Immuno-Oncology Drugs Market Summary

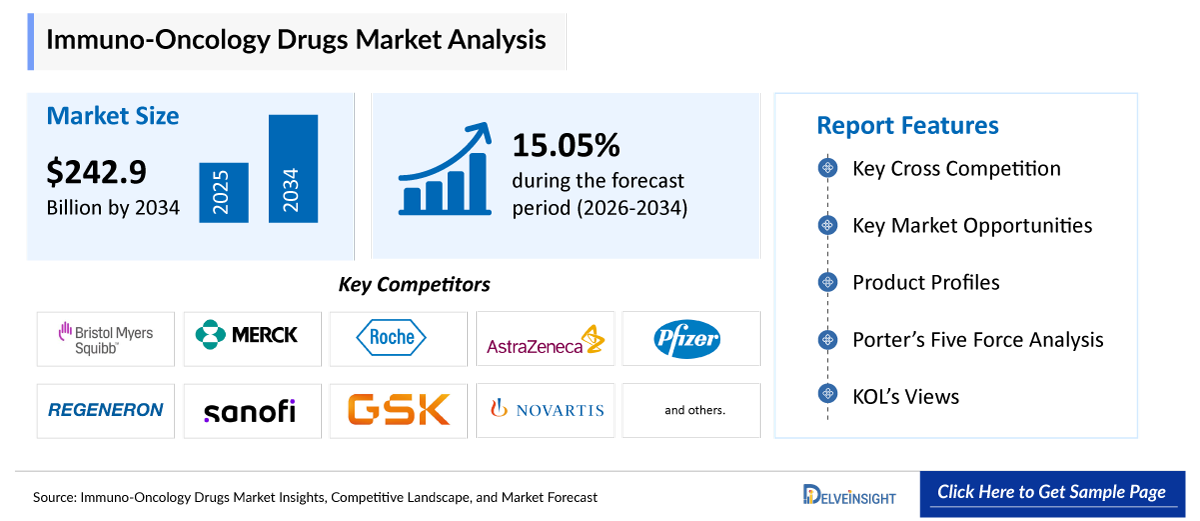

- The global immuno-oncology drugs market size is expected to increase from USD 69,398.94 million in 2025 to USD 242,912 million by 2034, reflecting strong and sustained growth.

- The global immuno-oncology drugs market is growing at a CAGR of 15.05% during the forecast period from 2026 to 2034.

- The immuno-oncology drugs market is being strongly driven by the rising global cancer burden, which is expanding the patient population and increasing demand for more effective, targeted therapies. At the same time, a robust pipeline and continuous drug approvals are accelerating market growth by introducing new therapies and expanding indications for existing drugs, thereby widening treatment accessibility. In parallel, technological advancements in cell and gene therapy, particularly innovations like CAR-T and engineered immune cells, are transforming treatment outcomes and opening new opportunities in both hematological and solid tumors. Collectively, these factors are reinforcing each other, growing demand, sustained innovation, and improved clinical success, leading to the rapid expansion of the immuno-oncology drugs market.

- The leading companies operating in the immuno-oncology drugs market include Bristol-Myers Squibb Company, Merck & Co., Inc., F. Hoffmann-La Roche AG, AstraZeneca PLC, Pfizer Inc, Regeneron Pharmaceuticals, Inc., Sanofi S.A., GlaxoSmithKline plc, Incyte Corporation, Novartis AG, Gilead Sciences, Inc., Kite Pharma, Inc. (a Gilead Company), bluebird bio, Inc., Amgen Inc., Janssen Pharmaceuticals, and others.

- North America is expected to dominate the immuno-oncology drugs market due to its high cancer prevalence, strong presence of leading biopharmaceutical companies, and early adoption of advanced therapies such as checkpoint inhibitors and CAR-T treatments. The region also benefits from robust R&D investments, favorable regulatory support, and widespread availability of biomarker-based diagnostics, which enable personalized treatment approaches. Additionally, well-established healthcare infrastructure and higher healthcare spending further support the rapid uptake and commercialization of immuno-oncology therapies in the region.

- In the therapy type segment of the immuno-oncology drugs market, the immune checkpoint inhibitors category is estimated to account for the largest market share in 2025.

Request for unlocking the report of the @ Immuno-Oncology Drugs Market Insights

Immuno-Oncology Drugs Market Size and Forecasts

|

Report Metrics |

Details |

|

2025 Market Size |

USD 69,398.94 million |

|

2034 Projected Market Size |

USD 242,912.00 million |

|

Growth Rate (2026-2034) |

15.05% CAGR |

|

Largest Market |

North America |

|

Fastest Growing Market |

Asia-Pacific |

|

Market Structure |

Moderately Concentrated |

Factors Contributing to the Growth of the Immuno-Oncology Drugs Market

- Rising global cancer burden leading to a surge in immuno-oncology: The increasing incidence of cancers such as lung, breast, and colorectal cancer is a primary growth driver. Aging populations, lifestyle changes, and environmental factors are contributing to a higher patient pool, creating sustained demand for advanced and effective treatment options like immuno-oncology therapies.

- Strong pipeline and continuous drug approvals: Pharmaceutical companies are heavily investing in immuno-oncology R&D, resulting in a robust clinical pipeline of checkpoint inhibitors, CAR-T therapies, and next-generation immunotherapies. Frequent regulatory approvals are expanding treatment indications and market size.

