Oncology Drugs Market Summary

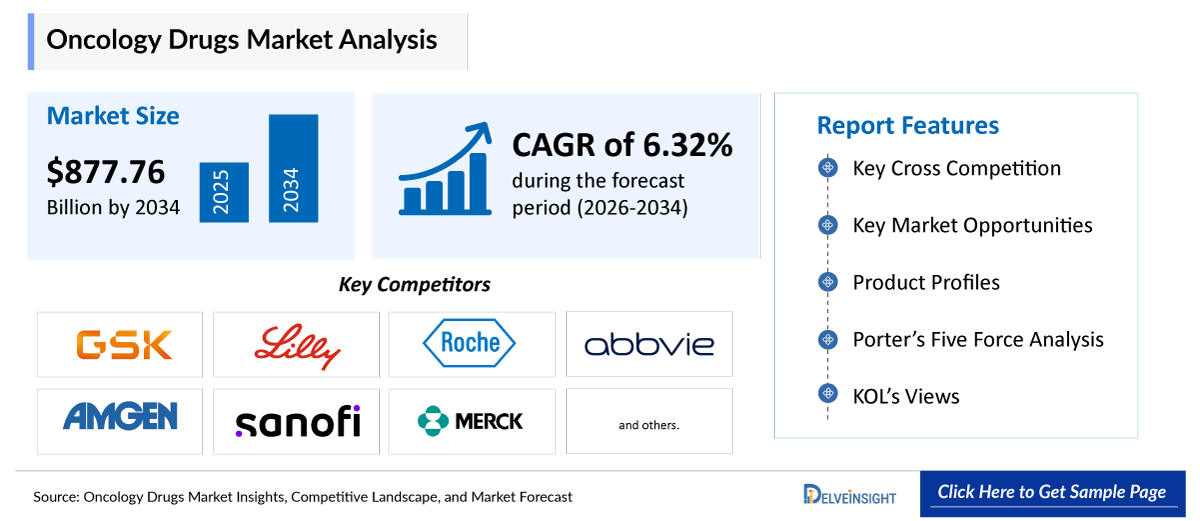

- The global oncology drugs market is expected to increase from USD 283.53 billion in 2025 to USD 877.76 billion by 2034, reflecting strong and sustained growth.

- The global oncology drugs market size is growing at a CAGR of 13.45% during the forecast period from 2026 to 2034.

- The demand for oncology drugs is primarily driven by the rising global incidence of cancer, fueled by a combination of factors including aging populations, underlying health conditions such as obesity, lifestyle changes, and increased environmental exposures. Rising cancer risk factors are increasing the global cancer burden, prompting rapid advancements in oncology. Targeted therapies and immunotherapies are leading innovations, offering more precise treatments with fewer side effects than traditional chemotherapy. Additionally, the market is witnessing a surge in drug development and launch activities by biotech companies and pharmaceutical firms, driven by both commercial opportunity and unmet clinical needs. Together, these trends are creating a highly supportive environment for sustained growth, positioning the oncology drugs market for robust and steady expansion during the forecast period from 2026 to 2034.

- The leading companies operating in the oncology drugs market include GlaxoSmithKline, Eli Lilly & Company, F. Hoffmann-La Roche Ltd, AbbVie Inc., Amgen Inc, Sanofi, Merck & Co., Inc, Novartis AG, Pfizer Inc, AstraZeneca, Bristol Myers Squibb., Gilead Sciences, Inc., Janssen Global Services, LLC, BAYER AG., Celldex Therapeutics Inc., Alaunos Therapeutics, Inc., Astellas Pharma Inc., Genentech, Inc., Sandoz International GmbH, and BeiGene, and others.

