Uveitis Market

- The Uveitis Market Size in the 7MM was approximately ~USD 1,468.66 million in 2022 and is projected to increase due to increasing awareness of the disease and the launch of the emerging therapies during the forecast period (2023–2034).

- In 2022, the Uveitis Market Size was highest in the US among the 7MM, accounting for approximately USD 759.03 million, which is expected to increase by 2034.

- The Uveitis Prevalence has been increasing in the US due to the rising occurrence of uveitis-associated conditions, increasing awareness, and improved diagnosis of uveitis.

- Advancements in disease nomenclature for classification, clinical trials, drug delivery systems, multimodality diagnostic imaging, and laboratory testing involving “omics” technology have provided insight into disease pathogenesis. Moreover, insights into ocular immunology have also led to a better understanding of the molecular mechanisms that underlie etiology and susceptibility to uveitis.

- The ongoing research efforts are leading to a better understanding of uveitis risk factors, and treatment strategies, driving innovation in disease management.

- Corticosteroids are used as first-line therapy to treat inflammation in Uveitis Patients. Further, immunomodulatory drugs are given as steroid-sparing agents when quiescence is not obtained with corticosteroids. Surgical interventions such as vitrectomy or the implantation of sustained-release devices are considered in extreme cases of uveitis.

- One of the major concerns in understanding the market for uveitis is that there is a lack of evidence to support the efficacy of many interventions used in the daily management of uveitis. Furthermore, no proper consensus guidelines are available in the US, EU4, and the UK, and Japan for managing different types of uveitis and its associated conditions.

- Immunosuppressant agents form the standard gold treatment for noninfectious uveitis, patients who require prolonged treatment, or those with recurrent or refractory uveitis. Although they show effective outcomes, long-term use is associated with severe side effects or adverse events.

- With no curative therapy and the large side effects associated with the current treatment regime, there is a need for therapies that are effective in a short time with no associated complications or effects besides treating the associated complications like edema or glaucoma.

- However, emerging therapies TRS01, licaminlimab (OCS-02), and vamikibart (RO720220/ RG6179) can potentially create a positive shift in the uveitis market size during the forecast period.

- If approved, Tarsier Pharma’s TRS01 would be the first nonsteroidal eye drops to treat noninfectious anterior uveitis.

- OCS-02, a single-chain antibody fragment with a dual mechanism of action, anti-inflammation, and anti-necrosis, is supposed to address the significant medical need for a steroid-sparing agent and a topical biologic without the associated systemic risks.

- Roche’s RG6179, a recombinant humanized immunoglobulin, suppresses IL-6 signaling and acts against uveitic macular edema. It is expected to enter the US market by 2026.

Request for unlocking the CAGR of the "Uveitis Drugs Market"

Key Factors Driving Uveitis Market

Rising Uveitis Prevalence in the US

The prevalence of uveitis has been steadily rising in the US, primarily due to the growing burden of uveitis-associated conditions, increasing awareness, and improved diagnostic approaches. In 2022, the US contributed to the largest diagnosed prevalent population in the 7MM, accounting for nearly 37.5% of cases, whereas Spain reported the lowest share at around 7%. This upward trend is anticipated to continue over the coming years, reflecting advancements in screening and disease recognition.

Advancements in Uveitis Diagnostics and Pathogenesis

Progress in disease classification, multimodality imaging, laboratory testing with “omics” technology, and ocular immunology research has enhanced the understanding of uveitis pathogenesis. These insights are enabling more accurate diagnosis, risk factor identification, and tailored treatment strategies. However, a lack of standardized consensus guidelines across the US, EU4, the UK, and Japan continues to hinder consistent disease management.

Uveitis Treatment Approaches

Corticosteroids remain the first-line therapy for controlling inflammation in uveitis patients, while immunomodulatory agents are used as steroid-sparing alternatives in refractory or recurrent cases. Surgical interventions, such as vitrectomy or sustained-release device implantation, are reserved for severe cases. Despite these treatment options, long-term use of immunosuppressants is associated with adverse effects, and no curative therapies are available, leaving significant unmet needs in disease management.

Launch of Emerging Uveitis Drugs

The uveitis therapeutic landscape is poised for transformation with the emergence of novel agents. Tarsier Pharma’s TRS01, if approved, would become the first nonsteroidal eye drop for noninfectious anterior uveitis. Licaminlimab (OCS-02), a single-chain antibody fragment with dual anti-inflammatory and anti-necrosis activity, is positioned as a topical biologic and steroid-sparing agent with reduced systemic risks. Roche’s vamikibart (RG6179), a recombinant humanized immunoglobulin targeting IL-6 signaling, is expected to enter the US market by 2026 to address uveitic macular edema. These therapies could significantly shift treatment paradigms, addressing safety and efficacy gaps in current care.

