Upstream Bioprocessing Market Summary

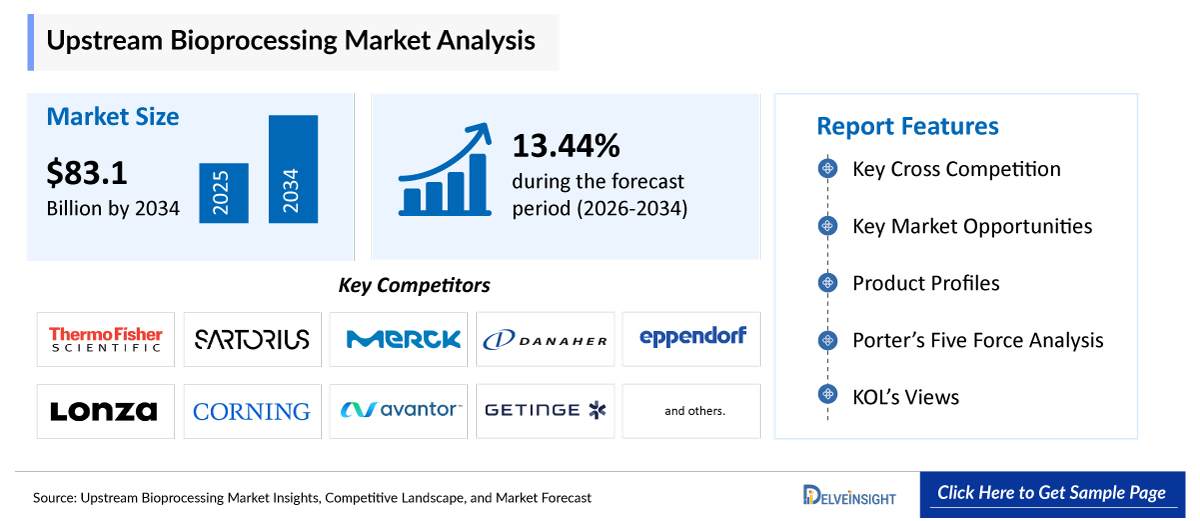

- The global upstream bioprocessing market size is expected to increase from USD 26,820.10 million in 2025 to USD 83,061.31 million by 2034, reflecting strong and sustained growth.

- The global upstream bioprocessing market is growing at a CAGR of 13.44% during the forecast period from 2026 to 2034.

- The rising demand for biologics, rapid growth in cell & gene therapy manufacturing, and increasing vaccine production activities are collectively driving significant expansion in the upstream bioprocessing market. The growing use of monoclonal antibodies, recombinant proteins, and advanced therapeutics has increased the need for efficient cell culture systems, bioreactors, media, and fermentation technologies. At the same time, the expanding development of cell and gene therapies requires highly specialized upstream processing platforms for viral vector and cell expansion production. In addition, increasing global vaccine manufacturing activities and pandemic preparedness initiatives are accelerating investments in large-scale bioprocessing infrastructure. Together, these factors are boosting the adoption of single-use technologies, automation systems, and continuous bioprocessing solutions, thereby supporting overall market growth for companies such as Thermo Fisher Scientific Inc., Sartorius AG, and Danaher Corporation.

- The leading companies operating in the upstream bioprocessing market include Thermo Fisher Scientific Inc., Sartorius AG, Merck KGaA, Danaher Corporation, Eppendorf SE, Lonza Group AG, Corning Incorporated, Avantor, Inc., Getinge AB, Repligen Corporation, FUJIFILM Irvine Scientific, Inc., PBS Biotech, Inc., Hamilton Company, Entegris, Inc., Meissner Filtration Products, Inc., Applikon Biotechnology B.V., Kühner AG, Cellexus International Ltd., GE HealthCare Technologies Inc., AGC Biologics, and others.

- North America is expected to dominate the upstream bioprocessing market due to the strong presence of major biopharmaceutical and biotechnology companies, advanced biomanufacturing infrastructure, and increasing investments in biologics, vaccines, and cell & gene therapy production. The region benefits from high adoption of single-use bioprocessing technologies, continuous manufacturing systems, and automation platforms, along with significant research funding and favorable regulatory support. In addition, the growing presence of leading companies such as Thermo Fisher Scientific Inc., Danaher Corporation, Repligen Corporation, and Avantor, Inc. is further supporting regional market growth through continuous product innovation and manufacturing expansion.

- In the product segment of the upstream bioprocessing market, the instruments/equipment category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Upstream Bioprocessing Market Insights

Upstream Bioprocessing Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 26,820.10 million |

|

2034 Projected Market Size |

USD 83,061.31 million |

|

Growth Rate (2026-2034) |

13.44% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Upstream Bioprocessing Market

- Rising demand for biologics is leading to a surge in upstream bioprocessing: Increasing use of monoclonal antibodies, recombinant proteins, and biosimilars is driving the need for advanced upstream bioprocessing systems for large-scale biologics production.

