Brain Cancer Market Summary

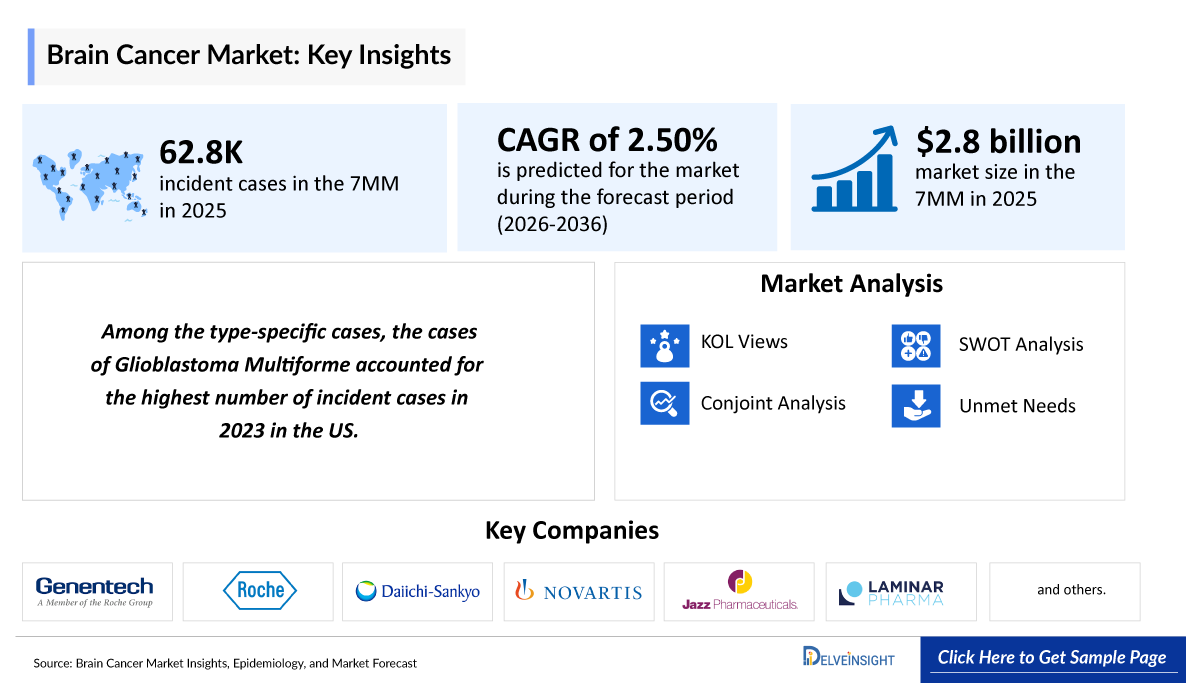

- The Brain Cancer market was valued at approximately USD 2,800 million in 2025 and is projected to grow at a steady CAGR of 2.5% CAGR during 2026–2036.

- According to DelveInsight estimates, in 2025, the United States accounted for the highest brain cancer market size, i.e., approximately USD 1,500 million, although recent analyses suggest potential upside driven by increasing adoption of novel and targeted therapies.

- The leading Brain Cancer companies developing therapies in the treatment market include - Genentech, Roche, Daiichi Sankyo, Novartis, Jazz Pharmaceuticals, Laminar Pharma, Aivita Biomedical, Merck, Arbor Pharmaceuticals, Orbus Therapeutics, VBL Therapeutics, Bayer, Kazia Therapeutics, and others.

Brain Cancer Market & Epidemiology Insights and Trends

- Currently, the treatment regimen of brain cancer mainly includes surgery, radiation therapy, chemotherapy, targeted therapy, and other local treatments not applicable for use in the majority of patients, such as Gliadel Wafer Implant.

- Treatment decisions are guided by multiple factors, including the tumor’s size, type, and grade; whether it is exerting pressure on critical areas of the brain; and if it has spread within the central nervous system or to other parts of the body. Additionally, potential side effects, the patient’s overall health, and their personal treatment preferences are key considerations in determining the most appropriate approach.

- In August 2025, Jazz Pharma announced US Food and Drug Administration (FDA) approval of dordaviprone (MODEYSO) as the first and only treatment for recurrent H3 K27M-mutant diffuse midline glioma.

- In March 2023, the US FDA approved dabrafenib (TAFINLAR) with trametinib (MEKINIST) for pediatric patients 1 year of age and older with low-grade glioma with a BRAF V600E mutation who require systemic therapy.

