DNA Diagnostics Market Summary

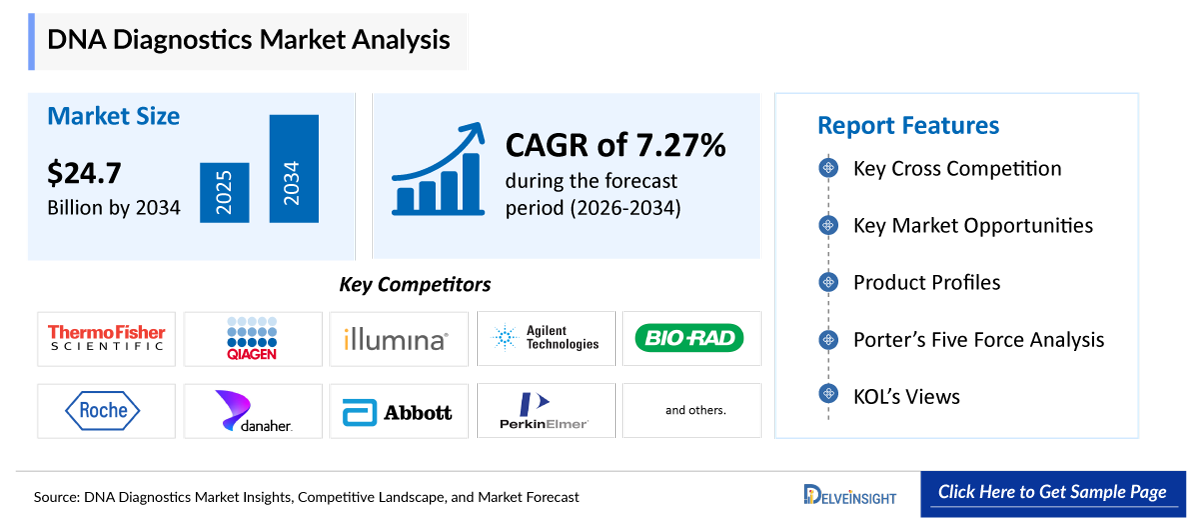

- The Global DNA Diagnostics Market Size is expected to increase from USD 13,219.91 million in 2025 to USD 24,777.44 million by 2034, reflecting strong and sustained growth.

- The Global DNA Diagnostics Market Size is growing at a CAGR of 7.27% during the forecast period from 2026 to 2034.

DNA Diagnostics Market Size and Forecasts

- The DNA diagnostics Market is being strongly driven by the combined impact of rising disease burden, expanding screening programs, and rapid technological advancements. The increasing prevalence of genetic disorders, infectious diseases, and chronic conditions such as cancer has created a growing need for accurate and early diagnostic solutions, where techniques like Polymerase Chain Reaction and Next-Generation Sequencing play a crucial role. At the same time, the expansion of prenatal and newborn screening programs is boosting the routine adoption of DNA-based tests for early detection of abnormalities.

- These trends are further amplified by continuous advancements in molecular technologies, which have improved speed, accuracy, and cost-efficiency, making DNA diagnostics more accessible across clinical and consumer settings. Collectively, these factors are accelerating market growth by increasing demand, broadening applications, and enhancing the overall adoption of DNA diagnostic solutions globally.

- The leading DNA Diagnostics Companies include Thermo Fisher Scientific Inc., QIAGEN N.V., Illumina, Inc., Agilent Technologies, Inc., Bio-Rad Laboratories, Inc., Roche Diagnostics International AG, Danaher Corporation, Abbott Laboratories, PerkinElmer, Inc., Promega Corporation, Eurofins Scientific SE, Myriad Genetics, Inc., Invitae Corporation, Natera, Inc., Fulgent Genetics, Inc., BGI Genomics Co., Ltd., Takara Bio Inc., New England Biolabs, Inc., Zymo Research Corporation, and others.