DelveInsight’s “Uveitis Drugs Market Insights, Epidemiology, and Market Forecast – 2034” report delivers an in-depth understanding of uveitis, historical and forecasted epidemiology, as well as the Uveitis therapeutics market trends in the United States, EU4 (Germany, France, Italy, and Spain) and the United Kingdom, and Japan.

The Uveitis Drugs Market Report provides current treatment practices, emerging drugs, market share of individual therapies, and current and forecasted 7MM uveitis market size from 2020 to 2034. The report also covers current uveitis treatment market practices/algorithms and unmet medical needs to curate the best opportunities and assess the market’s potential.

|

Study Period |

2020 to 2034 |

|

Forecast Period |

2024-2034 |

|

Geographies Covered |

|

|

Uveitis Market |

|

|

Uveitiss Market Size | |

|

Uveitis Companies |

Tarsier Pharma, Oculis Pharma, Roche, Eleven Biotherapeutics, Eli Lilly and Company, Eyevensys, Acelyrin, Affibody Medical, Priovant Therapeutics, and others. |

|

Uveitis Epidemiology Segmentation |

|

Uveitis Treatment Market

Uveitis is a sight-threatening inflammatory disease affecting the middle uveal layer of the eye. The inflammation usually happens when the immune system fights an infection affecting the uveal tract (composed of the iris, choroid, and ciliary body) and adjacent structures (including the sclera, cornea, vitreous humor, retina, and optic nerve head).

Uveitis is one of the leading causes of visual morbidity, with over one-third of patients with uveitis having a visual impairment and accounting for about 10–15% of blindness cases worldwide. Uveitis can affect people of all ages and can vary significantly by geographic location and age of the patient. Anterior uveitis is the most prevalent form, accounting for approximately 50% of uveitis cases, while posterior uveitis is the least common.

Uveitis can occur at any age, but the peak incidence is between 20 and 59. Studies suggest females under age 50 appear to be the most affected. Additionally, the presence of other autoimmune diseases, psychological stress, and vitamin D deficiency had a bigger risk for noninfectious uveitis (NIU). Unlike other ocular diseases, such as glaucoma or age-related macular degeneration, which generally affect elderly populations, uveitis can occur in all age groups and affects young adults. The epidemiology varies depending on genetic and ethnic factors, environmental factors, gender, and idiopathic diseases associated with uveitis.

Uveitis can occur either as a co-manifestation of various autoimmune disorders and infections or as a side effect of medications and toxins. However, uveitis means the immune system is fighting an eye infection, but it can also happen when the immune system attacks healthy tissue in the eyes. Sometimes uveitis goes away quickly, but it can return, and sometimes it is a chronic condition.

Some common symptoms associated with uveitis include blurry vision with redness and sensation of pain, developing sensitivity to light, floaters in vision, and the presence of a white spot on the lower part of the eye. An individual’s one eye or both may be affected. The pathophysiology of uveitis is not well understood; groups have hypothesized that trauma to the eye can cause cell injury or death, leading to the release of inflammatory cytokines leading to post-traumatic uveitis.

Uveitis is caused due to molecular mimicry, where an infectious agent crossreacts with ocular-specific antigens. This molecular mimicry between retinal S-Ag peptides and a peptide from disease-associated HLA-B antigens leads to targeting ocular proteins and inflammatory response.

Uveitis Diagnosis

Uveitis is diagnosed after a complete evaluation of the past medical, family, and ophthalmic history of the patient. A full review of systems may also help identify a systemic disease with ocular manifestations. A visual acuity test, an ocular pressure test, and a slit lamp exam are performed by an ophthalmologist. The diagnosis and management of uveitis can be tricky for multiple reasons.

Further details related to country-based variations are provided in the report…

Uveitis Treatment

Treatment for uveitis aims to help reduce inflammation and relieve pain and discomfort in the eye, which can prevent permanent loss of vision or other complications. The latest uveitis treatment guidelines emphasize early diagnosis and appropriate therapy to prevent complications. The primary goal of treating uveitis is getting rid of inflammation as fast as possible. Currently approved options include XIPERE, OZURDEX, HUMIRA, YUTIQ/ILUVIEN, RETISERT, and DUREZOL. The uveitis pipeline drugs market shows significant potential, driven by innovative therapies and ongoing clinical developments.

