How Novel Therapies Could Transform the Ulcerative Colitis Treatment Landscape

Jul 14, 2025

Nearly two decades ago, treatment options for ulcerative colitis were limited, and selecting appropriate ulcerative colitis medications largely depended on disease severity and prior therapy response. Physicians often relied on combination approaches to optimize outcomes. Historically, the primary treatments for ulcerative colitis medications included aminosalicylates and immunomodulators such as azathioprine, 6-mercaptopurine, and methotrexate, while biologics were reserved for more severe or refractory cases. Commonly recognized ulcerative colitis medications names in this category include adalimumab, golimumab, infliximab, ustekinumab, and vedolizumab.

Today, however, the landscape has evolved significantly with the introduction of new ulcerative colitis medications, including JAK inhibitors, S1P receptor modulators, and IL-23 inhibitors. This expanding ulcerative colitis medications list has made the market more dynamic and competitive, reshaping physician decision-making and raising important considerations around what is the best medicine for ulcerative colitis based on individual patient profiles.

For patients with mild to moderate disease, first-line treatments for ulcerative colitis medications typically include aminosalicylates or corticosteroid induction followed by 5-ASA maintenance therapy. In contrast, moderate to severe cases often require immunosuppressants such as azathioprine or 6-mercaptopurine for maintenance after corticosteroid induction. Anti-TNF agents, used with or without immunomodulators, play a key role in achieving mucosal healing and sustained remission in these patients.

Downloads

Click Here To Get the Article in PDF

Recent Articles

- Taltz (Ixekizumab) in Treatment of Plaque psoriasis

- New Player in Ulcerative Colitis Treatment: Pfizer’s Etrasimod Entry Counters BMS’ Zeposia

- Bristol-Myers Squibb’s Opdivo Approval; Mirati’s KRAS-inhibitor Adagrasib; J&J and Legend Bi...

- FDA’s Ok to Roche’s Oral SMA Therapy; Roche’s Etrolizumab Mixed Results in Ulce...

- FDA Grants Orphan Drug Designation for Ractigen’s RAG-21 in ALS; Intellia’s Nexiguran RMAT for AT...

In the current ulcerative colitis treatment market landscape, AbbVie is one of the strongest players, and HUMIRA is a best-selling product approved for several autoimmune indications. HUMIRA lost exclusivity in the US in January 2023. Since then, ten biosimilars have been launched, including AMJEVITA, YUFLYMA, CYLTEZO, and others, resulting in a ~32% drop in global HUMIRA sales in 2023.

Ulcerative colitis is a relatively common chronic inflammatory bowel disease in the United States, affecting an estimated 900,000 to 1 million people. It is more frequently diagnosed in adults between the ages of 15 and 35, although it can occur at any age. The prevalence has been steadily increasing, likely due to improved diagnosis and environmental factors. While ulcerative colitis affects both men and women equally, it is more common in developed countries and urban populations, highlighting the role of lifestyle and environmental influences in the disease.

In response, AbbVie is actively mitigating HUMIRA’s patent losses by expanding its immunology portfolio through RINVOQ (upadacitinib) and SKYRIZI (risankizumab). In June 2024, the FDA approved SKYRIZI for moderate to severe ulcerative colitis, followed by approval in Japan in the same month, and RINVOQ was already FDA approved in March 2022 for moderately to severely active ulcerative colitis in adults. To treat ulcerative colitis, SKYRIZI became the first IL-23 inhibitor. In ulcerative colitis treatment options, the addition of SKYRIZI has helped AbbVie strengthen its IBD portfolio.

SKYRIZI and RINVOQ are performing exceptionally well and are expected to continue capturing significant market share across IBD (Crohn’s disease, ulcerative colitis), along with other indications like psoriatic disease, and atopic dermatitis. SKYRIZI’s sales and RINVOQ’s sales in 2024 were outstanding, generating a combined total of over USD 17.6 billion in sales (USD 11.7 billion from SKYRIZI and USD 5.9 billion from RINVOQ), marking a year-over-year growth of more than 50%. While both UC drugs are growing, RINVOQ’s sales have been increasing at a slightly more modest growth rate than SKYRIZI.

