Monoclonal Antibodies Fueling the Next Wave of Growth in the Interstitial Lung Disease Treatment

Jul 13, 2026

Table of Contents

Summary

- ILD is a heterogeneous group of 200+ chronic lung disorders marked by inflammation and progressive scarring that cause worsening breathlessness, declining lung function, and shortened life expectancy.

- Monoclonal antibodies (mAbs) are reshaping ILD care by precisely targeting inflammatory and fibrotic pathways, offering potential for greater efficacy, improved safety, and more personalized treatment versus traditional antifibrotics.

- Roche’s ACTEMRA (tocilizumab), an IL-6 receptor mAb for SSc‑ILD, has demonstrated that a targeted biologic can achieve meaningful commercial traction (around USD 172 million in 2025) and disrupt antifibrotic‑dominated treatment dynamics.

- Several late‑ and mid‑stage mAb programs are advancing (notably GSK’s belimumab/BENLYSTA in late‑stage SSc‑ILD, Merck’s tulisokibart, Sanofi’s amlitelimab), signaling a mechanistic pivot toward precision immunomodulation across SSc‑ILD, CTD‑ILD, and other subtypes.

Interstitial lung disease (ILD) represents one of the most challenging areas in respiratory medicine, encompassing more than 200 chronic lung disorders characterized by inflammation and progressive scarring of lung tissue. Despite advances in diagnosis, many patients continue to experience declining lung function, worsening breathlessness, and shortened life expectancy. The growing global burden of ILD, driven by aging populations, increasing prevalence of autoimmune diseases, environmental exposures, and improved disease recognition, has intensified the demand for therapies that can do more than simply slow disease progression.

Downloads

Click Here To Get the Article in PDF

Recent Articles

- Outset Medical captures; Wright Medical Group to takeover Cartiva; Y-mAbs Therapeutics prepares f...

- Apollomics raises; Pear Therapeutics raises $64M; Lilly to acquire Loxo

- Ofev’s expanded use; Arkin Bio-Ventures II launch; USD 125 M for COVID-19 treatment

- Gilead’s Livdelzi FDA Approval for Primary Biliary Cholangitis; Incyte and Syndax’s Niktimv...

- The Changing Landscape of Multiple Myeloma Therapies Market

In 2025, the diagnosed prevalent ILD cases across the 7MM reached 1.3 million across the leading markets (the US, EU4, the UK, and Japan). This figure is expected to rise to 1.6 million by 2036. Behind that steady climb sits a disease category that clinicians once described almost entirely in terms of decline, declining lung function, declining quality of life, declining options. That description is starting to change, and monoclonal antibodies are a big reason why.

By precisely targeting key inflammatory and fibrotic pathways involved in disease progression, these biologics are redefining treatment strategies, offering the potential for greater efficacy, improved safety profiles, and more personalized care. Unlike conventional therapies, monoclonal antibodies are designed to interrupt the underlying mechanisms that drive lung injury and fibrosis, making them an increasingly attractive option for both autoimmune-associated and progressive fibrosing ILDs.

DelveInsight’s analysis puts the ILD market across the seven major markets at roughly USD 6 billion in 2025, with an expected compound annual growth rate of 8.7% through 2036. That growth isn’t coming from nowhere. Earlier diagnosis, rising treatment uptake, longer treatment durations, the broadening use of antifibrotics across multiple ILD subtypes, and the arrival of premium-priced, phenotype-specific therapies are all converging to push the market forward.