First-line of Therapy: Corticosteroids

Corticosteroids are the mainstay of therapy for acute uveitis of noninfectious causes and can be used with antibiotics in some cases of infectious uveitis. They can be given by drops, injection around or inside the eye, mouth, or IV infusions, depending on the location and severity of inflammation. Unfortunately, they can never be depended upon for long-term control of uveitis as they inevitably cause complications, such as cataracts and glaucoma. Starting therapy of the treatment algorithm of uveitis is the administration of topical corticosteroids; high-potency glucocorticoids are more efficacious than low-potency preparations; therefore, the high-potency drugs, such as prednisolone acetate 1% or dexamethasone 0.1%, should be used. If that therapy fails, patients receive topical and systemic corticosteroids in combination.

Second Line of Therapy: Immunosuppressant

The appropriate treatment and choice of uveitis immunosuppressive therapy depend on the extent and severity of the inflammatory process; the need for immunosuppressive drugs depends on the cause of the inflammation. Methotrexate is used as a second line in treating juvenile idiopathic arthritis-associated uveitis. According to a report, only 15% of patients with intermediate uveitis need immunosuppressive agents. Of patients with scleritis, about one-third will respond to oral corticosteroid drugs, and one-fourth will need other immunosuppressive drug treatment. Nearly all patients with Behçet’s disease and about two-thirds of those with sympathetic ophthalmia require immunosuppressive drugs.

Third Line of Therapy: Biologics

In current uveitis practice, biologics are usually used as third-line agents as rescue therapy for refractory cases in a step-up approach. However, uveitis specialists have ongoing arguments regarding whether biologics should be considered first-line therapy in certain cases (for instance, pan uveitis in Behçet disease with macular involvement) following a top-down approach. No biologics have been specifically approved for uveitis; however, adalimumab is approved for treating NIU.

With appropriate treatment, most episodes of anterior uveitis disappear within a few days or weeks, but patients often suffer recurrences. Inflammation associated with posterior uveitis can last months to years and cause permanent vision damage, even when treated.

.jpg)

Uveitis Epidemiology

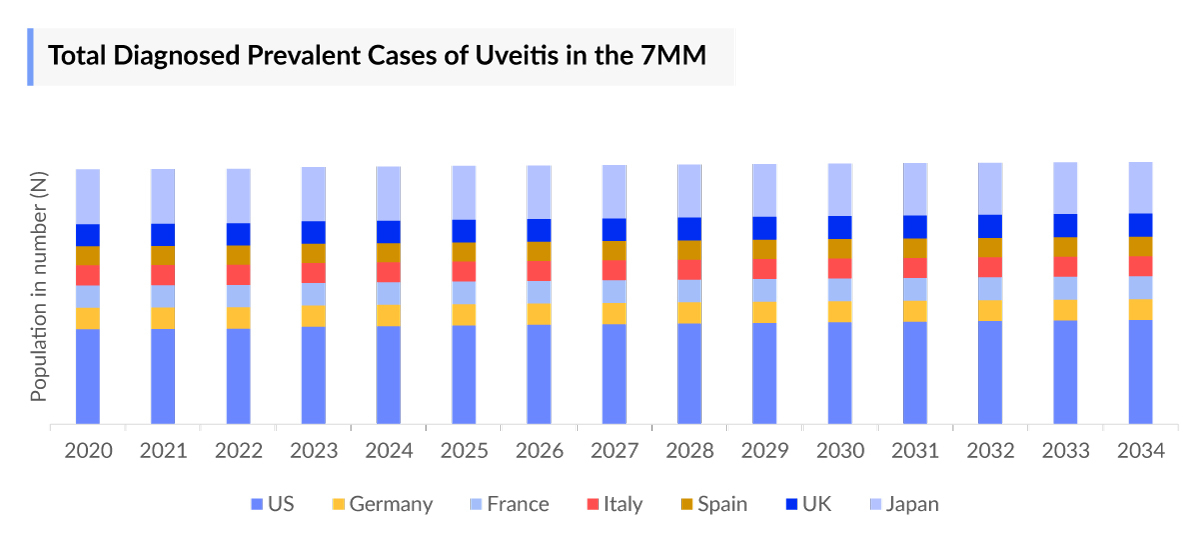

As the market is derived using a patient-based model, the uveitis epidemiology chapter in the report provides historical as well as forecasted epidemiology segmented by total diagnosed prevalent cases of uveitis, type-specific diagnosed prevalent cases of uveitis, diagnosed prevalent cases of uveitis by anatomical location, and etiology-specific diagnosed prevalent cases of uveitis, in the 7MM covering the United States, EU4 countries (Germany, France, Italy, and Spain) and the United Kingdom, and Japan from 2020 to 2034.

- As per DelveInsight analysis, in 2022, there were approximately 1,009,025 Uveitis diagnosed prevalent cases in the 7MM.

- The total number of Uveitis diagnosed prevalent cases in the US was around 378,281 in 2022.

