Cutaneous Lupus Erythematosus Market

Cutaneous Lupus Erythematosus (CLE) Insights and Trends

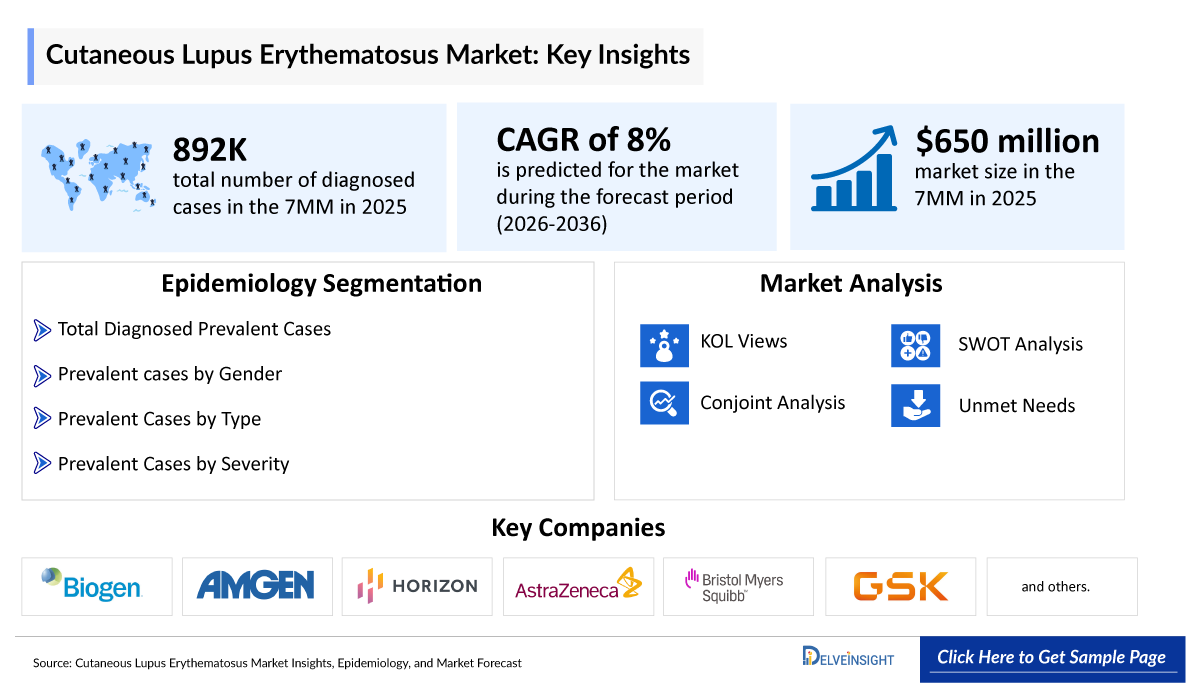

- According to DelveInsight’s analysis, Cutaneous Lupus Erythematosus market size was found to be ~USD 970 million in the leading markets (the United States, the EU4 (Germany, France, Italy, and Spain), the United Kingdom, and Japan) in 2025.

- Cutaneous Lupus Erythematosus is a chronic autoimmune skin disease comprising acute, subacute, and chronic subtypes, with discoid lupus erythematosus (DLE) being the most common; it predominantly affects women, may occur independently or with systemic lupus erythematosus (SLE), and remains underdiagnosed due to its heterogeneous clinical presentation and overlap with other inflammatory skin disorders, often resulting in diagnostic delays and suboptimal disease management.

- Cutaneous Lupus Erythematosus occurs in up to 70–80% of patients with SLE and is the initial manifestation in approximately 29%, making dermatologists key players in early detection, risk stratification, and co-management. DLE accounts for approximately 60–85% of Cutaneous Lupus Erythematosus cases, making it the dominant subtype worldwide.

- The CLASI (Cutaneous Lupus Erythematosus Disease Area and Severity Index) becomes the accepted primary endpoint in clinical trials, drug development is increasingly focusing on skin-specific outcomes.

- Current treatment strategies primarily rely on topical corticosteroids, calcineurin inhibitors, antimalarials, systemic corticosteroids, and broad immunosuppressive agents. However, treatment outcomes remain suboptimal, with many patients experiencing persistent disease activity.

- Japan's CLE treatment landscape changed markedly after hydroxychloroquine approval in 2015. Following decades of limited systemic options after chloroquine withdrawal due to retinal toxicity, hydroxychloroquine has become the preferred first-line systemic therapy, supported by insurance coverage.