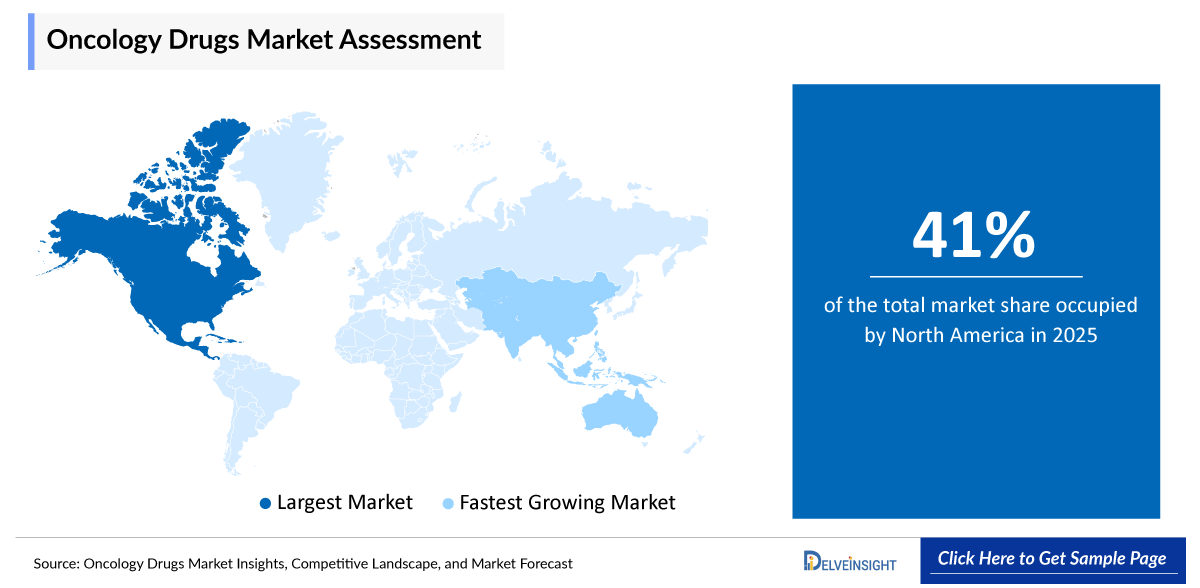

- North America is expected to dominate the Oncology Drugs market due to the rising prevalence of cancer, strong presence of leading pharmaceutical and biotechnology companies, and high adoption of advanced cancer therapies such as targeted therapy, immunotherapy, and precision medicine. The region also benefits from well-established healthcare infrastructure, significant investments in oncology research and development, and favorable reimbursement policies. In addition, increasing FDA approvals for novel oncology drugs and growing clinical trial activities in the United States and Canada are further supporting market growth across the region.

- In the therapy type segment of the oncology drugs market, the immunotherapy category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Oncology Drugs Market Insights

Oncology Drugs Market Size and Forecasts:

|

Report Metrics |

Details |

|

2025 Market Size |

USD 283.53 billion |

|

2034 Projected Market Size |

USD 877.76 billion |

|

Growth Rate (2026-2034) |

13.45% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Oncology Drugs Market

- Growing incidences of cancer globally and associated risk factors: The increasing prevalence of cancer worldwide, driven by factors such as aging populations, unhealthy lifestyles, smoking, alcohol consumption, obesity, and environmental pollution, is significantly boosting the demand for oncology drugs. As the number of cancer patients continues to rise, healthcare systems and pharmaceutical companies are focusing more on developing effective treatment options, thereby driving the growth of the oncology drugs market.

- Advancements in targeted therapies and immunotherapies: Rapid advancements in targeted therapies and immunotherapies are transforming cancer treatment by offering more precise, effective, and personalized treatment options with fewer side effects compared to traditional chemotherapy. These innovations are improving patient outcomes and increasing the adoption of advanced oncology drugs, which is contributing substantially to overall market expansion.

- Growing number of drug development and launch activities among biotech companies and pharmaceutical firms: The increasing involvement of biotechnology companies and pharmaceutical firms in oncology drug research, clinical trials, and new product launches is accelerating market growth. Continuous investments in research and development, along with frequent regulatory approvals for novel cancer therapies, are expanding the availability of innovative oncology drugs and strengthening the competitive landscape of the market.

