Radioligand Therapies: A Rapidly Emerging Pillar in the Oncology Market

Mar 09, 2026

Table of Contents

Summary

- Radioligand therapy is becoming a crucial component of cancer treatment.

- Approved radioligand therapy includes LUTATHERA (for GEP-NETs), XOFIGO, PLUVICTO (both for prostate cancer), and ZEVALIN (for follicular B-cell non-Hodgkin’s lymphoma).

- Leading companies such as Novartis, Curium Pharma, Lantheus, Eli Lilly and Company, Fusion Pharmaceuticals, AstraZeneca, Clarity Pharmaceuticals, Bayer, ITM Isotope Technologies, ARTBIO, Convergent Therapeutics, Perspective Therapeutics, PRECIRIX, Ariceum Therapeutic, Nuclidium, and others are currently active in the RLT domain.

Radioligand therapies (RLTs) are rapidly moving from niche options to a foundational pillar of modern oncology, especially in neuroendocrine tumors and advanced prostate cancer, with a robust late‑stage pipeline set to expand their use across multiple solid tumors. As clinical evidence, regulatory support, and investment from big pharma accelerate, radioligands are poised to reshape cancer care and create a high‑growth market across the US, EU4, the UK, and Japan over the next decade.

Downloads

Click Here To Get the Article in PDF

Recent Articles

- Hanmi Pharmaceutical and Eli Lilly and Company Join Forces to Advance Sonefpeglutide Development;...

- Gastroenteropancreatic Neuroendocrine Tumours Market To Gain Substantial Momentum With Entrance o...

- Novartis Bets Big on Radioligand Therapy with Multiple Pipeline Candidates and Expanding Trials

- Edwards’s Pascal Precision System; Abbott’s New Spinal Cord Stimulation Device; Imagin to A...

- CEPI Grants $41.3 Million to Valneva; Innovent Achieves Phase III Success for Mazdutide; GSK’s BL...

What are Radioligand Therapies?

Radioligand therapy combines a targeting molecule with a radioactive isotope to deliver radiation directly to cancer cells while sparing surrounding healthy tissue. The ligand binds to a specific receptor or antigen overexpressed on tumor cells, carrying the radionuclide into the malignant tissue where it emits cytotoxic radiation and induces DNA damage.

Unlike external beam radiotherapy, which irradiates a defined field from outside the body, RLT is systemic and tumor‑seeking, and unlike chemotherapy, it is designed to selectively target cancer cells rather than all rapidly dividing cells. Many radioligand platforms also support a “theranostic” approach, whereby a diagnostic radiotracer is first used to identify appropriate patients and visualize disease burden, followed by a therapeutic radioligand using the same target.

Epidemiology and Addressable Patient Pool

The near‑term growth opportunity in RLT is underpinned by large and rising patient pools across a set of priority indications, including prostate cancer, breast cancer, ES‑SCLC, GEP‑NETs, follicular lymphoma, and glioblastoma multiforme. In the US alone (2024 estimates), there are roughly 3.8 million prevalent prostate cancer cases, about 298,000 incident breast cancer cases, approximately 29,000 ES‑SCLC incident cases, nearly 15,800 follicular lymphoma incident cases, and about 13,100 glioblastoma incident cases.

According to Sadaf Javed, Manager of Forecasting and Analytics at DelveInsight, these indications collectively translate into a substantial “radioligand‑eligible” population once factors such as stage at diagnosis, biomarker expression (e.g., PSMA, SSTR), and treatment eligibility are applied.

Differences of Radioligand Therapy from Other Therapies

Radioligand therapy employs radioactive compounds that selectively bind to cancer cells and destroy them while sparing most healthy tissue. In contrast to chemotherapy or conventional radiation therapy, it delivers radiation directly to malignant cells through highly specific molecular targeting. Radioligands are distinctive because they can serve both diagnostic and therapeutic purposes in cancer care.

This targeted strategy often leads to fewer adverse effects and enables more personalized treatment. Compared with many existing therapies, it provides a more precise, effective, and generally better-tolerated option for patients. Ongoing research is expanding its application to additional cancer types. With its combination of targeted delivery and dual diagnostic–treatment capability, radioligand therapy is emerging as an important advancement in modern oncology.

The Rising Tide of Targeted Radioligand Therapies

Radioligand therapy is quickly gaining recognition as an effective treatment option. It is mainly utilized for metastatic neuroendocrine tumors and prostate cancer cases that no longer respond to standard chemotherapy or radiotherapy. Several radioligand therapies, including Novartis’ LUTATHERA (for GEP-NETs) and PLUVICTO (prostate cancer), Bayer’s XOFIGO (prostate cancer), and Spectrum Pharmaceuticals’ ZEVALIN (for follicular B-cell non-Hodgkin’s lymphoma).