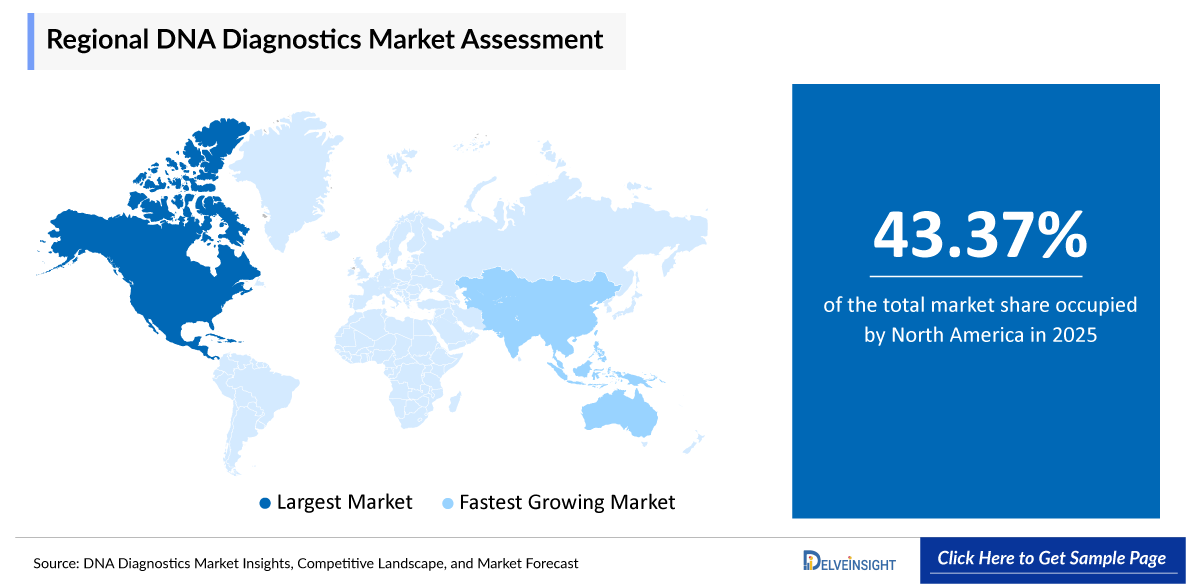

- North America is expected to dominate the DNA diagnostics market due to its highly advanced healthcare infrastructure, strong presence of leading biotechnology and diagnostics companies, and rapid adoption of innovative technologies such as Next-Generation Sequencing and Polymerase Chain Reaction. The region also benefits from significant government funding for genomics research, high awareness regarding early disease detection, and a well-established regulatory framework that supports the commercialization of advanced diagnostic solutions.

- Additionally, the rising prevalence of chronic and genetic diseases, along with increasing demand for personalized medicine, further strengthens market growth in North America.

- In the product & services segment of the DNA diagnostics market, the reagents & kits category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ DNA Diagnostics Market Insights

DNA Diagnostics Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 13,219.91 million |

|

2034 Projected Market Size |

USD 24,777.44 million |

|

Growth Rate (2026-2034) |

7.27% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Key Factors Contributing to the Growth of the DNA Diagnostics Market

-

Rising prevalence of genetic, infectious, and chronic diseases leading to a surge in DNA diagnostics

The increasing incidence of genetic disorders, cancer, cardiovascular diseases, infectious diseases, and rare diseases is a major growth driver. DNA diagnostics enables early detection and precise identification of mutations, which is critical for effective treatment. In oncology, especially, genetic profiling has become standard practice.

-

Expansion of prenatal and newborn screening

Non-invasive prenatal testing (NIPT) and newborn genetic screening are gaining widespread adoption. These tests help detect chromosomal abnormalities early, leading to better clinical decision-making and improved healthcare outcomes.

-

Growing adoption of advanced technologies

Rapid advancements in technologies such as Next-Generation Sequencing and Polymerase Chain Reaction have significantly improved speed, accuracy, and scalability. These innovations are making DNA testing more accessible and cost-effective, thereby expanding market adoption.

What are the latest DNA Diagnostics Market Dynamics and Trends?

The rising burden of cancer, genetic disorders, and infectious diseases worldwide is significantly boosting the overall DNA Diagnostics market. Cancer is a major driver of the DNA diagnostics market due to the growing need for precision oncology and early detection.

According to the data provided by the British Heart Foundation (2026), approximately 650 million people were living with cardiovascular disease across the world. DNA-based testing enables identification of genetic mutations, tumor biomarkers, and hereditary cancer risks, allowing clinicians to select targeted therapies and monitor disease progression. Techniques such as Next-Generation Sequencing and Polymerase Chain Reaction are widely used for tumor profiling and liquid biopsy, improving treatment outcomes.

Furthermore, Sepsis is boosting the DNA diagnostics market by creating a strong demand for rapid and accurate pathogen identification. According to the World Sepsis Day Organization (2025), around 47 to 50 million cases of sepsis occur each year across the world. Traditional diagnostic methods often take time, whereas DNA-based tests can quickly detect the presence of bacterial or fungal DNA in the bloodstream, enabling early and targeted treatment.

