atherectomy systems are expanding clinical applications, improving patient outcomes, and transforming how cardiologists approach complex PCI. As R&D accelerates and more advanced technologies emerge, the plaque modification device market is expected to experience sustained, strong growth in the coming years.

Plaque Modification Devices Market Report Segmentation

This plaque modification devices market report offers a comprehensive overview of the global Plaque Modification Devices market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product Type (Atherectomy Devices, Intravascular Lithotripsy (IVL) Systems, Specialized Balloons, {Cutting Balloons, Scoring Balloons, and Others), Application (Coronary Artery Disease and Peripheral Artery Disease), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing plaque modification devices market.

Plaque modification devices are specialized cardiovascular tools used to treat hardened, calcified, and complex atherosclerotic plaques in the coronary and peripheral arteries when standard balloon angioplasty cannot adequately open the vessel. These devices, including atherectomy systems, intravascular lithotripsy (IVL), cutting balloons, scoring balloons, and ultra high-pressure balloons, which are designed to break, shave, score, or fracture calcified plaque to improve vessel compliance.

The overall market of plaque modification devices is being collectively boosted by several converging factors. The rising prevalence of atherosclerosis and calcified CAD/PAD, are increasing the need for effective vessel-preparation tools during interventions. At the same time, the shift toward minimally invasive endovascular procedures is driving demand for advanced devices that ensure safer and more efficient treatment of complex, calcified lesions. Alongside this, key manufacturers are rapidly introducing new technologies and improving existing products, further boosting clinical adoption. Together, rising disease prevalence, expanding minimally invasive treatments, and continuous product innovation are collectively accelerating the overall growth of the plaque modification devices market.

Get More Insights into the Report @ Plaque Modification Devices Market

What are the latest Plaque Modification Devices market dynamics and trends?

The global market for plaque modification devices has witnessed significant growth in recent years, largely driven by the increasing prevalence of atherosclerosis and calcified coronary/peripheral artery disease (CAD & PAD). These conditions increasingly lead to complex and heavily calcified arterial blockages that cannot be effectively treated with standard balloon angioplasty or stents alone.

According to the data provided by the National Health Institute (2024), atherosclerosis is a chronic inflammatory disease of the arteries and is the underlying cause of about 50% of all deaths in westernized society.

Atherosclerosis is significantly boosting the market for plaque modification devices because it leads to the progressive buildup of hardened, calcified plaque inside the arteries, creating lesions that are increasingly difficult to treat with conventional angioplasty or stenting alone and ultimately leading to increased to death rates. As the disease advances, the plaque becomes more rigid and heavily calcified, reducing vessel elasticity and making it challenging for standard balloons to adequately expand the vessel.

This clinical challenge directly fuels the adoption of specialized plaque modification devices such as atherectomy systems, scoring balloons, cutting balloons, intravascular lithotripsy (IVL) systems, and super-high-pressure balloons. These devices offer superior lesion preparation by debulking, cracking, or modifying hardened plaques, making stent deployment easier, safer, and more durable, thereby boosting the overall market of plaque modification devices.

Additionally, according to the British Heart Foundation (2025), the most common cardiovascular conditions are coronary (ischaemic) heart disease with global prevalence estimated at 250 million and peripheral arterial (vascular) disease with global prevalence of 110 million.

Furthermore, according to the data provided by the Institute for Health Metrics and Evaluation (2023), the number of people aged 40 years and older with peripheral artery disease was 113 million globally.

These conditions are characterized by the buildup of atherosclerotic plaques within the arteries, which leads to narrowing or blockage of blood vessels, restricting blood flow to the heart, limbs, and other vital organs. The rising prevalence of CAD and PAD, driven by risk factors such as aging populations, diabetes, obesity, hypertension, and sedentary lifestyles, has significantly increased the need for effective interventional treatments.

Plaque modification devices, including atherectomy systems, orbital and rotational devices, and intravascular lithotripsy tools, play a critical role in preparing calcified or hardened lesions for subsequent stent placement or balloon angioplasty. By facilitating better lesion preparation, these devices improve procedural outcomes, reduce complications, and enhance long-term vessel patency.