LUTATHERA was the first radioligand therapy to receive FDA approval for adult patients with GEP-NETs and has recently gained authorization for pediatric use as well. According to Novartis’ 2025 annual report, sales of LUTATHERA grew mainly in the US, Europe, and Japan, fueled by increasing demand and its adoption in earlier lines of treatment (within approved indications) in the US and Japan. For the full year of 2025, LUTATHERA generated approximately USD 816 million in revenue.

Sadaf commented that the pharmaceutical industry is becoming more interested in targeted radiation therapy as a novel, promising cancer treatment option as a result of the LUTATHERA success story.

In 2022, the FDA approved PLUVICTO, marking it as the first targeted radioligand therapy for patients with mCRPC. Despite supply constraints and its use primarily in the third-line setting, the therapy achieved nearly USD 980 million in revenue within 18 months of launch. Its potential in earlier, pre-taxane treatment settings continues to draw considerable interest. In 2025, PLUVICTO’s sales reached USD 1.9 billion.

XOFIGO, developed by Bayer, is a radioactive therapy that emits alpha particles. It is approved for patients with castration-resistant prostate cancer who have symptomatic bone metastases and no detectable visceral metastases. The recommended dosage is 55 kBq (1.49 microcuries) per kilogram of body weight, administered every 4 weeks for a total of six doses. The drug is delivered via a slow intravenous injection over the course of one minute.

The growing adoption and commercial success of these radioligand therapies highlight the expanding role of targeted radiation in oncology. With approvals extending to broader patient populations and ongoing clinical investigations exploring earlier lines of therapy, radioligand therapy is poised to become a cornerstone in precision cancer treatment. As more companies invest in research and development, the landscape is likely to see an increasing number of novel radioligand candidates, offering patients safer, more effective, and highly personalized therapeutic options in the years ahead.

The Competitive Landscape of Radioligand Therapy

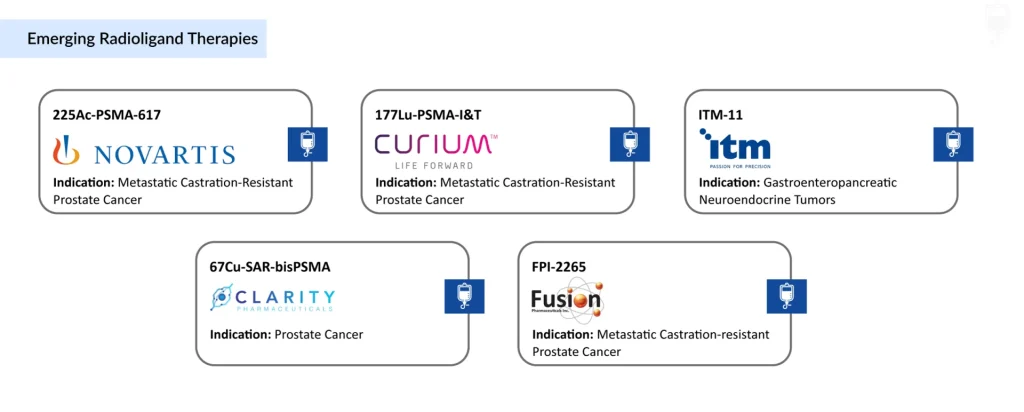

The competitive landscape is led by large multinationals and specialized radiopharma companies, with Novartis currently in a dominant position due to its two marketed Lu‑177 agents and broad pipeline. Novartis is advancing several radioligand candidates, including 177Lu-PSMA-617, 225Ac‑PSMA‑617, 177Lu-NNS309, 177Lu-NeoB, AAA614, and ESP359.

Apart from Novartis, several other companies such as Curium Pharma (177Lu-PSMA-I&T), Lantheus and Eli Lilly and Company (Lu-PNT2002 and LNTH-1095), Fusion Pharmaceuticals and AstraZeneca (FPI-2265), Clarity Pharmaceuticals (67CU SAR-BBN and 64Cu-SAR-BBN), Bayer (225Ac-PSMA-Trillium, 225Ac-Pelgifatamab, and 225Ac-GPC3), ITM Isotope Technologies (ITM-11), ARTBIO (212Pb-NG001), Convergent Therapeutics (CONV01-α), Perspective Therapeutics (VMT-α-NET, VMT01, and PSV359), PRECIRIX (CAM-FAP-Ac-225), Ariceum Therapeutics (225Ac-SSO110 and ATT001), Nuclidium (NU101 and NU201), and others are are involved in developing novel radioligand therapies for various indications such as prostate cancer, breast cancer, and various solid tumors.