- Bevacizumab (AVASTIN) was approved for recurrent Glioblastoma Multiforme (GBM) in the US in 2009, based on two Phase II trials demonstrating 6-month progression-free survival (PFS) rates of 29% and 43%. In 2013, AVASTIN completed its confirmatory trial in newly diagnosed GBM patients and did not meet its primary endpoint of overall survival. Based on the results of this trial, Genentech, for AVASTIN, did not receive approval in the European Union for newly diagnosed GBM; however, AVASTIN remains indicated in the United States and Japan for GBM. Also, AVASTIN and carmustine wafers implants have been approved in Japan since 2013.

Brain Cancer Market Size and Forecast in the 7MM

-

2025 Brain Cancer Market Size: ~USD 2,800 million

-

Brain Cancer Growth Rate (2026–2036): 2.5% CAGR

Download the Sample PDF to Get More Insight @ Brain Cancer Market Forecast

Key Factors Driving the Brain Cancer Market

- High Unmet Need in Brain Cancer: Brain tumors, particularly high-grade gliomas (HGGs) such as glioblastoma, are among the most aggressive and difficult-to-treat cancers due to their rapid progression, resistance to conventional therapies, and inability to achieve complete surgical resection. The lack of curative treatment options and poor survival outcomes continue to drive demand for novel and more effective therapies.

- Advancements in Multimodal Treatment Approaches: The current standard of care involves a combination of surgery, radiation therapy, and chemotherapy, tailored based on tumor type, location, and patient characteristics. The concept of “maximum safe resection” followed by adjuvant therapies has improved disease management, while advancements in radiation delivery techniques and chemotherapy regimens have contributed to incremental clinical benefits, supporting market growth.

- Emergence of Targeted and Anti-Angiogenic Therapies: The growing understanding of molecular pathways involved in brain tumors has led to the development of targeted therapies aimed at pathways such as EGFR, PI3K/mTOR, and VEGF. Agents like bevacizumab (AVASTIN) have demonstrated clinical utility, particularly in recurrent settings, and have paved the way for further innovation in precision oncology.

- Expanding Role of Chemotherapy and Novel Delivery Approaches: Chemotherapy remains a cornerstone in brain cancer treatment, especially in cases where surgical resection is not feasible. Alkylating agents such as temozolomide (TEMODAR), carmustine, and lomustine are widely used, with ongoing research focusing on improving delivery methods (e.g., localized wafers, intrathecal delivery) to enhance efficacy and reduce systemic toxicity.

- Emerging Brain Cancer Competitive Landscape: The emerging brain cancer landscape is being shaped by a robust pipeline of innovative therapies, including AV-GBM-1, enzastaurin, durvalumab, and LAM561, spanning immunotherapy, targeted, and metabolic approaches. This diversification reflects a shift toward personalized, mechanism-driven treatments and is intensifying competition across pharma and biotech players. As these candidates advance, they are expected to overcome current limitations such as resistance and poor survival outcomes, ultimately driving market growth and improving patient care.

DelveInsight's ‘Brain Cancer Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of the Brain Cancer, historical and forecasted epidemiology, as well as the Brain Cancer therapeutics market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The Brain Cancer market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates brain cancer patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in brain cancer and maps the competitive and clinical landscape to uncover high‑value opportunities, providing a clear outlook on future market growth potential.

Scope of the Brain Cancer Market Report | |

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

Brain Cancer Market CAGR (Forecast period) |

2.5% (2026 ̶ 2036) |

|

Brain Cancer Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

Brain Cancer Companies |

|

|

Brain Cancer Therapies |

|

|

Brain Cancer Market |

Segmented by

|

|

Analysis |

|

Brain Cancer Disease Understanding

Brain Cancer Overview

A brain tumor, known as an intracranial tumor, central nervous system (CNS) tumors represent a group of diseases that have in common the abnormal development of mass lesions in the brain, spinal cord, or its coverings. A brain tumor can be classified into two main groups, i.e., primary and metastatic. A primary brain tumor is often described as “low grade” or “high grade”. A low-grade tumor generally grows slowly, but it can turn into a high-grade tumor, whereas a high-grade tumor is more likely to grow faster. Secondary brain tumors, also called brain metastases, are much more common than primary tumors in adults. The most common types of primary tumors in adults are meningiomas and astrocytomas, such as glioblastomas. In children, the most common types of brain tumors include medulloblastomas, low-grade astrocytomas (pilocytic), ependymomas, craniopharyngiomas, and brainstem gliomas. Brain tumors in children usually come from different tissues than those affecting adults. Treatments that are fairly well-tolerated by the adult brain (such as radiation therapy) may prevent normal development of a child’s brain, especially in children younger than age five.