- Growth in cell & gene therapy manufacturing: The expanding pipeline of cell therapies, gene therapies, and viral vectors is increasing demand for efficient cell culture, media, and bioreactor technologies.

- Increasing vaccine production activities: Growing global focus on vaccine development and pandemic preparedness is boosting investment in upstream fermentation and cell culture infrastructure.

Upstream Bioprocessing Market Report Segmentation

This upstream bioprocessing market report offers a comprehensive overview of the global upstream bioprocessing market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Product (Instruments/Equipment {Bioreactors & Fermenters, Cell Culture Systems, Filtration Systems, and Others}, Consumables & Accessories, Software, and Services), Workflow (Cell Line Development, Media Preparation, Cell Culture/Fermentation, and Others), Use-Type (Single-use and Multi-use), Mode (In-house and Outsourced), End-Users (Biopharma & Biotech Companies, Contract Development and Manufacturing Organizations (CDMOs), Academic & Research Institutes), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing upstream bioprocessing market.

Upstream bioprocessing refers to the initial stage of biopharmaceutical manufacturing where living cells or microorganisms are cultivated to produce biological products such as monoclonal antibodies, vaccines, recombinant proteins, and cell & gene therapies. It includes processes such as cell line development, media preparation, cell culture, fermentation, and bioreactor operations before the product moves to downstream purification and final formulation. The process plays a critical role in ensuring high product yield, quality, and manufacturing efficiency in biologics production.

The rising demand for biologics, rapid growth in cell & gene therapy manufacturing, and increasing vaccine production activities are collectively driving substantial expansion in the upstream bioprocessing market. The increasing adoption of biologic drugs such as monoclonal antibodies, recombinant proteins, biosimilars, and therapeutic enzymes for the treatment of cancer, autoimmune disorders, and infectious diseases has significantly increased the requirement for advanced upstream technologies, including bioreactors, fermenters, cell culture media, filtration systems, and process monitoring solutions. Pharmaceutical and biotechnology companies are continuously expanding their production capacities to meet the growing global demand for biologics, thereby accelerating investments in upstream manufacturing infrastructure.

Simultaneously, the rapid advancement of cell and gene therapies is creating strong demand for highly specialized upstream bioprocessing platforms capable of supporting viral vector production, stem cell expansion, and genetically modified cell cultivation. These therapies require highly controlled and scalable manufacturing environments, which is encouraging the adoption of single-use bioreactors, perfusion systems, and automated cell culture technologies. In addition, increasing clinical trials and regulatory approvals for CAR-T therapies, gene-modified therapies, and regenerative medicine products are further supporting market growth.

Moreover, rising vaccine production activities across the globe, particularly after the COVID-19 pandemic, have increased investments in large-scale fermentation and cell culture facilities. Governments and private organizations are prioritizing pandemic preparedness and domestic biologics manufacturing capabilities, leading to increased funding for bioprocessing infrastructure expansion. These factors are collectively driving the adoption of continuous bioprocessing, AI-based automation, real-time monitoring systems, and disposable technologies to improve production efficiency, scalability, and contamination control. As a result, leading companies such as Thermo Fisher Scientific Inc., Sartorius AG, Danaher Corporation, and Merck KGaA are increasingly expanding their upstream bioprocessing portfolios and manufacturing capabilities to address the growing global demand.

Get More Insights into the Report @ Upstream Bioprocessing Market Trends

What are the latest upstream bioprocessing market dynamics and trends?

The rising demand for biologics is significantly driving the growth of the upstream bioprocessing market as biopharmaceutical companies increase the production of monoclonal antibodies, recombinant proteins, biosimilars, vaccines, and other biologic therapies. The growing prevalence of cancer, autoimmune diseases, and infectious disorders is increasing the need for advanced cell culture systems, bioreactors, fermentation technologies, and specialized media. In response, companies are expanding biologics manufacturing capacity and adopting single-use and continuous bioprocessing technologies to improve production efficiency, scalability, and flexibility. Additionally, the growing focus on personalized medicine and next-generation therapeutics is further boosting demand for advanced upstream bioprocessing solutions.