- The US contributed to the largest Uveitis diagnosed prevalent population, acquiring ~37.5% of the 7MM in 2022. Whereas Spain accounted for the least, with around ~7% of the total population share, respectively, in 2022.

- In the US, patients diagnosed with noninfectious uveitis (NIU) are higher in number than infectious uveitis (IU). In 2022, there were nearly 344,587 cases of NIU, while IU accounted for around 33,695 cases. These numbers are expected to rise during the forecast period due to the rise of overall uveitis infection in the US.

- According to DelveInsight estimates, in EU4 and the UK, based on anatomical location highest cases of uveitis were diagnosed in anterior uveitis, while intermediate uveitis has the least cases. In EU4 and the UK, anterior uveitis accounted for approximately 203,439, followed by 84,154 cases in posterior uveitis, 81,773 cases in pan uveitis, and 46,485 in intermediate uveitis in 2022, which are projected to increase during the forecast period.

- Japan accounted for approximately 214,892 diagnosed prevalent cases of uveitis, out of which nearly 8,039 cases were of HLA-B27-associated uveitis, 17,315 sarcoidosis, 9,894 Behçet’s disease, 8,658 Vogt–Koyanagi–Harada disease, 618 JIA, 309 ankylosing spondylitis, 3,092 tuberculosis, 11,749 herpes, 81,628 idiopathic, and 73,589 others cases in 2022. These uveitis cases are expected to change during the forecast period in Japan (2023–2034).

Uveitis Drugs Market Chapters

The Uveitis drugs market chapter segment of the uveitis drugs market report encloses a detailed analysis of uveitis-marketed drugs and late-stage (Phase III and Phase II) Uveitis pipeline drugs. It also helps understand the uveitis clinical trials details, expressive pharmacological action, agreements and collaborations, approval and patent details, advantages and disadvantages of each included drug and the latest Uveitis news and press releases.

Uveitis Marketed Drugs

- XIPERE: Clearside Biomedical/Bausch+Lomb

XIPERE, a triamcinolone acetonide injectable suspension, is the first approved medicine delivery via injection for suprachoroidal use to treat macular edema associated with uveitis in the US. Delivering the medicine to the suprachoroidal space (SCS) allows targeted delivery of the therapy with low levels elsewhere in the eye.

In October 2021, the US FDA approved XIPERE (triamcinolone acetonide injectable suspension) for suprachoroidal use to treat macular edema associated with uveitis, a form of eye inflammation. The recommended dosage is 4 mg (0.1 mL), administered as a suprachoroidal injection. It is a 40 mg/mL suspension in a single-dose glass vial with the supplied SCS microinjection. Furthermore, the American Medical Association has granted a new permanent Category 1 Current Procedural Terminology (CPT) code for Bausch & Lomb’s XIPERE to help facilitate better access and adoption of the product.

YUTIQ is a sterile nonbioerodible intravitreal implant with 0.18 mg fluocinolone acetonide. It releases the drug at an initial rate of 0.25 µg/day in a 36-month sustained-release drug delivery system. YUTIQ contains a corticosteroid and is indicated for treating chronic noninfectious uveitis affecting the posterior segment of the eye. It is preloaded into a single-dose applicator to facilitate the injection of the implant directly into the vitreous. It was approved by the US FDA in October 2018 and launched commercially in February 2019.

Uveitis Emerging Drugs

- TRS01: Tarsier Pharma

TRS01, a lead product of Tarsier Pharmaceuticals, first in first-in-class topical immune modulator agent. Dazdotuftide (TRS) is a breakthrough platform technology for treating blinding ocular diseases. TRS was developed to ‘re-engineer’ the immune system. The platform approaches inflammatory diseases from within the system. The technology can effectively treat various autoimmune and inflammatory ocular diseases. TRS01 is a polypeptide conjugate with a dual mechanism of action; the investigational agent induces anti-inflammatory macrophages and inhibits the nuclear factor-kB (Nf-kB) signaling pathway by toll-like receptor 4 (TLR4).

TRS01 has completed a Phase III trial, called TRS4Vision, in patients with active noninfectious anterior uveitis, including those with uveitis glaucoma. The trial met its secondary endpoint; however, it failed to meet the primary endpoint. Based on the safety and potency of the TRS01 and a positive Type C meeting with the US FDA, the company plans to initiate a second Phase III trial (Tarsier-04) for the treatment of noninfectious uveitis, including uveitic glaucoma with revised endpoints. Additionally, the company is developing TRS02 intravitreal injection for intermediate, posterior, or pan uveitis.

