Stem Cell Market Summary

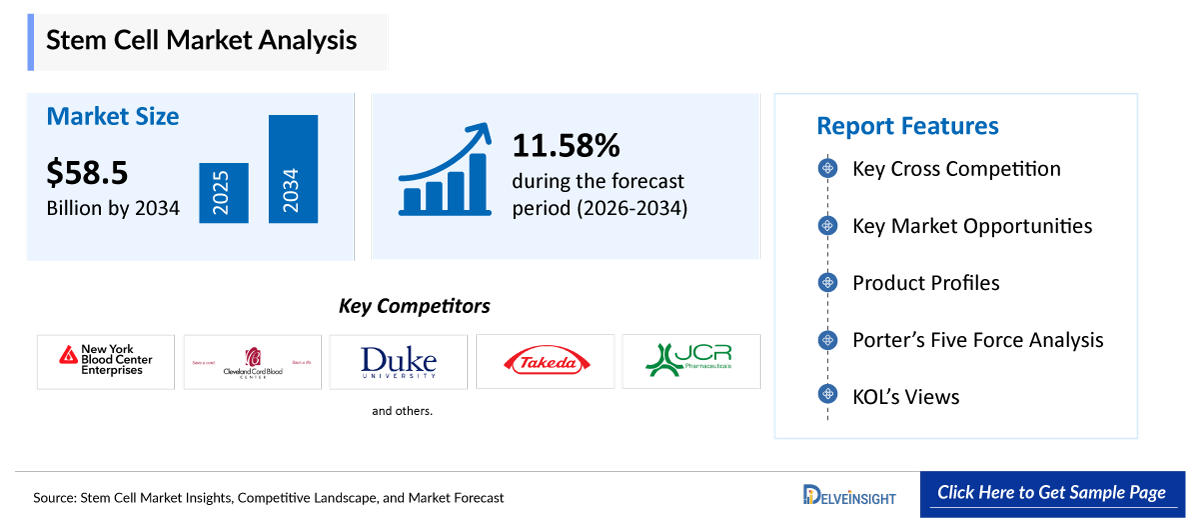

- The Global Stem Cell Market is expected to increase from USD 21,956.46 million in 2025 to USD 58,572.15 million by 2034, reflecting strong and sustained growth.

- The Global Stem Cell Market is growing at a CAGR of 11.58% during the forecast period from 2026 to 2034.

Stem Cell Market Insights & Forecast

- The rising prevalence of chronic and degenerative diseases is significantly increasing the demand for effective and long-term treatment solutions, where Stem Cell therapies offer strong regenerative potential. At the same time, the growing clinical success of hematopoietic Stem Cell transplants, particularly in treating blood disorders and cancers, has established trust among healthcare providers and patients, supporting wider adoption.

- Additionally, continuous advancements in Stem Cell technologies, such as improved cell expansion, cryopreservation, and gene-modified Stem Cells, along with increasing product development activities by key market players, are enhancing treatment efficacy and expanding therapeutic applications. Collectively, these factors are driving the growth of the overall Stem Cell market by accelerating innovation, improving clinical outcomes, and broadening the scope of use across multiple disease areas.

- The leading Stem Cell Therapy Companies such as New York Blood Center, Cleveland Cord Blood Center, Duke University, Takeda Pharmaceutical Company, JCR Pharmaceuticals, Medipost, Stempeutics Research, Nipro Corporation, Vericel Corporation, Holostem Terapie Avanzate, Orchard Therapeutics, Bluebird Bio, Cynata Therapeutics, Sumitomo Pharma Co., Ltd., and others.