- Emerging key players in CLE treatment includes Merck Healthcare KGaA (Enpatoran [M5049]), Biogen (Litifilimab [BIIB059]), AstraZeneca and BMS (Anifrolumab [SAPHNELO]), Ventus Therapeutics (VENT-03), DualityBio (DB-2304), and Gilead Sciences (Edecesertib [GS-5718]) among others.

- Litifilimab remains the most clinically advanced CLE-specific biologic, supported by positive clinical data, Food and Drug Administration (FDA) Breakthrough Therapy Designation (BTD), and a targeted Blood Dendritic Cell Antigen 2 (BDCA2) mechanism that modulates plasmacytoid dendritic cell-driven interferon production.

- CLE continues to be regarded as less clinically severe compared to SLE, which has historically deprioritized it in terms of therapeutic investment, guideline development, and reimbursement focus. The absence of dedicated CLE treatment guidelines, with clinicians instead relying on SLE-derived protocols, further reinforces the diagnosis and treatment gap.

- The termination of certain clinical programs and recruitment challenges observed within the CLE pipeline highlight the inherent development risks associated with novel immunology targets. Combined with limited long-term efficacy and safety data for several emerging assets, these uncertainties may delay innovation, increase development risk, and influence the pace of future market evolution.

Cutaneous Lupus Erythematosus (CLE) Market Size and Forecast in the 7MM

- 2025 CLE Market Size: ~970 million

- 2036 Projected CLE Market Size: ~4,300 million

- CLE Growth Rate (2026–2036): ~14.6% CAGR

DelveInsight's ‘Cutaneous Lupus Erythematosus (CLE) Market Insights, Epidemiology and Market Forecast – 2036’ report delivers an in-depth understanding of the CLE, historical and forecasted epidemiology, as well as the CLE market trends in the United States, EU4 (Germany, Spain, Italy, and France) and the United Kingdom, and Japan.

The Cutaneous Lupus Erythematosus market report delivers a comprehensive analysis of the current treatment landscape, including standards of care, clinical practices, and evolving therapeutic algorithms. It evaluates CLE patient burden trends, revenue & market share dynamics, peak patient share & therapy uptake analysis, and provides an in-depth market size assessment, and growth rate projections (Historical & Forecast 2022–2036) across global regions. The report highlights key unmet medical needs in CLE and maps the competitive and clinical landscape to uncover high-value opportunities, providing a clear outlook on future market growth potential.

|

Study Period |

2022–2036 |

|

Historical Year |

2022–2025 |

|

Forecast Period |

2026–2036 |

|

Base Year |

2026 |

|

Geographies Covered |

|

|

Cutaneous Lupus Erythematosus (CLE) Market CAGR (Forecast period) |

~14.6% (2026–2036) |

|

Cutaneous Lupus Erythematosus (CLE) Epidemiology Segmentation Analysis |

Patient Burden Assessment

|

|

Cutaneous Lupus Erythematosus (CLE) Companies |

|

|

Cutaneous Lupus Erythematosus (CLE) Therapies |

|

|

Cutaneous Lupus Erythematosus (CLE) Market |

Segmented by

|

|

Analysis |

|

Key Factors Driving the Cutaneous Lupus Erythematosus (CLE) Market

High Unmet Need for Effective and Approved Therapies

Current CLE management largely depends on off-label therapies and demonstrate variable efficacy with safety concerns during long-term use. The absence of multiple approved disease-specific therapies creates significant opportunities for novel agents capable of delivering durable skin clearance with improved tolerability.

Expanding Clinical Development Pipeline

The CLE pipeline has expanded considerably, with multiple investigational therapies progressing through clinical development. Novel monoclonal antibodies, immune modulators, kinase inhibitors, and other targeted therapies are being evaluated to address patients who remain refractory to conventional treatments. Positive clinical trial outcomes and potential regulatory approvals are anticipated to accelerate market growth.