- OCS-02 (licaminlimab): Oculis Pharma

OCS-02 (licaminlimab) is a single-chain antibody fragment (scFv) that binds to and neutralizes the activity of human TNFa, with a dual mechanism of action (MoA), anti-inflammation, and anti-necrosis. Unlike full-length monoclonal antibodies, scFv fragments can penetrate ocular surface tissues when used as eye drops due to the smaller molecule size giving it the potential to become the first approved topical biologic for DED (dry eye disease) (OCS-02 was previously known as LME636).

The company plans to initiate a Phase IIb clinical trial to evaluate its potential treatment for noninfectious anterior uveitis following a Phase IIb trial for DED, whose patient’s first visit occurred in late 2023.

If approved, OCS-02 is anticipated as the first topical, nonsteroidal therapy or biologic for noninfectious anterior uveitis. It is supposed to address the significant medical need for a steroid-sparing agent and for a topical biologic to be indicated specifically for noninfectious anterior uveitis without the associated systemic risks.

Uveitis Drugs Market Class Insights

A severe intraocular inflammatory condition of the uveal tract known as uveitis frequently results in vision loss, blindness, and reduced quality of life. With the disease having a variable presentation, diagnosis and management are difficult. Treatment aims at obtaining quiescence of the disease, either by treating the infectious agent or treating the immune condition.

The current promising pharmacological classes for uveitis treatment include corticosteroids, immunosuppressants, and biologics. The uveitis drugs market is growing, driven by innovative therapies and increasing global prevalence.

Topical steroids like prednisolone 1% or dexamethasone 0.1% for anterior uveitis, mydriatic and cycloplegic agents to prevent the formation of posterior synechiae and for relieving photophobia and pain secondary to ciliary spasm are recommended. Difluprednate is recommended when there is posterior inflammation or macular edema. Systemic corticosteroids are typically reserved for bilateral uveitis, systemic disease, or when topical/local therapies fail to control inflammation; oral prednisone is the most commonly used drug. When the inflammation is severe, involving all the uveal layers and eventually the optic nerve, IV corticosteroids are needed to achieve ocular remission. Several intravitreal steroid injections are utilized in the treatment of uveitis. The approved products include YUTIQ, OZURDEX, XIPERE, RETISERT, and TRIESENCE. However, long-term corticosteroid treatment can cause serious systemic and ocular side effects, such as hypertension, diabetes, cataracts, and glaucoma.

Alternatively, immunomodulatory drugs are given as steroid-sparing agents when quiescence is not obtained with corticosteroids or in case of reactivation or new complications onset. These have good clinical results for systemic and ocular inflammatory diseases. It includes the antimetabolites (methotrexate, azathioprine, and mycophenolate mofetil); the calcineurin inhibitors (cyclosporine, tacrolimus, and sirolimus); alkylating agents (cyclophosphamide and chlorambucil). Despite these promising clinical results, it is used off-label for treating NIU. Refractory and recurrent uveitis require a combination of IMT agents. IMT is continued for 2 years while the patient is in remission before considering tapering medication.

These biologic response modifiers represent the next medications in the stepladder approach to noninfectious uveitis. Biologic response modifiers that include the tumor necrosis factor (TNF)-a inhibitors infliximab, adalimumab, etanercept, golimumab, and certolizumab; lymphocyte inhibitors include daclizumab, rituximab, abatacept, and basiliximab; specific receptor antagonists includes anakinra, canakinumab, gevokizumab, tocilizumab, alemtuzumab, efalizumab, secukinumab, and ustekinumab; and interferon (INF) treatments. While anti-TNF-a is the most widely used for treating uveitis. These medications are chosen, by adding or switching, when other immunosuppressive agents are ineffective. TNF-a is an important cytokine involved in ocular inflammation and tissue damage. Anti-TNF-a is also recommended for children. Adalimumab is a fully human anti-TNF-a monoclonal antibody approved for treating several immune-mediated inflammatory diseases, including noninfectious intermediate, posterior, and panuveitis. The lone approved product in this category, enjoying a major market share of biologics, is AbbVie’s HUMIRA.

Uveitis Market Outlook

Uveitis is a serious intraocular inflammatory disorder of the uveal tract, often associated with visual impairment, blindness, and decreased quality of life. It often affects patients in their most active and economically productive years. It is the leading cause of preventable blindness worldwide and is a critically underserved disease in terms of treatment.

With the disease having a variable presentation, diagnosis and management are difficult. A prompt diagnosis, with the correct diagnostic approach and assessment of appropriate treatment, is extremely important to reduce inflammation and attain complete remission, thereby mitigating or avoiding ocular complications, permanent cumulative damage, and long-term vision loss. Treatment aims at obtaining quiescence of the disease, either by treating the infectious agent or treating the immune condition.