In response to this growing demand, several leading companies are actively expanding their upstream bioprocessing capabilities and launching advanced technologies. For example, in September 2024, Danaher Corporation, through Cytiva, opened its first Innovation Hub in Korea to support biopharmaceutical manufacturing and filtration product development in the Asia-Pacific region. Furthermore, in October 2024, Thermo Fisher Scientific Inc. introduced new CDMO and CRO services and expanded manufacturing operations to support biologics, cell therapies, and gene therapy production. Additionally, in January 2025, Sartorius AG reported strong growth in its bioprocess solutions division, driven by increasing demand for consumables and products used in advanced biologic therapies, while also expanding its portfolio for biologics and cell & gene therapy manufacturing. Furthermore, companies are increasingly investing in integrated and continuous bioprocessing technologies to improve manufacturing efficiency. These developments collectively demonstrate how the growing biologics industry is accelerating innovation, infrastructure expansion, and technology adoption across the upstream bioprocessing market.

Additionally, increasing vaccine production activities are significantly driving the growth of the upstream bioprocessing market as governments and biopharmaceutical companies continue expanding vaccine manufacturing capacity to address infectious diseases and improve pandemic preparedness. Vaccine production requires advanced upstream technologies such as cell culture systems, bioreactors, fermenters, filtration systems, and specialized media for large-scale microbial and mammalian cell cultivation. The growing demand for mRNA, recombinant, and viral vector vaccines is accelerating investments in single-use bioreactors, automated manufacturing systems, and continuous bioprocessing technologies to improve scalability, production efficiency, and contamination control. Additionally, increasing government funding and global immunization programs are further supporting the modernization of vaccine manufacturing infrastructure. Several companies are actively expanding their vaccine and biologics manufacturing capabilities to address this increasing demand. In August 2024, FUJIFILM Diosynth Biotechnologies opened a new microbial manufacturing facility in Billingham, U.K., which tripled microbial production throughput through the addition of advanced fermentation and upstream processing infrastructure for biologics and vaccine production. Thus, the factors mentioned above are expected to boost the overall market of upstream bioprocessing during the forecast period.

However, the risk of contamination is a major limiting factor in the upstream bioprocessing market because cell culture and fermentation processes are highly sensitive to microbial, viral, or cross-batch contamination. Even minor contamination can disrupt cell growth, reduce product quality, and lead to complete batch failures, resulting in significant financial losses and production delays. This challenge becomes more critical in large-scale biologics, vaccines, and cell therapy manufacturing, where sterile processing conditions must be maintained continuously. Furthermore, the stringent regulatory requirements also restrain market growth, as biopharmaceutical manufacturers must comply with strict guidelines related to product safety, sterility, process validation, and manufacturing consistency. Regulatory agencies require extensive documentation, quality control testing, and validation procedures, which increase operational complexity, development timelines, and manufacturing costs. These compliance requirements can create challenges for small and mid-sized manufacturers trying to scale upstream bioprocessing operations efficiently.

Upstream Bioprocessing Market Segment Analysis

Upstream Bioprocessing Market by Product (Instruments/Equipment {Bioreactors & Fermenters, Cell Culture Systems, Filtration Systems, and Others}, Consumables & Accessories, Software, and Services), Workflow (Cell Line Development, Media Preparation, Cell Culture/Fermentation, and Others), Use-Type (Single-use and Multi-use), Mode (In-house and Outsourced), End-Users (Biopharma & Biotech Companies, Contract Development and Manufacturing Organizations (CDMOs), Academic & Research Institutes), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Product: Bioreactors & Fermenters under the instruments/equipment category is expected to dominate the market with the largest revenue share.

In the product segment of the upstream bioprocessing market, the bioreactors & fermenters under the instruments/equipment category are contributing to 35% of total market revenue in 2025, because they serve as the core systems for cell culture and microbial fermentation processes used in biologics manufacturing. These systems provide highly controlled environments for the cultivation of mammalian cells, bacteria, yeast, and other microorganisms required for the production of monoclonal antibodies, recombinant proteins, vaccines, biosimilars, and cell & gene therapies. The increasing global demand for biologics and advanced therapeutics is driving strong adoption of large-scale stainless-steel bioreactors as well as flexible single-use bioreactor systems that improve scalability, reduce contamination risks, minimize cleaning requirements, and lower operational costs. In addition, continuous advancements in automation, process monitoring, perfusion technologies, and high-cell-density cultivation are improving production efficiency and accelerating manufacturing timelines, further supporting market expansion.

The rapid growth of vaccine manufacturing, biosimilar production, and CDMO outsourcing activities is also increasing investments in advanced bioreactor infrastructure. Biopharmaceutical companies are increasingly adopting single-use and modular bioreactor systems because they offer faster setup times, operational flexibility, and lower capital expenditure compared to conventional stainless-steel facilities. Moreover, the expansion of cell and gene therapy manufacturing is creating strong demand for scalable and automated bioreactor platforms capable of supporting sensitive cell expansion and viral vector production processes.

