Bridging Today and Tomorrow in Myasthenia Gravis Treatment: A Strategic Review of Marketed Treatments and Developmental Frontiers

Aug 29, 2025

Table of Contents

Myasthenia gravis is a rare autoimmune neuromuscular disorder marked by fluctuating muscle weakness due to impaired communication between nerves and muscles. Most cases involve autoantibodies against Acetylcholine Receptors (AChRs), reducing their numbers, blocking function, or disrupting alignment, leading to diminished muscle responsiveness. Symptoms often begin with ocular issues, drooping eyelids, or double vision, with many progressing to generalized myasthenia gravis (gMG) affecting facial, limb, neck, or swallowing muscles. Severe cases can compromise breathing, causing a myasthenic crisis requiring urgent intervention. Emerging biologics and complement inhibitors are improving outcomes, while treatment strategies also consider prior therapy exposure, treatment-naïve or refractory patients, and some marketed drugs are now exploring pediatric use. Understanding its clinical spectrum sets the stage for examining myasthenia gravis’s epidemiological profile across the major markets.

“The management of myasthenia gravis is shifting from broad immunosuppression toward targeted, mechanism-based therapies that offer improved efficacy, reduced systemic toxicity, and potential disease modification.”

Downloads

Click Here To Get the Article in PDF

Recent Articles

- AstraZeneca and Daiichi Sankyo’s Enhertu US Approval; Basilea’s ZEVTERA FDA Approval; Genmab’s Pr...

- Eisai Submits Marketing Authorization Application for Tasurgratinib; CHMP Issues Positive Opinion...

- Eisai Announces Solo Development of Farletuzumab Ecteribulin (FZEC); Johnson & Johnson’s Nipo...

- Myasthenia Gravis Awareness Month

- FcRn Inhibitors for Autoimmune Disorders: A Promising Therapeutic Approach

Epidemiological and Market Trends in Myasthenia Gravis

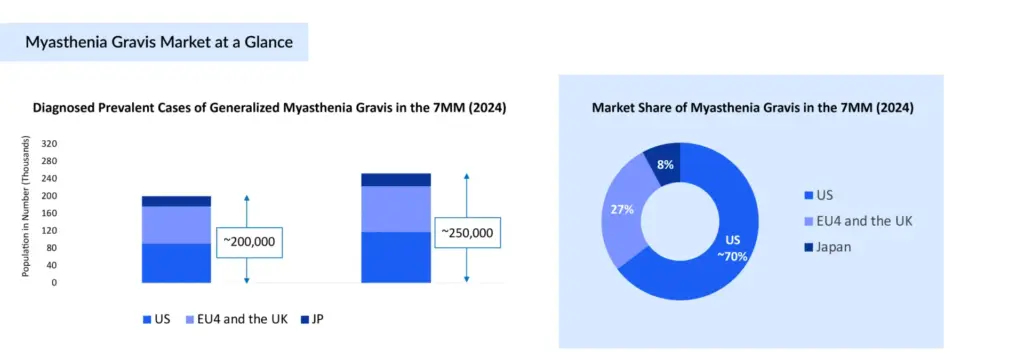

Across the US, EU4, the UK, and Japan, over 300,000 individuals are living with myasthenia gravis, with the United States recording a prevalence of 37 per 100,000 in 2024. Of these, approximately 200,000 are diagnosed with gMG in the major markets. This steady clinical burden reflects not only the chronic nature of gMG but also the impact of better diagnostic capabilities, heightened awareness, longer patient survival, and an aging demographic—all contributing to a gradual rise in diagnosed cases. As prevalence grows and patient populations expand, the evolving treatment landscape presents significant implications for the market outlook in these regions.

