Urothelial Carcinoma Market

Urothelial Carcinoma Insights and Trends

- According to DelveInsight estimates, in 2025, the United States accounted for the urothelial carcinoma largest market size, although recent analyses suggest potential upside driven by increasing adoption of novel and targeted therapies.

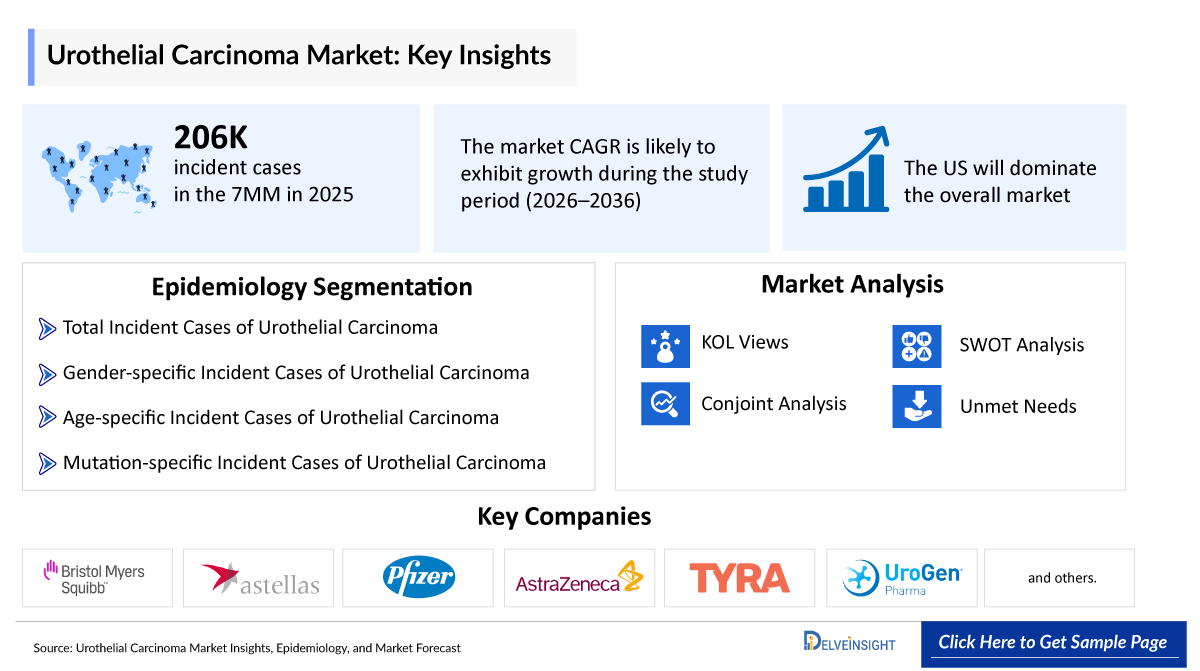

- In 2025, approximately 206,300 incident cases of urothelial carcinoma existed in the 7MM.

- Bladder cancer is the most prevalent malignancy of the urinary tract, with over 90% of cases in Europe classified as urothelial carcinomas.

- Approximately 4–10% of urothelial carcinomas cases arise in the upper urinary tract, including the renal pelvis and ureter.

- Around one-quarter of patients are diagnosed at the metastatic stage, where prognosis is poor, with overall survival typically ranging from 8–15 months, particularly in untreated individuals.

- Metastatic urothelial carcinoma is associated with a poor prognosis, with a 5-year overall survival rate of less than 5%, highlighting the aggressive nature of the disease.

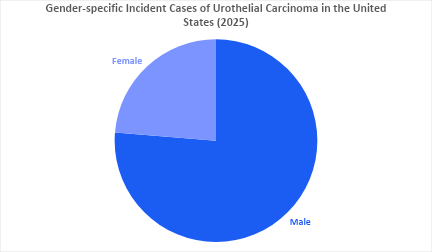

- The majority of urothelial carcinoma occurs in males and has approximately a two to threefold greater incidence than in females.

