Cell and Gene Therapy CDMO Market Summary

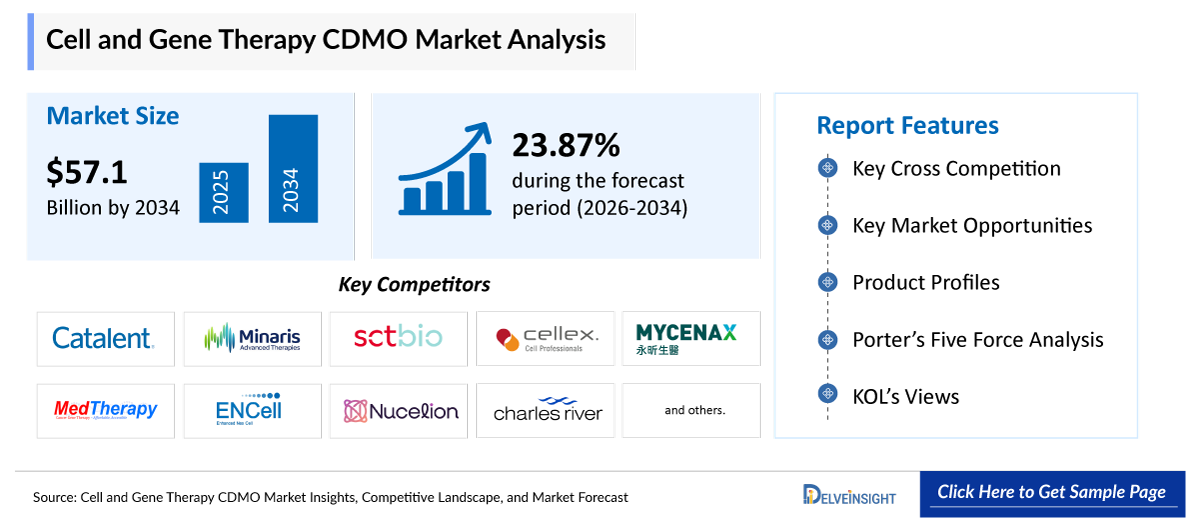

- The global cell and gene therapy CDMO market size is expected to increase from USD 8,395.79 million in 2025 to USD 57,125.77 million by 2034, reflecting strong and sustained growth.

- The global cell and gene therapy CDMO market is growing at a CAGR of 23.87% during the forecast period from 2026 to 2034.

- The cell and gene therapy CDMO market is being strongly driven by the rapid growth of cell and gene therapy pipelines, increasing demand for personalized medicine, and rising investments in the sector. Biotech and pharmaceutical companies are actively developing advanced therapies such as CAR-T, stem cell, and gene editing treatments for cancer and rare diseases, creating significant demand for outsourced manufacturing and development services. Additionally, the growing focus on personalized therapies requires specialized production, quality control, and logistics capabilities, which CDMOs are well-equipped to provide. Increasing funding from venture capital firms, pharmaceutical companies, and government organizations is further accelerating research and commercialization activities, leading many emerging biotech firms to rely on CDMOs for cost-effective and scalable manufacturing support.

- The leading companies operating in the cell and gene therapy CDMO market include Catalent, Inc., Minaris Advanced Therapies, SCTbio, a.s., Cellex Cell Professionals GmbH, Mycenax Biotech Inc., MedTherapy Biotech, ENCELL Co., Ltd., Nucelion Biotechnologies, Charles River Laboratories International, Inc., Lonza Group AG, Thermo Fisher Scientific Inc., WuXi AppTec Co., Ltd., and others.

- North America is expected to dominate the Cell and Gene Therapy CDMO market due to the strong presence of leading biotechnology and pharmaceutical companies, increasing investments in cell and gene therapy research, advanced healthcare infrastructure, and high adoption of innovative therapies. The region also benefits from favorable regulatory support, a growing number of clinical trials, and the presence of major CDMOs and viral vector manufacturing facilities, particularly in the United States.

- In the product type segment of the cell and gene therapy CDMO market, the cell therapy category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Cell and Gene Therapy CDMO Market Insights

Cell and Gene Therapy CDMO Market Size and Forecasts:

|

Report Metrics |

Details |

|

2025 Market Size |

USD 8,395.79 million |

|

2034 Projected Market Size |

USD 57,125.77 million |

|

Growth Rate (2026-2034) |

23.87% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Cell and Gene Therapy CDMO Market

- Rapid growth of cell & gene therapy pipeline leading to a surge in cell and gene therapy CDMO: The growing number of cell and gene therapies under development is significantly boosting the cell and gene therapy CDMO market. Biotech and pharmaceutical companies are increasingly developing therapies such as CAR-T, stem cell therapies, and gene editing treatments for cancer and rare diseases. Since many companies lack large-scale manufacturing capabilities and technical expertise, they rely on CDMOs for process development, clinical manufacturing, and commercialization support, thereby increasing demand for outsourced services.