Oncology Drugs Market Report Segmentation

This oncology drugs market report offers a comprehensive overview of the global oncology drugs market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Therapy Type (Chemotherapy, Hormonal Therapy, Targeted Therapy [Gene Therapy and Immunotherapy], and Others), Modality (Small Molecule and Biologics), Route of Administration (Oral and Parenteral), Indication (Breast Cancer, Lung Cancer, Prostate Cancer, Colorectal Cancer, and Others), Distribution Channel (Hospital & Retail Pharmacies and Online Pharmacies), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing Oncology Drugs market.

Oncology drugs are medications specifically designed for the prevention, diagnosis, and treatment of cancer. They work by targeting and destroying cancer cells, slowing their growth, or preventing their spread to other parts of the body. These drugs include chemotherapy, targeted therapy, immunotherapy, and hormonal therapy, and are used either alone or in combination depending on the type and stage of cancer.

The demand for oncology drugs is primarily driven by the rising global incidence of cancer, fueled by a combination of factors such as aging populations, genetic predisposition, unhealthy lifestyles, obesity, smoking, alcohol consumption, and increased exposure to environmental pollutants. These risk factors are significantly contributing to the growing global cancer burden, which in turn is accelerating the need for effective and advanced treatment options. In response, the oncology field is witnessing rapid scientific and technological progress, particularly in targeted therapies and immunotherapies, which are transforming cancer care by offering more precise, personalized, and effective treatment approaches with reduced toxicity compared to conventional chemotherapy.

Furthermore, the market is experiencing a strong rise in drug development activities, with biotech companies and pharmaceutical firms actively investing in research, clinical trials, and novel drug launches to address unmet medical needs and expand their oncology portfolios. Supportive regulatory pathways and increasing approvals of innovative cancer therapies are further strengthening this momentum. Collectively, these factors are creating a highly favorable environment for sustained market expansion, positioning the oncology drugs market for robust and steady growth over the forecast period from 2026 to 2034.

Get More Insights into the Report @ Oncology Drugs Market Trends

What are the latest oncology drugs market dynamics and trends?

The rising prevalence of cancer is significantly increasing the demand for novel and effective therapies, thereby accelerating the oncology drugs market globally.

According to the data provided by the International Agency for Research on Cancer (2026)

- Cancer: The estimated new cases of cancer would rise to 32.6 million by 2045 across the world.

- Prostate Cancer: The estimated global new cases of prostate cancer would reach up to 18,29,988 by 2030.

- Colorectal Cancer: The projections estimated that the new cases of colorectal cancer would rise to 3.29 million by 2045.

- Cervix Uteri: The projections estimated that the new cases of cervix uteri would rise to 9,08,612 by 2045.

Prostate cancer, colorectal cancer, cervical cancer, and other major cancer types are collectively driving the growth of the oncology drugs market due to their rising global incidence and increasing need for effective treatment options. Prostate cancer, particularly common among aging male populations, is boosting demand for hormone therapies, targeted therapies, and novel precision medicines that improve survival outcomes. Colorectal cancer is rising due to lifestyle factors such as unhealthy diets, obesity, and sedentary habits, leading to greater use of chemotherapy, immunotherapy, and biologics. Cervical cancer, largely linked to HPV infection, is supporting market growth through increasing adoption of immunotherapies and the development of advanced targeted treatments, especially in regions with expanding screening and awareness programs. Other cancers, including liver, ovarian, bladder, and pancreatic cancers, further contribute to market expansion due to their high unmet clinical needs and limited existing treatment options. Together, the growing burden of these cancers is driving continuous research, drug development, and adoption of innovative therapies, thereby significantly boosting the overall oncology drugs market.