- The current treatment of urothelial carcinoma involves a multimodal approach that includes surgical interventions like Transurethral Resection (TUR) for diagnosis, staging, and initial control of non-muscle invasive disease, with re-TUR and radical cystectomy indicated for more advanced or recurrent cases.

- The initial management and prognosis of patients with urothelial carcinoma are largely determined by key factors such as the tumor’s anatomical location, stage (extent of disease), and histological grade. In cases of non-muscle-invasive bladder cancer (NMIBC), excluding carcinoma in situ (CIS), transurethral resection is commonly performed and is associated with favorable survival outcomes. Additionally, intravesical immunotherapy with the Bacillus Calmette–Guérin (BCG) vaccine is an effective treatment approach for NMIBC, as it significantly reduces the risk of disease recurrence and progression.

- Approved drugs for the treatment of urothelial carcinoma include nivolumab (OPDIVO), enfortumab vedotin-ejfv (PADCEV), pembrolizumab (KEYTRUDA), avelumab (BAVENCIO), erdafitinib (BALVERSA), and others.

- The emerging urothelial carcinoma pipeline is increasingly focused on next-generation ADCs, bispecific antibodies, targeted small molecules, cell therapies, and novel immunotherapy combinations aimed at improving survival outcomes and overcoming resistance to checkpoint inhibitors. Key late-stage and emerging candidates include Disitamab vedotin (HER2-targeted ADC), Tar-200, Cetrelimab, Nogapendekin alfa inbakicept (IL-15 agonist immunotherapy), and next-generation FGFR inhibitors and TIGIT-targeting immunotherapies.

Urothelial Carcinoma and Forecast in the 7MM

- 2025 Urothelial Carcinoma Market Size: ~USD XX million

- 2036 Urothelial Carcinoma Market Size: ~USD XX million

- Urothelial Carcinoma Growth Rate (2026–2036): XX% CAGR

Request for Unlocking the Sample Page of the Report @ Urothelial Carcinoma Market

DelveInsight's ‘Urothelial Carcinoma Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of the urothelial carcinoma, historical and forecasted epidemiology, as well as urothelial carcinoma market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The Urothelial Carcinoma market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates urothelial carcinoma patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in urothelial carcinoma and maps the competitive and clinical landscape to uncover high‑value opportunities, providing a clear outlook on future market growth potential.

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

Urothelial Carcinoma Market CAGR (Study period/Forecast period) |

XX% (2026 ̶ 2036) |

|

Urothelial Carcinoma Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

Urothelial Carcinoma Companies |

|

|

Urothelial Carcinoma Therapies |

|

|

Urothelial Carcinoma Market |

Segmented by

|

|

Analysis |

|

Key Factors Driving the Urothelial Carcinoma Market

Rising Incidence and Disease Burden of Urothelial Carcinoma

The increasing incidence of bladder cancer, particularly among the aging population, is a major factor driving the urothelial carcinoma market, as urothelial carcinoma accounts for nearly 90% of bladder cancer cases. Risk factors such as smoking, occupational exposure to chemicals, chronic bladder inflammation, and rising recurrence rates continue to contribute to the growing disease burden, increasing demand for effective long-term treatment options.

Increasing Focus on Personalized and Biomarker-Driven Treatment Approaches

Growing emphasis on precision medicine and biomarker testing is driving the adoption of personalized treatment strategies in urothelial carcinoma. The identification of actionable mutations and biomarkers is helping physicians optimize treatment selection, improve patient outcomes, and expand the eligible population for targeted therapies.

Robust Pipeline and Novel Combination Strategies

The urothelial carcinoma pipeline remains highly competitive, with pharmaceutical companies actively developing next-generation immunotherapies, targeted therapies, ADCs, and combination regimens. Ongoing clinical trials focused on improving response durability and overcoming treatment resistance are expected to further strengthen the market during the forecast period.

