DNA Microarray Market Summary

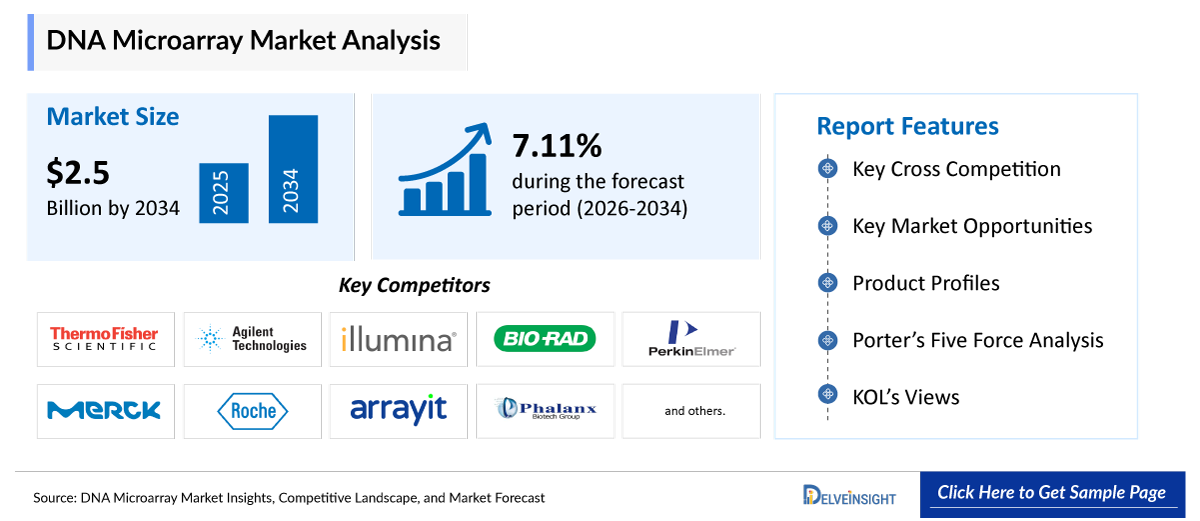

- The Global DNA Microarray Market is expected to increase from USD 2,596.21 million in 2025 to USD 2,596.21 million by 2034, reflecting strong and sustained growth.

- The Global DNA Microarray Market is growing at a CAGR of 7.11% during the forecast period from 2026 to 2034.

DNA Microarray Market Insights & Forecast

- The rising prevalence of genetic and chronic diseases, including cancer and inherited disorders, is significantly increasing the demand for DNA Microarrays for applications such as gene expression profiling, mutation detection, and early diagnosis. Simultaneously, the growing use of DNA Microarrays in drug discovery and development is enabling pharmaceutical and biotechnology companies to identify biomarkers, analyze gene-drug interactions, and accelerate the development of targeted therapies, thereby improving efficiency and reducing costs. In addition, the increase in product development activities among key market players, such as the introduction of advanced, high-throughput, and cost-effective Microarray platforms, is further enhancing their adoption across research and clinical settings. Collectively, these factors are driving the overall growth of the DNA Microarray market by expanding its application scope, improving technological capabilities, and increasing global demand.

- The leading DNA Microarray Companies such as Thermo Fisher Scientific, Agilent Technologies, Illumina, Bio-Rad Laboratories, PerkinElmer, Merck KGaA, Roche, Arrayit Corporation, Phalanx Biotech Group, CapitalBio Corporation, Applied Microarrays, LC Sciences, Oxford Gene Technology, Akonni Biosystems, Arraystar Inc., Febit Holding GmbH, CustomArray Inc., Microarrays Inc., Molecular Devices, Scienion AG, and others.