Several recent industry developments highlight the growing importance of bioreactors & fermenters in upstream bioprocessing. For instance, in March 2025, Danaher Corporation, through its Cytiva business, expanded its Xcellerex platform with large-scale 500 L and 2,000 L single-use bioreactors to support increasing monoclonal antibody and vaccine production requirements. Similarly, in April 2025, WuXi Biologics (Cayman) Inc. completed commercial-scale production campaigns using three 5,000 L single-use bioreactors, demonstrating how CDMOs are rapidly scaling biologics manufacturing capacity while avoiding major capital investments associated with traditional stainless-steel facilities. These developments demonstrate how advanced bioreactor technologies are becoming essential for improving manufacturing flexibility, accelerating biologics production, and supporting the overall growth of the upstream bioprocessing market.

By Workflow: The cell culture/fermentation category dominates the market.

Within the workflow segment of the upstream bioprocessing market, the cell culture/fermentation category is anticipated to dominate, accounting for around 47% of the market share in 2025. Cell culture and fermentation are the core drivers of the upstream bioprocessing market because they directly control the growth of living cells used to produce biologics such as monoclonal antibodies, vaccines, recombinant proteins, and cell & gene therapy products. These processes determine overall productivity, yield, and product quality, making them the most critical and value-generating stage in biomanufacturing. The growing adoption of high-density cell culture systems, perfusion bioreactors, optimized media, and advanced fermentation technologies has significantly increased production efficiency while reducing manufacturing time and cost. In addition, the rise of single-use bioreactors, automation, and real-time monitoring systems has improved scalability and flexibility, which is strongly boosting demand for upstream bioprocessing solutions globally.

Recent developments further highlight this growth. In July 2023, Merck KGaA (MilliporeSigma) expanded its cell culture media production capacity in the U.S. to meet rising biologics demand. In September 2023, Getinge launched the AppliFlex ST GMP single-use bioreactor for advanced therapy production, including cell and gene therapies. These innovations show a strong industry focus on scalable and efficient cell culture and fermentation technologies, which are directly accelerating growth in the upstream bioprocessing market.

Thus, the factors mentioned above are expected to boost the market of cell culture/fermentation, thereby escalating the overall market of upstream bioprocessing.

By Use-Type: The multi-use category dominates the market.

Within the use-type segment of the upstream bioprocessing market, the multi-use category is anticipated to dominate, accounting for around 52% of the market share in 2025. Multi-use systems are significantly boosting the overall upstream bioprocessing market because they form the foundation of large-scale, commercial biologics manufacturing, especially for high-volume production of monoclonal antibodies, vaccines, and recombinant proteins. These systems, typically stainless-steel bioreactors and fermenters, are preferred in established pharmaceutical facilities due to their high durability, proven scalability (often 10,000–20,000 L or more), process robustness, and lower cost per batch in long-term production. Because they support repeated use after cleaning and sterilization (CIP/SIP), they are highly suitable for continuous, large-batch manufacturing, which still accounts for a major share of global biologics output. Their reliability and ability to maintain consistent product quality across long production campaigns make them essential in commercial-scale facilities, thereby sustaining strong demand for upstream bioprocessing equipment, media, sensors, and process control systems. Although single-use systems are growing rapidly, multi-use systems continue to dominate in high-volume production environments, especially for blockbuster biologics, ensuring stable and large revenue contribution to the overall upstream market.

Recent developments highlight ongoing investment and modernization in multi-use platforms. In March 2025, Lonza expanded its bioprocessing capabilities by strengthening its multi-use bioreactor manufacturing footprint through the acquisition of a bioprocessing unit, enhancing large-scale production capacity for biologics. In September 2024, Sartorius AG and Merck KGaA entered into a strategic collaboration to integrate advanced bioreactor technologies and analytics, improving efficiency and process control in both stainless-steel and hybrid multi-use systems. These developments show that even with the rise of single-use technologies, multi-use systems remain a critical backbone of industrial-scale bioprocessing, thereby continuing to drive significant market value.

By Mode: The in-house category dominates the market.

Within the mode segment of the upstream bioprocessing market, the in-house category is anticipated to dominate, accounting for around 65% of the market share in 2025. The in-house segment is strongly boosting the upstream bioprocessing market because large pharmaceutical and biotechnology companies continue to invest heavily in their own manufacturing infrastructure to maintain full control over cell culture, fermentation, process optimization, and product quality. In-house production enables better regulatory compliance, faster process development, and protection of intellectual property, which is especially critical for high-value biologics such as monoclonal antibodies, vaccines, and advanced therapies. These companies are also upgrading and expanding internal facilities with advanced bioreactors, automated control systems, and high-efficiency cell culture platforms, which drives continuous demand for upstream equipment, media, and consumables. As a result, in-house manufacturing remains the dominant mode and a key revenue driver for the overall upstream bioprocessing market.