Analyzing the current ulcerative colitis treatment scenario, the consensus of physicians is leaning toward the prescription of oral inflammatory bowel disease medications, which is a highly positive sign for RINVOQ. In terms of acceptance, convenience, and adherence, oral drugs with a good safety profile are an enticing option for ulcerative colitis patients. At present, there are three JAK inhibitors approved for patients with moderate to severe UC: XELJANZ (tofacitinib), JYSELECA (filgotinib), and RINVOQ (upadacitinib). One major barrier to the adoption of JAK inhibitors is “safety”. Safety concerns, such as cardiovascular events, thromboembolism, and malignancy, have plagued this class of therapy, and this issue has led to class-wide regulatory restrictions for JAKi use across all inflammatory diseases.

Analysts at DelveInsight view RINVOQ as the better option and might lead the ulcerative colitis treatment market space. As per the analysis and survey, RINVOQ could be the most preferred among physicians based on the different attributes such as safety, efficacy, clinical response, and mucosal healing. Also, RINVOQ showed better and superior results to XELJANZ. Despite the warning associated with the JAK inhibitors class and restricted usage of RINVOQ, the majority of physicians are not hesitant to use it due to its better efficacy. Also, they believed that it would be unfair if we paint Rinvoq’s future with the same brush as tofacitinib, as these risks have not been reported in inflammatory bowel disease or ulcerative colitis specifically. Rinvoq presented a clinical remission of 42% and 52% for 15 mg and 45 mg dosages, respectively, and showed that around 26% of untreated moderate and severe ulcerative colitis patients received remission in 8 weeks.

If we look at another ulcerative colitis drug in the same class, i.e., JYSELECA (filgotinib), it was expected to provide similar or better efficacy than Pfizer’s XELJANZ (tofacitinib) but with fewer side effects. It showed significant improvement in stool frequency and rectal bleeding in patients on a 200 mg daily dose. However, the FDA rejected the NDA and raised concerns over the 200 mg dose and the drug’s impact on sperm parameters in male patients. The company is not planning to proceed with the indication in the US as filgotinib results are not promising. The drug was approved in Europe and Japan for ulcerative colitis treatment in 2021 and 2022, respectively, based on findings from Phase IIb/III SELECTION study. One new class entry is ZEPOSIA (ozanimod) of the S1PR receptor modulator class, which is the first-in-class drug approved in May 2021 in the US and in November 2021 in the EU for moderately to severely active ulcerative colitis treatment. It was initially approved for the treatment of multiple sclerosis. Compared to RINVOQ, ZEPOSIA has demonstrated a clinical remission rate of 18.4%.

In ulcerative colitis, ZEPOSIA from BMS is no longer the only S1P receptor modulator. Marketed as VELSIPITY (etrasimod), it received FDA approval in October 2023 and European approval in February 2024 as a second-in-class S1P receptor modulator after ZEPOSIA. VELSIPITY has shown statistically significant results in the ELEVATE UC 12 and UC 52 trials, with remission rates of approximately 27% to 32% at induction and sustained responses at 52 weeks. Unlike ZEPOSIA, VELSIPITY does not require dose titration and has demonstrated higher efficacy, making it the preferred agent among physicians in the S1P class. The drug’s launch has given Pfizer a much-needed boost in the UC space, following its acquisition of Arena Pharmaceuticals. o Head-to-head studies are comparing the efficacy and safety of VELSIPITY versus ZEPOSIA. However, VELSIPITY has demonstrated better efficacy than ZEPOSIA did in their separate trials. Although the uptake of ZEPOSIA and VELSIPITY has been somewhat sluggish, they seem to be living up to what has been reported from key clinical trials in the real world.

Many KOLs were positive about ZEPOSIA’s market uptake and were vocal about their willingness to use this agent as a first-line moderate-to-severe ulcerative colitis treatment if launched before RINVOQ and VELSIPITY. However, the market for ZEPOSIA turned out to be different. In the current landscape of RINVOQ vs ZEPOSIA, the best positioning for approved S1P receptor modulators in ulcerative colitis would be for patients who need their first advanced therapy and for patients who would prefer a safe, oral alternative, because S1P receptor modulators do not function nearly as quickly as JAK inhibitors.