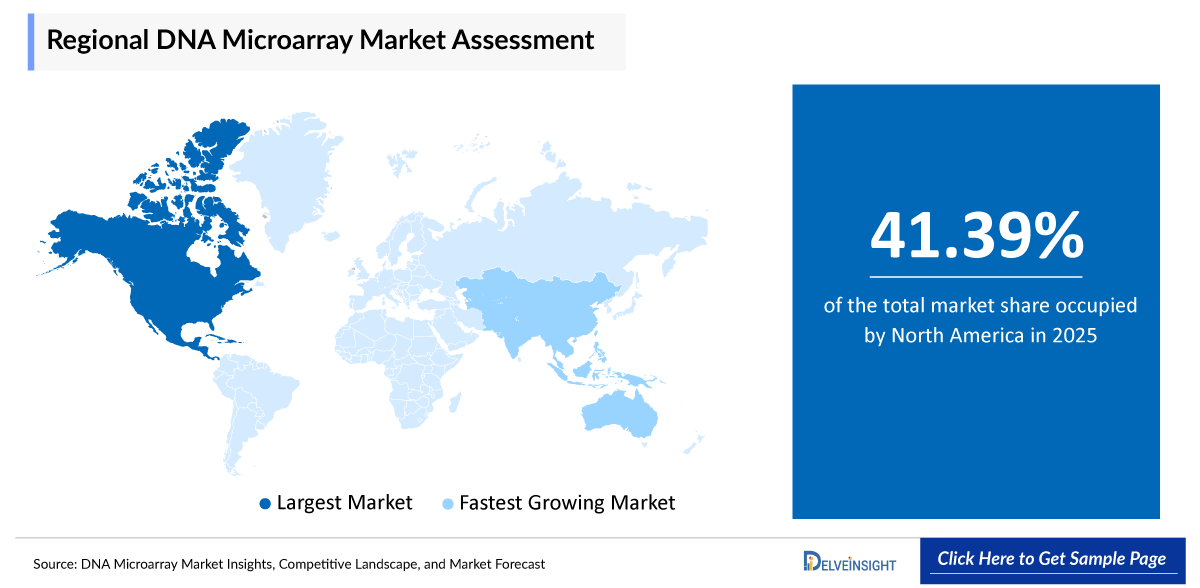

- North America is expected to dominate the DNA Microarrays Market due to the strong presence of leading biotechnology and pharmaceutical companies, advanced healthcare infrastructure, and high adoption of genomic technologies. The region also benefits from significant government funding for genomics research, the increasing prevalence of chronic and genetic diseases, and extensive use of DNA Microarrays in drug discovery and clinical diagnostics. Additionally, continuous product innovations and the presence of key market players further support market growth, making North America a leading contributor to the global DNA Microarrays market.

- In the Microarray type segment of the DNA Microarray Market, the oligonucleotide DNA Microarrays category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ DNA Microarray Market

DNA Microarray Market Size and Forecasts

Report Metrics |

Details |

|

2025 Market Size | |

|

2034 Projected Market Size | |

|

Growth Rate (2026-2034) | |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the DNA Microarray Market

-

The Rising Cases of Chronic & Genetic Diseases Leading to a Surge in DNA Microarray

The increasing incidence of diseases such as cancer, cardiovascular disorders, and rare genetic conditions is significantly driving the demand for DNA Microarrays. These tools enable large-scale gene expression profiling and mutation detection, supporting early diagnosis and targeted treatment strategies.

-

Increasing Use in Drug Discovery & Development

Pharmaceutical and biotechnology companies are increasingly adopting DNA Microarrays for biomarker discovery, toxicity studies, and drug response analysis. This accelerates drug development timelines and reduces the risk of late-stage failures.

-

Increase in Product Development Activities among the key Market Players

The increase in product development activities among key market players is significantly boosting the DNA Microarray market by driving the introduction of more advanced, high-throughput, and cost-effective platforms. Continuous innovations such as improved sensitivity, faster processing times, and enhanced data analysis capabilities are expanding the applicability of Microarrays in research, diagnostics, and drug discovery. Additionally, the development of specialized arrays for specific diseases and genomic applications is attracting a wider user base, thereby increasing adoption across academic, clinical, and pharmaceutical settings and contributing to overall market growth.

DNA Microarray Market Report Segmentation

This DNA Microarray Market Report offers a comprehensive overview of the Global DNA Microarray Market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product Type (Instruments, Consumables, Software and Services), Microarray Type (cDNA Microarrays, Oligonucleotide DNA Microarrays, SNP (Single Nucleotide Polymorphism) Microarrays, and Comparative Genomic Hybridization (CGH) Microarrays), Application (Gene Expression Analysis, Genotyping & SNP Analysis, and Others), End-Users (Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, and Others), and geography.