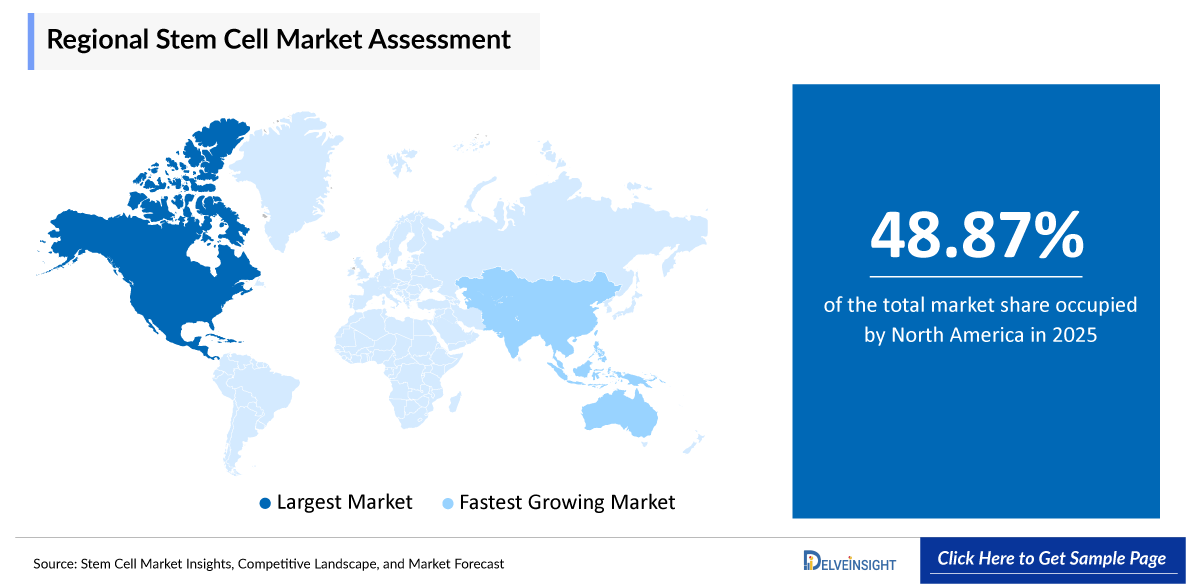

- North America is expected to dominate the Stem Cell Market due to the presence of advanced healthcare infrastructure, strong investment in regenerative medicine, and a high number of ongoing clinical trials and product approvals. Additionally, the region benefits from increasing prevalence of chronic diseases, well-established research institutions, and the presence of key market players, all of which contribute to early adoption and commercialization of innovative Stem Cell therapies.

- In the therapy type segment of the Stem Cell market, the allogenic category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Stem Cell Market

Stem Cell Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size | |

|

2034 Projected Market Size | |

|

Growth Rate (2026-2034) | |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Stem Cell Market

-

Rising prevalence of chronic & degenerative diseases leading to a surge in Stem Cell therapy

The increasing incidence of diseases such as cancer, cardiovascular disorders, diabetes, and neurodegenerative conditions is significantly driving demand for Stem Cell therapies. These therapies offer regenerative and potentially curative solutions, especially where conventional treatments only manage symptoms.

-

Increasing success of hematopoietic Stem Cell transplants

The widespread clinical success of bone marrow and cord blood transplants in treating blood disorders (e.g., leukemia, lymphoma) continues to be a major driver, forming the largest revenue-generating segment of the market.

-

Advancements in Stem Cell technologies and an increase in product development activities among the key market players

Advancements in Stem Cell technologies, such as improved cell expansion, gene modification, and cryopreservation, are enhancing treatment efficacy and scalability. At the same time, increasing product development activities by key market players are expanding the pipeline and accelerating approvals, collectively driving the growth of the Stem Cell market.

Stem Cell Market Report Segmentation

This Stem Cell market report offers a comprehensive overview of the Global Stem Cell market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Therapy Type (Allogenic and Autologous), Cell Source (Adult Stem Cells {Hematopoietic Stem Cells (HSCs), Mesenchymal Stem Cells (MSCs), and Others}, Embryonic Stem Cells (ESCs), and Induced Pluripotent Stem Cells (iPSCs)), Therapeutic Application (Hematological Disorders, Musculoskeletal Disorders, Neurological Disorders, and Others), Technology (Cell Collection & Isolation, Cell Expansion & Culturing, Cryopreservation & Storage, and Others), End-Users (Hospitals & Transplant Centers, Academic & Research Institutes, and Others), and geography.

The Stem Cell Therapy Market Report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing Stem Cell market.

Stem Cell therapy is a medical treatment that uses Stem Cells, unique cells capable of self-renewal and differentiation, to repair, replace, or regenerate damaged tissues and organs. It is widely used in treating blood disorders and is increasingly being explored for regenerative medicine applications across various chronic and degenerative diseases. The rising prevalence of chronic and degenerative diseases, including cancer, cardiovascular disorders, and neurological conditions, is significantly increasing the demand for advanced and long-term treatment solutions, where Stem Cell therapies offer strong regenerative and potentially curative capabilities.

At the same time, the growing clinical success of hematopoietic Stem Cell transplants, particularly in treating blood disorders such as leukemia and lymphoma, has strengthened confidence among healthcare providers and patients, leading to wider clinical adoption. In addition, continuous advancements in Stem Cell technologies, such as enhanced cell expansion techniques, improved cryopreservation methods, and the development of gene-modified Stem Cells, are improving treatment efficacy, safety, and scalability.