- Increasing Demand for Personalized Medicine: The rising focus on personalized medicine is driving demand for cell and gene therapy CDMOs because many advanced therapies are customized for individual patients. Treatments such as autologous CAR-T therapy require specialized manufacturing, strict quality control, and complex logistics. CDMOs provide the advanced infrastructure and expertise needed for these personalized therapies, helping companies deliver patient-specific treatments efficiently and accelerating overall market growth.

- Increasing investment & funding in cell and gene therapy: Growing investments from venture capital firms, pharmaceutical companies, and government organizations are accelerating research and commercialization of cell and gene therapies. Many emerging biotech startups receiving funding do not have in-house manufacturing facilities, leading them to outsource development and production activities to CDMOs. This rising flow of funding and strategic partnerships is expanding manufacturing demand and supporting the rapid growth of the Cell and Gene Therapy CDMO market.

Cell and Gene Therapy CDMO Market Report Segmentation

This cell and gene therapy CDMO market report offers a comprehensive overview of the global cell and gene therapy CDMO market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product Type (Cell Therapy, Gene Therapy, and Gene-Modified Cell Therapy), Service Type (Process Development Services, Manufacturing Services, and Others), Development Phase (Pre-clinical Phase, Clinical Phase, and Commercial Manufacturing), Indication (Oncology, Rare Diseases, and Others), End-Users (Biopharmaceutical Companies, Biotechnology Startups, and Academic & Research Institutes), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing cell and gene therapy CDMO market.

A Cell and Gene Therapy CDMO (Contract Development and Manufacturing Organization) is a specialized company that provides outsourced services for the development, manufacturing, testing, and commercialization of cell and gene therapies. These organizations help biotechnology and pharmaceutical companies produce advanced therapies such as CAR-T cells, stem cell therapies, and gene therapies by offering expertise, GMP manufacturing facilities, regulatory support, and scalable production capabilities.

The Cell and Gene Therapy CDMO market is experiencing significant growth due to the rapid expansion of cell and gene therapy pipelines, increasing demand for personalized medicine, and rising investments across the biotechnology and pharmaceutical industries. Companies worldwide are actively developing advanced therapies such as CAR-T cell therapies, stem cell therapies, gene editing technologies, and viral vector-based treatments for cancer, rare genetic disorders, and autoimmune diseases. As the number of clinical trials and therapy approvals continues to rise, the demand for specialized outsourced manufacturing and development services is also increasing.

In addition, the growing focus on personalized medicine is creating strong demand for highly specialized manufacturing processes, as many therapies are tailored to individual patients and require strict quality control, cold-chain logistics, and advanced production infrastructure. Most small and mid-sized biotech companies lack the financial resources, technical expertise, and GMP-compliant facilities needed for large-scale manufacturing, making CDMOs critical partners in therapy development and commercialization. Furthermore, increasing investments from venture capital firms, pharmaceutical companies, and government organizations are accelerating innovation and clinical research activities in the cell and gene therapy sector. This rising funding environment is encouraging emerging biotech firms to outsource process development, analytical testing, and commercial manufacturing to CDMOs, thereby driving overall market growth.

Get More Insights into the Report @ Cell and Gene Therapy CDMO Market Trends

What are the latest cell and gene therapy CDMO market dynamics and trends?

The cell and gene therapy CDMO market is being strongly driven by the rapid growth of cell and gene therapy pipelines, increasing demand for personalized medicine, and rising investments in the sector.

The rapid growth of the cell and gene therapy pipeline is one of the major factors driving the expansion of the Cell and Gene Therapy CDMO market. Over the past few years, there has been a significant increase in the number of therapies being developed for cancer, rare genetic disorders, autoimmune diseases, and neurological conditions. Biopharmaceutical and biotechnology companies are increasingly investing in advanced treatment approaches such as CAR-T cell therapies, stem cell therapies, gene editing technologies like CRISPR, and viral vector-based gene therapies. As more therapies move from preclinical research into clinical trials and commercialization stages, the demand for specialized manufacturing, process development, analytical testing, and regulatory support continues to rise. For instance, in March 2026, Lonza expanded its commercial manufacturing agreement with Genetix Biotherapeutics for the production of the gene therapy ZYNTEGLO™, reflecting increasing commercial demand for gene therapy manufacturing services.