The DNA Microarray Market Report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing DNA Microarray Market.

A DNA Microarray is a laboratory tool used to analyze the expression of thousands of genes simultaneously. It consists of a solid surface, such as a glass slide or chip, onto which numerous DNA probes are fixed in a grid pattern. When a labeled DNA or RNA sample is applied, complementary sequences bind to these probes, allowing researchers to measure gene activity, detect mutations, and study genetic variations in a high-throughput and efficient manner.

The rising prevalence of genetic and chronic diseases, including cancer and inherited disorders, is significantly increasing the demand for DNA Microarrays, as these tools enable large-scale gene expression profiling, mutation detection, and early-stage diagnosis with high efficiency. As healthcare systems shift toward precision medicine, the need for technologies that can rapidly analyze genetic variations across large populations is further strengthening the adoption of Microarrays.

Simultaneously, the growing use of DNA Microarrays in drug discovery and development is empowering pharmaceutical and biotechnology companies to identify novel biomarkers, study gene-drug interactions, and understand disease pathways at a molecular level. This not only accelerates the development of targeted therapies but also reduces overall research costs and minimizes the risk of failure in later stages of clinical trials.

In addition, the increase in product development activities among key market players, such as the launch of advanced, high-throughput, and cost-effective Microarray platforms with improved sensitivity, accuracy, and data analysis capabilities, is further enhancing their usability across diverse applications. Companies are also focusing on developing disease-specific and application-specific arrays, which are expanding their relevance in both clinical diagnostics and research environments. Collectively, these factors are driving the robust growth of the DNA Microarray market by broadening its application scope, advancing technological capabilities, and increasing its adoption across academic institutions, diagnostic laboratories, and pharmaceutical industries worldwide.

Get More Insights into the Report @ DNA Microarray Market

What are the latest DNA Microarray Market Dynamics and Trends?

The Global DNA Microarrays Market has witnessed significant growth in recent years. This expansion is driven primarily by the increasing prevalence of chronic and genetic disorders.

According to the World Health Organization (2026) and the International Agency for Research on Cancer (IARC), in 2025, new cancer cases were projected to reach 2,13,25,245, increasing to 3,52,81,056 by 2050. Cancer is a major driver of the DNA Microarray market due to the increasing need for precise tumor classification and personalized treatment strategies. DNA Microarrays enable large-scale gene expression profiling, helping researchers and clinicians identify cancer subtypes, detect mutations, and discover biomarkers for early diagnosis and prognosis. Their widespread use in oncology research and targeted therapy development is significantly increasing demand for Microarray technologies.

Alzheimer’s Disease is another major driver of the DNA Microarray Market. The Alzheimer’s Association (2025) reported over 7 million Americans living with Alzheimer’s, expected to rise to nearly 13 million by 2050. The growing prevalence of Alzheimer’s disease is boosting the adoption of DNA Microarrays for studying gene expression changes and identifying genetic risk factors associated with neurodegeneration. Microarrays help researchers understand disease pathways, discover potential biomarkers for early detection, and support the development of targeted therapies, thereby driving their use in neurological research and diagnostics.

Additionally, the rare and orphan genetic disorders are further escalating the adoption of DNA Microarrays. According to the data provided by the Muscular Dystrophy Association (2026), Duchenne Muscular Dystrophy occurs in approximately 1 in 3,500 to 5,000 male births. Duchenne muscular dystrophy is driving the DNA Microarray Market due to the need for detailed genetic analysis and mutation detection in this inherited disorder. DNA Microarrays are used to identify gene deletions, duplications, and expression patterns, enabling accurate diagnosis and carrier screening. Their role in advancing research for gene-based therapies and personalized treatment approaches is further contributing to market growth.

Furthermore, the increasing use of DNA Microarrays in drug discovery and development is significantly boosting the overall market by enabling rapid, high-throughput analysis of gene expression, biomarker identification, and drug response profiling. This allows pharmaceutical and biotechnology companies to accelerate target identification, reduce drug development timelines, and improve the success rate of clinical trials. For instance, in January 2024, Thermo Fisher Scientific launched the Axiom™ PangenomiX Array, a highly advanced and ethnically diverse genotyping Microarray designed for pharmacogenomics and large-scale disease research, enabling more accurate biomarker discovery and drug response analysis.