Cutaneous Lupus Erythematosus (CLE) Understanding and Treatment Algorithm

Cutaneous Lupus Erythematosus (CLE) Overview and Diagnosis

CLE is a chronic autoimmune inflammatory skin disorder characterized by immune-mediated damage to the skin, resulting in photosensitive lesions that may lead to scarring, dyspigmentation, and permanent alopecia depending on the disease subtype. CLE encompasses a spectrum of clinical presentations, including acute (ACLE), subacute (SCLE), and chronic forms (CCLE), with Discoid Lupus Erythematosus (DLE) being the most common chronic subtype. While some patients have disease confined to the skin, others may develop or coexist with SLE. The pathogenesis involves a complex interplay of genetic susceptibility, ultraviolet (UV) radiation, environmental triggers, and immune dysregulation, particularly activation of type I interferon signaling, autoreactive T and B lymphocytes, and pro-inflammatory cytokines. CLE significantly impacts patients' quality of life owing to visible skin lesions, chronic disease course, pain, pruritus, and psychosocial distress.

The diagnosis of CLE is based on a combination of clinical evaluation, histopathological examination, and laboratory investigations. Dermatological assessment focuses on lesion morphology, distribution, photosensitivity, and evidence of scarring or pigmentary changes. Confirmation is typically obtained through skin biopsy, which demonstrates interface dermatitis and other characteristic histological features, while direct immunofluorescence may reveal immunoglobulin and complement deposition at the dermoepidermal junction. Laboratory investigations include antinuclear antibody (ANA) testing, anti-double-stranded DNA antibodies, anti-Ro/SSA and anti-La/SSB antibodies, complement levels, and other autoimmune markers to evaluate systemic involvement. Disease severity and treatment response are commonly monitored using validated scoring tools such as the CLASI, while patients are periodically assessed for progression to systemic lupus.

Further details are provided in the report....

Current Cutaneous Lupus Erythematosus (CLE) Treatment Landscape

Management of CLE aims to suppress cutaneous inflammation, prevent disease flares, minimize irreversible skin damage, and improve quality of life. Non-pharmacological measures, including strict photoprotection, sunscreen use, smoking cessation, and avoidance of known triggers, form the foundation of therapy. Mild localized disease is generally treated with topical corticosteroids or topical calcineurin inhibitors, whereas patients with extensive or refractory disease often require systemic treatment. Antimalarial agents, particularly hydroxychloroquine, remain the first-line systemic therapy, with other immunomodulatory agents and short courses of systemic corticosteroids reserved for more severe disease. The therapeutic landscape is evolving with the development of targeted biologics and small molecules that inhibit type I interferon signaling, B-cell activation, and other immune pathways, offering the potential for more effective and steroid-sparing treatment options for patients with moderate-to-severe or treatment-resistant CLE.

Further details related to country-based variations are provided in the report.

Cutaneous Lupus Erythematosus (CLE) Unmet Needs

The section “unmet needs of CLE” outlines the critical gaps between the current state of patient care, diagnosis, and the ideal & effective management of the disease. It highlights the obstacles experienced by patients, clinicians, and researchers and identifies potential solutions for future progress.

- Lack of approved targeted therapies

- Clinical heterogeneity and diagnostic complexity in cle

- Persistent symptoms and flares despite treatment in cle

- Irreversible skin damage and side effects of existing cle treatments, and others…..

Note: Comprehensive unmet needs insights in CLE and their strategic implications are provided in the full report.

Cutaneous Lupus Erythematosus (CLE) Epidemiology

Key Findings from CLE Epidemiological Analysis and Forecast

- Among the 7MM, the US accounted for the highest number of cases of Cutaneous Lupus Erythematosus in 2025, with ~390,500 cases. These cases are anticipated to increase by 2036.

- According to DelveInsight’s analysis, the total treated cases of CLE by line of therapy were highest in first line in US in 2025 with ~273,400 cases.

- Among the EU4 and the UK, Spain (~30%) accounted for the highest diagnosed prevalent cases of CLE in 2025 followed by UK. The lowest number of cases were seen in Italy.

- In the United States, among the type-specific cases of CLE reported in 2025, CCLE had the highest number, with ~247,600 cases followed by SCLE.

- In Spain, among the severity-specific cases, mild (~55) accounted for the highest number of cases followed by moderate and severe in 2025.

- Across the 7MM, the gender-specific distribution of CLE cases was higher among females than males in 2025.

Cutaneous Lupus Erythematosus (CLE) Drug Analysis & Competitive Landscape

The Cutaneous Lupus Erythematosus drug chapter provides a detailed, market-focused review of the emerging pipeline across Phase III/II clinical trials and preclinical trials. It covers the mechanism of action, clinical trial data, regulatory approvals, patents, collaborations, and strategic partnerships for each therapy, along with their advantages, limitations, and recent developments. This section offers critical insights into the CLE treatment landscape, supporting market assessment, competitive analysis, and growth forecasting for the CLE therapeutics market.

