Cracks in the mCRPC Treatment Market: 8 Companies at Risk of Falling Behind

May 29, 2026

Table of Contents

Summary

- The mCRPC market, valued at around USD 8 billion in 2025, is undergoing rapid disruption driven by scientific innovation, patent expirations, and shifting treatment paradigms.

- Once dominated by blockbuster androgen receptor inhibitors like ZYTIGA and XTANDI, the landscape is now fragmenting under pressure from generic competition, precision medicine, and emerging therapies such as radioligand treatments.

- Legacy leaders such as Johnson & Johnson, Pfizer, Astellas, GSK, Sanofi, AstraZeneca, and Merck are already losing ground.

The metastatic castration-resistant prostate cancer (mCRPC) market is in the middle of a seismic transformation. Radioligand therapies are rewriting treatment algorithms. Patent cliffs are eroding billion-dollar franchises overnight. Generic manufacturers are circling like hawks. And precision medicine is carving the patient pool into smaller, mutation-defined segments that legacy drugs never anticipated.

Downloads

Click Here To Get the Article in PDF

Recent Articles

- Another Feather in the Cap for Xtandi and Keytruda — The Two Main Cancer Drugs

- Phase III RUBY Trial of Jemperli Plus Chemotherapy Updates; FDA Approves Roche’s Vabysmo for RVO;...

- Radioligand Therapies: A Rapidly Emerging Pillar in the Oncology Market

- Top 10 Expected Oncology Drug Launches in 2023

- Prostate Cancer Market Experiences an Influx of the Pharma Players Veering the Market Ahead

For pharma investors, oncologists, and market analysts, the burning question is no longer who is winning; it’s who is about to lose, and why.

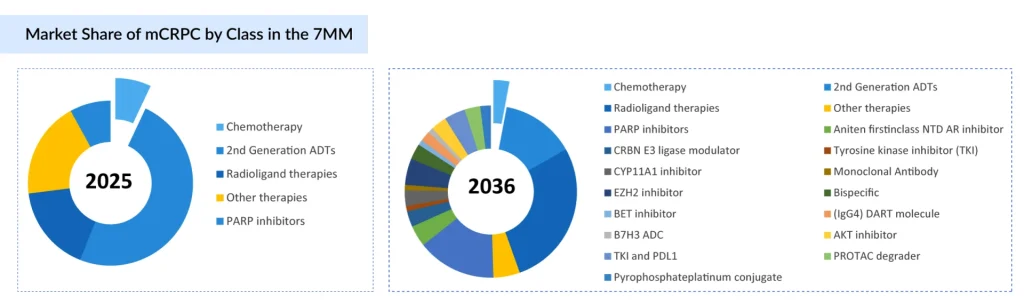

The mCRPC Market: A Snapshot of What’s at Stake

The metastatic castration-resistant prostate cancer market was valued at approximately USD 8 billion in 2025, with the U.S. alone accounting for roughly USD 5.4 billion of that figure. A diverse arsenal of therapeutic classes now competes for the same patients: androgen receptor inhibitors (ARIs), CYP17 inhibitors, PARP inhibitors, microtubule inhibitors, radioligand therapies (RLTs), and GnRH antagonists.

For years, the market was a two-horse race dominated by Johnson & Johnson’s ZYTIGA (abiraterone) and Astellas Pharma/Pfizer’s XTANDI (enzalutamide). Together, they formed the backbone of first-line mCRPC treatment. But the ground beneath both of these giants is crumbling, and they are far from alone.

Johnson & Johnson (Janssen): ZYTIGA’s Freefall is Already Happening

If you want to understand what market share collapse looks like in real time, look no further than Johnson & Johnson’s ZYTIGA (abiraterone acetate). ZYTIGA was once a blockbuster in the truest sense, generating USD 755 million in a single quarter at its peak and holding roughly 30% of first-line mCRPC prescriptions. Today, those numbers are a distant memory.

Generic abiraterone entered the U.S. market in late 2020 following years of patent litigation. The impact was catastrophic. According to studies on post-generic market dynamics, ZYTIGA’s market share fell to approximately 14% following generic entry, with monthly net sales across the entire abiraterone market collapsing by 85%. J&J’s own SEC filings show worldwide ZYTIGA revenues plunging 32.4% year-over-year in recent quarters, with U.S. revenue effectively annihilated.

J&J attempted to soften the blow with its next-generation combination, AKEEGA (niraparib + abiraterone acetate), which received FDA approval in 2023. But AKEEGA’s label was restricted to BRCA-mutated mCRPC patients only, a far narrower population than the broad, biomarker-unselected label ZYTIGA once enjoyed. While AKEEGA represents an intelligent lifecycle management play, it cannot replicate the revenue volumes of a broadly prescribed standard of care.

J&J also explored combining ERLEADA (apalutamide) with ZYTIGA, but ultimately decided against pursuing a regulatory filing after disappointing trial data. The result: Janssen is fighting on a shrinking front in mCRPC, relying on a biomarker-gated product in a world that once handed it millions of patients.

J&J has already lost market share in mCRPC. The question is how much further ZYTIGA’s legacy volume falls, and whether AKEEGA can compensate.