- Technological advancements in cell & gene therapy: Innovations in CAR-T cell therapy, gene editing, and engineered immune cells are transforming cancer treatment. These technologies are opening new avenues, particularly in hematological malignancies and solid tumors.

Immuno-Oncology Drugs Market Report Segmentation

This immuno-oncology drugs market report offers a comprehensive overview of the global immuno-oncology drugs market, highlighting key trends, growth drivers, challenges, and opportunities. It covers detailed market segmentation by Therapy Type (Immune Checkpoint Inhibitors, CAR T-Cell Therapy, Monoclonal Antibodies, Cancer Vaccines, and Others), Drug Class (PD-1 Inhibitors, PD-L1 Inhibitors, CTLA-4 Inhibitors, and Others), Cancer Type (Lung Cancer, Breast Cancer, Melanoma, Leukemia, Lymphoma, and Others), End-Users (Hospitals, Cancer Treatment Centers, Research Institutes, and Others), and geography. The report provides valuable insights into the competitive landscape, regulatory environment, and market dynamics across major markets, including North America, Europe, and Asia-Pacific. Featuring in-depth profiles of leading industry players and recent product innovations, this report equips businesses with essential data to identify market potential, develop strategic plans, and capitalize on emerging opportunities in the rapidly growing immuno-oncology drugs market.

Immuno-oncology is a branch of cancer treatment that uses the body’s immune system to recognize and destroy cancer cells. Instead of directly attacking tumors like chemotherapy or radiation, it enhances or modifies immune responses so they can better detect and fight cancer. This approach includes therapies such as immune checkpoint inhibitors, CAR T-cell therapy, and cancer vaccines, and has improved outcomes in several types of cancer by providing more targeted and long-lasting responses.

The immuno-oncology drugs market is being strongly driven by the rising global cancer burden, which continues to expand the patient pool due to aging populations, lifestyle changes, and increasing incidence of both solid and hematological malignancies. This growing demand is pushing healthcare systems to adopt more effective and targeted treatment approaches beyond conventional therapies. At the same time, a robust clinical pipeline and continuous drug approvals are accelerating market growth, with pharmaceutical companies consistently introducing novel immune checkpoint inhibitors, next-generation biologics, and combination therapies. These approvals are not only bringing new drugs to market but also expanding the indications of existing therapies across multiple cancer types, thereby improving treatment accessibility and adoption rates.

In parallel, technological advancements in cell and gene therapy, particularly innovations such as CAR-T cell therapies, T-cell receptor (TCR) therapies, and genetically engineered immune cells, are significantly transforming treatment outcomes. These advanced therapies are showing promising results, especially in difficult-to-treat and relapsed cancers, while also expanding into solid tumor applications. Moreover, continuous improvements in manufacturing processes, safety profiles, and scalability are making these therapies more commercially viable. Collectively, the interplay of increasing disease burden, sustained innovation, and strong clinical success is creating a powerful growth cycle, driving rapid expansion and long-term opportunities in the immuno-oncology drugs market.

Get More Insights into the Report @ Immuno-Oncology Drugs Market Trends

What are the latest immuno-oncology drugs market dynamics and trends?

The increasing global burden of cancer, including melanoma, lung cancer, breast cancer, leukemia, lymphoma, colorectal cancer, and other solid tumors, is one of the primary factors driving the growth of the immuno-oncology drugs market. The rising prevalence of cancer has significantly increased the demand for advanced therapeutic approaches that offer improved survival outcomes, targeted action, and long-term disease management compared to conventional chemotherapy and radiation therapies. Immuno-oncology therapies, particularly immune checkpoint inhibitors, CAR-T cell therapies, monoclonal antibodies, and cancer vaccines, are increasingly being adopted due to their ability to harness the body’s immune system to recognize and eliminate cancer cells more effectively.

According to data published by the Melanoma Research Foundation (2026), nearly 234,680 Americans are expected to be diagnosed with melanoma in 2026. Among these, more than 112,000 cases are projected to be invasive melanoma (Stage I-IV), while approximately 122,680 cases will involve melanoma in situ. The growing incidence of melanoma is particularly supporting the demand for PD-1 and PD-L1 inhibitors such as pembrolizumab and nivolumab, which have become standard-of-care therapies for advanced melanoma treatment.

Similarly, the increasing incidence of breast cancer continues to create substantial opportunities for immuno-oncology therapeutics. According to the International Agency for Research on Cancer (IARC) (2026), the global number of new breast cancer cases is expected to reach approximately 2.7 million by 2030. Rising adoption of immunotherapies for triple-negative breast cancer (TNBC), along with increasing research into biomarker-driven targeted immunotherapies, is expected to further accelerate market growth over the forecast period.

In addition, the strong clinical pipeline and continuous regulatory approvals of novel immunotherapies are significantly strengthening the immuno-oncology drugs market by expanding treatment accessibility and broadening therapeutic indications across multiple cancer types. Pharmaceutical and biotechnology companies are heavily investing in next-generation checkpoint inhibitors, bispecific antibodies, tumor-infiltrating lymphocyte (TIL) therapies, cancer vaccines, NK-cell therapies, and personalized cell therapies to improve efficacy and reduce toxicity.

According to the Euromed Foundation (2025), regulatory activity in immuno-oncology has accelerated considerably, with the U.S. FDA approving 17 new immunotherapy indications in 2024, including advanced checkpoint inhibitors and innovative cell-based therapies. These approvals highlight the rapid advancement of personalized cancer care and precision oncology approaches. Furthermore, in September 2025, the FDA approved a subcutaneous formulation of pembrolizumab (Keytruda), improving treatment convenience, reducing administration time, and enhancing patient accessibility. Pembrolizumab, a humanized monoclonal antibody targeting the PD-1 receptor, remains one of the most widely used and commercially successful immuno-oncology therapies globally.

