The gMG Treatment Gold Rush: Key Companies Racing Toward Breakthrough Launches by 2036

Apr 24, 2026

Table of Contents

Summary

- Generalized Myasthenia Gravis (gMG) is a chronic autoimmune neuromuscular disorder, with ~195,000 diagnosed patients across seven major markets in 2025, projected to reach ~250,000 by 2036.

- Despite recent approvals of FcRn blockers and complement inhibitors, major unmet needs remain, including unpredictable treatment response, disease recurrence, and steroid-free durable remission.

- Leading companies such as Novartis, Alexion AstraZeneca Rare Disease, Cabaletta Bio, UCB, Immunovant, Roivant Sciences, Cartesian Therapeutics, Merck KGaA, RemeGen, Regeneron Pharmaceuticals, and others are evaluating their lead assets, eyeing to capture a significant share of the gMG market.

Generalized Myasthenia Gravis is not a rare disease in the shadows anymore. Once treated with blunt-force immunosuppression and little else, gMG has become one of the hottest arenas in rare neuromuscular disease drug development, drawing in some of the world’s largest pharmaceutical companies alongside nimble biotechs armed with transformative technologies.

Downloads

Click Here To Get the Article in PDF

Recent Articles

- FcRn Inhibitors for Autoimmune Disorders: A Promising Therapeutic Approach

- FcRn Inhibitors Being The Fastest Growing Class, Plans To Get Explored In 20+ Indications

- Can FcRn Antagonists Be The Game-Changer in the Generalized Myasthenia Gravis (gMG) Treatment Mar...

- Biogen’s Aduhelm; FDA Approves Sanofi’s Enjaymo; NHS & Orchard Signs a Deal; Bri...

- VBL Therapeutics’ VB-111 (ofranergene obadenovec); BMS’s mavacamten (Camzyos); Merck’s KEYTRUDA; ...

The disease, a chronic autoimmune disorder in which antibodies disrupt signaling at the neuromuscular junction, affects roughly 195,000 diagnosed gMG patients across the seven major markets today, a number expected to approach 250,000 by 2036. The underlying patient need remains enormous: despite recent FDA approvals of FcRn blockers and complement inhibitors, key unmet needs persist, including unpredictable treatment response, disease recurrence, and the near-impossible challenge of achieving steroid-free, durable remission.

Key Companies, One Disease, A Decade of Change

What’s unfolding now is a remarkable convergence of mechanistic innovation, from RNA-based CAR-T cells and dual complement inhibitors to BTK antagonists and BLyS/APRIL dual-blockade. Below, we profile the leading companies whose pipeline assets are poised to reshape this landscape before 2036, drawing on data from a comprehensive market forecast report covering the US, EU4, the UK, and Japan.

Novartis

Novartis is one of the most strategically positioned players in the gMG pipeline, and uniquely so, because it is running two distinct mechanistic programs simultaneously. That kind of depth signals a genuine long-term commitment to gMG, not a one-bet wonder.

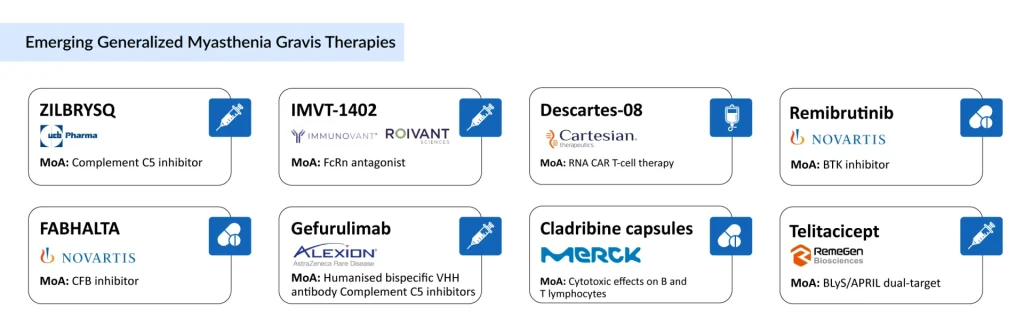

Remibrutinib is a highly selective, covalent BTK inhibitor being evaluated in Phase III for gMG. BTK inhibition is a significant upstream strategy: rather than mopping up the IgG antibodies that damage the neuromuscular junction, remibrutinib targets the B-cell signaling pathway that drives their production in the first place. As an oral agent, rare in this space dominated by IV and subcutaneous biologics, it carries obvious appeal for patients and payers alike. Regulatory filing is anticipated in 2028 or later.