Fast diagnosis is critical in sepsis management, as delays can lead to severe complications or death. The adoption of molecular techniques like Polymerase Chain Reaction is enhancing diagnostic speed and sensitivity, thereby driving the use of DNA diagnostics in critical care settings.

Additionally, Tuberculosis is contributing to market growth due to the need for accurate detection and identification of drug-resistant strains. According to the World Health Organization (2026), in 2024, an estimated 10.7 million people fell ill with TB worldwide. DNA diagnostics allow rapid detection of Mycobacterium tuberculosis and its resistance patterns, which are essential for effective treatment planning. Molecular diagnostic tools, especially Polymerase Chain Reaction, are increasingly replacing conventional methods because of their higher accuracy and faster turnaround time.

With the continued global burden of tuberculosis, particularly in developing regions, the demand for reliable DNA-based diagnostic solutions is steadily increasing. Furthermore, the expansion of prenatal and newborn screening is significantly boosting the DNA diagnostics market by increasing the routine adoption of genetic testing at early life stages.

Modern screening methods, particularly non-invasive prenatal testing (NIPT), allow early detection of chromosomal abnormalities such as Down syndrome using simple maternal blood samples, making testing safer and more widely accepted. This shift toward preventive healthcare is driving higher testing volumes globally.

Recent Developments further highlight this growth

In October 2023, the Indian Council of Medical Research (ICMR) launched a national initiative to promote NIPT and improve maternal–fetal health outcomes, while in March 2025, Sysmex introduced an AI-integrated microarray-based prenatal screening platform to enhance detection accuracy. Additionally, the increasing product development activities and government initiatives are further boosting the overall market of DNA diagnostics.

For instance, in March 2026, Co-Diagnostics, Inc. announced the expanded commercialization of PCR-based DNA diagnostic products (PCR Pro®, SARAGENE®) across South Asia markets, targeting a $13 billion market across Bangladesh, Pakistan, Nepal, and Sri Lanka.

Thus, the factors mentioned above are expected to boost the overall market of DNA diagnostics during the forecast period.

However, the ethical and privacy concerns, along with the risk of false positives and false negatives, are key limiting factors for the DNA diagnostics market. The handling of sensitive genetic data raises serious issues around data security, consent, and potential misuse, which can reduce patient trust and slow adoption, especially in regions with weak regulatory frameworks.

At the same time, although technologies like Polymerase Chain Reaction and Next-Generation Sequencing offer high accuracy, the possibility of incorrect results can lead to misdiagnosis, unnecessary treatments, or missed conditions. These risks increase hesitation among healthcare providers and patients, thereby restraining the widespread adoption and growth of DNA diagnostic solutions.

DNA Diagnostics Market Report Segmentation

This DNA diagnostics market report offers a comprehensive overview of the global DNA diagnostics market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Products & Services (Instruments, Reagents & Kits, and Software & Services), Technology (Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), and Others), Application (Infectious Disease Diagnostics, Cancer Genetic Diagnostics, Prenatal Testing, and Others), End-Users (Hospitals & Diagnostic Laboratories, Research Institutes & Academic Centers, and Others), and geography.

The DNA Diagnostics market report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing DNA diagnostics market.

DNA diagnostics is a method of identifying diseases or health conditions by analyzing an individual’s genetic material (DNA). It involves detecting specific gene mutations, variations, or pathogen DNA using techniques such as Polymerase Chain Reaction and Next-Generation Sequencing. This approach enables early, accurate diagnosis of genetic disorders, cancers, and infectious diseases, and supports personalized treatment decisions in modern healthcare.

The DNA diagnostics market is being strongly driven by the combined impact of rising disease burden, expanding screening programs, and rapid technological advancements. The increasing prevalence of genetic disorders, infectious diseases, and chronic conditions such as cancer has created a growing need for highly accurate, early-stage diagnostic solutions, where techniques like Polymerase Chain Reaction and Next-Generation Sequencing play a crucial role by enabling precise detection of genetic mutations and pathogens. At the same time, the expansion of prenatal and newborn screening programs is significantly boosting the routine adoption of DNA-based tests, as these allow early identification of chromosomal abnormalities and inherited conditions, improving clinical outcomes and reducing long-term healthcare costs.

