Spinal Cord Injury Market Summary

Spinal Cord Injury (SCI) Insights and Trends

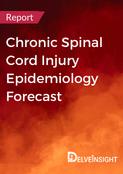

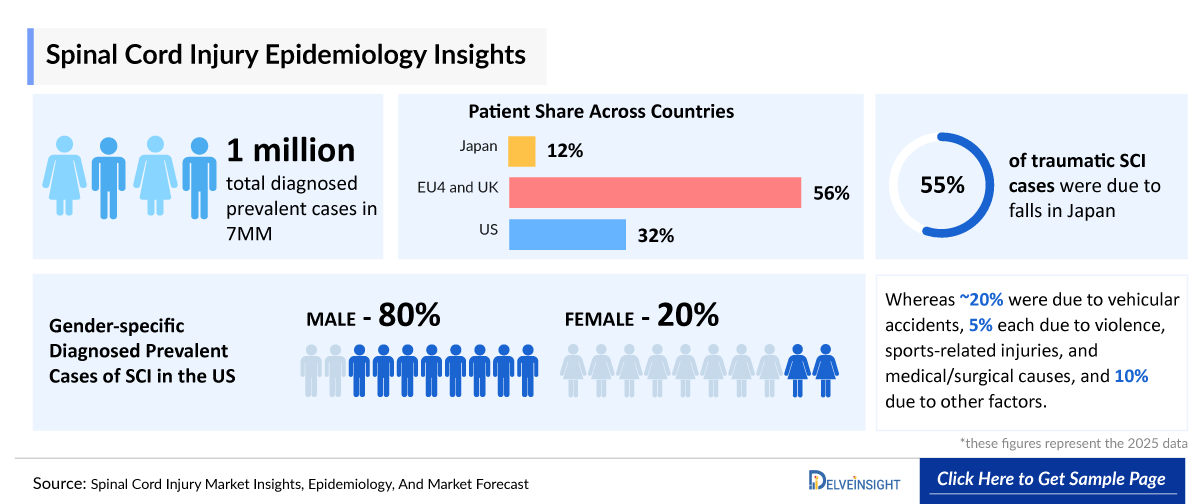

- According to DelveInsight's analysis, the SCI market in the 7MM (the US, EU4, UK, and Japan) was valued at approximately USD 350 million in 2025. Driven by the anticipated clinical entry of disease-modifying therapies and a growing diagnosed patient pool, the market is projected to expand at a robust Compound Annual Growth Rate (CAGR) of 18.3%, within the 7MM.

- The United States continues to hold the largest market share, with a revenue of ~USD 150 million in 2025. DelveInsight estimates this will rise significantly by 2036, with the US expected to account for approximately 49% of the total SCI market across the 7MM, underpinned by a high diagnosed prevalent base of approximately 310,000 cases, with males representing nearly 80% of the affected population.

- In EU4 and the UK, the total market size was estimated at USD 160 million in 2025, accounting for the majority of non-US 7MM revenue, and is projected to grow by 2036 at a CAGR of 10.7%. The region reported approximately 380,000 traumatic and 150,000 non-traumatic diagnosed prevalent SCI cases in 2025, figures that are expected to rise steadily through the forecast period (2026-2036).

- Japan accounted for approximately USD 50 million of the total SCI market in 2025, contributing approximately 60,000 cases due to falls in 2025, followed by vehicular accidents with around 20,000 cases. The Japanese market is expected to grow through 2036, driven by an aging population and increasing cases from fall-related injuries.

- Advances in diagnostic and patient stratification pathways, along with increased awareness of both traumatic and non-traumatic SCI subtypes, are enabling earlier identification and facilitating more timely clinical intervention, particularly in acute injury settings.

- The Spinal Cord Injury emerging pipeline toward 2026 is focused on neuroprotective and regenerative approaches, with key players including AbbVie, Mitsubishi Tanabe Pharma America, Neuroplast, and Kringle Pharma actively advancing assets across clinical trial stages. Notably, elezanumab (ABT-555), one of the therapies is expected to enter the US by 2028.