Additionally, the increase in product development activities is playing a pivotal role in boosting the overall market for plaque modification devices by driving innovation, expanding clinical applicability, improving procedural outcomes, and increasing physician confidence in using these tools. For instance, in October 2025, FastWave Medical announced new first-in-human and pre-clinical data for its Sola coronary laser intravascular lithotripsy (L-IVL) system. Furthermore, in January 2025, Boston Scientific Corporation announced that it has entered into a definitive agreement to acquire Bolt Medical, Inc., the developer of an intravascular lithotripsy (IVL) advanced laser-based platform for the treatment of coronary and peripheral artery disease.

Thus, the factors mentioned above are expected to boost the overall market of plaque modification devices during the forecast period from 202 to 2034.

However, the market growth of plaque modification devices is significantly constrained by the inherent risk of procedural complications, which makes many clinicians cautious about their routine use, especially in complex or fragile vascular anatomies. Additioanlly, the market for plaque modification devices is significantly limited by the rigorous regulatory clearance standards imposed by agencies such as the U.S. FDA, the European Medicines Agency (EMA), and regulatory bodies across Asia-Pacific, which make it challenging for manufacturers to bring new technologies to market quickly, thereby limiting the market of plaque modification devices.

Plaque Modification Devices Market Segment Analysis

Plaque Modification Devices Market by Product Type (Atherectomy Devices, Intravascular Lithotripsy (IVL) Systems, Specialized Balloons, {Cutting Balloons, Scoring Balloons, and Others), Application (Coronary Artery Disease and Peripheral Artery Disease), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product Type: Specialized Balloons Hold the Largest Revenue Share

In the product type segment of the plaque modification devices market, the others sub-segment of the specialized balloons category, is expected to hold the largest revenue share of 46.52% in 2025. The “others” category of plaque modification devices, which includes super high-pressure balloons (SHPBs), non-compliant (NC) balloons, and semi-compliant (SC) balloons, is significantly driving the overall market growth by addressing a wide range of complex coronary and peripheral artery lesions.

SHPBs, such as SIS Medical’s OPN NC, are specifically designed to withstand extremely high inflation pressures often up to 35–40 atmospheres allowing interventional cardiologists to safely dilate rigid, fibrotic, or heavily calcified plaques that are difficult to treat with conventional balloons.

This capability ensures optimal lumen expansion, proper stent deployment, and a reduction in procedural complications such as restenosis or underexpansion, while enabling the treatment of complex lesions including ostial, bifurcation, and long diffuse calcified segments.

Non-compliant balloons, including Medtronic’s NC Euphora and NC Sprinter RX, Nipro’s Powered 3 NC, and Terumo’s Accuforce, maintain a stable diameter even at high pressures, allowing precise post-dilatation, improved stent apposition, and safe treatment of resistant lesions where semicompliant balloons may fail due to overexpansion or dog-boning.

Semi-compliant balloons, such as Medtronic’s Sprinter Legend RX and Euphora SC, Nipro’s Thouzer™, and Ordis’s IKAZUCHI ZERO SC, provide a controlled degree of compliance that allows them to adapt to vessel anatomy during pre-dilatation and lesion preparation, particularly in tortuous or variable-caliber vessels.

By offering both high-pressure performance and anatomical adaptability, NC and SC balloons enhance deliverability, reduce procedural complications, and enable interventionalists to manage a broader range of lesions with fewer device exchanges.

The combined availability of SHPBs, NC, and SC balloons from multiple manufacturers not only improves procedural outcomes and physician confidence but also encourages competition and broader adoption in hospitals and cardiac centers.

This comprehensive expansion of the therapeutic toolkit for plaque modification ultimately stimulates market growth, increases procedural volumes, and drives continued innovation in the field of interventional cardiology.

By Application: Coronary Artery Disease Category Dominates the Market

Coronary Artery Diseases are significantly boosting the overall market of plaque modification devices holding the major revenue share of 61.71% in 2025, because it represents both the largest global disease burden and the most significant source of complex coronary lesions requiring specialised intervention.

According to the 2024 JACC study titled “Global Prevalence of Coronary Artery Disease: An Update from the Global Burden of Disease Study”, there were an estimated 315 million prevalent cases of CAD worldwide, with a 95% uncertainty interval of 273 to 362 million population.