By End-Users: The Biopharma & Biotech Companies category dominates the market.

Within the end-user segment of the upstream bioprocessing market, biopharmaceutical and biotechnology companies dominate due to their strong focus on developing and manufacturing biologics such as monoclonal antibodies, vaccines, recombinant proteins, and cell & gene therapies. These companies invest heavily in advanced cell culture systems, fermentation technologies, and bioreactor platforms to ensure high productivity, scalability, and regulatory compliance during early-stage and commercial production. Their continuous expansion of biologics pipelines, along with rising demand for innovative therapies, drives the majority of upstream bioprocessing adoption. Additionally, large pharma and biotech firms often operate integrated in-house facilities, further strengthening their position as the leading end-user segment in the market.

Upstream Bioprocessing Market Regional Analysis

North America Upstream Bioprocessing Market Trends

North America is expected to account for the highest proportion of 37% of the Upstream Bioprocessing market in 2025, out of all regions. North America is a key growth engine for the upstream bioprocessing market, primarily due to its strong biopharmaceutical ecosystem, high R&D spending, and the presence of leading global players such as Thermo Fisher Scientific, Danaher (Cytiva), Merck KGaA (MilliporeSigma), and Sartorius. The region benefits from a highly developed biomanufacturing infrastructure, advanced clinical pipeline (especially in monoclonal antibodies, vaccines, and cell & gene therapies), and strong regulatory support from the FDA, which accelerates adoption of advanced upstream technologies like high-density cell culture systems, fermentation platforms, single-use bioreactors, and continuous processing solutions. Additionally, the growing number of CDMOs, biotech startups, and academic–industry collaborations in the U.S. and Canada is increasing demand for scalable and flexible upstream solutions, thereby driving significant equipment, media, and consumables consumption. North America also leads in technology innovation, where companies are actively expanding capacity and upgrading facilities to meet rising biologics demand, making the region the largest revenue contributor in the global upstream bioprocessing market.

Recent developments further highlight this dominance. In February 2025, Thermo Fisher Scientific announced the acquisition of Solventum’s purification and filtration business (~$4.1 billion) to strengthen its bioprocessing portfolio in North America and expand upstream/downstream integration capabilities. Additionally, in January 2025, Sartorius AG announced major investments in expanding single-use bioprocessing technologies in North America, aimed at increasing production capacity and supporting biologics manufacturing demand. In March 2024, Thermo Fisher also invested in expanding its North American bioprocessing infrastructure to enhance single-use and cell culture production systems, reflecting continued regional capacity expansion. These strategic investments and facility expansions demonstrate how North America continues to drive upstream bioprocessing growth through strong innovation, infrastructure scaling, and consolidation of advanced biomanufacturing technologies.

Europe Upstream Bioprocessing Market Trend

The Upstream Bioprocessing market in Europe is witnessing strong and sustained growth due to the region’s advanced biopharmaceutical ecosystem, strong regulatory framework, and high investment in biotechnology research and manufacturing. Europe is home to several global leaders, such as Sartorius AG, Merck KGaA, Lonza, Cytiva (Danaher), and Eppendorf, which are continuously expanding their upstream capabilities in cell culture, fermentation, bioreactors, and process automation technologies. The region benefits from a well-established network of biopharma companies, CDMOs, and academic–industry collaborations, which is accelerating demand for scalable and flexible upstream solutions. In addition, the rising focus on biosimilars, monoclonal antibodies, vaccines, and cell & gene therapies is driving higher adoption of advanced cell culture systems, single-use technologies, and high-efficiency fermentation platforms. Countries such as Germany, the UK, Switzerland, and France are major hubs, supported by strong government funding, innovation-friendly regulations, and continuous modernization of manufacturing facilities. As a result, Europe is becoming a key innovation and production base, significantly contributing to global upstream bioprocessing market expansion.

Recent developments in Europe further highlight this growth trajectory. In June 2025, Cytiva (Danaher) announced a USD 1.6 billion investment plan through 2028 to expand bioprocessing manufacturing capacity across Europe and other regions, strengthening upstream production infrastructure. In September 2024, MilliporeSigma (Merck KGaA) expanded its bioprocessing production capabilities in Europe to support growing demand for cell culture media and biologics manufacturing.

Thus, the factors mentioned above are expected to boost the overall market of upstream bioprocessing across the region.

Asia-Pacific Upstream Bioprocessing Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the upstream bioprocessing market due to the rapid expansion of the biopharmaceutical industry, increasing investments in biologics manufacturing, and growing adoption of advanced cell culture and fermentation technologies. Countries such as China, India, Japan, and South Korea are strengthening their biomanufacturing capabilities through government support, rising R&D activities, and expansion of CDMOs to meet global demand for vaccines, monoclonal antibodies, and biosimilars. Additionally, lower manufacturing costs, availability of skilled workforce, and increasing outsourcing from Western pharmaceutical companies are accelerating the adoption of upstream bioprocessing solutions across the region.