- A mechanistically diverse late-stage pipeline, encompassing neuroprotective, anti-inflammatory, and regenerative modalities is expected to drive long-term innovation and sustain market expansion well beyond the near-term forecast horizon.

- Safety, tolerability, and adherence challenges, particularly in the acute care setting and among patients managing long-term paralysis-related comorbidities remain key determinants of real-world treatment effectiveness and commercial uptake for emerging therapies.

Spinal Cord Injury Market size and forecast

- 2025 Spinal Cord Injury (SCI) Market Size in 7MM: ~USD 350 million

- Spinal Cord Injury (SCI) Growth Rate (2026–2036) in the 7MM: 18.3% CAGR

DelveInsight’s ‘Spinal Cord Injury (SCI) – Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of SCI, historical and forecasted epidemiology, as well as the market trends in the United States, EU4 (Germany, Spain, Italy, and France), the United Kingdom, and Japan.

The SCI market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates, SCI patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment, and growth rate projections (Historical & Forecast 2026 –2036) across the 7MM regions. The report highlights key unmet medical needs in SCI and maps the competitive and clinical landscape to uncover high‑value opportunities, providing a clear outlook on future market growth potential.

Scope of the Spinal Cord Injury Market Report | |

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2025 |

|

Geographies Covered |

|

|

SCI Market CAGR (Forecast period) |

18.3% (2026-2036) |

|

SCI Epidemiology Segmentation Analysis |

|

|

SCI Companies |

|

|

SCI Therapies |

|

|

SCI Market Segmentation |

|

|

Analysis |

|

Spinal Cord Injury Understanding and Treatment Algorithm

Spinal Cord Injury Overview and Diagnosis

SCI refers to a sudden disruption of the spinal cord’s neuronal tissue within the spinal canal resulting from trauma, disease, or degeneration. This complex injury varies widely in its impact, with each case presenting unique challenges. Depending on the level and type of damage, SCI can manifest as upper or lower motor neuron lesions, leading to varying degrees of motor, sensory, and autonomic dysfunction. These effects may be temporary or permanent.

Effective SCI management requires a comprehensive approach. It begins with a precise clinical examination and neurological classification of the injury. This is complemented by detailed radiological assessments of the vertebral column to understand the extent and nature of the damage, ensuring accurate diagnosis and tailored treatment plans. The management of SCI requires a comprehensive and multidisciplinary approach aimed at optimizing recovery, enhancing quality of life, and addressing the complex physical and psychological challenges faced by individuals. Treatment strategies encompass immediate medical intervention, surgical procedures, pharmacological therapies, and rehabilitation programs.

Further details are provided in the report.

Current Spinal Cord Injury Treatment Landscape

The overall SCI treatment landscape is steadily evolving, driven by the advancement of neuroprotective agents, anti-inflammatory therapies, and an emerging class of regenerative and disease-modifying candidates. Key components of current standard practice include Pregabalin (LYRICA), the sole FDA-approved medication for SCI-related neuropathic pain, which targets the alpha2-delta subunit of voltage-gated calcium channels to reduce the release of pain-related neurotransmitters functioning distinctly from opioid, GABA, or cyclooxygenase pathways. Anti-inflammatory agents and corticosteroids such as methylprednisolone, though increasingly contested due to tolerability concerns have historically formed the backbone of acute injury management, aimed at limiting secondary neurological damage. In Japan, STEMIRAC has received conditional PMDA approval for neurological symptom management.

In addition, next-generation pipeline assets are designed to move beyond symptom management toward true neuroprotection and functional recovery. KP-100IT, an intrathecally administered hepatocyte growth factor formulation, has demonstrated promising motor function improvements in acute SCI patients, particularly those classified as Frankel grade A. Neuro-Cells, derived from human neural stem cells, aim to promote neuroprotection through the release of neurotrophic factors supporting neuronal survival and repair. MT-3921, a monoclonal antibody targeting neuroinflammatory and cell death pathways, seeks to attenuate secondary injury cascades and restore motor function. Further candidates including elezanumab (ABT-555), and others collectively represent a mechanistically diverse late-stage pipeline spanning anti-inflammatory, axonal regeneration, and neuromodulatory approaches.