As CAD patients present with increasingly calcified, fibrotic, and resistant plaques often due to aging populations, diabetes, chronic kidney disease, and long-standing hypertension traditional balloon angioplasty alone is often insufficient to achieve optimal lesion preparation.

This clinical shift creates a greater need for specialized plaque modification technologies such as scoring balloons, cutting balloons, rotational and orbital atherectomy devices, intravascular lithotripsy (IVL), and super-high-pressure balloons, which can modify or debulk hardened plaques to restore vessel compliance and allow successful stent placement.

Furthermore, the growing trend of performing PCI in more complex lesions left main disease, bifurcations, in-stent restenosis, and severe calcification directly increases the utilization of these devices, as proper lesion preparation is essential for long-term stent expansion and patency.

However, the market momentum is further strengthened by continuous innovation and strategic consolidation within the industry.

A notable example occurred in March 2025 when Abbott announced that the U.S. Food and Drug Administration (FDA) have approved an investigational device exemption (IDE) for its Coronary Intravascular Lithotripsy (IVL) System to evaluate the treatment of severe calcification in coronary arteries prior to stenting.

Thus, the hospitals and interventional cardiologists, driven by the need to reduce complications, improve procedural success, and minimize the risk of stent under-expansion, now integrate plaque modification tools as a standard part of coronary interventions.

With increasing CAD prevalence, expanded clinical guidelines supporting calcified-lesion preparation, and rapid innovation by leading manufacturers, the global market for plaque modification devices continues to expand significantly.

Plaque Modification Devices Market Regional Analysis

North America Plaque Modification Devices Market Trends

North America is expected to account for the highest proportion of 38.87% of the plaque modification devices market in 2025, out of all regions. This domination is due to the combination of factors, including the region's advanced healthcare infrastructure, high adoption of technologically advanced medical devices, and increasing prevalence of peripheral artery disease (PAD) and coronary artery disease (CAD). Additionally, the presence of key market players involved in product development activites are further driving demand for plaque modification devices across hospitals in North America. These factors collectively position the region as a leading contributor to the global market.

According to DelveInsight’s 2024 analysis, PAD affected approximately 4.6 million males and 5.2 million females in the country, forming a large patient population that frequently requires advanced endovascular interventions. In parallel, the Centers for Disease Control and Prevention (CDC, 2024) reported that 6.2 million U.S. adults were living with heart failure in 2022, a condition strongly associated with underlying CAD and PAD.

Additionally, as per the same source mentioned above reported that, about 1 in 20 adults age 20 and older have CAD (about 5%) in the United States. Patients with CAD and PAD especially those with long-standing diabetes, chronic kidney disease, and advanced age often present with heavily calcified plaques that limit the effectiveness of conventional balloon angioplasty and stenting. Plaque modification devices such as atherectomy systems, intravascular lithotripsy, and specialty balloons enable effective calcium disruption, improve vessel compliance, and facilitate optimal stent expansion, thereby reducing procedural complications and restenosis rates.

Furthermore, the regulatory approvals are further strengthening market momentum. For example, in March 2025, Abbott announced that the U.S. FDA had granted an Investigational Device Exemption (IDE) for its Coronary Intravascular Lithotripsy (IVL) System, enabling the launch of the TECTONIC Coronary Artery Disease IVL clinical trial, which plans to enroll up to 335 patients across 47 U.S. sites. This regulatory progress reflects growing confidence in plaque-modification technologies and supports their expanded evaluation and clinical adoption. Market expansion is also propelled by active innovation and strategic acquisitions.

In January 2025, Boston Scientific Corporation entered into a definitive agreement to acquire Bolt Medical, Inc., the developer of an advanced laser-based IVL platform for the treatment of both coronary and peripheral artery disease. Such investments highlight the increasing focus of major industry players on next-generation devices aimed at improving outcomes in complex arterial disease.

Therefore, the rising prevalence of CAD and PAD, strong regulatory support, and robust industry innovation are expected to significantly accelerate the growth of the North America plaque modification devices market throughout the forecast period.

Europe Plaque Modification Devices Market Trends

In Europe, the growth of the plaque modification devices market is being strongly driven by the increasing prevalence of coronary artery disease (CAD) and peripheral artery disease (PAD). According to the British Heart Foundation (2024), the UK recorded approximately 403,826 active cases of peripheral artery disease in 2023, highlighting a considerable clinical need for plaque modification technologies including atherectomy systems, intravascular lithotripsy (IVL), cutting and scoring balloons, and ultra-high-pressure balloons to optimize endovascular outcomes.