In 2024, the myasthenia gravis across the major markets, the US, EU4, the UK, and Japan, exceeded USD 4 billion, with the US accounting for over USD 3 billion, reflecting its dominant position supported by a substantial patient base, advanced healthcare infrastructure, and early adoption of novel therapies. Market growth is being driven by the rapid uptake of monoclonal antibodies, which have set new treatment benchmarks in gMG. Looking ahead, the pipeline, featuring CAR T-cell therapies, bispecific antibodies, small molecules, and other innovative modalities, is poised to further diversify the therapeutic landscape, intensifying competition and reshaping market dynamics over time.

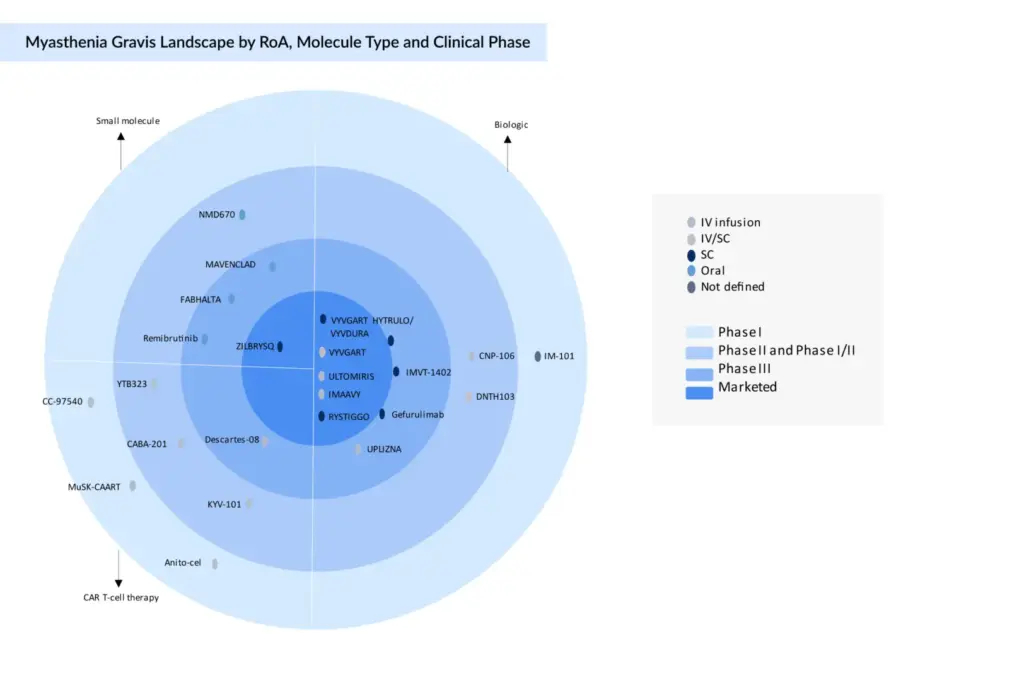

The current market for gMG is predominantly driven by monoclonal antibodies, with the majority targeting either the neonatal Fc Receptor (FcRn) or the complement C5 pathway. Notable FcRn antagonists include RYSTIGGO (rozanolixizumab) and VYVGART (efgartigimod alfa), while leading complement C5 inhibitors comprise ZILBRYSQ (zilucoplan) and ULTOMIRIS (ravulizumab). Several of these therapies are also extending their clinical focus toward pediatric populations, reflecting a growing emphasis on broader patient access. Examples include RYSTIGGO, ZILBRYSQ, and ULTOMIRIS, which are actively being investigated or positioned for younger patient segments, aiming to address unmet therapeutic needs in children and adolescents.