In addition, pharmaceutical companies are ramping up research and development to meet rising clinical needs. In May 2025, AbbVie announced that the U.S. Food and Drug Administration (FDA) granted accelerated approval for EMRELIS™ (telisotuzumab vedotin-tllv) for the treatment of adult patients with locally advanced or metastatic, non-squamous NSCLC with high c-Met protein overexpression who have received prior systemic therapy.

Thus, the factors mentioned above are expected to boost the overall market of Oncology Drugs during the forecast period.

However, the high cost of cancer drugs and complications and safety concerns associated with cancer therapies, among others, are some of the key constraints that may limit the growth of the oncology drugs market.

Oncology Drugs Market Segment Analysis

Oncology Drugs Market by Therapy Type (Chemotherapy, Hormonal Therapy, Targeted Therapy [Gene Therapy and Immunotherapy], and Others), Modality (Small Molecule and Biologics), Route of Administration (Oral and Parenteral), Indication (Breast Cancer, Lung Cancer, Prostate Cancer, Colorectal Cancer, and Others), Distribution Channel (Hospital & Retail Pharmacies and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Therapy Type: Immunotherapy under the targeted therapy category is expected to dominate the market with the largest revenue share.

In the therapy type segment of the oncology drugs market, the immunotherapy under the targeted therapy category is contributing to 71.67% of total market revenue in 2025, due to its ability to selectively stimulate the body’s immune system to recognize and destroy cancer cells. Unlike traditional chemotherapy, immunotherapy offers a more precise and personalized treatment approach, resulting in improved efficacy and reduced side effects. The increasing adoption of immune checkpoint inhibitors, CAR-T cell therapies, and monoclonal antibodies has transformed cancer treatment outcomes across multiple cancer types, including lung, melanoma, and hematologic malignancies. Continuous advancements in research and a growing number of regulatory approvals are further expanding its clinical applications. As a result, immunotherapy is emerging as one of the fastest-growing and most influential segments within the oncology drugs market, driving strong demand and overall market expansion.

The immunotherapy segment of the oncology drugs market is further propelled by intensive R&D activities and active regulatory approvals from leading pharmaceutical companies. For example, in September 2024, the U.S. FDA approved Roche’s Tecentriq Hybryza, the first and only subcutaneous anti-PD-L1 cancer immunotherapy, which offers faster administration and improved patient convenience.

Similarly, in May 2024, Amgen received FDA approval for IMDELLTRA™ (tarlatamab-dlle), a first-in-class immunotherapy for adult patients with extensive-stage small cell lung cancer (ES-SCLC) who have experienced disease progression after platinum-based chemotherapy.

These developments highlight the growing momentum in the immunotherapy field, where the combination of clinical efficacy, expanding indications, innovative product launches, and increased investment in immuno-oncology research is expected to drive substantial segment growth. Thus, the factors mentioned above are likely to boost the market segment and thereby increase the overall market of oncology drugs across the globe.

By Modality: The biologics category dominates the market.

Within the modality segment of the oncology drugs market, the biologics category is anticipated to dominate, accounting for around 60% of the market share in 2025, due to the rapid shift toward highly targeted, mechanism-based cancer therapies and the increasing clinical success of immune-oncology agents. Biologics such as monoclonal antibodies (mAbs), immune checkpoint inhibitors (PD-1/PD-L1 inhibitors), antibody-drug conjugates (ADCs), cytokines, and therapeutic proteins have transformed cancer treatment by offering higher specificity, improved survival outcomes, and reduced off-target toxicity compared to conventional small-molecule chemotherapies.

The dominance of biologics is strongly supported by the expanding approvals of blockbuster immunotherapies like pembrolizumab (Keytruda), nivolumab (Opdivo), atezolizumab (Tecentriq), and durvalumab (Imfinzi), which are now widely used across multiple cancer indications, including lung, melanoma, colorectal, and head & neck cancers. In recent developments, biologics continue to lead oncology innovation, as evidenced by the FDA approval of cosibelimab-ipdl (Unloxcyt) in December 2024 for metastatic or locally advanced cutaneous squamous cell carcinoma, marking another PD-L1 blocking monoclonal antibody entering the market. Similarly, nivolumab plus hyaluronidase-nvhy (Opdivo Qvantig) received FDA approval in December 2024, expanding the use of PD-1 inhibition across multiple solid tumor indications via a subcutaneous formulation, improving patient convenience and treatment accessibility.