Further details related to country-based variations are provided in the report.

Spinal Cord Injury Unmet Needs

The section “unmet needs of Spinal Cord Injury” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Need for effective neuroprotective strategies

- Implementing policies that address financial barriers and improve access to rehabilitation services

- Need for personalized medicine

- Long-term care and rehabilitation

- and others…..

Note: Comprehensive unmet needs insights in SCI and their strategic implications are provided in the full report.

Spinal Cord Injury Epidemiology

Key Findings from Spinal Cord Injury Epidemiological Analysis and Forecast

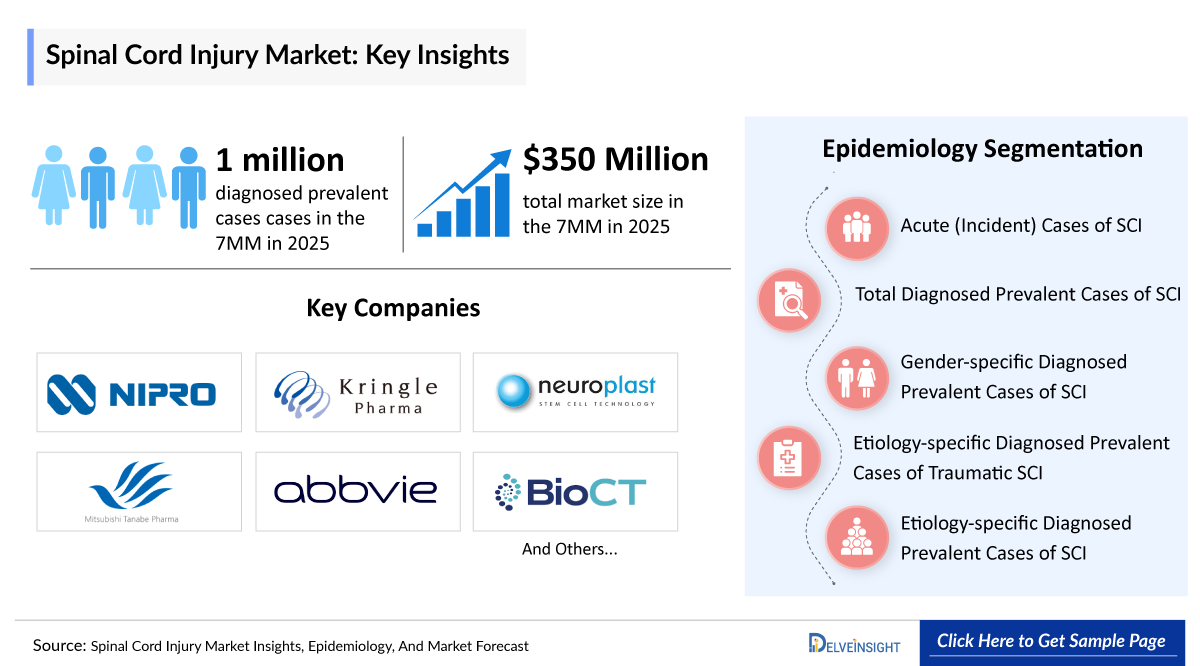

- In 2025, there were an estimated ~1 million total diagnosed prevalent cases of Spinal Cord Injury across the 7MM, with the number expected to rise by 2036.

- According to DelveInsight’s estimates, there were approximately 19,000 acute (incidence) cases of SCI across the US in 2025, with the number expected to rise by 2036.

- According to DelveInsight’s estimates, there were approximately 300,000 diagnosed prevalent cases of SCI across the US in 2025, with the number expected to rise by 2036.

- In 2025, the US reported approximately 250,000 male and 60,000 female cases of SCI, with these numbers expected to increase by 2036.