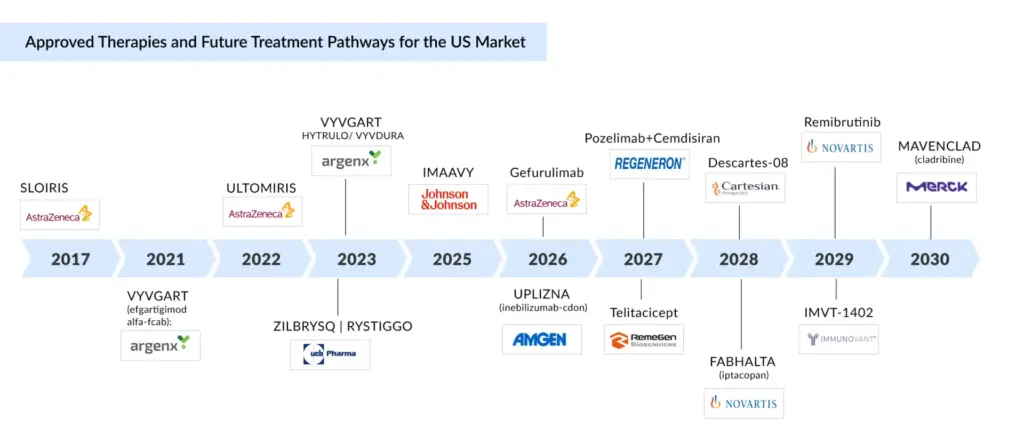

In June 2023, UCB became the first company to receive the US FDA approval for RYSTIGGO (rozanolixizumab), a treatment for myasthenia gravis that targets both AChR and MuSK antibody-positive patients. This approval represents a major advancement by addressing a broader spectrum of myasthenia gravis subtypes, including the harder-to-treat MuSK-positive cases. UCB also introduced ZILBRYSQ (zilucoplan), the first subcutaneous (SC) complement C5 inhibitor approved for AChR-positive myasthenia gravis, offering a convenient self-administered treatment option.

“While complement and FcRn inhibitors continue to dominate the myasthenia gravis pipeline, novel mechanisms of action – such as CAR T-cell therapies – are also gaining traction in ongoing research.”

Post-SOLIRIS Patent Expiry: Market Shifts and Strategic Responses

Following the patent expiry of SOLIRIS (eculizumab), the gMG treatment landscape is undergoing a notable strategic transformation. The entry of biosimilar competitors is intensifying pricing pressures and expanding access, reshaping market dynamics. Anticipating this shift, AstraZeneca has strategically advanced ULTOMIRIS, a longer-acting, next-generation C5 inhibitor, as the preferred replacement. This move not only helps retain its patient base but also offers advantages such as reduced dosing frequency. However, AstraZeneca’s position is complicated by ongoing antitrust litigation over alleged tactics to delay biosimilar competition, raising broader debates around affordability, equitable access, and the interplay between innovation and market exclusivity in rare diseases.

“AstraZeneca is leveraging ULTOMIRIS to cushion the impact of SOLIRIS losing exclusivity, aiming to safeguard patient retention and mitigate revenue erosion amid mounting biosimilar entry.”

Shaping Myasthenia Gravis’s Treatment Future

There remains a significant need for emerging therapies in gMG, particularly for patients who are refractory to current treatments, require steroid-sparing strategies, or belong to underserved groups such as pediatric and MuSK-positive subpopulations. The development pipeline is diverse, spanning multiple therapeutic classes that aim to address distinct disease mechanisms and improve patient outcomes.

In the late-stage development pipeline for gMG, FcRn antagonists such as IMVT-1402 (Immunovant/Roivant Sciences) are progressing toward potential regulatory submission anticipated in 2027, representing an evolution beyond current therapies. CAR T-cell therapies, including Descartes-08 (Cartesian Therapeutics) and KYV-101 (Kyverna Therapeutics), are advancing rapidly, with KYV-101 expected to release interim Phase II data in the second half of 2025 and preparing for a registrational Phase III trial following a successful end-of-Phase II FDA meeting in early 2025. Additional early-phase candidates from Novartis, Cabaletta Bio, and Arcellx further highlight the transformative potential of immune cell reprogramming approaches to achieve durable disease control.