Additionally, biologic-based immunotherapies continue to expand in solid tumors and hematologic malignancies, with multiple checkpoint inhibitors and novel antibodies gaining accelerated approvals for lung, esophageal, and skin cancers.

Furthermore, the increasing adoption of biologics is further driven by advancements in next-generation antibody engineering, bispecific antibodies, and antibody-drug conjugates, along with strong clinical pipelines from companies such as Merck, Bristol Myers Squibb, Roche, and AstraZeneca. Overall, the biologics category is anticipated to maintain its dominance in the oncology drugs market due to continuous innovation, expanding indications, and sustained regulatory momentum supporting immunotherapy and targeted biologic treatments across a wide range of cancer types.

By Route of Administration: Parenteral category dominates the market.

Within the route of administration segment of the oncology drugs market, the parenteral category is anticipated to dominate, accounting for around 68% of the market share in 2025, as they remain the primary route for administering most high-value cancer treatments, including chemotherapy, monoclonal antibodies, immune checkpoint inhibitors, and other biologics. These therapies ensure rapid systemic delivery, precise dosing control, and higher bioavailability, which are critical for managing moderate to advanced-stage cancers. Hospital-based infusion treatments also contribute to higher overall revenue generation due to the involvement of clinical administration, supportive care, and repeat dosing cycles. Additionally, the growing adoption of advanced biologics and immunotherapies, which are predominantly parenteral in nature, is further strengthening this segment’s dominance. Continuous advancements in infusion technologies and expanding cancer treatment infrastructure worldwide are also supporting higher patient access, thereby driving sustained growth of the parenteral segment and the overall oncology drugs market.

By Indication: Lung cancer category dominates the market

Within the indication segment of the oncology drugs market, the lung cancer category is anticipated to dominate, accounting for around 22% of the market share in 2025. Lung cancer is one of the most significant drivers of the oncology drugs market due to its high global incidence, strong mortality burden, and continuous need for advanced treatment options. It accounts for a large proportion of cancer cases worldwide, especially non-small cell lung cancer (NSCLC), which has led to extensive adoption of targeted therapies, immunotherapies, and combination regimens.

The increasing identification of genetic mutations (such as EGFR, ALK, ROS-1, and KRAS) has further accelerated the development of precision medicines, boosting demand for novel oncology drugs. Continuous innovation is evident from multiple recent regulatory approvals, including zongertinib (Hernexeos) for HER2-mutant NSCLC in February 2026, telisotuzumab vedotin (EMRELIS) for c-Met–overexpressing NSCLC in May 2025, and amivantamab-vmjw (Rybrevant) with chemotherapy for EGFR-mutated NSCLC in March 2024.

Additionally, combination and chemotherapy-free regimens such as Lazcluze–Rybrevant and expanded immunotherapy-based approaches are further improving survival outcomes and expanding treatment lines. These continuous advancements, along with frequent drug approvals and expanding patient eligibility, are significantly increasing drug consumption and revenues, thereby positioning lung cancer as a major growth engine for the global oncology drugs market.

By Distribution Channel: The hospital and retail pharmacies category dominates the market

Hospital and retail pharmacies play a crucial role in boosting the oncology drugs market by ensuring efficient and widespread access to cancer treatments. Hospital pharmacies dominate the distribution of oncology drugs as most advanced therapies, including chemotherapy, immunotherapy, and biologics, require clinical administration, careful dosing, and patient monitoring in hospital settings. This leads to higher drug utilization and consistent demand within healthcare facilities. At the same time, retail pharmacies are expanding access to oral oncology drugs, particularly targeted therapies and supportive care medications, improving convenience and adherence for patients undergoing long-term treatment. The combined presence of both channels strengthens the overall distribution network, enhances treatment accessibility, and supports the continuous growth of the oncology drugs market.