In addition, continuous advancements in molecular technologies, automation, and bioinformatics have enhanced the speed, sensitivity, and scalability of DNA testing while steadily reducing costs, making these diagnostics more accessible not only in advanced hospitals and laboratories but also in emerging markets and even direct-to-consumer settings. The integration of AI-driven data analysis further strengthens interpretation accuracy and supports personalized treatment decisions. Collectively, these factors are accelerating market growth by increasing testing volumes, expanding applications across oncology, infectious diseases, and preventive healthcare, and driving widespread adoption of DNA diagnostic solutions globally.

Get More Insights into the Report @ DNA Diagnostics Market Trends

DNA Diagnostics Market Segment Analysis

DNA Diagnostics Market by Products & Services (Instruments, Reagents & Kits, and Software & Services), Technology (Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), and Others), Application (Infectious Disease Diagnostics, Cancer Genetic Diagnostics, Prenatal Testing, and Others), End-Users (Hospitals & Diagnostic Laboratories, Research Institutes & Academic Centers, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

-

DNA Diagnostics Market Segmentation By Product & Services

Reagents & Kits in DNA diagnostics are expected to dominate the market with the largest revenue share. In the product & services segment of the DNA diagnostics market, the reagents & kits category is contributing to 61.76% of total market revenue in 2025, due to its recurring demand, wide applicability, and essential role in every diagnostic workflow. Unlike instruments, which are one-time capital investments, reagents and kits are consumables that must be continuously purchased for each test, ensuring a steady revenue stream for manufacturers.

These include PCR reagents, sequencing kits, sample preparation kits, and extraction kits that are critical for techniques such as Polymerase Chain Reaction and Next-Generation Sequencing. The growing volume of diagnostic testing, driven by rising cases of cancer, infectious diseases, and genetic disorders, has led to increased consumption of these products across hospitals, diagnostic laboratories, and research institutes. Additionally, continuous innovation in ready-to-use, high-sensitivity, and rapid testing kits is improving efficiency and reducing turnaround time, further accelerating adoption.

The expansion of decentralized and point-of-care testing, along with increasing use in emerging markets, is also fueling demand for affordable and easy-to-use kits. Collectively, these factors make reagents & kits the largest and fastest-growing segment within the DNA diagnostics market.

Additionally, the increasing product development activities are further escalating the overall market of the reagents & kits category in the DNA diagnostics market. For instance, in February 2026, New England Biolabs (NEB) launched the Monarch® Mag Cell-free DNA (cfDNA) Extraction Kit, offering a magnetic bead-based, scalable, and reproducible method for isolating cfDNA from biofluids. The kit facilitates efficient, high-yield extraction for biomarker analysis and supports automation, catering to challenging samples with input volumes of 1-4 ml.

As a result, the reagents & kits segment not only supports the adoption of DNA diagnostics but also acts as a key revenue generator, thereby significantly boosting the overall growth of the DNA diagnostics market.

-

DNA Diagnostics Market Segmentation By TechnologyThe

Polymerase Chain Reaction (PCR) category dominates the market. Within the technology segment of the DNA diagnostics market, the Polymerase Chain Reaction (PCR) category is anticipated to dominate, accounting for around 51.34% of the market share in 2025, due to its high sensitivity, rapid turnaround time, and cost-effectiveness compared to other advanced technologies.

PCR is widely used for detecting infectious diseases, genetic mutations, and cancer biomarkers because it can amplify even minute amounts of DNA, enabling early and accurate diagnosis. Its strong adoption across hospitals, diagnostic laboratories, and point-of-care settings further strengthens its market position. Additionally, the availability of a wide range of ready-to-use reagents and kits, along with continuous advancements such as real-time PCR and digital PCR, has enhanced its efficiency and scalability.

Compared to more complex and expensive methods like Next-Generation Sequencing, PCR remains more accessible, especially in emerging markets, thereby driving its widespread use and dominance in the DNA diagnostics market. Additionally, the increase in product development activities is further escalating the overall market. For instance, in January 2025, Thermo Fisher Scientific received FDA 510(k) clearance for the Applied BioSystems TaqPath COVID-19 diagnostic PCR kit.

Thus, the factors mentioned above are expected to boost the market of the category and thereby boost the overall DNA diagnostics market.

-

DNA Diagnostics Market Segmentation By Application

The cancer genetic diagnostics category dominates the market. Within the application segment of the DNA diagnostics market, the cancer genetic diagnostics category is anticipated to dominate, accounting for around 29.87% of the market share in 2025, due to the rising global burden of cancer and the increasing shift toward precision oncology.