Increasing product development activities and investments by key market players are further accelerating the pipeline of innovative therapies and expanding their applications across areas such as orthopedics, dermatology, and rare genetic diseases. Collectively, these factors are driving the overall growth of the Stem Cell market by fostering innovation, improving patient outcomes, and broadening the scope of therapeutic use across multiple disease segments.

Get More Insights into the Report @ Stem Cell Market

What are the latest Stem Cell Market Dynamics and Trends?

The Global Stem Cell therapy market has witnessed significant growth in recent years. This expansion is driven primarily by the increasing prevalence of chronic and degenerative disorders such as leukemia, lymphoma, neurological disorders, and cardiovascular disorders, among others.

According to the World Health Organization (2026) and the International Agency for Research on Cancer (IARC), in 2025, new leukemia and Non-Hodgkin lymphoma cases were projected to reach 5,15,145 and 5,89,872, with projections further estimated to increase 8,00,698 and 9,60,173, respectively, by 2050. The rising incidence of leukemia and non-Hodgkin lymphoma is significantly boosting the Stem Cell market, as these conditions are among the primary indications for hematopoietic Stem Cell transplantation (HSCT).

Stem Cell transplants are often used when conventional treatments such as chemotherapy fail or when relapse occurs, making them a critical part of treatment protocols. The high clinical success and established use of HSCT in these cancers have increased physician confidence and patient adoption, thereby driving demand for Stem Cell therapies. Additionally, the growing number of diagnosed cases and improved transplant outcomes are further expanding the market by increasing the volume of procedures performed globally.

Alzheimer’s disease is another main driver of the Stem Cell market. The Alzheimer’s Association (2025) reported over 7 million Americans living with Alzheimer’s, expected to rise to nearly 13 million by 2050. The rising prevalence of Alzheimer’s disease is boosting the Stem Cell market by increasing the demand for innovative treatments that can address neurodegeneration rather than just manage symptoms. As current therapies offer limited efficacy, Stem Cell-based approaches are being actively explored for their potential to repair damaged neural tissues and improve cognitive function. This has led to increased research activities, clinical trials, and investments by key players, thereby driving market growth in the neurological segment.

Additionally, the increasing success of hematopoietic Stem Cell transplants (HSCT) is significantly boosting the Stem Cell market by improving survival rates, expanding patient eligibility, and building strong clinical confidence. Over the years, outcomes of HSCT have steadily improved across different patient populations due to better donor matching, conditioning regimens, and supportive care, making it a more reliable and widely accepted treatment option. Recent approvals and clinical advancements further highlight this progress.

For instance, in April 2023, Omisirge received its first approval for patients with hematologic malignancies, demonstrating faster neutrophil recovery and reduced infection risk after transplant. Subsequently, in December 2025, it was approved for severe Aplastic Anemia, where clinical studies showed around 86% early and sustained recovery and over 90% survival rates, indicating significantly improved transplant outcomes. Similarly, the approval of Ryoncil in December 2024 for treating graft-versus-host disease (a major complication post-transplant) demonstrates how advancements are improving post-transplant safety and success rates.

Collectively, these improvements are reducing complications, shortening recovery times, and increasing survival rates, which in turn is driving higher adoption of Stem Cell therapies, encouraging further investments, and expanding the overall Stem Cell Therapy Market. Thus, the factors mentioned above are expected to boost the overall Stem Cell Therapy Market during the forecasted period.

However, high treatment costs, combined with complex and evolving regulatory requirements, are significantly limiting the growth of the Stem Cell market. The high cost of therapy development, manufacturing, and treatment reduces patient accessibility and places a financial burden on healthcare systems, while stringent regulatory processes delay product approvals and commercialization. Together, these factors slow down market entry for new therapies, restrict widespread adoption, and create barriers for both patients and manufacturers, ultimately hindering overall market growth.

