Vascular Closure Devices Market Summary

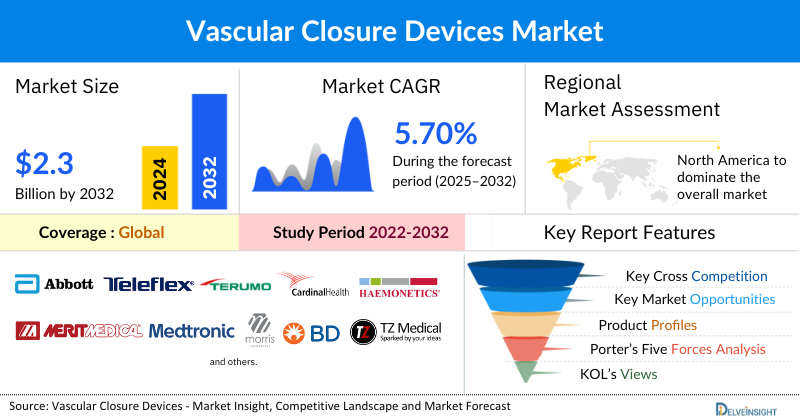

- The global vascular closure devices market is expected to increase from USD 1,548.87 million in 2024 to USD 2,398.52 million by 2032, reflecting strong and sustained growth.

- The global vascular closure devices market is growing at a CAGR of 5.70% during the forecast period from 2025 to 2032.

- The market of vascular closure devices is being primarily driven by the increasing prevalence of cardiovascular diseases and associated risk factors, growing adoption of minimally invasive procedures, increasing technological advancements in devices, and an increase in product development activities among the key market players.

- The leading companies operating in the vascular closure devices market include Abbott, Teleflex Incorporated, Terumo Medical Corporation, Cardinal Health, Haemonetics Corporation, Merit Medical Systems, Medtronic, Morris Innovative, BD, TZ Medical, Vasorum Ltd, Tricol Biomedical, Vivasure Medical Ltd., Transluminal Technologies, W. L. Gore & Associates, Inc., Meril Life Sciences Pvt. Ltd., Gem srl, Vasorum Ltd., Rex Medical, Tricol Biomedical, and others.

- North America is expected to dominate the overall vascular closure devices market due to its high prevalence of cardiovascular diseases and an aging population, which drives demand for interventional procedures. The region's advanced healthcare infrastructure, high expenditure, and rapid adoption of new technologies also contribute to its dominance. Additionally, favorable reimbursement policies and a growing trend toward outpatient procedures, which VCDs facilitate, further solidify its market leadership.

- In the product type of devices segment of the vascular closure devices market, the active approximators category is estimated to account for the largest market share in 2024.

Request for unlocking the report of the @Vascular Closure Devices Market

Vascular Closure Devices Market Size and Forecasts

|

Report Metrics |

Details |

|

2024 Market Size |

USD 1,548.87 million |

|

2032 Projected Market Size |

USD 2,398.52 million |

|

Growth Rate (2025-2032) |

5.70% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Consolidated |

Factors Contributing to the Growth of the Vascular Closure Devices Market

- Increasing prevalence of cardiovascular diseases and associated risk factors leading to a surge in vascular closure devices: The rise in cardiovascular diseases (CVDs) and related risk factors is a major driver for the vascular closure device (VCD) market. An aging global population and lifestyle-related issues like obesity and diabetes are increasing the number of patients with CVDs. This leads to a surge in minimally invasive procedures, such as angioplasty, that require quick and effective vessel closure. VCDs are essential for these procedures, as they reduce complications, shorten recovery times, and allow for earlier patient discharge, directly boosting their demand.

- Growing adoption of minimally invasive procedures is escalating the market of vascular closure devices: The growing adoption of minimally invasive procedures is a key driver for the vascular closure device (VCD) market. These procedures, such as angioplasty and stenting, are increasingly favored over traditional open surgery because they offer benefits like smaller incisions, less pain, and faster recovery. VCDs are essential to these procedures, as they provide a quick and reliable way to seal the arterial access site, significantly reducing hemostasis time and allowing for earlier patient mobilization and discharge. This, in turn, improves patient comfort and workflow efficiency in hospitals and ambulatory surgical centers, making VCDs a critical component of modern, cost-effective healthcare.

