Top Obesity Drugs by Revenue in 2025: The Biggest Winners in the Weight Loss Market

Jul 10, 2026

Table of Contents

Summary

- The obesity treatment market has shifted from a niche category to a major pharma growth engine, with revenues in the leading markets rising from about $16 billion in 2025 to a projected $80 billion by 2034 and potentially more than $100 billion by 2036.

- Eli Lilly led the category in 2025, driven by MOUNJARO and ZEPBOUND; Lilly’s obesity and diabetes portfolio generated more than $36 billion in 2025 sales, and the company said those products helped power its record revenue growth.

- Novo Nordisk’s WEGOVY and OZEMPIC remained major revenue drivers, but Lilly’s faster growth shifted the competitive balance in Lilly’s favor across the GLP-1 market.

- The market is entering a new phase beyond injectables, with both Novo Nordisk’s WEGOVY pill and Lilly’s FOUNDAYO (orforglipron) approved in 2025–2026, making oral GLP-1s the next big battleground.

The obesity treatment market isn’t just growing, it’s exploding at a pace few therapeutic categories have ever matched. The obesity medicines market across the leading markets (the US, EU4, the UK, and Japan) reached $16 billion in 2025 across the 7MM, and is forecast to rise to $80 billion in 2034, before reaching between $100 billion by 2036. To put that in perspective: a single drug class has become so lucrative that it single-handedly vaulted a 150-year-old insulin company into the trillion-dollar club.

Downloads

Click Here To Get the Article in PDF

Recent Articles

- An Insight Into the Weight Loss and Obesity Market

- Booming Healthcare sector in MENA: Lucrative opportunity for Global pharma players

- Assessing the Growing Role & the Demand of Chronic Disease Management Apps

- Novo Nordisk vs. Eli Lilly: The Battle for Anti-Obesity Drug Market Dominance

- Future Avenues for Prediabetes Treatment: The Road Ahead

Here’s a number that should stop any pharma strategist mid-scroll: the total prevalent cases of obesity are expected to rise from ~194 million in 2025 to ~228 million by 2036 across the leading markets, as per DelveInsight., and a 2025 FAIR Health study found that more than 2% of all U.S. adults were already taking a GLP-1 specifically for weight loss in 2024, a figure that has only climbed since. One molecule, tirzepatide, became the best-selling drug on the planet in Q3 2025, dethroning Merck’s KEYTRUDA, a cancer blockbuster that took the crown for years. That’s the scale of disruption happening in the obesity treatment market right now.

This isn’t a niche corner of pharma anymore. It’s the new center of gravity. For anyone tracking the pharma companies’ obesity drug space, the obesity management market, or the broader obesity drug development pipeline, 2025 was the year the duopoly of Eli Lilly and Novo Nordisk turned obesity into the most-watched battlefield in the industry, and 2026 is shaping up to be even bigger.

Why the Obesity Market Got This Big, This Fast

Before the rankings, it helps to understand what’s fueling this surge. Causes of obesity are multifactorial, genetics, sedentary lifestyles, ultra-processed diets, sleep disruption, certain medications, and, in some cases, acquired hypothalamic obesity resulting from tumors, surgery, or radiation affecting the brain’s appetite-regulating centers. What changed in the last five years isn’t the disease; it’s the treatment. What advances have been made in anti-obesity pharmacotherapy over the last five years, and are they reaching the patients who need them in the US? The honest answer is: tremendous advances, uneven access. GLP-1 and GLP-1/GIP dual agonists have delivered weight loss approaching surgical outcomes without a scalpel, but high list prices, insurance exclusions, and supply constraints have kept large swaths of the eligible population on the sidelines, even as the US obesity management market races ahead in dollar terms.

Now, let’s count down the top-selling obesity drugs of 2025, from smallest to largest by global revenue.