DNA-based testing plays a critical role in identifying tumor-specific mutations, enabling early detection, risk assessment, and selection of targeted therapies tailored to a patient’s genetic profile. Advanced technologies such as Next-Generation Sequencing and Polymerase Chain Reaction are widely used for tumor profiling, liquid biopsy, and monitoring treatment response, making them essential tools in modern cancer care. Additionally, the growing adoption of companion diagnostics, increasing awareness of hereditary cancers, and continuous advancements in genomic research are further driving demand.

Compared to other applications, cancer diagnostics generates higher testing volumes and clinical importance, thereby positioning it as the leading segment in the DNA diagnostics market. Additionally, the increase in product development activities is further escalating the overall market.

For instance, in November 2024, Illumina, Inc., a global leader in DNA sequencing and array-based technologies, announced that it will release TruSight™ Oncology 500 v2 (TSO 500 v2), a new version of its flagship cancer research assay to enable comprehensive genomic profiling (CGP).

Thus, the factors mentioned above are expected to boost the market of the category and thereby boost the overall DNA Diagnostics market.

-

DNA Diagnostics Market Segmentation By End-Users

The hospitals and diagnostic laboratories category dominates the market. In the end-users segment of the DNA diagnostics market, the hospitals & diagnostic laboratories category dominates due to their central role in conducting large volumes of routine and specialized testing. These facilities are equipped with advanced infrastructure, skilled professionals, and integrated workflows required for complex molecular diagnostics, enabling the widespread use of technologies such as Polymerase Chain Reaction and Next-Generation Sequencing.

Hospitals rely on DNA diagnostics for critical applications such as cancer profiling, infectious disease detection, and prenatal screening, while diagnostic laboratories handle high-throughput sample processing and offer cost-effective testing services. Additionally, increasing patient inflow, rising awareness of early disease detection, and the growing adoption of personalized medicine are further driving demand in these settings. Their ability to deliver accurate, timely, and scalable diagnostic services positions hospitals and diagnostic laboratories as the leading end users in the DNA diagnostics market.

DNA Diagnostics Market Regional Analysis

-

North America DNA Diagnostics Market Trends

North America is expected to account for the highest proportion of 43.37% of the DNA Diagnostics market in 2025, out of all regions. North America is expected to dominate the DNA diagnostics market due to its highly advanced healthcare infrastructure, strong presence of leading biotechnology and diagnostics companies, and rapid adoption of innovative technologies such as Next-Generation Sequencing and Polymerase Chain Reaction.

The region also benefits from significant government funding for genomics research, high awareness regarding early disease detection, and a well-established regulatory framework that supports the commercialization of advanced diagnostic solutions. Additionally, the rising prevalence of chronic and genetic diseases, along with increasing demand for personalized medicine, further strengthens market growth in North America.

According to the recent data provided by the American Cancer Society (2026), in 2026, approximately 2,114,850 new cancer cases are projected to occur in the United States.

Furthermore, according to the data provided by the Centre for Disease Control and Prevention (2026), each year, at least 1.7 million adults and more than 18,000 children in the U.S. develop sepsis. Additionally, as per the same source, in 2023, the United States reported 9,633 cases of tuberculosis disease.

Cancer, sepsis, and tuberculosis are collectively driving strong growth in the DNA diagnostics market by increasing the need for rapid, accurate, and early disease detection. In cancer, genetic profiling helps identify mutations and guide targeted therapies, making precision diagnostics essential. In sepsis, where early intervention is critical to survival, DNA-based tests enable fast identification of pathogens compared to traditional culture methods.

Similarly, in tuberculosis, molecular diagnostics improve detection accuracy, including drug-resistant strains, supporting timely treatment decisions. Technologies such as Polymerase Chain Reaction and Next-Generation Sequencing play a key role by offering high sensitivity and speed. Together, the rising global burden of these diseases and the demand for precise, time-efficient diagnostics are significantly accelerating the adoption and expansion of DNA diagnostic solutions.

However, the increase in product development activities among the key market players is further boosting the overall market. For instance, in October, 2025, GeneDx received FDA Breakthrough Device designation for its ExomeDx and GenomeDx tests, aiming to accelerate access to rapid, accurate diagnoses for rare, life-threatening genetic diseases.