Cutaneous Lupus Erythematosus (CLE) Pipeline Analysis

Enpatoran (M5049): Merck Healthcare KGaA

Enpatoran is an investigational, highly specific, potential first-in-class immune modulator. It aims to overcome the limitations of currently available lupus therapies by providing selective inhibition of Toll-Like Receptors 7 and 8 (TLR7/8), which are known as key lupus-relevant disease drivers. It is currently being investigated in a Phase III trial.

Litifilimab (BIIB059): Biogen

Litifilimab is a humanized IgG1 monoclonal antibody targeting BDCA2 and is being investigated for the potential treatment of CLE. Litifilimab is a first-in-class therapy targeting BDCA2 in CLE. Litifilimab's second positive Phase II CLE dataset showed a meaningful reduction of disease activity in people living with CLE.

|

Competitive Landscape of Pipeline Drugs | ||||||

|

Drug Name |

Company |

Highest Phase |

Indication |

RoA |

MoA |

Anticipated Launch in the US |

|

Litifilimab (BIIB059) |

Biogen |

III |

CLE |

SC |

Anti-BDCA2 |

2028 |

|

Enpatoran (M5049) |

Merck Healthcare KGaA |

III |

CLE |

Oral |

TLR7/8 antagonist |

Information is available in the full report |

|

Anifrolumab (SAPHNELO) |

AstraZeneca and BMS |

III |

CLE |

SC |

Type I IFN receptor antagonist |

Information is available in the full report |

|

VENT-03 |

Ventus Therapeutics |

II |

CLE |

Oral |

cGAS inhibitor |

Information is available in the full report |

|

Imeroprubart (IMVT-1402) |

Immunovant Sciences GmbH (Roivant) |

II |

CLE |

SC |

Anti-neonatal Fc receptor (FcRn) |

Information is available in the full report |

|

DB-2304 |

DualityBio |

II |

CLE |

IV/SC |

Anti-BDCA2 |

Information is available in the full report |

|

Daxdilimab (VIB7734/ HZN-7734 |

Amgen |

II |

DLE |

SC |

Target ILT7 |

Information is available in the full report |

|

RSLV-132 |

Resolve Therapeutics |

II |

Cutaneous manifestations in subjects with SLE |

IV infusion |

B-cell inhibitor, Interferon alpha inhibitors |

Information is available in the full report |

|

Note: Launch insights are provisional and may change with future report updates or the occurrence of major key catalysts. | ||||||

Cutaneous Lupus Erythematosus (CLE) Key Players, Market Leaders and Emerging Companies

- Merck Healthcare KGaA

- Biogen

- AstraZeneca

- BMS

- Ventus Therapeutics

- Immunovant Sciences GmbH

- DualityBio

- Amgen

- Resolve Therapeutics, and others

Cutaneous Lupus Erythematosus (CLE) Drug Updates

- Biogen, in its 2025 annual report, anticipated that the Phase III AMETHYST study in CLE readout is expected in mid-year 2027.

- AstraZeneca in its Q1 2026 updates, anticipates data readout in 2027 of anifrolumab in CLE.

- In January 2026, Biogen announced that the US FDA has granted BTD for litifilimab for the treatment of CLE. The designation is based on the available litifilimab data, including the Phase II LILAC study.

- In December 2025, Ventus Therapeutics announced that top-line data from the 28-day placebo-controlled portion of the trial is expected in 2H of 2026, with data from the 2-month open-label extension to follow.

- In May 2026, Immunovant, in its corporate overview, anticipated proof-of-concept trial topline results expected in 2H 2026 of imeroprubart in CLE.

- In May 2026, according to Gilead Q1 2026 presentation, edecesertib Phase II (COSMIC) updates and new study FPI are expected in 2H of 2026.

Cutaneous Lupus Erythematosus (CLE) Market Outlook

The treatment landscape for Cutaneous Lupus Erythematosus is undergoing a gradual transition from a heavy reliance on conventional off-label immunosuppressive therapies toward targeted immunomodulatory agents designed to address the underlying disease mechanisms.