Stem Cell Market Segment Analysis

Stem Cell Market by Therapy Type (Allogenic and Autologous), Cell Source (Adult Stem Cells {Hematopoietic Stem Cells (HSCs), Mesenchymal Stem Cells (MSCs), and Others}, Embryonic Stem Cells (ESCs), and Induced Pluripotent Stem Cells (iPSCs)), Therapeutic Application (Hematological Disorders, Musculoskeletal Disorders, Neurological Disorders, and Others), Technology (Cell Collection & Isolation, Cell Expansion & Culturing, Cryopreservation & Storage, and Others), End-Users (Hospitals & Transplant Centers, Academic & Research Institutes, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Therapy Type: Allogenic in Stem Cell Category is Expected to Dominate the Market with the Largest Revenue Share

In the therapy type segment of the Stem Cell market, the allogenic category is contributing to 62.45% of total market revenue in 2025. Unlike autologous therapies, allogeneic Stem Cell therapies use donor-derived cells, enabling off-the-shelf treatment availability, faster treatment timelines, and the ability to treat a larger patient population, particularly in hematological disorders where matched donors are required. This has significantly increased adoption in hospitals and transplant centers. Moreover, continuous advancements in donor matching, graft engineering, and cell expansion technologies have improved transplant outcomes, reduced complications such as graft-versus-host disease, and enhanced survival rates, further strengthening confidence among clinicians.

Recent approvals strongly highlight this growth trend. For instance, Omisirge (omidubicel-onlv) received its first approval in April 2023, becoming the first FDA-approved expanded cord blood Stem Cell therapy, designed to accelerate neutrophil recovery and reduce infection risk in patients undergoing hematopoietic Stem Cell transplantation. This innovation addresses a key limitation of traditional cord blood transplants, low cell count, by enabling ex vivo expansion of Stem Cells, thereby significantly improving clinical outcomes.

Furthermore, in December 2025, the therapy received an additional approval for treating severe aplastic anemia, expanding its clinical utility and reinforcing the role of allogeneic therapies in addressing unmet medical needs.

Such advancements and regulatory approvals are accelerating the commercialization of allogeneic Stem Cell therapies, encouraging investments from key market players, and expanding their application across multiple disease areas. Collectively, the ability to provide standardized, scalable, and clinically effective treatments is positioning the allogeneic segment as a major growth driver in the Global Stem Cell market.

By Cell Source: Hematopoietic Stem Cells (HSCs) under the Adult Stem Cell Category Dominate the Market

Within the cell source segment of the Stem Cell market, the Hematopoietic Stem Cells (HSCs) under the adult Stem Cell category are expected to hold a significant revenue share in 2025, due to their established clinical success, wide range of indications, and continuous regulatory advancements. HSCs, primarily derived from bone marrow, peripheral blood, and umbilical cord blood, are the backbone of hematopoietic Stem Cell transplantation (HSCT), which remains the standard-of-care treatment for several life-threatening blood disorders such as leukemia, lymphoma, and aplastic anemia.

The dominance of this segment is further strengthened by decades of clinical validation, high procedure volumes globally, and strong physician confidence. Additionally, improvements in donor matching, conditioning regimens, and supportive care have significantly enhanced transplant success rates and patient survival, thereby increasing adoption.

Recent approvals further reinforce the growth of this segment. For instance, Omisirge (omidubicel-onlv) received FDA approval in April 2023 for use in patients with hematologic malignancies undergoing cord blood transplantation, demonstrating faster neutrophil recovery and reduced infection risk. Building on this, the therapy received an expanded approval in December, 2025, becoming the first hematopoietic Stem Cell transplant therapy approved for severe aplastic anemia, significantly broadening its clinical application. This product is particularly notable as it uses chemically enhanced cord blood-derived HSCs, addressing key limitations of traditional cord blood transplants such as delayed engraftment and infection risk.

Such advancements highlight how innovation within HSC-based therapies is improving treatment outcomes, expanding patient eligibility (especially for those without matched donors), and enabling faster recovery. Collectively, the strong clinical foundation, increasing number of approvals, and technological enhancements in HSC therapies are driving their dominance and significantly boosting the overall Stem Cell market.

By Therapeutic Application: Hematological Disorders Category Dominates the Market

In the application segment of the Stem Cell market, the hematological disorders category is projected to dominate due to its strong clinical foundation, high procedure volume, and well-established treatment protocols. Hematopoietic Stem Cell transplantation (HSCT) has become the standard-of-care for a wide range of blood disorders, including leukemia, lymphoma, multiple myeloma, aplastic anemia, and inherited blood diseases, making it the most widely adopted application of Stem Cell therapy.

The dominance of this segment is primarily driven by the rising Global incidence of hematologic malignancies such as leukemia. Moreover, HSCT is often used as a curative or life-saving treatment, especially in high-risk or relapsed patients, which further strengthens its clinical importance and adoption. Continuous advancements such as improved donor matching, reduced-intensity conditioning regimens, and graft engineering have significantly enhanced survival rates and reduced complications, thereby increasing physician confidence and expanding patient eligibility.