Thus, the factors mentioned above are expected to boost the overall market of DNA Microarrays during the forecasted period.

However, the high cost of DNA Microarray instruments, consumables, and data analysis, combined with strong competition from advanced technologies such as next-generation sequencing (NGS), qPCR, and CRISPR-based screening platforms, is significantly restraining the DNA Microarray Market Growth. These newer technologies offer higher sensitivity, broader genomic coverage, and greater flexibility, leading many researchers and pharmaceutical companies to shift away from Microarrays. At the same time, stringent data privacy regulations governing clinical genomic data sharing are limiting access to large datasets required for research, validation, and biomarker discovery. Collectively, these factors are reducing adoption rates, slowing innovation, and creating barriers for widespread use of DNA Microarrays in both clinical and research settings.

DNA Microarray Market Segment Analysis

DNA Microarray Market by Product Type (Instruments, Consumables, Software and Services), Microarray Type (cDNA Microarrays, Oligonucleotide DNA Microarrays, SNP (Single Nucleotide Polymorphism) Microarrays, and Comparative Genomic Hybridization (CGH) Microarrays), Application (Gene Expression Analysis, Genotyping & SNP Analysis, and Others), End-Users (Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World).

By Product Type: Instruments in the DNA Microarray category are projected to register the highest revenue share.

In the product type segment of the DNA Microarray market, the instruments category is projected to grow at the fastest CAGR of 8.41% during the forecast period from 2026 to 2034. The instruments category plays a crucial role in driving overall market growth by enabling efficient, high-throughput, and accurate genomic analysis. Instruments such as Microarray scanners, hybridization ovens, and automated processing systems form the backbone of the Microarray workflow, as they directly impact data quality, reproducibility, and operational efficiency.

Continuous technological advancements, such as improved resolution scanners, faster processing speeds, enhanced sensitivity, and integration with automation and robotics, are making these instruments more reliable and user-friendly, thereby increasing their adoption across academic research institutes, pharmaceutical and biotechnology companies, and clinical laboratories.

Moreover, the growing demand for large-scale gene expression studies, biomarker discovery, and precision medicine is pushing laboratories to invest in advanced instrumentation capable of handling high sample volumes with minimal error. The introduction of compact, cost-effective, and fully automated systems is also enabling smaller labs and emerging markets to adopt DNA Microarray technologies. In addition, many key market players are offering integrated instrument platforms bundled with software and consumables, creating complete end-to-end solutions that streamline workflows and enhance productivity.

This not only increases instrument sales but also drives recurring demand for associated consumables and services. For instance, in August 2023, Thermo Fisher launched the Applied Biosystems™ CytoScan™ HD Accel array, designed to deliver rapid turnaround (~2 days) and improved whole-genome coverage. This platform enhances lab productivity and supports high-throughput cytogenetic analysis, strengthening instrument demand. Collectively, these factors make the instruments segment a key growth engine in the DNA Microarray Market, as it supports scalability, improves performance, and expands the accessibility of Microarray-based applications across diverse end-user segments.

By Microarray Type: Oligonucleotide DNA Microarrays Category Dominates the Market

Within the Microarray type segment of the DNA Microarray market, the oligonucleotide DNA Microarrays category is anticipated to dominate, accounting for around 61.32% of the market share in 2025, due to its high specificity, reproducibility, and scalability in genomic analysis. These Microarrays utilize short, synthetic DNA Sequences (oligonucleotides) as probes, allowing for precise detection of gene expression, single-nucleotide polymorphisms (SNPs), and genetic variations. Compared to traditional cDNA arrays, oligonucleotide Microarrays offer better sensitivity, reduced cross-hybridization, and the ability to design highly customized arrays for specific research or clinical applications. This makes them highly preferred in advanced fields such as pharmacogenomics, cancer research, and precision medicine.