Furthermore, the strategic mergers and acquisitions among the key market players across the region are further escalating the overall market. For instance, in March, 2026, Agilent Technologies, Inc. announced a definitive agreement to acquire Biocare Medical for $950 million in an all-cash deal. This strategic acquisition strengthens Agilent’s Life Sciences and Diagnostics Markets unit by adding specialized tissue diagnostics, immunohistochemistry (IHC), and molecular pathology products to its portfolio.

Collectively, these factors are expected to significantly drive the growth of the DNA diagnostics market in the U.S. throughout the forecast period of 2026 to 2034.

-

Europe DNA Diagnostics Market Trends

The DNA diagnostics market in Europe is witnessing strong and sustained growth due to the region’s well-established healthcare infrastructure, increasing focus on early disease detection, and rapid integration of advanced molecular technologies into clinical practice. Countries such as Germany, France, and the UK are heavily investing in genomic medicine, national screening programs, and precision oncology, which is significantly driving demand for DNA-based testing.

The widespread use of technologies like Polymerase Chain Reaction and Next-Generation Sequencing, along with strong reimbursement systems and regulatory support, is further accelerating adoption. Additionally, Europe’s emphasis on infectious disease surveillance and cancer diagnostics is contributing to consistent testing volumes across hospitals and diagnostic laboratories.

Recent developments further highlight this growth trajectory

For instance, in January 2026, QIAGEN N.V. announced the expansion of new DNA assay kits, including lentivirus detection and host-cell DNA analysis kits, to support advanced genomic applications and cell therapy workflows in Europe. Additionally, in February 2026, Integrated DNA Technologies introduced an expanded innovation roadmap for next-generation sequencing solutions, strengthening Europe’s capabilities in high-throughput genomic diagnostics.

Thus, the factors mentioned above are expected to boost the overall market of DNA diagnostics in Europe during the forecast period.

-

Asia-Pacific DNA Diagnostics Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the DNA diagnostics market due to its large and rapidly growing population, high burden of infectious and chronic diseases, and continuous expansion of healthcare infrastructure across countries such as China, India, Japan, and South Korea. Increasing government investments in genomics and precision medicine programs, along with rising awareness of early disease detection, are significantly boosting the adoption of advanced molecular diagnostics.

Technologies like Polymerase Chain Reaction and Next-Generation Sequencing are being widely integrated into clinical workflows due to their cost-effectiveness and scalability, especially for infectious disease testing and oncology applications.

Recent developments further support this growth trend

- In February 2026, Integrated DNA Technologies expanded its innovation roadmap for next-generation sequencing solutions, strengthening genomic capabilities across the Asia-Pacific.

- Furthermore, strong government-backed genome programs and precision medicine initiatives across countries like China, India, and Japan are driving large-scale adoption of sequencing technologies and DNA-based testing. Collectively, these factors, including rising disease burden, expanding healthcare access, technological advancements, and continuous product innovation, are positioning the Asia Pacific as one of the fastest-growing regions in the DNA diagnostics market.

Who are the major players in the DNA Diagnostics Market?

DNA Diagnostics Companies

- Thermo Fisher Scientific Inc.

- QIAGEN N.V.

- Illumina, Inc.

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- Roche Diagnostics

- Danaher Corporation

- Abbott Laboratories

- PerkinElmer, Inc.

- Promega Corporation

- Eurofins Scientific SE

- Myriad Genetics, Inc.

- Invitae Corporation

- Natera, Inc.

- Fulgent Genetics, Inc.

- BGI Genomics Co., Ltd.

- Takara Bio Inc.

- New England Biolabs, Inc.

- Zymo Research Corporation, and others

How is the competitive landscape shaping the DNA Diagnostics Market?

The competitive landscape of the DNA diagnostics market is highly dynamic and moderately consolidated, shaped by the strong presence of global leaders such as Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd., Illumina, Inc., and QIAGEN N.V., along with a growing number of emerging and niche players.

Competition in this market is driven less by price and more by technological innovation, product portfolio expansion, and clinical accuracy, with companies heavily investing in advanced platforms such as PCR and next-generation sequencing. Strategic initiatives such as mergers and acquisitions, partnerships, and continuous product launches are common, enabling companies to strengthen their capabilities, expand geographic reach, and access new technologies.

Additionally, the market is characterized by moderate concentration, where a few top players hold a significant share, while mid-sized and emerging companies compete through specialized offerings and cost-effective solutions. The increasing focus on precision medicine, oncology diagnostics, and liquid biopsy has intensified competition, pushing companies to innovate rapidly and differentiate their offerings.