Additionally, the growing burden of hematological diseases worldwide is further accelerating market growth. Stem Cell transplantation has emerged as a cornerstone therapy for conditions like leukemia, lymphoma, and certain autoimmune and genetic disorders, driving consistent demand across healthcare systems. The increasing use of HSCT as both a first-line and salvage therapy, along with its expanding application in rare genetic diseases such as sickle cell disease and thalassemia, is further broadening the scope of this segment.

By Technology: Cell Collection & Isolation Category Dominates the Market

In the technology segment of the Stem Cell market, the cell collection & isolation category is projected to dominate due to its fundamental role as the first and most critical step in the Stem Cell therapy workflow. Efficient collection and isolation of high-quality Stem Cells directly impact the success, safety, and efficacy of subsequent processes such as expansion and transplantation.

The increasing number of Stem Cell transplants, growing use of cord blood and bone marrow sources, and advancements in isolation techniques are driving demand for reliable and standardized collection methods. As a result, this segment holds a significant share in the market by enabling consistent and scalable production of Stem Cell therapies.

By End-Users: Hospitals & Transplant Centers Category Dominates the Market

In the end-user segment of the Stem Cell market, hospitals and transplant centers dominate due to their advanced infrastructure, specialized expertise, and ability to perform complex procedures such as hematopoietic Stem Cell transplants. These settings have access to skilled healthcare professionals, GMP-compliant facilities, and comprehensive patient care, including pre- and post-transplant management. Additionally, the high volume of Stem Cell transplant procedures and increasing patient preference for treatment in well-equipped clinical environments further drive the dominance of this segment.

Stem Cell Market Regional Analysis

North America Stem Cell Market Trends

North America is expected to account for the highest proportion of 48.87% of the Stem Cell market in 2025, out of all regions. North America is expected to dominate the Stem Cell market due to the presence of advanced healthcare infrastructure, strong investment in regenerative medicine, and a high number of ongoing clinical trials and product approvals. Additionally, the region benefits from increasing prevalence of chronic diseases, well-established research institutions, and the presence of key market players, all of which contribute to early adoption and commercialization of innovative Stem Cell therapies.

According to the International Agency for Research on Cancer (2026), in 2025, the estimated new cases of leukemia in North America were projected to reach 76,085 cases, and the projections were further estimated to increase to 1,05,205 cases by 2050. The rising Global incidence of leukemia, especially Acute Myeloid Leukemia and Acute Lymphoblastic Leukemia, is increasing demand for Stem Cell-based treatments. Additionally, improvements in matched unrelated donor registries, cord blood banking, and reduced-intensity conditioning regimens have expanded transplant eligibility to older and more fragile patients. Advancements in haploidentical transplants and better graft-versus-host disease (GVHD) management are also improving success rates, further driving adoption of Stem Cell therapies in leukemia care worldwide.

Additionally, the Stem Cell market is being strongly driven by the increasing success of hematopoietic Stem Cell transplants (HSCT), along with rapid technological advancements and robust product development activities by key players across the region. The region benefits from a highly advanced healthcare infrastructure, strong regulatory support from the U.S. Food and Drug Administration, and a high volume of clinical trials, all of which accelerate innovation and commercialization. The improving success rates of HSCT due to better donor matching, conditioning regimens, and supportive care have increased physician confidence and patient adoption, making Stem Cell therapies a standard treatment for several hematological disorders.

Recent approvals highlight this momentum. For instance, Omisirge (omidubicel-onlv) was first approved in April 2023 in the U.S. for patients with hematologic malignancies undergoing cord blood transplantation, demonstrating faster neutrophil recovery and reduced infection risk. This was followed by an expanded approval in December, 2025, making it the first HSCT therapy approved for severe aplastic anemia, significantly broadening its clinical application. Additionally, Ryoncil (remestemcel-L) received FDA approval in December 2024, becoming the first mesenchymal Stem Cell (MSC) therapy approved in the U.S. for steroid-refractory graft-versus-host disease, a major complication following Stem Cell transplantation.

These approvals demonstrate how advancements such as ex vivo expansion, improved cell processing, and novel Stem Cell sources are enhancing treatment efficacy and safety. At the same time, increasing R&D investments and pipeline expansion by biotech companies are accelerating innovation and expanding therapeutic applications. Collectively, the strong clinical success of HSCT, coupled with continuous technological progress and frequent regulatory approvals in North America, is significantly boosting the growth of the Stem Cell market in the region.