Brain Cancer Diagnosis

Brain cancer diagnosis is a multi-step process that combines clinical evaluation, advanced imaging, and molecular testing to accurately identify and characterize tumors. It typically begins with a detailed neurological examination to assess symptoms such as headaches, seizures, cognitive changes, or motor deficits. Imaging techniques, particularly contrast-enhanced MRI (the gold standard) and CT scans, are used to determine the tumor’s size, location, and extent, as well as its impact on surrounding brain structures. Advanced imaging modalities, including functional MRI (fMRI), MR spectroscopy, and PET scans, further help differentiate tumor types and guide surgical planning.

A definitive diagnosis is established through biopsy or surgical resection, allowing for histopathological examination of tumor tissue. In recent years, molecular diagnostics have become integral to classification, with biomarkers such as IDH mutation, MGMT promoter methylation, and 1p/19q co-deletion playing a crucial role in diagnosis, prognosis, and treatment selection. Additionally, emerging techniques like next-generation sequencing (NGS) and liquid biopsy are improving diagnostic precision and enabling more personalized treatment approaches. Overall, advancements in imaging and molecular profiling are significantly enhancing early detection, disease stratification, and clinical decision-making in brain cancer.

Further details are provided in the report....

Brain Cancer Treatment

Brain cancer treatment involves a multimodal approach tailored to tumor type, grade, location, and patient condition. The primary goal is to control tumor growth, relieve symptoms, and preserve neurological function. Standard treatment typically begins with surgery, where neurosurgeons aim for “maximum safe resection” to remove as much of the tumor as possible without damaging critical brain areas. In some low-grade tumors, surgery alone may be sufficient, while high-grade tumors usually require additional therapies. Following surgery, radiation therapy is commonly used to destroy remaining tumor cells and reduce the risk of recurrence. Advanced techniques such as IMRT, stereotactic radiosurgery (SRS), and proton therapy allow precise targeting of tumors while minimizing damage to surrounding healthy tissue.

Chemotherapy is another key component, especially for high-grade tumors. The most widely used drug is temozolomide (TEMODAR), often given alongside radiation and as maintenance therapy. Other agents such as carmustine, lomustine, and combination regimens (e.g., PCV) may also be used depending on the tumor type. Targeted therapy is increasingly used to block specific molecular pathways involved in tumor growth. For example, bevacizumab (AVASTIN) is used in recurrent brain tumors to inhibit angiogenesis and control disease progression.

In addition to conventional treatments, novel therapies are emerging. Tumor treating fields delivered via OPTUNE have shown survival benefits in glioblastoma when combined with chemotherapy. Minimally invasive techniques like laser thermal ablation are also being explored for tumors in difficult-to-reach areas. Supportive care is an essential part of treatment, including corticosteroids to reduce brain swelling and anticonvulsants to manage seizures. Despite these approaches, brain cancer, especially high-grade tumors, remains challenging to treat due to high recurrence rates and resistance to therapy, underscoring the need for continued innovation in targeted and immunotherapeutic strategies.

Further details related to country-based variations are provided in the report...

Brain Cancer Unmet Needs

The section “unmet needs of brain cancer” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Low-overall Survival

- Lack of Effective Treatment

- Lack of Information and Support Services

- Need for Successful Target Inhibition and Drug Delivery Strategies

- Limited Research Regarding Anaplastic Tumors

- Need for Successful Target Inhibition and Drug Delivery Strategies

- Limited Research Regarding Anaplastic Tumors and others…..

Comprehensive unmet needs insights in brain cancer and their strategic implications are provided in the full report....

Brain Cancer Epidemiology

The Brain Cancer epidemiology section provides insights about the historical and current Brain Cancer patient pool and forecasted trends for individual seven major countries. It helps to recognize the causes of current and forecasted trends by exploring numerous studies and views of key opinion leaders. This part of the Brain Cancer market report also provides the diagnosed patient pool and their trends along with assumptions undertaken.