- Increasing technological advancements in vascular closure devices: Technological advancements in vascular closure devices (VCDs) are a key market driver. Innovations in large-bore closure are supporting complex procedures like TAVR, which require devices to seal larger punctures safely. The use of bioabsorbable materials reduces long-term complications and improves patient safety. Additionally, enhanced efficiency and automated features in new VCDs are helping to shorten procedure times and facilitate faster patient recovery, making these devices a vital tool for modern healthcare.

Vascular Closure Devices Market Report Segmentation

This vascular closure devices market report offers a comprehensive overview of the global Vascular Closure Devices market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product Type (Active Approximators [Suture-Based, Clip-Based, and Assisted Compression Devices], Passive Approximators [Sealant-Or-Gel-Based and Bio-absorbable Plugs], and Others), Access (Femoral and Radial), End-User (Hospitals & Clinics, Ambulatory Surgical Centers, and Others), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing vascular closure devices market.

A vascular closure device (VCD) is a medical device used to seal the small puncture hole in an artery after a catheter-based procedure, such as a cardiac catheterization or other endovascular surgery. During these procedures, a catheter is inserted through a small incision in the skin (often in the groin, using the femoral artery) to access a blood vessel. At the end of the procedure, this hole, known as the access site, needs to be closed to prevent bleeding.

The overall market for vascular closure devices is experiencing significant growth, driven by a convergence of powerful factors. The rising prevalence of cardiovascular diseases (CVDs) globally, fueled by an aging population and lifestyle risk factors, is leading to a higher volume of diagnostic and interventional procedures like cardiac catheterization and angioplasty.

Simultaneously, the growing adoption of minimally invasive techniques is increasing the demand for efficient and effective closure solutions. These devices are crucial for reducing complications, such as bleeding and hematoma, and significantly shortening patient recovery time and hospital stays, which aligns with the shift toward outpatient and ambulatory surgical centers.

Furthermore, continuous technological advancements are a key driver. Innovations in device design and materials, including the development of bioabsorbable plugs, suture-based systems, and clip-based devices, are enhancing the safety, precision, and ease of use of VCDs. This ongoing product development by major players in the market is expanding the range of innovative solutions, catering to different procedural needs, including large-bore procedures. These advancements, combined with the focus on improving patient outcomes and overall procedural efficiency, are fueling the strong market expansion.

Get More Insights into the Report @Vascular Closure Devices Market

What are the latest Vascular Closure Devices Market Dynamics and Trends?

The vascular closure devices (VCD) market is witnessing strong growth, driven by the rising prevalence of cardiovascular diseases (CVDs) and associated risk factors such as hypertension, diabetes, and obesity. According to DelveInsight’s estimates (2024), in 2023, the 7MM accounted for nearly 26 million cases of atherosclerotic cardiovascular disease, a figure projected to rise further by 2034. Since these procedures typically require arterial access, the need for efficient closure solutions is critical to minimize bleeding complications, accelerate recovery, and improve patient outcomes.

With the global burden of CVD increasing, hospitals and clinics are performing a higher volume of catheter-based interventions, thereby fueling demand for VCDs as an essential component of post-procedural care. Additionally, as per our analyst estimates (2025), in 2024, approximately 590 million adults (aged 20-79 years) were living with diabetes worldwide, with the number expected to reach 854 million by 2050. Given the significantly higher cardiovascular risk in diabetic patients, who often require angiography, angioplasty, and other catheter-based procedures, the growing diabetic population is further accelerating demand for safe and effective vascular closure solutions.

Moreover, active product development and regulatory approvals are strengthening the market outlook. For example, in September 2024, Cordis received FDA approval for its MYNX Control venous VCD (6-12F), featuring Grip Technology with hydrophilic polyethylene glycol (PEG). The MYNX Control sealant reportedly resorbs three times faster than collagen-based alternatives, enabling rapid hemostasis and improved patient safety.