For instance, platforms like Affymetrix GeneChip™ arrays (by Thermo Fisher Scientific) and SurePrint G3 oligonucleotide Microarrays (by Agilent Technologies) are widely used for gene expression profiling and genomic studies, supporting large-scale research projects and clinical diagnostics. Similarly, Illumina’s Infinium™ BeadChips are extensively utilized for genotyping and population-scale genomic studies, further demonstrating the dominance of oligonucleotide-based technologies. The growing demand for high-throughput and accurate genomic tools in drug discovery, biomarker identification, and disease diagnosis is further accelerating the adoption of these Microarrays. Additionally, continuous advancements in probe design, miniaturization, and integration with automated systems are enhancing performance while reducing costs, making them more accessible across laboratories. Collectively, these advantages and widespread applications position oligonucleotide DNA Microarrays as a key driver in expanding the overall DNA Microarray Market.

By Application: Gene Expression Analysis Category Dominates the Market

In the application segment of the DNA Microarray Market, the gene expression analysis category is projected to dominate, accounting for around 53.42% of the market share in 2025, due to its critical role in understanding disease mechanisms, identifying biomarkers, and enabling precision medicine. DNA Microarrays allow the simultaneous analysis of thousands of genes, making them highly valuable for large-scale transcriptomic studies in cancer, neurological disorders, and drug discovery. This high-throughput capability and cost-effectiveness have led to widespread adoption across research and clinical settings, with gene expression applications accounting for a significant share of usage in genomics studies.

Recent developments further support this dominance, for instance, in 2024, researchers, including teams from the Academician I.N. Blokhina Nizhny Novgorod Scientific Research Institute of Epidemiology and Microbiology, developed a DNA Microarray platform for the parallel detection of pneumonia-causing pathogens, demonstrating its expanding application in gene expression-based diagnostics and infectious disease research. Additionally, in December 2025, advancements in transcriptomic analysis methods, including improved differential gene expression techniques, have enhanced the accuracy and integration of Microarray-based studies with other omics technologies. Collectively, these advancements and the growing reliance on gene expression profiling in biomedical research are driving the dominance of this segment and significantly contributing to the overall growth of the DNA Microarray Market.

By End-Users: Academic & Research Institutes Category Dominates the Market

In the end-user segment of the DNA Microarray market, the academic and research institutes category dominates due to the extensive use of Microarray technologies in genomics research, gene expression studies, and biomarker discovery. These institutions are major recipients of government and private funding for large-scale research projects, which drives the adoption of advanced genomic tools like DNA Microarrays. Additionally, universities and research centers frequently conduct studies on cancer, genetic disorders, and drug development, where high-throughput gene analysis is essential. The continuous focus on innovation, availability of skilled professionals, and collaborations with biotechnology and pharmaceutical companies further strengthen the dominance of academic and research institutes in the DNA Microarray market.

DNA Microarray Market Regional Analysis

North America DNA Microarray Market Trends

North America is expected to account for the highest proportion of 41.39% of the DNA Microarray market in 2025, out of all regions. This dominance is driven by the strong presence of leading biotechnology and pharmaceutical companies, advanced healthcare infrastructure, and high adoption of genomic technologies. The region also benefits from significant government funding for genomics research, the increasing prevalence of chronic and genetic diseases, and extensive use of DNA Microarrays in drug discovery and clinical diagnostics. Additionally, continuous product innovations and the presence of key market players further support market growth, making North America a leading contributor to the global DNA Microarrays market.

According to the International Agency for Research on Cancer (2026), in 2025, the estimated new cases of cancer in North America were projected to reach 28,50,879 cases, and the projections were further estimated to increase to 3,979,416 cases by 2050. DNA Microarrays enable large-scale gene expression analysis, helping in the identification of cancer subtypes, the detection of genetic mutations, and the discovery of biomarkers for targeted therapies. Their widespread use in oncology research and drug development is increasing demand across pharmaceutical companies, research institutes, and clinical laboratories.

Furthermore, the Centers for Disease Control and Prevention (2024) reported that there were an estimated 31,800 new cases of HIV Infection in the United States. HIV infections are driving the adoption of DNA Microarrays by enabling detailed analysis of host-virus interactions and gene expression changes during infection. Microarrays are used to study viral mutations, monitor disease progression, and identify biomarkers for treatment response. Their application in improving antiretroviral therapy strategies and supporting infectious disease research is contributing to the growth of the DNA Microarray market.