Oncology Drugs Market Regional Analysis

North America Oncology Drugs Market Trends

North America is expected to account for the highest proportion of 41% of the oncology drugs market in 2025, out of all regions. North America is expected to dominate the Oncology Drugs market due to the rising prevalence of cancer, strong presence of leading pharmaceutical and biotechnology companies, and high adoption of advanced cancer therapies such as targeted therapy, immunotherapy, and precision medicine. The region also benefits from well-established healthcare infrastructure, significant investments in oncology research and development, and favorable reimbursement policies. In addition, increasing FDA approvals for novel oncology drugs and growing clinical trial activities in the United States and Canada are further supporting market growth across the region.

According to the data provided by the Zero Prostate Cancer Organization (2026), approximately 333,830 new cases of prostate cancer are expected to be diagnosed in 2026. Additionally, as per the same source, there are more than 3.5 million prostate cancer survivors in the U.S. This surge in cancer cases has led to a heightened focus on early diagnosis, treatment innovation, and accessibility. Pharmaceutical and biotech companies are investing heavily in research and development to meet this growing demand, leading to the discovery and commercialization of new oncology drugs, including targeted therapies and immunotherapies. These novel drugs are designed to treat cancer more precisely by focusing on specific genetic mutations or immune pathways, offering better patient outcomes with fewer side effects.

Moreover, leading pharmaceutical companies are making substantial investments in research and development to advance cutting-edge targeted therapies. For example, in March 2025, AstraZeneca secured FDA approval for Imfinzi, marking it as the first and only perioperative immunotherapy for patients with muscle-invasive bladder cancer in the United States, a breakthrough that offers new hope for improved patient outcomes.

Similarly, strategic partnerships are fueling innovation in the oncology landscape. In June 2025, BioNTech and Bristol Myers Squibb announced a global collaboration to co-develop and commercialize BNT327, a next-generation bispecific antibody designed to target multiple solid tumor types, potentially transforming treatment options for a broad spectrum of cancer patients.

Collectively, the rising burden of cancer and product launches and approvals is propelling the demand for oncology drugs in North America, reinforcing its position as a leading region in the global market.

Europe Oncology Drugs Market Trend

The oncology drugs market in Europe is witnessing strong and sustained growth due to the rising burden of cancer across the region, increasing adoption of advanced therapies such as immunotherapies and targeted treatments, and continuous innovation by pharmaceutical companies. Europe benefits from a well-established healthcare infrastructure, a supportive regulatory framework by the European Medicines Agency (EMA), and growing access to novel cancer medicines across major markets such as Germany, France, and the UK. Additionally, increasing investments in oncology R&D and a high number of clinical trials are further accelerating market expansion. Recent regulatory approvals are also strengthening this growth trend, for example, the EMA and FDA jointly expanded the use of darolutamide (Nubeqa) for prostate cancer in June 2025, reflecting ongoing label expansions for targeted therapies. In November 2024, tislelizumab (Tevimbra) received approval in Europe for gastric and gastroesophageal junction cancers, supporting the growing role of immunotherapy in solid tumors. More recently, durvalumab (Imfinzi) was approved in the European Union for expanded use in gastric and gastroesophageal cancers as part of combination therapy, further highlighting Europe’s rapid adoption of innovative oncology regimens.

Collectively, these advancements and approvals are enhancing patient access to cutting-edge treatments, thereby driving sustained and robust growth of the oncology drugs market in Europe.