Additionally, the increase in product development activites among the key market players are further boosting the overall market of plaque modification devices. For instance, in January 2024, BrosMed Medical announced that it has obtained CE mark for the RevoEdge High-Pressure Coronary Cutting Balloon under the European Medical Device Regulation (MDR). Redefining the standards of cutting balloons, this cutting-edge device is designed to offer unparalleled cutting performance and crossability.

Asia-Pacific Plaque Modification Devices Market Trends

The Asia Pacific region is emerging as a significant growth driver for the plaque modification devices market growing at a fastest CAGR of 8.77% during the forecast period from 2026 to 2034, fueled by a increasing prevalence of coronary artery disease (CAD) and peripheral artery disease (PAD), and a high burden of metabolic risk factors. According to a National Library of Medicine study (2023), approximately 330 million individuals in China were affected by some form of cardiovascular disease. This includes 11.4 million cases of coronary heart disease and a large hypertensive population of nearly 245 million adults both major drivers of advanced atherosclerosis and calcified arterial lesions that often require specialized plaque-modification tools during revascularization.

Additionally, the presence of key ,market players involved in product development activities are further boosting the overall market of plaque modification devices across the China. For instance, in February 2024, MicroPort® RotaPace, an associated company of MicroPort® Coronary, has officially received market approval in China for the TomaHawk® Integrated Coronary Intravascular Lithotripsy System (TomaHawk®).

Asia-Pacific’s rapidly advancing healthcare infrastructure, expanding network of catheterization laboratories, and strong governmental support for cardiovascular innovation are accelerating the clinical adoption of plaque-modification devices. Thus, due to the above-mentioned factors, the plaque modification devices market in China is experiencing growth.

Who are the major players in the plaque modification devices market?

The following are the leading companies in the plaque modification devices market. These companies collectively hold the largest market share and dictate industry trends.

- Abbott

- Boston Scientific Corporation

- Medtronic

- Johnson & Johnson Services Inc.

- BD

- Terumo Corporation

- Koninklijke Philips N.V.

- Nipro Corporation

- AngioDynamics, Inc.

- Elixir Medical

- Avinger Inc.

- SIS Medical

- BrosMed Medical Co., Ltd.

- OrbusNeich

- MicroPort Scientific Corporation.

- Cagent Vascular

- INVAMED

- Cordis

- Sonosemi Medical Co., Ltd.

- APR Medtech Ltd.

- Others

How is the competitive landscape shaping the plaque modification devices market?

The competitive landscape of the plaque modification devices market is shaped by a mix of established medical device giants and specialized innovators, resulting in a moderately concentrated yet dynamic environment. Leading players hold significant market shares due to their extensive product portfolios, strong global distribution channels, and ongoing investments in R&D to enhance device performance and clinical outcomes. At the same time, a growing number of niche and emerging companies are introducing novel technologies such as advanced atherectomy systems, intravascular lithotripsy, and specialty balloon catheters intensifying competition and driving innovation. Strategic activities including mergers and acquisitions, partnerships, and regulatory approvals are further influencing market positioning, enabling companies to expand their footprints and complement existing offerings. Overall, while top-tier firms maintain a competitive edge, the influx of new entrants and continuous technological advancements are fostering a competitive landscape that balances concentration with innovation.

Recent Developmental Activities in the Plaque Modification Devices Market

- In October 2025, Elixir Medical, a developer of disruptive technologies to treat cardiovascular disease, today announced key milestone and full market release of its LithiX™ Hertz Contact (HC) Intravascular Lithotripsy System (IVL), following the announcement of CE Mark approval.

- In October 2025, FastWave Medical announced new first-in-human and pre-clinical data for its Sola coronary laser intravascular lithotripsy (L-IVL) system.

- In May 2025, FastWave Medical, a pioneering intravascular lithotripsy (IVL) startup, has secured Institutional Review Board (IRB) approval to commence a coronary feasibility study utilizing Sola™, its novel laser IVL (L-IVL) system. FastWave is partnering with Clinical Accelerator to achieve this milestone, paving the way for its planned U.S. pivotal trial.