Europe Stem Cell Market Trends

The Stem Cell market in Europe is experiencing robust growth driven by strong regulatory support, increasing public–private investments, and continuous advancements in regenerative medicine. The region has established a well-defined regulatory framework under the European Medicines Agency (EMA) for Advanced Therapy Medicinal Products (ATMPs), which has accelerated the development and commercialization of Stem Cell therapies.

A major milestone was the approval of Holoclar by the European Commission in February 2015, marking the first Stem Cell–based medicinal product approved in the Western world for treating limbal Stem Cell deficiency caused by eye burns, demonstrating Europe’s leadership in translating research into clinical therapies. Building on this foundation, Europe continues to witness significant development activities, such as the acquisition of Holostem Terapie Avanzate in December 2023 by ENEA Tech and Biomedical, aimed at strengthening manufacturing capabilities and ensuring the continued availability of advanced Stem Cell therapies.

Additionally, large-scale funding initiatives under programs like Horizon Europe (2024) are actively supporting Stem Cell and gene therapy research, including mesenchymal Stem Cell (MSC) projects across countries like Germany, France, and Sweden, thereby accelerating clinical trials and regulatory progress. The region is also benefiting from a rapidly aging population, with over 20% of Europeans aged 60 and above in 2024, driving demand for regenerative treatments for conditions such as osteoarthritis and other degenerative disorders.

Furthermore, increasing collaboration between academic institutions, biotech companies, and government bodies is fostering innovation and expanding the pipeline of Stem Cell-based therapies across multiple therapeutic areas, including ophthalmology, orthopedics, and rare diseases. Collectively, these factors, including strong regulatory backing, continuous R&D investments, landmark approvals, and rising disease burden, are significantly driving the growth of the Stem Cell market in Europe.

Asia-Pacific Stem Cell Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the Stem Cell market due to a strong combination of supportive government policies, rapid clinical translation, expanding biotechnology infrastructure, rising healthcare investments, and a large patient population with unmet medical needs. Countries such as China, Japan, South Korea, and India are playing a central role in accelerating both research and commercialization of Stem Cell therapies.

Japan has particularly advanced the field through its fast-track regenerative medicine approval system, which enabled breakthrough progress such as the March 2026 conditional approval of iPSC-derived therapies like ReHeart and Amusepri for heart failure and Parkinson’s Disease, marking one of the world’s first real-world applications of reprogrammed Stem Cell treatments.

These developments are supported by rising clinical trial activity, with China reporting a sharp increase in regenerative medicine trials and expanding domestic biotech innovation under national initiatives like “Made in China 2025.” South Korea is strengthening its position through government-backed R&D funding and translational research programs focused on cost-effective Stem Cell applications, while India is emerging as a cost-competitive hub for clinical research and biomanufacturing.

Additionally, APAC benefits from increasing healthcare expenditure, improving insurance coverage for advanced therapies in countries like China, and growing medical tourism demand for regenerative treatments. Collectively, these factors are transforming Asia Pacific into not only a fast-growing market but also a Global innovation and manufacturing hub for Stem Cell therapy.

Who are the major players in the Stem Cell Market?

The following are the leading companies in the Stem Cell market. These companies collectively hold the largest market share and dictate industry trends.

- New York Blood Center

- Cleveland Cord Blood Center

- Duke University

- Takeda Pharmaceutical Company

- JCR Pharmaceuticals

- Medipost

- Stempeutics Research

- Nipro Corporation

- Vericel Corporation

- Holostem Terapie Avanzate

- Orchard Therapeutics

- Bluebird Bio

- Orchard Therapeutics

- Cynata Therapeutics

- Sumitomo Pharma Co., Ltd.

- Others

How is the competitive landscape shaping the Stem Cell market?

The competitive landscape of the Stem Cell market is moderately concentrated and highly innovation-driven, characterized by the presence of a few established biopharmaceutical companies alongside a large number of emerging biotechnology firms and academic spin-offs. Leading players typically maintain their position through strong clinical pipelines, proprietary Stem Cell technologies, advanced manufacturing capabilities, and regulatory expertise, enabling them to bring therapies from research to commercialization more efficiently.