Urothelial Carcinoma Understanding and Treatment Algorithm

Urothelial Carcinoma Overview and Diagnosis

Urothelial carcinoma spans a broad clinical spectrum. At one end, it presents as a low-grade, non-muscle-invasive disease that, while rarely life-threatening, is prone to recurrence and requires long-term surveillance. At the other extreme, it manifests as high-grade disease, either non-muscle-invasive or muscle-invasive, with significantly higher risks. Muscle-invasive bladder cancer (MIBC) is life-threatening and demands prompt treatment. High-grade non-muscle-invasive disease carries a notable risk of progression to muscle-invasive or metastatic stages, often with poor outcomes. Metastatic progression occurs in approximately 25% of pT2, 50% of pT3, and 80% of pT4 tumors, with corresponding five-year survival rates of 67%, 35%, and 27%. Due to the heterogeneity of urothelial carcinoma, particularly in intermediate cases, standard treatment approaches may not be effective for up to 25% of patients.

Urothelial Carcinoma Diagnosis

Urine cytology is the most commonly used noninvasive test for detecting urothelial tumors, although its sensitivity remains limited. Cystoscopy continues to be the gold standard for diagnosis and surveillance of bladder cancer despite being invasive and costly. Several urine-based biomarkers, including BTA Stat, BTA TRAK, NMP-22, ImmunoCyt/uCyt, and UroVysion, have received FDA clearance or approval to support diagnosis and monitoring. Imaging techniques such as computed tomography (CT) are widely used to assess tumor location, extent, and multifocal disease, largely replacing intravenous pyelography (IVP). The US Preventive Services Task Force (USPSTF) does not recommend routine bladder cancer screening in asymptomatic adults due to the low predictive value of current noninvasive tests.

Further details are provided in the report.

Urothelial Carcinoma Treatment

The treatment of urothelial carcinoma depends on disease stage and patient eligibility, with goals focused on tumor control, recurrence prevention, and survival improvement. Non-muscle invasive disease is primarily managed with transurethral resection of bladder tumor (TURBT) followed by intravesical therapies such as BCG or chemotherapy. Muscle-invasive disease is typically treated with radical cystectomy combined with platinum-based chemotherapy, while radiation therapy may be used in select patients. In advanced and metastatic settings, immune checkpoint inhibitors such as Pembrolizumab, Nivolumab, and Atezolizumab have significantly expanded treatment options. Targeted therapies and antibody-drug conjugates, including Erdafitinib, Enfortumab vedotin-ejfv, and Sacituzumab govitecan, are further driving the shift toward personalized and biomarker-driven treatment strategies.

Further details related to country-based variations are provided in the report.

Urothelial Carcinoma Unmet Needs

The section “unmet needs of Urothelial Carcinoma” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- High recurrence and progression rates

- Limited efficacy of current treatment options

- Poor prognosis in advanced/metastatic disease

- Treatment-related toxicities and quality-of-life burden

- Limited options for cisplatin-ineligible patients

- Need for novel and more durable therapies and others….

Comprehensive unmet needs insights in Urothelial Carcinoma and their strategic implications are provided in the full report.

Urothelial Carcinoma Epidemiology

Key Findings from Urothelial Carcinoma Epidemiological Analysis and Forecast

- According to DelveInsight’s estimates, in 2025, there were nearly 206,300 incident cases of urothelial carcinoma in the 7MM.

- In EU4 and the UK, males accounted for more incident cases of urothelial carcinoma, i.e., nearly 75%, as compared to females, in 2025.

- As per the analysis, the median age of diagnosis of urothelial carcinoma is 69 years in men and 71 years in women.

- Tumors occurring in along the renal calyces and renal pelvis are twice as common as tumors found in the ureters. Carcinoma in situ (CIS) in the upper urinary tract may exist in 11–36% of individuals and UTUC can be multifocal in 10–20% of patients. Over 60% of UTUCs are muscle invasive at diagnosis and about 17% of cases are synchronous with a bladder tumor.

- Among the mutations observed in urothelial carcinoma, approximately 50% of the patients had a TP53 mutation, followed by a FGFR3 mutation (nearly 30%) in the United States.

- Following treatment for UTUC, recurrence in the bladder occurs in 29% of UTUC patients, depending on patient-, tumour- and treatment-specific characteristics compared to a 2–5% recurrence rate in the contralateral upper tract.

- Nearly all cases of urothelial carcinoma are UBCs, whereas UTUC accounts for just 5–10% of all urothelial malignancies.