Key Findings from Brain Cancer Epidemiological Analysis and Forecast

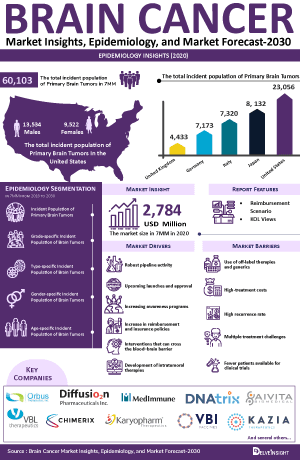

- According to DelveInsight’s estimates, the total incident cases of brain cancer in the 7MM were approximately 62,800 in 2025.

- It has been observed that the incidence of high-grade brain tumors is higher (~70%) than that of low-grade brain tumors (~30%) in the United States.

- It is observed that brain tumors are found to be more common in males (~58%) as compared to females (~42%) in the United States.

- Among EU4 and the UK, Germany accounted for the highest number of glioma cases, followed by France, whereas Spain had the lowest number of cases in 2025.

- In 2025, among brain tumors in other parts of the central nervous system in the United States, glioblastoma was more common in adults than in pediatrics, followed by anaplastic astrocytoma, which was also found to be more prevalent in adults than in pediatrics.

- In the United States, among all the age groups, 40–64 years accounted for the highest number of brain tumor cases, i.e., around 44%, in 2025, followed by the age group ≥65 years (39%).

Brain Cancer Epidemiology Segmentation

- Total Incident Cases of Brain Tumor/Central Nervous System

- Total Incident Cases of Brain Cancer

- Grade-Specific Incident Cases of Brain Cancer

- Type-Specific Incident Cases of Brain Cancer

- Gender-Specific Incident Cases of Brain Cancer

- Age-Specific Incident Cases of Brain Cancer

Recent Developments in the Brain Cancer Treatment Landscape

- In January 2026, Bayer reported ongoing evaluation of regorafenib in glioblastoma through platform trials such as GBM AGILE, highlighting its continued investigation in both newly diagnosed and recurrent settings.

- In November 2025, Northwest Biotherapeutics advanced regulatory engagement for DCVax-L following Phase III data demonstrating improved overall survival in glioblastoma patients, with efforts focused on potential approvals.

- In September 2025, Daiichi Sankyo continued post-marketing and clinical development activities for teserpaturev (DELYTACT), an oncolytic virus approved in Japan for malignant glioma, with additional studies exploring global expansion opportunities.

- In August 2025, Jazz Pharma announced US FDA approval of MODEYSO as the first and only treatment for recurrent H3 K27 M-mutant diffuse midline glioma.

- In March 2023, the US FDA approved TAFINLAR + MEKINIST for pediatric patients 1 year of age and older with BRAF V600E low-grade glioma. The FDA also approved liquid formulations of TAFINLAR and MEKINIST, marking the first time a BRAF/MEK inhibitor has been developed in a formulation suitable for patients as young as 1 year of age. The approval was based on the positive data from the Phase II/III TADPOLE trial.

Brain Cancer Drug Chapters & Competitive Analysis

The brain cancer drug chapter provides a detailed, market-focused review of approved therapies and the emerging pipeline across Phase I–III Brain Cancer clinical trials. It covers the mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, and strategic partnerships for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the brain cancer treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the brain cancer therapeutics market.

Approved Therapies for Brain Cancer

Bevacizumab (AVASTIN): Roche

AVASTIN is a recombinant humanized monoclonal IgG1 antibody that functions as an anti-angiogenic agent by inhibiting vascular endothelial growth factor (VEGF). By binding to VEGF, AVASTIN prevents its interaction with VEGFR-1 and VEGFR-2 receptors on endothelial cells, thereby suppressing tumor angiogenesis and limiting tumor growth. The US FDA approved AVASTIN in 2017 for the treatment of adult patients with recurrent GBM following disease progression after prior therapy. Despite its widespread use in the recurrent setting, AVASTIN has demonstrated limited overall survival benefit, with its clinical utility primarily associated with symptomatic relief and progression-free survival improvement. Following patent expiration, the bevacizumab market has experienced increased competition with the entry of multiple biosimilars. Approved biosimilars include MVASI (Amgen), ZIRABEV (Pfizer), and ALYMSYS (Amneal Pharmaceuticals), which have enhanced treatment accessibility and introduced pricing pressures in the market. The first biosimilar, MVASI, received FDA approval in 2017, marking a significant shift toward cost-effective anti-VEGF therapies. In recent years, AVASTIN has continued to be evaluated in combination with immunotherapies, targeted agents, and novel treatment modalities to improve outcomes in glioma. However, its role remains largely confined to recurrent disease management, with ongoing research focused on optimizing combination strategies and identifying responsive patient subgroups.

