Neuroprotection Devices: Advancing Brain Protection Through Medical Innovation

Nov 19, 2025

Table of Contents

The preservation of neuronal function following acute insults, such as ischemic events, traumatic brain injury (TBI), or cardiac arrest, represents one of the most significant challenges in modern critical care and neurology. Neuroprotection encompasses strategies and devices designed to minimize secondary injury and maintain the structural and functional integrity of the central and peripheral nervous systems. The global market for neuroprotection devices is driven by the rising incidence of cardiovascular and neurological disorders, coupled with technological advancements aimed at real-time monitoring and interventional damage control.

Categorization and Functional Spectrum of Neuroprotection Technologies

Neuroprotection devices are broadly classified based on their mechanism of action, ranging from mechanical intervention and physiological modulation to sophisticated bio-engineered solutions.

Downloads

Click Here To Get the Article in PDF

Recent Articles

- Laborie Medical Acquired Urotronic; Sirtex’s LAVA Liquid Embolic System; Paige’s Cancer Detection...

- Zimmer Biomet Wins FDA Breakthrough Status for Iodine-Treated Hip Implant; Terumo Gains U.S. Clea...

- Algernon’s NP-120 (ifenprodil); Pieris’s cinrebafusp alfa (PRS-343) clinical trial; Gaumard...

- The Question That Remains Unanswered: What Might Be Causing Alzheimer’s?

- Innovative RoA in Traumatic Brain Injury Treatment: Intranasal and Intrathecal Approaches

Strategies for Ischemic Insult Prevention: Cerebral Embolic Protection Devices (CEPDs)

Cerebral Embolic Protection Devices (CEPDs) are a critical subset of neuroprotective tools, primarily used during cardiovascular procedures like Transcatheter Aortic Valve Replacement (TAVR) or carotid artery stenting. These devices are designed to capture and filter or deflect embolic debris that could otherwise travel to the cerebral vasculature, potentially causing stroke. Their application represents a direct, mechanical approach to neuroprotection, offering immediate mitigation of procedure-related cerebral ischemia.

Modulating Metabolism for Cerebral Salvage: Controlled Therapeutic Hypothermia Systems

Controlled Therapeutic Hypothermia Systems involve the controlled lowering of the body’s core temperature. This induced metabolic state is highly neuroprotective, as it reduces the brain’s oxygen and energy demand, suppresses excitotoxicity, stabilizes the blood-brain barrier, and mitigates inflammatory response following an injury (such as cardiac arrest or severe TBI). These systems require highly sophisticated feedback loops for precise temperature management, employing external or endovascular cooling methods.

Real-time Vigilance for Neural Integrity: Intraoperative Neurophysiological Monitoring (IONM)

Intraoperative Neurophysiological Monitoring (IONM) Systems are not directly interventional but provide critical, real-time neuroprotection through surveillance. By monitoring the electrical activity of the central and peripheral nervous systems (e.g., using Somatosensory Evoked Potentials (SSEPs), Motor Evoked Potentials (MEPs), or Electromyography (EMG)), IONM allows surgical teams to detect impending neural injury during complex procedures. This early warning enables immediate surgical adjustments, thereby preventing permanent neurological deficits.

Advanced Neurotherapeutic Delivery Platforms and Cell-Based Interventions

This category represents the future of pharmacological and biological neuroprotection:

- Drug Delivery Devices: Includes specialized catheters, micro-pumps, and targeted nanoparticle systems designed to bypass the Blood-Brain Barrier (BBB) and deliver neuroprotective agents (e.g., anti-excitotoxic, anti-apoptotic, or anti-inflammatory drugs) directly to the site of injury in a sustained manner. The global drug delivery devices market is expected to grow from USD 492 billion in 2024 to USD 760 billion by 2032, reflecting strong, sustained growth at a CAGR of 5.66%. The increasing prevalence of chronic diseases primarily drives the market for drug delivery devices, the growing demand for self-administration and home healthcare, the increased use of biologics and biosimilars, technological advancements, and increased product development activities among key market players.