Pfizer & Astellas: The $4 Billion XTANDI Patent Cliff Is Coming

XTANDI (enzalutamide) is the current king of the mCRPC market. In 2025, it commanded approximately USD 2 billion in the metastatic prostate cancer segment alone, holding the largest share among androgen receptor pathway inhibitors in the US. Sadaf Javed, an oncology expert at DelveInsight, projects global XTANDI sales to peak at USD 3 billion in 2025 in the 7MM. Then comes the cliff.

XTANDI’s European patents are expiring in 2026. U.S. patents follow in 2027. Generic manufacturers have already filed Paragraph IV challenges, and at least three tentative approvals for generic enzalutamide have been issued by the FDA. Competitors are actively mining XTANDI’s patent family for synthesis and crystalline form gaps to accelerate entry.

When ZYTIGA lost patent protection, its U.S. revenues dropped to near-zero within quarters. XTANDI faces the same trajectory. Javed further projects XTANDI revenues will collapse from USD 1.5 billion in 2025 to just USD 951 million by 2036 in the US, a 37% decline driven almost entirely by generic erosion.

Pfizer and Astellas have attempted to extend XTANDI’s commercial life by exploring combination strategies, including the FDA-approved pairing of Talazoparib (Talzenna) + Enzalutamide for HRR-mutated mCRPC. However, advisors voted against broader label expansion to HRR-negative patients, limiting the addressable population significantly.

For Astellas in particular, which depends heavily on XTANDI for its oncology revenue, the 2026–2027 window represents an existential financial challenge.

Clovis Oncology (Acquired by Pharma & Schwiez): A Cautionary Tale of mCRPC Failure

Few stories in the mCRPC PARP inhibitor space are as stark as that of Clovis Oncology’s RUBRACA (rucaparib). Approved in 2016 as the second PARP inhibitor to reach the market, RUBRACA never gained meaningful commercial traction. The drug struggled to differentiate against LYNPARZA and failed to demonstrate a competitive label breadth.

By 2022, FDA safety scrutiny on PARP inhibitors in heavily pre-treated ovarian cancer had cast a shadow across the class. The FDA ultimately withdrew RUBRACA’s ovarian cancer indications in March 2024. The financial pressure proved fatal; Clovis filed for bankruptcy in 2023, and RUBRACA was sold off in a bankruptcy sale. Pharma& Schwiez submitted the highest bid at the auction and brought the drug.

In mCRPC specifically, RUBRACA’s TRITON3 trial showed rPFS benefit, but almost exclusively in the BRCA-positive population, severely limiting its commercial reach. It never achieved the scale needed to compete.

GSK: ZEJULA’s mCRPC Position is Marginal and Shrinking

GSK’s ZEJULA (niraparib) achieved second-place standing in the broader PARP inhibitor market. But in mCRPC specifically, ZEJULA has never held a meaningful position. Niraparib’s mCRPC strategy took a different path; Janssen combined it with abiraterone to create AKEEGA, licensed under J&J’s umbrella. This means the core niraparib molecule lives on in mCRPC through AKEEGA, but GSK does not directly benefit from that franchise in the same way.

ZEJULA’s ovarian cancer indications were withdrawn alongside LYNPARZA and RUBRACA in early 2024, a regulatory setback that constricted the drug’s overall commercial narrative. Without a strong mCRPC standalone label, GSK’s footprint in this specific indication is peripheral.

Sanofi: JEVTANA’s Chemotherapy Window Is Closing

Sanofi’s JEVTANA (cabazitaxel) remains an approved mCRPC treatment, specifically for patients previously treated with docetaxel. It is an established microtubule inhibitor with a clear, if narrow, role in later lines of therapy. But JEVTANA is under structural pressure from multiple directions. Earlier treatment intensification, as ARIs like XTANDI and NUBEQA are increasingly used in hormone-sensitive disease, patients arrive at later mCRPC settings having already exhausted more options, compressing the chemotherapy window.

Radioligand therapy displacement, Novartis’ PLUVICTO, now approved in the pre-taxane setting following the PSMAfore trial, is pulling patients away from the chemotherapy sequencing that JEVTANA depended on. Declining chemotherapy preference, oncologists and patients increasingly prefer targeted, better-tolerated agents over traditional cytotoxic chemotherapy, where options exist

JEVTANA is not facing a generic threat imminently, but it is facing something equally dangerous: therapeutic irrelevance as the treatment algorithm evolves around it.

AstraZeneca/Merck: LYNPARZA Faces the Squeeze of Combination Competition

LYNPARZA (olaparib) remains the PARP inhibitor market leader and holds an approved mCRPC indication for BRCA-mutated patients. AstraZeneca and Merck have aggressively pursued lifecycle management, including filing for first-line mCRPC use. However, LYNPARZA is not immune to the squeeze:

- Combination pressure: AKEEGA (niraparib/abiraterone) and the TALZENNA/XTANDI combo received concurrent 2023 approvals in BRCA-mutated mCRPC, directly competing for the same patient population.