Ramandeep Singh, Senior Consultant of Forecasting at DelveInsight, said that its late-stage development timeline and the increasingly competitive landscape, featuring FcRn inhibitors, complement inhibitors, and other biologics, may pose challenges to market uptake. If successful, however, remibrutinib’s convenient oral dosing and differentiated mechanism of action could position it well, particularly among patients seeking targeted, steroid-sparing treatment alternatives, as per Singh.

FABHALTA (Iptacopan), already approved for paroxysmal nocturnal hemoglobinuria, is being repurposed for gMG in Phase III. It is an oral proximal complement inhibitor targeting factor B of the alternative pathway. Novartis has planned its regulatory submission for 2027, making FABHALTA the earlier of its two gMG filings. The oral route of administration and the distinct complement pathway target differentiate it from the already-crowded C5 inhibitor space.

Sadaf Javed, Manager of Forecasting and Analytics at DelveInsight, said that with its oral administration and potential applicability across a range of complement-mediated conditions, Iptacopan may establish a distinct position in the gMG treatment landscape, particularly for patients who do not achieve adequate control with current therapies.

Alexion AstraZeneca Rare Disease

If any company has gMG sewn into its institutional DNA, it is Alexion, the inventors of SOLIRIS (eculizumab), the first biologic to crack the complement pathway in this disease. Now operating under AstraZeneca’s rare disease umbrella, Alexion is pushing complement inhibition to its next evolutionary form with gefurulimab.

Gefurulimab is a half-life extended bispecific antibody that simultaneously targets C5 and human serum albumin, a design meant to achieve deeper, longer-lasting C5 blockade with potentially less frequent dosing. The Phase III PREVAIL trial delivered remarkable results: in October 2025, gefurulimab showed statistically significant and clinically meaningful improvement in MG-ADL scores at Week 26 in adults with gMG, with improvements observed as early as Week 1 and sustained across the study. All primary and secondary endpoints were met.

Alexion also continues to generate real-world evidence for ULTOMIRIS (ravulizumab), its long-acting C5 inhibitor already approved for gMG. Data presented at the 2025 European Academy of Neurology Congress demonstrated meaningful reductions in steroid burden and hospitalization, real-world proof points that will matter in payer negotiations for gefurulimab’s eventual commercial launch.

DelveInsight analysts highlight that the switch from SOLIRIS to ULTOMIRIS helps Alexion defend its market share ahead of potential SOLIRIS biosimilars, effectively extending the lifecycle of its complement platform.

Cabaletta Bio

Cabaletta Bio represents perhaps the most conceptually audacious bet in the gMG pipeline: the possibility of achieving genuine, long-lasting immune reset through precision CAR-T cell therapy. While other companies optimize dosing intervals or delivery routes, Cabaletta is asking a fundamentally different question: What if you could treat gMG once?

CABA-201 is an anti-CD19 CAR-T cell therapy designed to deplete B cells that produce pathogenic antibodies in autoimmune diseases like gMG. CD19 CAR-T has already demonstrated striking disease remission in early trials across multiple autoimmune conditions, and Cabaletta is bringing this approach specifically to gMG and MuSK-positive patients through its targeted CAART (chimeric autoantibody receptor T-cell) platform.

MuSK-CAART is Cabaletta’s disease-specific precision asset, a T-cell engineered to display the MuSK antigen and selectively eliminate only the B-cells producing anti-MuSK antibodies. This targeted approach could transform care for a patient subgroup historically underserved by AChR-focused therapies. Appearing in the pipeline landscape alongside CABA-201, it reflects the company’s dual-track strategy for comprehensive gMG coverage.

UCB

UCB enters the forecast period not as a company hoping to launch, but as one of two dominant commercial incumbents in the modern gMG era, alongside argenx. UCB’s rare distinction is that it holds two approved gMG therapies with complementary mechanisms: RYSTIGGO (rozanolixizumab), an FcRn blocker administered subcutaneously, and ZILBRYSQ (zilucoplan), the first self-administered subcutaneous C5 inhibitor for gMG.

The strategic value of owning both FcRn inhibition and complement inhibition cannot be overstated. It positions UCB to address a broader patient population. AChR-positive patients benefit from both approaches, while sequencing flexibility creates long-term commercial staying power. UCB has been generating landmark real-world outcomes data for both products, presenting more than 21 abstracts at the 2025 MGFA International Conference.