“Immunovant has opted not to file batoclimab for approval, despite its late-stage status, citing limitations in formulation and dosing. Instead, the company is advancing IMVT-1402, a next-generation FcRn inhibitor built on insights from batoclimab’s Phase III data, aiming for improved efficacy, safety, and patient convenience.”

Simultaneously, small-molecule therapies such as remibrutinib (Novartis), a BTK inhibitor, and FABHALTA (Novartis), a complement Factor B inhibitor, are advancing as oral, nonantibody alternatives that promise greater patient convenience and expanded accessibility, with remibrutinib targeting regulatory filings in or beyond 2028 and iptacopan submission planned for 2027.

Significant clinical milestones were reported in April 2025, when Cartesian Therapeutics revealed sustained long-term efficacy of Descartes-08 following a single treatment course. Twelve-month follow-up data demonstrated an average 4.8-point improvement in the myasthenia gravis Activities of Daily Living (MG-ADL) score, with the greatest benefits observed in biologic-naïve patients, who exhibited a 7.1-point reduction and 57% maintained minimal symptom expression. The consistent safety profile supports outpatient administration, reinforcing the therapy’s potential for durable, accessible disease management. The pivotal Phase III AURORA trial is on track to initiate patient dosing in the second quarter of 2025.

Bispecific antibodies are emerging within the gMG treatment landscape, exemplified by AstraZeneca’s gefurulimab, which is undergoing evaluation in pediatric populations—marking a critical step toward age-specific therapies. In July 2025, gefurulimab demonstrated statistically significant and clinically meaningful improvements in daily functioning among adults with AChR antibody-positive gMG, successfully meeting all primary and secondary endpoints in the Phase III PREVAIL trial. Complement pathway inhibitors like Regeneron’s pozelimab, combined with Alnylam’s cemdisiran, anticipate pivotal data in the latter half of 2025, while Dianthus Therapeutics’ DNTH103 targets the complement C1s pathway, with top-line Phase II data expected in September 2025.

CD19-directed antibody UPLIZNA (inebilizumab-cdon, Amgen) is progressing steadily through regulatory channels, with final submission planned in the first half of 2025. The FDA has accepted Phase III data from the MINT trial, assigning a Prescription Drug User Fee Act (PDUFA) date of December 14, 2025. Meanwhile, innovative immunomodulators such as RemeGen’s telitacicept, targeting BLyS/APRIL dual pathways, have achieved Orphan Drug Designation (ODD) from both the US Food and Drug Administration (FDA) and European Medicines Agency (EMA), marking it as the first dual-target biologic for myasthenia gravis to receive such recognition. This underscores the increasing focus on novel immunological targets within the myasthenia gravis pipeline.

Beyond late-stage candidates, early-phase programs are expanding the therapeutic horizon with experimental molecules like BHV-1310 (Biohaven), AT-1608 (Ahead Therapeutics), TOL2 (Flerie/Toleranzia), IM-101 (ImmunAbs), and CNP-106 (COUR Pharmaceutical). Collectively, these diverse approaches signal a paradigm shift toward more precise, mechanism-driven treatments, potentially redefining the standard of care for both adult and pediatric myasthenia gravis patients in the near future.

Long-term Myasthenia Gravis Market Outlook Through 2030

Several therapies for myasthenia gravis are already approved, but attention is increasingly shifting toward the pediatric segment. Examples include ZILBRYSQ (zilucoplan) and ULTOMIRIS (ravulizumab), both under a Risk Evaluation and Mitigation Strategy (REMS), as well as RYSTIGGO (rozanolixizumab), which is also being explored for pediatric patients.

The myasthenia gravis treatment landscape is entering a dynamic growth phase, with multiple late-stage innovations poised for approval within the next 5 years. Standout candidates include IMVT-1402, Descartes-08, remibrutinib, gefurulimab, MAVENCLAD (cladribine), telitacicept, UPLIZNA (inebilizumab-cdon), FABHALTA (iptacopan), and the pozelimab + cemdisiran combination.