Additionally, most therapy developers, especially small and mid-sized biotech companies, do not possess the advanced infrastructure, GMP-certified facilities, skilled workforce, or technical expertise required to manufacture complex cell and gene therapies at scale. Manufacturing these therapies involves highly specialized procedures such as viral vector production, cell isolation, genetic modification, cryopreservation, and sterile fill-finish operations, which are expensive and technically challenging to establish internally. As a result, companies increasingly partner with CDMOs to accelerate development timelines, reduce operational costs, and ensure compliance with stringent regulatory standards. Supporting this trend, in September 2025, Thermo Fisher Scientific partnered with South Korean CDMO Dr. Park to equip a new viral vector manufacturing facility for large-scale gene therapy production, highlighting the growing investment in manufacturing infrastructure.

Furthermore, the increasing number of clinical trials worldwide has created a strong demand for flexible and scalable manufacturing capacity. CDMOs help therapy developers manage fluctuating production needs from early-stage clinical batches to commercial-scale manufacturing. The rapid expansion of the therapy pipeline has also encouraged CDMOs to invest in advanced technologies, automated manufacturing systems, and expanded production facilities. For example, in October 2025, Lonza launched new TheraPEAK® AmpliCell® Cytokines and 293-GT® Medium systems designed to improve scalability and consistency in cell and gene therapy manufacturing workflows. Consequently, the growing pipeline of cell and gene therapies is directly increasing outsourcing activities and fueling long-term growth in the Cell and Gene Therapy CDMO market. Thus, the factors mentioned above are expected to boost the overall market of cell and gene therapy CDMO during the forecast period.

However, high manufacturing complexity and stringent regulatory requirements are collectively acting as major limiting factors for the Cell and Gene Therapy CDMO market. Manufacturing cell and gene therapies involves highly specialized processes such as viral vector production, cell engineering, cryopreservation, and sterile fill-finish operations, which require advanced infrastructure, skilled professionals, and strict quality control measures. At the same time, regulatory agencies such as the FDA and EMA impose rigorous guidelines related to product safety, efficacy, traceability, and GMP compliance. Meeting these complex manufacturing and regulatory standards increases operational costs, extends development timelines, and raises the risk of production delays or batch failures, thereby restricting the growth and scalability of the Cell and Gene Therapy CDMO market.

Cell and Gene Therapy CDMO Market Segment Analysis

Cell and Gene Therapy CDMO Market by Product Type (Cell Therapy, Gene Therapy, and Gene-Modified Cell Therapy), Service Type (Process Development Services, Manufacturing Services, and Others), Development Phase (Pre-clinical Phase, Clinical Phase, and Commercial Manufacturing), Indication (Oncology, Rare Diseases, and Others), End-Users (Biopharmaceutical Companies, Biotechnology Startups, and Academic & Research Institutes), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product Type: Cell Therapy is expected to dominate the market with the largest revenue share.

In the product type segment of the cell and gene therapy CDMO market, the cell therapy category is contributing to 48% of total market revenue in 2025, due to the increasing development and commercialization of advanced therapies such as CAR-T cell therapies, stem cell therapies, T-cell therapies, and regenerative medicine products. The rising prevalence of cancer, autoimmune diseases, and rare genetic disorders has accelerated demand for innovative cell-based treatments, leading biotechnology and pharmaceutical companies to expand their clinical pipelines. Since cell therapies require highly specialized manufacturing processes involving cell isolation, expansion, genetic modification, cryopreservation, and sterile handling, many therapy developers rely on CDMOs for technical expertise and GMP-compliant production facilities. Additionally, the growing number of clinical trials, regulatory approvals, and investments in personalized medicine is increasing outsourcing activities for cell therapy manufacturing. CDMOs are also expanding their production capacities and adopting automated and closed-system technologies to support scalable and efficient manufacturing, further driving the growth of the overall Cell and gene therapy CDMO market.

Additionally, the increasing product development activities are further escalating the overall market of the category in the cell and gene therapy CDMO market. For instance, in April 2026, Catalent, Inc. expanded its commercial licensing agreement with Cartherics to support the manufacturing and commercialization of iPSC-derived CAR-NK cell therapies for cancer treatment, strengthening its position in advanced cell therapy manufacturing. As a result, the cell therapy segment not only supports the adoption of cell and gene therapy CDMOs but also acts as a key revenue generator, thereby significantly boosting the overall growth of the cell and gene therapy CDMO market.

By Service Type: The manufacturing services category dominates the market.