While the market for vascular closure devices is growing due to rising cardiovascular disease rates and the shift toward minimally invasive procedures, its future expansion faces significant hurdles. A major limiting factor is the risk of complications, which includes bleeding, hematoma, vessel injury, infection, and arterial occlusion. These risks can lead to serious patient issues, increased healthcare costs, and a cautious approach by clinicians. Additionally, the stringent regulatory standards imposed by bodies like the FDA present a major barrier. The approval process for these devices is long, costly, and requires extensive clinical trials to prove safety and efficacy. This, combined with the need for continuous post-market surveillance, can delay the market entry of new products and stifle innovation, ultimately hindering overall market growth.

Vascular Closure Devices Market Segment Analysis

Vascular Closure Devices Market by Product Type (Active Approximators [Suture-Based, Clip-Based, and Assisted Compression Devices], Passive Approximators [Sealant-Or-Gel-Based and Bio-absorbable Plugs], and others), Access (Femoral and Radial), End-User (Hospitals & Clinics, Ambulatory Surgical Centers, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product Type: Active Approximators Category Dominates the Market

In the vascular closure devices market, the active approximators category is led by the suture-based segment, which is projected to dominate in 2024, accounting for around 60% of the market share. Suture-based active approximators are significantly boosting the overall market of vascular closure devices by providing a highly reliable and effective solution for sealing large-bore arterial access sites, particularly in complex cardiovascular and endovascular interventions. Unlike traditional manual compression or simpler closure methods, these devices use precise suture-mediated mechanisms to actively approximate and close the vessel wall, which ensures stronger hemostasis and reduces the risk of complications such as bleeding, pseudoaneurysm, or infection. Their ability to handle large sheath sizes makes them especially valuable in transcatheter aortic valve replacement (TAVR), endovascular aneurysm repair (EVAR), and other advanced catheter-based procedures that are rapidly increasing worldwide due to the growing prevalence of cardiovascular diseases.

Moreover, suture-based active approximators enable faster patient mobilization, shorter hospital stays, and improved overall procedural efficiency, aligning well with the healthcare industry’s push toward minimally invasive techniques and enhanced patient outcomes. Continuous product development by leading manufacturers, combined with growing physician preference for dependable and versatile closure methods, is further driving adoption. For instance, in June 2024, Haemonetics received FDA premarket approval for the Vascade MVP XL mid-bore venous closure system, followed by a limited market release and a full market release to U.S. hospitals in August 2024.

As a result, suture-based active approximators are not only expanding their market share but also accelerating the growth of the vascular closure devices market as a whole by setting new standards in safety, efficacy, and applicability across a wide range of cardiovascular interventions.

By Access: Femoral Category Dominates the Market

Within the access segment of the vascular closure devices market, the femoral is anticipated to dominate, accounting for around 85% of the market share in 2024. The femoral artery remains the primary access site for many cardiovascular and endovascular interventions, including angioplasty, TAVR, and EVAR, due to its large size and ease of catheter insertion. However, it carries higher risks of bleeding and complications compared to radial access, driving demand for vascular closure devices (VCDs). Devices such as suture-based approximators, collagen plugs, and sealant systems enable rapid hemostasis, lower complication rates, and faster recovery. With rising cardiovascular cases, increasing large-bore femoral procedures, and ongoing technological advancements, the need for reliable closure systems is growing. Supporting this, a study of over 28,000 atrial fibrillation patients showed VCDs significantly reduced vascular complications and bleeding, reinforcing their clinical value and boosting market growth.

By End-User: Hospitals & Clinics Dominate the Market

In the vascular closure devices market, hospitals and clinics are expected to remain the largest end-user segment in 2024, driven by the high volume of cardiovascular and endovascular procedures performed in these settings. Their advanced infrastructure, availability of skilled specialists, and ability to handle complex interventions such as TAVR, EVAR, and angioplasty make them the primary users of closure devices. Additionally, the growing patient pool, preference for minimally invasive treatments, and continuous adoption of new technologies further strengthen their dominance in the market.

Vascular Closure Devices Market Regional Analysis

North America Vascular Closure Devices Market Trends

North America is projected to dominate the global vascular closure devices (VCD) market in 2024, holding nearly 45% of the total share. This leadership is primarily attributed to the region’s high prevalence of cardiovascular diseases, an aging population driving interventional procedures, and a well-established healthcare infrastructure. High healthcare expenditure, rapid adoption of advanced technologies, favorable reimbursement policies, and a growing shift toward outpatient procedures, where VCDs play a critical role, further reinforce its dominance.