The recommended treatment scenario starts with the least aggressive treatments to induce inflammation remission and progresses to more aggressive treatments and, eventually, inflammation remission. The choice of therapy (including the administration route) depends on the underlying diagnosis, the aggressiveness of the disease, laterality, and the presence of comorbid conditions. It is also essential to balance the ability of these drugs to induce disease remission against their potential side effects and toxicities. Corticosteroids, immunomodulators, and biologics are the various treatment options besides surgery.

The current market has been segmented into different commonly used therapeutic classes based on the prevailing treatment pattern across the 7MM, which presents minor variations in the overall prescription pattern. YUTIQ/ILUVIEN, HUMIRA, and XIPERE are the major drugs covered in the forecast model.

Key Uveitis Companies including RG6179, TRS01, OCS-02, OCS-01, EYS606, and others are evaluating their lead candidates in different stages of clinical development. They aim to investigate their products for the treatment of uveitis.

- The Uveitis market size in the 7MM was approximately USD 1,468.66 million in 2022 and is projected to increase due to increasing awareness of the disease and the launch of the emerging therapies during the forecast period (2023–2034).

- According to DelveInsight’s estimates, among the 7MM, the US had the largest Uveitis market share, with a revenue of USD 759.03 million in 2022, followed by Japan, Germany, and others.

- Among EU4 and the UK countries, Germany accounted for the maximum Uveitis market size with approximately USD 115.73 million in 2022, while Spain occupied the bottom of the ladder with nearly USD 90.49 million in 2022.

- Japan accounted for the second largest Uveitis drugs market among the 7MM, with approximately USD 196.62 million in 2022, expected to increase during the forecast period (2023–2034).

- The current standard of care for uveitis includes corticosteroids like YUTIQ/ILUVIEN, XIPERE-for macular edema, immunosuppressants, biologics like HUMIRA, NSAIDs, and others. As per DelveInsight’s estimates, in the 7MM, the second highest market share was captured by corticosteroids accounting for USD 344.78 million, out of which YUTIQ/ILUVIEN accounted for USD 32.34 million, while other corticosteroids accounted for USD 312.44 million, in 2022.

- The Uveitis emerging pipeline is robust, and the major players involved are Tarsier Pharma (TRS01), Roche/Eleven Biotherapeutics (vamikibart (RO720220/RG6179)), Oculis Pharma (licaminlimab (OCS-02)), and others.

- Tarsier Pharma TRS01 is a topical immune modulator agent with the potential to treat active noninfectious anterior uveitis with or without uveitic glaucoma. It is expected to enter the US market by 2026 and is projected to generate a revenue of USD 2.91 million in its launch year.

Uveitis Drugs Uptake

This section focuses on the uptake rate of potential Uveitis drugs expected to be launched in the market during 2020–2034. For example, vamikibart (RO720220/RG6179), a monoclonal antibody, is being developed for a target patient pool having uveitic macular edema and is projected to enter EU4 and the UK in, 2027, is predicted to have a slow-medium uptake during the forecast period.

Uveitis Pipeline Development Activities

The Uveitis pipeline segment provides insights into Uveitis clinical trials within Phase III, Phase II, and Phase I. It also analyzes key Uveitis companies involved in developing targeted therapeutics.

Pipeline development activities

The Uveitis pipeline segment covers information on collaborations, acquisitions and mergers, licensing, and patent details for Uveitis emerging therapies.

KOL Views

To keep up with current Uveitis market trends, we take KOLs and SMEs’ opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry Experts contacted for insights on uveitis evolving Uveitis treatment market landscape, patient reliance on conventional therapies, patient therapy switching acceptability, and drug uptake, along with challenges related to accessibility, including Medical/scientific writers, Medical Professionals, Professors, Directors, and Others.

DelveInsight’s analysts connected with 50+ KOLs to gather insights; however, interviews were conducted with 15+ KOLs in the 7MM. Centers like the University of California, University of Nebraska Medical Center Omaha, Johns Hopkins University School of Medicine, University Medical Center Schleswig Holstein, Sapienza University of Rome, and University of Tokyo School of Medicine were contacted. Their opinion helps understand and validate current and emerging therapy treatment patterns or uveitis market trends. This will support the clients in potential upcoming novel treatments by identifying the overall scenario of the market and the unmet needs.

Physician’s View

According to our primary research analysis, several corticosteroids with different modes of action (topical, oral, or injections), some possessing more than one, are available in the market and prescribed as monotherapy or adjunctive therapy in different lines of treatment. Many cases can be successfully managed with prompt diagnosis and treatment, reducing vision loss and complications. However, some types of uveitis are chronic or recurrent, necessitating ongoing treatment and monitoring to preserve vision and avoid complications. As a result, each patient's treatment plan is tailored to their specific needs based on factors such as the type of uveitis, its frequency, etiology, and anatomical location, the person’s age, and associated complications. For elderly patients, factors such as overall health, medication tolerance, and functional status are taken into account.