Dordaviprone (MODEYSO): Jazz Pharmaceuticals

MODEYSO is the first and only treatment option approved by the FDA for this ultra-rare and aggressive brain tumor that affects an estimated 2,000 people in the US each year, many of whom are children and young adults. The disease is characterized by rapid progression and historically has had no effective systemic treatment options. To address this urgent unmet patient need, MODEYSO is expected to be commercially available in the coming weeks.

In August 2025, Jazz Pharmaceuticals announced that the US FDA had granted accelerated approval for MODEYSO for the treatment of adult and pediatric patients 1 year of age and older with diffuse midline glioma harboring an H3 K27M mutation with progressive disease following prior therapy.1 Continued approval for this indication may be contingent upon verification and description of clinical benefit in the Phase 3 ACTION confirmatory trial.

Brain Cancer Marketed/Approved Therapies | ||||||

|

Drug/Therapy |

Company |

Indication |

Molecule Type |

RoA |

MoA |

Marketed Region |

|

Temozolomide (TEMODAR) |

Merck |

Glioblastoma |

Alkylating Agent |

Oral; Injection |

Alkylation (methylation) mainly at the O6 and N7 positions of guanine |

US: 2005 EU: 1999 JP: 2006 |

|

Delytact |

Daiichi Sankyo |

Malignant Glioma |

Genetically engineered oncolytic herpes simplex virus type 1 |

Intratumoral |

Selective replication in cancer cells and enhanced induction of antitumor immune response |

JP: 2021 |

|

TAFINLAR (dabrafenib) + MEKINIST (trametinib) |

Novartis |

Low-grade and high-grade glioma (BRAF mutation) |

Small Molecule |

Oral |

Inhibits MAPK pathway and inhibits the cell growth of various BRAFV600E-positive tumors |

US: 2022 |

Note: Detailed marketed therapies assessment will be provided in the final report....

Brain Cancer Pipeline Analysis

Regorafenib: Bayer

Regorafenib is an oral multi-kinase inhibitor that potently blocks multiple protein kinases involved in tumor angiogenesis (VEGFR1, -2, -3, TIE2), oncogenesis (KIT, RET, RAF-1, BRAF), metastasis (VEGFR3, PDGFR, FGFR), and tumor immunity (CSF1R). It is an inhibitor of multiple membrane-bound and intracellular kinases involved in normal cellular functions and pathologic processes such as oncogenesis, tumor angiogenesis, and maintenance of the tumor microenvironment.

In May 2022, a new strategy, world premiere, was developed by the Veneto Oncology Institute, which officially inaugurates the Phase I experimental study called “Regoma 2”, the so-called “first-line” therapy; that is, it acts on the time factor and in a "synergistic" way. Phase I study to evaluate the tolerability of the Regorafenib and temozolomide combination with or without radiotherapy in patients with a new diagnosis of Glioblastoma. A Phase I REGOMA-2 study (2025) is actively evaluating regorafenib in combination with temozolomide and radiotherapy in newly diagnosed GBM, showing acceptable safety and tolerability.

LAM561 (2-OHOA): Laminar Pharmaceuticals

LAM561 (2-OHOA: 2-hydroxyoleic acid) is the first-in-class anticancer drug acting through cell membrane lipid modification. In October 2022, LAM561 received FTD from the FDA for the treatment of glioblastoma. Earlier, in October 2011, the EMA granted ODD to 2-OHOA for treating glioma.

As per the pipeline, the company anticipates the launch of LAM561 for adult glioma patients in 2026 and for pediatric glioma patients in 2027. In November 2024, the CLINGIO trial database was locked after reaching 66 PFS events, prompting the interim analysis of the Clinical Study Report (CSR), which provided the first open-label, unblinded readout of the trial. The study will continue until 90 overall survival events are reached, at which point the final analysis is expected to be conducted, with an estimated completion date in Q4 2026

Comparison of Brain Cancer Emerging Drugs Under Development | |||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Molecule Type |

Anticipated Launch in the US |

|

AV-GBM-1 |

Aivita Bio-medical |

III |

Newly-diagnosed Glioblastoma |

SC |

Pan-antigenic, targeting multiple antigens, including all neoantigens, from autologous tumor-initiating cells that are responsible for the tumor growth. |

Dendritic Cell |

2027 |

|

Enzastaurin |

Denovo Pharma |

II |

Newly diagnosed GBM |

Oral |

Inhibits protein kinase C beta activity |

Small Molecule |

Information is available in the full report |

|

Paxalisib (GDC-0084) |

Kazia Therapeutics |

II/III |

Newly-diagnosed Glioblastoma Multiforme, Newly Diagnosed Diffuse Intrinsic Pontine Glioma or Diffuse Midline Gliomas and Progressive or Recurrent High-Grade Glioma |

Oral |

PI3K pathway inhibitor |

Small molecule |

Information is available in the full report |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | |||||||

Note: A detailed emerging therapies assessment will be provided in the final report...