Within the service type segment of the cell and gene therapy CDMO market, the manufacturing services category is anticipated to dominate, accounting for around 46% of the market share in 2025, due to the increasing complexity and large-scale production requirements of advanced cell and gene therapies. Manufacturing cell and gene therapies involves highly specialized processes such as viral vector production, cell isolation, genetic modification, cell expansion, purification, cryopreservation, and sterile fill-finish operations, all of which require advanced GMP-compliant infrastructure and technical expertise. Most biotechnology and pharmaceutical companies, particularly small and mid-sized firms, lack the in-house capabilities and financial resources needed to establish and operate such sophisticated manufacturing facilities. As a result, they increasingly rely on CDMOs for clinical and commercial-scale manufacturing support.

Additionally, the rapid growth in the number of clinical trials and approved therapies, especially CAR-T therapies, stem cell therapies, and gene editing treatments, has significantly increased demand for scalable and flexible manufacturing capacity. CDMOs offer integrated manufacturing solutions that help therapy developers reduce operational costs, accelerate production timelines, maintain regulatory compliance, and ensure consistent product quality. The growing adoption of automated manufacturing systems, closed processing technologies, and advanced bioprocessing platforms by CDMOs is further improving manufacturing efficiency and scalability. Consequently, rising outsourcing activities, increasing commercial production demand, and continuous investments in manufacturing infrastructure are collectively driving the dominance of the manufacturing services segment in the Cell and Gene Therapy CDMO market.

By Development Phase: The pre-clinical phase category dominates the market.

Within the development phase segment of the cell and gene therapy CDMO market, the pre-clinical phase category is anticipated to dominate, accounting for around 63% of the market share in 2025, due to the rapidly increasing number of early-stage cell and gene therapy candidates entering research and development pipelines. Biotechnology and pharmaceutical companies are heavily investing in innovative therapies such as CAR-T cell therapies, stem cell therapies, CRISPR-based gene editing technologies, and viral vector-based gene therapies for cancer, rare genetic disorders, neurological diseases, and autoimmune conditions. Since most therapies are still in the early stages of development, companies require extensive support for process development, analytical testing, vector development, cell line optimization, formulation development, and small-scale GMP manufacturing before advancing into human clinical trials. As a result, demand for pre-clinical outsourcing services offered by CDMOs is growing significantly.

Additionally, many emerging biotech startups and research organizations lack the infrastructure, technical expertise, and regulatory experience required to perform complex pre-clinical manufacturing activities internally. CDMOs provide specialized capabilities, advanced technologies, and scalable development platforms that help therapy developers accelerate research timelines, reduce operational costs, and improve regulatory readiness before entering clinical phases. The increasing number of investigational new drug (IND) applications and preclinical collaborations is further strengthening this segment.

Several recent company-specific developments highlight this trend. In February 2026, Catalent, Inc., announced a partnership with S.Biomedics to develop and manufacture TED-A9, an allogeneic stem cell therapy for Parkinson’s disease, further expanding pre-clinical and clinical cell therapy manufacturing activities. Thus, the factors mentioned above are expected to boost the market segment, thereby escalating the overall market of cell and gene therapy CDMO.

By Indication: Oncology category dominates the market

Within the indication segment of the cell and gene therapy CDMO market, the oncology category is anticipated to dominate, accounting for around 55% of the market share in 2025, due to the rising prevalence of cancer and the increasing development of advanced therapies such as CAR-T cell therapies, TCR-T therapies, and gene-edited immunotherapies for cancer treatment. The growing number of oncology-focused clinical trials and regulatory approvals has significantly increased demand for specialized manufacturing, viral vector production, and cell engineering services. Since these therapies require complex and highly regulated manufacturing processes, biotechnology and pharmaceutical companies increasingly rely on CDMOs for scalable production, process development, and regulatory support, thereby driving the growth of the oncology segment in the cell and gene therapy CDMO market.

By End-Users: The biopharmaceutical companies category dominates the market

In the end-users segment of the cell and gene therapy CDMO market, the biopharmaceutical companies category dominates the overall market due to the increasing investment in advanced cell and gene therapy research and commercialization. Biopharmaceutical companies are actively developing therapies such as CAR-T, stem cell, and gene editing treatments for cancer and rare diseases, creating strong demand for outsourced manufacturing and development services. Since these therapies require specialized GMP facilities, advanced technologies, and regulatory expertise, many biopharmaceutical companies rely on CDMOs for process development, clinical manufacturing, analytical testing, and commercial-scale production, thereby driving the growth of this segment.