Additionally, as per the data provided by the Centre for Disease Control and Prevention (2025), the prevalence of Duchenne or Becker muscular dystrophy in the United States was about 1 in every 5,000 males aged 5-9 years. Duchenne and Becker muscular dystrophy are boosting the DNA Microarray market due to the increasing need for precise genetic analysis and early diagnosis of these inherited disorders. DNA Microarrays are widely used to detect gene deletions, duplications, and expression changes in the dystrophin gene, enabling accurate diagnosis, carrier screening, and disease monitoring. Additionally, their role in supporting research for gene therapies and personalized treatment approaches is driving demand among academic institutes and biotechnology companies, thereby contributing to the overall growth of the DNA Microarray market.

Furthermore, the increasing product development activities among the key market players are further escalating the DNA Microarray Market across the region. For instance, in March 2023, the U.S.-based company Vaxess Technologies secured $9 million in funding to advance its Microarray-based intradermal delivery platform. Thus, the factors mentioned above are expected to escalate the overall market of DNA Microarrays across the region during the forecast period.

Europe DNA Microarray Market Trends

The DNA Microarray Market in Europe is experiencing robust growth, driven by the rising burden of chronic diseases, strong research infrastructure, and increasing adoption of precision medicine.

According to IARC (2026), the estimated number of new cancer cases in Europe reached 4,571,813 in 2025 and is projected to increase to 5,569,243 by 2050, highlighting a substantial rise in demand for advanced genomic diagnostic tools such as DNA Microarrays for early detection, biomarker identification, and targeted therapy development. This growing disease burden, combined with increasing investments in genomics and biotechnology across countries such as Germany, the U.K., and France, is significantly accelerating market expansion.

Additionally, the recent development activities among key market players further reinforce this growth trajectory. For instance, in May 2025, Agilent Technologies received European regulatory approval for its SurePrint G3 Human CNV Microarray, expanding its clinical and research applications across European markets. In addition, companies such as Thermo Fisher Scientific and Illumina continue to strengthen their presence in Europe through ongoing product enhancements, collaborations, and integration of high-throughput Microarray platforms with bioinformatics tools. Moreover, increasing demand for personalized medicine and genomic profiling is driving the adoption of Microarray technologies across healthcare and research institutions in Europe.

Collectively, the rising disease prevalence, strong regulatory support, and continuous innovation by key players are fueling the sustained and robust growth of the DNA Microarray market in Europe.

Asia-Pacific DNA Microarray Market Trends

The Asia Pacific region is emerging as a significant growth driver for the DNA Microarray market due to rapid advancements in healthcare infrastructure, increasing investments in genomics and biotechnology, and the expanding presence of pharmaceutical and research organizations across countries such as China, India, Japan, and South Korea. The rising prevalence of chronic and genetic diseases in the region is driving demand for advanced diagnostic tools, including DNA Microarrays, for applications such as gene expression analysis, mutation detection, and personalized medicine.

According to the data provided by the Alzheimer’s Association (2026), in India, more than 4 million people had some form of dementia. DNA Microarrays enable large-scale gene expression analysis, helping researchers identify genetic risk factors, biomarkers, and disease pathways associated with neurodegeneration. This supports early diagnosis, patient stratification, and the development of targeted therapies. As the global prevalence of dementia continues to rise, the demand for advanced genomic tools like DNA Microarrays in neurological research and drug discovery is also increasing, thereby contributing to overall market growth.

In addition, strong government initiatives supporting genomic research, growing awareness about genetic testing, and increasing collaborations between academic institutions and industry players are further accelerating market growth. The availability of cost-effective technologies and a large patient population base also make the Asia Pacific an attractive market for key players, thereby contributing to the rapid adoption and expansion of DNA Microarray technologies across research, clinical, and drug development settings.

Who are the major players in the DNA Microarray Market?

The following are the leading companies in the DNA Microarray Market. These companies collectively hold the largest market share and dictate industry trends.

- Thermo Fisher Scientific

- Agilent Technologies

- Illumina

- Bio-Rad Laboratories

- PerkinElmer

- Merck KGaA

- F. Hoffmann-La Roche Ltd.

- Arrayit Corporation

- Phalanx Biotech Group

- CapitalBio Corporation

- Applied Microarrays

- LC Sciences

- Oxford Gene Technology

- Akonni Biosystems

- Arraystar Inc.

- Febit Holding GmbH

- CustomArray Inc.

- Microarrays Inc.