- In the United States in 2025, Urothelial Carcinoma was found to be more incident in age group 80 years and above (~30,000) followed by age group 70-79 years.

- In Japan, among stage specific urothelial carcinoma in 2025, Non-muscle invasive urothelial carcinoma was found to be more incident (~15,600 cases), followed by muscle invasive urothelial carcinoma with locally advanced or metastatic urothelial carcinoma was the lowest.

Urothelial Carcinoma Drug Chapters & Competitive Analysis

The urothelial carcinoma drug chapter provides a detailed, market-focused review of approved therapies and the emerging pipeline across Phase I–III clinical trials. It covers the mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, and strategic partnerships for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the urothelial carcinoma treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the urothelial carcinoma therapeutics market.

Approved Therapies for Urothelial Carcinoma

Nivolumab (OPDIVO): Bristol-Myers Squibb

Nivolumab (OPDIVO), developed by Bristol-Myers Squibb is a human monoclonal antibody that blocks the interaction between PD-1 and its ligands, PD-L1 and PD-L2. In August 2021, the US FDA approved OPDIVO for the adjuvant treatment of patients with urothelial carcinoma who are at high risk of recurrence after undergoing radical resection, regardless of prior neoadjuvant chemotherapy, nodal involvement or PD-L1 status. In March 2024, the US FDA approved OPDIVO, in combination with cisplatin and gemcitabine, for the first-line treatment of adult patients with unresectable or metastatic urothelial carcinoma.

Enfortumab vedotin-ejfv (PADCEV): Astellas Pharma/Pfizer

Enfortumab vedotin-ejfv (PADCEV), developed by Astellas Pharma and Pfizer, is a Nectin-4 directed ADC comprised of a fully human anti-Nectin-4 IgG1 kappa monoclonal antibody (AGS-22C3) conjugated to the small molecule microtubule disrupting agent, monomethyl auristatin E (MMAE) via a protease-cleavable maleimidocaproyl valine-citrulline (vc) linker (SGD-1006). The US FDA has approved PADCEV in combination with KEYTRUDA for the treatment of adult patients with locally advanced or metastatic urothelial cancer.

In August 2024, the European Commission granted marketing authorization for PADCEV in combination with KEYTRUDA for the first-line treatment of adult patients with unresectable or metastatic urothelial cancer, who are eligible for platinum-containing chemotherapy.

|

Urothelial Carcinoma Marketed/Approved Therapies | ||||||

|

Drug/Therapy |

Company |

Indication |

Molecule Type |

RoA |

MoA |

Marketed Region |

|

Nivolumab (OPDIVO) |

Bristol Myers Squibb |

Urothelial carcinoma |

Monoclonal antibody |

IV infusion |

PD-1 immune checkpoint inhibitor |

US: 2017 EU: 2017 |

|

Enfortumab vedotin-ejfv (PADCEV) |

Astellas Pharma/ Pfizer |

Locally advanced or metastatic urothelial carcinoma |

ADC |

IV infusion |

Nectin-4-directed antibody linked to microtubule-disrupting agent |

US: 2019 EU: 2022 JP: 2021 |

|

Erdafitinib (BALVERSA) |

Johnson & Johnson |

Metastatic urothelial carcinoma |

Small molecule |

Oral |

Pan-FGFR tyrosine kinase inhibitor (targets FGFR1, FGFR2, FGFR3, and FGFR4) |

US:2019 EU:2024 |

Urothelial Carcinoma Pipeline Analysis

Disitamab vedotin (AIDIXI): Pfizer

Disitamab vedotin is a novel ADC that selectively delivers the anti-cancer agent monomethyl auristatin E (MMAE) into HER2-expressing tumor cells. In collaboration with RemeGen, Pfizer is currently conducting two clinical trials for Disitamab vedotin. One trial is in Phase III, focusing on first-line treatment for HER2 (≥IHC1+) mUC (SGNDV001), while the other is in Phase II, aimed at treating second-line and beyond urothelial cancer with HER2 expression.

In September 2025, Enfortumab vedotin-ejfv in combination with Pembrolizumab demonstrated promising Phase III EV-303/KEYNOTE-905 trial results in cisplatin-ineligible muscle-invasive urothelial carcinoma, highlighting the potential to redefine the standard of care in this patient population, according to updates presented by Pfizer.