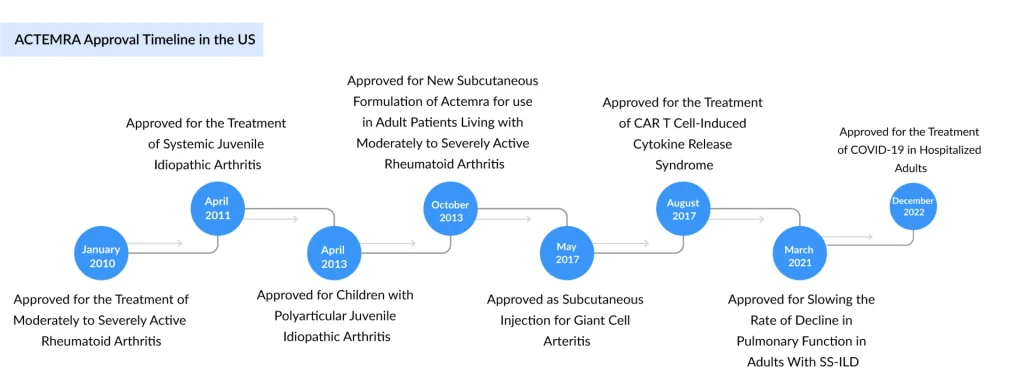

Roche’s ACTEMRA: The Monoclonal Antibody Making Waves

Of everything reshaping this market, one story stands out from a competitive-intelligence standpoint: a monoclonal antibody is now genuinely challenging a field that has long been dominated by antifibrotics and prostacyclin-pathway agents. Roche’s ACTEMRA (tocilizumab), an IL-6 receptor-targeting monoclonal antibody, has carved out a defined niche in systemic sclerosis-associated ILD (SSc-ILD), where it works by blocking the inflammatory signaling thought to drive early fibrotic progression. It’s a fundamentally different mechanism from the antifibrotics that dominate the broader ILD category, and that difference is exactly what makes it disruptive.

Where OFEV and its antifibrotic peers slow fibrosis once it’s underway, ACTEMRA intervenes upstream, at the inflammatory drivers, an approach that resonates with physicians managing earlier-stage, inflammation-predominant disease. This positioning places ACTEMRA in direct competition with several established therapies across the interstitial lung disease treatment landscape. Boehringer Ingelheim’s OFEV (nintedanib) and its newer stablemate JASCAYD continue to serve as the cornerstone antifibrotic therapies, supported by broad approvals spanning idiopathic pulmonary fibrosis and progressive fibrosing ILD subtypes. Meanwhile, United Therapeutics’ TYVASO, TYVASO DPI, and TREPROST dominate the prostacyclin-pathway segment, primarily targeting pulmonary hypertension associated with ILD (PH-ILD). Adding further competitive pressure, Liquidia Corporation’s YUTREPIA, a dry-powder formulation of treprostinil, has emerged as the latest entrant seeking market share within the growing PH-ILD treatment space.

The revenue picture in 2025 shows just how uneven this competitive field still is. ACTEMRA, despite its narrower SSc-ILD indication, has climbed to around USD 172 million, a meaningful foothold for a therapy competing against much larger, more established categories. What makes ACTEMRA’s performance notable isn’t the absolute number; it’s the trajectory and the precedent. It has been proven that a targeted monoclonal antibody, addressing a clinically distinct and previously underserved inflammatory phenotype, can build durable revenue in a market long assumed to belong almost exclusively to antifibrotics and prostacyclin analogs. That proof point is precisely what’s now drawing several major biopharma players toward mAb-based ILD strategies of their own.

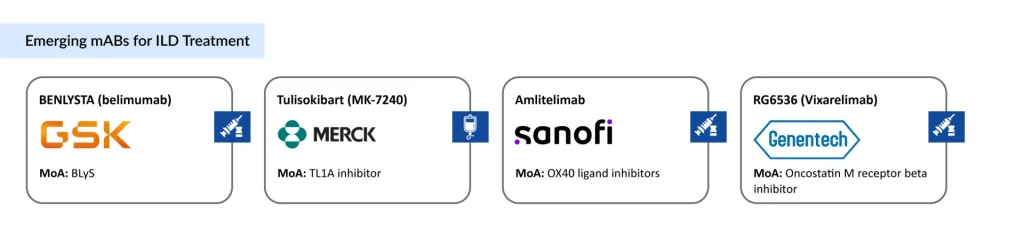

The Next Wave: Emerging Monoclonal Antibodies to Watch

If ACTEMRA opened the door, the next generation of monoclonal antibodies is walking through it. Several large-cap and mid-cap developers are now testing antibody-based approaches across SSc-ILD, CTD-ILD, and idiopathic pulmonary fibrosis, each going after a slightly different immunological driver of fibrotic lung disease.

GSK’s BENLYSTA (belimumab)

BENLYSTA is a fully human monoclonal antibody that selectively inhibits B-lymphocyte stimulator (BLyS), a cytokine that B cells depend on to survive and mature. By binding soluble BLyS, belimumab suppresses autoreactive B cells and limits their transformation into antibody-producing plasma cells, ultimately dialing down autoimmune activity. Already established in autoimmune disease, BENLYSTA is now advancing through Phase II/III and Phase III trials for systemic sclerosis-associated interstitial lung disease (SSc-ILD) and connective tissue disease-associated interstitial lung disease (CTD-ILD).