MOUNJARO: Eli Lilly’s Diabetes Powerhouse Leading the Pack

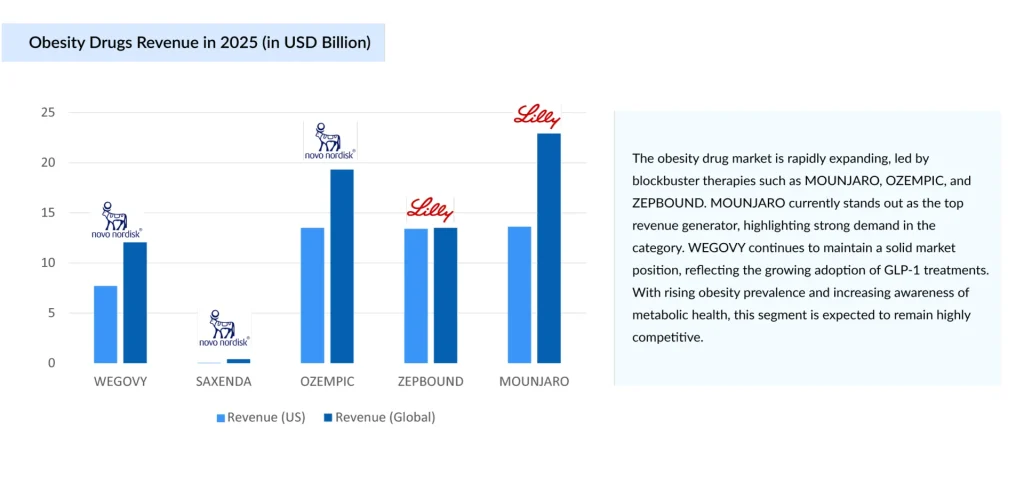

MOUNJARO, Eli Lilly’s dual GIP/GLP-1 receptor agonist approved for type 2 diabetes, ended 2025 as the single highest-revenue product in this entire category. Though, like OZEMPIC, technically a diabetes-labeled product whose off-label and adjacent obesity use has been massive. MOUNJARO nearly doubled sales in 2025 to $22.9 billion, and combined with ZEPBOUND, MOUNJARO generated $9.0 billion in H1 2025 alone, up 90% year-over-year, while ZEPBOUND added $5.7 billion in the same half. By Q3 2025, the tirzepatide franchise as a whole had become a phenomenon: tirzepatide topped $10 billion in the third quarter, officially becoming the world’s best-selling drug, surpassing Merck’s KEYTRUDA, which brought in $8.1 billion that quarter.

The financial knock-on effect for Lilly has been staggering. Lilly posted $65.18 billion in FY2025 revenue, up 44.7% year-over-year, the largest growth rate among the top 20 pharma companies, vaulting it past Merck, Pfizer, and AbbVie into the No. 1 spot in pharma for the first time. In November 2025, Lilly became the first pharma company to enter the trillion-dollar club, joining the ranks of tech giants like Nvidia, Apple, Microsoft, and Alphabet. Tirzepatide’s dominance is the single biggest reason the obesity market overtook so many legacy therapeutic categories in such a short window, and it’s a case study that will be taught in business schools for years on how top pharma companies in obesity drug space can pivot an entire corporate trajectory around one molecule.

The remarkable surge in MOUNJARO’s adoption is driven by several key factors. Its superior clinical performance has played a major role, as tirzepatide’s dual mechanism of action, targeting both GIP and GLP-1 receptors, has consistently demonstrated greater average weight loss than semaglutide in head-to-head clinical trials while delivering excellent glycemic control. This has made it an increasingly preferred treatment for patients living with both type 2 diabetes and obesity.

Growth has also been supported by Eli Lilly’s aggressive manufacturing expansion, with billions of dollars invested in new API and fill-finish production facilities throughout 2024 and 2025, significantly easing the supply constraints that limited the drug’s early commercial uptake. Additionally, positive cardiovascular and renal outcomes have strengthened MOUNJARO’s clinical value, leading to expanded prescribing across a broader patient population, particularly those with type 2 diabetes who are at increased risk of cardiovascular and kidney complications. Together, these factors have accelerated physician confidence, improved product availability, and expanded the drug’s market reach.