Moreover, increasing adoption of combination immunotherapy regimens is further contributing to market expansion. Combination approaches involving checkpoint inhibitors with chemotherapy, targeted therapies, radiotherapy, or other immunotherapies are demonstrating improved clinical outcomes and higher response rates across several cancer indications, including non-small cell lung cancer (NSCLC), renal cell carcinoma, and hepatocellular carcinoma.

The growing focus on precision medicine and biomarker-based treatment selection is also accelerating the adoption of immuno-oncology therapies. Advancements in genomic profiling, companion diagnostics, artificial intelligence-driven biomarker discovery, and liquid biopsy technologies are improving patient stratification and enabling more personalized treatment approaches.

Additionally, increasing healthcare expenditure, rising oncology drug spending, favorable reimbursement policies in developed economies, and expanding research collaborations between pharmaceutical companies and academic institutions are further supporting market growth. The increasing number of clinical trials investigating novel immunotherapy combinations and earlier-line treatment settings is expected to create substantial growth opportunities over the coming years. Therefore, the factors mentioned above are expected to significantly drive the growth of the global immuno-oncology drugs market during the forecast period.

However, despite strong growth potential, the market faces several challenges. The lack of highly reliable predictive biomarkers and stringent regulatory approval requirements remains a major limiting factor for the immuno-oncology drugs market. Currently used biomarkers, such as PD-L1 expression, tumor mutational burden (TMB), and microsatellite instability (MSI), often fail to consistently predict patient response to therapy, leading to suboptimal patient selection, inconsistent clinical outcomes, and inefficient utilization of expensive immunotherapies.

Furthermore, the regulatory approval process for immuno-oncology therapies is highly complex and time-intensive due to the need for extensive clinical validation, long-term survival data, biomarker validation studies, and rigorous safety assessments. Immune-related adverse events, high treatment costs, and manufacturing complexities associated with advanced cell therapies such as CAR-T therapies also pose significant commercialization and accessibility challenges, particularly in low- and middle-income countries. These factors may hinder market growth to a certain extent during the forecast period.

Immuno-Oncology Drugs Market Segment Analysis

Immuno-Oncology Drugs Market by Therapy Type (Immune Checkpoint Inhibitors, CAR T-Cell Therapy, Monoclonal Antibodies, Cancer Vaccines, and Others), Drug Class (PD-1 Inhibitors, PD-L1 Inhibitors, CTLA-4 Inhibitors, and Others), Cancer Type (Lung Cancer, Breast Cancer, Melanoma, Leukemia, Lymphoma, and Others), End-Users (Hospitals, Cancer Treatment Centers, Research Institutes, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World)

By Therapy Type: Immune checkpoint inhibitors are expected to dominate the market with the largest revenue share

In the therapy type segment of the immuno-oncology drugs market, the immune checkpoint inhibitors (ICIs) category is estimated to contribute approximately 67% of the total market revenue in 2025, primarily due to their remarkable clinical success, broad therapeutic applicability, and expanding adoption across multiple cancer indications. Immune checkpoint inhibitors have revolutionized modern oncology by targeting critical immune regulatory pathways such as PD-1, PD-L1, and CTLA-4, thereby restoring the immune system’s ability to identify and destroy cancer cells more effectively. These therapies have demonstrated durable clinical responses, prolonged overall survival, and improved progression-free survival in several malignancies, particularly melanoma, non-small cell lung cancer (NSCLC), renal cell carcinoma, urothelial carcinoma, and head & neck cancers.

The widespread adoption of ICIs has been strongly supported by the commercial success of blockbuster drugs such as Keytruda (pembrolizumab), Opdivo (nivolumab), Tecentriq (atezolizumab), Imfinzi (durvalumab), and Yervoy (ipilimumab). Among these, PD-1 inhibitors have emerged as the leading revenue-generating class due to their superior efficacy profiles and broader approval landscape. The increasing use of checkpoint inhibitors as first-line therapies, adjuvant therapies, neoadjuvant therapies, and combination regimens has significantly strengthened their market penetration across both early-stage and advanced cancers.

Additionally, the continuous expansion of regulatory approvals and label extensions is further accelerating the growth of the immune checkpoint inhibitors segment. Regulatory agencies such as the U.S. FDA and the European Medicines Agency (EMA) have increasingly approved ICIs across a wider range of tumor types and treatment settings, supporting their integration into standard oncology treatment guidelines. For instance, in December 2024, the FDA approved a PD-L1 checkpoint inhibitor for advanced cutaneous squamous cell carcinoma, thereby expanding immunotherapy treatment options within skin cancer management. Furthermore, in March 2025, durvalumab (Imfinzi) received approval as part of a combination regimen for muscle-invasive bladder cancer, marking its strategic expansion into earlier-stage treatment settings and strengthening AstraZeneca’s immuno-oncology portfolio.

Moreover, pharmaceutical and biotechnology companies are heavily investing in next-generation checkpoint inhibitors and novel combination approaches aimed at improving therapeutic efficacy, minimizing immune-related adverse events, and overcoming resistance mechanisms associated with current immunotherapies. Combination regimens involving ICIs with chemotherapy, targeted therapy, radiation therapy, cancer vaccines, bispecific antibodies, and cell therapies are demonstrating enhanced response rates and improved clinical outcomes across several cancer indications. These advancements are expected to further expand the eligible patient population and sustain long-term market growth.