At the same time, numerous smaller companies are actively engaged in developing next-generation therapies such as induced pluripotent Stem Cell (iPSC)–based treatments, mesenchymal Stem Cell (MSC) platforms, and gene-edited regenerative solutions, which contribute to a highly dynamic and competitive innovation ecosystem. The Stem Cell Therapy market is increasingly shaped by strategic collaborations, licensing agreements, and mergers and acquisitions, as larger pharmaceutical companies seek to strengthen their regenerative medicine portfolios by partnering with or acquiring specialized biotech firms.

Academic institutions and research organizations also play a crucial role, often serving as the origin of early-stage discoveries that are later translated into commercial therapies through industry partnerships. Overall, the competitive structure can be described as a dual-layer ecosystem, where a relatively small group of established players focuses on commercialization and Global expansion, while a broad base of innovative startups and research-driven organizations continuously fuels technological advancement and pipeline development in Stem Cell therapy.

Stem Cell Market Recent Breakthroughs and Developments

- In March 2026, Japan approved Amchepry, the world’s first regenerative medicine treatment using induced pluripotent stem (iPS) cells to treat Parkinson’s disease.

- In December 2025, Cipla Limited announced the launch of Ciplostem, an innovative allogeneic mesenchymal stromal cell (MSC) therapy for Knee Osteoarthritis, approved by the Drug Controller General of India (DCGI). Developed by Stempeutics Research, the therapy offers a disease-modifying treatment option targeting Grade II and III Knee OA and marks a significant advancement in Cipla’s entry into Orthobiologic medicine.

- In April 2025, an off-the-shelf, iPSC-derived CAR T-cell therapy for the treatment of active moderate to severe Systemic Lupus Erythematosus, including Lupus Nephritis, was granted an FDA RMAT designation for entering Phase I clinical trial.

- In February 2025, the FDA granted IND clearance for Fertilo (Figure 2), the first iPSC-based therapy to enter a U.S. Phase III trial.

- In December 2024, Ryoncil received FDA approval as the first MSC therapy for pediatric steroid-refractory acute graft versus host disease (SR-aGVHD) in patients aged ≥2 months.

- In April 2023, Omisirge received FDA approval. for patients (12–65 years) with hematologic malignancies undergoing cord blood transplantation.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Stem Cell Market CAGR |

XX% |

|

Stem Cell Companies |

New York Blood Center, Cleveland Cord Blood Center, Duke University, Takeda Pharmaceutical Company, JCR Pharmaceuticals, Medipost, Stempeutics Research, Nipro Corporation, Vericel Corporation, Holostem Terapie Avanzate, Orchard Therapeutics, Bluebird Bio, Cynata Therapeutics, Sumitomo Pharma Co., Ltd., and others. |

|

Stem Cell Market Segments |

by Therapy Type, by Cell Source, by Therapeutic Application, by Technology, by End-Users, and by Geography |

|

Stem Cell Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Stem Cell Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Stem Cell Market Segmentation

· Stem Cell Market by Therapy Type Exposure

o Allogenic

o Autologous

· Stem Cell Market Source Exposure

o Adult Stem Cells

§ Hematopoietic Stem Cells (HSCs)

§ Mesenchymal Stem Cells (MSCs)

§ Others

o Embryonic Stem Cells (ESCs)

o Induced Pluripotent Stem Cells (iPSCs)

· Stem Cell Market Application Exposure

o Hematological Disorders

o Musculoskeletal Disorders

o Neurological Disorders

o Others

· Stem Cell Market Technology Exposure

o Cell Collection & Isolation

o Cell Expansion & Culturing

o Cryopreservation & Storage

o Others

· Stem Cell Market End-Users Exposure

o Hospitals & Transplant Centers

o Academic & Research Institutes

o Others

· Stem Cell Market Geography Exposure

o North America Stem Cell Market

§ United States Stem Cell Market

§ Canada Stem Cell Market

§ Mexico Stem Cell Market

o Europe Stem Cell Market

§ United Kingdom Stem Cell Market

§ Germany Stem Cell Market

§ France Stem Cell Market

§ Italy Stem Cell Market

§ Spain Stem Cell Market

§ Rest of Europe Stem Cell Market

o Asia-Pacific Stem Cell Market

§ China Stem Cell Market

§ Japan Stem Cell Market

§ India Stem Cell Market

§ Australia Stem Cell Market

§ South Korea Stem Cell Market

§ Rest of Asia-Pacific Stem Cell Market

o Rest of the World Stem Cell Market

§ South America Stem Cell Market

§ Middle East Stem Cell Market

§ Africa Stem Cell Market

Stem Cell Market Recent Industry Trends and Milestones (2022-2026)