There has been a significant shift in the UC market, as three new IL-23 inhibitors have been approved for the treatment of UC. This class has a lower likelihood of development of neutralizing antibodies and has the advantage of a favorable side effect profile, particularly when compared to anti-TNF agents. IL-23 therapies in UC are emerging as a strong contender against anti-TNFs. OMVOH (mirikizumab), the first-in-class α4‑IL‑23 agent, was approved in Japan in March 2023, in the EU in May 2023, and in the US in October 2023 for the treatment of moderate to severe ulcerative colitis. The drug showed significant induction and maintenance remission in clinical trials and presents an attractive alternative to both ustekinumab and anti-TNF agents. On the other hand, Johnson & Johnson’s TREMFYA (guselkumab), another IL-23 inhibitor, was FDA-approved in September 2024 for adult ulcerative colitis, marking the company’s fourth biologic in this space. It enters into direct competition with AbbVie’s SKYRIZI and will need aggressive payer contracting to gain traction. To ensure its commercial success, TREMFYA should adopt an approach similar to SKYRIZI, such as contracting payors for easy ulcerative colitis market access so that physicians do not face any hurdles in prescribing the drug.

With growing biosimilar activity, STELARA (ustekinumab) has now seen multiple biosimilars (including STEQEYMA, WEZLANA & others) approved in the US and EU between July 2024 and June 2025. Celltrion’s STEQEYMA (ustekinumab-stba) gained FDA approval in December 2024 for both UC and Crohn’s disease. Settlements involving Formycon–Fresenius and Johnson & Johnson for FYB202 in March 2024 also point toward intensified biosimilar competition in the IL-12/23 inhibitor class. These approvals are expected to significantly improve access to biologics in both the US and EU markets.

The ulcerative colitis current market and its pipeline are now crowded with multiple UC drugs of different and new drug classes. There is also growing interest in a few novel emerging therapies in the ulcerative colitis pipeline with enormous potential. The drug list and pipeline for colitis are robust. These UC treatment drugs continue to progress in late-to-mid-stage trials and could offer new mechanisms for patients unresponsive to current biologics and oral agents.