The segment is also benefiting from increasing advancements in precision oncology and biomarker-driven treatment selection. The growing use of companion diagnostics, genomic profiling, PD-L1 testing, tumor mutational burden (TMB) analysis, and liquid biopsy technologies is enabling more personalized immunotherapy approaches, thereby improving patient stratification and treatment effectiveness. Furthermore, rising awareness among oncologists and patients regarding the long-term survival benefits of immunotherapy compared with traditional chemotherapy is contributing to higher adoption rates globally.

In addition, the increasing prevalence of cancer worldwide continues to generate substantial demand for immune checkpoint inhibitors. Lung cancer alone remains the largest application area for ICIs, supported by the high incidence of NSCLC and strong clinical evidence supporting immunotherapy-based regimens. The growing geriatric population, rising healthcare expenditure, improving reimbursement coverage for oncology biologics, and increasing investments in cancer research are further supporting segment expansion.

As a result, the immune checkpoint inhibitors segment not only represents the cornerstone of the immuno-oncology drugs market but also serves as the primary revenue generator within the industry. Owing to strong clinical evidence, continuous product innovation, robust pipeline development, expanding regulatory approvals, and increasing physician confidence, the segment is expected to maintain its dominant position and continue significantly driving the overall growth of the global immuno-oncology drugs market during the forecast period.

By Drug Class: PD-1 Inhibitors category dominates the market

Within the drug class segment of the immuno-oncology drugs market, the PD-1 Inhibitors category is anticipated to dominate, accounting for around 75% of the market share in 2025, due to their strong clinical efficacy, broad applicability across multiple cancer types, and favorable safety profile compared to other checkpoint inhibitors. These therapies work by blocking the PD-1 pathway, thereby enhancing the immune system’s ability to detect and destroy cancer cells, and have demonstrated durable responses and improved overall survival in cancers such as lung cancer, melanoma, head & neck cancer, and Hodgkin lymphoma. Their widespread adoption is further supported by extensive clinical evidence, continuous regulatory approvals, and frequent label expansions into both early-stage and advanced disease settings. In addition, PD-1 inhibitors are increasingly being used in combination regimens with chemotherapy, targeted therapy, and other immunotherapies, which enhances treatment outcomes and expands their clinical utility. With a strong pipeline, high physician preference, and growing patient eligibility driven by biomarker-based approaches, PD-1 inhibitors are expected to remain the leading and fastest-growing drug class in the immuno-oncology drugs market.

By Cancer Type: The lung cancer category dominates the market

Within the cancer type segment of the immuno-oncology drugs market, the lung cancer category is anticipated to dominate, accounting for approximately 31% of the total market share in 2025. The segment’s dominance is primarily attributed to the high global prevalence and mortality associated with lung cancer, making it one of the largest and most commercially significant oncology indications worldwide. The growing disease burden continues to create substantial demand for advanced immunotherapy-based treatment approaches that improve survival outcomes and disease management.

According to data published by the American Cancer Society (2026), approximately 229,410 new cases of lung cancer are expected to be diagnosed in the United States in 2026. Lung cancer remains one of the leading causes of cancer-related deaths globally, particularly due to the high incidence of non-small cell lung cancer (NSCLC), which accounts for nearly 85% of all lung cancer cases. The large patient population eligible for immunotherapy treatment is significantly contributing to the strong market share of this segment.

The increasing adoption of immune checkpoint inhibitors has transformed the treatment landscape for lung cancer, especially NSCLC. Immuno-oncology therapies targeting PD-1 and PD-L1 pathways, including pembrolizumab (Keytruda), nivolumab (Opdivo), atezolizumab (Tecentriq), and durvalumab (Imfinzi), are now widely utilized as first-line monotherapies as well as combination regimens alongside chemotherapy and targeted therapies. These therapies have demonstrated substantial improvements in overall survival, progression-free survival, and durable response rates compared to traditional chemotherapy approaches, thereby accelerating their clinical adoption.

Furthermore, continuous regulatory approvals and label expansions are significantly strengthening the lung cancer segment within the immuno-oncology drugs market. Pharmaceutical companies are increasingly focusing on expanding immunotherapy indications into earlier-stage disease settings, adjuvant therapies, and perioperative treatment regimens. For instance, in December 2024, the U.S. FDA approved durvalumab for limited-stage small cell lung cancer (SCLC) following chemoradiation therapy, representing a major advancement in expanding immunotherapy utilization into earlier-stage lung cancer treatment. Such approvals are increasing treatment accessibility and broadening the eligible patient population for immuno-oncology therapies.

In addition, the strong pipeline of novel immunotherapies and combination strategies continues to support segment growth. Numerous ongoing clinical trials are evaluating checkpoint inhibitors in combination with chemotherapy, targeted therapies, bispecific antibodies, cancer vaccines, and next-generation immunomodulators to improve therapeutic efficacy and overcome treatment resistance. These developments are expected to further enhance treatment outcomes and drive long-term market expansion.

The growing adoption of biomarker-driven precision oncology is another major factor supporting the dominance of the lung cancer segment. Increasing utilization of biomarker testing, including PD-L1 expression analysis, tumor mutational burden (TMB), EGFR mutation testing, and liquid biopsy technologies, is enabling improved patient stratification and optimized treatment selection. This precision medicine approach enhances treatment response rates and supports more personalized immunotherapy regimens.