Cell and Gene Therapy CDMO Market Regional Analysis

North America Cell and Gene Therapy CDMO Market Trends

North America is expected to account for the highest proportion of 40% of the cell and gene therapy CDMO market in 2025, out of all regions. The cell and gene therapy CDMO market in North America is being strongly driven by the rapid growth of cell and gene therapy pipelines, increasing demand for personalized medicine, and rising investments and funding in advanced therapeutics. The region has become a major hub for the development of CAR-T therapies, stem cell therapies, gene editing technologies, and viral vector-based treatments due to the strong presence of biotechnology companies, advanced healthcare infrastructure, and supportive regulatory pathways. The growing number of therapies targeting cancer, rare genetic disorders, autoimmune diseases, and neurological conditions has significantly increased the need for outsourced process development, analytical testing, clinical manufacturing, and commercial-scale production services. Supporting this trend, in March 2026, Catalent partnered with GelMEDIX for the development and clinical manufacturing of iPSC-derived therapies for ocular and retinal diseases, strengthening early-stage cell therapy manufacturing capabilities in North America.

Additionally, the increasing demand for personalized medicine is also accelerating market growth, as therapies such as autologous CAR-T and gene-edited cell therapies require highly specialized manufacturing processes, advanced cold-chain logistics, and GMP-compliant facilities. Since many therapy developers lack the infrastructure and expertise required for these complex operations, outsourcing to CDMOs has increased significantly. Reflecting this trend, in September 2025, Made Scientific and Syenex announced a technology partnership to improve scalability and efficiency in engineered T-cell therapy manufacturing using advanced gene delivery systems, aiming to reduce production timelines and manufacturing costs.

Furthermore, increasing investments and funding activities are accelerating manufacturing expansion across North America. Venture capital firms, pharmaceutical companies, and biotechnology investors are heavily supporting advanced therapy developers, many of which rely on CDMOs for scalable manufacturing support. In August 2025, US WorldMeds completed the acquisition of Adaptimmune’s cell therapy portfolio, including TECELRA® and other T-cell therapy assets, to strengthen commercialization and manufacturing activities in the oncology cell therapy space. In addition, several CDMOs are expanding manufacturing technologies and infrastructure to support rising therapy demand. For example, in September 2025, Dr. Park CDMO selected Thermo Fisher Scientific technologies to equip its new viral vector manufacturing facility capable of supporting large-scale AAV vector production for global cell and gene therapy programs.

Collectively, the expanding therapy pipeline, increasing adoption of personalized medicine, and growing investments in advanced manufacturing technologies are significantly driving the growth of the Cell and Gene Therapy CDMO market in North America.

Europe Cell and Gene Therapy CDMO Market Trends

The Cell and Gene Therapy CDMO market in Europe is witnessing strong and sustained growth due to the region’s well-established biotechnology ecosystem, increasing number of early-stage and clinical-stage therapies, strong academic research base, and supportive regulatory environment. Countries such as the UK, Germany, and France are emerging as key hubs for advanced therapy development, supported by collaborations between research institutes, biotech firms, and CDMOs. The growing pipeline of cell and gene therapies targeting cancer, rare diseases, and genetic disorders is significantly increasing demand for outsourced development and manufacturing services across Europe. Additionally, the presence of leading CDMOs and continuous investments in viral vector manufacturing and cell therapy platforms are further strengthening the market.

Recent company-specific developments highlight this growth trend. In February 2026, Oxford Biomedica signed a new multi-year commercial supply agreement with Bristol Myers Squibb to manufacture lentiviral vectors for CAR-T programs, reinforcing Europe’s role in commercial-scale gene therapy manufacturing. In April 2026, Oxford Biomedica also launched a fast-track AAV and lentiviral vector development platform to accelerate early-stage and clinical manufacturing timelines for therapy developers.

Overall, increasing innovation, strategic collaborations, and continuous investments in advanced therapy manufacturing technologies are driving the expansion of the cell and gene therapy CDMO market in Europe.

Asia-Pacific Cell and Gene Therapy CDMO Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the Cell and Gene Therapy CDMO (CDMO) market due to increasing investments in biotechnology and healthcare infrastructure, a rising number of clinical trials, and a growing focus on advanced therapies such as CAR-T, gene therapy, and stem cell treatments. Countries like China, Japan, South Korea, and India are rapidly expanding their biomanufacturing capabilities and attracting global pharmaceutical companies due to lower operational costs and skilled workforce availability. Additionally, supportive government initiatives, improving regulatory frameworks, and the presence of emerging CDMOs are further accelerating outsourcing activities, making APAC a key region for future market growth.