The current pipeline contains gene therapy, monoclonal antibodies, recombinant fusion proteins, and several small molecules that target different anti-inflammatory pathways in uveitis. The entry of these drugs will provide different options relating to patient-specific needs.

Qualitative Analysis

We perform Qualitative and Uveitis drugs market Intelligence analysis using various approaches, such as SWOT analysis and Conjoint Analysis. In the SWOT analysis, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided. These pointers are based on the Analyst’s discretion and assessment of the patient burden, cost analysis, and existing and evolving Uveitis treatment market landscape.

Conjoint Analysis analyzes multiple emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

In efficacy, the trial’s primary and secondary outcome measures are evaluated; for instance, in uveitis trials, one of the most important primary outcome measures is the anterior chamber cell (ACC) grade.

Further, the therapies’ safety is evaluated wherein the acceptability, tolerability, and adverse events are majorly observed, and it sets a clear understanding of the side effects posed by the drug in the trials. In addition, the scoring is also based on the route of administration, order of entry and designation, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Uveitis Drugs Market Access and Reimbursement

Reimbursement of rare disease therapies can be limited due to lack of supporting policies and funding, challenges of high prices, lack of specific approaches to evaluating rare disease drugs given limited evidence, and payers’ concerns about budget impact. The high cost of rare disease drugs usually has a limited impact on the budget due to the small number of eligible patients being prescribed the drug. The US FDA has approved several rare disease therapies in recent years. From a patient perspective, health insurance and payer coverage guidelines surrounding rare disease treatments restrict broad access to these treatments, leaving only a small number of patients who can bypass insurance and pay for products independently.

In June 2022, the CMS issued a product-specific J-Code for XIPERE (triamcinolone acetonide) effective July 1, 2022. J-Codes are reimbursement codes used by commercial insurers and government payers to identify therapies administered by a healthcare professional incident to the office visit. Issuing the permanent J-Code helped facilitate access to XIPERE for Americans suffering from macular edema associated with uveitis and helped streamline the reimbursement process. It became commercially available in March 2022. The new J-Code is J3299.

Blue Cross and Blue Shield of Alabama provide coverage for XIPERE (triamcinolone acetonide injectable suspension). The coverage is provided for 12 weeks and may be renewed.

In October 2018, the US FDA approved YUTIQ (fluocinolone acetonide intravitreal implant) to treat chronic noninfectious uveitis affecting the posterior segment of the eye. In July 2019, the CMS had assigned a specific and permanent reimbursement J-code, J7314, through the Healthcare Common Procedure Coding System (HCPCS) for YUTIQ, 0.18 mg 3-year micro-insert for chronic, noninfectious uveitis affecting the posterior segment of the eye. Furthermore, the code J7314 became effective in October 2019.

Patient assistance programs (PAPs) are usually sponsored by pharmaceutical companies and provide free or discounted medicines and copay programs to low-income, uninsured, and underinsured people who meet specific guidelines. Eligibility requirements vary for each program.

The YUTIQ developing company EyePoint Pharmaceuticals, Inc. provides EyePoint Assist HCP Portal that allows patients to conduct a benefits investigation, confirm insurance eligibility, and gain access to financial and reimbursement support.

OZURDEX is an intravitreal implant of 0.7 mg dexamethasone approved in the US in September 2010 for treating noninfectious uveitis affecting the posterior segment of the eye. Recognizing that reimbursement is a significant patient consideration, Allergan EyeCueSM provides a convenient and efficient way to help manage OZURDEX reimbursement processes. Through the OZURDEX saving program, eligible commercially insured patients may pay as little as USD 0 for OZURDEX.

An intravitreal implant RETISERT, for treating chronic noninfectious uveitis affecting the posterior segment, has a Medicare payment rate of almost USD 20,000 when used in a hospital outpatient setting, according to a press release from Bausch + Lomb. RETISERT (fluocinolone acetonide intravitreal implant) 0.59 mg was launched in the US in June, following approval by the FDA in April. The Centers for Medicare & Medicaid Services has designated the single-indication orphan drug eligible for Medicare pass-through payment under the hospital outpatient prospective payment system.

The European Union (EU) is the most biosimilar-friendly market, along with the European Economic Area countries (Iceland, Liechtenstein, and Norway), with the US vamping up its policies to align itself with its Trans-Atlantic neighbor. Biosimilar competition in Europe has brought about discounts to AbbVie’s blockbuster immunosuppressant drug HUMIRA upwards of 80% during tendering. Overall, biosimilar uptake has increased in Europe because biologic “copycats” are cheaper, but full faith in these products is still required from physicians and patients.