Additionally, rising awareness regarding early cancer screening and diagnosis programs is contributing to earlier detection and higher treatment rates for lung cancer patients. Government initiatives, increasing healthcare expenditure, improving reimbursement coverage for oncology biologics, and growing investments in cancer research and clinical development are further accelerating the adoption of immuno-oncology therapies in lung cancer treatment.

Moreover, lung cancer remains a key strategic focus area for leading pharmaceutical and biotechnology companies due to its large commercial potential and high unmet medical need. Major market players continue to invest heavily in clinical trials, combination therapy development, and next-generation checkpoint inhibitors to strengthen their oncology portfolios and expand market presence.

Thus, the factors mentioned above are expected to significantly drive the growth of the lung cancer segment, thereby substantially contributing to the overall expansion of the global immuno-oncology drugs market during the forecast period.

By End-Users: The Hospitals category dominates the market

In the end-users segment of the immuno-oncology drugs market, the hospitals category dominates due to its central role in the diagnosis, treatment, and management of cancer patients. Hospitals are equipped with advanced infrastructure, specialized oncology departments, and multidisciplinary care teams, including oncologists, immunologists, and trained nursing staff, which are essential for administering complex immuno-oncology therapies such as immune checkpoint inhibitors and CAR-T cell treatments. These therapies often require controlled clinical settings, continuous patient monitoring, and the ability to manage severe immune-related adverse events, capabilities that are primarily available in hospital environments. Additionally, hospitals act as key hubs for clinical trials, early adoption of novel therapies, and collaboration with pharmaceutical companies, further strengthening their dominance. As a result, hospitals account for the largest share of the market and are expected to remain the primary treatment setting for immuno-oncology therapies due to their comprehensive care capabilities and strong patient preference for hospital-based treatment.

Immuno-Oncology Drugs Market Regional Analysis

North America Immuno-Oncology Drugs Market Trends

North America is expected to account for the highest proportion of 41% of the immuno-oncology drugs market in 2025, out of all regions. North America is expected to dominate the immuno-oncology drugs market due to its high cancer prevalence, strong presence of leading biopharmaceutical companies, and early adoption of advanced therapies such as checkpoint inhibitors and CAR-T treatments. The region also benefits from robust R&D investments, favorable regulatory support, and widespread availability of biomarker-based diagnostics, which enable personalized treatment approaches. Additionally, well-established healthcare infrastructure and higher healthcare spending further support the rapid uptake and commercialization of immuno-oncology therapies in the region.

According to the recent data provided by the AIM at Melanoma Foundation (2026), in 2026, there will be 234,680 cases of melanoma diagnosed in the United States. Of those, 122,680 cases will be noninvasive (in situ), and 112,000 cases will be invasive. Melanoma is significantly boosting the growth of the immuno-oncology drugs market because it has been one of the most responsive cancers to immunotherapy, particularly immune checkpoint inhibitors such as PD-1 and CTLA-4 inhibitors. Treatments like Pembrolizumab, Nivolumab, and Ipilimumab have demonstrated high efficacy in advanced melanoma, significantly improving survival rates and driving widespread adoption. Additionally, melanoma has been a key focus area for clinical trials and early approvals of novel immunotherapies, including combination therapies and cell-based treatments, making it a model indication for innovation.

Additionally, the immuno-oncology drugs market in North America is being significantly boosted by a strong clinical pipeline, continuous drug approvals, and rapid technological advancements in cell and gene therapy, particularly CAR-T and next-generation immune-based treatments. The region has witnessed a steady increase in regulatory activity, with the U.S. Food and Drug Administration approving and expanding multiple immunotherapy indications. For instance, in February, 2026, pembrolizumab (a leading PD-1 inhibitor) received a new approval/label expansion, highlighting the continued dominance and lifecycle extension of checkpoint inhibitors. In 2025, the FDA approved 46 novel drugs, many of which included oncology and immunotherapy agents, reflecting a highly active approval landscape.

At the same time, advancements in cell and gene therapy are transforming treatment paradigms. CAR-T therapies continue to expand, with seven FDA-approved CAR-T products available by 2025 and ongoing trials exploring their use in additional cancers. A major milestone occurred in December 2025, when lisocabtagene maraleucel became the first CAR-T therapy approved for marginal zone lymphoma, demonstrating the expansion of cell therapies into new indications.

These continuous approvals, expanding indications, and strong clinical trial momentum, combined with breakthroughs such as tumor-infiltrating lymphocyte (TIL) therapies and engineered cell therapies, are enhancing treatment efficacy and personalization. As a result, North America remains the leading hub for immuno-oncology innovation, with its strong regulatory support, advanced R&D ecosystem, and rapid adoption of cutting-edge cell and gene therapies collectively driving sustained market growth.

Europe Immuno-Oncology Drugs Market Trends

The immuno-oncology drugs market in Europe is witnessing strong and sustained growth, driven by a combination of increasing regulatory approvals, a rapidly expanding clinical pipeline, and continuous innovation in advanced therapies such as CAR-T and immune checkpoint inhibitors. The region benefits from a well-established regulatory framework led by the European Medicines Agency (EMA), which has significantly accelerated oncology drug approvals in recent years, rising to an average of around 14 new cancer medicines annually during 2021–2024.