These late-stage programs reflect growing confidence in B-cell-targeted therapy as a way to preserve lung function, reduce immune-driven inflammation, and slow fibrotic progression. In February 2023, GSK announced that the US FDA had granted ODD to BENLYSTA (belimumab), a B-cell–inhibiting monoclonal antibody, for the potential treatment of systemic sclerosis. The therapy is expected to launch in 2029 in the US, followed by 2030 across the EU4 and the UK, and 2031 in Japan, reflecting its anticipated global commercialization timeline.

Aparna Thakur, Project Manager of Forecasting at DelveInsight, points out that BENLYSTA’s move into late-stage SSc-ILD trials signals GSK’s confidence in BLyS inhibition as a disease-modifying strategy for immune-driven fibrosis, backed by an already well-understood safety profile. Its ultimate value in ILD, though, will hinge on the efficacy data still to come, since late-stage results haven’t been disclosed yet.

Merck’s Tulisokibart

TL1A inhibitor

Originally developed by Prometheus Biosciences before Merck’s acquisition, tulisokibart targets TL1A, a cytokine implicated in fibrotic and inflammatory tissue remodeling. It is currently in a Phase II study evaluating safety and efficacy specifically in SSc-ILD patients, with eligibility criteria built around confirmed HRCT-diagnosed disease and defined FVC/DLCO thresholds. TL1A inhibition is one of the more closely watched mechanisms in immunology right now, and a positive readout in ILD would meaningfully expand the target’s relevance beyond inflammatory bowel disease.

Sanofi’s Amlitelimab

OX40 ligand inhibitors

This fully human, non-depleting antibody targets OX40-ligand, a costimulatory molecule involved in T-cell-driven inflammation. Beyond its more advanced programs in atopic dermatitis and asthma, amlitelimab is an active treatment arm in CONQUEST, a Phase IIb platform trial run in partnership with the Scleroderma Research Foundation specifically for SSc-ILD. Notably, Boehringer Ingelheim, the company behind OFEV and JASCAYD, is co-funding this same platform with its own investigational agent, an unusual arrangement that underscores how seriously incumbents are taking the mAb threat.

Genentech’s RG6536 (Vixarelimab)

Oncostatin M receptor beta inhibitor

Vixarelimab, an antibody targeting the oncostatin M receptor beta (OSMRβ) pathway, was being tested in a Phase II study spanning both idiopathic pulmonary fibrosis and SSc-ILD. That trial was discontinued after an independent data monitoring committee’s unblinded review pointed toward a trend of futility, not a safety signal. It’s a reminder that this emerging class carries real scientific risk alongside its promise, and not every mechanism explored in ILD will make it to market.

The Third Pillar of ILD Therapy Emerges

Put together, these programs signal a genuine mechanistic pivot. For years, ILD management leaned on two pillars: antifibrotics to slow scarring and prostacyclin-pathway agents to manage associated pulmonary hypertension. Monoclonal antibodies introduce a third pillar built around precision immunomodulation: targeting IL-6 signaling, BLyS, TL1A, OX40-ligand, and other pathways implicated in the inflammatory-to-fibrotic transition.z

If even two or three of these emerging antibodies clear Phase III and reach approval, the competitive dynamics DelveInsight is currently tracking, OFEV’s dominance, TYVASO’s pulmonary hypertension niche, YUTREPIA’s uphill commercial climb, JASCAYD’s early-stage ramp, and ACTEMRA’s proof-of-concept success, will look very different by the early 2030s.

Success would likely come at the expense of broad-spectrum antifibrotic share in inflammation-predominant patient subgroups, while also creating entirely new premium-priced segments within CTD-ILD and SSc-ILD specifically. Incumbents are clearly aware of this: Boehringer Ingelheim’s decision to co-fund a rival’s platform trial rather than sit on the sidelines is a telling sign of how the next decade of ILD competition is expected to unfold.

For now, ACTEMRA remains the only monoclonal antibody with meaningful commercial traction in ILD. But with belimumab in Phase III, tulisokibart and amlitelimab progressing through Phase II, and multiple pharma majors now willing to co-invest in shared trial infrastructure, the “rise” looks less like a prediction and more like a trend already well underway.

Downloads

Article in PDF

Recent Articles

- Apollomics raises; Pear Therapeutics raises $64M; Lilly to acquire Loxo

- The Changing Landscape of Multiple Myeloma Therapies Market

- Unleashing the Potential: CD38 Directed Therapies Revolutionize Multiple Myeloma Treatment

- Outset Medical captures; Wright Medical Group to takeover Cartiva; Y-mAbs Therapeutics prepares f...

- What are Monoclonal Antibodies and How Can They Treat COVID-19?