Asia-Pacific Oncology Drugs Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the oncology drugs market due to the rapidly increasing cancer burden, large and aging population base, and improving access to advanced healthcare services. The rising incidence of cancers such as lung, breast, colorectal, and liver cancer, particularly in countries like China, India, and Japan, is significantly boosting the demand for effective oncology treatments. In addition, growing healthcare expenditure, expanding health insurance coverage, and increasing government initiatives for cancer screening and early diagnosis are supporting wider treatment adoption. The region is also witnessing strong growth in pharmaceutical manufacturing capabilities, rising clinical trial activities, and increasing participation of both global and local biotech companies in oncology drug development. Furthermore, faster regulatory approvals and improved availability of targeted therapies and immunotherapies are enhancing patient access to innovative treatments. Collectively, these factors are positioning APAC as one of the fastest-growing and most important regions in the global oncology drugs market.

Who are the major players in the oncology drugs market?

The following are the leading companies in the oncology drugs market. These companies collectively hold the largest market share and dictate industry trends.

- GlaxoSmithKline

- Eli Lilly & Company

- F. Hoffmann-La Roche Ltd.

- AbbVie Inc.

- Amgen Inc.

- Sanofi

- Merck & Co., Inc.

- Novartis AG

- Pfizer Inc.

- AstraZeneca

- Bristol Myers Squibb.

- Gilead Sciences, Inc.

- Janssen Global Services, LLC

- BAYER AG.

- Celldex Therapeutics Inc.

- Alaunos Therapeutics, Inc.

- Astellas Pharma Inc.

- Genentech, Inc.

- Sandoz International GmbH

- BeiGene, and others

How is the competitive landscape shaping the oncology drugs market?

The competitive landscape of the oncology drugs market is highly dynamic and rapidly evolving, driven by strong participation from global pharmaceutical companies, biotechnology firms, and emerging startups. Leading players are heavily investing in research and development to introduce innovative therapies such as targeted drugs, immunotherapies, and combination regimens that improve survival outcomes and reduce side effects. Strategic collaborations, mergers and acquisitions, and licensing agreements are also becoming common as companies aim to expand their oncology portfolios and strengthen pipeline capabilities. In addition, increasing focus on precision medicine and biomarker-driven therapies is intensifying competition, as companies strive to develop more personalized and effective cancer treatments. Regulatory incentives, fast-track approvals, and orphan drug designations are further encouraging innovation and market entry. Overall, this intense competition is accelerating drug innovation, expanding treatment options, and driving sustained growth in the global oncology drugs market.

Recent Developmental Activities in the Oncology Drugs Market

- In February 2026, zongertinib (Hernexeos) was approved for HER2-mutant NSCLC, further highlighting the growing role of targeted small molecules in precision oncology.

- In July 2025, sunvozertinib (Zegfrovy) received accelerated approval for EGFR exon 20 insertion mutation-positive NSCLC, expanding treatment options for difficult-to-treat lung cancers.

- In June 2025, the FDA approved taletrectinib (Ibtrozi), a ROS1 tyrosine kinase inhibitor for ROS1-positive non-small cell lung cancer, demonstrating strong clinical efficacy in previously treated patients.

- In May 2025, AbbVie announced that the U.S. Food and Drug Administration (FDA) granted accelerated approval for EMRELIS™ (telisotuzumab vedotin-tllv) for the treatment of adult patients with locally advanced or metastatic, non-squamous NSCLC with high c-Met protein overexpression who have received prior systemic therapy.

- In September 2024, the U.S. FDA approved Roche’s Tecentriq Hybryza, the first and only subcutaneous anti-PD-L1 cancer immunotherapy, which offers faster administration and improved patient convenience.

- In May 2024, Amgen received FDA approval for IMDELLTRA™ (tarlatamab-dlle), a first-in-class immunotherapy for adult patients with extensive-stage small cell lung cancer (ES-SCLC) who have experienced disease progression after platinum-based chemotherapy.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Oncology Drugs Market CAGR |