For anyone tracking the Eli Lilly GLP-1 drugs pipeline, MOUNJARO is the foundation asset, the commercial engine funding the company’s next wave of new GLP-1 competitors to its own products, including the oral candidate orforglipron.

OZEMPIC: Novo Nordisk’s Diabetes Flagship, Still a Juggernaut

Technically approved for type 2 diabetes, not obesity, OZEMPIC deserves a mention because its off-label and adjacent use in weight management has been enormous, and its revenue dwarfs almost everything else in the cardiometabolic space. OZEMPIC brought in $19.3 billion in 2025, making it one of the highest-grossing pharmaceutical products in the world, obesity-label or not. Its commercial footprint has been instrumental in normalizing GLP-1 therapy and expanding the broader obesity treatment conversation well beyond the clinic.

In 2025, several key factors supported the continued growth of OZEMPIC. One of the primary drivers was the expansion of its approved cardiovascular and renal indications. Backed by positive outcomes from clinical trials, updated labeling positioned OZEMPIC as a preferred treatment not only for glycemic control in patients with type 2 diabetes but also for those at elevated risk of cardiovascular disease and chronic kidney disease, significantly broadening its eligible patient population.

Growth was also fueled by Novo Nordisk’s continued international expansion. Markets across Europe, China, and several emerging economies delivered strong demand, helping offset increasing pricing pressures in the United States. At the same time, Novo’s agreement to participate in US Most Favoured Nation–style pricing arrangements and Medicare Part D negotiations is expected to compress per-unit revenue going into 2026, a trend worth watching for anyone trying to evaluate the healthcare company Novo Nordisk on GLP-1 drugs for weight loss and diabetes care more broadly.

OZEMPIC’s slide to second place doesn’t signal weakness; it signals just how explosively its closest rival has grown. This shift is one of the most closely watched data points in any Novo Nordisk vs Eli Lilly GLP-1 weight loss market analysis published over the past year.

ZEPBOUND: The Fastest-Growing Obesity Brand in the Portfolio

ZEPBOUND, the obesity-indicated version of tirzepatide, had an extraordinary year. ZEPBOUND, Eli Lilly’s tirzepatide brand specifically indicated for chronic weight management, posted roughly $13.5 billion in 2025 sales, a jaw-dropping 175% increase over the prior year, making it the fastest-growing of the five drugs on this list by a wide margin.

ZEPBOUND’s growth curve illustrates just how quickly the GLP-1 obesity drugs pipeline has matured from a niche specialty category into a mainstream consumer health category. Lilly’s rapid success with ZEPBOUND has been fueled by several strategic factors. The company expanded patient access through direct-to-consumer self-pay and direct-ship programs, reducing barriers for individuals without comprehensive insurance coverage for weight-loss therapies and significantly widening the addressable market.

At the same time, ZEPBOUND strengthened its competitive position by highlighting superior efficacy in head-to-head clinical studies against semaglutide-based therapies, reinforcing its advantage in the increasingly competitive GLP-1 weight-loss market. Additionally, Lilly’s substantial manufacturing investments began yielding results in 2025, enabling the company to overcome earlier supply constraints and meet the strong demand that had been accumulating since the drug’s launch.

Combined, MOUNJARO and ZEPBOUND delivered more than $36 billion in 2025, enough to make Eli Lilly’s tirzepatide franchise one of the largest pharmaceutical revenue lines ever recorded, less than four years after launch.