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenarios, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

The Uveitis drugs market report provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenarios, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

Further details will be provided in the report....

Uveitis Treatment Market Report Scope

- The Uveitis treatment market report covers a segment of key events, an executive summary, descriptive overview, explaining its causes, signs and symptoms, pathogenesis, and currently available therapies.

- Comprehensive insight has been provided into the Uveitis epidemiology segments and forecasts, the future growth potential of diagnosis rate, disease progression, and treatment guidelines.

- Additionally, an all-inclusive account of the current and Uveitis emerging therapies, along with the elaborative profiles of late-stage and prominent therapies, will impact the current Uveitis treatment market landscape.

- A detailed review of the uveitis drugs market, historical and forecasted Anterior Uveitis Treatment Market Size, Uveitis market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The Uveitis treatment market report provides an edge while developing business strategies, by understanding trends, through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help shape and drive the 7MM uveitis drugs market.

Uveitis Therapeutics Market Report Insights

- Patient-based Uveitis Market Forecasting

- Uveitis Therapeutic Approaches

- Uveitis Pipeline Drugs Analysis

- Uveitis Treatment Market Size

- Uveitis Market Trends

- Existing and Future Uveitis Drugs Market Opportunity

Uveitis Therapeutics Market Report Key Strengths

- 12 years Uveitis Market Forecast

- The 7MM Coverage

- Uveitis Epidemiology Segmentation

- Key Cross Competition

- Attribute analysis

- Uveitis Drugs Uptake

- Key Uveitis Market Forecast Assumptions

Uveitis Treatment Market Report Assessment

- Current Uveitis Treatment Market Practices

- Uveitis Unmet Needs

- Uveitis Pipeline Drugs Analysis Profiles

- Uveitis Drugs Market Attractiveness

- Qualitative Analysis (SWOT and Conjoint Analysis)

- Uveitis Market Drivers

- Uveitis Market Barriers

Key Questions Answered

Anterior Uveitis Treatment Market Insights

- What was the total Uveitis treatment market size by therapies, and Uveitis drugs market share (%) distribution in 2020, and what would it look like by 2034? What are the contributing factors for this growth?

- How will TRS01 and licaminlimab (OCS-02) affect the treatment paradigm of uveitis?

- How will YUTIQ compete with upcoming products and marketed therapies?

- Which drug is going to be the largest contributor by 2034?

- What are the pricing variations among different geographies for approved and marketed therapies?

- How would future opportunities affect the market dynamics and subsequent analysis of the associated trends?

Uveitis Epidemiology Insights

- What are the disease risks, burdens, and Uveitis unmet needs? What will be the growth opportunities across the 7MM concerning the patient population with uveitis?

- What is the historical and forecasted uveitis patient pool in the United States, EU4 (Germany, France, Italy, and Spain) the United Kingdom, and Japan?

- Out of the above-mentioned countries, which country would have the highest Uveitis diagnosed prevalent population during the forecast period (2023–2034)?

- What factors are factors contributing to the growth of uveitis prevalence cases?

Current Anterior Uveitis Treatment Market Scenario, Marketed Drugs, and Emerging Therapies

- What are the current options for the Uveitis treatment? What are the current guidelines for treating uveitis in the US and Europe?

- How many companies are developing therapies for the Uveitis treatment?

- How many emerging therapies are in the mid-stage and late stage of development for treating uveitis?

- What are the recent novel therapies, targets, Uveitis mechanisms of action, and technologies developed to overcome the limitations of existing therapies?

- What is the cost burden of current treatment on the patient?

- Patient acceptability in terms of preferred treatment options as per real-world scenarios?

- What are the country-specific accessibility issues of approved therapies?

- What is the 7MM historical and forecasted Anterior Uveitis Treatment Market?

Reasons to Buy

- The Anterior Uveitis Treatment Market report will help develop business strategies by understanding the latest trends and changing treatment dynamics driving the uveitis drugs market.

- Insights on patient burden/disease Uveitis Prevalence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing Uveitis drugs market opportunities in varying geographies and the growth potential over the coming years.

- Distribution of historical and current patient share based on real-world prescription data in the US, EU4 (Germany, France, Italy, and Spain) and the United Kingdom, and Japan.

- Identifying strong upcoming players in the Uveitis drugs market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- Highlights of Access and Reimbursement policies for uveitis, barriers to accessibility of approved therapies (HUMIRA, YUTIQ/ILUVIEN, XIPERE, etc.), and patient assistance programs.

- To understand Key Opinion Leaders’ perspectives around the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the Uveitis unmet needs of the existing Anterior Uveitis Treatment Market so that the upcoming players can strengthen their development and launch strategy.

Stay Updated with new articles:-