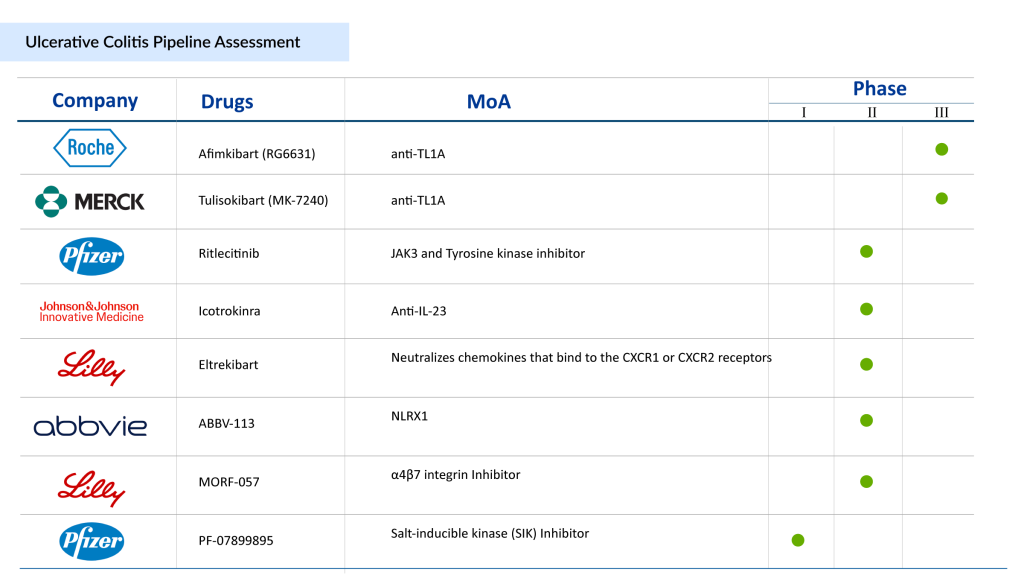

Anti-TL1A therapies represent a promising new class of treatments for ulcerative colitis. Anti-TL1A that is currently being evaluated for the UC treatment in Phase III is Merck’s Tulisokibart (MK-7240). In the Phase II ARTEMIS-UC study (NCT04996797), tulisokibart showed superior efficacy in achieving clinical remission for ulcerative colitis patients. Merck became the first company to initiate phase III clinical studies for an anti-TL1A antibody in inflammatory bowel disease. This marks a significant step in the development of a new class of drugs targeting TL1A for IBD. Roche’s Afimkibart (RG6631) is another potential therapy targeting TL1A, currently being evaluated in a Phase III clinical trial (NCT06588855) for the treatment of moderately to severely active ulcerative colitis.

Takeda also has a presence in the inflammatory bowel disease (IBD) space with their approved therapy ENTYVIO (vedolizumab). ENTYVIO remains Takeda’s one of the leading growth drivers and continues to hold the top market share despite increasing competition from rivals like AbbVie’s SKYRIZI and RINVOQ. Takeda still promotes ENTYVIO as the leading IBD brand, further supported by the approval of its pen formulation (September 27, 2023: in the United States). ENTYVIO’s competitors, like RINVOQ, SKYRIZI, and Etrasimod, are expanding treatment options in a rapidly evolving IBD market. Owing to these reasons, Takeda is also preparing to enter the UC market with another product, i.e., Zasocitinib (TAK-279), an oral and selective allosteric inhibitor of tyrosine kinase 2 (TYK2).

Janssen’s pipeline also includes a UC drug known as Icotrokinra. Icotrokinra is the first targeted oral peptide designed to block the IL-23 receptor. On March 10, 2025, J&J shared topline data from the Phase IIb ANTHEM-UC study, showing that Icotrokinra induced clinical remission in up to 30.2% of patients at Week 12 and had a favorable safety profile.

On March 28, 2025, Palatin Technologies reported positive topline results from a Phase II trial of PL8177, its novel oral therapy and selective melanocortin-1 receptor (MC1R) agonist, developed for treating active ulcerative colitis. The trial evaluated the safety, tolerability, and efficacy of PL8177 in adults with active UC.

Driven by deeper insights into disease biology and rising recognition of unmet needs, the ulcerative colitis landscape is undergoing rapid transformation. New ulcerative colitis medications are redefining the standard of care, delivering improved safety and efficacy profiles. The expansion of ulcerative colitis medications list, including advanced oral therapies, non-TNF biologics, and biosimilars, is reshaping treatment strategies and broadening options for patients and clinicians alike.

There are several new and emerging treatments for ulcerative colitis that are transforming how the disease is managed. Recent advances include targeted biologic therapies such as IL-23 inhibitors (e.g., mirikizumab and risankizumab) and newer oral drugs like S1P receptor modulators (etrasimod), which help control inflammation more precisely and improve remission rates. In addition, JAK inhibitors and next-generation small molecules are offering faster symptom relief and more convenient oral dosing options. Ongoing clinical trials are also exploring innovative approaches, including microbiome-based therapies and novel immune-targeting drugs, aiming to provide longer-lasting results and personalized treatment strategies. Exciting pipeline developments, such as investigational drugs like SPY001, are showing promising remission outcomes, indicating a strong future for more effective and patient-friendly therapies.

As stakeholders increasingly explore ulcerative colitis medications names that offer convenience and better adherence, innovation is shifting toward patient-friendly formats, particularly oral therapies. The growing focus on treatments for ulcerative colitis medications is also fueling discussions around what is the best medicine for ulcerative colitis, with decisions becoming more personalized based on disease severity, response, and patient preference.

Nicotine is not a published cure for ulcerative colitis, although it has been studied for its potential effects on the disease. Some research has suggested that nicotine may have a mild anti-inflammatory effect in certain patients, particularly those who previously smoked, but the results have been inconsistent and not strong enough to support its use as a standard treatment. Moreover, nicotine use carries significant health risks, including cardiovascular and addiction-related concerns, which outweigh any limited benefits. Current medical guidelines do not recommend nicotine as a therapy, and ulcerative colitis is best managed with evidence-based treatments such as biologics, immunosuppressants, and newer targeted therapies under medical supervision.