- Label restrictions: The withdrawal of LYNPARZA’s heavily pre-treated ovarian cancer indication in 2024, after the SOLO3 trial showed a 33% greater risk of death vs. chemotherapy, damaged the drug’s overall brand perception, even though the mCRPC label was unaffected.

- Biomarker-limited ceiling: With a patient pool restricted to those harboring BRCA mutations (roughly 10–15% of mCRPC patients), LYNPARZA’s addressable market in prostate cancer is inherently constrained.

As per Javed, AstraZeneca and Merck are not at risk of losing LYNPARZA’s position entirely, but will face intensifying competition in the biomarker-selected mCRPC segment from well-resourced combination regimens.

The Bigger Picture: Structural Forces Reshaping the mCRPC Market

Beyond individual company dynamics, several macro forces are permanently redrawing the competitive map:

The Radioligand Revolution: Novartis has established itself as an industry frontrunner in the RLT space. Novartis’ PLUVICTO (lutetium-177 PSMA-617) generated unexpectedly strong revenues from third-line mCRPC following its 2022 approval. With the PSMAfore trial supporting approval in the pre-taxane setting in 2024, and PSMAddition demonstrating benefit in mHSPC, PLUVICTO is methodically consuming patient populations that once fell to ARIs and chemotherapy. The companies losing out are those whose drugs occupy exactly the treatment lines that Pluvicto is now colonizing.

The Precision Medicine Segmentation Effect: mCRPC is no longer one market; it is a mosaic of molecularly defined sub-populations. BRCA1/2-mutated, HRR-positive, PSMA-positive, AR-amplified, and wild-type patients each have different optimal therapies. Companies with broad, biomarker-agnostic legacy franchises (ZYTIGA, XTANDI) are seeing their addressable patient populations fractured by genomic stratification.

Generic Pricing Destruction: The history of ZYTIGA is a preview of what awaits XTANDI. Once high-volume branded drugs lose exclusivity in oncology, price erosion is rapid and structural. The ZYTIGA experience showed monthly net sales across the combined branded/generic abiraterone market falling 85% post-generic entry. No lifecycle management strategy has fully reversed that trajectory in small-molecule oncology.

This Is Not Decline, It’s Disruption

The companies losing share in mCRPC are not failing because they made bad drugs. ZYTIGA and XTANDI redefined prostate cancer treatment for a generation. RUBRACA was a meaningful scientific advance. The problem is that science moved faster than their commercial lifecycles.

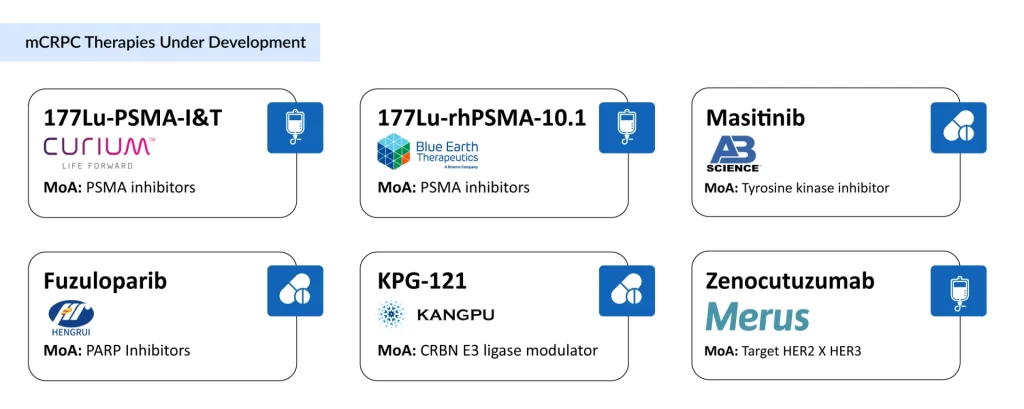

The 2036 mCRPC market will look almost unrecognizable compared to today’s, dominated by radioligand therapies, precision combination regimens, and biomarker-driven sequencing. The new entrants in the mCRPC drug development space, such as Curium (177Lu-PSMA-I&T), AB Science (Masitinib), Lantheus and Eli Lilly/POINT Biopharma (177Lu-PNT2002), Telix Pharmaceuticals (177Lu-DOTA-rosopatamab), Tavanta Therapeutics (TAVT-45), Kangpu Biopharmaceuticals (KPG-121), Merus (Zenocutuzumab), and others, will further change the dynamics of the market.

In conclusion, companies that are not building for that future, or that are banking too heavily on legacy revenue, are the ones most at risk.

Downloads

Article in PDF

Recent Articles

- Early but strong clinical data of Arvinas’s ARV-110 in Men with mCRPC that support a potential pa...

- A Quick Recap from ASCO GU 2023: Prostate and Urothelial Cancer Highlights

- Boehringer Ingelheim’s Diabetic Macular Ischemia Study; Novartis’ Mariana Oncology Acquisition; A...

- The Next Wave of Radioligand Therapies: 5 Candidates to Watch

- Novartis Bets Big on Radioligand Therapy with Multiple Pipeline Candidates and Expanding Trials