Recent development activities further highlight this growth trajectory. In March 2025, Europe approved an additional indication for lisocabtagene maraleucel (CAR-T therapy) for follicular lymphoma, reflecting the expansion of cell-based immunotherapies into new cancer segments. Furthermore, in April 2026, the EU approved tovorafen for pediatric glioma, demonstrating continued innovation in targeted and immune-related oncology treatments. On the strategic front, May, 2025 marked a notable acquisition when Helix BioPharma Corp. acquired oncology assets from Laevoroc Immunology AG to strengthen its immuno-oncology pipeline, reflecting increasing consolidation and investment activity in the region.

Additionally, Europe is actively advancing next-generation therapies through extensive clinical trials and collaborative initiatives, particularly in CAR-T and engineered T-cell therapies, with growing efforts to standardize and scale these treatments across the region. Supported by strong healthcare systems, increasing cancer burden, favorable reimbursement frameworks, and cross-border research collaborations, these continuous approvals, product launches, and strategic deals are collectively driving the sustained expansion of the immuno-oncology drugs market in Europe.

Asia-Pacific Immuno-Oncology Drugs Market Trends

The Asia Pacific (APAC) region is emerging as a major growth driver for the immuno-oncology drugs market due to a combination of rising cancer incidence, improving healthcare infrastructure, increasing healthcare expenditure, and strong government support for advanced therapies. Countries such as China, Japan, India, and South Korea are witnessing a significant surge in cancer cases, particularly lung, liver, and gastric cancers, which is accelerating the demand for innovative treatments like immune checkpoint inhibitors and CAR-T cell therapies. In addition, regulatory bodies such as the National Medical Products Administration and the Pharmaceuticals and Medical Devices Agency are actively streamlining approval processes, enabling faster market entry for novel immunotherapies.

The region is also benefiting from increasing clinical trial activity and collaborations between global pharmaceutical companies and local biotech firms to expand access to advanced treatments. For instance, in recent years, several PD-1/PD-L1 inhibitors, such as those developed by domestic players, have received approvals in China, while Japan continues to adopt combination immunotherapy regimens for multiple cancer types. Furthermore, rising investments in biotechnology, expansion of hospital infrastructure, and growing awareness about early cancer diagnosis are supporting market growth. Collectively, these factors position APAC as one of the fastest-growing and most strategically important regions in the global immuno-oncology landscape.

Who are the major players in the immuno-oncology drugs market?

The following are the leading companies in the immuno-oncology drugs market. These companies collectively hold the largest market share and dictate industry trends.

- Bristol-Myers Squibb Company

- Merck & Co., Inc.

- F. Hoffmann-La Roche AG

- AstraZeneca PLC

- Pfizer Inc.

- Regeneron Pharmaceuticals, Inc.

- Sanofi S.A.

- GlaxoSmithKline plc

- Incyte Corporation

- Novartis AG

- Gilead Sciences, Inc.

- Kite Pharma, Inc. (a Gilead Company)

- bluebird bio, Inc.

- Amgen Inc.

- Janssen Pharmaceuticals, and others

How is the competitive landscape shaping the immuno-oncology drugs market?

The competitive landscape of the immuno-oncology drugs market is highly dynamic and increasingly intense, characterized by the dominance of a few global pharmaceutical leaders alongside a rapidly expanding pool of emerging biotech players. Major companies such as Merck & Co., Bristol-Myers Squibb, Roche, and AstraZeneca lead the market with blockbuster immune checkpoint inhibitors like Keytruda, Opdivo, and Tecentriq, collectively holding a significant share of global revenues. The market is moderately concentrated, leveraging strong R&D pipelines, extensive clinical trial programs, and global commercialization capabilities. However, competition is intensifying due to the rapid entry of new players, particularly from Asia, and the growing presence of mid-sized biotech firms focusing on niche indications and novel immune targets. Strategic collaborations, mergers and acquisitions, and co-development agreements have become key competitive strategies to expand product portfolios and accelerate innovation.

Additionally, the competitive focus is shifting from monotherapy to combination therapies (such as PD-1 with CTLA-4, VEGF, or LAG-3 inhibitors), as well as next-generation modalities like bispecific antibodies and CAR-T cell therapies, further diversifying the landscape. The anticipated patent expirations of leading drugs toward the end of the decade are also expected to trigger biosimilar competition and pricing pressures, reshaping market dynamics. Overall, the immuno-oncology drugs market is evolving from a leader-dominated structure to a more fragmented yet innovation-driven ecosystem, where continuous clinical advancements and strategic positioning determine competitive success.

Recent Developmental Activities in the Immuno-Oncology Drugs Market

- In April 2026, the EU approved tovorafen for pediatric glioma, demonstrating continued innovation in targeted and immune-related oncology treatments.

- In February 2026, pembrolizumab (a leading PD-1 inhibitor) received a new approval/label expansion, highlighting the continued dominance and lifecycle extension of checkpoint inhibitors.

- In December 2025, when lisocabtagene maraleucel became the first CAR-T therapy approved for marginal zone lymphoma, demonstrating the expansion of cell therapies into new indications.

- In December 2025, the FDA approved lisocabtagene maraleucel, a CD19-directed autologous CAR T-cell therapy, for adults with relapsed or refractory marginal zone lymphoma after at least two prior lines of systemic therapy. This approval marked a major milestone by bringing CAR T-cell therapy into indolent B-cell lymphomas.

- In October, 2025, the FDA approved a combination of Atezolizumab with lurbinectedin for extensive-stage SCLC maintenance therapy, based on the Phase III IMforte trial, which showed improved survival outcomes.