Prednisone typically works relatively quickly for ulcerative colitis, with many patients beginning to notice symptom improvement within a few days to a week after starting treatment. It helps reduce inflammation in the colon, leading to decreased diarrhea, bleeding, and abdominal pain. However, the full therapeutic effect may take one to two weeks or longer, depending on the severity of the condition and individual response. Prednisone is generally used as a short-term treatment to control flare-ups rather than for long-term management due to its potential side effects.

Looking ahead, the competitive landscape for ulcerative colitis medications will be shaped by long-term clinical outcomes, pricing and payer dynamics, real-world adherence, and the ability of new entrants to stand out in an increasingly crowded and competitive market.

FAQs

The treatment options for ulcerative colitis vary based on the disease’s severity and can be categorized into six main types: conventional therapies, biologics, S1P-receptor modulators, and JAK inhibitors. New mechanisms of action, such as LANCL2 protein stimulators, miR-124 enhancers, TNF-like ligand 1A inhibitors, and toll-like receptor 9 agonists, among others, are expected to broaden the range of ulcerative colitis medications.

Several FDA-approved drugs for ulcerative colitis are SIMPONI (Janssen Pharmaceuticals), ENTYVIO (Takeda Pharmaceuticals), XELJANZ/XELJANZ XR (Pfizer), STELARA (Janssen Pharmaceuticals), CAROGRA (EA Pharma/Kissei Pharma), JYSELECA (Gilead Sciences and Galapagos NV), RINVOQ (AbbVie), ZEPOSIA (Bristol-Myers Squibb), REMICADE (Janssen Pharmaceuticals), HUMIRA (AbbVie), OMVOH (Eli Lilly), and SKYRIZI (AbbVie).

Companies such as Janssen Pharmaceuticals (TREMFYA), Abivax (ABX464), Landos Biopharma/NImmune (BT-11), Merck (Tulisokibart), Eli Lilly (MORF-057), Takeda (TAK-279), Mesoblast Ltd. (Remestemcel-L), and others are currently evaluating their lead ulcerative colitis drugs in various stages of clinical trials.

Several types of medications are used to manage ulcerative colitis, depending on the severity of the disease. These include aminosalicylates (such as mesalamine) to reduce inflammation, corticosteroids (like prednisone) for short-term control of flare-ups, immunomodulators to suppress the immune response, and biologic therapies (such as anti-TNF and anti-IL-23 agents) that target specific inflammatory pathways. Newer oral treatments, including JAK inhibitors and S1P receptor modulators, are also increasingly used for moderate to severe cases. Treatment is usually personalized based on the patient’s condition and response to therapy.

SKYRIZI and RINVOQ have emerged as AbbVie’s two key therapies aimed at mitigating the impact of Humira’s patent expiry and sustaining overall revenue growth. These therapies are gaining strategic importance in enhancing AbbVie’s financial metrics. RINVOQ’s sales and SKYRIZI’s sales continue to grow steadily from year to year.

The time to see results can vary between medications. Infliximab, a biologic therapy, may begin to show improvement within 1 to 2 weeks, but full benefits are often observed after several weeks of continued treatment. Rinvoq (upadacitinib), an oral JAK inhibitor, typically works faster, with some patients experiencing symptom relief within a few days to a week, and more significant improvement within 2 to 8 weeks. However, response times can differ based on disease severity and individual patient factors.

Downloads

Article in PDF

Recent Articles

- Top 7 Breakthrough Drugs for Ulcerative Colitis Treatment

- Agios’ PYRUKYND SNDA Accepted by FDA for Thalassemia; BridgeBio’s BBO-8520 Gets FDA Fast Track fo...

- Humira’s patent; Teva laying off; GSK aims; Thermo acquires Patheon; J& J’s Invokana

- HUMIRA Biosimilars in the US: The Talk of the Psoriatic Arthritis Treatment Market

- Pfizer to acquire Arena Pharma; Takeda’s ‘Wave 2’ multiple myeloma med data; No...