According to DelveInsight’s estimates (2024), the United States had approximately 38.6 million people living with diabetes in 2024, a figure projected to rise to 43.5 million by 2050. Additionally, in 2023, around 14 million males and 11,000 females in the U.S. were affected by atherosclerotic cardiovascular disease. The rising prevalence of diabetes and CVDs significantly boosts demand for VCDs, as these conditions often necessitate diagnostic and interventional procedures such as angiography, angioplasty, TAVR, and EVAR. Diabetic patients, in particular, face higher cardiovascular risks, requiring frequent arterial access and making effective closure solutions essential to minimize bleeding, enhance recovery, and improve safety.

Moreover, the increasing preference for minimally invasive procedures is creating additional momentum for VCD adoption. These interventions rely on small puncture-based arterial access rather than open incisions, offering faster recovery and fewer complications. A recent regulatory milestone underscores this trend. In March 2025, Vasorum USA, Inc. received FDA approval for its Celt ACD Plus System, a next-generation small-bore arterial closure device designed to enhance procedural outcomes.

Taken together, these factors position North America as the leading market for vascular closure devices, with continued growth expected through rising procedure volumes, chronic disease burden, and sustained innovation.

Europe Vascular Closure Devices Market Trends

Europe is driving growth in the vascular closure devices market due to its rapidly rising burden of cardiovascular diseases, an aging population requiring more interventional procedures, and strong adoption of minimally invasive techniques such as angioplasty, TAVR, and EVAR. The region benefits from well-established healthcare infrastructure, increasing investments in advanced catheter-based interventions, and widespread physician preference for closure devices over manual compression to improve patient outcomes. Additionally, favorable regulatory approvals, such as CE marks for innovative closure systems like Vivasure’s PerQseal Elite, are accelerating market penetration. Growing awareness among patients, along with supportive reimbursement policies across many European countries, further strengthens the adoption of vascular closure devices, making Europe one of the key contributors to global market expansion..

Asia-Pacific Vascular Closure Devices Market Trends

Asia-Pacific is emerging as a major growth driver for the vascular closure devices market due to its large and growing patient population, rising prevalence of diabetes and cardiovascular diseases, and increasing adoption of minimally invasive procedures. Rapid improvements in healthcare infrastructure, particularly in countries like China, India, and Japan, are supporting higher volumes of catheter-based interventions such as angioplasty and TAVR, creating strong demand for reliable closure solutions. Additionally, greater awareness of advanced treatment options and rising investments by global and regional players to introduce innovative closure devices in the region are accelerating market growth. Favorable government initiatives and improving reimbursement frameworks are further boosting adoption, positioning Asia-Pacific as one of the fastest-growing markets for vascular closure devices.

Who are the major players in the vascular closure devices market?

The following are the leading companies in the vascular closure devices market. These companies collectively hold the largest market share and dictate industry trends.

- Abbott

- Teleflex Incorporated

- Terumo Medical Corporation

- Cardinal Health

- Haemonetics Corporation

- Merit Medical Systems

- Medtronic

- Morris Innovative

- BD

- TZ Medical

- Vasorum Ltd.

- Tricol Biomedical

- Vivasure Medical Ltd.

- Transluminal Technologies

- W. L. Gore & Associates, Inc.

- Meril Life Sciences Pvt. Ltd.

- Gem srl

- Vasorum Ltd.

- Rex Medical

- Tricol Biomedical

- Others

How is the competitive landscape shaping the vascular closure devices market?

The competitive landscape of the vascular closure devices (VCDs) market is moderately concentrated, with major players like Abbott, Terumo, Cardinal Health, and Teleflex dominating through strong brand presence, broad product portfolios, and global networks. Growth is being shaped by a focus on large-bore closure devices for procedures such as TAVR and EVAR, where technologies like Teleflex’s MANTA are becoming critical. At the same time, smaller companies are driving innovation with bioabsorbable and specialized venous closure solutions, often leading to acquisitions by larger firms, as seen with Haemonetics acquiring Cardiva Medical. Strategic mergers, partnerships, and geographic expansion into high-growth regions like Asia-Pacific further intensify competition, ensuring a dynamic balance between established leaders and niche innovators.