- In March 2025, Abbott announced that the U.S. Food and Drug Administration (FDA) has approved an investigational device exemption (IDE) for its Coronary Intravascular Lithotripsy (IVL) System to evaluate the treatment of severe calcification in coronary arteries prior to stenting. The TECTONIC Coronary Artery Disease (CAD) Intravascular Lithotripsy (IVL) clinical trial will enroll up to 335 people in 47 sites in the U.S.

- In January 2025, Amplitude Vascular Systems (AVS), a medical device company focused on safely and effectively treating severely calcified arterial disease with its novel PULSE IVL™ platform, announced that it has completed a Series B round of financing of $36M. The funding will support the U.S. peripheral commercial launch as well as U.S. coronary and carotid IDE trials for the company’s Pulse Intravascular Lithotripsy™ (PIVL™) device.

- In January 2025, Boston Scientific Corporation announced that it has entered into a definitive agreement to acquire Bolt Medical, Inc., the developer of an intravascular lithotripsy (IVL) advanced laser-based platform for the treatment of coronary and peripheral artery disease.

- In January 2025, The FireRaptor® Integrated Coronary Rotational Atherectomy System, including the FireRaptor® Coronary Rotational Atherectomy Console, the FireRaptor® Coronary Atherectomy Catheter, and the FireRaptor® Coronary Atherectomy Guidewire, developed by MicroPort® RotaPace, has officially received market approval in China.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Plaque Modification Devices Market CAGR |

7.16% |

|

Key Companies in the Plaque Modification Devices Market |

Abbott, Boston Scientific Corporation, Medtronic, Johnson & Johnson Services Inc., BD, Terumo Corporation, Koninklijke Philips N.V., Nipro Corporation, AngioDynamics, Inc., Elixir Medical, Avinger Inc., SIS Medical, BrosMed Medical Co., Ltd., OrbusNeich, MicroPort Scientific Corporation., Cagent Vascular, INVAMED, Cordis, Sonosemi Medical Co., Ltd., APR Medtech Ltd., and others. |

|

Plaque Modification Devices Market Segments |

by Product Type, by Application, and by Geography |

|

Plaque Modification Devices Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Plaque Modification Devices Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Plaque Modification Devices Market Segmentation

- Plaque Modification Devices by Product Type Exposure

- Atherectomy Devices

- Intravascular Lithotripsy (IVL) Systems

- Specialized Balloons

- Cutting Balloons

- Scoring Balloons

- Others

- Plaque Modification Devices Application Exposure

- Coronary Artery Disease

- Peripheral Artery Disease

- Plaque Modification Devices Geography Exposure

- North America Plaque Modification Devices Market

- United States Plaque Modification Devices Market

- Canada Plaque Modification Devices Market

- Mexico Plaque Modification Devices Market

- Europe Plaque Modification Devices Market

- United Kingdom Plaque Modification Devices Market

- Germany Plaque Modification Devices Market

- France Plaque Modification Devices Market

- Italy Plaque Modification Devices Market

- Spain Plaque Modification Devices Market

- Rest of Europe Plaque Modification Devices Market

- Asia-Pacific Plaque Modification Devices Market

- China Plaque Modification Devices Market

- Japan Plaque Modification Devices Market

- India Plaque Modification Devices Market

- Australia Plaque Modification Devices Market

- South Korea Plaque Modification Devices Market

- Rest of Asia-Pacific Plaque Modification Devices Market

- Rest of the World Plaque Modification Devices Market

- South America Plaque Modification Devices Market

- Middle East Plaque Modification Devices Market

- Africa Plaque Modification Devices Market

- North America Plaque Modification Devices Market

Plaque Modification Devices Market Recent Industry Trends and Milestones (2022-2026)

|

Category |

Key Developments |

|

Plaque Modification Devices Regulatory Approvals |

MicroPort® - FireRaptor® (NMPA), MicroPort®- TomaHawk® (NMPA), AngioDynamics, Inc. - Auryon XL (FDA) |

|

Product Launch in the Plaque Modification Devices Market |

Elixir Medical launched LithiX™ Hertz Contact (HC) Intravascular Lithotripsy System, |

|

Acquisition in the Plaque Modification Devices Market |

Boston Scientific Corporation entered into a definitive agreement to acquire Bolt Medical, Inc., Johnson & Johnson announced that it had completed its acquisition of Shockwave Medical. |