- Cell-Based Neuroprotection: Involves the use of stem cells or progenitor cells, delivered systemically or locally, which can promote tissue repair, modulate the inflammatory environment, release neurotrophic factors, and potentially replace damaged neurons.

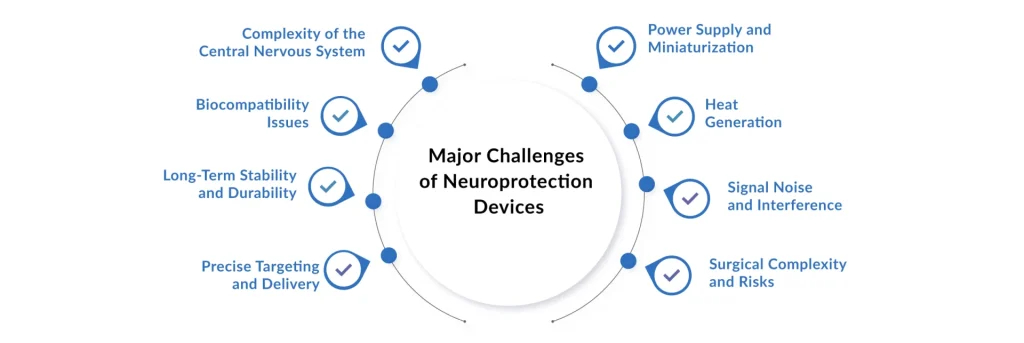

Translational Hurdles and Technical Constraints in Neuroprotection Implementation

Despite significant research, the widespread commercial adoption and clinical success of many neuroprotection devices and therapies face substantial obstacles:

- Challenge of Translation: Many promising neuroprotective agents and strategies successful in preclinical models have failed in human clinical trials, highlighting a fundamental gap in translating animal models of injury to complex human pathophysiology.

- Optimal Timing and Dose: For many interventional techniques (like hypothermia or drug delivery), determining the precise therapeutic window, duration, and optimal ‘dose’ (e.g., target temperature or drug concentration) remains a critical challenge.

- Technical Complexity: Devices like CEPDs or advanced IONM systems require highly specialized training and infrastructure. Ineffective deployment can negate their protective benefits or introduce new complications.

- Variability in Patient Response: The heterogeneity of neurological injuries and patient comorbidities complicates standardized treatment protocols, often leading to unpredictable clinical outcomes.

Complementary Modalities: The Regulatory and Multimodal Landscape

Multimodal and Integrated Neuroprotection Protocols

The trend in neuroprotection is moving away from single-target interventions toward synergistic multimodal protocols. This involves the simultaneous application of complementary strategies, such as:

- Combining IONM for surveillance with CEPDs for mechanical protection.

- Integrating controlled normothermia maintenance (a form of neuroprotection) with BBB-penetrant drug delivery.

- Optimizing systemic factors (e.g., blood pressure, oxygenation) to support the primary neuroprotective device.

Regulatory and Reimbursement Landscape

A crucial driver and challenge for the market is the regulatory pathway. Devices must demonstrate not just safety but also significant, measurable clinical efficacy in preventing stroke or improving long-term neurological outcome, which can be a protracted and costly process. Furthermore, reimbursement policies from national health authorities and private payers determine commercial viability, favoring devices with compelling cost-benefit evidence and demonstrated patient benefit.