|

Category |

Key Developments |

|

Stem Cell Product Approval |

Sumitomo Pharma Co., Ltd. - Amchepry (PMDA approval), Gamida Cell Ltd. – Omisirge (FDA approval), Mesoblast, Inc. – Ryoncil (FDA approval). |

|

Stem Cell Product Launch |

Cipla Limited announced the launch of Ciplostem, an innovative allogeneic mesenchymal stromal cell (MSC) therapy for Knee Osteoarthritis (Knee OA) |

|

Stem Cell Partnership |

Cipla partnered with Stempeutics. |

|

Company Strategy |

Vertex Pharmaceuticals: Focuses on iPSC-derived cell replacement therapies, especially for chronic diseases like type 1 diabetes. Bayer (BlueRock Therapeutics): Prioritizing dopamine neuron replacement therapies for Parkinson’s disease using Stem Cell technology. |

|

Emerging Technology |

Induced Pluripotent Stem Cell (iPSC) Technology, CRISPR-Cas9 Gene Editing in Stem Cells, Organoid Technology (3D Mini-Organs), Stem Cell–Derived CAR-T and Immune Cell Engineering, AI and Computational Stem Cell Design, and others. |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are increasingly transforming Stem Cell therapy by improving the way Stem Cells are discovered, engineered, differentiated, and translated into clinical applications. Artificial intelligence and machine learning algorithms are being used to analyze large-scale genomic, proteomic, and cellular imaging data to predict how Stem Cells will behave under different conditions, enabling faster identification of optimal differentiation pathways for generating specific cell types such as neurons, cardiomyocytes, and pancreatic beta cells.

AI is also enhancing drug discovery and toxicity screening by using Stem Cell–derived organoids and in-silico models to simulate human biological responses more accurately than traditional animal testing. In addition, AI-driven platforms are supporting quality control in Stem Cell manufacturing, helping detect abnormalities, reduce variability, and ensure batch-to-batch consistency in cell production. Machine learning models are further being applied to optimize gene editing outcomes (such as CRISPR-based modifications) by predicting off-target effects and improving precision in genetic correction of Stem Cells.

In clinical research, AI is assisting in patient stratification and treatment personalization, identifying which patients are most likely to respond to Stem Cell therapies based on genetic and clinical profiles. Overall, AI is accelerating the entire Stem Cell therapy pipeline from research and development to manufacturing and clinical deployment, making regenerative medicine more efficient, scalable, and clinically reliable.

U.S. Tariff Impact Analysis on Stem Cell Market

The U.S. tariff impact on the Stem Cell market is primarily characterized by rising manufacturing costs, supply chain disruptions, and a strategic shift toward domestic production and localized sourcing of raw materials and cell therapy components. Since Stem Cell therapies depend heavily on specialized inputs such as cell culture media, growth factors, bioreactors, cryopreservation materials, and single-use bioprocessing systems, tariffs on imported biopharmaceutical materials and equipment increase overall production expenses and create pricing pressure across the value chain.

This particularly affects biotech startups and mid-sized regenerative medicine companies, which often rely on Global suppliers from Europe and Asia for critical raw materials. As a result, many companies are now restructuring supply chains, increasing investments in U.S.-based manufacturing facilities, and partnering with domestic CDMOs to reduce tariff exposure and ensure regulatory compliance. At the same time, tariffs are indirectly encouraging regionalization of Stem Cell therapy production, which may improve supply security but can slow down innovation due to higher operational costs and longer setup timelines.

Overall, while U.S. tariff policies aim to strengthen domestic biomanufacturing, in the short term, they are increasing financial and operational pressure on Stem Cell therapy developers, potentially delaying clinical development and commercialization of advanced regenerative therapies.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

TreeFrog Therapeutics |

€64 million |

Series B |

iPSC-derived cell therapy pipeline |

PSC-derived cell therapy pipeline (Parkinson’s, cardiac, metabolic disorders) |

|

XellSmart Biopharmaceutical |

RMB 100 million |

Series B |

iPSC-derived neural precursor cell therapy for ALS and neurological disorders |

iPSC-based differentiation platform for subtype-specific neural cells |

Key Takeaways from the Stem Cell Market Report Study

- Stem Cell Market size analysis for the current Stem Cell market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the Stem Cell market.

- Various opportunities available for the other competitors in the Stem Cell market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current Stem Cell market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the Stem Cell market growth in the future?

Stay updated with us for Recent Articles @ New DelveInsight Blogs

-market-Goutieres-Syndrome.png&w=256&q=75)