Recent Developmental Activities in the Vascular Closure Devices Market

- In June 2025, Vivasure Medical announced that it had received European CE Mark approval for an expanded indication for its fully bioresorbable, sutureless PerQseal Elite, covering large-bore venous closure.

- In May 2025, Zylox-Tonbridge secured regulatory clearance for its ZYLOX Unicorn™ VCD in Indonesia, marking its first international approval and first Southeast Asian market entry.

- In September 2024, Cordis received FDA approval for its MYNX Control venous vascular closure device (VCD), designed for access sites ranging from 6-12F. Utilizing Grip Technology with hydrophilic polyethylene glycol (PEG), the MYNX Control sealant reportedly resorbs three times faster than collagen-based alternatives, ensuring rapid hemostasis.

- In August 2024, Haemonetics announced the full market launch of its Vascade MVP XL mid-bore venous closure system in the U.S. This system, part of the Vascade portfolio, features an expanded collagen use and a larger disc, suitable for 10–12F sheaths in procedures like cryoablation and left atrial appendage closure.

- In July 2024, Cordis obtained FDA approval for the Mynx Control VCD for 6-12 French access sites, aiming for a launch soon after.

- In June 2024, Haemonetics introduced a limited market release of the VASCADE MVP XL system, featuring collapsible disc technology and a resorbable collagen patch for quicker hemostasis.

- In April 2024, Vivasure Medical announced the successful treatment of its first large-bore venous patient with the PerQseal Elite vascular closure system, a fully absorbable, sutureless device. This implant was part of the ELITE Venous Clinical Study led by Prof. Nicolas Van Mieghem at Erasmus Medical Centre in Rotterdam.

|

Report Metrics |

Details |

|

Study Period |

2022 to 2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2032 |

|

Vascular Closure Devices Market CAGR |

5.70% |

|

Key Companies in the Vascular Closure Devices Market |

Abbott, Teleflex Incorporated, Terumo Medical Corporation, Cardinal Health, Haemonetics Corporation, Merit Medical Systems, Medtronic, Morris Innovative, BD, TZ Medical, Vasorum Ltd, Tricol Biomedical, Vivasure Medical Ltd., Transluminal Technologies, W. L. Gore & Associates, Inc., Meril Life Sciences Pvt. Ltd., Gem srl, Vasorum Ltd., Rex Medical, Tricol Biomedical, and others. |

|

Vascular Closure Devices Market Segments |

by Product Type, by Access, by End-user, and by Geography |

|

Vascular Closure Devices Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Vascular Closure Devices Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Vascular Closure Devices Market Segmentation

- Vascular Closure Devices Product Type Exposure

- Active Approximators

- Suture-Based

- Clip-Based

- Assisted Compression Devices

- Passive Approximators

- Sealant-Or-Gel-Based

- Bio-absorbable Plugs

- Others

- Active Approximators

- Vascular Closure Devices Access Exposure

- Femoral

- Radial

- Vascular Closure Devices End-Users Exposure

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Others

- Vascular Closure Devices Geography Exposure

- North America Vascular Closure Devices Market

- United States Vascular Closure Devices Market

- Canada Vascular Closure Devices Market

- Mexico Vascular Closure Devices Market

- Europe Vascular Closure Devices Market

- United Kingdom Vascular Closure Devices Market

- Germany Vascular Closure Devices Market

- France Vascular Closure Devices Market

- Italy Vascular Closure Devices Market

- Spain Vascular Closure Devices Market

- Rest of Europe Vascular Closure Devices Market

- Asia-Pacific Vascular Closure Devices Market

- China Vascular Closure Devices Market

- Japan Vascular Closure Devices Market

- India Vascular Closure Devices Market

- Australia Vascular Closure Devices Market

- South Korea Vascular Closure Devices Market

- Rest of Asia-Pacific Vascular Closure Devices Market

- Rest of the World Vascular Closure Devices Market

- South America Vascular Closure Devices Market

- Middle East Vascular Closure Devices Market

- Africa Vascular Closure Devices Market

- North America Vascular Closure Devices Market

Vascular Closure Devices Market Recent Industry Trends and Milestones (2022-2025)