Who are the major players in the upstream bioprocessing market?

The following are the leading companies in the upstream bioprocessing market. These companies collectively hold the largest market share and dictate industry trends.

- Thermo Fisher Scientific Inc.

- Sartorius AG

- Merck KGaA

- Danaher Corporation

- Eppendorf SE

- Lonza Group AG

- Corning Incorporated

- Avantor, Inc.

- Getinge AB

- Repligen Corporation

- FUJIFILM Irvine Scientific, Inc.

- PBS Biotech, Inc.

- Hamilton Company

- Entegris, Inc.

- Meissner Filtration Products, Inc.

- Applikon Biotechnology B.V.

- Kühner AG

- Cellexus International Ltd.

- GE HealthCare Technologies Inc.

- AGC Biologics, and others

How is the competitive landscape shaping the upstream bioprocessing market?

The competitive landscape of the upstream bioprocessing market is becoming increasingly dynamic and consolidated, driven by strong competition among global life science giants such as Thermo Fisher Scientific, Danaher (Cytiva), Merck KGaA (MilliporeSigma), Sartorius AG, and Lonza. These companies are focusing on strategic acquisitions, capacity expansions, and technology integration to strengthen their upstream portfolios across cell culture, fermentation systems, single-use bioreactors, and process analytics. Competition is also intensifying due to rising demand for flexible, scalable, and automated biomanufacturing solutions, pushing players to invest in next-generation technologies like continuous bioprocessing, digital bioprocess monitoring, and AI-driven process optimization. At the same time, the growing presence of CDMOs and emerging biotech firms is reshaping the market by increasing outsourcing trends and driving demand for cost-efficient upstream solutions. Partnerships between biopharma companies and technology providers are also expanding, enabling faster process development and commercialization. Overall, the competitive landscape is characterized by innovation-led growth, consolidation through mergers and acquisitions, and increasing emphasis on integrated upstream bioprocessing platforms.

Recent Developmental Activities in the Upstream Bioprocessing Market

- In June 2025, Cytiva (Danaher) announced a USD 1.6 billion investment plan through 2028 to expand bioprocessing manufacturing capacity across Europe and other regions, strengthening upstream production infrastructure.

- In February 2025, Thermo Fisher Scientific announced the acquisition of Solventum’s purification and filtration business (~$4.1 billion) to strengthen its bioprocessing portfolio in North America and expand upstream/downstream integration capabilities.

- In January 2025, Sartorius AG announced major investments in expanding single-use bioprocessing technologies in North America, aimed at increasing production capacity and supporting biologics manufacturing demand.

- In November 2024, Thermo Fisher Scientific Inc. announced the expansion of its bioprocess design center in Hyderabad, India, to support upstream and downstream vaccine and biologics manufacturing workflows, including single-use bioreactor scale-up and cell culture media development.

- In September 2024, MilliporeSigma (Merck KGaA) expanded its bioprocessing production capabilities in Europe to support growing demand for cell culture media and biologics manufacturing.

- In September 2024, Danaher Corporation, through Cytiva, opened its first Innovation Hub in Korea to support biopharmaceutical manufacturing and filtration product development in the Asia-Pacific region.

- In October 2024, Thermo Fisher Scientific Inc. introduced new CDMO and CRO services and expanded manufacturing operations to support biologics, cell therapies, and gene therapy production.

- In August 2024, FUJIFILM Diosynth Biotechnologies opened a new microbial manufacturing facility in Billingham, U.K., which tripled microbial production throughput through the addition of advanced fermentation and upstream processing infrastructure for biologics and vaccine production.

- In May 2024, Sartorius AG collaborated with Sanofi to commercialize integrated continuous biomanufacturing platforms aimed at improving productivity and reducing resource consumption in biologics production.

- In January 2025, Sartorius AG reported strong growth in its bioprocess solutions division driven by increasing demand for consumables and products used in advanced biologic therapies, while also expanding its portfolio for biologics and cell & gene therapy manufacturing.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Upstream Bioprocessing Market CAGR |

13.44% |

|

Key Companies in the Upstream Bioprocessing Market |

Thermo Fisher Scientific Inc., Sartorius AG, Merck KGaA, Danaher Corporation, Eppendorf SE, Lonza Group AG, Corning Incorporated, Avantor, Inc., Getinge AB, Repligen Corporation, FUJIFILM Irvine Scientific, Inc., PBS Biotech, Inc., Hamilton Company, Entegris, Inc., Meissner Filtration Products, Inc., Applikon Biotechnology B.V., Kühner AG, Cellexus International Ltd., GE HealthCare Technologies Inc., AGC Biologics, and others. |

|

Upstream Bioprocessing Market Segments |

by Product, by Workflow, by Use-Type, by Mode, by End-Users, and by Geography |

|

Upstream Bioprocessing Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Upstream Bioprocessing Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Upstream Bioprocessing Market Segmentation