Who are the major players in the cell and gene therapy CDMO market?

The following are the leading companies in the cell and gene therapy CDMO market. These companies collectively hold the largest market share and dictate industry trends.

- Catalent, Inc.

- Minaris Advanced Therapies

- SCTbio, a.s.

- Cellex Cell Professionals GmbH

- Mycenax Biotech Inc.

- MedTherapy Biotech

- ENCELL Co., Ltd.

- Nucelion Biotechnologies

- Charles River Laboratories International, Inc.

- Lonza Group AG

- Thermo Fisher Scientific Inc.

- WuXi AppTec Co., Ltd., and others

How is the competitive landscape shaping the Cell and Gene Therapy CDMO market?

The competitive landscape of the Cell and Gene Therapy CDMO market is becoming increasingly dynamic and intense, shaped by the presence of both large, established players and emerging specialized firms. Leading companies such as Lonza Group, Catalent, Thermo Fisher Scientific, and WuXi AppTec dominate the market by leveraging their global manufacturing footprint, strong regulatory expertise, and ability to offer end-to-end services from development to commercial production. At the same time, a growing number of smaller and mid-sized CDMOs are entering the market with niche capabilities such as CAR-T manufacturing, viral vector production, and gene editing, intensifying competition.

Competition is primarily driven by factors such as technological capabilities, scalability of manufacturing, regulatory compliance, and the ability to provide integrated solutions. Companies are increasingly focusing on strategic collaborations, capacity expansions, and technology innovations to strengthen their market position and meet rising demand from biopharmaceutical clients. For instance, major players are heavily investing in expanding viral vector and cell therapy manufacturing capacity to address the growing pipeline of therapies and outsourcing needs.

Additionally, the market is moderately consolidated, with a limited number of large players holding significant market share, while new entrants continue to emerge with specialized offerings. This combination of consolidation and innovation is shaping a competitive environment where speed, quality, cost-efficiency, and global reach are key differentiators. As a result, the competitive landscape is evolving toward integrated, technology-driven CDMO models, with companies striving to become long-term strategic partners for therapy developers rather than just service providers.

Recent Developmental Activities in the Cell and Gene Therapy CDMO Market

- In May 2026, ProBio introduced a specialized packaging integrity testing service designed to de-risk the transportation and storage of Cell and Gene Therapy (CGT) products. Because CGT materials are often stored at ultra-low temperatures, conventional packaging tests frequently fail to detect microscopic breaches. ProBio’s new solution utilizes Helium Leak Detection technology, offering significantly higher sensitivity than traditional methods. This initiative ensures sterile integrity throughout the cold chain, helping developers avoid catastrophic product loss and ensuring patient safety. The expansion marks a significant step in ProBio’s role as a CDMO addressing the unique logistical challenges of advanced therapeutics.

- In April 2026, Catalent, Inc. expanded its commercial licensing agreement with Cartherics to support the manufacturing and commercialization of iPSC-derived CAR-NK cell therapies for cancer treatment, strengthening its position in advanced cell therapy manufacturing.

- In March 2026, Lonza expanded its commercial manufacturing agreement with Genetix Biotherapeutics for the production of the gene therapy ZYNTEGLO™, reflecting increasing commercial demand for gene therapy manufacturing services.

- In March 2026, Catalent partnered with GelMEDIX for the development and clinical manufacturing of iPSC-derived therapies for ocular and retinal diseases, strengthening early-stage cell therapy manufacturing capabilities in North America.

- In February 2026, Oxford Biomedica signed a new multi-year commercial supply agreement with Bristol Myers Squibb to manufacture lentiviral vectors for CAR-T programs, reinforcing Europe’s role in commercial-scale gene therapy manufacturing.

- In October 2025, Lonza launched new TheraPEAK® AmpliCell® Cytokines and 293-GT® Medium systems designed to improve scalability and consistency in cell and gene therapy manufacturing workflows. Consequently, the growing pipeline of cell and gene therapies is directly increasing outsourcing activities and fueling long-term growth in the Cell and Gene Therapy CDMO market.

- In September 2025, Thermo Fisher Scientific partnered with South Korean CDMO Dr. Park to equip a new viral vector manufacturing facility for large-scale gene therapy production, highlighting the growing investment in manufacturing infrastructure.

- In September 2025, Made Scientific and Syenex announced a technology partnership to improve scalability and efficiency in engineered T-cell therapy manufacturing using advanced gene delivery systems, aiming to reduce production timelines and manufacturing costs.