The development of these therapies in different stages is clearly suggesting an upcoming wave of new approvals that could diversify targets, isotopes, and tumor types addressed.

Potential Barriers to Integration of Radioligand Therapies

Barriers to the broader integration of radioligand therapy in cancer care include limited awareness and understanding among healthcare providers, insufficient professional training, workforce planning gaps, and constrained hospital resources. Evolving legislation, regulation, and policy further complicate adoption. Shortages of trained personnel and inconsistent availability of diagnostic tools like PET scanners contribute to waitlists and scheduling difficulties.

The uptake of RLT is restricted by a lack of specialized centers and trained staff. Expanding dedicated training programs and establishing multidisciplinary care teams are crucial to improving patient outcomes and addressing unmet needs. Access remains limited in Europe and the US due to the scarcity of treatment centers, highlighting the need for coordinated care networks. Isotope production is also challenging because of limited manufacturing facilities and the short half-lives of these compounds. Additionally, high infrastructure costs and incomplete regulatory and reimbursement frameworks hinder wider clinical adoption.

Oncologists face particular obstacles in administering PSMA-targeted therapy for prostate cancer. Lutetium Lu 177 vipivotide tetraxetan (PLUVICTO) was approved in 2022 for PSMA-avid patients, but practical challenges have restricted its use. Patients must undergo PSMA PET scans to confirm eligibility, yet the availability of these scans remains limited in some settings. Supply shortages in 2022–2023 delayed access to 177Lu-PSMA-617, and even after supply issues were resolved, delays persist. For patients with aggressive disease, the interval from PSMA PET ordering to treatment can be critical—patients in the VISION trial who did not receive the radioligand had a median progression-free survival of only 3.4 months. Insurance approvals and the high cost of therapy add further barriers.

The absence of standardized referral pathways in Europe complicates onboarding for new RLT centers, especially those with limited experience. Developing uniform referral guidelines and ensuring the involvement of multidisciplinary teams are essential for consistent, efficient diagnosis and treatment across European Member States.

Future Outlook of Radioligand Therapies

The future of radioligand therapies looks highly promising, driven by advances in molecular targeting, imaging technologies, and radioisotope development. These therapies, which combine the precision of targeted molecular binding with the cytotoxicity of radioactive isotopes, are increasingly being explored across a range of cancers, including prostate, breast, neuroendocrine, and glioblastoma.

The growing understanding of tumor-specific antigens and receptors allows for the design of radioligands that can selectively bind malignant cells while sparing healthy tissue, improving both efficacy and safety profiles compared to conventional therapies. Additionally, innovations in isotope chemistry, including alpha-emitting isotopes such as actinium-225, are opening new avenues for treating tumors resistant to traditional therapies.

Beyond oncology, radioligand therapies are expected to expand into other disease areas, potentially including autoimmune disorders and targeted imaging for early diagnosis. The integration of theranostics, a combined approach of therapy and diagnostics, will enable clinicians to personalize treatments by assessing tumor burden, receptor expression, and treatment response in real time. This personalization is anticipated to optimize dosing, minimize side effects, and improve overall outcomes, making RLTs a cornerstone of precision medicine.

Furthermore, the commercial and regulatory landscape is becoming increasingly favorable for radioligand therapies. With several radioligand agents already approved and numerous candidates in late-stage clinical trials, partnerships between pharmaceutical companies, academic institutions, and radiochemistry experts are accelerating development pipelines. Investments in scalable isotope production and streamlined delivery mechanisms will be critical to meet anticipated demand.

Sadaf concluded that the market for radioligand therapies is expected to grow significantly in the coming years. This is due to the increasing number of patients who are being diagnosed with cancer, the growing awareness of radioligand therapies, the increasing number of radioligand therapies that are under clinical trials, and the increasing interest of major pharmaceutical companies in it.

Overall, the outlook for radioligand therapies is one of rapid innovation, broader clinical adoption, and the potential to transform treatment paradigms across multiple cancers and beyond.

Downloads

Article in PDF

Recent Articles

- With early-stage data, Chimeric antigen receptor T cell (CART) finding its way towards entering P...

- Gastroenteropancreatic Neuroendocrine Tumours Market To Gain Substantial Momentum With Entrance o...

- B7-H3, an emerging immune checkpoint molecule in metastatic CRPC and other cancers

- Clover’s SCB-1019 RSV Revaccination Study Clears U.S. IND; FDA Approves AMVUTTRA for ATTR-CM CV R...

- Gilead’s Magrolimab Plus Azacitidine for MDS; FDA Approveds VANFLYTA for Newly Diagnosed AML; FDA...