Notably, in May 2025, the Japanese PMDA approved rozanolixizumab for home self-administration via both an infusion pump and a newly approved manual push syringe method. This kind of regulatory progression toward patient convenience reflects UCB’s understanding that in chronic rare diseases, patient experience is a competitive differentiator, not a commodity.

Immunovant/Roivant Sciences

In the increasingly competitive FcRn blocker space, IMVT-1402 is Immunovant’s bid for best-in-class status. The fully human anti-FcRn monoclonal antibody is designed to reduce pathogenic IgG levels, the core mechanism behind FcRn blockade, while preserving albumin levels, a differentiation point over earlier FcRn inhibitors that saw albumin reduction as an off-target effect.

The company’s Phase III program is well underway, with top-line results anticipated in 2027. In December 2025, Immunovant raised USD 550 million through an underwritten stock offering, a signal of substantial investor confidence in IMVT-1402’s commercial prospects. Roivant Sciences, the biopharma incubator behind Immunovant, has a strong track record of identifying and commercializing differentiated assets, and the financial backing here ensures IMVT-1402 will be positioned aggressively at launch.

Javed commented that IMVT-1402 emerges as a strategically important and clinically promising asset in Immunovant’s pipeline, with the potential to set a new standard in FcRn inhibition by combining potency with a clean safety profile, critical factors for long-term success in autoimmune indications.

Cartesian Therapeutics

Cartesian Therapeutics is building something unprecedented in gMG, and arguably in all of autoimmune disease: a non-viral, mRNA-based CAR-T cell therapy that could one day make long-lasting disease remission not just possible, but practical. Descartes-08 uses autologous T cells transiently engineered with mRNA, not viral vectors, to express a chimeric antigen receptor targeting BCMA (B-cell maturation antigen), driving elimination of antibody-secreting plasma cells responsible for pathogenic IgG production.

The mRNA engineering approach is significant. Unlike conventional viral CAR-T programs, Descartes-08 does not permanently integrate into the genome; it delivers CAR expression transiently, potentially allowing for repeated dosing and avoiding some of the toxicity concerns that have limited CAR-T adoption in non-oncology settings. This design philosophy positions Descartes-08 as potentially the most patient-friendly version of cell therapy for autoimmune disease.

In May 2025, the first participant was enrolled in the Phase III AURORA trial, a landmark moment given that Descartes-08 had already received both FDA Orphan Drug Designation and Regenerative Medicine Advanced Therapy (RMAT) designation, accelerating its review pathway. Earlier Phase II data showed clinical responses in gMG patients, generating substantial industry buzz. Cartesian emerged from a November 2023 merger with Selecta Biosciences, valued at USD 60.25 million, bringing complementary tolerogenic technology to enhance its platform.

Having received RMAT and Orphan Drug Designations, and with its Phase III AURORA trial progressing under the FDA’s Special Protocol Assessment, Aparna Thakur, Assistant Project Manager, Forecasting at DelveInsight, said that Descartes-08 is emerging as a promising first-in-class, durable, and patient-convenient cell therapy for generalized myasthenia gravis. If clinical outcomes are favorable, it has the potential to reshape the autoimmune neurology landscape by addressing the need for safer, longer-lasting, and more patient-friendly treatment options.

Merck KGaA

Merck KGaA (operating as EMD Serono in North America) is pursuing an intriguing repurposing approach for gMG with cladribine capsules, an oral drug already approved for relapsing multiple sclerosis. Cladribine is a lymphocyte-depleting purine nucleoside analogue that selectively eliminates lymphocytes, including B and T cells that drive autoimmune pathology in gMG.

As per Thakur, initial findings from small, treatment-refractory cohorts indicate promising symptom improvement; however, regulatory approval will depend on outcomes from pivotal trials, anticipated around mid-2028. If these trials are successful, Thakur said, cladribine may emerge as a differentiated and more patient-convenient option compared to burdensome parenteral immunosuppressants, particularly appealing for individuals with gMG who prefer less frequent, at-home dosing.

The strategy is compelling: oral dosing, an established safety profile from the MS indication, and a mechanism that targets the upstream cellular drivers of pathogenic antibody production. In August 2024, Merck dosed the first patient in the Phase III MyClad trial, and in November 2025, the US FDA granted cladribine capsules Fast Track Designation for gMG, a regulatory signal that validates the scientific rationale and opens accelerated review pathways.