Brain Cancer Key Players, Market Leaders, and Emerging Companies

- Genentech

- Roche

- Daiichi Sankyo

- Novartis

- Jazz Pharmaceuticals

- Laminar Pharma

- Aivita Biomedical

- Merck

- Arbor Pharmaceuticals

- Orbus Therapeutics

- VBL Therapeutics

- Bayer

- Kazia Therapeutics, and others

Brain Cancer Market Outlook

Brain tumors are classified into low-grade (Grade I–II) and high-grade (Grade III–IV) tumors, with high-grade tumors demonstrating rapid progression, aggressive behavior, and poor prognosis. From a market perspective, high-grade brain tumors, particularly glioblastoma, account for the majority of the clinical and commercial burden due to their limited treatment options and high unmet need.

The brain cancer market is primarily driven by the complexity of treatment and the lack of curative therapies. Tumors are often difficult to completely resect due to their location in critical brain regions and their infiltrative nature, while the blood–brain barrier further limits the effectiveness of systemic therapies. As a result, current treatment approaches rely on a multimodal strategy involving surgery, radiation therapy, and chemotherapy, often administered sequentially or in combination.

Surgery remains the first-line intervention, followed by radiation and chemotherapy, with TEMODAR being a key backbone therapy. Other cytotoxic agents such as carmustine, lomustine, and combination regimens continue to be used, although their efficacy is limited and often associated with toxicity. In addition, targeted therapies such as AVASTIN have been introduced, particularly in recurrent settings, providing incremental clinical benefits and expanding treatment options.

The majority of chemotherapeutic drugs are cytotoxic drugs. Cytotoxic drugs are designed to destroy tumor cells. They work by making tumor cells unable to reproduce themselves. Carmustine (BCNU), Lomustine (CCNU), or Gleostine (Generic), Gliadel wafer (biodegradable discs infused with BCNU), Temozolomide (Temodar), Cisplatin, Carboplatin, Etoposide, and Irinotecan are examples of cytotoxic drugs. They may be given as a single agent or in combination, i.e., PCV (Procarbazine, CCNU, and Vincristine), Carboplatin/ Etoposide. Only BCNU/CCNU, Gliadel wafer, and Temodar have been approved by the FDA for the treatment of high-grade brain tumors. Carmustine is the generic name for the trade name drug BiCNU. It is a cell-cycle phase nonspecific alkylating antineoplastic agent, which is used in the treatment of brain tumors and various other malignant neoplasms. It is a nitrogen mustard β-chloro-nitrosourea compound used as an alkylating agent.

Despite these available therapies, treatment remains largely palliative, with high recurrence rates and poor long-term survival outcomes, especially in high-grade tumors. This has led to sustained investment in research and development, focusing on novel therapeutic approaches targeting molecular pathways such as EGFR, PI3K/mTOR, and VEGF.

Looking ahead, the brain cancer market is expected to evolve with advancements in targeted therapies, improved drug delivery strategies to overcome the blood–brain barrier, and increasing adoption of combination treatment approaches. However, challenges such as therapeutic resistance, tumor heterogeneity, and high clinical trial failure rates continue to limit rapid progress. Overall, the market is anticipated to witness gradual growth, driven by innovation and the persistent need for more effective and durable treatment options.

- The total market size of brain cancer in the 7MM is approximately USD 2,800 million in 2025 and is projected to grow during the forecast period (2026–2036).

- According to the estimates, the United States recorded the highest market share, i.e., around 65% of the total market size of brain cancer, in 2025.

- Among the EU4 and the UK, Germany has the maximum revenue share in 2025, while Spain has the lowest market share.

- Conditional and time-limited approval of Daiichi’s DELYTACT, an intratumoral oncolytic virus therapy, has opened new doors for other players, such as DNAtrix and Istari Oncology, to develop oncolytic virus therapies, which can prove to be a potential mechanism of action in brain cancer treatment in the future.

Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in Brain Cancer (2022–2036 Forecast)

The existing brain cancer treatment landscape is primarily dominated by therapeutic classes such as alkylating agents, vascular endothelial growth factor (VEGF) inhibitors, targeted therapies, and emerging immunotherapy approaches. Among anti-angiogenic agents, AVASTIN plays a key role by inhibiting VEGF, a signaling protein that promotes tumor angiogenesis. By blocking VEGF, bevacizumab restricts the formation of new blood vessels that supply oxygen and nutrients to tumors, thereby slowing tumor growth. Unlike conventional chemotherapy, its mechanism focuses on starving the tumor rather than directly killing cancer cells.

Moving to alkylating agents, temozolomide (TEMODAR) remains the backbone of brain cancer treatment. It acts by methylating DNA, leading to DNA damage and inhibition of tumor cell replication. Its ability to cross the blood–brain barrier and its established efficacy in combination with radiation therapy have led to widespread adoption and strong guideline recommendations in high-grade brain tumors. Other cytotoxic agents such as carmustine and lomustine also contribute to this class, often used in specific clinical settings or combination regimens.

Targeted therapies are gaining traction, focusing on molecular pathways involved in tumor growth and survival. MAPK pathway inhibitors such as dabrafenib (TAFINLAR) and trametinib (MEKINIST) target BRAF V600E-mutant tumors by inhibiting key proteins in the MAPK signaling cascade, thereby suppressing tumor cell proliferation. Additionally, therapies targeting pathways such as EGFR, PI3K/mTOR, and NTRK fusions are expanding the scope of precision medicine in brain cancer.

Looking ahead, the brain cancer treatment landscape is expected to evolve significantly with the emergence of novel therapeutic classes, including cancer vaccines, dendritic cell-based immunotherapies, oncolytic viruses, and gene therapies. These innovative approaches aim to overcome limitations of current treatments, such as tumor heterogeneity, resistance, and restricted drug delivery due to the blood–brain barrier. Over the 2026–2036 forecast period, these emerging modalities are anticipated to diversify the market, improve patient outcomes, and gradually shift treatment paradigms toward more personalized and targeted approaches.

Further details will be provided in the report….

Brain Cancer Drug Uptake

This section focuses on the uptake rate of potential Brain Cancer drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the brain cancer market's uptake by drugs, patient uptake by therapy, and sales of each drug.

The uptake of therapies in brain cancer is expected to differ across conventional chemotherapies, targeted agents, device-based therapies, and emerging immunotherapies. Established treatments such as temozolomide (TEMODAR) continue to dominate frontline management due to their proven survival benefit and compatibility with radiation therapy, while bevacizumab (AVASTIN) remains widely used in recurrent settings for disease control and symptom relief. Device-based therapy such as OPTUNE is gaining increasing adoption in newly diagnosed glioblastoma. In addition, cytotoxic agents such as carmustine and lomustine continue to be utilized in specific settings, while targeted therapies including dabrafenib and trametinib, along with emerging IDH inhibitors such as vorasidenib and newer agents like dordaviprone, are witnessing gradual uptake in biomarker-defined patient populations, reflecting the shift toward precision medicine.

On the other hand, emerging therapies including cancer vaccines such as DCVax-L, SurVaxM, and AV-GBM-1; oncolytic viruses such as DNX-2401 and teserpaturev; and novel targeted agents like ONC201, regorafenib, and enzastaurin (DB-102)—are expected to witness gradual but progressive uptake over the forecast period. Additional modalities such as gene therapy candidates (e.g., ofranergene obadenovec/VB-111), immunotherapies like durvalumab, and other vaccine-based approaches (e.g., IGV-001, ITI-1000) are also under investigation. Their adoption will depend on clinical trial success, regulatory approvals, and biomarker-driven patient selection. As long-term efficacy and safety data mature and combination strategies are optimized, these next-generation therapies are anticipated to gain traction, particularly in recurrent and treatment-resistant brain cancer populations, thereby reshaping the treatment landscape.

Further detailed analysis of emerging therapies' drug uptake in the report…

Brain Cancer Market Access and Reimbursement Scenario

-

The United States

The US Reimbursement for Brain Cancer Therapies | |

|

Drug |

Access Program |

|

Bevacizumab (AVASTIN) |

|

|

Temozolomide (TEMODAR) |

|

Reimbursement is a crucial factor that affects the drug’s access to the market. Often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

Further details are provided in the final report….