- Upstream Bioprocessing by Product Exposure

- Instruments/Equipment

- Bioreactors & Fermenters

- Cell Culture Systems

- Filtration Systems

- Others

- Consumables & Accessories

- Software

- Services

- Instruments/Equipment

- Upstream Bioprocessing by Workflow Exposure

- Cell Line Development

- Media Preparation

- Cell Culture/Fermentation

- Others

- Upstream Bioprocessing Use-Type Exposure

- Single-use

- Multi-use

- Upstream Bioprocessing Mode Exposure

- In-house

- Outsourced

- Upstream Bioprocessing End-Users Exposure

- Biopharma & Biotech Companies

- Contract Development and Manufacturing Organizations (CDMOs)

- Academic & Research Institutes

Upstream Bioprocessing Geography Exposure

- North America Upstream Bioprocessing Market

- United States Upstream Bioprocessing Market

- Canada Upstream Bioprocessing Market

- Mexico Upstream Bioprocessing Market

- Europe Upstream Bioprocessing Market

- United Kingdom Upstream Bioprocessing Market

- Germany Upstream Bioprocessing Market

- France Upstream Bioprocessing Market

- Italy Upstream Bioprocessing Market

- Spain Upstream Bioprocessing Market

- Rest of Europe Upstream Bioprocessing Market

- Asia-Pacific Upstream Bioprocessing Market

- China Upstream Bioprocessing Market

- Japan Upstream Bioprocessing Market

- India Upstream Bioprocessing Market

- Australia Upstream Bioprocessing Market

- South Korea Upstream Bioprocessing Market

- Rest of Asia-Pacific Upstream Bioprocessing Market

- Rest of the World Upstream Bioprocessing Market

- South America Upstream Bioprocessing Market

- Middle East Upstream Bioprocessing Market

- Africa Upstream Bioprocessing Market

Upstream Bioprocessing Market Recent Industry Trends and Milestones (2023-2026):

|

Category |

Key Developments |

|

Upstream Bioprocessing Product Expansion |

Thermo Fisher Scientific Inc. announced the expansion of its bioprocess design center in India, and MilliporeSigma (Merck KGaA) expanded its bioprocessing production capabilities in Europe to support growing demand for cell culture media and biologics manufacturing. |

|

Upstream Bioprocessing Product Acquisition |

Thermo Fisher Scientific announced the acquisition of Solventum’s purification and filtration business. |

|

Upstream Bioprocessing Product Launch |

Thermo Fisher Scientific Inc. introduced new CDMO and CRO services and expanded manufacturing operations to support biologics, cell therapies, and gene therapy production. |

|

Company Strategy |

Danaher Corporation

Sartorius AG · Focus on modular and flexible upstream bioprocessing systems (especially single-use bioreactors) · Strong push toward automation and process analytics (PAT tools) for real-time monitoring · Expansion of bioreactor and filtration capacity to meet rising biologics demand · Strategic investment in digital bioprocessing and AI-enabled process optimization · Aggressive global expansion, especially in North America and the Asia-Pacific region. |

|

Emerging Technology |

Single-Use Bioreactor (SUB) Advancements, Process Analytical Technology (PAT) & Real-Time Monitoring, Artificial Intelligence (AI) & Machine Learning Integration, Continuous Bioprocessing & Perfusion Systems, and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are increasingly transforming upstream bioprocessing by enabling smarter, faster, and more consistent biomanufacturing processes. In upstream workflows such as cell line development, media optimization, and cell culture/fermentation, artificial intelligence (AI) and machine learning (ML) are being used to predict optimal growth conditions, improve yield, and reduce process variability. AI-driven predictive models analyze large datasets from bioreactors, such as pH, dissolved oxygen, glucose consumption, and metabolite accumulation, to optimize feeding strategies and detect deviations in real time. One of the most important applications is in digital twins of bioreactors, where virtual models simulate cell culture behavior to reduce experimental cycles and accelerate process development. AI is also widely used in cell line development, where algorithms screen and select high-producing clones more efficiently than traditional manual methods, significantly shortening development timelines for monoclonal antibodies and recombinant proteins. Additionally, automated bioprocess control systems powered by AI enable real-time adjustments in perfusion and fed-batch systems, improving product consistency and scalability. Companies such as Sartorius, Cytiva (Danaher), and Thermo Fisher Scientific are integrating AI-based analytics into their bioprocess platforms to enhance upstream productivity and support continuous biomanufacturing. Overall, AI is shifting upstream bioprocessing from an experience-based discipline to a data-driven, predictive, and highly automated manufacturing ecosystem, improving both efficiency and commercial scalability.