- According to DelveInsight’s estimates, there were approximately 500,000 diagnosed prevalent cases of SCI across EU4 and the UK in 2025, with the number expected to rise by 2036.

- In 2025, in the UK, there were approximately 93,000 diagnosed prevalent cases of traumatic SCI and 13,000 cases of non-traumatic SCI. These numbers are expected to rise by 2036.

- In 2025, Japan recorded approximately 20% of traumatic SCI cases due to vehicular accidents, 55% due to falls, 5% each due to violence, sports-related injuries, and medical/surgical causes, and 10% due to other factors.

Spinal Cord Injury Drug Analysis & Competitive Landscape

The SCI drug chapter provides a detailed, market-focused review of approved therapies and the emerging pipeline across Phase I - Phase III clinical trials. It covers mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, strategic partnerships upcoming Key catalyst for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the SCI treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the SCI therapeutics market.

Spinal Cord Injury Approved Therapies for

STEMIRAC: Nipro Corporation

STEMIRAC is an autologous mesenchymal stem cell therapy developed by Nipro Corporation, designed to treat patients with traumatic SCI. It involves isolating mesenchymal stem cells from the patient's bone marrow, culturing them in vitro, and cryopreserving them for future use. This innovative treatment aims to improve neurological symptoms and motor functions associated with spinal cord injuries.

Note: Detailed marketed therapies assessment will be provided in the final report.

Spinal Cord Injury Pipeline Analysis

Oremepermin alfa: Kringle Pharma

Oremepermin alfa (also known as KP-100IT), developed by Kringle Pharma, is an intrathecal formulation of Hepatocyte Growth Factor (HGF) designed for the treatment of acute SCI. By targeting nerve cell protection and facilitating axonal regeneration, the therapy holds promise for improving motor function recovery in affected patients

- In Japan, a Phase III clinical trial has been completed, and the company plans to initiate an additional study prior to submitting a marketing authorization application, with the new trial expected to begin in 2026. In the United States, preparations are underway to file an Investigational New Drug (IND) application in 2026 to support the initiation of a pivotal Phase III trial.

- In December 2025, Kringle Pharma submitted an application to the European Medicines Agency seeking orphan drug designation (ODD) for oremepermin alpha in acute spinal cord injury. The therapy has already been granted ODD for acute SCI in Japan (September 2019) and the United States (June 2025).

Note: Detailed emerging therapies assessment will be provided in the final report.

Competitive Landscape of Pipeline Drugs | ||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Anticipated Launch in the US |

|

Oremepermin alfa |

Kringle Pharma |

III |

Acute SCI |

Intrathecal injection |

Target nerve cell protection and facilitating axonal regeneration |

Information is available in the full |

|

Elezanumab (ABT–555) |

AbbVie |

II |

SCI |

IV infusion |

RGMA protein inhibitors |

2028 |

|

Neuro–Cells |

Neuroplast |

II/III |

Acute Traumatic Spinal Cord Injury (TSCI) |

Intrathecal injection |

Cell replacement |

Information is available in the full |

|

Unasnemab (MT–3921) |

Mitsubishi Tanabe Pharma America |

II |

Acute Traumatic Cervical Spinal Cord Injury |

IV infusion |

RGMA protein inhibitors |

Information is available in the full |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | ||||||

Spinal Cord Injury Key Players, Market Leaders and Emerging Companies

- AbbVie

- Mitsubishi Tanabe Pharma America

- Neuroplast

- Kringle Pharma

- Pharmazz

- and others

Spinal Cord Injury Drug Updates

- In February 2024, Kringle Pharma reported topline results from its Phase III study evaluating oremepermin alfa for the treatment of acute spinal cord injury.

- In July 2023, Nipro Corporation initiated a corporate clinical trial for chronic SCI. By expanding the indication of STEMIRAC to include not only subacute but also chronic SCI, Nipro Corporation aims to expedite its commercialization and ensure that STEMIRAC reaches those in need of treatment as early as possible.