- Molecular Devices

- Scienion AG

- Others

How is the competitive landscape shaping the DNA Microarray Market?

The competitive landscape of the DNA Microarray market is characterized by a moderately consolidated structure, where a few dominant players, such as Thermo Fisher Scientific, Illumina, and Agilent Technologies, hold a significant share, while several mid- and niche players contribute through specialized offerings. These leading companies are actively competing through continuous product innovation, strategic collaborations, mergers and acquisitions, and expansion of their product portfolios to strengthen their market position.

For instance, advancements such as high-density Microarrays, integration with bioinformatics and AI-based analytics, and development of customized arrays are key differentiators among competitors. Additionally, partnerships with research institutions and pharmaceutical companies are enabling broader application in precision medicine and drug discovery. The market also shows high innovation intensity, with companies focusing on improving sensitivity, throughput, and cost-efficiency to stay competitive. Despite competition from next-generation sequencing (NGS), Microarray companies are maintaining relevance by enhancing clinical and research applications. Overall, the competitive environment is dynamic and innovation-driven, with top players accounting for a major share while continuously investing in technology upgrades and strategic initiatives to sustain growth and differentiation.

DNA Microarray Market Recent Breakthroughs and Developments

- In May 2025, Agilent Technologies received European regulatory approval for its SurePrint G3 Human CNV Microarray, expanding its clinical and research applications across European markets.

- In January 2024, Thermo Fisher Scientific launched the Axiom™ PangenomiX Array, a highly advanced and ethnically diverse genotyping Microarray designed for pharmacogenomics and large-scale disease research, enabling more accurate biomarker discovery and drug response analysis.

- In August 2023, Thermo Fisher launched the Applied Biosystems™ CytoScan™ HD Accel array, designed to deliver rapid turnaround (~2 days) and improved whole-genome coverage. This platform enhances lab productivity and supports high-throughput cytogenetic analysis, strengthening instrument demand.

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

DNA Microarray Market CAGR | |

|

DNA Microarray Companies |

Thermo Fisher Scientific, Agilent Technologies, Illumina, Bio-Rad Laboratories, PerkinElmer, Merck KGaA, Roche, Arrayit Corporation, Phalanx Biotech Group, CapitalBio Corporation, Applied Microarrays, LC Sciences, Oxford Gene Technology, Akonni Biosystems, Arraystar Inc., Febit Holding GmbH, CustomArray Inc., Microarrays Inc., Molecular Devices, Scienion AG, and others. |

|

DNA Microarray Market Segments |

by Product Type, by Microarray Type, by Application, by End-Users, and by Geography |

|

DNA Microarray Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

DNA Microarray Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

DNA Microarray Market Segmentation

· DNA Microarray by Product Type Exposure

o Instruments

o Consumables

o Software

o Services

· DNA Microarray Microarray Type Exposure

o cDNA Microarrays

o Oligonucleotide DNA Microarrays

o SNP (Single Nucleotide Polymorphism) Microarrays

o Comparative Genomic Hybridization (CGH) Microarrays

· DNA Microarray Application Exposure

o Gene Expression Analysis

o Genotyping & SNP Analysis

o Others

· Ambulance End-Users Exposure

o Academic & Research Institutes

o Pharmaceutical & Biotechnology Companies

o Others

· DNA Microarray Geography Exposure

o North America DNA Microarray Market

§ United States DNA Microarray Market

§ Canada DNA Microarray Market

§ Mexico DNA Microarray Market

o Europe DNA Microarray Market

§ United Kingdom DNA Microarray Market

§ Germany DNA Microarray Market

§ France DNA Microarray Market

§ Italy DNA Microarray Market

§ Spain DNA Microarray Market

§ Rest of Europe DNA Microarray Market

o Asia-Pacific DNA Microarray Market

§ China DNA Microarray Market

§ Japan DNA Microarray Market

§ India DNA Microarray Market

§ Australia DNA Microarray Market

§ South Korea DNA Microarray Market

§ Rest of Asia-Pacific DNA Microarray Market

o Rest of the World DNA Microarray Market

§ South America DNA Microarray Market

§ Middle East DNA Microarray Market

§ Africa DNA Microarray Market

DNA Microarray Market Recent Industry Trends and Milestones (2022-2026)