Dabogratinib (TYRA-300): Tyra Biosciences

Dabogratinib is TYRA's lead precision medicine candidate stemming from its in-house SNÅP platform. Dabogratinib is an investigational, oral, FGFR3-selective inhibitor currently in Phase II development for the treatment of urologic cancers and skeletal dysplasias, specifically LG-UTUC. Dabogratinib was the first orally available, FGFR3 selective inhibitor to enter clinical development and it has been studied in more than 100 patients to date across multiple clinical studies. To date, oral dabogratinib has demonstrated very positive target engagement with FGFR3, favorable anti-tumor effects and safety results in oncology, and an optimized QD dosing regimen. Oral dabogratinib is currently advancing in three Phase II clinical trials for LG-UTUC (SURF303)

|

Comparison of Emerging Drugs Under Development | |||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Molecule Type |

Anticipated Launch in the US |

|

Disitamab vedotin (AIDIXI/RC48) |

Pfizer |

III |

HER2-expressing locally advanced or metastatic urothelial carcinoma |

IV |

HER2-targeted that delivers MMAE to HER2-expressing tumor cells |

Antibody-drug conjugate (ADC) |

Information is available in the full report |

|

Dabogratinib (TYRA-300) |

Tyra Biosciences |

II |

Advanced/ metastatic urothelial carcinoma with FGFR3 alterations |

Oral |

Selective FGFR3 inhibitor |

Small molecule |

Information is available in the full report |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | |||||||

Note: A detailed emerging therapies assessment will be provided in the final report

Urothelial Carcinoma Key Players, Market Leaders and Emerging Companies

- Bristol Myers Squibb

- Astellas

- Pfizer

- AstraZeneca

- Tyra Biosciences

- UroGen Pharma

- Johnson & Johnson

- Taiho Oncology, and others

Urothelial Carcinoma Key Players Drug Updates

- In April 2026, Mabwell to Present Latest Clinical Data on 9MW2821 Combined with Toripalimab for Urothelial Carcinoma in Oral and Poster Presentations at ASCO 2026.

- In November 2025 – Pembrolizumab + Enfortumab vedotin-ejfv, The US FDA approved pembrolizumab in combination with PADCEV as perioperative treatment for cisplatin-ineligible patients with muscle-invasive bladder cancer (MIBC), marking a major expansion of ADC + immunotherapy use in earlier-stage disease.

- In June 2025, the data of OPDIVO + YERVOY for cisplatin-ineligible metastatic urothelial carcinoma, presented at the ASCO 2025, failed to improve the overall survival.

- In April 2025, UroGen Pharma initiated the Phase III trial of UGN-104 for the treatment of patients with low-grade upper tract urothelial carcinoma.

- In February 2025, Pfizer and Astellas announced updated results from the Phase III EV-302 (KEYNOTE-A39) trial, showing sustained Overall Survival (OS) and Progression-free Survival (PFS) benefits with PADCEV + KEYTRUDA in previously untreated locally advanced or metastatic urothelial carcinoma after a median follow-up of 29.1 months. Additionally, the data was also presented at ASCO GU 2025 in San Francisco, CA, on February 14.

Drug Class Insights

Urothelial Carcinoma Market Outlook

The urothelial carcinoma market has evolved significantly from being primarily dependent on platinum-based chemotherapy to a more diversified landscape driven by immunotherapies, ADCs, and targeted therapies. Historically, cisplatin- and carboplatin-based chemotherapy remained the standard of care for advanced disease, while surgery dominated earlier-stage management. However, poor survival outcomes in metastatic disease and high recurrence rates created substantial unmet needs.

The introduction of immune checkpoint inhibitors such as pembrolizumab (KEYTRUDA), nivolumab (OPDIVO), and avelumab (BAVENCIO) expanded treatment options, particularly in maintenance and later-line settings. Among these, avelumab gained strong adoption as maintenance therapy following platinum chemotherapy.