- In February 2016, STEMIRAC was designated as a breakthrough product under Japan's SAKIGAKE designation system, which aims to accelerate the development of regenerative medical products for the treatment of neurological symptoms and functional disorders associated with SCI.

Spinal Cord Injury Market Outlook

SCI is a devastating and life-altering neurological condition resulting from traumatic or non-traumatic damage to the spinal cord, leading to partial or complete loss of motor, sensory, and autonomic function below the level of injury. Though most commonly affecting young adults due to vehicular accidents and falls, SCI is increasingly observed across broader age groups, including older individuals where fall-related injuries are a growing contributor. It is progressive in its secondary pathophysiology, triggering a cascade of inflammation, ischemia, and neuronal cell death that extends beyond the initial injury site. The absence of a curative treatment, the high lifetime cost of care, the profound impact on patients and caregivers, and the complexity of spinal cord regeneration make SCI one of the most challenging conditions in modern medicine.

Key marketed therapies shaping current management

- Pregabalin (LYRICA): LYRICA is the sole FDA-approved medication for neuropathic pain associated with SCI, with generic versions also available. Pregabalin targets the alpha2-delta subunit of voltage-gated calcium channels, reducing the release of pain-related neurotransmitters and modulating pain pathways in SCI. While structurally related to GABA, it does not bind to GABA receptors or affect GABA levels, nor does it impact sodium channels, opiate receptors, or cyclooxygenase activity, making it a mechanistically distinct option in SCI-related neuropathic pain management.

- Methylprednisolone: This intravenous corticosteroid, administered shortly after injury, targets acute inflammation and seeks to limit secondary nerve cell damage. However, its widespread use has become contentious due to potential side effects, leading to a decline in its recommendation as a routine standard of care.

- Tramadol: A low-affinity μ-opioid receptor agonist that also inhibits serotonin and norepinephrine reuptake, tramadol provides meaningful analgesic relief with a comparatively reduced opioid side-effect burden, making it a commonly employed option in chronic SCI pain management.

- Gabapentin: Gabapentin binds to the α2δ subunit of voltage-gated calcium channels, reducing neuropathic pain by inhibiting the release of excitatory neurotransmitters, and is widely used as part of multimodal pain management regimens in SCI patients.

- Cannabinoids (THC/CBD): THC and CBD exert their effects by binding to CB1 and CB2 receptors in the brain and spinal cord, modulating pain perception, reducing neuroinflammation, and providing analgesic effects — positioning cannabinoid-based therapies as an emerging adjunctive option in SCI symptom management.

- STEMIRAC: In 2018, STEMIRAC became the world's first stem cell therapy to receive conditional approval from Japan's PMDA for the treatment of neurological symptoms associated with SCI. Developed by Nipro Corporation and Sapporo Medical University, it is an autologous mesenchymal stem cell (MSC) therapy delivered via intravenous infusion. However, as of early 2026, the December 2025 full approval deadline has passed without a confirmed transition to unconditional approval.

- In 2025, the US dominated the SCI market across the 7MM, accounting for 44% of the total market share. The market size in the US was valued at USD 150 million, driven largely by the anticipated impact of emerging therapies on market growth.

Further details will be provided in the report….

Spinal Cord Injury Drug Uptake

This section focuses on the uptake rate of potential drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the SCI drug’s uptake, performance at peak, factors affecting performance during prime years of growth, patient uptake by therapy, and anticipated sales generated by each drug.

Current therapies for SCI primarily emphasize rehabilitation and symptom management, highlighting a significant unmet need for treatments that promote nerve regeneration and functional recovery. The future of pharmacological treatments for SCI appears increasingly promising, with ongoing efforts to repurpose existing drugs and develop innovative therapeutic agents. Elezanumab (ABT-555), one of the emerging therapies, is anticipated to enter the market in 2028, generating a significant portion in revenue during its launch year. By 2036, this is expected to rise significantly, driven by a medium-fast uptake

Detailed insights of emerging therapies' drug uptake is included in the report…

Market Access and Reimbursement of Approved Therapies in Spinal Cord Injury (SCI)

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of approved therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

NOTE: Further Details are provided in the final report….