WEGOVY: Novo Nordisk’s Obesity-Care Anchor

WEGOVY, semaglutide’s purpose-built obesity formulation, is where Novo Nordisk’s weight-loss franchise truly lives. WEGOVY sales reached $12.05 billion in 2025, and combined with SAXENDA, obesity products SAXENDA and WEGOVY together delivered $12.5 billion, reflecting very strong demand despite supply constraints. Novo Nordisk’s WEGOVY was a genuine watershed product: in March 2024, it became the first obesity medication approved to reduce cardiovascular risk, cutting major adverse cardiovascular events by 20% in high-risk adults. It also broke new ground again at the very end of 2025, when the oral pill form of WEGOVY became the first oral GLP-1 receptor agonist approved for obesity treatment, opening up a needle-free pathway that could meaningfully widen the antiobesity prescription drug market.

WEGOVY remains central to Novo’s identity as the pioneer of the anti-obesity GLP-1 category and continues to serve as the company’s flagship growth driver beyond its diabetes portfolio. The drug’s momentum has been strengthened by the expansion of its label to include the reduction of major adverse cardiovascular events in overweight or obese adults with established cardiovascular disease, significantly broadening its adoption among cardiologists in addition to endocrinologists and obesity specialists.

At the same time, Novo has pushed hard on next-generation formats, including an oral semaglutide pill and a higher-dose “HD” injectable version, both clear signals of where the GLP-1 obesity drugs pipeline is headed industry-wide. However, WEGOVY’s growth rate has cooled relative to ZEPBOUND’s, a clear marker in the ongoing Novo Nordisk vs Eli Lilly GLP-1 weight loss market comparison that Lilly’s tirzepatide franchise is currently winning the growth race, even as Novo retains a large global volume base.

Novo has responded with notable strategic moves, including price cuts of up to 70% in parts of the US market, a bet that higher volume at lower price points can offset margin compression and defend market share against ZEPBOUND’s momentum.

SAXENDA: The Foundation of Novo Nordisk’s Obesity Franchise

SAXENDA, Novo Nordisk’s older liraglutide-based injectable, is the elder statesman of this list. Approved for weight loss back in 2014, it’s been steadily overshadowed by next-generation GLP-1s. SAXENDA generated an estimated $493.4 million in global revenue in 2025, with approximately $40.8 million in sales coming from the US, reflecting a slight decline in global share as next-gen, more potent GLP-1 and GIP/GLP-1 therapies like WEGOVY and ZEPBOUND have entered the market. It remains relevant chiefly in markets where access to newer therapies is still limited.

The Oral Disruption: A New Front Opens in 2026

The latest GLP-1 obesity drugs developments are no longer just about injectables. The end of 2025 brought the first oral GLP-1 medication for obesity treatment, a pill form of Wegovy. Lilly answered almost immediately: on April 1, 2026, the FDA approved FOUNDAYO (orforglipron), Eli Lilly’s once-daily oral GLP-1 for obesity, the first oral GLP-1 approved for weight management as a small molecule, and the fastest new molecular entity approval since 2002, clearing the FDA under the Commissioner’s National Priority Voucher program just 50 days after filing.

The two oral drugs are already being compared head-to-head in clinical conversation, if not formal trials: at the highest dose, Lilly’s orforglipron led to 11.2% average body weight loss over nearly 17 months, while the Wegovy pill has touted higher numerical results in its own trials, though the two drugs haven’t actually been tested head-to-head to determine superiority.

This oral wave matters enormously for the FDA approved anti-obesity medications indications 2025 landscape and beyond, because pills solve two of the biggest barriers slowing adoption: needle aversion and manufacturing-driven supply shortages. Easier production, in turn, could meaningfully lower costs, a critical lever given that these GLP-1 drugs can cost upwards of $1,000 a month at list price.