A major shift in the market has been driven by enfortumab vedotin (PADCEV), an ADC targeting Nectin-4. Its combination with pembrolizumab has emerged as a new first-line standard for metastatic urothelial carcinoma after demonstrating strong overall survival and progression-free survival benefits in the Phase III EV-302 trial. Recent 2025 updates and expansion into earlier-stage muscle-invasive bladder cancer are expected to further strengthen its market position.

Targeted therapies such as erdafitinib (BALVERSA) continue to serve patients with FGFR2/3 mutations, supporting the growth of precision medicine in urothelial carcinoma. However, setbacks such as the withdrawal of sacituzumab govitecan (TRODELVY) in this indication have created competitive shifts within the ADC segment.

Overall, the urothelial carcinoma market is expected to grow steadily through 2036, driven by expanding use of ADC-immunotherapy combinations, earlier-line treatment adoption, and continued development of novel targeted therapies.

Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in Urothelial Carcinoma (2022–2036 Forecast)

The urothelial carcinoma market is expected to witness strong growth over the forecast period, driven by the transition from conventional chemotherapy toward targeted therapies and immuno-oncology approaches. While surgery and platinum-based chemotherapy continue to remain standard treatments, many patients are ineligible for cisplatin due to comorbidities, creating opportunities for alternative therapies. Immune checkpoint inhibitors, particularly PD-1/PD-L1 monoclonal antibodies such as Pembrolizumab and Nivolumab, have expanded treatment options, although response rates remain limited in some metastatic settings. Consequently, antibody-drug conjugates (ADCs) such as Enfortumab vedotin-ejfv and Sacituzumab govitecan are gaining momentum due to their targeted cytotoxic delivery and improved efficacy. Additionally, FGFR-targeted small molecules such as Erdafitinib and emerging modalities including CAR-T therapies, cytokine-based immunotherapies, and macrophage-targeted agents are expected to further drive the shift toward precision-based and next-generation treatment strategies.

Further details will be provided in the report….

Urothelial Carcinoma Drug Uptake

This section focuses on the uptake rate of potential drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the urothelial carcinoma market's uptake by drugs, patient uptake by therapy, and sales of each drug.

The uptake of therapies in urothelial carcinoma is expected to vary across chemotherapy, immune checkpoint inhibitors, ADCs, targeted therapies, and emerging combination regimens. Established platinum-based chemotherapies such as cisplatin and carboplatin-based regimens continue to maintain significant uptake in first-line treatment, particularly in eligible patients, due to long-standing physician familiarity, broad accessibility, and lower treatment costs. However, their uptake is gradually declining in metastatic settings due to survival limitations and the emergence of more effective targeted therapies.

Among immunotherapies, checkpoint inhibitors such as pembrolizumab (KEYTRUDA), nivolumab (OPDIVO), and avelumab (BAVENCIO) continue to witness strong adoption in maintenance and later-line settings. Avelumab maintains notable uptake as maintenance therapy following platinum chemotherapy due to its proven survival benefit in advanced urothelial carcinoma. Recently approved ADCs are expected to witness the fastest uptake during the forecast period. Enfortumab vedotin (PADCEV) has emerged as a major market leader, particularly following its strong Phase III EV-302 results in combination with pembrolizumab, which established the regimen as a new first-line standard for metastatic urothelial carcinoma. Its expanding use in earlier-stage muscle-invasive bladder cancer is expected to further accelerate uptake. Meanwhile, sacituzumab govitecan (TRODELVY) is expected to experience limited uptake following its withdrawal in metastatic urothelial carcinoma.

On the other hand, emerging therapies including next-generation ADCs, novel immunotherapy combinations, and precision oncology approaches are expected to witness gradual uptake following clinical success and regulatory approvals.

Overall, market uptake is expected to increasingly shift toward ADC-immunotherapy combinations and targeted therapies, while traditional chemotherapy and standalone immunotherapies continue to retain usage in specific patient populations due to cost advantages and established treatment experience.

Further detailed analysis of emerging therapies' drug uptake in the report…

Market Access and Reimbursement of Urothelial Carcinoma

-

The United States

|

The US Reimbursement for Urothelial Carcinoma | |

|

Drug |

Access Program |

|

Nivolumab (OPDIVO) |

|

|

Erdafitinib (BALVERSA) |

|

Reimbursement is a crucial factor that affects the drug’s access to the market. Often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

Further details are provided in the final report….