At the same time, strong collaborations with hospitals, diagnostic laboratories, and pharmaceutical companies are helping key players build long-term market positions. Overall, this evolving competitive environment is accelerating innovation, improving diagnostic capabilities, and ultimately driving the growth and transformation of the DNA diagnostics market.

DNA Diagnostics Market Recent Breakthroughs and Developments

- In March 2026, Co-Diagnostics, Inc. announced the expanded commercialization of PCR-based DNA diagnostic products (PCR Pro®, SARAGENE®) across South Asia markets, targeting a $13 billion market across Bangladesh, Pakistan, Nepal, and Sri Lanka.

- In March 2026, Agilent Technologies, Inc. announced a definitive agreement to acquire Biocare Medical for $950 million in an all-cash deal. This strategic acquisition strengthens Agilent’s Life Sciences and Diagnostics Markets unit by adding specialized tissue diagnostics, immunohistochemistry (IHC), and molecular pathology products to its portfolio.

- In February 2026, New England Biolabs (NEB) launched the Monarch® Mag Cell-free DNA (cfDNA) Extraction Kit, offering a magnetic bead-based, scalable, and reproducible method for isolating cfDNA from biofluids. The kit facilitates efficient, high-yield extraction for biomarker analysis and supports automation, catering to challenging samples with input volumes of 1-4 ml.

- In February 2026, Integrated DNA Technologies introduced an expanded innovation roadmap for next-generation sequencing solutions, strengthening Europe’s capabilities in high-throughput genomic diagnostics.

- In October 2025, GeneDx received FDA Breakthrough Device designation for its ExomeDx and GenomeDx tests, aiming to accelerate access to rapid, accurate diagnoses for rare, life-threatening genetic diseases.

- In January 2025, Thermo Fisher Scientific received FDA 510(k) clearance for the Applied BioSystems TaqPath COVID-19 diagnostic PCR kit.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

DNA Diagnostics Market CAGR | |

|

DNA Diagnostics Companies |

Thermo Fisher Scientific Inc., QIAGEN N.V., Illumina, Inc., Agilent Technologies, Inc., Bio-Rad Laboratories, Inc., Roche Diagnostics International AG, Danaher Corporation, Abbott Laboratories, PerkinElmer, Inc., Promega Corporation, Eurofins Scientific SE, Myriad Genetics, Inc., Invitae Corporation, Natera, Inc., Fulgent Genetics, Inc., BGI Genomics Co., Ltd., Takara Bio Inc., New England Biolabs, Inc., Zymo Research Corporation, and others. |

|

DNA Diagnostics Market Segments |

by Product & Services, by Technology, by Application, by End-Users, and by Geography |

|

DNA Diagnostics Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

DNA Diagnostics Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

DNA Diagnostics Market Segmentation

- DNA Diagnostics by Product & Services Exposure

- Instruments

- Reagents & Kits

- Software & Services

- DNA Diagnostics Technology Exposure

- Polymerase Chain Reaction (PCR)

- Next-Generation Sequencing (NGS)

- Others

- DNA Diagnostics Application Exposure

- Infectious Disease Diagnostics

- Cancer Genetic Diagnostics

- Prenatal Testing

- Others

- DNA Diagnostics End-Users Exposure

- Hospitals & Diagnostic Laboratories

- Research Institutes & Academic Centers

- Others

DNA Diagnostics Geography Exposure

- North America DNA Diagnostics Market

- United States DNA Diagnostics Market

- Canada DNA Diagnostics Market

- Mexico DNA Diagnostics Market

- Europe DNA Diagnostics Market

- United Kingdom DNA Diagnostics Market

- Germany DNA Diagnostics Market

- France DNA Diagnostics Market

- Italy DNA Diagnostics Market

- Spain DNA Diagnostics Market

- Rest of Europe DNA Diagnostics Market

- Asia-Pacific DNA Diagnostics Market

- China DNA Diagnostics Market

- Japan DNA Diagnostics Market

- India DNA Diagnostics Market

- Australia DNA Diagnostics Market

- South Korea DNA Diagnostics Market

- Rest of Asia-Pacific DNA Diagnostics Market

- Rest of the World DNA Diagnostics Market

- South America DNA Diagnostics Market

- Middle East DNA Diagnostics Market

- Africa DNA Diagnostics Market

DNA Diagnostics Market Recent Industry Trends and Milestones (2023-2026):