Category |

Key Developments |

|

DNA Microarray Product Approval |

Agilent Technologies received European regulatory approval for its SurePrint G3 Human CNV Microarray. |

|

DNA Microarray Product Launch |

Thermo Fisher Scientific introduced the Axiom™ PangenomiX Array to enable population-scale disease and pharmacogenomics research, while also launching the Applied Biosystems™ CytoScan™ HD Accel array to advance cytogenetic analysis through enhanced genomic coverage and faster turnaround times. |

|

Company Strategy |

Thermo Fisher is focusing on expanding its end-to-end genomics portfolio by integrating DNA Microarrays with sequencing and bioinformatics tools. Illumina is leveraging its strong R&D capabilities to enhance high-density Microarray technologies and expand into population-scale genomic screening programs. Agilent is focusing on custom Microarray solutions and flexible assay design, particularly for cancer research and molecular diagnostics. |

|

Emerging Technology |

AI & Machine Learning Integration, Multi-Omics Integration, In-situ Synthesis Microarrays, High-Density & Miniaturized Biochips, Advanced Surface Chemistry & Materials, Label-Free Detection Technologies, and Others |

Impact Analysis

AI-Powered Innovations and Applications

AI-powered innovations are significantly transforming DNA Microarray technologies by enhancing data analysis, accuracy, and clinical applicability. The integration of artificial intelligence and machine learning algorithms enables the efficient processing of large-scale gene expression datasets, helping to identify complex patterns, biomarkers, and disease signatures with greater precision and speed. AI-driven tools are widely used for gene expression profiling, cancer classification, and prediction of disease outcomes, improving diagnostic accuracy and supporting personalized treatment decisions.

In drug discovery, AI enhances Microarray-based studies by enabling rapid identification of drug targets, analyzing gene–drug interactions, and predicting therapeutic responses, thereby reducing development time and costs. Additionally, AI supports automated quality control, normalization, and interpretation of Microarray data, minimizing human error and improving reproducibility. The combination of AI with DNA Microarrays is also enabling advancements in precision medicine, population genomics, and clinical decision support systems, making Microarray platforms more intelligent, scalable, and efficient across research and healthcare applications.

U.S. Tariff Impact Analysis on the DNA Microarray Market

The U.S. tariff impact on the DNA Microarray market is largely indirect but significant, as Microarrays are part of the broader biotechnology and medical device ecosystem. Recent U.S. tariff policies, particularly those introduced in April 2025, including baseline tariffs of around 10% and higher duties (up to 25%-125%) on imports from countries such as China and the EU, are increasing the cost of critical components used in Microarray instruments and consumables, such as sensors, chips, reagents, and electronic modules. Since nearly 90% of U.S. biotech companies rely on imported components, tariffs are expected to significantly raise manufacturing costs, disrupt supply chains, and delay product development timelines.

For the DNA Microarray market specifically, these cost pressures can lead to higher pricing of instruments and consumables, reduced affordability for research institutions, and slower adoption rates. Additionally, tariffs are forcing companies to restructure supply chains, shift sourcing strategies, and invest in domestic manufacturing, which may increase operational complexity and delay innovation. However, on the positive side, such policies may encourage local production and strengthen domestic capabilities in the long term. Overall, U.S. tariffs are acting as a mixed-impact factor, creating short-term restraints through cost escalation and supply disruptions while potentially supporting long-term market resilience and domestic growth in the DNA Microarray industry.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Startup Funding & Investment Trends

Company Name |

Total Funding |

Main Products |

Stage of Development |

Core Technology |

|

Vaxess |

$9M |

- |

Microarray Drug Delivery Platform |

To continue to advance its work in GLP-1 and expand manufacturing capabilities to support the lead program and new partnerships for additional therapeutics. |

|

DNAnexus |

later $15 million |

Series C |

Cloud-based genomic data analysis platform |

AI-driven bioinformatics + cloud computing for large-scale genomic data (including Microarray datasets) |

Key Takeaways from the DNA Microarray Market Report Study

- Market size analysis for the current DNA Microarray market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the DNA Microarray market.

- Various opportunities available for the other competitors in the DNA Microarray market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current DNA Microarray market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the DNA Microarray market growth in the future?

Stay updated with us for Recent Articles @ New DelveInsight Blogs