|

Category |

Key Developments |

|

Vascular Closure Devices Product Launches |

Vascade MVP XL by Haemonetics, PerQseal Elite by Vivasure Medical |

|

Vascular Closure Devices Regulatory Approvals |

Vivasure Medical - PerQseal Elite (CE), Cordis - MYNX (FDA) |

|

Partnerships in the Vascular Closure Devices Market |

Haemonetics Corporation with Vivasure Medical, Teleflex & InSeal Medical, Abbott Laboratories & Essential Medical |

|

Acquisitions in the Vascular Closure Devices Market |

Teleflex acquired BIOTRONIK, Haemonetics acquired OpSens, Inc. |

|

Company Strategy |

Abbott: Focus on proven suture-mediated technology and targeting the large-bore segment. Terumo Corporation: Strategy is to acquire companies with innovative technologies to complement their existing portfolio in vascular closure devices |

|

Emerging Technology |

Bioabsorbable Materials, Large-Bore Closure Systems, Suture-Based Active Approximators (Next-Gen), Hybrid Closure Devices |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are increasingly transforming the vascular closure devices (VCDs) market by enhancing accuracy, safety, and efficiency across the entire care pathway. In pre-procedural planning, AI analyzes patient-specific imaging data to identify optimal access sites and predict risks, allowing for more personalized closure strategies. During deployment, AI integrated with ultrasound or fluoroscopy provides real-time guidance, ensuring precise device placement and reducing operator error, while predictive analytics help anticipate complications such as bleeding or hematoma. AI is also reshaping device design through machine learning driven simulation and analysis, accelerating the development of bioabsorbable and large-bore closure systems. Additionally, AI-powered VR/AR training tools are improving physician skills, while wearable sensors and digital platforms enable remote monitoring and post-procedure care, supporting early detection of closure-related issues. The integration of AI with robotic-assisted interventions further enhances precision, particularly in large-bore procedures like TAVR and EVAR. Collectively, these innovations are driving the adoption of next-generation VCDs by improving patient safety, streamlining workflows, and opening new opportunities for growth in the market.

U.S. Tariff Impact Analysis on the Vascular Closure Devices Market:

The U.S. tariff impact on the vascular closure devices (VCDs) market is shaped by trade policies affecting medical device imports, particularly from manufacturing hubs in Europe and Asia. Tariffs on raw materials such as polymers, sutures, and metal components, as well as on finished devices, can increase production and procurement costs for U.S. distributors and healthcare providers. This may lead to higher device prices, potentially affecting hospital purchasing decisions and reimbursement dynamics. However, since vascular closure devices are critical for cardiovascular and endovascular procedures, demand remains relatively inelastic, with hospitals prioritizing patient safety and procedural efficiency over cost concerns. At the same time, tariffs are encouraging some manufacturers to localize production in the U.S. to reduce dependency on imports, which could strengthen domestic supply chains and foster long-term market resilience. Overall, while tariffs may temporarily pressure margins and pricing, the essential role of VCDs in modern interventional cardiology ensures steady market growth.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Main Products |

Stage of Development |

Core Technology |

|

Vivasure Medical |

€30 million |

PerQseal® and PerQseal+, PerQseal Blue |

Series D |

Development of fully absorbable, sutureless, and entirely synthetic implantable patches |

|

Vasorum Ltd. |

£5 million |

CELT ACD |

- |

The device is designed for both arterial and venous closure and is positioned as an alternative to manual compression, particularly in diagnostic and interventional cardiology procedures. |

Key takeaways from the Vascular Closure Devices market report study

- Market size analysis for the current vascular closure devices market size (2024), and market forecast for 8 years (2025 to 2032)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the vascular closure devices market.

- Various opportunities available for the other competitors in the vascular closure devices market space.

- What are the top-performing segments in 2024? How these segments will perform in 2032?

- Which are the top-performing regions and countries in the current vascular closure devices market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the vascular closure devices market growth in the future?