- In September, 2025, the FDA approved a subcutaneous formulation of pembrolizumab, improving convenience and accessibility for patients. Pembrolizumab (brand name Keytruda) is a humanized monoclonal antibody and a widely used immuno-oncology drug (immunotherapy) that acts as a PD-1 inhibitor.

- In May 2025, Helix BioPharma Corp. acquired oncology assets from Laevoroc Immunology AG to strengthen and expand its immuno-oncology pipeline. The acquisition highlights the growing trend of strategic consolidation, licensing, and investment activities within the immuno-oncology sector, as companies increasingly focus on enhancing their oncology portfolios and accelerating the development of next-generation cancer immunotherapies.

- In March 2025, durvalumab (Imfinzi) received approval in combination therapy for muscle-invasive bladder cancer, marking its expansion into earlier treatment settings.

- In March 2025, Europe approved an additional indication for lisocabtagene maraleucel (CAR-T therapy) for follicular lymphoma, reflecting the expansion of cell-based immunotherapies into new cancer segments.

- In December 2024, the FDA approved a PD-L1 checkpoint inhibitor for advanced cutaneous squamous cell carcinoma, expanding treatment options in skin cancers.

- In December 2024, the FDA approved Durvalumab for limited-stage small cell lung cancer (SCLC) following chemoradiation, expanding immunotherapy use into earlier-stage disease.

|

Report Metrics |

Details |

|

Study Period |

2023 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Immuno-Oncology Drugs Market CAGR |

15.05% |

|

Key Companies in the Immuno-Oncology Drugs Market |

Bristol-Myers Squibb Company, Merck & Co., Inc., F. Hoffmann-La Roche AG, AstraZeneca PLC, Pfizer Inc., Regeneron Pharmaceuticals, Inc., Sanofi S.A., GlaxoSmithKline plc, Incyte Corporation, Novartis AG, Gilead Sciences, Inc., Kite Pharma, Inc. (a Gilead Company), bluebird bio, Inc., Amgen Inc., Janssen Pharmaceuticals, and others. |

|

Immuno-Oncology Drugs Market Segments |

by Therapy Type, by Drug Class, by Cancer Type, by End-Users, and by Geography |

|

Immuno-Oncology Drugs Market Regional Scope |

North America, Europe, Asia Pacific, Middle East, Africa, and South America |

|

Immuno-Oncology Drugs Market Country Scope |

U.S., Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, Australia, South Korea, and key Countries |

Immuno-Oncology Drugs Market Segmentation

- Immuno-Oncology Drugs by Therapy Type Exposure

- Immune Checkpoint Inhibitors

- CAR T-Cell Therapy

- Monoclonal Antibodies

- Cancer Vaccines

- Others

- Immuno-Oncology Drug Class Exposure

- PD-1 Inhibitors

- PD-L1 Inhibitors

- CTLA-4 Inhibitors

- Others

- Immuno-Oncology Drugs Cancer Type Exposure

- Lung Cancer

- Breast Cancer

- Melanoma

- Leukemia

- Lymphoma

- Others

- Immuno-Oncology Drugs End-Users Exposure

- Hospitals

- Cancer Treatment Centers

- Research Institutes

- Others

Immuno-Oncology Drugs Geography Exposure

- North America Immuno-Oncology Drugs Market

- United States Immuno-Oncology Drugs Market

- Canada Immuno-Oncology Drugs Market

- Mexico Immuno-Oncology Drugs Market

- Europe Immuno-Oncology Drugs Market

- United Kingdom Immuno-Oncology Drugs Market

- Germany Immuno-Oncology Drugs Market

- France Immuno-Oncology Drugs Market

- Italy Immuno-Oncology Drugs Market

- Spain Immuno-Oncology Drugs Market

- Rest of Europe Immuno-Oncology Drugs Market

- Asia-Pacific Immuno-Oncology Drugs Market

- China Immuno-Oncology Drugs Market

- Japan Immuno-Oncology Drugs Market

- India Immuno-Oncology Drugs Market

- Australia Immuno-Oncology Drugs Market

- South Korea Immuno-Oncology Drugs Market

- Rest of Asia-Pacific Immuno-Oncology Drugs Market

- Rest of the World Immuno-Oncology Drugs Market

- South America Immuno-Oncology Drugs Market

- Middle East Immuno-Oncology Drugs Market

- Africa Immuno-Oncology Drugs Market

Immuno-Oncology Drugs Market Recent Industry Trends and Milestones (2023-2026):

|

Category |

Key Developments |

|

Immuno-Oncology Product Approval |

The EU approved tovorafen for pediatric glioma, the FDA approved lisocabtagene maraleucel, a CD19-directed autologous CAR T-cell therapy, FDA approved a combination of Atezolizumab with lurbinectedin for extensive-stage SCLC maintenance therapy. |

|

Immuno-Oncology Product Acquisition |

Helix BioPharma Corp. acquired oncology assets from Laevoroc Immunology AG |

|

Company Strategy |

Merck & Co.