Current management remains centered on photoprotection, topical corticosteroids, calcineurin inhibitors, antimalarials such as hydroxychloroquine, and systemic immunosuppressants including methotrexate, mycophenolate mofetil, azathioprine, dapsone, retinoids, and short-term corticosteroids. Although these therapies remain the standard of care, many patients experience inadequate or incomplete responses, frequent relapses, cumulative treatment-related toxicities, and prolonged corticosteroid exposure. The lack of multiple approved therapies specifically indicated for CLE highlights a substantial unmet need for safer, more effective, and durable treatment options.

Among the emerging therapies, enpatoran, litifilimab¸and anifrolumab represent some of the most promising pipeline candidates poised to transform the CLE treatment paradigm. Enpatoran is the most advanced candidate in the class, with Phase III development positioning it as a potential first-in-class. It aims to suppress innate immune activation and downstream type I interferon production, offering a novel oral targeted approach for autoimmune skin inflammation. Litifilimab Phase III development underway and BTD, highlighting its potential as a first-in-class targeted therapy for CLE. It selectively inhibits plasmacytoid dendritic cells, thereby reducing interferon-mediated inflammation that plays a central role in CLE pathogenesis. Anifrolumab, already approved for SLE, inhibits the type I interferon receptor and has demonstrated encouraging efficacy in improving cutaneous manifestations, positioning it as a strong candidate for expanded use in CLE.

Collectively, these mechanism-based therapies have the potential to reduce dependence on broad immunosuppression and chronic corticosteroid use while delivering improved efficacy, better safety profiles, and more durable disease control. If ongoing clinical studies continue to demonstrate positive outcomes and secure regulatory approvals, these next-generation immunotherapies are expected to significantly reshape the CLE market by establishing targeted therapies as the future standard of care for patients with moderate-to-severe or treatment-refractory disease.

Overall the launch and uptake of novel targeted therapies, increasing diagnosed patient population, greater adoption of biologics and advanced systemic treatments are expected to drive steady growth in the 7MM CLE market from 2022–2036, with strong commercial implications for both marketed products and emerging pipelines.

- Among the 7MM, the US accounted for the largest market size of CLE i.e., USD ~780 million in 2025.

- In 2036, among all the emerging therapies for CLE, the highest revenue is estimated to be generated by enpatoran followed by litifilimab, in the US.

- The entry of late-stage candidates such as enpatoran is expected to intensify competition in the CLE treatment landscape during the latter forecast period.

Further details will be provided in the report….

Drug Class/Insights into Leading Emerging and Marketed Therapies in CLE (2022–2036 Forecast)

The CLE market (2022–2036 forecast) emerging pipeline is primarily centered on innate immune pathway inhibitors and type I interferon-targeted biologics, reflecting the growing understanding of interferon-driven disease pathogenesis.

TLR 7/8 antagonist : Enpatoran is a first-in-class oral dual TLR7/8 antagonist designed to inhibit activation of the innate immune system. By blocking TLR7/8-mediated signaling, enpatoran suppresses the production of pro-inflammatory cytokines, particularly type I interferons, which play a central role in CLE pathogenesis.

Anti-BDCA2: Litifilimab is a humanized monoclonal antibody targeting BDCA2, a receptor selectively expressed on plasmacytoid dendritic cells (pDCs). Binding to BDCA2 inhibits pDC activation and markedly reduces type I interferon production, thereby interrupting one of the key inflammatory pathways driving skin lesions in CLE.

Type I Interferon Receptor (IFNAR1) Monoclonal Antibodies: Anifrolumab is a fully human monoclonal antibody directed against IFNAR1. By blocking signaling from all type I interferons, it suppresses downstream inflammatory responses responsible for keratinocyte injury and cutaneous inflammation in lupus.

CLE innovation is increasingly being driven by targeted immunomodulatory therapies that interrupt key pathogenic pathways, particularly the type I interferon axis, plasmacytoid dendritic cells, and TLR signaling.

Cutaneous Lupus Erythematosus (CLE) Drug Uptake

This section focuses on the uptake rate of potential drugs expected to be launched in the market during the forecast period (2026–2036). The analysis covers the CLE drug’s uptake, performance at peak, factors affecting performance during prime years of growth, patient uptake by therapy, and anticipated sales generated by each drug.