Global Neuroprotection Devices Market Trajectory: Competitive Landscape and Future Outlook

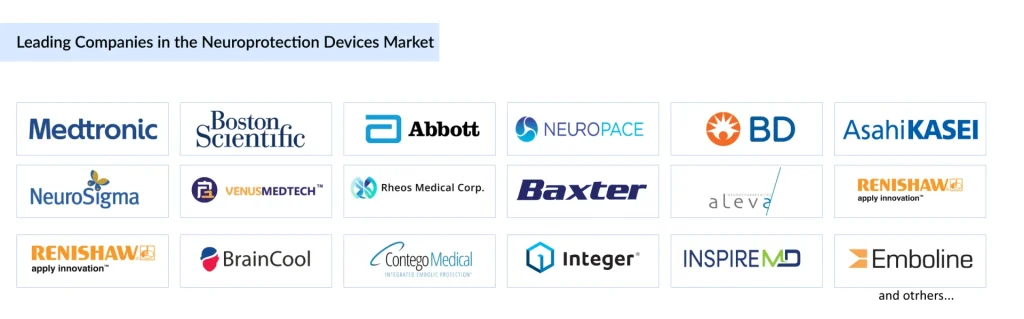

The embolic protection devices market, a significant component of the broader neuroprotection sector, was valued at approximately USD 648 million in 2024 and is expected to reach USD 1.6 billion by 2032, growing at a CAGR of 7.58%. On the other hand, the global neuroprotection devices market is growing at a CAGR of 6.87% during the forecast period from 2025 to 2032. Currently, the market is moderately consolidated, with the top four players, Medtronic, Boston Scientific, Abbott, and Cordis (a Cardinal Health company), accounting for approximately 90% of market share.

Other significant competitors include NeuroPace, Inc., BD, Asahi Kasei Corporation, NeuroSigma, Inc., Venus Medtech (Hangzhou) Inc., Rheos Medical Corp., Baxter, Aleva Neurotherapeutics, Renishaw plc., Belmont Medical Technologies, BrainCool AB, Contego Medical, Inc., Integer Holdings Corporation, InspireMD Inc., Emboline, Inc., Keystone Heart Ltd., Lepu Medical Technology (Beijing) Co., Ltd., and others. Companies are pursuing strategies including technological innovation, strategic partnerships, regulatory approvals, and geographical expansion to strengthen their market positions.

North America maintains the largest market share, driven by its advanced healthcare infrastructure, high cardiovascular disease prevalence, substantial R&D investment, and strong regulatory support. The region is projected to experience the fastest growth through 2032, supported by ongoing product launches and favorable reimbursement policies. Europe is the second-largest market, while the Asia-Pacific region is expected to exhibit significant growth driven by improvements in healthcare infrastructure, rising healthcare expenditure, and increasing awareness of interventional procedures.

The field of neuroprotection devices stands at a transformative juncture. As cardiovascular disease prevalence continues rising, with approximately 640 million people living with heart and circulatory diseases globally and 200 million affected by coronary heart disease, the demand for effective neuroprotection during interventional procedures will intensify.

Several factors will drive continued market expansion: aging global populations with increased susceptibility to neurovascular disorders, technological innovations producing safer and more effective devices, expanding clinical indications beyond traditional applications, growing awareness among clinicians about procedural stroke prevention, and favorable regulatory environments supporting innovation.

The integration of neurotechnology with wearable sensors, artificial intelligence, and advanced imaging promises platforms for disease prevention and early diagnosis, shifting healthcare from reactive treatment to proactive prevention. Brain-computer interfaces and neural prostheses will continue advancing, offering new possibilities for patients with paralysis, neurodegenerative diseases, and other neurological conditions. Overall, the continued convergence of neuroscience, bioengineering, and clinical medicine positions neuroprotection devices at the forefront of 21st-century healthcare innovation.

Downloads

Article in PDF

Recent Articles

- Innovative RoA in Traumatic Brain Injury Treatment: Intranasal and Intrathecal Approaches

- Philips Teamed with SyntheticMR; BioPhotas’s Celluma Light Therapy; Boston Scientific’s AGE...

- CereVasc’s eShunt System Study; FDA Approves NGS-Based CDx for Trastuzumab Deruxtecan; Nanopath S...

- Laborie Medical Acquired Urotronic; Sirtex’s LAVA Liquid Embolic System; Paige’s Cancer Detection...

- Algernon’s NP-120 (ifenprodil); Pieris’s cinrebafusp alfa (PRS-343) clinical trial; Gaumard...