For a market used to high-cost injectables and infused biologics, an oral immunotherapy with a finite treatment course and a known tolerability profile could represent a meaningful access and adherence advantage, particularly for patients in earlier lines of therapy or in markets with reimbursement constraints.

RemeGen

Telitacicept brings a truly unique mechanism to the gMG treatment pipeline, one that no other asset in the field can replicate. As a recombinant fusion protein that simultaneously blocks both BLyS (B-lymphocyte stimulator) and APRIL (A Proliferation-Inducing Ligand), telitacicept suppresses B-cell survival, maturation, and differentiation through two complementary pathways. This dual-target approach may achieve more complete B-cell depletion and plasma cell suppression than single-target agents.

RemeGen’s global Phase III trial for gMG enrolled its first US patient in August 2024, marking a significant expansion of telitacicept’s clinical footprint beyond China, where it is already approved for systemic lupus erythematosus and IgA nephropathy. In June 2025, both the FDA and EMA granted telitacicept Orphan Drug Designation for gMG, regulatory milestones that provide development incentives and market exclusivity protections.

The asset is being developed in partnership with Vor Bio for certain indications, reflecting a collaborative model for global reach. Should Phase III data be positive, telitacicept would be the first subcutaneous B-cell survival inhibitor approved for gMG, a meaningful positioning in a market hungry for mechanistic diversity.

Regeneron Pharmaceuticals

Regeneron is taking the most conceptually ambitious approach to C5 inhibition in gMG, a combination strategy that attacks C5 at two distinct levels. Pozelimab is a fully human anti-C5 monoclonal antibody that blocks C5 cleavage (preventing complement activation), while cemdisiran is an investigational siRNA that knocks down hepatic C5 protein production at the mRNA level. Together, they form a dual-modality combination designed to achieve more complete and sustained C5 suppression than either agent could achieve alone.

In August 2025, Regeneron reported that both cemdisiran monotherapy and the cemdisiran-pozelimab combination met the primary and key secondary endpoints in the Phase III NIMBLE trial in adults with gMG. Meeting endpoints with both the monotherapy and the combination is a nuanced outcome; it opens multiple potential regulatory pathways while also raising questions about what the optimal regimen will be in clinical practice.

Regeneron’s entry into gMG is backed by its deep antibody engineering heritage. The company has generated multiple blockbuster therapeutics across immunology and ophthalmology using its proprietary VelociSuite platform. The siRNA component reflects Regeneron’s growing investment in RNA therapeutics, a technology space expected to generate multiple approvals across diseases in the coming decade. With Phase III data in hand, the company is on track for regulatory submission within the forecast window.

The Bottom Line: A Decade That Will Redefine gMG Care

What emerges from this pipeline survey is not simply a list of drugs in development; it is a picture of a disease category undergoing a fundamental paradigm shift. The gMG treatment story through 2036 will be told in three overlapping chapters: the expansion of targeted biologics (FcRn blockers, complement inhibitors, B-cell suppressors) into broader patient populations including MuSK-positive and seronegative subtypes; the maturation of oral agents that democratize access for patients who struggle with infusion-based regimens; and the slow but potentially revolutionary arrival of cell therapies aiming not at management but at cure.

From Novartis running dual programs in BTK inhibition and complement blockade, to Cartesian Therapeutics advancing mRNA-engineered CAR-T into Phase III, to Regeneron combining antibody and siRNA modalities for deeper C5 suppression, the mechanistic diversity on display is extraordinary. No single mechanism will win the gMG market by 2036. Instead, what the market will reward is precise patient stratification, durable efficacy data, and access models that can serve a patient population spread across 7 major markets with profoundly different healthcare systems.

The gMG market is expected to cross USD 15.6 billion by 2036. For the 250,000 patients expected to be diagnosed by that year, the real prize is not market share; it is a treatment landscape where safe, lasting disease control becomes the rule rather than the exception.

Downloads

Article in PDF

Recent Articles

- FcRn Inhibitors for Autoimmune Disorders: A Promising Therapeutic Approach

- J&J Enters gMG Arena with IMAAVY Approval, Challenging AstraZeneca, Argenx, and UCB

- Agios’ PYRUKYND SNDA Accepted by FDA for Thalassemia; BridgeBio’s BBO-8520 Gets FDA Fast Track fo...

- FcRn Inhibitors Being The Fastest Growing Class, Plans To Get Explored In 20+ Indications

- VBL Therapeutics’ VB-111 (ofranergene obadenovec); BMS’s mavacamten (Camzyos); Merck’s KEYTRUDA; ...