|

Category |

Key Developments |

|

DNA Diagnostics Product Launch |

New England Biolabs (NEB) launched the Monarch® Mag Cell-free DNA (cfDNA) Extraction Kit, and Integrated DNA Technologies introduced an expanded innovation roadmap for next-generation sequencing solutions. |

|

DNA Diagnostics Product Approval |

GeneDx received FDA Breakthrough Device designation for its ExomeDx and GenomeDx tests. Thermo Fisher Scientific received FDA 510(k) clearance for the Applied BioSystems TaqPath COVID-19 diagnostic PCR kit. |

|

DNA Diagnostics Product Acquisition |

Agilent Technologies, Inc., announced a definitive agreement to acquire Biocare Medical for $950 million in an all-cash deal. |

|

DNA Diagnostics Product Merger |

Becton, Dickinson and Company + Waters Corporation announced a $17.5 billion merger combining diagnostics and biosciences capabilities. |

|

Company Strategy |

Thermo Fisher Scientific Inc. · Focuses heavily on strategic acquisitions to expand its molecular diagnostics portfolio (e.g., attempt to acquire QIAGEN to strengthen diagnostics capabilities) · Invests strongly in R&D and innovation across PCR, sequencing, and bioinformatics solutions · Expands end-to-end workflow solutions (instruments + reagents + software)

QIAGEN N.V.

· Implements portfolio optimization by removing low-margin products and focusing on high-growth segments |

|

Emerging Technology |

Point-of-Care (POC) Diagnostic Devices, Microfluidics-Based Diagnostics, Non-Invasive Optical Technologies, Smartphone-Based Diagnostics, Artificial Intelligence (AI) & Machine Learning, and others |

Impact Analysis

AI-Powered Innovations and Applications:

Artificial intelligence (AI) is rapidly transforming DNA diagnostics by enhancing the speed, accuracy, and depth of genetic analysis. AI-powered innovations, particularly machine learning and deep learning, are widely used to process massive genomic datasets, enabling tasks such as variant calling, genome annotation, and mutation classification with higher precision than traditional methods. These technologies can identify subtle genetic patterns, detect rare mutations, and predict disease risks by analyzing complex DNA sequences, which significantly improves early diagnosis and clinical decision-making.

AI is also playing a crucial role in personalized medicine, where it helps match patients with targeted therapies based on their genetic profile, especially in cancer and rare diseases. Additionally, AI enables integration of multi-omics data (genomics, proteomics, transcriptomics), supports biomarker discovery, and enhances pathogen detection in infectious diseases. Overall, AI-driven applications are making DNA diagnostics more efficient, scalable, and predictive, thereby accelerating the shift toward precision healthcare and significantly boosting the capabilities of modern diagnostic systems.

U.S. Tariff Impact Analysis on the DNA Diagnostics Market:

The U.S. tariff impact on the DNA diagnostics market is creating a mixed but largely restrictive effect on growth, primarily by increasing costs and disrupting global supply chains. Since a significant portion of diagnostic instruments, reagents, and components are imported, new tariffs imposed in 2025 (ranging from ~10% to over 25% depending on country and product) have led to higher procurement costs for manufacturers and healthcare providers. This directly affects DNA diagnostic technologies, including PCR systems, sequencing instruments, and consumables, which rely heavily on globally sourced raw materials and components.

Additionally, tariffs are causing supply chain disruptions and delays, forcing companies to rethink sourcing strategies, shift manufacturing locations, or consider reshoring, often at higher operational costs. Smaller and mid-sized companies are particularly impacted, as they have limited ability to absorb rising costs, which can reduce competitiveness and slow innovation.

At the same time, increased prices for diagnostic products may be passed on to hospitals and laboratories, potentially limiting adoption rates. Overall, while large players are adapting through diversification and pricing strategies, U.S. tariffs are acting as a short-term constraint on market expansion, increasing cost pressures and operational complexity in the DNA diagnostics market.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

Key takeaways from the DNA Diagnostics market report study

- Market size analysis for the current DNA diagnostics market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the DNA diagnostics market.

- Various opportunities available for the other competitors in the DNA diagnostics market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current DNA diagnostics market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the DNA diagnostics market growth in the future.

Startup Funding & Investment Trends:

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Daisy Genomics |

$2.5 Million |

Seed |

Low-cost DNA/RNA sequencing platform |

NGS (Next-Generation Sequencing) |

Stay updated with us for Recent Articles @ New DelveInsight Blogs