|

Company Strategy |

Shockwave Medical (Johnson & Johnson MedTech) and Boston Scientific focused heavily on developing differentiated technologies like intravascular lithotripsy (IVL) and advanced atherectomy systems to address heavily calcified lesions more safely and effectively, Abbott Laboratories and Medtronic pursue acquisitions and strategic integrations to broaden their cardiovascular portfolios. By acquiring innovative plaque modification technologies or complementary devices, these companies enhance their end-to-end interventional offerings. |

|

Emerging Technology |

Micro-drill and novel debulking technologies, high-frequency vibro-atherectomy, smart/adaptive device feedback systems, hybrid and combination approaches, and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are increasingly being integrated into plaque modification devices and associated interventional workflows to improve procedural precision, patient outcomes, and clinical decision-making. Machine learning algorithms are being developed to analyze pre-procedural imaging, such as intravascular ultrasound (IVUS), optical coherence tomography (OCT), and CT angiography, to accurately characterize plaque composition, quantify calcification, and predict lesion compliance, enabling clinicians to select the most appropriate plaque modification strategy. During procedures, AI-assisted guidance systems can provide real-time feedback on device positioning, optimal atherectomy passes, and energy delivery, helping to reduce operator variability and procedural risks. Furthermore, predictive analytics models are being used to forecast restenosis likelihood and long-term outcomes based on patient-specific anatomical and procedural data, which supports personalized treatment planning. Beyond the devices themselves, AI is also enhancing training simulators and robotic-assisted interventional platforms, allowing practitioners to refine their skills in complex plaque modification scenarios. Collectively, these AI-powered applications are transforming the plaque modification landscape by enhancing accuracy, standardizing care, and driving more data-driven, outcome-oriented interventions.

U.S. Tariff Impact Analysis on Plaque Modification Devices Market:

U.S. tariff policies have had a noticeable impact on the broader medical device market, including segments relevant to plaque modification devices, by influencing costs, supply chains, and market dynamics. Higher tariffs on imported medical equipment and components many of which are sourced from key manufacturing hubs in Asia and Europe are pushing up production costs for device makers, potentially leading manufacturers to either absorb the added expenses or pass them on through higher prices for hospitals and healthcare providers. This dynamic can compress profit margins and slow growth in sectors such as cardiovascular and interventional devices, where international supply chains are deeply integrated, because companies like Medtronic, Abbott, and Boston Scientific rely on imported parts and finished products for the U.S. market.

Tariff-induced cost increases and supply chain disruptions may also affect accessibility and adoption of advanced plaque modification technologies; higher device prices can strain hospital procurement budgets especially in smaller or rural facilities leading to delayed purchases or preference for lower-cost alternatives. Furthermore, tariff uncertainty complicates long-term planning and investment, potentially slowing innovation and production expansion, as firms reevaluate manufacturing locations or explore reshoring to mitigate tariff exposure.

At the same time, policy responses such as domestic manufacturing incentives or trade negotiations could reshape competitive positioning over time, influencing where and how plaque modification devices are produced and priced. Overall, while tariffs aim to bolster U.S. manufacturing, their short- to mid-term effects on the plaque modification devices market include increased costs, supply chain vulnerabilities, and slower adoption rates, all of which can impact market growth and strategic decision-making for manufacturers and healthcare systems alike.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Main Products |

Stage of Development |

Core Technology |

|

SpectraWAVE, Inc. |

$50M |

HyperVue™ |

Series B |

SpectraWAVE’s HyperVue™ Imaging System combines DeepOCT™ and near-infrared spectroscopy (NIRS) to image coronary arteries, guiding interventional procedures. NIRS helps identify high-risk plaques and patients, supporting better treatment decisions in the cath lab. |

|

AVS |

$20M |

Advance Plaque-shattering Arterial Disease Treatment |

Series B |

The system that AVS is developing uses pressure waves to shatter calcium that has built up in arteries. |

Key takeaways from the plaque modification devices market report study

- Market size analysis for the current plaque modification devices market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the plaque modification devices market.

- Various opportunities available for the other competitors in the plaque modification devices market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current plaque modification devices market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the plaque modification devices market growth in the future?