Urothelial Carcinoma Therapies Price Scenario & Trends

Pricing and analogue assessment of Urothelial Carcinoma therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, closest and most appropriate analogue selection for emerging therapies, and understanding of how pricing influences market access, adherence, and long-term uptake.

Further details are provided in the final report….

Industry Experts and Physician Views for Urothelial Carcinoma

To keep up with Urothelial Carcinoma market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry experts were contacted for insights on the Urothelial Carcinoma emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in Urothelial Carcinoma, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 10+ KOLs to gather insights; however, interviews were conducted with 6+ KOLs in the 7MM. Centers such as the Case Comprehensive Cancer Center, School of Medicine, Cleveland, Seidman Cancer Center, University Hospitals Cleveland Medical Center, Harvard Medical School, Boston etc. were contacted. Their opinion helps understand and validate current and emerging Urothelial Carcinoma therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in Urothelial Carcinoma.

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“Despite advances in diagnostic and therapeutic strategies, metastatic urothelial carcinoma remains a significant challenge. The diagnostic and monitoring techniques used for urologic cancers comprise a group of invasive methodologies that still lack sensitivity and specificity. Early diagnosis is crucial to improve patient outcomes and current treatments offer a range of options to manage urothelial carcinoma and metastatic urothelial carcinoma.” |

|

United States |

“With the aim of bringing treatment with immunotherapy into earlier lines and offer these active therapies to more patients with advanced urothelial carcinoma, different therapeutic approaches have been developed in the upfront setting, including the use of CPIs as single agents, combinations of CPIs ± CT or ADC and the use of CPIs as maintenance after non-progression with first-line CT.” |

Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis. In the SWOT analysis of Urothelial Carcinoma, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are majorly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Report

- The report covers a segment of key events, an executive summary, a descriptive overview of urothelial carcinoma, explaining its causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the Urothelial carcinoma market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM Urothelial carcinoma market.

Report Insights

- Urothelial Carcinoma Patient Population Forecast

- Urothelial Carcinoma Therapeutics Market Size

- Urothelial Carcinoma Pipeline Analysis

- Urothelial Carcinoma Market Size and Trends

- Urothelial Carcinoma Market Opportunity (Current and forecasted)

Report Key Strengths

- Epidemiology‑based (Epi‑based) Bottom‑up Forecasting

- Artificial Intelligence (AI)-enabled Market Research Report

- 11-year forecast

- Urothelial Carcinoma Market Outlook (North America, Europe, Asia-Pacific)

- Patient Burden Trends (by geography)

- Urothelial Carcinoma Treatment Addressable Market (TAM)

- Urothelial Carcinoma Competitive Landscape

- Urothelial Carcinoma Major Companies Insights

- Urothelial Carcinoma Price Trends and Analogue Assessment

- Urothelial Carcinoma Therapies Drug Adoption/Uptake

- Urothelial Carcinoma Therapies Peak Patient Share analysis

Report Assessment

- Urothelial Carcinoma Current Treatment Practices

- Urothelial Carcinoma Unmet Needs

- Urothelial Carcinoma Clinical Development Analysis

- Urothelial Carcinoma Emerging Drugs Product Profiles

- Urothelial Carcinoma Market Attractiveness

- Urothelial Carcinoma Qualitative Analysis (SWOT and Conjoint Analysis)

FAQs

Market Insights

- What was the Urothelial Carcinoma market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of Urothelial Carcinoma?

- What are the disease risks, burdens, and unmet needs of Urothelial Carcinoma? What will be the growth opportunities across the 7MM concerning the patient population with Urothelial Carcinoma?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of Urothelial Carcinoma? What are the current guidelines for treating Urothelial Carcinoma in the US, Europe, and Japan?

Reasons to Buy

- The report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the Urothelial Carcinoma market.

- Bottom-up forecasting builds from the affected population to product forecasts, delivering a robust, data-driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI)-enabled report summarize and simplify complex datasets within the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data-driven decisions.