- In August 2025, US WorldMeds completed the acquisition of Adaptimmune’s cell therapy portfolio, including TECELRA® and other T-cell therapy assets, to strengthen commercialization and manufacturing activities in the oncology cell therapy space.

- In November 2024, AGC Biologics supported the FDA approval of Autolus Therapeutics’ CAR-T gene therapy (AUCATZYL®), where its Milan facility manufactured the required lentiviral vectors, highlighting how late-stage gene therapy approvals depend on CDMO-produced viral vectors.

- In October 2024, AGC Biologics began operations at its new state-of-the-art manufacturing facility in Copenhagen, Denmark, strengthening its European production capacity following regulatory inspection and licensing.

- In May, 2024, Catalent entered a strategic partnership with Siren Biotechnology to support AAV-based immuno-gene therapy development and GMP manufacturing, strengthening its role in clinical-stage AAV vector supply for oncology programs.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Cell and Gene Therapy CDMO Market CAGR |

23.87% |

|

Key Companies in the Cell and Gene Therapy CDMO Market |

Catalent, Inc., Minaris Advanced Therapies, SCTbio, a.s., Cellex Cell Professionals GmbH, Mycenax Biotech Inc., MedTherapy Biotech, ENCELL Co., Ltd., Nucelion Biotechnologies, Charles River Laboratories International, Inc., Lonza Group AG, Thermo Fisher Scientific Inc., WuXi AppTec Co., Ltd., and others. |

|

Cell and Gene Therapy CDMO Market Segments |

by Product Type, by Service Type, by Development Phase, by Indication, by End-Users, and by Geography |

|

Cell and Gene Therapy CDMO Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Cell and Gene Therapy CDMO Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Cell and Gene Therapy CDMO Market Segmentation

- Cell and Gene Therapy CDMO by Product Type Exposure

- Cell Therapy

- Gene Therapy

- Gene-Modified Cell Therapy

- Cell and Gene Therapy CDMO Service Type Exposure

- Process Development Services

- Manufacturing Services

- Others

- Cell and Gene Therapy CDMO Development Phase Exposure

- Pre-clinical Phase

- Clinical Phase

- Commercial Manufacturing

- Cell and Gene Therapy CDMO Indication Exposure

- Oncology

- Rare Diseases

- Others

- Cell and Gene Therapy CDMO End-Users Exposure

- Biopharmaceutical Companies

- Biotechnology Startups

- Academic & Research Institutes

Cell and Gene Therapy CDMO Geography Exposure

- North America Cell and Gene Therapy CDMO Market

- United States Cell and Gene Therapy CDMO Market

- Canada Cell and Gene Therapy CDMO Market

- Mexico Cell and Gene Therapy CDMO Market

- Europe Cell and Gene Therapy CDMO Market

- United Kingdom Cell and Gene Therapy CDMO Market

- Germany Cell and Gene Therapy CDMO Market

- France Cell and Gene Therapy CDMO Market

- Italy Cell and Gene Therapy CDMO Market

- Spain Cell and Gene Therapy CDMO Market

- Rest of Europe Cell and Gene Therapy CDMO Market

- Asia-Pacific Cell and Gene Therapy CDMO Market

- China Cell and Gene Therapy CDMO Market

- Japan Cell and Gene Therapy CDMO Market

- India Cell and Gene Therapy CDMO Market

- Australia Cell and Gene Therapy CDMO Market

- South Korea Cell and Gene Therapy CDMO Market

- Rest of Asia-Pacific Cell and Gene Therapy CDMO Market

- Rest of the World Cell and Gene Therapy CDMO Market

- South America Cell and Gene Therapy CDMO Market

- Middle East Cell and Gene Therapy CDMO Market

- Africa Cell and Gene Therapy CDMO Market

Cell and Gene Therapy CDMO Market Recent Industry Trends and Milestones (2023-2026):

|

Category |

Key Developments |

|

Cell and Gene Therapy CDMO Product Partnership |

Catalent partnered with GelMEDIX for the development and clinical manufacturing of iPSC-derived therapies for ocular and retinal diseases. Thermo Fisher Scientific partnered with South Korean CDMO Dr. Park to equip a new viral vector manufacturing facility for large-scale gene therapy production. |

|

Cell and Gene Therapy CDMO Product Launch |

ProBio launched its 128,000 sq. ft. GMP viral vector and plasmid DNA manufacturing facility in New Jersey, AGC Biologics launched a dedicated Cell and Gene Technologies Division to enhance its CDMO capabilities and support increasing demand from gene therapy developers across Europe. |