U.S. Tariff Impact Analysis on Upstream Bioprocessing Market:

The U.S. tariff impact on the upstream bioprocessing market is primarily reflected through higher production costs, supply chain disruptions, and increased pricing pressure on bioprocessing equipment and consumables. Since upstream bioprocessing relies heavily on imported inputs such as bioreactors, single-use systems, chromatography resins, cell culture media, reagents, and specialized fermentation components, tariffs on pharmaceutical and life science imports increase the overall cost base for biopharma companies and CDMOs. This leads to higher capital expenditure (CapEx) for new biomanufacturing facilities and increased operational expenditure (OpEx) for ongoing cell culture and fermentation processes, which can slow down expansion plans or shift sourcing strategies toward domestic suppliers.

According to industry analyses, tariffs on life science imports could significantly reshape sourcing patterns and may force companies to restructure global supply chains, localize manufacturing in the U.S., or negotiate long-term supplier contracts to mitigate cost volatility. At the same time, tariffs are accelerating onshoring of biomanufacturing capacity, which indirectly boosts demand for upstream equipment such as fermenters, single-use bioreactors, and process control systems within the U.S. market as companies invest in domestic production infrastructure. However, this transition also creates short-term cost inflation and procurement delays due to limited domestic capacity for certain high-end bioprocessing components.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Key takeaways from the upstream bioprocessing market report study

- Market size analysis for the current upstream bioprocessing market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the upstream bioprocessing market.

- Various opportunities available for the other competitors in the upstream bioprocessing market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current upstream bioprocessing market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the upstream bioprocessing market growth in the future.

Startup Funding & Investment Trends:

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Enduro Genetics (Denmark) |

€12 million |

Series A |

Cell programming platform for microbial bioproduction |

Increases fermentation yield, reduces production cost, and improves scalability in biomanufacturing |

Frequently Asked Questions for the Upstream Bioprocessing Market

1. What is the growth rate of the upstream bioprocessing market?

The upstream bioprocessing market is estimated to grow at a CAGR of 13.44% during the forecast period from 2026 to 2034.

2. What is the market size for upstream bioprocessing?

The global upstream bioprocessing market size is expected to increase from USD 26,820.10 million in 2025 to USD 83,061.31 million by 2034.

3. Which region has the highest share in the upstream bioprocessing market?

North America is expected to dominate the upstream bioprocessing market due to the strong presence of major biopharmaceutical and biotechnology companies, advanced biomanufacturing infrastructure, and increasing investments in biologics, vaccines, and cell & gene therapy production. The region benefits from high adoption of single-use bioprocessing technologies, continuous manufacturing systems, and automation platforms, along with significant research funding and favorable regulatory support. In addition, the growing presence of leading companies such as Thermo Fisher Scientific Inc., Danaher Corporation, Repligen Corporation, and Avantor, Inc. is further supporting regional market growth through continuous product innovation and manufacturing expansion.

4. What are the drivers for the upstream bioprocessing market?

The rising demand for biologics, rapid growth in cell & gene therapy manufacturing, and increasing vaccine production activities are collectively driving significant expansion in the upstream bioprocessing market. The growing use of monoclonal antibodies, recombinant proteins, and advanced therapeutics has increased the need for efficient cell culture systems, bioreactors, media, and fermentation technologies. At the same time, the expanding development of cell and gene therapies requires highly specialized upstream processing platforms for viral vector and cell expansion production. In addition, increasing global vaccine manufacturing activities and pandemic preparedness initiatives are accelerating investments in large-scale bioprocessing infrastructure. Together, these factors are boosting the adoption of single-use technologies, automation systems, and continuous bioprocessing solutions, thereby supporting overall market growth for companies such as Thermo Fisher Scientific Inc., Sartorius AG, and Danaher Corporation.

5. Who are the key players operating in the upstream bioprocessing market?

Some of the key market players operating in the upstream bioprocessing market include Thermo Fisher Scientific Inc., Sartorius AG, Merck KGaA, Danaher Corporation, Eppendorf SE, Lonza Group AG, Corning Incorporated, Avantor, Inc., Getinge AB, Repligen Corporation, FUJIFILM Irvine Scientific, Inc., PBS Biotech, Inc., Hamilton Company, Entegris, Inc., Meissner Filtration Products, Inc., Applikon Biotechnology B.V., Kühner AG, Cellexus International Ltd., GE HealthCare Technologies Inc., AGC Biologics, and others.