Bristol-Myers Squibb · Strengthens its immuno-oncology portfolio with Opdivo and Yervoy by developing dual and triple combination regimens. The company is also investing in next-generation immunotherapies, including cell therapies and checkpoint combinations (e.g., LAG-3 inhibitors), while leveraging strategic acquisitions like Celgene to enhance pipeline depth. |

|

Emerging Technology |

Next-Generation Immune Checkpoint Inhibitors, CAR-T Cell Therapy Advancements, Bispecific Antibodies, Cancer Vaccines (mRNA & Personalized Vaccines), Tumor-Infiltrating Lymphocyte (TIL) Therapy, Oncolytic Virus Therapy, AI and Biomarker-Driven Immunotherapy, Microbiome-Based Immunotherapy, and others |

Impact Analysis

AI-Powered Innovations and Applications:

AI-powered innovations are playing a transformative role in advancing the field of immuno-oncology by enabling a shift toward highly personalized, data-driven cancer care. With the increasing complexity of tumor biology and immune system interactions, artificial intelligence, particularly machine learning and deep learning, is being widely adopted to process and analyze vast multi-omics datasets, including genomics, transcriptomics, proteomics, and real-world clinical data. These technologies help identify novel biomarkers and predict patient response to immunotherapies such as checkpoint inhibitors, thereby improving patient selection and treatment outcomes. Companies like IBM Time are leveraging AI platforms to integrate clinical and molecular data, supporting oncologists in making more precise treatment decisions. In drug discovery, AI is significantly reducing timelines and costs by identifying new immune targets, predicting drug target interactions, and optimizing antibody engineering, which is critical for the development of next-generation immunotherapies.

Furthermore, AI is revolutionizing clinical trials by enabling smarter patient recruitment, real-time monitoring, and adaptive trial designs, thus increasing trial efficiency and success rates. In diagnostics, AI-powered imaging and digital pathology tools are enhancing tumor microenvironment analysis by accurately identifying immune cell infiltration patterns and tumor heterogeneity; companies such as PathAI are at the forefront of this innovation. Additionally, AI is being used to design personalized cancer vaccines by identifying tumor-specific neoantigens and to optimize combination therapy regimens by predicting synergistic drug interactions. Emerging applications also include the use of natural language processing (NLP) to extract insights from unstructured medical records and scientific literature, as well as AI-driven modeling of immune system dynamics to better understand resistance mechanisms. Overall, AI is not only accelerating innovation across the immuno-oncology value chain from discovery and development to diagnosis and treatment but also improving clinical outcomes by enabling more targeted, efficient, and individualized therapeutic approaches.

U.S. Tariff Impact Analysis on Immuno-Oncology Drugs Market:

The U.S. tariff impact on the immuno-oncology drugs market is becoming increasingly significant, particularly following the 2026 implementation of Section 232 tariffs on patented pharmaceuticals and biologics, which include many high-value immuno-oncology therapies such as checkpoint inhibitors and cell therapies. Under this policy, tariffs of up to 100% on imported patented drugs and associated active pharmaceutical ingredients (APIs) are anticipated to significantly increase the overall cost burden for pharmaceutical manufacturers and healthcare systems, as well as disrupt established global supply chains. Since immuno-oncology products are typically high-cost, patented biologics, they are more exposed to these tariffs compared to generics and biosimilars, which are largely exempt, thereby creating pricing pressures, reducing affordability and patient access, and compelling companies to shift toward domestic manufacturing and localized production strategies to mitigate financial impact. This is expected to create pricing pressures, potentially increasing treatment costs and limiting patient access, while also forcing pharmaceutical companies to reassess supply chain strategies, including reshoring manufacturing to the U.S. to avoid tariff burdens.

Additionally, tariffs on APIs and key raw materials, many of which are sourced from countries like China and India, can disrupt production and lead to delays or shortages in critical oncology therapies. From a strategic perspective, while tariffs may encourage domestic production and strengthen U.S.-based manufacturing capabilities in the long term, in the short term, they are likely to reduce profit margins, slow innovation investments, and create operational challenges for global immuno-oncology players. Overall, the U.S. tariff environment introduces both risks and structural shifts in the immuno-oncology drugs market, balancing between supply chain localization benefits and increased cost and access challenges.

How This Analysis Helps Clients

- Cost Management: By understanding the tariff landscape, clients can anticipate cost increases and adjust pricing strategies accordingly, ensuring profitability.

- Supply Chain Optimization: Clients can identify alternative sourcing options and diversify their supply chains to reduce dependency on high-tariff regions, enhancing resilience.

- Regulatory Navigation: Expert guidance on navigating the evolving regulatory environment helps clients maintain compliance and avoid potential legal challenges.

- Strategic Planning: Insights into tariff impacts enable clients to make informed decisions about manufacturing locations, partnerships, and market entry strategies.

Key takeaways from the immuno-oncology drugs market report study

- Market size analysis for the current immuno-oncology drugs market size (2025), and market forecast for 8 years (2026 to 2034)

- Top key product/technology developments, mergers, acquisitions, partnerships, and joint ventures happened over the last 3 years.

- Key companies dominating the immuno-oncology drugs market.

- Various opportunities available for the other competitors in the immuno-oncology drugs market space.

- What are the top-performing segments in 2025? How these segments will perform in 2034?

- Which are the top-performing regions and countries in the current immuno-oncology drugs market scenario?

- Which are the regions and countries where companies should have concentrated on opportunities for the immuno-oncology drugs market growth in the future.

Startup Funding & Investment Trends:

|

Company Name |

Total Funding |

Stage of Development |

Main Product |

Core Technology |

|

NexCure Inc. |

$19 million |

Series A |

CAR-T therapy delivery platform for outpatient settings |

To expand access to advanced immunotherapies by enabling decentralized delivery of CAR-T and other cell therapies, addressing infrastructure and capacity constraints in oncology care |