Among the emerging therapies for CLE, Litifilimab (BIIB059) is expected to achieve the strongest uptake if approved, supported by its first-in-class BDCA2-targeting mechanism, positive Phase II efficacy data, and FDA Breakthrough Therapy Designation (BTD). Enpatoran (M5049) and Deucravacitinib (SOTYKTU/BMS-986165) are also anticipated to experience medium-fast uptake, driven by their differentiated mechanisms of action, promising clinical efficacy, and potential to address significant unmet needs in moderate-to-severe CLE. Anifrolumab (SAPHNELO), Daxdilimab (VIB7734), and VENT-03 are expected to witness moderate uptake, supported by their clinical potential and growing physician confidence. In contrast, Imeroprubart (IMVT-1402) and Edecesertib (GS-5718) are projected to demonstrate slow-to-medium uptake, while RSLV-132 is anticipated to have the slowest uptake, primarily due to its comparatively earlier clinical development, the need for additional long-term efficacy and safety data, and increasing competition within the evolving CLE treatment landscape.

Detailed insights of emerging therapies' drug uptake is included in the report

Market Access and Reimbursement of Approved therapies in Cutaneous Lupus Erythematosus (CLE)

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of approved therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

Reimbursement is a crucial factor that affects the drug’s access to the market. Often, the decision to reimburse comes down to the price of the drug relative to the benefit it produces in treated patients. To reduce the healthcare burden of these high-cost therapies, many payment models are being considered by payers and other industry insiders.

NOTE: Further Details are provided in the final report….

Cutaneous Lupus Erythematosus (CLE) Therapies Price Scenario & Trends

Pricing and analogue assessment of CLE therapies highlights evolving price dynamics structures. This section summarizes the cost of approved treatments, closest and most appropriate analogue selection for emerging therapies, and understanding of how pricing influences market access, adherence, and long-term uptake.

Most of the assets under consideration for CLE are first-in-class molecules targeting novel pathways. Given their potential to address currently untapped markets and their eligibility for innovation-related pricing adjustments (e.g., breakthrough innovation, high clinical usefulness, orphan designation, where applicable), sponsors are likely to seek premium pricing at launch. To estimate launch-year pricing, an annual price growth rate of 3% was applied from the benchmark year through the anticipated launch year.

Industry Experts and Physician Views for Cutaneous Lupus Erythematosus (CLE)

To keep up with CLE market trends, we take Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) opinions working in the domain through primary research to fill the data gaps and validate our secondary research. Industry experts were contacted for insights on the CLE emerging therapies, evolving treatment landscape, patient adherence to conventional therapies, therapy switching trends, drug adoption and uptake, accessibility challenges, and epidemiology and real-world prescription patterns in CLE, including MD, PhD, Instructor, Postdoctoral Researcher, Professor, Researcher, and others.

DelveInsight’s analysts connected with 15+ KOLs to gather insights at the country level. Centers such as Perelman School of Medicine, Heinrich Heine University, and The University of Manchester etc. were contacted. Their opinion helps understand and validate current and emerging CLE therapies, highlight unmet medical needs, provide epidemiological context, and support strategic decisions for market access, therapy adoption, and pipeline prioritization in CLE.

|

Region |

Key Opinion Leaders (KOLs) and Subject Matter Experts (SMEs) |

|

United States |

“Based on current research and clinical data, CLE remains a highly underdiagnosed and misdiagnosed condition across global markets. The gap between prevalent cases (total people with the disease) and diagnosed cases (those identified in clinical claims) is a major focus for companies developing new targeted therapies.” |

|

Germany |

“CLE is associated with an increased risk of several systemic comorbidities, including hypertension, dyslipidemia, anxiety disorders, obesity, depression, and type 2 diabetes. Beyond health impacts, patients face rising insurance costs and out-of-pocket spending, which frequently leads to medical debt and delayed care.” |

Qualitative Analysis: SWOT and Conjoint Analysis

We perform qualitative and market Intelligence analysis using various approaches, such as SWOT analysis and conjoint analysis.

In the SWOT analysis of CLE, strengths, weaknesses, opportunities, and threats in terms of disease diagnosis, patient awareness, patient burden, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint analysis analyzes emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

The team of analysts analyzes promising emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. In efficacy, the trial’s primary and secondary outcome measures are evaluated, whereas the therapies’ safety is evaluated, wherein the acceptability, tolerability, and adverse events are majorly observed. In addition, the scoring is also based on the route of administration, order of entry, probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Scope of the Report

- The report covers a segment of key events, an executive summary, a descriptive overview of Cutaneous Lupus Erythematosus (CLE) explaining their causes, signs and symptoms, pathogenesis, and currently available treatments.

- Comprehensive insight has been provided into the epidemiology segments and forecasts, the future growth potential of the diagnosis rate, and disease progression along treatment guidelines.