Spinal Cord Injury Price Scenario & Trends

Pricing and analogue assessment of SCI therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, closest and most appropriate analogue selection for emerging therapies, and understanding of how pricing influences market access, adherence, and long-term uptake.

- Pricing of SCI Approved Drugs

Autologous mesenchymal stem cell therapy (STEMIRAC), the only conditionally approved SCI-specific therapy globally, carries a substantially higher treatment cost relative to standard pharmacological options, reflective of the complex manufacturing process involved in harvesting, expanding, and reinfusing a patient's own bone marrow-derived mesenchymal stem cells. The estimated treatment cost for STEMIRAC in Japan — the sole market where it holds conditional approval is approximately USD 135,000. No equivalent pricing has been established in the US or EU markets, given that STEMIRAC does not currently hold regulatory approval outside of Japan.

Industry Experts and Physician Views for Spinal Cord Injury

To keep up with SCI market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry Experts were contacted for insights on the SCI emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in SCI, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 8+ KOLs to gather insights at country level. Centers such as the Memorial Sloan Kettering Cancer Center, University of California San Francisco, State University of New York Upstate Medical University, etc. were contacted.

Their opinion helps understand and validate current and emerging SCI therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in SCI.

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“In the US, the focus is on neuroprotective strategies and advancing acute care for SCI patients. Therapies targeting secondary injury mechanisms, such as inflammation and apoptosis, are critical for improving long-term outcomes. Combination approaches involving pharmacological agents and rehabilitative strategies are emerging as effective paradigms for enhancing recovery.” |

|

Germany |

“While technological innovations such as exoskeletons and neuroprosthetics have made significant strides, the integration of these technologies into daily rehabilitation practices remains limited. Ongoing research is crucial to bridge this gap and make these advancements accessible to a broader patient population.” |

Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of SCI, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided. Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are majorly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Spinal Cord Injury Market Report

- The report covers a segment of key events, an executive summary, a descriptive overview of SCI, explaining their causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of mid and late stage therapies, will have an impact on the current treatment landscape.

- A detailed review of the SCI market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM SCI market.

Spinal Cord Injury Market Report Insights

- SCI Patient population forecast

- SCI therapeutics market size

- SCI pipeline analysis

- SCI market size and trends

- SCI market opportunity (Current and forecasted)

Spinal Cord Injury Market Report Key Strengths

- Epidemiology‑based (EPI ‑ based) bottom‑up forecasting

- Artificial Intelligence (AI) - enabled market research report

- 11-year forecast

- SCI market outlook (North America, Europe, Asia-Pacific)

- SCI Burden trends (by geography)

- SCI Treatment addressable Market (TAM)

- SCI Competitive Landscape

- SCI major companies Insights

- SCI Price trends and analogue assessment

- SCI Therapies Drug Adoption/Uptake

- SCI Therapies Peak Patient Share analysis

Spinal Cord Injury Market Report Assessment

- SCI Current treatment practices

- SCI Unmet needs

- SCI Clinical development Analysis

- SCI emerging drugs product profiles

- SCI Market attractiveness

- SCI Qualitative analysis (SWOT and conjoint analysis)

Key Questions Answered in the Spinal Cord Injury Market Report

Market Insights

- What was the SCI market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of SCI?

- What are the disease risks, burdens, and unmet needs of SCI? What will be the growth opportunities across the 7MM concerning the patient population with SCI?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of SCI? What are the current guidelines for treating SCI in the US, Europe, and Japan?

Reasons to Buy Spinal Cord Injury Market Report

- The report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the SCI market.

- Bottom‑up forecasting builds from the affected population to product forecasts, delivering a robust, data‑driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease prevalence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI) ‑ enabled report summarize and simplify complex datasets within the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data‑driven decisions.