What’s Next: Combinations, Triple Agonists, and Amylin’s Moment

If 2025 was about GLP-1 monotherapy dominance, the next wave of obesity drugs in development is about combining and layering mechanisms for even deeper, more durable weight loss. What new combinations of incretin plus other mechanisms for obesity are in trials, and which sponsors are leading? Three threads stand out:

Triple agonists. Lilly’s retatrutide, targeting GIP, GLP-1, and glucagon receptors simultaneously, just delivered the most dramatic efficacy data yet seen in a Phase 3 obesity trial. In the TRIUMPH-1 study, people on the highest 12mg dose lost an average of 25% of their body weight at 80 weeks, compared with just 3.9% on placebo, with severely obese patients on escalated doses losing up to 30% of body weight over two years. For comparison, the highest available doses of tirzepatide and semaglutide have both shown around 20% weight loss after 72 weeks in earlier trials. Lilly is also studying retatrutide for knee osteoarthritis, where it has shown up to 28.7% average weight loss alongside significant pain reduction, with regulatory submission expected in 2026. The Pharmaceutical Journal + 2

Eli Lilly eloralintide development status, obesity treatment. Amylin agonism is the other big mechanism Lilly is betting on. Eloralintide, an investigational once-weekly selective amylin receptor agonist, demonstrated superior mean weight reductions of 9.5% to 20.1% compared to 0.4% with placebo in a Phase 2 trial of 263 adults with obesity, with improvements also seen across waist circumference, blood pressure, lipids, glycemic control, and inflammation markers. Lilly plans to initiate Phase 3 enrollment by the end of 2025, and is also testing eloralintide in combination with tirzepatide, a clear signal that incretin-plus-amylin combination therapy is one of the leading next-generation strategies, distinct from pure incretin mechanisms and potentially offering a more tolerable side-effect profile.

A widening competitive field. The duopoly era is ending. 2025 saw a bidding war between Pfizer and Novo Nordisk for obesity biotech Metsera, ultimately won by Pfizer for up to $10 billion, while in 2026, AstraZeneca’s partnership with China’s CSPC reflects growing interest in Chinese obesity-drug innovation and manufacturing, together signaling a market that will cease to be a two-company race and instead be actively contested by multiple major pharmaceutical players. Roche, too, has entered the fray, dropping $1.65 billion upfront with up to $3.6 billion more in milestones to partner with Zealand Pharma on its long-acting amylin analog petrelintide for obesity.

So, which companies are best positioned in obesity treatment based on current brands and late-stage pipeline? On current evidence, Eli Lilly holds the strongest combined position, commercial dominance through MOUNJARO/ZEPBOUND, a first-mover oral small molecule in Foundayo, and the deepest late-stage pipeline spanning retatrutide and eloralintide. Novo Nordisk remains a close second, with first-mover advantage in oral peptide delivery and a broad real-world evidence base, though it faces headwinds from leadership turnover and pricing pressure. Pfizer, Roche, and AstraZeneca represent the most credible “third wave” challengers, each anchoring their obesity ambitions in M&A and external partnerships rather than purely organic pipelines.

The Future of Obesity Treatments

The future of obesity treatments looks less like a single blockbuster drug and more like a layered toolkit: incretins for broad efficacy, amylin agonists for tolerability and combination potential, triple agonists for maximal weight loss, and oral formulations for access and convenience. Add in the likely entrance of muscle-preservation therapies, comorbidity-specific label expansions (cardiovascular, MASH, osteoarthritis, sleep apnea), and a genuinely competitive field beyond Lilly and Novo, and the next five years could make 2025’s numbers look almost modest by comparison.

For an industry that spent decades treating obesity as a lifestyle issue rather than a chronic disease, this is a remarkable turnaround. The science has finally caught up to the scale of the problem, and the revenue numbers prove that the market has noticed. The only open question left is how fast affordability and access can catch up to the science, because the molecules, clearly, are no longer the bottleneck.

Downloads

Article in PDF

Recent Articles

- Commercial

- Redefining Liver Disease in the Metabolic Era: From NASH to MASH and the Rise of Obesity‐targeted...

- Novo Nordisk vs. Eli Lilly: The Battle for Anti-Obesity Drug Market Dominance

- The Race to Redefine Obesity Treatment

- Assessing the Growing Role & the Demand of Chronic Disease Management Apps