|

Cell and Gene Therapy CDMO Product Approval |

The FDA approved Otarmeni (lunsotogene parvec-cwha), the first dual AAV vector-based gene therapy for genetic hearing loss. The European Commission approved Autolus Therapeutics’ CAR-T therapy, AUCATZYL®, which relies on lentiviral vector manufacturing. |

|

Cell and Gene Therapy CDMO Product Expansion |

Catalent, Inc. expanded its commercial licensing agreement with Cartherics to support the manufacturing and commercialization of iPSC-derived CAR-NK cell therapies. Lonza expanded its commercial manufacturing agreement with Genetix Biotherapeutics for the production of the gene therapy ZYNTEGLO™ |

|

Company Strategy |

Lonza Group

Thermo Fisher Scientific · Strengthened position via acquisitions such as Patheon, PPD, and Brammer Bio. · Provides end-to-end services including clinical trials, manufacturing, and analytical testing. · Focuses on viral vector manufacturing and fill-finish capabilities. · Strategy centered on being a one-stop solution provider for pharma clients. |

|

Emerging Technology |

Automated & Closed-System Manufacturing, Advanced Viral Vector Production Technologies, Single-Use (Disposable) Bioprocessing Technologies, Modular & Platform-Based Manufacturing, Digitalization & Smart Manufacturing, Artificial Intelligence (AI) & Machine Learning, Process Analytical Technology (PAT), Digital Twin Technology, Gene Editing Technologies, and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are increasingly transforming the Cell and Gene Therapy CDMO market by improving efficiency, accuracy, and scalability across the entire development and manufacturing workflow. Artificial intelligence and machine learning are being used to optimize complex bioprocesses such as cell expansion, viral vector production, and gene editing by analyzing large datasets to identify optimal conditions and reduce variability. AI also plays a critical role in predictive analytics, enabling CDMOs to forecast batch failures, improve yield, and enhance product quality through real-time monitoring and process control. In addition, AI-driven digital twins and simulation models allow manufacturers to virtually replicate production processes, helping to optimize workflows and reduce development timelines before actual implementation. AI is further applied in quality control and regulatory compliance by automating data analysis, detecting anomalies, and ensuring adherence to strict GMP standards. Moreover, in areas such as supply chain management and personalized medicine, AI helps streamline logistics, patient-specific manufacturing, and scheduling, especially for autologous therapies like CAR-T. Overall, AI-powered technologies are enabling CDMOs to reduce costs, accelerate time-to-market, and deliver more consistent and scalable cell and gene therapy manufacturing solutions.

U.S. Tariff Impact Analysis on Cell and Gene Therapy CDMO Market:

The U.S. tariff impact on the Cell and Gene Therapy CDMO market is creating a complex mix of challenges and strategic shifts across the industry. Recent tariff policies, including proposals and implementations of up to 100% tariffs on imported patented pharmaceuticals and key inputs (April 2026), along with baseline tariffs of around 10–25% on imports from major regions, are significantly increasing manufacturing and procurement costs for life sciences companies. These tariffs are disrupting global supply chains, particularly for critical components such as viral vectors, APIs, and bioprocessing materials, which are often sourced internationally, thereby raising overall production costs and creating pricing pressure.

For CDMOs, especially those relying on cross-border manufacturing models, tariffs introduce uncertainty, reduce cost competitiveness, and may impact outsourcing decisions. In some cases, CDMOs and biotech firms exporting to the U.S. face additional financial burdens, with certain companies potentially exposed to tariffs as high as 20–100% depending on compliance with U.S. pricing or manufacturing policies. At the same time, these tariffs are accelerating a strategic shift toward domestic manufacturing (“onshoring”), as companies invest in U.S.-based production facilities to avoid tariff exposure and ensure supply chain resilience.

Overall, while U.S. tariffs act as a short-term constraint by increasing costs and disrupting global CDMO operations, they are also reshaping the market by encouraging local manufacturing expansion, strategic partnerships, and supply chain diversification, ultimately transforming how Cell and Gene Therapy CDMOs operate in the long term.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Key takeaways from the Cell and Gene Therapy CDMO market report study

- Market size analysis for the current cell and gene therapy CDMO market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the cell and gene therapy CDMO market.

- Various opportunities available for the other competitors in the cell and gene therapy CDMO market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current cell and gene therapy CDMO market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the cell and gene therapy CDMO market growth in the future.

Startup Funding & Investment Trends:

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Cellares |

$257 Million |

Series D |

Automated cell therapy manufacturing (CAR-T, cell therapies) |

Smart Factory platform for fully automated, end-to-end cell therapy manufacturing |