Amgen’s UPLIZNA (inebilizumab-cdon) is expected to launch in early 2026, offering a targeted approach to suppress pathogenic autoantibodies central to gMG, alongside the potential launch of gefurulimab, an advanced anti-inflammatory therapy, in the same year. By 2030, Merck’s MAVENCLAD (cladribine), already approved in multiple sclerosis and other autoimmune conditions, could emerge as an oral, convenience-driven alternative for myasthenia gravis.

Other promising entrants between 2027 and 2029 include

- Remegen’s telitacicept, a dual TNFSF13B/TNFSF13 inhibitor (Q3 2027).

- Regeneron’s pozelimab + Alnylam’s cemdisiran, a C5 inhibitor–RNAi combination targeting complement activation (Q1 2027).

- Cartesian Therapeutics’ Descartes-08, an autologous mRNA CAR T-cell therapy targeting BCMA, potentially enabling one-time durable remission (early 2028).

- Novartis’ FABHALTA (iptacopan), a complement Factor B inhibitor (2028).

By 2029, further diversification is expected with Immunovant’s IMVT-1402 (next-generation FcRn inhibitor) and Novartis’ remibrutinib (BTK inhibitor).

These projections are based on DelveInsight’s internal forecast models, integrating clinical trial progress, regulatory developments, and competitive launch patterns to refine approval timelines. The resulting landscape reflects both deepening mechanistic diversity and a growing focus on pediatric applicability alongside adult care.

“Significant advances have been made in myasthenia gravis treatment in recent years, marked by a rapidly evolving therapeutic landscape. Promising late-stage candidates such as inebilizumab, telitacicept, and pozelimab + cemdisiran are expected to further improve disease management and expand treatment options.”

Myasthenia Gravis Treatment Future Outlook

The myasthenia gravis market is entering a transformative era marked by expanding therapeutic diversity, strategic repositioning, and increasing attention to underserved populations, particularly pediatric patients. The post-SOLIRIS (eculizumab) environment has triggered competitive realignment, with ULTOMIRIS (rasvulizumab) and ZILBRYSQ (zilucoplan) leading the next-generation C5 inhibitor space under REMS oversight, alongside FcRn-targeting agents like RYSTIGGO (rozanolixizumab) gaining traction. The shift toward pediatric trials reflects a broader recognition of early intervention benefits and the market’s potential in pediatric cohorts.

Myasthenia gravis emerging assets, ranging from oral small molecules like remibrutinib and FABHALTA (iptacopan) to advanced modalities such as CAR T-cell therapies (Descartes-08) and bispecific antibodies (gefurulimab), are poised to reshape disease management through targeted, mechanism-driven approaches. Combination strategies like pozelimab + cemdisiran further highlight innovation in complement inhibition.

By 2030, the myasthenia gravis treatment ecosystem will be characterized by greater mechanistic breadth, improved convenience, and expanded patient reach, supported by both established biologics and disruptive newcomers. This evolution is likely to enhance competitive intensity while addressing critical gaps in refractory, MuSK-positive, and pediatric subgroups. The next 5 years will not only redefine therapeutic standards but also recalibrate market leadership as innovation, access, and patient segmentation converge in shaping myasthenia gravis’s future trajectory.

Downloads

Article in PDF

Recent Articles

- J&J Enters gMG Arena with IMAAVY Approval, Challenging AstraZeneca, Argenx, and UCB

- FDA rejects BioMarin’s Valoctocogene Roxaparvovec; J&J inks $6.5B deal; Alzheon bags $...

- FDA Approves PENBRAYA for Most Common Serogroups Causing Meningococcal Disease; BIMZELX Approved ...

- Eisai Submits Marketing Authorization Application for Tasurgratinib; CHMP Issues Positive Opinion...

- FDA Expands SOLIRIS for Pediatric Myasthenia Gravis; vTv’s Cadisegliatin Program Resumes as FDA L...