13.45% |

|

Key Companies in the Oncology Drugs Market |

GlaxoSmithKline, Eli Lilly & Company, F. Hoffmann-La Roche Ltd, AbbVie Inc., Amgen Inc, Sanofi, Merck & Co., Inc, Novartis AG, Pfizer Inc, AstraZeneca, Bristol Myers Squibb., Gilead Sciences, Inc., Janssen Global Services, LLC, BAYER AG., Celldex Therapeutics Inc., Alaunos Therapeutics, Inc., Astellas Pharma Inc., Genentech, Inc., Sandoz International GmbH, and BeiGene, and others. |

|

Oncology Drugs Market Segments |

by Therapy Type, by Modality, by Route of Administration, by Indication, by Distribution Channel, and by Geography |

|

Oncology Drugs Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Oncology Drugs Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Oncology Drugs Market Segmentation

- Oncology Drugs by Therapy Type Exposure

- Chemotherapy

- Hormonal Therapy

- Targeted Therapy

- Gene Therapy

- Immunotherapy

- Others

- Oncology Drugs by Modality Exposure

- Small Molecule

- Biologic

- Oncology Drugs Route of Administration Exposure

- Oral

- Parenteral

- Oncology Drugs Route of Administration Exposure

- Breast Cancer

- Lung Cancer

- Prostate Cancer

- Colorectal Cancer

- Others

- Oncology Drugs Distribution Channel Exposure

- Hospital & Retail Pharmacies

- Online Pharmacies

Oncology Drugs Geography Exposure

- North America Oncology Drugs Market

- United States Oncology Drugs Market

- Canada Oncology Drugs Market

- Mexico Oncology Drugs Market

- Europe Oncology Drugs Market

- United Kingdom Oncology Drugs Market

- Germany Oncology Drugs Market

- France Oncology Drugs Market

- Italy Oncology Drugs Market

- Spain Oncology Drugs Market

- Rest of Europe Oncology Drugs Market

- Asia-Pacific Oncology Drugs Market

- China Oncology Drugs Market

- Japan Oncology Drugs Market

- India Oncology Drugs Market

- Australia Oncology Drugs Market

- South Korea Oncology Drugs Market

- Rest of Asia-Pacific Oncology Drugs Market

- Rest of the World Oncology Drugs Market

- South America Oncology Drugs Market

- Middle East Oncology Drugs Market

- Africa Oncology Drugs Market

Oncology Drugs Market Recent Industry Trends and Milestones (2023-2026):

|

Category |

Key Developments |

|

Oncology Drugs Product Approvals |

FDA approved taletrectinib (Ibtrozi), AbbVie announced that the U.S. Food and Drug Administration (FDA) granted accelerated approval for EMRELIS™ (telisotuzumab vedotin-tllv), the U.S. FDA approved Roche’s Tecentriq Hybryza, the first and only subcutaneous anti-PD-L1 cancer immunotherapy. |

|

Company Strategy |

F. Hoffmann-La Roche

Novartis AG · Emphasis on cell and gene therapy innovations, including CAR-T therapies for hematologic cancers. · Focus on developing next-generation targeted small molecules and radioligand therapies. · Strengthening oncology portfolio through global clinical trials and regulatory expansions. |

|

Emerging Technology |

CAR-T cell therapy, immune checkpoint inhibitors, bispecific antibodies, antibody-drug conjugates (ADCs), cancer vaccines, gene editing technologies (CRISPR), mRNA-based cancer therapies, tumor microenvironment targeting therapies, liquid biopsy-guided precision oncology, AI-driven drug discovery, nanotechnology-based drug delivery systems, radioligand therapy, personalized cancer therapeutics, oncolytic virus therapy, and multi-omics-based biomarker discovery, and others |

Key takeaways from the oncology drugs market report study

- Market size analysis for the current oncology drugs market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the oncology drugs market.

- Various opportunities available for the other competitors in the oncology drugs market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current oncology drugs market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the oncology drugs market growth in the future.

Startup Funding & Investment Trends:

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

Caribou Bioscience |

USD 304 million |

- |

CRISPR-based allogeneic CAR-T therapies (CB-010, CB-011) |

Blood cancers (lymphoma, multiple myeloma) using gene-edited cell therapy |