Brain Cancer Therapies Price Scenario & Trends

Pricing and analogue assessment of brain cancer therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, the closest and most appropriate analogue selection for emerging therapies, and the understanding of how pricing influences market access, adherence, and long-term uptake.

-

Pricing of Brain Cancer-Approved Drugs

The wholesale acquisition cost (WAC) of temozolomide (TEMODAR) oral capsules varies by strength; for example, a 100 mg capsule costs approximately USD 150–200 per unit, resulting in an estimated annual cost of USD 6,000–12,000 depending on dosing regimen and treatment duration.

Further details are provided in the final report….

Industry Experts and Physician Views for Brain Cancer

To keep up with brain cancer market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry experts were contacted for insights on the brain cancer emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in brain cancer, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 10+ KOLs to gather insights; however, interviews were conducted with 6+ KOLs in the 7MM. Centers such as the Miami Cancer Institute, Division of Hematology & Oncology, and the Anderson Cancer Center, etc. were contacted. Their opinion helps understand and validate current and emerging brain cancer therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in brain cancer.

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“Despite advances in radiation, chemotherapy, and surgery, outcomes for patients with glioblastoma remain poor, with average survival ranging from 15 to 18 months.” |

|

“Based on the efficacy and safety profile of tovorafenib observed to date from the FIREFLY-1 trial population, we plan to submit a new drug application in the first half of [2023] that will include additional follow-up from the full study population.” |

Brain Cancer Report Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of Brain cancer, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are mainly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Brain Cancer Market Report

- The report covers a segment of key events, an executive summary, a descriptive overview of brain cancer, explaining its causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the brain cancer market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM brain cancer market.

Brain Cancer Market Report Insights

- Brain Cancer Patient Population Forecast

- Brain Cancer Therapeutics Market Size

- Brain Cancer Pipeline Analysis

- Brain Cancer Market Size and Trends

- Brain Cancer Market Opportunity (Current and forecasted)

Brain Cancer Market Report Key Strengths

- Brain Cancer Epidemiology‑based (Epi‑based) Bottom‑up Forecasting

- Artificial Intelligence (AI)-enabled Market Research Report

- 11-year forecast

- Brain Cancer Market Outlook (North America, Europe, Asia-Pacific)

- Patient Burden Trends (by geography)

- Brain Cancer Treatment Addressable Market (TAM)

- Brain Cancer Competitive Landscape

- Brain Cancer Major Companies Insights

- Brain Cancer Price Trends and Analogue Assessment

- Brain Cancer Therapies Drug Adoption/Uptake

- Brain Cancer Therapies Peak Patient Share Analysis

Brain Cancer Market Report Assessment

- Brain Cancer Current Treatment Practices

- Brain Cancer Unmet Needs

- Brain Cancer Clinical Development Analysis

- Brain Cancer Emerging Drugs Product Profiles

- Brain Cancer Market Attractiveness

- Brain Cancer Qualitative Analysis (SWOT and Conjoint Analysis)

- Brain Cancer Market Drivers

- Brain Cancer Market Barriers

FAQs Related to Brain Cancer Market Report:

Brain Cancer Market Insights

- What was the brain cancer market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of brain cancer?

- What are the disease risks, burdens, and unmet needs of brain cancer? What will be the growth opportunities across the 7MM concerning the patient population with brain cancer?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of brain cancer? What are the current guidelines for treating brain cancer in the US, Europe, and Japan?

Reasons to Buy Brain Cancer Market Forecast Report

- The report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the brain cancer market.

- Bottom-up forecasting builds from the affected population to product forecasts, delivering a robust, data-driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential current and emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights into the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI)-enabled report summarize and simplify complex datasets within the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data-driven decisions.

Stay Updated with us for Recent Articles

- Alpheus Medical Treats First High-Grade Glioma Brain Cancer Patient with its Proprietary Platform; Karidum’s Next Generation Globe® Pulsed Field System

- VistaGen’s PH94B for Anxiety Disorder; Keytruda for Head and Neck Cancer Treatment; Bavarian Nordic’s Smallpox Vaccine Imvanex; CAMP4 Raises USD 100 Million; Incyte's WU-CART-007; Incyte’s Opzelura for Vitiligo; AstraZeneca and Merck’s Lynparza; Sumitomo Pharma’s DSP-0390 for Brain Cancer

- The novel therapy for brain cancer treatments

- Identity Crises Faced by a Venerable Brain-Cancer Cell Line

- Latest DelveInsight Blogs