- Additionally, an all-inclusive account of both the current and emerging treatments, along with the elaborative profiles of late-stage and prominent therapies, will have an impact on the current treatment landscape.

- A detailed review of the Cutaneous Lupus Erythematosus (CLE) market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The report provides an edge while developing business strategies by understanding trends through SWOT analysis and expert insights/KOL views, patient journey, and treatment preferences that help in shaping and driving the 7MM Cutaneous Lupus Erythematosus (CLE) market.

Report Insights

- Cutaneous Lupus Erythematosus (CLE) Patient Population Forecast

- Cutaneous Lupus Erythematosus (CLE) Therapeutics Market Size

- Cutaneous Lupus Erythematosus (CLE) Pipeline Analysis

- Cutaneous Lupus Erythematosus (CLE) Market Size and Trends

- Cutaneous Lupus Erythematosus (CLE) Market Opportunity (Current and Forecasted)

Report Key Strengths

- Epidemiology-based (Epi-based) Bottom-up Forecasting

- Artificial Intelligence (AI)-Enabled Market Research Report

- 11-Year Forecast

- Cutaneous Lupus Erythematosus (CLE) Market Outlook (North America, Europe, Asia-Pacific)

- Patient Burden Trends (By Geography)

- Cutaneous Lupus Erythematosus (CLE) Treatment Addressable Market (TAM)

- Cutaneous Lupus Erythematosus (CLE) Competitve Landscape

- Cutaneous Lupus Erythematosus (CLE)) Major Companies Insights

- Cutaneous Lupus Erythematosus (CLE) Price Trends and Analogue Assessment

- Cutaneous Lupus Erythematosus (CLE) Therapies Drug Adoption/Uptake

- Cutaneous Lupus Erythematosus (CLE) Therapies Peak Patient Share Analysis

Report Assessment

- Cutaneous Lupus Erythematosus (CLE) Current Treatment Practices

- Cutaneous Lupus Erythematosus (CLE) Unmet Needs

- Cutaneous Lupus Erythematosus (CLE) Clinical Development Analysis

- Cutaneous Lupus Erythematosus (CLE) Emerging Drugs Product Profiles

- Cutaneous Lupus Erythematosus (CLE) Market attractiveness

- Cutaneous Lupus Erythematosus (CLE) Qualitative Analysis (SWOT and Conjoint Analysis)

FAQs

Market Insights

- What was the Cutaneous Lupus Erythematosus (CLE) market size, the market size by therapies, market share (%) distribution in 2025, and what would it look like by 2036? What are the contributing factors for this growth?

- What are the anticipated pricing variations among different geographies for the emerging therapies in the future?

- What can be the future treatment paradigm of Cutaneous Lupus Erythematosus (CLE)?

- What are the disease risks, burdens, and unmet needs of Cutaneous Lupus Erythematosus (CLE)? What will be the growth opportunities across the 7MM concerning the patient population with Cutaneous Lupus Erythematosus (CLE)?

- Who is the major future competitor in the market, and how will the competitors affect their market share?

- What are the current options for the treatment of Cutaneous Lupus Erythematosus (CLE)? What are the current guidelines for treating CLE in the US, Europe, and Japan?

Reasons to Buy

- The report will help in developing business strategies by understanding the latest trends and changing treatment dynamics driving the Cutaneous Lupus Erythematosus (CLE) market.

- Bottom up forecasting builds from the affected population to product forecasts, delivering a robust, data driven approach ideal for new therapies and novel classes.

- Insights on patient burden/disease incidence, evolution in diagnosis, and factors contributing to the change in the epidemiology of the disease during the forecast years.

- Understand the existing market opportunities in varying geographies and the growth potential over the coming years.

- Identifying strong upcoming players in the market will help devise strategies to help get ahead of competitors.

- Detailed analysis and ranking of class-wise potential emerging therapies under the conjoint analysis section to provide visibility around leading classes.

- To understand KOLs’ perspectives on the accessibility, acceptability, and compliance-related challenges of existing treatment to overcome barriers in the future.

- Detailed insights on the unmet needs of the existing market so that the upcoming players can strengthen their development and launch strategy.

- This Artificial Intelligence (AI) enabled report summarize and simplify complex datasets with in the report into clear, actionable insights for stakeholders, investors, and healthcare providers, enabling faster, data driven decisions.

-pipeline.png&w=256&q=75)